North America Flexible Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

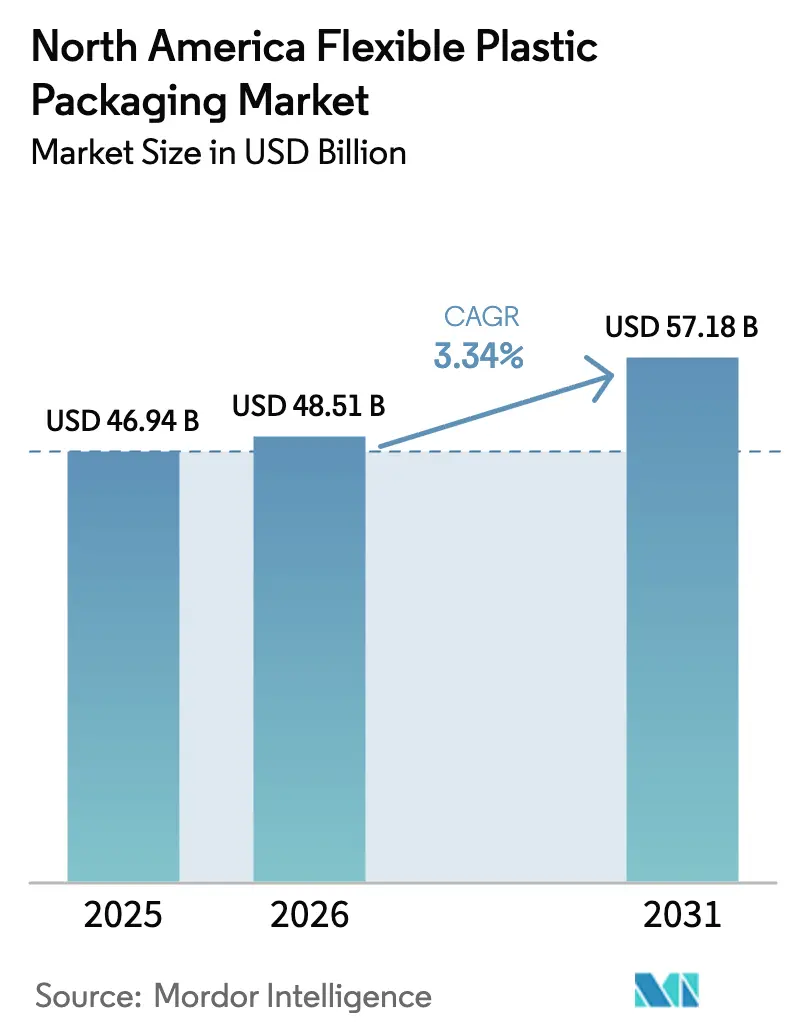

| Base Year Market Size (2025) | USD 46.94 Billion |

| Market Size (2026) | USD 48.51 Billion |

| Market Size (2031) | USD 57.18 Billion |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Flexible Plastic Packaging Market Analysis by Mordor Intelligence

North America flexible plastic packaging market size in 2026 is estimated at USD 48.51 billion, growing from 2025 value of USD 46.94 billion with 2031 projections showing USD 57.18 billion, growing at 3.34% CAGR over 2026-2031. Competition among multinational converters, expanding e-commerce fulfillment, and mandated shifts toward recyclable mono-material films are shaping a steady, value-driven growth path rather than rapid volume expansion. Polyethylene maintains a broad footprint across food, mailer, and industrial formats, while polypropylene gains ground as processors migrate to recyclable barrier solutions aligned with Extended Producer Responsibility rules. Mailer pouches, stretch films, and digitally printed short-run SKUs respond to direct-to-consumer supply-chain demands. At the country level, the United States keeps the lion’s share of demand, yet Mexico delivers the fastest growth on the back of nearshoring manufacturing and rising consumer packaged-goods output. Together, these forces sustain the North America flexible plastic packaging market as an innovation-led, medium-growth arena.

Key Report Takeaways

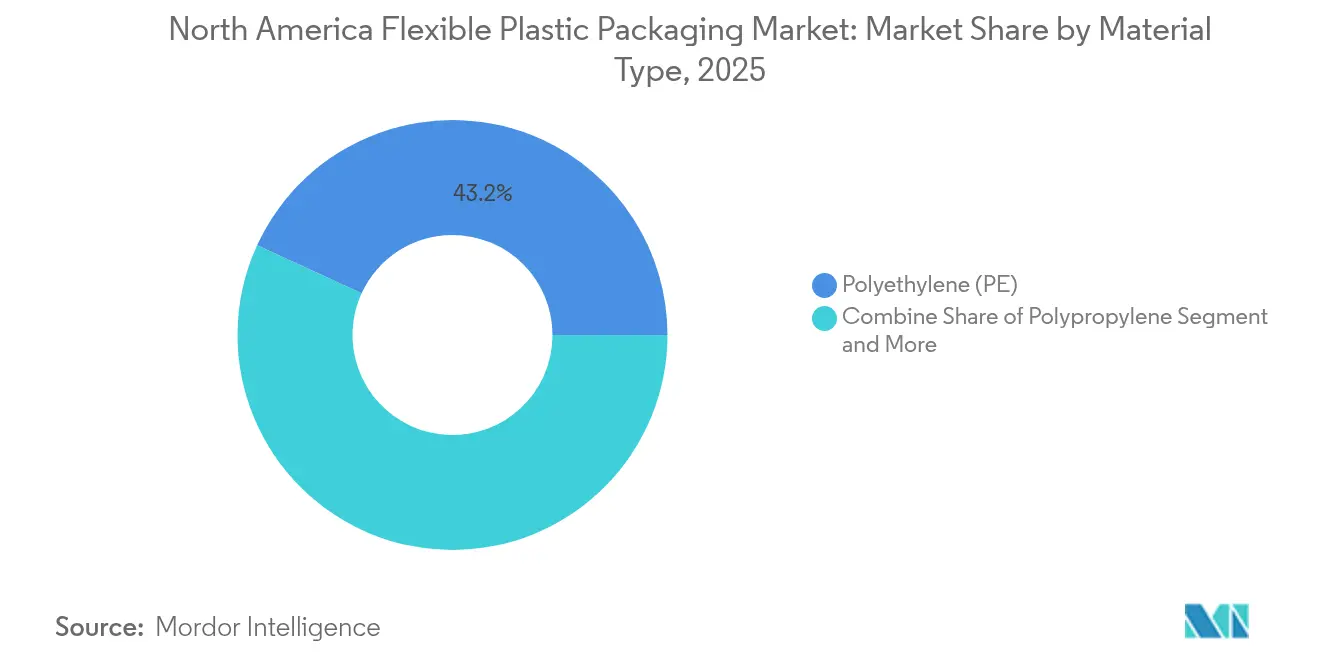

- By material type, polyethylene dominated with 43.15% of North America flexible plastic packaging market share in 2025, while polypropylene recorded the highest projected CAGR at 6.12% through 2031.

- By product type, pouches led with 45.10% revenue share in 2025; films and wraps are forecast to expand at a 5.55% CAGR to 2031.

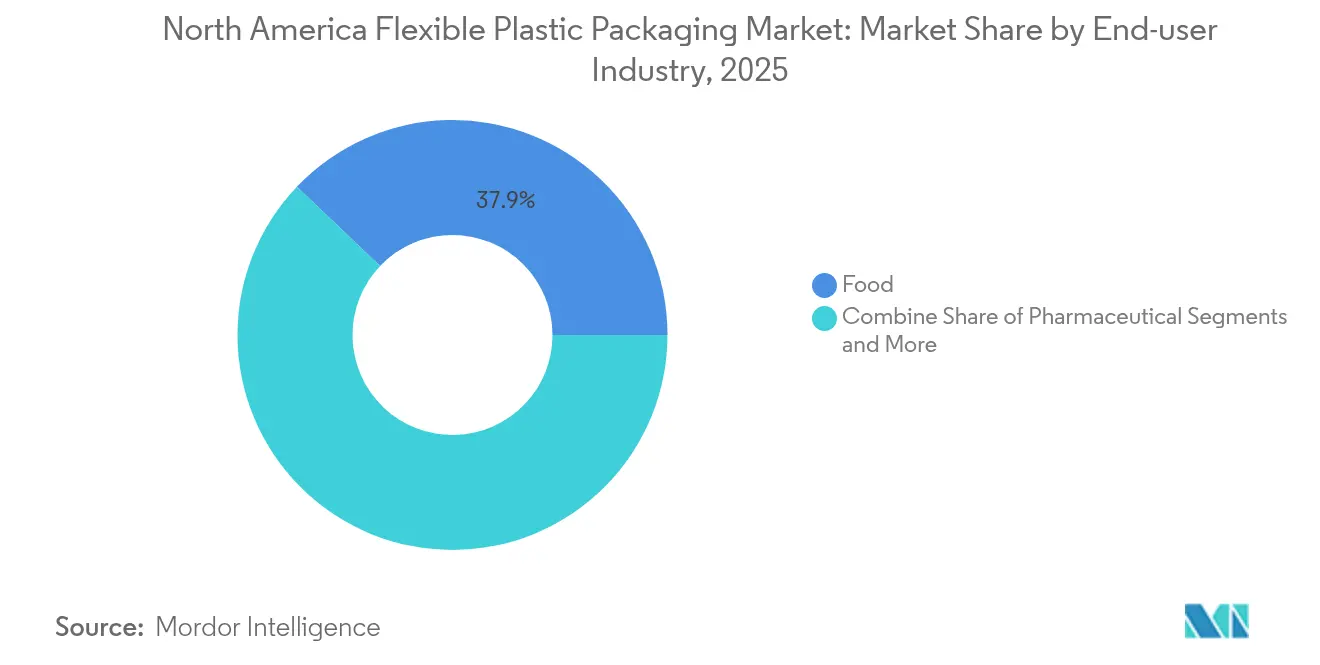

- By end-user industry, food captured 37.88% share of the North America flexible plastic packaging market size in 2025, whereas pharmaceutical packaging advances at a 7.65% CAGR through 2031.

- By distribution channel, direct sales held 58.20% of revenue in 2025, while indirect channels are projected to post a 4.38% CAGR over the forecast period.

- By country, the United States accounted for 77.45% of revenue in 2025; Mexico is projected to grow at a 5.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with North america forming one of the important contributors. Mordor Intelligence's global flexible plastic packaging market size report represents that cumulative total.

North America Flexible Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment boom elevating mailer and protective pouch demand | +0.8% | North America, US urban hubs | Short term (≤ 2 years) |

| High-barrier snack and ready-meal adoption by millennials | +0.6% | United States, urban Canada | Medium term (2-4 years) |

| Cannabis-infused edibles requiring child-resistant packs | +0.4% | Canada, select US states | Medium term (2-4 years) |

| Digitally printed short-run SKUs for retail private labels | +0.5% | North America | Short term (≤ 2 years) |

| Mono-material recyclable film shift under recycling mandates | +0.7% | United States, spillover to Canada, Mexico | Long term (≥ 4 years) |

| Accelerated fresh-produce home-delivery programs | +0.3% | North America urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce fulfillment boom elevating mailer and protective pouch demand

Brands shipping direct to consumers now prioritize puncture resistance and moisture control rather than traditional shelf appeal, lifting usage of mailer pouches engineered for automated sorting and multi-point handling. Investments in HP Indigo 200K presses allow converters to offer short-run customization that turns the shipping container into a branded experience. NFC tags and QR codes embedded in mailers improve last-mile traceability and deepen post-purchase engagement, creating ancillary revenue streams while cementing flexible packaging’s role in omnichannel commerce.

High-barrier snack and ready-meal adoption by millennials

Rising demand for premium snacks and convenience meals pushes converters to integrate oxygen- and aroma-barrier layers that extend shelf life without compromising visibility. Brand owners such as Mondelez report consumer willingness to pay more for packaging that pairs sustainability with freshness, encouraging mono-material designs incorporating EVOH or bio-based coatings. Plant-based protein snacks, prone to lipid oxidation, further accelerate adoption of high-barrier structures made from recyclable or compostable substrates.

Cannabis-infused edibles requiring child-resistant packs

Legalization expands a niche that demands pouches combining UV resistance, moisture barriers, and certified child-resistant closures. Health Canada’s March 2025 rule change permits transparent windows and enhanced label space, spurring innovation in multi-layer films that retain potency while meeting safety tests. [1]Health Canada, “Summary of changes following the streamlining of regulations,” canada.ca Multi-state operators seek modular designs that can be quickly adapted to shifting state mandates, making flexible formats ideal for regulatory agility.

Digitally printed short-run SKUs for retail private labels

Retailer consolidation fuels private-label proliferation, requiring fast artwork changes without high plate costs. Converters leveraging digital presses deliver sub-10-day lead times, enabling seasonal or regional variants at scale. [2]ePac press release, “ePac sets strategy for continued double-digit growth,” epacflexibles.com Hybrid workflows that marry digital graphics to conventional barrier coatings gain traction as brand owners demand both shelf impact and recyclability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchwork state-level EPR laws inflating compliance costs | -0.9% | United States | Medium term (2-4 years) |

| Escalating PE and PP resin price volatility | -0.7% | North America | Short term (≤ 2 years) |

| Capacity overhang in Gulf-Coast blown-film lines | -0.6% | US Gulf Coast, Mexico | Short term (≤ 2 years) |

| High sorting contamination rates limiting PCR supply | -0.4% | North America urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchwork state-level EPR laws inflating compliance costs

California, Oregon, Colorado, Maine, and Minnesota each impose unique fee schedules and recyclability targets, forcing converters to juggle parallel compliance schemes and maintain state-specific SKUs. For SMEs, the administrative burden rivals capital spending, delaying investment in advanced recycling ventures until harmonization emerges.

Escalating PE and PP resin price volatility

Polymer-grade propylene shortages and hurricane-related outages spur 3–5 cents-per-pound price swings, compressing converter margins and complicating long-term contracts. Buyers hedge via quarterly pricing windows or raw-material pass-through clauses, but volatility remains a brake on volume expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Breadth Meets Polypropylene Agility

Polyethylene retained 43.15% of North America flexible plastic packaging market share in 2025, anchored by its broad processing window and cost-effectiveness across frozen foods, mailers, and industrial liners. Polypropylene, in contrast, posts a 6.12% forecast CAGR, leveraging higher stiffness and heat resistance to capture stand-up pouch and retort film applications aligned with North America flexible plastic packaging market sustainability goals. The North America flexible plastic packaging market size for polypropylene is projected to expand as converters retrofit lines with orientation technology that unlocks mono-material recyclability.

Polyvinyl chloride remains entrenched in select medical devices where clarity and formability are critical, though environmental scrutiny restrains new investments. EVOH continues as a thin barrier layer atop PE or PP substrates in high-aroma snacks and ready-meals. Bioplastics—PLA, PHA, PBS—advance through pilot lines targeting premium organic food brands; Fraunhofer’s flex-grade PLA demonstrates heat-seal improvements but cost parity with fossil resins is yet to materialize. Specialty nanocomposites address aerospace and defense pouching where puncture resistance trumps recyclability.

By Product Type: Pouch Supremacy and Film Momentum

Pouches accounted for 45.10% revenue in 2025, underpinning the leadership position of the North America flexible plastic packaging market as brands favor lightweight, shelf-ready formats with easy-open and reclose features. Films and wraps, however, deliver the briskest 5.55% CAGR, buoyed by stretch-wrap downgauging in produce pallets and e-commerce cushioning. The North America flexible plastic packaging market size for films gains from Dole’s roll-out of Oxifilm stretch film that cuts pallet plastic by 85%.Bags remain indispensable in bulk flour, pet litter, and food-service bread where filling speed and tear resistance are decisive. Retort pouches, vacuum packs, and medical chevron bags represent niche volumes but command premium margins due to validation testing and sterilization compatibility. Easy-peel seals and laser scoring broaden convenience appeal, ensuring pouches stay at the heart of the North America flexible plastic packaging market.

By End-user Industry: Food Bulk Continues, Pharma Accelerates

Food held 37.88% of 2025 revenue thanks to entrenched demand across bakery, dairy, meat, and snack categories, fortifying the North America flexible plastic packaging market against cyclical shocks. Pharmaceuticals register an 7.65% CAGR as biologics, temperature-sensitive injectables, and cannabis edibles demand child-resistant and cold-chain compatible packs. The North America flexible plastic packaging market size for pharmaceutical formats is projected to widen due to Medicaid expansion and specialty-drug pipelines.

Beverage innovations such as bag-in-box wines and squeeze pouches for functional drinks tap the convenience premium. Personal and household care leverage stand-up spouted pouches that reduce rigid-bottle resin by up to 70%. Industrial chemicals and agricultural inputs adopt barrier liners that allow high-speed filling while reducing hazardous-goods leakage risks.

By Distribution Channel: Direct Scale, Indirect Expertise

Direct sales delivered 58.20% of 2025 turnover as global converters manage strategic accounts for major CPG companies, reinforcing the dominance of the North America flexible plastic packaging market. Indirect distribution’s 4.38% CAGR reflects small- and medium-sized brands seeking technical guidance from specialty resellers adept at navigating EPR, FDA, and Health Canada rules. Online portals democratize access to low-minimum-order pouches, allowing entrepreneurial brands to prototype without tying up capital. As SKU complexity rises, distributors embed pre-press, compliance, and inventory-management services into their offer, capturing margin through expertise rather than volume alone.

Geography Analysis

The United States contributed 77.45% of 2025 revenue, reflecting its expansive manufacturing base, deep e-commerce penetration, and active regulatory landscape that spurs recyclable mono-material adoption. Landmark deals such as Amcor’s USD 8.43 billion Berry Global acquisition amplify scale and R&D depth, positioning U.S. operations for EPR readiness. Digital-printing hubs clustered around Chicago, Cincinnati, and Dallas support rapid SKU change-overs for national retailers, reinforcing the central role of the North America flexible plastic packaging market in consumer fulfillment innovation.

Canada’s mature sector serves food, pharma, and cannabis applications, benefitting from Winpak’s tie-up with NOVA Chemicals to raise recycled-PE content. Health Canada flexibility on transparent cannabis windows fuels pouch redesigns aimed at shelf differentiation. Government grants for circular-economy pilots encourage investment in mechanical and advanced recycling, ensuring Canada remains a sustainability test-bed within the North America flexible plastic packaging industry.

Mexico posts a 5.22% forecast CAGR as automakers and electronics assemblers nearshore production, demanding ESD-safe bags and anti-corrosion films. Consumer-goods multinationals ramp local snack and beverage plants, creating pull-through for modified-atmosphere pouches. NAFTA successor USMCA provisions safeguard tariff-free polymer flows, while peso fluctuations give Mexican extruders a cost-advantage on exports to the U.S. east and west coasts. As suppliers co-locate near manufacturing clusters, the North America flexible plastic packaging market entrenches continental supply-chain resilience.

Coverage of the flexible plastic packaging market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Middle East and Africa, Asia, and Europe, alongside detailed country-level intelligence for Canada, United States, Indonesia, Saudi Arabia, South Africa, and Nigeria, each shaped by local operating conditions.

Competitive Landscape

Competitive Landscape

Merger activity worth USD 16.93 billion in 2024-2025 signals a quest for scale to shoulder EPR fees and bankroll advanced recycling. Amcor’s tie-up with Berry Global targets USD 650 million annual synergy and vaults the group to USD 24 billion revenue, cementing leadership in the North America flexible plastic packaging market. Novolex’s USD 6.7 billion Pactiv Evergreen deal reinforces food-service depth while opening cross-selling to retail multipacks.

Technology races center on digital press fleets, solvent-free lamination, and in-line recycling modules that upcycle trim into usable film core layers. Patent filings for temporary elastomeric barrier membranes reveal a push to dispense with metallized foil while retaining oxygen performance. Challenger brands such as ePac exploit a digital-only model that slashes lead time and minimums, capturing share among artisan coffee and direct-ship pet-food labels.

Resin volatility alongside Gulf-Coast overcapacity continues to test earnings. Top converters hedge through multi-year resin contracts or equity stakes in recycling ventures to de-risk virgin-resin swings. Smart-packaging pilots embedding Bluetooth-Low-Energy chips attract pharma and cold-chain clients seeking real-time integrity data, opening a high-margin frontier within the North America flexible plastic packaging market.

North America Flexible Plastic Packaging Industry Leaders

Sonoco Products Company

Amcor Plc

Sealed Air Corporation

Mondi PLC

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Novolex completed its USD 6.7 billion acquisition of Pactiv Evergreen, adding 250 brands and 39,000 SKUs to its portfolio

- April 2025: Dole Food Company expanded Oxifilm recyclable stretch film across Latin American produce operations, targeting 686,400 kg plastic savings in 2025.

- February 2025: Winpak posted Q4 2024 revenue of USD 285.1 million; flexible volumes gained 5% with CAPEX guidance of USD 110–130 million for 2025.

- January 2025: Amcor launched Lift-Off Sprints and Lift-Off Connect, dedicating USD 3 million yearly to start-ups focused on AI and sustainable packaging.

North America Flexible Plastic Packaging Market Report Scope

Flexible plastic packaging allows more economical and customizable options for packaging products. Flexible plastic packaging products are particularly useful in industries requiring versatile packaging, such as the food and beverage, personal care, and pharmaceutical industries. It has gained popularity due to its high efficiency and cost-effectiveness. Flexible plastic packaging combines the advantages of plastic materials such as PE and PP without compromising the product's printability, barrier protection, freshness, or ease of use. Consumers are looking for easy-to-use and lightweight packaging, and vendors are designing innovative packaging solutions to remain competitive in the growing organized retail market with the changing demands of customers. Shifting to an alternative lighter material, such as flexible pouches, provides more significant energy-saving benefits.

The North America Flexible Plastic Packaging Market Report is Segmented by Material (Polyethene [PE], Bi-Oriented Polypropylene [BOPP], Cast Polypropylene [CPP], Polyvinyl Chloride [PVC], Ethylene Vinyl Alcohol [EVOH], and Other Material Types [Polycarbonate, PHA, PLA, Acrylic, and ABS]), Product Type (Pouches, Bags, Films and Wraps, and Other Product Types), End-User Industry (Food [Frozen Food, Dry Food, Meat, Poultry, and Sea Food, Candy & Confectionery, Pet Food, Dairy Products, Fresh Produce and Other Food (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)], Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End User Industry [Automotive, Chemical, Agriculture ]), and Country (United States and Canada). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| Polyethylene (PE) |

| Polypropylene (BOPP and CPP) |

| Polyvinyl Chloride (PVC) |

| Ethylene-Vinyl Alcohol (EVOH) |

| Bioplastics (PLA, PHA, PBS) |

| Other Material Type |

| Pouches | Stand-Up Pouches |

| Flat and Pillow Pouches | |

| Bags (Gusseted, Wicketed) | |

| Films and Wraps (Shrink, Stretch, Lidding, MDO-PE) | |

| Other Product Type |

| Food | Frozen Foods |

| Dry Foods and Cereals | |

| Meat, Poultry and Seafood | |

| Candy and Confectionery | |

| Pet Food | |

| Fresh Produce | |

| Dairy Products | |

| Other Food Product | |

| Beverage | |

| Personal and Household Care | |

| Medical and Pharmaceutical | |

| Other End-user Industry |

| Direct Sales |

| Indirect Sales |

| United States |

| Canada |

| Mexico |

| By Material Type | Polyethylene (PE) | |

| Polypropylene (BOPP and CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Ethylene-Vinyl Alcohol (EVOH) | ||

| Bioplastics (PLA, PHA, PBS) | ||

| Other Material Type | ||

| By Product Type | Pouches | Stand-Up Pouches |

| Flat and Pillow Pouches | ||

| Bags (Gusseted, Wicketed) | ||

| Films and Wraps (Shrink, Stretch, Lidding, MDO-PE) | ||

| Other Product Type | ||

| By End-user Industry | Food | Frozen Foods |

| Dry Foods and Cereals | ||

| Meat, Poultry and Seafood | ||

| Candy and Confectionery | ||

| Pet Food | ||

| Fresh Produce | ||

| Dairy Products | ||

| Other Food Product | ||

| Beverage | ||

| Personal and Household Care | ||

| Medical and Pharmaceutical | ||

| Other End-user Industry | ||

| BY Distribution Channel | Direct Sales | |

| Indirect Sales | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size of the North America flexible plastic packaging market?

The market stands at USD 48.51 billion in 2026 and is forecast to reach USD 57.18 billion by 2031.

Which material leads the North America flexible plastic packaging market?

Polyethylene leads with 43.15% share, while polypropylene grows fastest at a 6.12% CAGR.

Why is Mexico the fastest-growing geography within the market?

Nearshoring manufacturing projects and rising consumer packaged-goods output push Mexico to a 5.22% CAGR through 2031.

How are state-level EPR laws affecting converters?

Varying fee structures across five U.S. states boost compliance costs by an estimated 0.9 percentage points on overall CAGR.

What product format is expanding the quickest?

Films and wraps are set to grow at a 5.55% CAGR, fueled by e-commerce packaging and downgauged stretch-wrap adoption.

Page last updated on: