Converted Flexible Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 275.23 Billion |

| Market Size (2031) | USD 351.92 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Converted Flexible Packaging Market Analysis by Mordor Intelligence

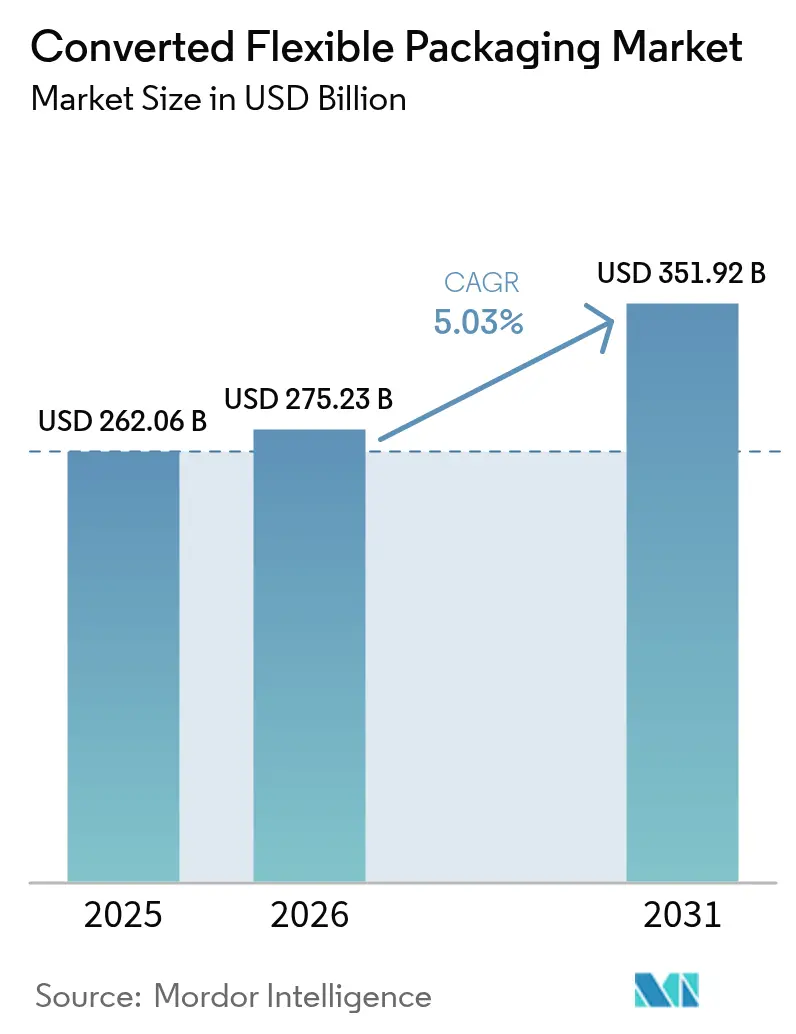

The converted flexible packaging market size was valued at USD 262.06 billion in 2025 and estimated to grow from USD 275.23 billion in 2026 to reach USD 351.92 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). This robust trajectory signals how regulatory mandates, mono-material film breakthroughs, and consumer demand for convenient, low-impact packs are reshaping value creation across food, pharmaceutical, e-commerce, and personal-care applications. Packaging converters are prioritizing recyclable structures, digital printing, and light-weighting strategies to trim logistics costs, reduce Scope 3 emissions, and meet Extended Producer Responsibility (EPR) fee thresholds in Europe and several U.S. states. Asia-Pacific anchors 40.12% of global demand, leveraging integrated supply chains and urban consumption growth, while the Middle East and Africa post the fastest 8.63% CAGR amid infrastructure upgrades and demographic tailwinds. Material shifts favor bioplastics, advancing at 7.75% CAGR, and high-barrier mono-polypropylene films aligned with EU recyclability rules. Competitive responses emphasize mergers for scale, as evidenced by Amcor’s USD 13.6 billion all-stock combination with Berry Global that targets USD 650 million synergy capture by 2027.

Key Report Takeaways

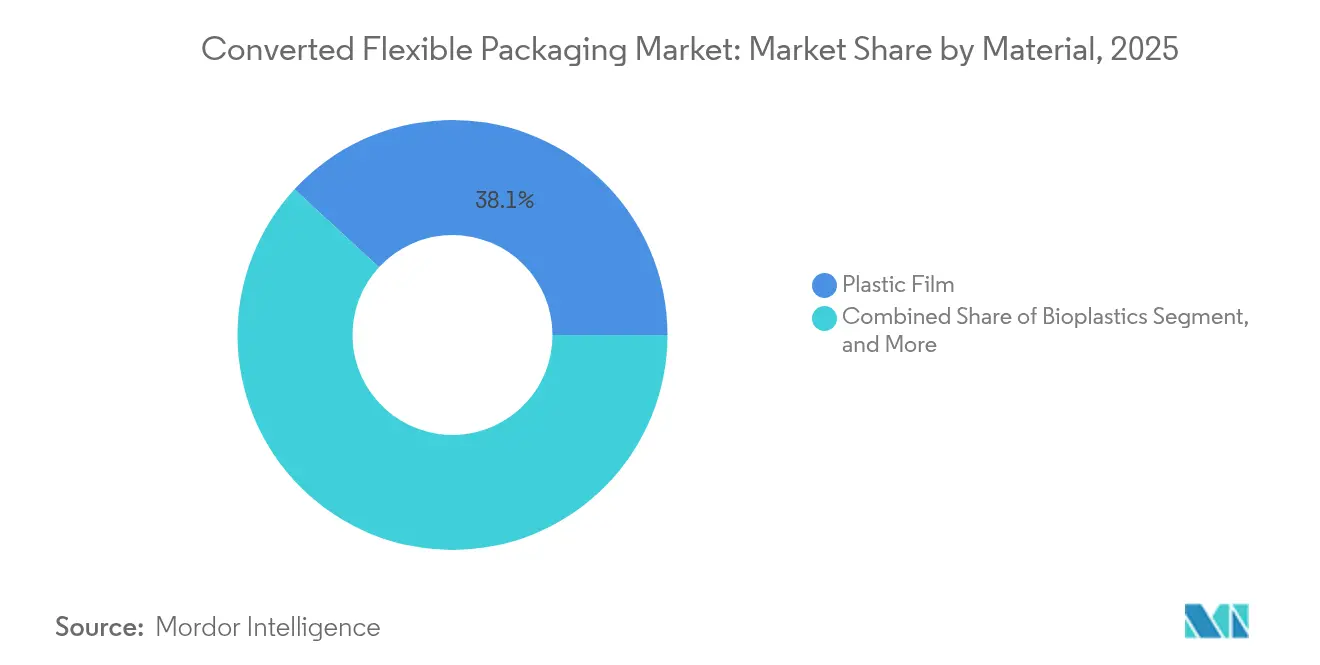

- By material, plastic films led with 38.14% of the converted flexible packaging market share in 2025, while bioplastics are forecast to climb at a 7.62% CAGR to 2031.

- By packaging format, pouches accounted for 61.63% of the converted flexible packaging market size in 2025 and are advancing at a 7.01% CAGR through 2031.

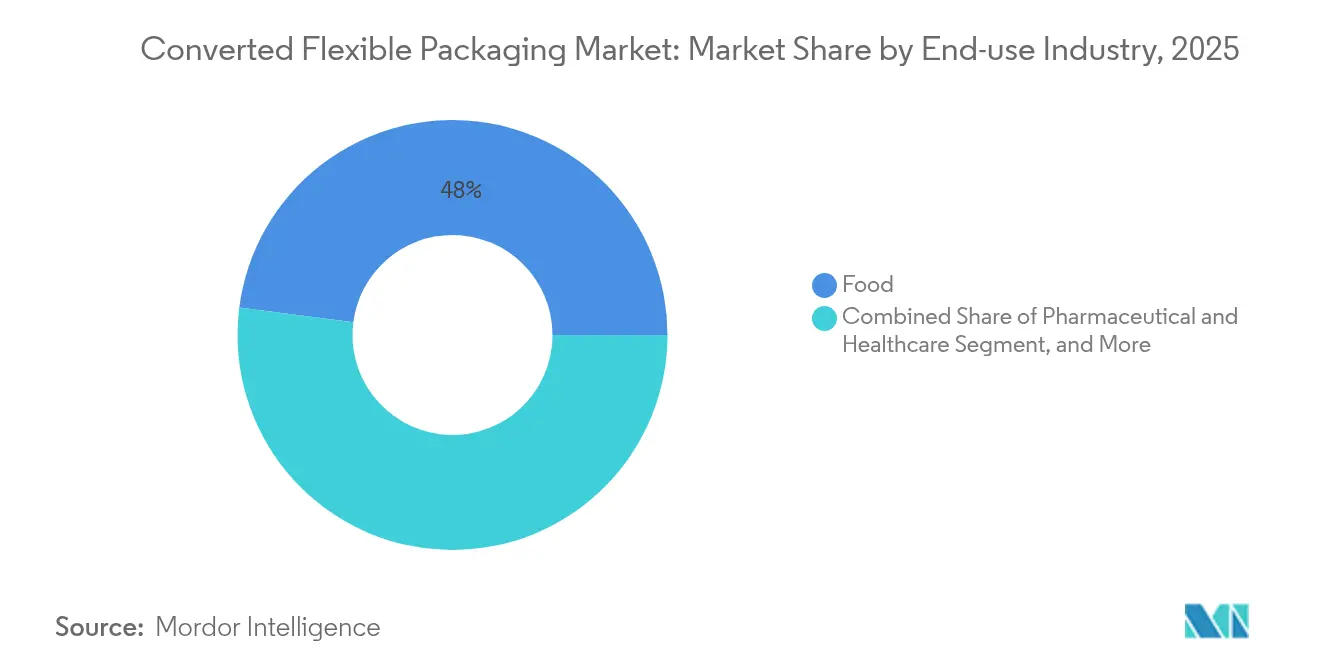

- By end-use industry, pharmaceutical and healthcare applications are progressing at an 8.3% CAGR to 2031, outpacing the mature food category that retained 47.96% revenue share in 2025.

- By distribution channel, the direct sales channel accounted for 81.14% of the converted flexible packaging market size in 2025, while the indirect sales channel is advancing at a 6.26% CAGR through 2031.

- By geography, the Middle East and Africa segment is positioned to expand at an 8.51% CAGR between 2026-2031, while Asia-Pacific captured 39.62% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Converted Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in on-the-go food and beverage consumption | +1.2% | Global, with early gains in North America, Asia-Pacific urban centers | Medium term (2-4 years) |

| E-commerce accelerating demand for protective mailer formats | +0.9% | Global, spill-over from North America and EU to emerging markets | Short term (≤ 2 years) |

| Adoption of high-barrier mono-material films for recyclability | +0.8% | EU core, expanding to North America, Asia-Pacific | Long term (≥ 4 years) |

| Advanced digital printing enabling low-MOQ SKU proliferation | +0.6% | North America and EU, selective Asia-Pacific markets | Medium term (2-4 years) |

| Government bans on rigid plastics in fresh-produce channels | +0.4% | EU, selective North American states, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in On-the-Go Food and Beverage Consumption

Urban lifestyles continue to compress mealtimes, prompting higher demand for ready-to-eat snacks, single-serve beverages, and resealable pouches. USDA 2024 food trend data showed more than 50% of U.S. consumers seek products that combine portability and environmental information on the pack. [1]USDA, “Food Trends 2025,” Extension.psu.edu Brands respond with lightweight stand-up pouches that lower shipping costs versus trays and jars, decreasing dimensional weight fees for omnichannel distribution. Digital presses such as HP Indigo 200K allow rapid artwork changes, helping regional brands trial limited-edition flavors without tying up working capital in plates. Regulatory scrutiny under the FDA’s New Era of Smarter Food Safety Blueprint elevates pack integrity during direct-to-consumer fulfillment, further reinforcing the converted flexible packaging market demand for high-barrier, resealable solutions.

E-commerce Accelerating Demand for Protective Mailer Formats

Parcel carriers process rising volumes of nutraceuticals, apparel and small electronics, prompting a pivot from corrugate to bubble mailers and recyclable polyethylene shippers that protect items while shrinking package weight. A 2024 Flexible Packaging Association LCA confirmed that poly mailers show lower greenhouse-gas footprints and 47% less fossil energy use than comparable rigid cartons. Amazon and Mondi co-developed curbside-recyclable mailers that won three sustainability awards in 2024, proving the brand equity upside of greener last-mile solutions. U.S. Department of Agriculture research into soy-based biopolymers indicates future entrants could shift protective mailers toward compostable substrates without compromising drop-test performance.

Adoption of High-Barrier Mono-Material Films for Recyclability

Converters race to replace multi-layer PET/Al foil laminates with mono-polypropylene or mono-polyethylene structures that pass Sort-B recycling protocols in Europe. Jindal Films’ BICOR™ MBH568 delivers ≥95% PP composition, matching oxygen and moisture barriers needed for salty snacks while enabling mechanical recycling streams. SÜDPACK’s latest portfolio trims cradle-to-gate CO₂ by one-third versus composite laminates, giving retailers an easy route to hit voluntary Scope 3 targets. EU Regulation 2025/40 accelerates roll-outs by requiring all packaging to be recyclable by 2030.

Advanced Digital Printing Enabling Low-MOQ SKU Proliferation

ePac Flexible Packaging’s fleet conversion to HP Indigo 200K presses hikes run speeds 30% and productivity 45%, letting micro-brands order 5,000-unit campaigns with photo-quality graphics. Windmöller & Hölscher plans a 150 m/min hybrid press that merges flexo white with aqueous-based digital colors for greener operations in 2026. Variable-data printing is turning pouches into engagement tools, embedding QR codes tied to loyalty programs or farm-level traceability, and cutting SKU launch cycles from six months to six weeks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-layer recycling infrastructure gaps | -1.1% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Crude-oil price volatility affecting polymer costs | -0.8% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Extended-Producer-Responsibility fees squeezing margins | -0.6% | EU, expanding to North America, selective Asia-Pacific | Medium term (2-4 years) |

| BOPP/BOPET film overcapacity driving price wars | -0.4% | Asia-Pacific core, spill-over effects globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Layer Recycling Infrastructure Gaps

Deposit-return schemes cover bottles but rarely target films, leaving consumers without pathways to recycle laminated snack or pharma packs. EU PPWR sets 2029 bottle collection targets but is silent on flexible formats, creating compliance uncertainty. [2]Lexology, “Important Changes to EU Packaging Rules,” Lexology.com Advanced recycling alliances, such as Mondelēz and Amcor, delivering Cadbury wrappers with 80% chemically recycled content, prove technical viability yet hinge on unscaled pyrolysis hubs. Capital needs exceeding USD 10 billion may delay infrastructure roll-out in Southeast Asia and LatAm, slowing circularity progress.

Crude-Oil Price Volatility Affecting Polymer Costs

Hurricane Beryl’s 2024 disruption added 5 cents per pound to U.S. polyethylene and polypropylene spot prices, while PET resin ticked up 1 cent amid ethylene glycol tightness. [3]Texas Chemistry Council, “Storm Disruptions Drive Up Resin Prices,” TexasChemistry.org Export volumes now claim 46% of U.S. PE output, heightening domestic shortages during weather events. Smaller converters with weekly resin buys face cash-flow strains as they cannot instantly re-price finished goods, thereby trimming gross margins for the converted flexible packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Disruption Accelerates Despite Plastic Film Dominance

Plastic films retained 38.14% converted flexible packaging market share in 2025 due to entrenched extrusion assets and proven performance in snack, dairy and e-commerce mailer applications. Within this cohort, polyethylene serves frozen foods and stretch hooding, whereas polypropylene gains traction via mono-material initiatives that support recyclability targets under EU 2025/40. Polyethylene terephthalate occupies high-barrier niches like coffee, but its multilayered nature intensifies EPR penalties. Aluminum foil remains critical for pharmaceuticals and instant beverages where 100% moisture-oxygen barrier is non-negotiable.

Bioplastics, although from a smaller base, chart a 7.62% CAGR anchored by starch-blend and PLA advancements that satisfy ASTM backyard-compostable draft standard WK81525. Investments by global resin majors and local start-ups signal capacity ramps that could double supply by 2030. Cost premiums over fossil polymers are narrowing, aided by sugarcane ethanol price stability and policy incentives. Food brands exploit compostable films for produce and single-serve coffee pods, aligning with municipal organics collection roll-outs. The converted flexible packaging market size for bioplastics, therefore, gains momentum as mandatory recycled-content thresholds spur trials of renewable substitutes for hard-to-recycle laminates.

By Packaging Format: Pouches Consolidate Market Leadership Through Versatility

Pouches dominated with 61.63% converted flexible packaging market share in 2025, driven by stand-up models that optimize shelf visibility and ship flat pre-fill, slashing freight emissions. Spout pouches expand into ready-to-drink sports beverages, while retortable variants target ambient pet food and baby food. Digital printing accelerates SKU tiering, enabling seasonal artwork and influencer collaborations without high MOQs. Rollstock and lidding films support high-speed form-fill-seal lines in snacks and yogurt, holding ground where capital equipment is amortized.

The converted flexible packaging market size for pouches is forecast to rise 7.01% CAGR through 2031 as mono-PE laminate breakthroughs close barrier gaps versus PET/foil. Paper-based stand-up pouches with internal bio-coatings debut in premium granola and confectionery, appealing to plastic reduction pledges. Bags and sacks address bulk grains and chemicals, yet slower e-commerce uptake caps expansion. Shaped and zipper formats provide differentiation in crowded aisles, and reseal features curb food waste, a metric tracked by many retailers. As omnichannel commerce blurs traditional trade boundaries, pouch versatility secures its growth trajectory.

By End-use Industry: Pharmaceutical Growth Outpaces Food Market Maturity

Food retained 47.96% revenue share in 2025, spanning bakery, confectionery, dairy, meat and ready meals. Reformulation toward cleaner labels and portion control bolsters demand for high-barrier resealable packs that extend shelf life and support snack-size ergonomics. However, the food segment’s mid-single-digit trajectory is eclipsed by pharmaceutical and healthcare packs advancing at an 8.3% CAGR.

The converted flexible packaging market size in pharma benefits from aging populations and cold-chain biologics that mandate laminated films with low oxygen-transmission rates. FDA’s 2025 serialization update compels tamper-evident and data-carrier features on sachets and blister lidding foils. Oncology and diabetes drug volumes rise, spurring demand for pre-fillable bags and IV pouches. Personal-care and cosmetics leverage metallized stand-up pouches for refill formats, responding to retailer circularity pilots. Household cleaners migrate to concentrated refills in spouted packs, yet reduced volume offsets some growth.

By Distribution Channel: Direct Sales Dominance Reflects Industry Consolidation

Direct contracts accounted for 81.14% converted flexible packaging market share in 2025 as converters engage brand owners via joint-development agreements and long-term price formulas that stabilize resin exposure. Post-pandemic supply chain regionalization has large CPGs preferring fewer but more integrated partners capable of delivering design, laminating, converting, and logistics services within one SLA.

Indirect channels, rising at 6.26% CAGR, comprise distributors and print brokers serving artisanal food makers, nutraceutical start-ups, and private-label retailers. Digital storefronts boost access to dieline libraries and quotation engines, lowering barriers for micro-runs. Hybrid models emerge where converters handle structural design and outsource printing to regional digital hubs. As consolidation abounds, the converted flexible packaging industry still prizes local responsiveness, keeping room for specialist brokers in remote geographies.

Geography Analysis

Asia-Pacific led with 39.62% share in 2025 on the back of integrated resin-to-film complexes, populous consumer bases, and agile converter ecosystems. China’s flexible packaging output hit RMB 121.34 billion in 2023 and is poised for 7.16% CAGR through 2027, buoyed by snack exports and rising ready-meal adoption. Indian demand advances alongside packaged food uptake, yet capacity lags, prompting UFlex to report INR 36,825 million net revenue in Q1 2024 as imports fill gaps. Oversupply of BOPP/BOPET films creates pricing headwinds, but long-term fundamentals remain intact.

North America benefits from a mature recycling infrastructure and e-commerce penetration. State-level EPR legislation drives brand conversions to mono-material pouches, while polymer sourcing risks from Gulf Coast hurricanes keep supply-chain diversification on executive agendas. Digital printing adoption leads globally, with ePac scaling 23 North American sites to service short runs, which raises the region’s technology benchmark.

Europe’s stringent PPWR and escalating EPR fees place it at the forefront of circular-economy innovation. German retailers stipulate minimum 30% recycled content in private-label flexible packs by 2028, accelerating R&D in chemical recycling. The United Kingdom formalized fee schedules in 2024, compelling immediate redesign of multilayer laminates. Eastern Europe serves as cost-competitive production base for Western brands, yet must align with EU recyclability directives.

The Middle East and Africa post the fastest 8.51% CAGR, buoyed by Gulf food-service expansion and African FMCG formalization. Saudi Vision 2030 targets 42% local food self-sufficiency, necessitating pouch and lidding film lines. Nigeria’s sachet water market remains a high-volume user of LDPE film, though environmental agencies push for thicker, recyclable structures.

South America records moderate growth, with Brazil’s agribusiness exports supporting barrier bag demand for coffee and meat. Argentina’s currency volatility tempers capital imports, yet regional players such as Grupo HZ continue to invest in laser scoring and water-based inks for differentiation.

Regulatory Landscape

Regulation (EU) 2025/40 (Packaging and Packaging Waste Regulation, PPWR) entered into force in February 2025 and applies from 12 August 2026, replacing Directive 94/62/EC. It codifies design-for-recycling obligations and is supported by a stepped rollout of secondary legislation, including European Commission guidance published in June 2026 and implementing acts on packaging labelling scheduled for Q4 2026. These requirements directly affect how flexible packs are structured, labelled, and documented for EU market access.

Food-contact compliance remains a core constraint for converted flexible packaging used in food and pharma. Commission Regulation (EU) 2025/351 amends EU rules on plastic materials intended for food contact and sets a transition timeline to 16 September 2026 for the first placing on the market of products complying with previous regulations. This tightens documentation and places limits on legacy materials during the transition window.

Value Chain Analysis

The converted flexible packaging value chain starts with petrochemical and bio-based feedstocks feeding into resin production, film extrusion (PE, PP, PET and specialty barrier layers), and then value-added converting. Converting includes printing (predominantly flexographic), laminating, coating, adhesive application, slitting, pouch-making, and inspection before distribution to brand owners, co-packers, and e-commerce shippers. Compliance and performance requirements increasingly push upstream, with EU PPWR rules applying from 12 August 2026. This drives converters and material suppliers to redesign toward mono-material structures and qualify inks, adhesives, and coatings that meet food-contact and recyclability constraints.

On the commercial side, contract models remain anchored in direct relationships between converters and large FMCG and healthcare buyers, while logistics and recycling pathways shape material choices, particularly for multi-layer laminates that still run into infrastructure gaps. Advanced recycling is being positioned as an enabling node for food- and medical-grade PCR feedstock where mechanical recycling faces quality limits. At the same time, the push for EU design-for-recycling criteria adds testing and documentation steps across material suppliers, converters, and brand owners.

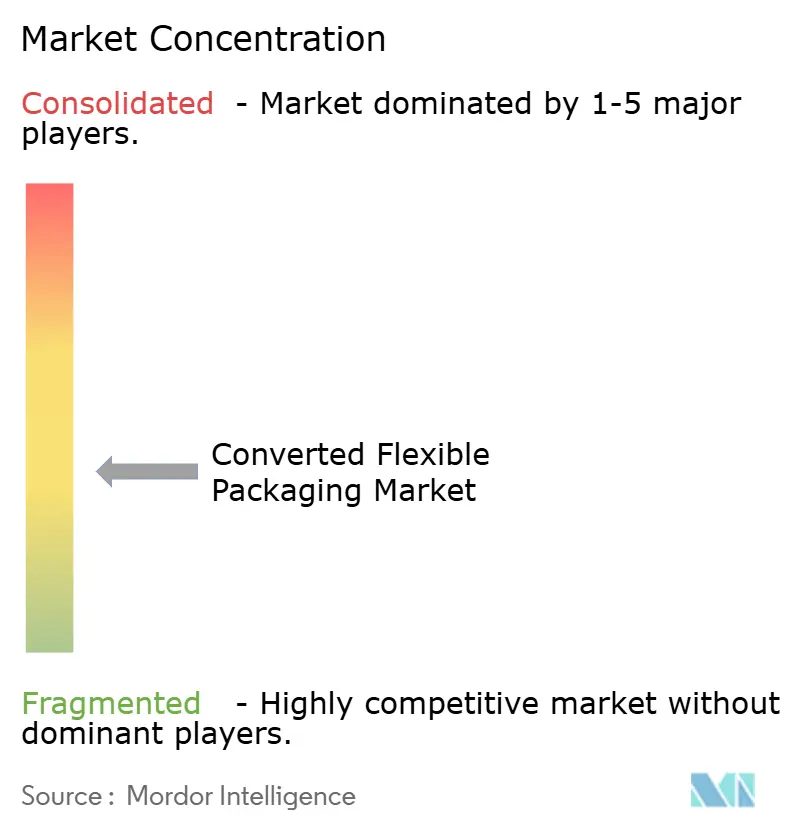

Competitive Landscape

The converted flexible packaging industry demonstrates moderate fragmentation. The Amcor-Berry merger exemplifies scale-driven synergy playbooks, promising USD 650 million cost takeaway via resin procurement, freight consolidation, and cross-selling. Mondi partners with Amazon on award-winning curbside-recyclable mailers, reflecting how co-innovation with e-commerce giants can unlock premium volumes.

Sealed Air leverages equipment-materials integration, linking Cryovac films with Ossid tray overwrappers to deliver verified shelf-life performance for poultry processors. ProAmpac expands its patent estate around mono-material and quadseal pouch designs to underpin private-label bids in North America.

White-space competition intensifies in digital web-to-print, AI-driven defect detection, and closed-loop recycling collaborations. Japanese conglomerate DNP commercialized CEFLEX-aligned PP film for retort applications, courting European co-packing partners. Start-ups pioneer compostable high-barrier cellulose, prompting incumbents to scout venture capital stakes. Patent filings such as Koninklijke Douwe Egberts’ 2-ply seal reinforce incremental advances that lower seal initiation temperature and permit downgauging.

Cost turbulence from resin swings encourages vertical integration; several Asian film producers commission downstream printing and pouching assets to capture margin, while Western converters pilot in-line extrusion-lamination to speed prototype cycles. Sustainability messaging has become table stakes; companies tout life-cycle assessments and carbon-neutral certifications to secure shelf listings with retailers that screen Scope 3 impacts.

Converted Flexible Packaging Industry Leaders

ProAmpac

Amcor Plc

Sealed Air Corporation

Sonoco Products Company

Constantia Flexibles Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Design-for-recycling execution creates whitespace for converters to industrialize mono-material, high-barrier structures and validate compatibility against emerging standards and guidance. A concrete signal is the publication of CEN EN 18120-1:2026, which formalizes definitions and a green/yellow/red compatibility classification. This provides brand owners and converters a shared way to specify recyclable flexible formats and de-risk EU commercialization decisions ahead of PPWR applicability from 12 August 2026.

Capacity and capability upgrades are clustering around high-speed printing and pouch conversion to handle SKU proliferation and premiumization while meeting sustainability constraints. Recent investment activity and operational moves include Coveris adding a high-speed Soma Proxima printing press and a Lemo wicketted-bag machine at two Poland facilities (completed April 2026), New Tech Plastics starting pouch production via an Ohio expansion (announced April 2026), and Cherat Packaging commissioning a second barrier film extrusion line (June 2026). Amcor’s July 2026 facility expansion announcement in China also highlights the pull toward regional manufacturing hubs that shorten lead times for pouches and barrier films used in food, pharma, and e-commerce applications.

Recent Industry Developments

- July 2026: Amcor announced the expansion of a packaging facility in China. The expansion strengthens local supply of converted flexible packaging and supports faster turnarounds for regional brand owners as Asia-Pacific remains the largest demand center.

- March 2026: ProAmpac completed the acquisition of TC Transcontinental Packaging (TCP) for about USD 1.51 billion. The deal expands ProAmpac’s scale and technology footprint across films and converting, supporting broader offerings in recyclable and high-performance flexible formats.

- November 2024: Mondelēz International and Amcor introduced Cadbury wrappers containing 80% recycled plastic using advanced recycling. The launch demonstrated a pathway for incorporating recycled content into high-volume flexible packaging where food-contact performance requirements have limited the use of mechanically recycled material.

Research Methodology Framework and Report Scope

Market Definition and Coverage

Converted flexible packaging is defined as packaging made by converting flexible substrates into finished packs, such as pouches, bags, and lidding or rollstock structures, which are then used by end users for packing, protection, and shelf presentation across everyday goods.

Scope exclusions: We exclude rigid packaging formats. We also do not count machinery, printing presses, or standalone raw resin, paper, or foil sales unless they are converted into a finished flexible pack.

Segmentation Overview

- By Material

- Plastic Film

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Other Plastic Films

- Paper and Paperboard

- Aluminum Foil

- Bioplastics

- Plastic Film

- By Packaging Format

- Pouches

- Rollstock and Lidding Films

- Bags and Sacks

- Other Packaging Formats

- By End-use Industry

- Food

- Bakery

- Dairy

- Confectionery

- Ready Meals

- Other Food Products

- Beverage

- Non-Alcoholic

- Alcoholic

- Pharmaceutical and Healthcare

- Personal Care and Cosmetics

- Household Products

- Other End-use Industries

- Food

- By Distribution Channel

- Direct Sales Channel

- Indirect Sales Channel

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Mexico

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand and supply context for flexible and converted packaging, then narrowing it to finished converted packs. For this, we rely on public sources such as the US Census Bureau manufacturing data, USITC and UN Comtrade trade statistics, Eurostat production and packaging waste series, and OECD environment indicators that help explain packaging usage and regulation signals.

Alongside these, we review company annual reports, investor presentations, and earnings transcripts to understand capacity additions, shifts in substrate mix, and pricing commentary that affects converted pack revenues. Where useful, we also use paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export records to validate trade flows and product descriptions. The sources mentioned above are illustrative and not exhaustive, and many other references were also used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work is used to confirm what is counted as a converted pack. It also helps pressure-test assumptions around product mix, typical price movement, and regional demand shifts. Interviews and surveys were conducted with packaging converters, material ecosystem experts, and procurement and packaging leads from key end-use industries across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | APAC: 37% |

| Mid tier: 53% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 16% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down model. We reconstruct packaging demand by linking end-use consumption needs to converted pack usage, then convert that volume into value using realistic pricing progression.

To keep the model grounded, we track inputs such as flexible pack penetration in food and beverage and retail, shifts toward pouches versus bags and rollstock, substrate mix changes across plastic film, paper, and foil structures, and the effect of lightweighting and downgauging on value growth.

After the main model is built, totals are corroborated with selective bottom-up approximations, including sampled converter revenue splits, channel checks for high-volume applications, and ASP times volume sanity checks for major formats. Where company disclosure does not cleanly separate converted flexible packaging from adjacent packaging revenues, gaps are handled through conservative allocation keys. These allocation keys are validated in interviews and then rechecked against trade and production signals. For forecasting, we use scenario analysis, supported by expert views on regulation-led material shifts, recycled content adoption, and the pace of capacity additions, which together shape the annual growth path.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number is not driven by a single data series. Outputs are compared against independent signals such as packaging production indices, trade direction by substrate and format proxies, and reported pricing commentary. Any unusual jumps are reviewed before sign-off.

A second analyst review confirms assumptions, currency treatment, and year alignment, and we re-contact respondents when a key variable moves outside the expected range. Reports are refreshed annually, and interim updates are added when material events occur, such as major regulation changes or sharp resin and paper price cycles. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Converted Flexible Packaging Market Sizing Compared With Other Published Estimates

Published market sizes for converted flexible packaging often vary, even when the same headline term is used, because firms do not always count the same pack formats, materials, or revenue points. Differences also come from the year used for pricing, the timing of currency conversion, and the level of primary validation for product mix and regional splits.

The biggest spread usually comes from whether rollstock and lidding films are counted as converted finished packs, and from how resin, paper, and foil price swings flow into average selling prices across pouches and bags. These assumptions are refreshed and rechecked through converter interviews and trade flow signals in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 262.06 B (2025) | |

| Industry Research Publisher A | USD 170.38 B (2024) | Uses an earlier base year and appears to apply a narrower revenue pool, with less clarity on whether rollstock and lidding are fully included within the converted pack total across regions. |

| Industry Research Publisher B | USD 331.60 B (2025) | Shows a higher 2025 value that likely reflects broader scope choices, such as folding in adjacent flexible packaging revenues or applying stronger price and mix escalation across materials and product types. |

The table indicates that scope choices around what qualifies as a converted pack, plus how price and mix are treated year to year, explain most of the difference across published values. When these inputs are stated clearly and checked against independent signals, users can follow the math and replicate the sizing steps with reasonable effort.

Key Questions Answered in the Report

What is the projected size of the global converted flexible packaging space by 2031?

It is set to climb from USD 262.06 billion in 2025 to USD 351.92 billion by 2031.

Which geography is expanding fastest through 2031?

The Middle East and Africa is advancing at an 8.51% CAGR between 2026-2031.

Why are pouches gaining such a dominant position among converted flexible formats?

Stand-up and spouted pouches lower freight emissions, offer strong shelf impact and now incorporate recyclable mono-material barriers, giving them 61.63% share in 2025 and a 7.01% CAGR to 2031.

How will EU Regulation 2025/40 change packaging design decisions after 2026?

The rule requires every pack sold in the EU to be recyclable by 2030 and imposes a 30% recycled-content minimum on single-use plastic bottles from August 2026, driving rapid adoption of mono-material films.

What role does digital printing play for small and medium brands in flexible packs?

High-speed presses such as the HP Indigo 200K enable 5,000-unit custom runs, cutting time-to-launch and inventory exposure for niche SKUs.

How concentrated is the competitive landscape after the Amcor-Berry combination?

The top five suppliers now command just over 60% combined share, corresponding to a concentration score of 6.

Page last updated on: