Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 49.03 Billion |

| Market Size (2026) | USD 50.77 Billion |

| Market Size (2031) | USD 60.44 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

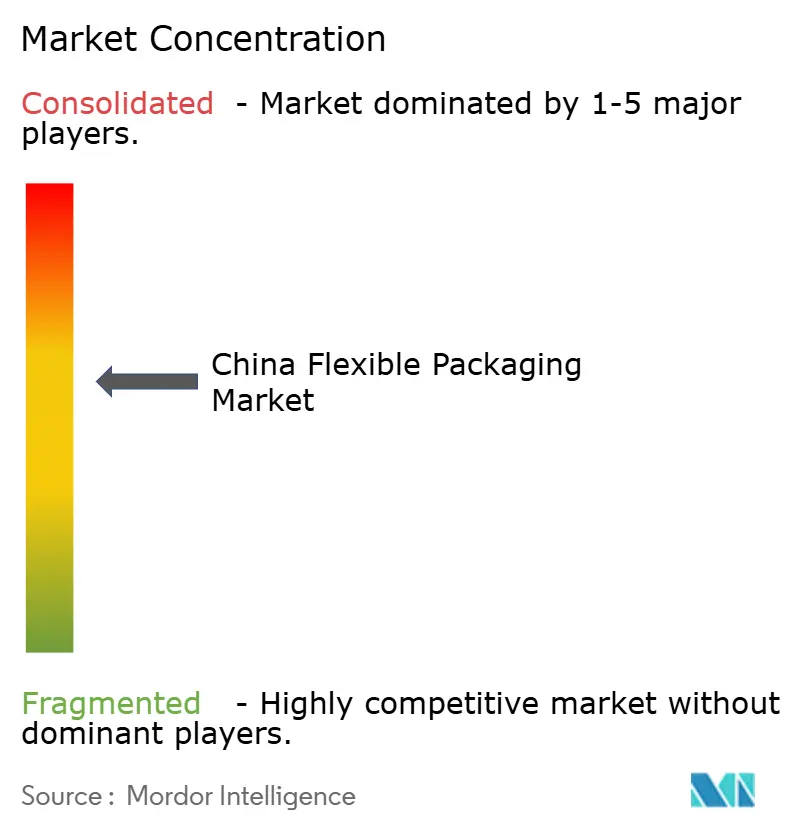

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Flexible Packaging Market Analysis by Mordor Intelligence

China flexible packaging market size in 2026 is estimated at USD 50.77 billion, growing from 2025 value of USD 49.03 billion with 2031 projections showing USD 60.44 billion, growing at 3.55% CAGR over 2026-2031. Steady growth is underpinned by sustained e-commerce expansion, wider cold-chain coverage, and rising regulatory scrutiny that is steering converters toward mono-material films and certified recycled content. Logistics platforms now specify puncture-resistant mailers, retailers are phasing out non-recyclable laminates, and personal-care brands demand short-run graphic customization, all of which funnel incremental value toward converters with advanced extrusion and digital-printing assets. Petrochemical oversupply keeps resin prices volatile, compressing margins for commodity formats, yet it simultaneously frees capital for firms willing to reposition around premium, high-barrier structures. Competitive intensity is sharpening as multinational incumbents defend share against agile domestic rivals that can match print quality while quoting faster lead times, especially for pilot SKUs targeting tier-2 and tier-3 cities. Overall, the China flexible packaging market is at a strategic crossroads where sustainability mandates are no longer optional and speed-to-market has become a decisive differentiator.

Key Report Takeaways

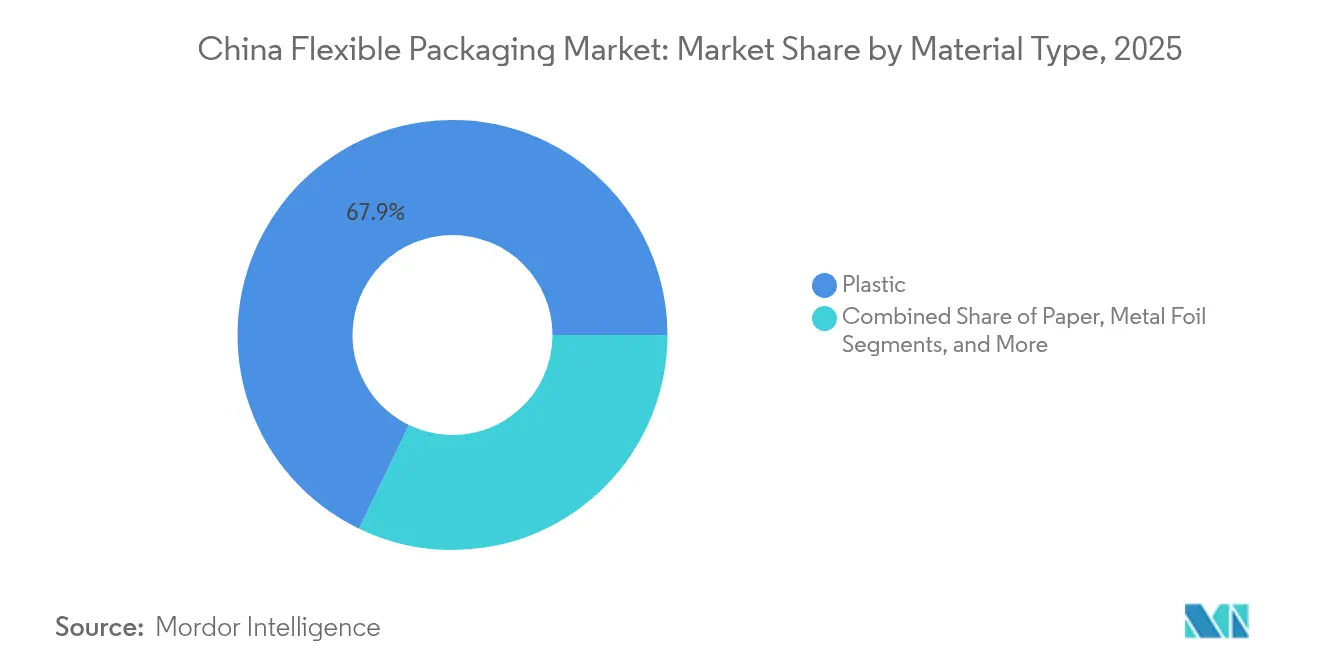

- By material type, plastic materials held 67.85% of China flexible packaging market share in 2025, while bioplastics are forecast to expand at a 5.32% CAGR through 2031.

- By product type, bags and pouches accounted for 47.10% of revenue in 2025, whereas sachets and stick packs are projected to grow at a 4.52% CAGR to 2031.

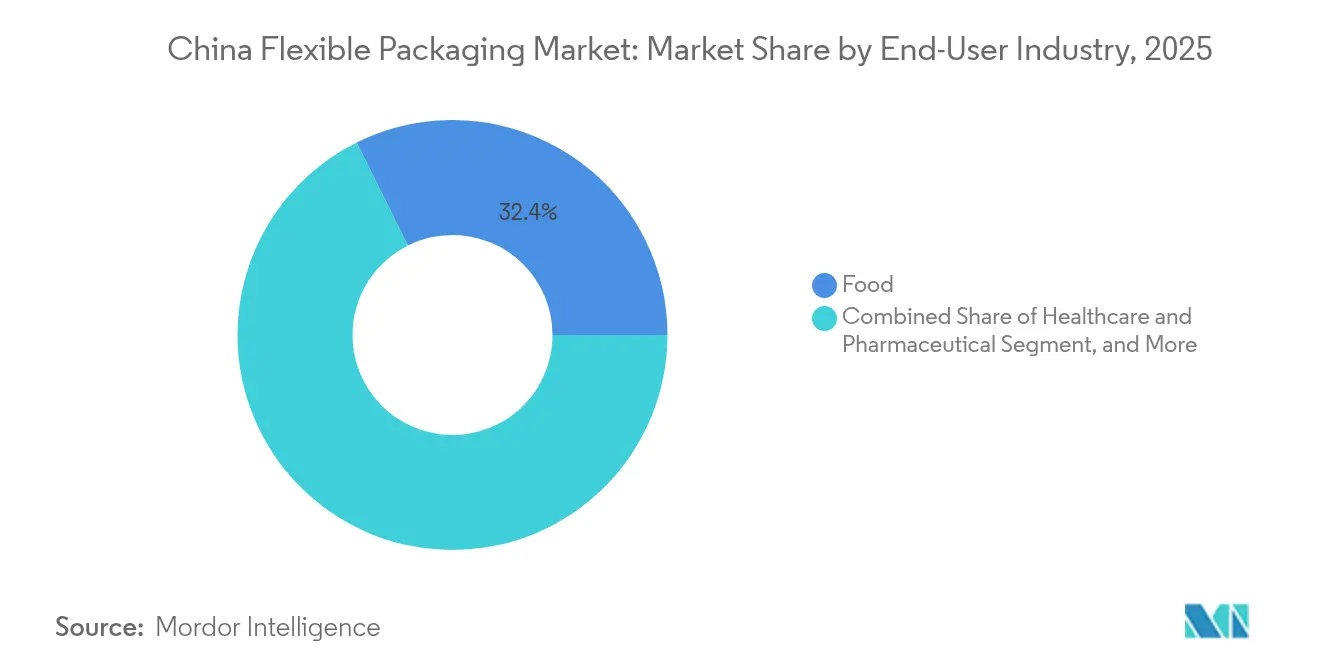

- By end-user industry, food dominated with a 32.35% share in 2025, yet personal care and cosmetics are advancing at a 5.45% CAGR to 2031.

- By printing technology, flexography commanded 45.20% of 2025 revenue, while digital printing is poised for a 5.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for E-Commerce Ready Packaging | +0.8% | National, concentrated in tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Government Push for Green Manufacturing | +0.6% | Coastal provinces (Jiangsu, Zhejiang, Guangdong) | Medium term (2-4 years) |

| Cold-Chain Logistics Expansion | +0.7% | Tier-2 and tier-3 cities nationwide | Short term (≤ 2 years) |

| Domestic FMCG Brands Seeking Differentiation | +0.5% | Tier-1 cities | Medium term (2-4 years) |

| High-Barrier Monomaterial Film Innovation | +0.4% | Yangtze River Delta, Pearl River Delta | Long term (≥ 4 years) |

| Private-Equity Capital Inflow | +0.3% | Jiangsu, Zhejiang, Shandong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for E-Commerce Ready Packaging

E-commerce logistics generated CNY 6.4 trillion (USD 0.91 trillion) in the first three quarters of 2024, up 4.2% year-on-year, prompting platforms to mandate mailers that survive conveyor handling and doorstep drop-offs without tearing. Converters have responded with co-extruded polyethylene-polyamide films that boost puncture resistance yet preserve heat-seal speed, enabling fulfillment centers to process an extra 8–10 parcels per minute. Freight operators favor flexible mailers because a unit weighs 40–50% less than a similar-sized corrugated box, cutting both carbon output and surcharges tied to dimensional weight. Brands add QR-code traceability and holographic seals, which elevate tooling costs beyond the reach of small converters lacking digital presses. The result is a bifurcated China flexible packaging market where premium e-commerce formats command 15–20% pricing power while commodity pillow packs chase volume. Large converters installing nanographic presses create an insurmountable moat around short-run orders, tightening the supply chain for last-mile durable mailers.

Government Push for Green Manufacturing in Packaging

The State Council’s 2024 Extended Producer Responsibility rules make brand owners financially accountable for post-consumer collection, accelerating demand for mono-polyethylene and polypropylene films that pass curbside recyclability tests.[1]State Council of China, “Extended Producer Responsibility Guidelines 2024,” www.gov.cn Coastal provinces with earlier enforcement clocks are auditing converter lines quarterly, and fines for non-compliant laminate structures rose 35% in 2024 over 2023. Brand procurement teams now score suppliers on recycled-content disclosure, nudging tier-1 converters to publish life-cycle inventory data and pursue ISO 14001 certifications. Smaller inland players face capital-expenditure barriers as each line retrofit costs USD 2–4 million, forcing them to cede multinational accounts or accept price erosion. Post-consumer resin suppliers have begun issuing food-contact compliant grades, giving early adopters a 3–4 percentage-point margin lift. Over the medium term, the new rules entrench a sustainability premium inside the China flexible packaging market while sidelining firms that continue to rely on mixed-material laminates.

Proliferation of Cold-Chain Logistics for Fresh Food Delivery

Rapid urbanization and higher disposable income push fresh seafood, meat, and dairy subscriptions that need films functioning from −18 °C to +4 °C without condensation failure. Platforms such as Meituan and Ele.me enlarged refrigerated-warehouse space 22% in 2024, adding demand for high-barrier mono-polyethylene pouches that match EVOH performance but remain mechanically recyclable. Nano-clay additives lower oxygen-transmission rates below 5 cm³/m²/day, a threshold once attainable only with metallized layers. Brands in tier-2 hubs trial tamper-evident, resealable designs that keep integrity during two freeze–thaw cycles, extending shelf life and allowing cross-regional shipping. Converters with peel-seal expertise secure contracts at 10–12% price premiums. The cold-chain build-out also widens geographic coverage of the China flexible packaging market, shifting order volumes from coastal mega-cities toward inland city clusters where cold storage was previously scarce.

Growth of Domestic FMCG Brands Requiring Differentiated Packs

Home-grown brands such as Tingyi, Uni-President, and Want Want use Instagram-ready packs to stand out, spurring adoption of matte finishes, holographic foils, and thermochromic inks that demand exacting presswork. A matte-finish stand-up pouch helped Tingyi raise retail price points 12–15% versus legacy pillow packs without a sales slowdown. Digital presses like HP Indigo narrow-web units supply serialized SKUs for regional promotions, shrinking time-to-shelf from six weeks to two. Converters able to print variable data in a single pass capture micro-segments from KOL-driven livestream sales that spike volumes unpredictably. The shift toward shorter runs reinforces digital’s ascendancy inside the China flexible packaging market, as flexographic setups fight declining average order sizes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-Use Plastics Ban Roadmap | −0.5% | Coastal provinces (Jiangsu, Zhejiang, Guangdong, Fujian) | Medium term (2-4 years) |

| Volatile Petrochemical Feedstock Prices | −0.4% | Petrochemical clusters in Shandong, Jiangsu, Zhejiang | Short term (≤ 2 years) |

| Recycling Infrastructure Gaps in Inland Cities | −0.3% | Tier-3 and tier-4 cities in Henan, Anhui, Hunan, Sichuan | Long term (≥ 4 years) |

| Rigid Sustainable Alternatives | −0.2% | Beverage and personal-care segments nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Single-Use Plastics Ban Roadmap

Provincial regulators scheduled phase-outs of non-recyclable multilayer films by 2026, demanding 85% recovery rates for flexible formats.[2]Ministry of Ecology and Environment, “Plastic Waste Management Guidelines 2024,” mee.gov.cn Lines that still laminate polyethylene with polyamide risk de-listing from supermarket shelves in Jiangsu and Zhejiang. Retooling a seven-layer extrusion line costs USD 2–4 million, weighing on firms with thin cash cushions. Some converters migrate production inland to skirt audits, but brand owners increasingly insist on site visits and ISO-14001 certificates, closing the loophole. The policy gap between coastal and inland regions fragments the China flexible packaging market, with advanced players nudging ahead while late adopters watch margin erosion.

Volatile Petrochemical Feedstock Prices

China added 18.7 million tpa of polypropylene and polyethylene capacity between 2024 and 2026, flipping into a net exporter and driving price swings that stretch converter working capital. Spot prices whipsawed by 3–5% within weeks in 2024, undermining fixed-price contracts. Large converters leverage multi-year supply frame agreements with Sinopec to secure a 3–5% cost edge, yet mid-tier firms struggle to hedge. Feedstock gyrations shift procurement teams to weekly quoting, clogging project pipelines and delaying innovation investment across the China flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bioplastics Scale While Plastics Remain Dominant

Plastic still owns 67.85% of China flexible packaging market share in 2025, propelled by polyethylene’s balance of seal strength and cost efficiency. Bioplastics, though comparatively small, are pacing at a 5.32% CAGR because consumer goods companies must hit 30% renewable-content pledges by 2028. The China flexible packaging market size for bioplastics in personal care is projected to rise sharply as brand owners willingly absorb the 20-30% cost premium. Polyethylene holds sway in staple food pouches and e-commerce mailers, aided by expansion of post-consumer resin grades that cut virgin usage without sacrificing machinability. Polypropylene’s clarity secures beverage overwraps, while polyethylene-terephthalate and polyamide appear in barrier-critical lines such as seafood packs. Over the forecast horizon, resin demand bifurcates between low-cost commodity films and high-barrier, mono-material solutions that satisfy recycling audits.

Bioplastics adoption centers on tier-1 cosmetic aisles, where polylactic-acid sachets convey clean-label cues. Moisture sensitivity challenges are gradually mitigated by multi-layer PLA-coated papers that withstand high-humidity logistics. Converters experimenting with starch-blend films bank on premium margin upside even at slower line speeds. Metal-foil laminates retreat to pharmaceutical niches as oxygen-barrier monomaterial designs mature. Taken together, material dynamics underscore how sustainability triggers value shifts inside the China flexible packaging market, spurring converters to recalibrate asset footprints toward recyclable or renewable substrates.

By Product Type: Sachets Surge as Bags Retain Scale

Bags and pouches delivered 47.10% of 2025 revenue, reflecting entrenched usage across snacks, frozen meat, and pet food. Sachets and stick packs, however, clock the fastest 4.52% CAGR as households gravitate toward single-serve convenience, especially in lower-tier cities. China flexible packaging market size for sachets in electrolyte powder alone is forecast to double by 2031 on the back of gym culture and direct-to-consumer beverage sachets. Stand-up pouches remain king where reclosing, spouts, or zippers extend product life once opened, but portion packs thrive on impulse buys and e-commerce sample bundles.

Digital printing fuels sachet customization, letting brands test micro-SKUs without cylinder cost, while Landa’s S10P platform pushes variable data at near flexographic speeds. Films and wraps face slowing growth as integrated e-commerce fulfilment reduces secondary overwrap needs. Labels and shrink sleeves gain in premium beverages, aided by tactile lacquers and anti-counterfeit inks. Overall, product-mix evolution reinforces the China flexible packaging market’s shift toward lightweight, portion-aligned formats that fit modern lifestyles.

By End-User Industry: Personal Care Gains Momentum Over Food Volume

Food held a commanding 32.35% revenue slice in 2025 thanks to daily consumption and diverse pouch formats. Yet personal care and cosmetics are projected to outstrip food with a 5.45% CAGR because domestic beauty startups weaponize packaging as a branding canvas. China flexible packaging industry players report order books tilting toward shampoo pouches, facial-mask sachets, and body-lotion tubes that feature metallic accents and soft-touch varnish. Within food, frozen snacks and ready-to-eat meals enjoy barrier-film upgrades that curb freezer burn, while dairy brands test spouted pouches for on-the-go yogurt.

Healthcare applications deliver steady demand for child-resistant closures that meet National Medical Products Administration standards, securing long-term contracts for converters proficient in multi-layer blister webs. Agricultural seed pouches rely on UV-stable films as rural mechanization expands. The duality of high-volume food versus high-margin personal care shapes capacity allocation across the China flexible packaging market, with converters hedging between volume stability and premium upside.

By Printing Technology: Digital Ascends While Flexography Holds the Base

Flexography still captures 45.20% of 2025 revenue, valued for its speed and low ink cost per impression. Yet digital presses post a 5.70% CAGR, driven by brand fascination with personalized sleeves and serialized QR codes linking to loyalty apps. The China flexible packaging market size for digital output is forecast to triple by 2031 as run lengths shrink and SKU counts escalate. Rotogravure preserves its niche in photo-grade confectionery foils where color fidelity trumps plate cost, but setup lead times lag fast-fashion launch schedules.

Converters embrace a hybrid floor plan, dedicating flexo to long runs while reserving digital lines for micro-batch drops. This dual gear strategy demands capital depth yet pays off with 15-20% price premiums on variable-data jobs. Regulatory pressure on solvent emissions nudges flexo presses toward water-based inks, further raising conversion costs. Digital platforms, by contrast, satisfy both speed and sustainability checklists, amplifying their pull across the China flexible packaging market.

Geography Analysis

Coastal strongholds in the Yangtze River Delta generate roughly 35-40% of national converter capacity, benefiting from feedstock proximity, port access, and front-line compliance expertise. The Pearl River Delta adds another 25-30%, specializing in high-barrier electronics wraps and pharma sachets, sectors that reward defect-free coating lines. Inland provinces such as Shandong and Sichuan scale plants to serve regional FMCG brands yet wrestle with recycling shortfalls that delay post-consumer resin uptake.

Tier-1 cities Beijing, Shanghai, Guangzhou, Shenzhen set the premium tone for differentiated packs, with e-commerce penetration surpassing 70%. Tier-2 hubs like Hangzhou and Chengdu see the fastest cold-chain build-out, translating into mono-PE pouches outfitted for low-temperature logistics. Lower-tier cities lag 15-20 percentage points behind national waste-collection targets, constraining closed-loop film streams and elevating virgin-resin reliance. Geographic disparities thus produce a two-speed China flexible packaging market, in which coastal clusters chase compliance premiums while inland zones compete primarily on unit cost.

Competitive Landscape

Multinationals Amcor, Mondi, Sealed Air, Tetra Pak retain high-barrier niches in pharma and aseptic dairy, leveraging global GMP certifications to secure multinational accounts. Domestic leaders such as Southern Packaging Group, Zhejiang Chengde, and Jiangsu Caihua counter with faster cycle times and region-specific design support, narrowing perceived quality gaps. Amcor’s April 2025 investment to add rotogravure and digital lines targets premium healthcare and personal-care packs where technical compliance justifies higher margins.[3]Amcor Plc, “China Expansion Announcement 2025,” amcor.com Conversely, Huhtamaki shuttered two plants in 2024, signaling an exit from commodity laminate formats to focus on molded fiber.

Jingfeng’s grab of Greatview expands retort-pouch reach, and Jiangsu Caihua’s stake in a digital-print specialist shores up short-run capability. Technology remains the battlefield; converters deploying machine-vision inspection have trimmed scrap by 12–15%, enhancing bids on high-volume snack packs. Going forward, hybrid print lines, monomaterial barrier films, and recycled-content verification will separate winners from laggards in the China flexible packaging market.

China Flexible Packaging Industry Leaders

Amcor Plc

Mondi Plc

Sealed Air Corporation

Huhtamaki Oyj

Tetra Pak International SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor Plc announced an investment to expand rotogravure and digital capacity in Jiangsu, targeting pharmaceutical and personal-care packs.

- March 2025: Tetra Pak opened an aseptic-carton line in Hohhot with 8 billion-unit annual capacity.

- February 2025: Mondi introduced a recyclable mono-polyethylene pet-food pouch with oxygen-barrier coating.

- January 2025: Sealed Air partnered with a Jiangsu converter to pilot AI-driven seal-inspection, cutting waste 12–15%.

China Flexible Packaging Market Report Scope

The China Flexible Packaging Market study examines the country’s growing demand for lightweight, durable, and cost-efficient packaging formats across major consumer and industrial applications. As flexible packaging gains traction due to rising food safety needs, convenience trends, and advancements in material innovation, the study evaluates key growth drivers and the market’s shift toward sustainable and high-performance solutions.

The China Flexible Packaging Market Report is Segmented by Material Type (Plastic, Paper, Metal Foil, Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, Sachets and Stick Packs, Labels and Sleeves), End-User Industry (Food, Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, Agriculture and Horticulture), Printing Technology (Flexography, Rotogravure, Digital Printing). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyamide (PA) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

By End-User Industry

| Food | Meat, Poultry and Seafood |

| Confectionery and Bakery | |

| Dairy Products | |

| Snacks | |

| Frozen Food | |

| Other Food Products | |

| Beverage | Alcoholic |

| Non-Alcoholic | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material Type | Plastic | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyamide (PA) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| By End-User Industry | Food | Meat, Poultry and Seafood |

| Confectionery and Bakery | ||

| Dairy Products | ||

| Snacks | ||

| Frozen Food | ||

| Other Food Products | ||

| Beverage | Alcoholic | |

| Non-Alcoholic | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-Use Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

How large is the China flexible packaging market in 2026?

The market is valued at USD 50.77 billion in 2026.

What is the expected growth rate for Chinas flexible packs to 2031?

Revenue is projected to rise at a 3.55% CAGR to USD 60.44 billion by 2031.

Which material segment in Chinese flexible packs is growing the fastest?

Bioplastics and compostable materials are expanding at a 5.32% CAGR through 2031.

Why are sachets gaining popularity in China?

Single-serve convenience, e-commerce sampling, and lower-tier city demand push sachet volumes at a 4.52% CAGR.

How is regulation influencing packaging choices?

Extended Producer Responsibility mandates and provincial plastics bans shift demand toward recyclable mono-material films and higher recycled content.

Which printing technology is set for the strongest growth?

Digital printing is forecast to grow 5.70% annually because it supports short-run, personalized packaging needs.

Page last updated on: