Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

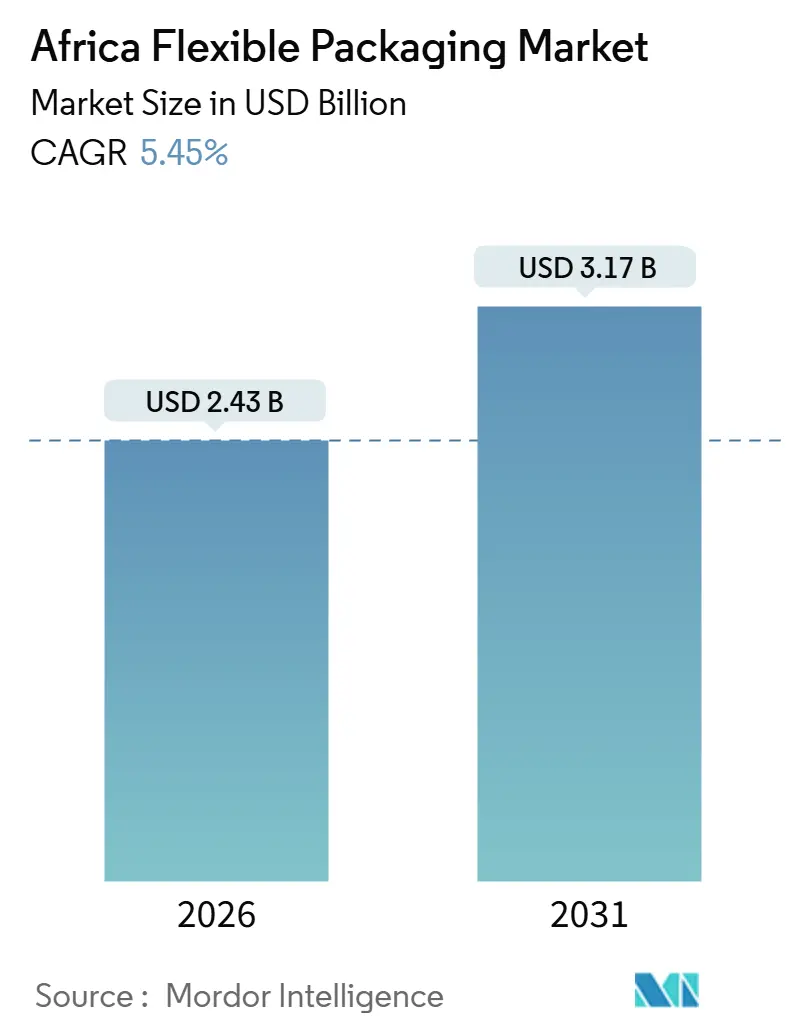

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Flexible Packaging Market Analysis by Mordor Intelligence

The Africa flexible packaging market size is valued at USD 2.43 billion in 2026 and is projected to reach USD 3.17 billion by 2031, expanding at a 5.45% CAGR over the forecast period. This growth arises from tariff reductions under the African Continental Free Trade Area that stimulate cross-border agri-food processing investments, the rapid rollout of modern retail formats in metropolitan corridors, and large brand owners’ sustainability targets that accelerate mono-material film adoption. Converters able to deliver longer shelf-life, low-cost formats while meeting recyclability criteria gain a structural advantage. Multinational commitments to local production amplify demand for high-barrier laminates, whereas extended producer responsibility rules in South Africa and Kenya tilt specifications toward polyethylene-based mono-structures. Supply security of virgin and recycled resins remains a strategic imperative as converters navigate volatile exchange rates and patchy petrochemical capacity. Regional demand still concentrates in South Africa, Nigeria, and Egypt, yet policy leadership in Kenya and Morocco heavily influences design-for-recycling benchmarks across the entire Africa flexible packaging market.

Key Report Takeaways

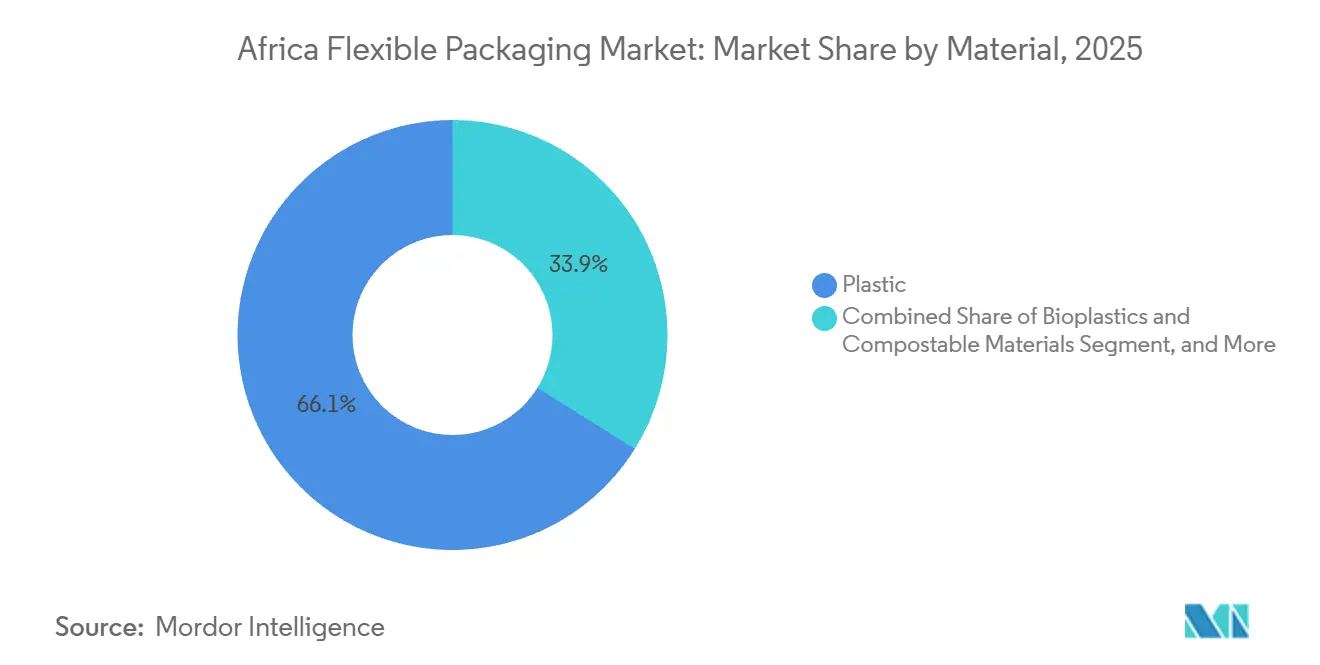

- By material, plastics led with 66.12% of the Africa flexible packaging market share in 2025 while bioplastics and compostables are forecast to advance at a 6.77% CAGR through 2031.

- By product type, bags and pouches commanded 47.63% of the Africa flexible packaging market size in 2025, whereas sachets and stick packs are expected to register the fastest 7.23% CAGR to 2031.

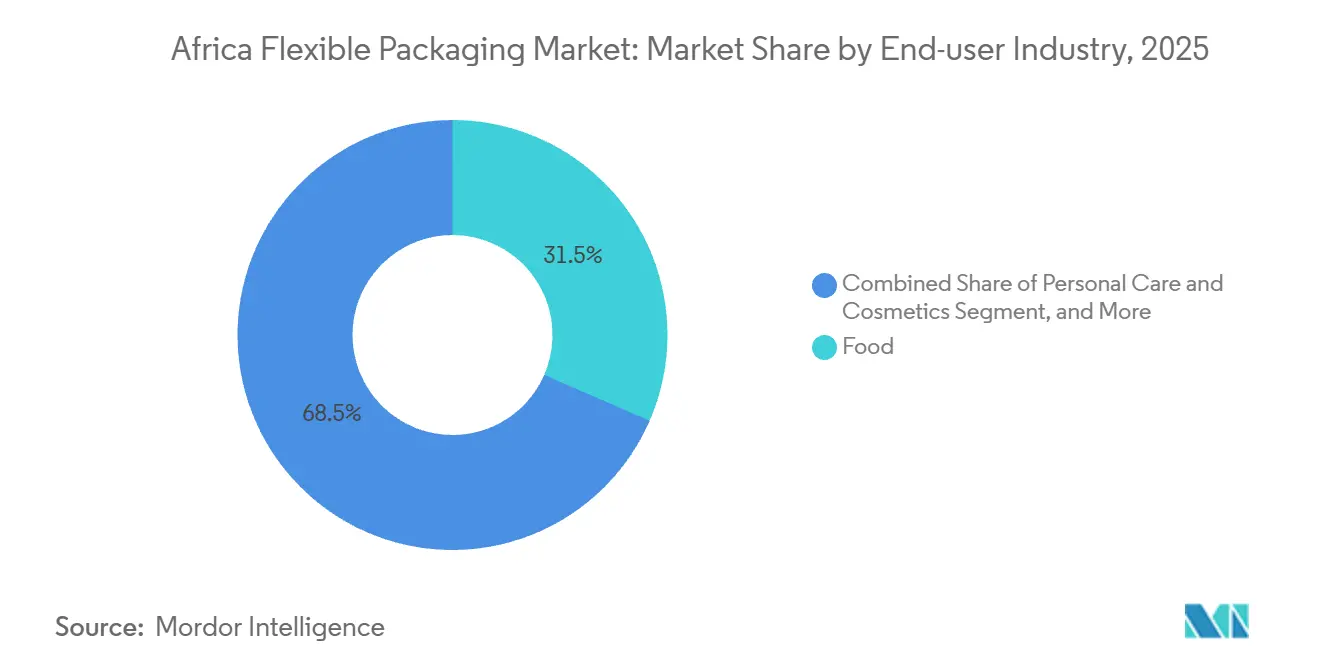

- By end-user, food accounted for 31.53% of the 2025 revenue, but personal care and cosmetics are poised to expand at a 6.87% CAGR from 2026-2031.

- By printing technology, flexography held 45.72% revenue share in 2025 and digital printing is projected to grow at a 7.01% CAGR as brands prioritize rapid design changeovers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Agri-food Processing Investments Under AfCFTA | +1.2% | Ghana, Côte d'Ivoire, Tanzania, Pan-African | Long term (≥ 4 years) |

| Longer Shelf-Life Requirements for Food Exports | +1.1% | Egypt, Morocco, South Africa | Medium term (2-4 years) |

| Growth of Modern Retail Formats Across Urban Africa | +1.0% | South Africa, Nigeria, Kenya, Ghana | Medium term (2-4 years) |

| Rising Demand for Convenient and On-the-Go Packaging | +0.8% | Nigeria, Kenya, South Africa urban centers | Short term (≤ 2 years) |

| Mainstream Adoption of Mono-Material Films | +0.7% | South Africa, Kenya, spillover to Nigeria, Egypt | Long term (≥ 4 years) |

| Government Incentives for Local Converting | +0.6% | Egypt, South Africa, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Agri-Food Processing Investments Under AfCFTA

Tariff elimination on 90% of goods catalyzed USD 12 billion in processing plants between 2023 and 2025, generating sustained pull for multilayer barrier films able to preserve cocoa, cashew, and cassava derivatives during intra-African transit. Rules-of-origin thresholds require producers to source packaging locally, boosting visibility of volume for converters certified to ISO 9001 and FSSC 22000. Nigeria’s cassava program alone targets 20 million t throughput by 2027, requiring moisture-barrier pouches that domestic suppliers such as Sonnex Packaging co-developed with machinery vendors. AfCFTA’s dispute-settlement body, operational since 2024, lowers trade-policy risk, encouraging converters to expand logistics footprints across customs unions. Collectively, these elements raise the baseline demand in the African flexible packaging market while rewarding plants with multilingual artwork capabilities and harmonized regulatory text libraries.

Longer Shelf-Life Requirements for Food Exports

Agricultural shipments from Africa to the European Union and the Middle East reached USD 35 billion in 2025, yet 30-40% post-harvest losses persist in areas with limited cold-chain access.[1]Food and Agriculture Organization, “News – Africa,” fao.org High-barrier films made from ethylene vinyl alcohol or metallized polyester extend shelf life by 2- to 3-fold, enabling Kenyan horticulture to reach European shelves within 72 hours without refrigeration. Morocco’s proximity to Iberian ports positions it as an early adopter of modified-atmosphere pouches, a platform Constantia Flexibles rolled out across North Africa in 2024. Egypt’s dual-sea access enables converters to distribute barrier laminates into Middle Eastern markets, where dates and nuts degrade rapidly in humid environments. Export imperatives, therefore, accelerate technology diffusion and help narrow the historic performance gap between locally converted and imported packaging.

Growth of Modern Retail Formats Across Urban Africa

Chain supermarkets and hypermarkets widened shelf space for packaged goods, compelling suppliers to adopt standardized sizes, clear barcode zones, and fully recyclable components. Shoprite’s pledge to reach 98.7% recyclable, reusable, or compostable packaging by 2025 forces upstream vendors to shift from foil-based laminates to recyclable mono-polyethylene structures. Carrefour’s entry into Kenya and Uganda further disseminates private-label guidelines that privilege drop-in recycled content and life-cycle assessments. Consolidated purchasing power lets retailers demand just-in-time deliveries, so converters with region-wide warehouses and route-to-market analytics win long-term framework contracts. As organized trade expands beyond 30% share of consumer goods in the Africa flexible packaging market during the outlook, suppliers unable to guarantee sustainability compliance risk delisting.

Rising Demand for Convenient and On-the-Go Packaging

Urbanization rates above 3.5% annually across sub-Saharan Africa produce commuting populations that favor portion-controlled formats. Nigeria’s urban dwellers surpassed 100 million in 2024, and street vendors account for more than 60% of food transactions, reinforcing demand for sachets and single-serve wraps.[2]United Nations Department of Economic and Social Affairs, “World Urbanization Prospects,” population.un.org Flexible films weigh 70-90% less than glass or rigid plastics, trimming logistics costs where fuel subsidies have been phased out. Rising female labor participation, already 52% in East Africa by 2025, reduces available meal-prep time, thereby lifting sales of ready-to-eat items that require high-performance barrier films.[3]International Labour Organization, “ILO Africa,” ilo.org These demographic forces sustain above-market growth for personal care, snack, and beverage sachets within the broader Africa flexible packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Volatility in Polymer Resin Prices | -0.7% | Import-dependent markets across West and East Africa | Short term (≤ 2 years) |

| Rising Anti-Plastic Legislation in Key Markets | -0.6% | Kenya, Rwanda, South Africa | Medium term (2-4 years) |

| Fragmented Collection and Recycling Infrastructure | -0.5% | Nigeria, Kenya, Ghana | Long term (≥ 4 years) |

| Import Tariff Barriers on High-Barrier Substrates | -0.4% | Nigeria, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Volatility in Polymer Resin Prices

Polyethylene and polypropylene swung between USD 800 and USD 1,400 per t in 2025, magnified by exchange-rate depreciation of local currencies such as the Nigerian naira, which fell 42% against the U.S. dollar over 24 months. Converters that import 70-85% of their feedstock struggle to maintain margins when resin spikes coincide with power outages and logistics bottlenecks. Egypt’s sole polypropylene producer covers only 40% of national demand, forcing imports even where domestic capacity exists. Creditworthy multinationals lock in multi-year supply at indexed discounts, but mid-tier converters often lack the collateral to secure such contracts. Consequently, price volatility tempers investment in new lines and may delay sustainability upgrades across the Africa flexible packaging market.

Rising Anti-Plastic Legislation in Key Markets

Kenya’s 2017 plastic bag ban imposes fines of up to USD 40,000 or up to 4 years' imprisonment, spurring a pivot toward paper-poly hybrids and certified compostables. Rwanda maintains similar prohibitions, while South Africa’s extended producer responsibility rules make brand owners finance collection and recycling. Such regulations increase compliance costs, especially for converters reliant on multilayer films that lack viable end-of-life solutions. Capital is therefore constrained toward recycling-ready mono-materials, yet these alternatives sometimes compromise barrier performance, creating trade-offs that restrain certain high-moisture applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Gain Traction Within a Plastic-Dominated Portfolio

Plastics command 66.12% of the Africa flexible packaging market share in 2025, highlighting entrenched cost and performance benefits, but bioplastics exhibit a sector-leading 6.77% CAGR through 2031. Multinational food-service chains in Cape Town switched to polylactic acid sachets following the 2024 compostable-packaging ordinance, elevating demand for EN 13432-certified films.

The mainstream portfolio still revolves around polyethylene in multiple densities and biaxially oriented polypropylene for snack laminates. Yet brand-owner hedges against future bans spur converters to co-extrude or laminate both fossil-based and bio-based resins on the same asset base. This dual-capability strategy deepens capital expense but secures relevance as governments expand single-use plastic restrictions across the Africa flexible packaging market.

By Product Type: Sachets Outpace Bags and Pouches on Affordability

Bags and pouches accounted for 47.63% of the Africa flexible packaging market in 2025, serving staples ranging from rice to powdered beverages. However, sachets and stick packs are forecast to grow at a brisk 7.23% CAGR backed by Nigeria’s unit-dose economy, where household spending per transaction rarely exceeds USD 0.20.

Converters winning in this segment deploy servo-driven form-fill-seal equipment that shifts between 10 ml sachets and 1 kg pillow pouches within hours, enabling simultaneous price-point experimentation. The operational agility, combined with high-barrier sealant layers, explains why sachet suppliers achieve line utilization rates near 85% even during seasonal demand dips, reinforcing their share in the African flexible packaging market.

By End-User: Personal Care Surges Ahead of Food’s Established Base

Food applications still account for 31.53% of market share in 2025, anchored by baked goods and dried staples. Yet the personal care and cosmetics segment is projected to register a 6.87% CAGR through 2031 as global brands localize production to avoid import duties and currency risk. Unilever’s USD 30 million expansion into Nigerian sachet shampoo illustrates the strategic pivot toward small-format, high-turnover SKUs.

Pharmaceutical demand, though lower in tonnage, commands premium margins due to good manufacturing practice certification and cold-form foil requirements. This dynamic adds complexity to converter portfolios, obliging stringent hygiene management while maintaining cost competitiveness in the mass food sector of the Africa flexible packaging market.

By Printing Technology: Digital Printing Accelerates for Short Runs

Flexography retained a 45.72% share in 2025, providing a balance of cost and substrate versatility. Digital presses, however, are set to expand at a 7.01% pace, driven by craft beverage brands needing 500-unit micro-runs and rapid artwork changes. HP Indigo installations in South Africa allow the same-week launch of seasonal designs, compressing the conventional six-week cycle.

Large converters hedge by operating both rotogravure for volumes above 500,000 linear m and digital for high-margin, short runs. Smaller players relying solely on mid-range flexo risk margin erosion as digital unit costs fall and customers seek personalization across the Africa flexible packaging market.

Geography Analysis

South Africa anchors regional demand with well-developed logistics, mandatory extended producer responsibility, and tax incentives that reimburse 35-55% of qualifying capital outlays. Publicly listed converters Transpaco Flexibles and CTP Flexibles upgraded lamination and printing assets in 2025, positioning themselves for higher recycled-content specifications from major retailers.

Nigeria offers scale, hosting 220 million citizens and the continent’s largest GDP, but acute currency swings and power deficits challenge cost control. Indigenous converters hedge by backward integrating into resin compounding and captive power generation, enabling them to supply sachets that dominate the personal-care and beverage categories. The Africa flexible packaging market here, therefore, couples high volume with volatile input economics.

Egypt leverages the Suez Canal Economic Zone’s 10% corporate tax rate to attract USD 200 million in UFlex investment in PET chips and aseptic cartons, scheduled for completion in fiscal 2026. The proximity to Middle Eastern demand centers allows local plants to operate export ratios above 40%, granting hard-currency buffers that counterparties in inland markets lack.

Kenya and Morocco serve as regulatory bellwethers. Kenya’s stringent bag ban expedites mono-material experimentation, while Morocco’s Euro-Mediterranean ties let converters fulfill both African and European orders without re-engineering quality systems. Their policy decisions routinely ripple across the wider Africa flexible packaging market as multinational brands harmonize designs for economies of scale.

Regulatory Landscape

Regulation across the Africa flexible packaging market is increasingly shaped by extended producer responsibility (EPR), single-use restrictions, and tighter food-contact and labeling controls. Kenya has moved from broad bans (notably its 2017 plastic carrier bag prohibition) toward more detailed plastic packaging controls, including labeling and design-for-recyclability requirements administered through national bodies such as the Kenya Bureau of Standards (KEBS) and environment authorities. South Africa continues to anchor compliance expectations through its EPR framework and food-contact oversight under the Foodstuffs, Disinfectants and Cosmetics Act 54 of 1972, with the South African Bureau of Standards (SABS) and related enforcement expectations influencing multinational packaging specifications.

Alongside this, there is a shift toward regional standards alignment to reduce technical barriers to trade under AfCFTA. The African Organisation for Standardisation (ARSO), including ARSO/TC 14 workstreams on food packaging and labeling, is developing harmonized standards that extend to topics such as recycled plastics for food-contact applications. Together, national enforcement and cross-border standardization are pushing converters toward traceability, clearer resin identification, and recycled-content declarations, particularly as design-for-recycling rules tighten in Kenya and Morocco.

Value Chain Analysis

The value chain starts with polymer and substrate inputs (PE, PP, PET, paper, and aluminum foil), then moves through resin compounding and film extrusion (blown and cast), printing (flexography, rotogravure, and digital), and conversion steps such as lamination (increasingly solventless), slitting, pouch and sachet making, and quality testing for migration and seal integrity. Brand owners and co-packers in food, personal care, and healthcare set specifications, while modern retailers and export channels require barcoding, labeling, and sustainability scorecards that force converters to manage artwork libraries and compliance documentation at scale.

Structural friction points remain concentrated in imported high-barrier and specialty films, with limited access to test labs and certification pathways. The uneven availability of post-consumer recyclate suitable for flexible formats also constrains options. As EPR and labeling enforcement expand, data capture and traceability requirements are increasing along the chain, which elevates the role of industry platforms and associations, such as South Africa-focused RPMASA, in sharing compliance guidance, recyclability protocols, and circularity coordination between converters, resin suppliers, and collectors.

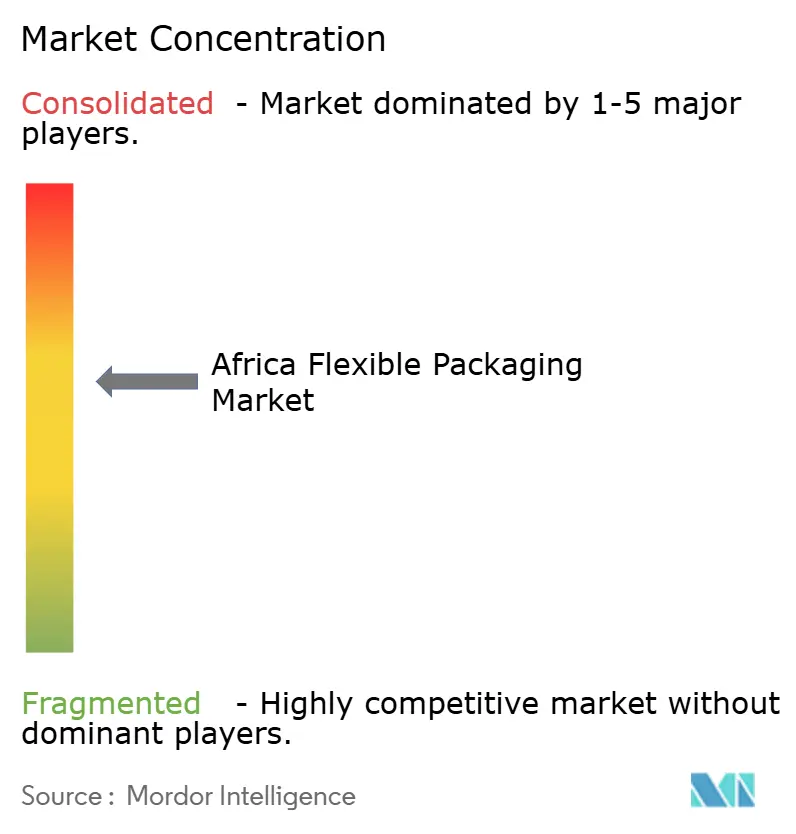

Competitive Landscape

The Africa flexible packaging market shows moderate concentration. Global majors, including Amcor, Huhtamaki, and Constantia Flexibles, dominate pharmaceutical and high-barrier niches that demand solventless lamination, in-house metallization, and stringent migration testing. Constantia’s March 2025 acquisition of Aluflexpack, which added 1,700 employees across nine sites, underscores ongoing consolidation aimed at securing geographic coverage and technical depth.

Regional champions like Sonnex Packaging Nigeria, Transpaco Flexibles, and CTP Flexibles compete through quicker order-to-delivery cycles and localized service. They leverage proximity to fast-moving consumer goods plants to offset narrower product breadth. White-space remains in bioplastics converting, digitally printed short runs, and pharmaceutical blister forming, where barriers to entry deter opportunistic entrants yet yield gross margins 15-25% above commodity film averages.

Technology adoption is the key differentiator. Plants investing in solventless lamination and water-based inks report 10-15% energy savings and faster regulatory approvals, aligning with retailer scorecards that now wield contractual penalties for non-compliance. Those persisting with solvent-based systems must budget for higher emissions levies and face mounting client attrition. This dual-track environment ensures market share migrates toward converters demonstrating both scale and sustainability credentials within the Africa flexible packaging market.

Africa Flexible Packaging Industry Leaders

Hana Packaging Limited

PrimePak Industries Nigeria Ltd

Aristocrat Industries Ltd

Huhtamaki Oyj

Constantia Flexibles Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Design-for-recycling and circular-economy compliance are creating whitespace for converters that can industrialize mono-material structures, integrate post-consumer recycled content where permitted, and document compliance for retailer and export audits. Kenya Plastics Pact activity and the issuance of more formal plastic packaging controls in 2026 provide a demand pull for standardized labeling, resin identification, and recyclability-aligned structures, especially in high-volume food and personal care formats where sachets and pouches dominate.

A second opportunity centers on capacity modernization and consolidation to serve multinational customers with consistent quality across countries. Mediterrania Capital Partners completing the acquisition of Amcor Flexibles Mohammedia in Morocco, via the holding company, points to continued investor appetite for scaled North African platforms with export adjacency. Technology upgrades that lift throughput and reduce waste, such as MFPL commissioning a 10-color BOBST rotogravure press in Tanzania, are also creating near-term operational levers for regional converters competing on cost, turnaround time, and compliance-ready packaging.

Recent Industry Developments

- April 2026: Mediterrania Capital Partners completed the acquisition of 100% of the holding company of Amcor Flexibles Mohammedia in Morocco. The transaction strengthens a scaled North African converting platform and supports consolidation in a market where multinational customers demand consistent quality and compliance across borders.

- September 2025: Modern Flexible Packaging Limited (MFPL) commissioned a 10-color BOBST NOVA RS 5003 rotogravure press in Tanzania. The installation increased printing capacity and reduced changeover waste, improving cost competitiveness for high-graphics flexible packaging used in food and FMCG applications.

- January 2024: UFlex commissioned an 18,000 t per year post-consumer recycled PET facility in Egypt. The project expanded local availability of recycled PET feedstock and supported brand-owner recycled-content programs tied to export-facing requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Africa flexible packaging market covers the value of flexible packaging materials and finished packs used for packing goods across key end uses in Africa, captured at the point of sale from converters to their customers, and expressed in USD.

Scope exclusions: This sizing excludes rigid packaging formats and also excludes the value of packaged goods (only the packaging itself is counted).

Segmentation Overview

- By Material

- Plastics

- Polyethylene (PE)

- Biaxially Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Other Plastics

- Paper

- Metal Foil

- Bioplastics and Compostable Materials

- Plastics

- By Product Type

- Bags and Pouches

- Films and Wraps

- Sachets and Stick Packs

- Other Product Types

- By End-user Industry

- Food

- Baked Goods

- Snacks

- Meat, Poultry and Seafood

- Confectionery

- Pet Food

- Other Food Products

- Beverage

- Healthcare and Pharmaceutical

- Personal Care and Cosmetics

- Agriculture and Horticulture

- Other End-User Industries

- Food

- By Printing Technology

- Flexography

- Rotogravure

- Digital Printing

- Other Printing Technologies

- By Country

- South Africa

- Nigeria

- Egypt

- Morocco

- Kenya

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundary of what should be counted as flexible packaging in Africa, and to anchor the model with practical demand and trade signals. We relied on public sources such as UN Comtrade trade statistics, World Bank macro indicators, FAO food production series, and UNIDO industrial statistics, which help explain demand cycles in packaged foods and local conversion activity.

To convert those signals into a market value view, filings and investor presentations of listed packaging and resin companies were screened for capacity notes and regional revenue commentary, and we also reviewed association publications such as packaging institute websites and plastics federation releases where available. Patent databases and an import and export shipment level database were used selectively to cross-check material shifts and flows in films, laminates, and packaging inputs. The sources listed here are illustrative only, and many other public references and documents were also used for clarification, validation, and back-checking.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate converter level demand, typical pricing movement, and the realistic pace of material substitution across the region. We spoke with a mix of packaging converters, raw material distributors, brand owner packaging teams, and logistics and procurement stakeholders across key African markets, and then the assumptions were revisited when answers did not line up with desk signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | |

| Mid tier: 51% | Functional/Unit leaders: 27% | |

| Smaller Players: 21% | Managers: 54% |

Market-Sizing & Forecasting

The model starts with a top-down build where packaging demand is reconstructed from end-use consumption signals and conversion activity, and then tied back to what is realistically supplied into Africa through local output and trade. Once the demand pool is shaped, we corroborate it with selective bottom-up approximations using sampled converter throughput, channel checks on films and laminates, and typical price bands for common formats, and then totals are adjusted only when more than one check points the same way.

Inputs that matter in this market include packaged food and beverage production trends, import and export movement of flexible packaging films and key polymers, the mix shift between mono-material films and multi-layer structures, average selling price movement by format (pouches, wraps, sachets), and capacity utilization direction in major converting hubs. For forecasting, scenario analysis was used so the range of outcomes stays tied to visible drivers such as food processing investments, inflation and FX effects on imported inputs, and regulatory pressure on packaging design. Where local country detail was thin, gaps were handled through proxy indicators like trade intensity and per-capita packaged food consumption, and the assumptions were then pressure-tested in interviews.

Data Validation & Update Cycle

Validation happens in several passes, starting with cross-checks between the model output and independent signals such as trade volumes, converter capacity announcements, and end-use output trends, which helps flag unrealistic jumps. We also run variance checks on pricing and volumes by format so that the total value does not get distorted by a single assumption.

Before sign-off, another analyst reviews the logic, the arithmetic, and the key assumptions, and follow-up calls are triggered when a major data point sits outside the expected range. Reports are refreshed annually, and interim updates are made when material events occur that can change demand or pricing. Right before delivery, we do a final pass so the published view reflects the latest available information.

Mordor Intelligence's Africa Flexible Packaging Market Sizing Compared With Other Published Estimates

Published market values for Africa flexible packaging do not always match, and the differences are usually not random. They often come from how each publisher draws the boundary between Africa-only versus wider regions, what gets counted as flexible packaging versus adjacent packaging types, and how pricing is converted into USD in high inflation environments.

Trade flow checks for films and laminates, along with converter capacity signals and end-use packaging intensity, are the evidence that keeps Mordor Intelligence's 2026 estimate tied to Africa-only consumption rather than broader Middle East and Africa totals. When those checks are not used, it becomes easier to blend in non-African demand, fold in wider packaging scopes, or apply aggressive price escalation, which pushes figures away from a repeatable demand pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.43 B (2026) | |

| Trade Journal A | USD 12.90 B (2025) | Uses a Middle East and Africa framing in the cited study, so the figure can blend non-African demand and may not keep the Africa-only boundary consistent with country-level consumption signals. |

| Regional Consultancy B | USD 12.80 B (2026) | Covers Middle East and Africa as one region and applies a broad flexible packaging scope across multiple applications, which can inflate the total if Africa-only volumes, format mix, and USD conversion timing are not isolated. |

The spread in the table is mainly explained by geography coverage and scope alignment, since MEA totals are materially larger than Africa-only totals even before pricing choices are applied. By keeping demand signals, pricing logic, and validation checks traceable to the same Africa boundary, the final figure stays easier to reproduce and to update when trade, capacity, or end-use conditions change.

Key Questions Answered in the Report

How large is the Africa flexible packaging market in 2026?

The Africa flexible packaging market size is USD 2.43 billion in 2026, with a 5.45% CAGR projected through 2031.

Which material segment is growing fastest?

Bioplastics and compostable materials show the quickest momentum, rising at a 6.77% CAGR through 2031.

Why are sachets important for brand owners in Africa?

Sachets priced between USD 0.05 and USD 0.20 enable affordable unit doses that match low daily spending levels, boosting trial and repeat purchase frequencies.

How is legislation shaping packaging design in Africa?

Bans on certain plastics, extended producer responsibility fees, and mono-material recycling mandates push converters toward polyethylene-based structures and certified compostables.

What competitive strategies help converters thrive?

Success hinges on solventless lamination, water-based inks, digital printing for short runs, and factory proximity to both modern retail hubs and export corridors.

Which countries set the tone for sustainability mandates?

Kenya and Morocco often introduce the continent’s first recycling or material-restriction rules, prompting brand owners to standardize compliant formats across the entire region.

Page last updated on: