Market Overview

| Study Period | 2020 - 2031 |

|---|---|

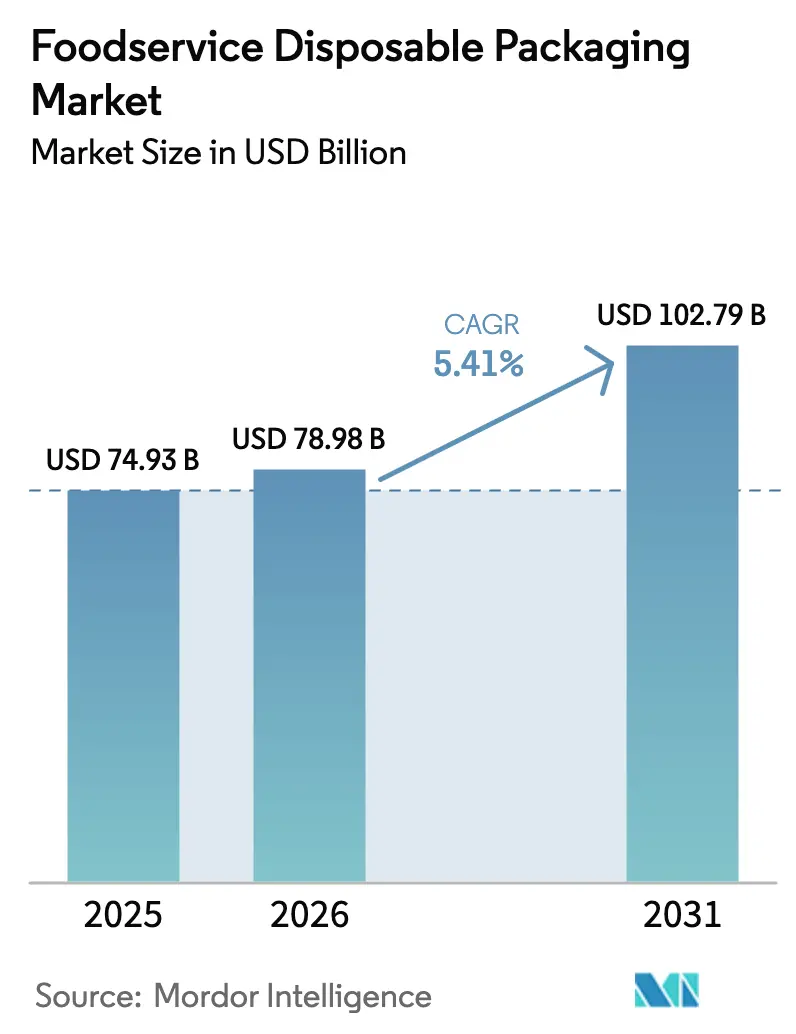

| Market Size (2026) | USD 78.98 Billion |

| Market Size (2031) | USD 102.79 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foodservice Disposable Packaging Market Analysis by Mordor Intelligence

The foodservice disposable packaging market size was valued at USD 74.93 billion in 2025 and estimated to grow from USD 78.98 billion in 2026 to reach USD 102.79 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). This performance confirms a resilient upward trajectory for the foodservice disposable packaging market despite cost inflation and regulatory pressure. Heightened off-premise dining, stricter material safety rules, and rapid institutional adoption continue to propel demand. Regulatory frameworks in the European Union and Asia-Pacific are accelerating material innovation toward fiber and bio-plastic formats, while digital food ordering underscores the need for tamper-evident containers that safeguard brand trust. Manufacturers are therefore prioritizing barrier technologies that exclude PFAS, improve recyclability, and reduce carbon footprints. Concurrently, supply-chain volatility—especially in polylactic acid (PLA) resin—has prompted regional production shifts and price hedging strategies. Competitive intensity remains moderate, with consolidation underway as firms pursue scale and research synergies to meet evolving customer specifications.

Key Report Takeaways

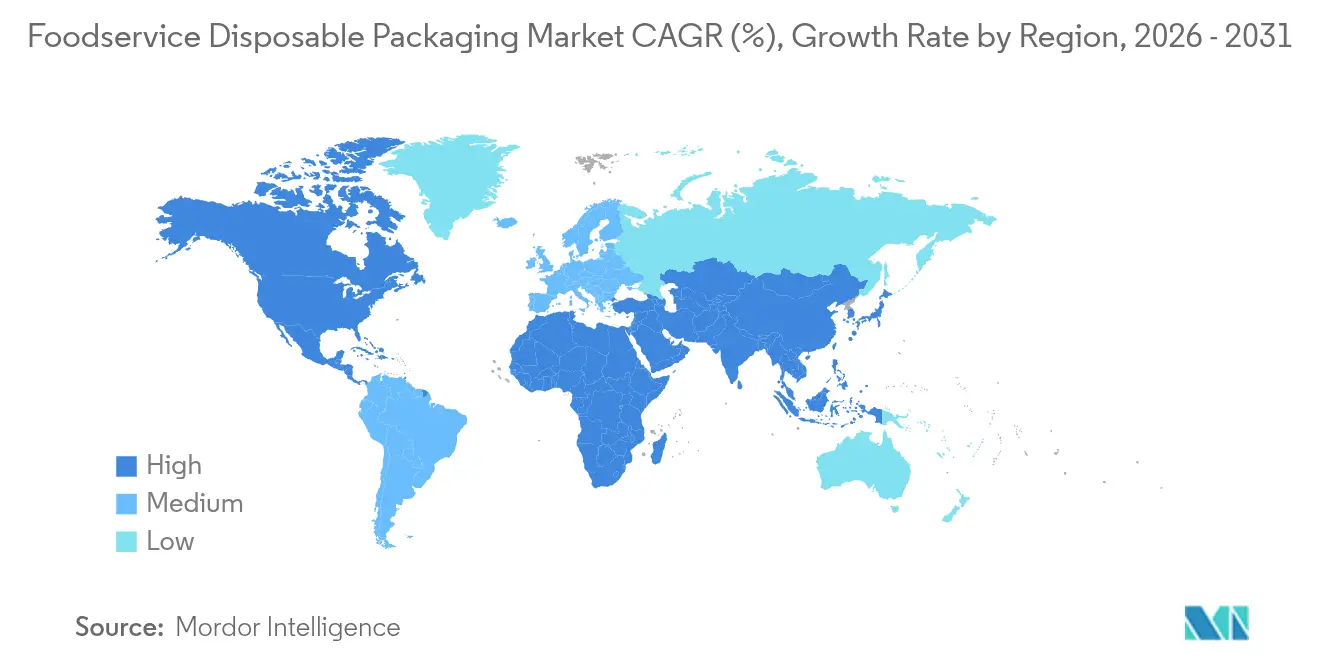

- By geography, Asia-Pacific led with 42.10% of foodservice disposable packaging market share in 2025, while the Middle East & Africa region is advancing at a 6.95% CAGR toward 2031.

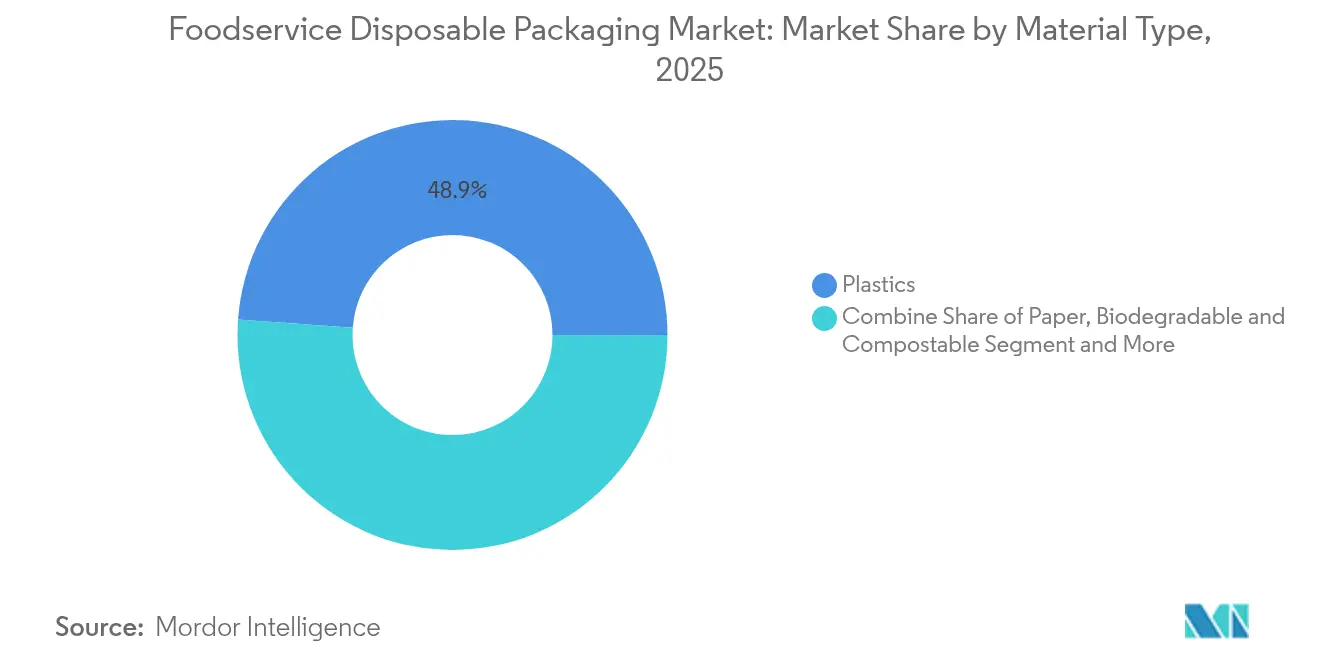

- By material, plastics retained 48.85% share of the foodservice disposable packaging market size in 2025, whereas biodegradable and compostable formats are expanding at a 8.88% CAGR.

- By product type, cups & lids secured 26.21% of the foodservice disposable packaging market share in 2025; trays & plates are set to grow at 6.92% CAGR through 2031.

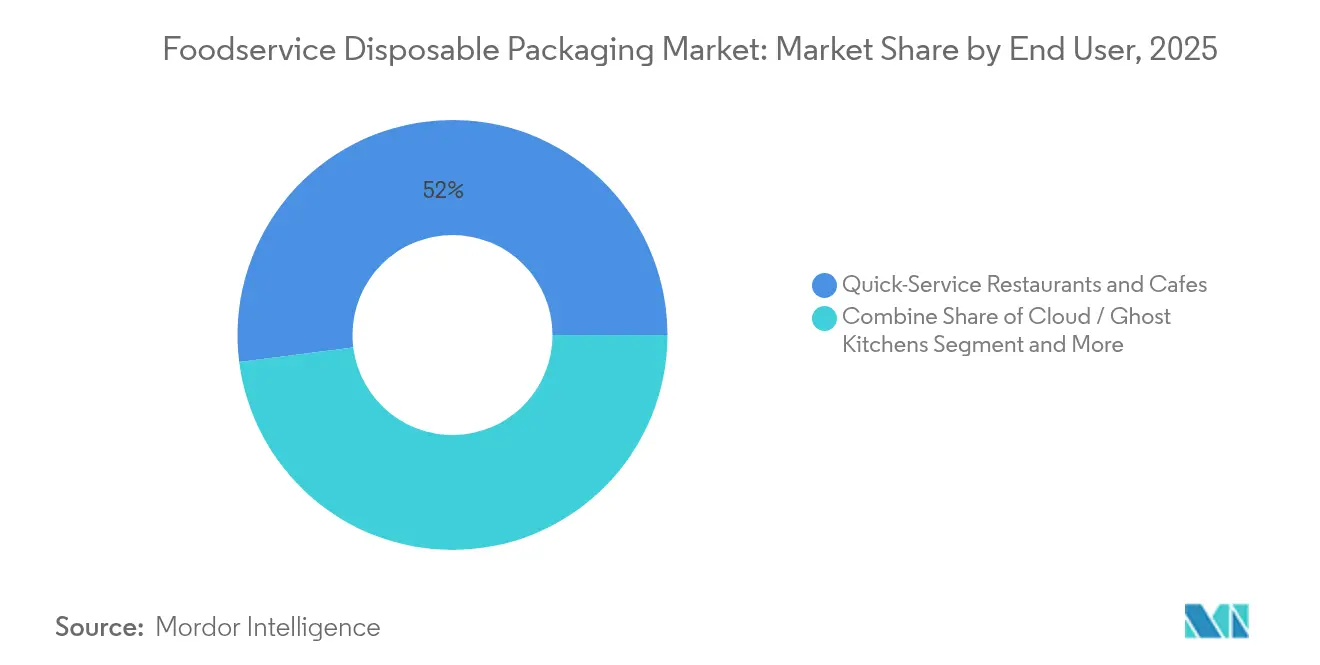

- By end user, quick-service restaurants accounted for 52.00% share of the foodservice disposable packaging market size in 2025, while ghost and cloud kitchens are rising at a 8.74% CAGR.

- By distribution channel, direct sales represented 56.20% of the foodservice disposable packaging market size in 2025; indirect channels are forecast to increase at 6.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Foodservice Disposable Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ghost kitchens and online delivery boosting tamper-evident packaging demand | +1.2% | Global – North America & Asia-Pacific core | Medium term (2-4 years) |

| EU and Asian sustainability mandates shifting demand to fiber-based packaging | +0.9% | Europe & Asia-Pacific with spill-over to North America | Long term (≥ 4 years) |

| Expansion of QSR chains in various countries | +0.8% | Global – strongest in emerging markets | Medium term (2-4 years) |

| Post-hygiene focus raising single-use trays in Middle-East institutions | +0.6% | Middle East & Africa; institutional sectors globally | Short term (≤ 2 years) |

| Adoption of heat-resistant molded-fiber bowls for hot off-premise meals | +0.5% | North America & Europe; expanding to Asia-Pacific | Medium term (2-4 years) |

| Diversified beverage menus driving cup-lid innovation | +0.4% | Global – led by North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Ghost Kitchens and Online Delivery Boosting Tamper-Evident Packaging Demand

Digital ordering now represents 40% of total U.S. restaurant sales, compelling operators without dining rooms to treat packaging as their primary brand touchpoint. Tamper-evident solutions such as DayMark Safety Systems’ TamperSeal labels and Dart Container’s ClearPac SafeSeal hinge technology reassure customers by showing visible breach indicators. [1]DayMark Safety Systems, “TamperSeal Labels,” daymarksafety.comBecause third-party platforms rank restaurants partly on security scores, adoption of such packaging is now a competitive necessity. Operators also favour integrated tamper features over add-on shrink bands to reduce labour steps and material usage.

EU and Asian Sustainability Mandates Shifting Demand to Fiber-Based Packaging

The European Union’s Packaging and Packaging Waste Regulation, effective February 2025, requires all packaging to achieve recyclability by 2030 and bans PFAS in food contact materials. Parallel policies—China’s GB 4806.15-2024 for food-contact adhesives and Japan’s Positive List for synthetic resins—tighten compliance thresholds across Asia. Producers such as Huhtamaki have scaled fiber-lid capacity in Northern Ireland to match this regulatory pull. Together, these rules reposition fiber as a compliance imperative rather than a voluntary sustainability choice, pushing global brands to redesign legacy SKUs.

Expansion of QSR Chains in Various Countries

Global quick-service chains are opening new outlets while tailoring menus to local tastes, driving uniform yet flexible packaging lines. Burger King’s roll-out of fibre-based wraps illustrates how multinational players reconcile brand consistency with country-specific material laws. Pactiv Evergreen’s SmartPour containers, featuring resealable closures, reduce ingredient loss and enhance in-store efficiency, thereby supporting faster counter-service formats. Segment growth thus stems not only from outlet expansion but also from packaging innovations that reduce service friction.

Post-Hygiene Focus Raising Single-Use Trays in Middle-East Institutions

Hospitals, universities, and large-scale canteens across the GCC have tightened hygiene protocols, favouring disposable trays that limit cross-contamination. Hotpack’s decision to invest USD 100 million in a New Jersey plant will supply both North American buyers and Middle-East export demand with customised single-use formats. Government procurement guidelines that weigh nutritional and environmental factors further reinforce purchase of compostable or recyclable trays, especially where dish-washing logistics are limited.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs: a major barrier to paper packaging adoption | -0.8% | Global – strongest in emerging markets | Medium term (2-4 years) |

| Municipal PFAS bans reducing viability of existing inventory | -0.6% | North America & Europe with ripple to Asia-Pacific | Short term (≤ 2 years) |

| PLA resin supply bottlenecks elevating bioplastic costs | -0.5% | Global – production centered in Asia-Pacific | Medium term (2-4 years) |

| Aggregator consolidation squeezing unit pricing for suppliers | -0.4% | North America & Europe delivery markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Costs: A Major Barrier to Paper Packaging Adoption

A second wave of containerboard price hikes of USD 70 per metric ton took effect in January 2025, burdening operators who had already absorbed earlier inflation. [2]Creative Edge Packaging, “Navigating the USD 70 Per Ton Increase,” cepkg.comEnergy and freight surcharges compound the premium for fibre formats over conventional plastics, slowing substitution in cost-sensitive emerging markets. Smaller foodservice businesses with tight cash flow have little bargaining power and often postpone switching to compostable paper, even where regulations encourage it.

Municipal PFAS Bans Reducing Viability of Existing Inventory

The U.S. FDA has ruled 35 PFAS-related food-contact notifications inactive, forcing a nationwide sell-through deadline of June 2025. [3]U.S. Food and Drug Administration, “Determination on 35 PFAS Notifications,” fda.govEleven U.S. states already enforce separate bans, complicating inventory planning for multi-state distributors. Manufacturers holding legacy stock face write-downs, and retailers must vet incoming supplies to avoid non-compliant materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Biodegradable Surge Challenges Plastic Dominance

Plastics held 48.85% of foodservice disposable packaging market share in 2025, yet biodegradable and compostable formats are accelerating at a 8.88% CAGR. Braskem’s launch of WENEW bio-circular polypropylene sourced from used cooking oil shows how drop-in replacements can decarbonise mainstream resin grades without performance loss. Amcor has secured European patents for AmFiber Performance Paper, a high-barrier recyclable paper that competes directly with metallised films. Graphic Packaging’s oven-ready PaperSeal Cook Tray extends fibre utility to hot applications, broadening addressable end-use cases.

Momentum in this segment also rides on supply-side capacity: global PLA production topped 700 kilotons in 2022, with Asia-Pacific controlling 70% of output and 60% of consumption. BioPak eliminated PFAS from its plant-fibre line in July 2024 and introduced PHA-lined coffee cups that meet home-compost standards. Sabert’s Pulp Ultra containers underscore how moisture-resistant coatings can allow fibre to displace plastic in greasy hot-food contexts. Collectively, these developments signal a tipping point where technical hurdles are receding faster than cost premiums.

By Product Type: Trays Accelerate as Cups Maintain Leadership

Cups & lids commanded 26.21% of the foodservice disposable packaging market size in 2025, supported by continued beverage innovation. SIG’s bag-in-box solution for cold-brew coffee trims weight versus glass and improves shelf-life. Conversely, trays & plates are projected to grow at a 6.92% CAGR as hot meal delivery proliferates. Huhtamaki’s fibre ready-meal trays for Nordic supermarkets prove that ovenable fibre can satisfy retail as well as foodservice channels.

Growth in trays is also linked to institutional catering where single-use solutions remain hygiene-critical. SEE’s compostable meat trays—54% bio-based and 45% recycled—illustrate hybrid material strategies that ease operator transition. ProAmpac’s leak-resistant RotiBag provides heat retention, integrated handles, and reduced packaging weight, demonstrating how targeted design solves delivery pain points while using fewer materials.

By End User: Ghost Kitchens Disrupt QSR Dominance

Quick-service restaurants still account for 52.00% of the foodservice disposable packaging market size in 2025 due to network scale and standardised menus. Nevertheless, ghost kitchens are expanding at a 8.74% CAGR, making them the fastest-growing end-user group. Their model eliminates dine-in space but places higher functional and aesthetic burdens on packaging, which becomes the only physical brand experience. Tamper evidence, temperature retention, and share-worthy presentation drive packaging specifications and willingness to pay.

Institutional catering likewise seeks single-use formats to satisfy elevated hygiene benchmarks. Large hospital chains and school districts increasingly include compostability clauses in tenders, nudging suppliers toward moulded fibre or rPET with verified end-of-life pathways. Full-service restaurants, meanwhile, continue to broaden take-out menus, blending traditional plating with off-premise-friendly containers.

By Distribution Channel: Indirect Sales Gain Momentum

Direct sales held 56.20% of foodservice disposable packaging market share in 2025, reflecting long-standing supplier contracts with multinational chains. Custom tooling, joint R&D, and volume rebates anchor these relationships. Yet the indirect channel is growing at 6.60% CAGR as small and medium operators multiply. Distributors add value by curating compliant SKUs and offering just-in-time inventory, a critical service for ghost kitchens operating with limited storage. E-commerce portals extend this reach, allowing niche producers to showcase compostable innovations without building sales teams in every region.

While direct relationships grant insight into customer forecasts, they expose manufacturers to concentration risk. Indirect channels diversify customer bases but require investments in digital catalogues and training that teach operators correct end-of-life disposal, reinforcing brand reputation and regulatory compliance.

Geography Analysis

Asia-Pacific dominated the foodservice disposable packaging market with 42.10% share in 2025. Robust quick-service expansion in India, Indonesia, and Vietnam, coupled with Beijing’s updated food-contact adhesive rule effective February 2025, ensures strong regulatory alignment toward safer materials. The region also hosts the bulk of global PLA capacity, establishing a cost advantage for biodegradable formats. Japan’s Positive List system entering force in June 2025 tightens resin compliance and spurs domestic fibre investment, while Hong Kong’s phased plastic tableware ban guides hospitality buyers toward compostable alternatives.

Europe remains an agenda-setter thanks to the Packaging and Packaging Waste Regulation that mandates full recyclability by 2030. Producers across the continent are accelerating fibre capacity, and extended producer responsibility schemes distance landfill from acceptable end-of-life routes. North America faces a patchwork of state-level PFAS bans; federal alignment arrived when the FDA completed the PFAS phase-out in February 2024. These overlapping rules complicate compliance but also create a market pull for barrier-coated paper bowls and rPET lids.

The Middle East & Africa region is expected to post 6.95% CAGR through 2031 as infrastructure growth feeds demand for institutional catering disposables. Local champions like Hotpack are investing abroad to secure resin supply and technical know-how, then re-importing finished or semi-finished goods to service GCC contracts. Pilot recycling projects, such as SIG’s beverage-carton retrieval in Egypt, aim to build circular solutions even in nascent waste-management systems.

Latin America shows steady demand growth as disposable tableware accompanies retail meal kits and convenience-store food programs. Regional producers often adapt European fibre designs but utilise locally sourced sugar-cane bagasse, reflecting both cost and sustainability priorities.

Competitive Landscape

The foodservice disposable packaging industry exhibits fragmentation, with global leaders holding noticeable but not overwhelming shares across product lines. Strategic M&A is reshaping the field: Novolex’s USD 6.7 billion merger with Pactiv Evergreen in April 2025 created a portfolio exceeding 250 brands and 39,000 SKUs. Amcor’s planned USD 8.4 billion acquisition of Berry Global similarly illustrates a push toward scale in research, recycling infrastructure, and global distribution.

Technology differentiation remains a core battleground. Dart Container’s Dry Molded Fiber roll-out in partnership with PulPac promises 80% lower CO₂ and faster cycles, making it attractive for high-volume SKUs. Huhtamaki is augmenting fibre cup and lid capacity to meet European and Asian compliance timetables, while Braskem’s bio-circular PP gives converters a drop-in resin with lower emissions. Numerous regional firms concentrate on niche opportunities: Genpak’s PFAS-free fibre line satisfies municipal bans; BioPak’s PHA coatings support backyard composting; and SEE’s hybrid trays bridge meat-case performance with compostability.

Competitive intensity is further shaped by raw-material volatility. PLA prices fluctuated to USD 2,390 per metric ton in Q4 2024, prompting processors to hedge supplies or co-develop feedstock contracts with bio-refineries. Upward cost pressure incentivises process innovations that reduce gram weights, expand rapid-cycle moulding, or incorporate higher recycled content without performance penalties.

Foodservice Disposable Packaging Industry Leaders

Huhtamäki Oyj

Sealed Air Corporation

Amcor plc

Smurfit Westrock

Novolex Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Metsä Group and Amcor formed a partnership to commercialise moulded-fibre food packs, merging Metsä’s pulp expertise with Amcor’s global converting capabilities.

- May 2025: Hotpack invested USD 100 million to open its first U.S. manufacturing site in Edison, New Jersey, targeting customised disposables for institutional buyers.

- April 2025: Novolex completed its USD 6.7 billion merger with Pactiv Evergreen, creating a combined paper, plastic, and fibre portfolio across North America and Europe.

- February 2025: The EU’s Packaging and Packaging Waste Regulation entered into application, banning PFAS in food-contact packaging and mandating full recyclability by 2030

Global Foodservice Disposable Packaging Market Report Scope

Disposable food packaging refers to packaging products such as containers, bowls, plates, trays, cartons, cups, forks, knives, spoons, straws, lids, bags, sacks, wrapping, and other items that are designed for one-time use. The use of such products in the foodservice sector is termed as food service disposable packaging.

For the scope of the study, the Foodservice Disposable Packaging Market is segmented by packaging format (paper-based, plastic, aluminum foil, tissues), end user (restaurants, retail establishments, institutional, and other end-user applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America).

The scope of the study for tissue is limited to paper-based, while the restaurants cover quick and full-service-based restaurants. The study tracks the foodservice disposable market through value accrued from the sales of disposable packaging solutions offered by vendors across the globe. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Material Type

| Plastics | Polypropylene (PP) |

| Polyethylene Terephthalate (PET) | |

| Other Plastic Types | |

| Paper | Coated paper |

| Kraft paper | |

| Molded fiber | |

| Aluminum | |

| Biodegradable and Compostable |

By Product Type

| Cups and Lids |

| Tubs and Containers |

| Trays and Plates |

| Cutlery, Stirrers and Straw |

| Other Product Types (Bags, Wraps, Boxes, Cartons, Clamshell, etc.) |

By End User

| Quick Service Restaurants and Cafes |

| Full-service Restaurants |

| Cloud / Ghost Kitchens |

| Institutional Catering (Hospitals, Schools) |

| Other End User |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastics | Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |||

| Other Plastic Types | |||

| Paper | Coated paper | ||

| Kraft paper | |||

| Molded fiber | |||

| Aluminum | |||

| Biodegradable and Compostable | |||

| By Product Type | Cups and Lids | ||

| Tubs and Containers | |||

| Trays and Plates | |||

| Cutlery, Stirrers and Straw | |||

| Other Product Types (Bags, Wraps, Boxes, Cartons, Clamshell, etc.) | |||

| By End User | Quick Service Restaurants and Cafes | ||

| Full-service Restaurants | |||

| Cloud / Ghost Kitchens | |||

| Institutional Catering (Hospitals, Schools) | |||

| Other End User | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the foodservice disposable packaging market?

The foodservice disposable packaging market size is USD 78.98 billion in 2026.

How fast is the foodservice disposable packaging market expected to grow?

The market is projected to register a 5.41% CAGR, reaching USD 102.79 billion by 2031.

Which region leads global demand?

Asia-Pacific commands 42.10% of 2025 revenue thanks to rapid urbanisation, QSR expansion, and strong local manufacturing.

Which material segment is growing the quickest?

Biodegradable and compostable packaging is forecast to expand at a 8.88% CAGR, driven by regulatory mandates and consumer preference.

What impact do PFAS bans have on suppliers?

National and municipal PFAS bans obligate companies to retire non-compliant inventory and invest in alternative barriers, trimming the sector’s CAGR by an estimated 0.6%.

Why are ghost kitchens important for packaging vendors?

Ghost kitchens rely entirely on delivery, making packaging the primary brand interface; this segment is projected to grow at 8.74% CAGR through 2031, spurring demand for tamper-evident, thermally robust solutions.

Page last updated on: