Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

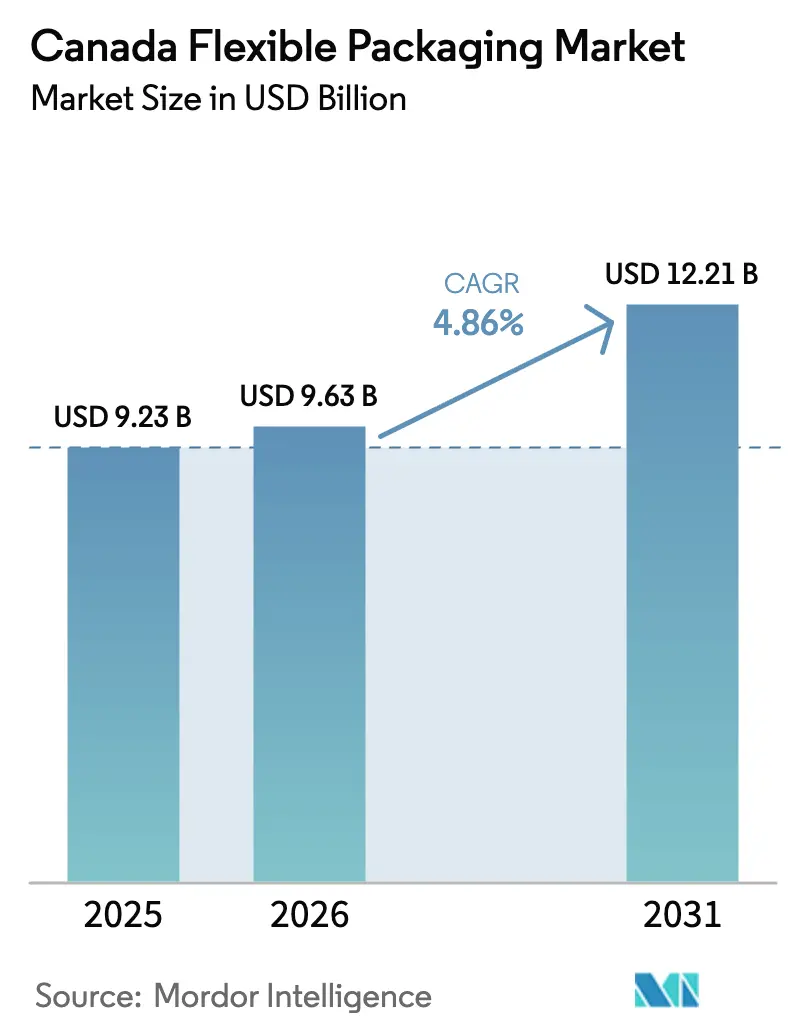

| Base Year Market Size (2025) | USD 9.23 Billion |

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 12.21 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

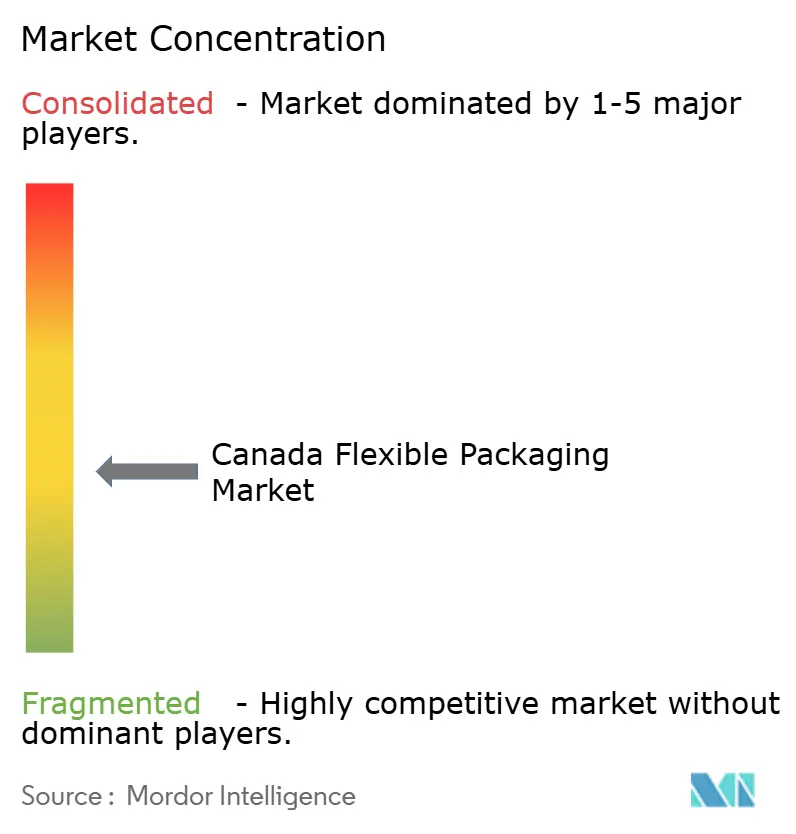

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Flexible Packaging Market Analysis by Mordor Intelligence

The Canada flexible packaging market size reached USD 9.63 billion in 2026 and is forecast to climb to USD 12.21 billion by 2031, reflecting a 4.86% CAGR over the period. This growth occurs despite margin compression, as converters switch from multi-layer laminates to mono-material films to meet new provincial extended producer responsibility (EPR) mandates. Retail private-label brands with circularity targets, booming agri-food exports that favor high-barrier pouches, and the rapid pivot to digital printing are expanding opportunity sets even as resin-price volatility and import competition weigh on profitability. Consolidation among multinational converters, alongside niche gains for digital-printing specialists, is reshaping how scale, access to recycled content, and automation capabilities translate into contract wins across food, personal care, and e-commerce channels.

Key Report Takeaways

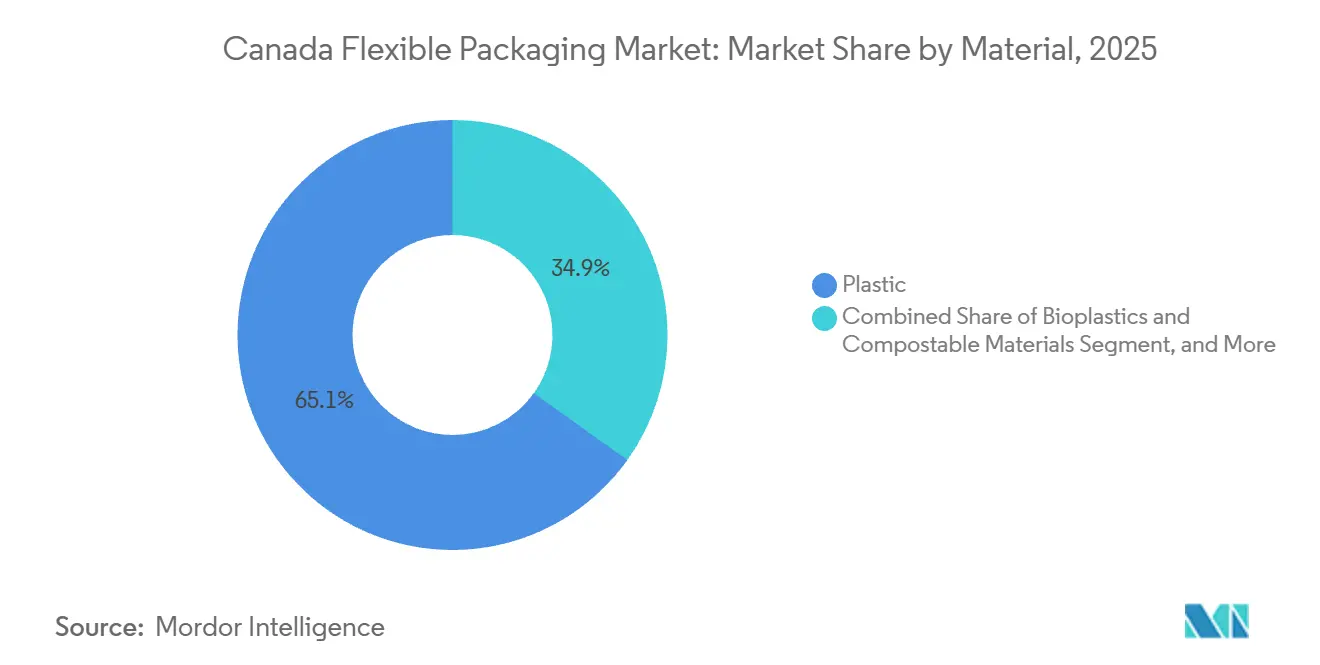

- By material, plastics held 65.12% of Canada flexible packaging market share in 2025, while bioplastics and compostables are projected to expand at a 5.77% CAGR through 2031.

- By product type, bags and pouches led with 46.63% revenue share in 2025; sachets and stick packs are forecast to grow at a 6.23% CAGR to 2031.

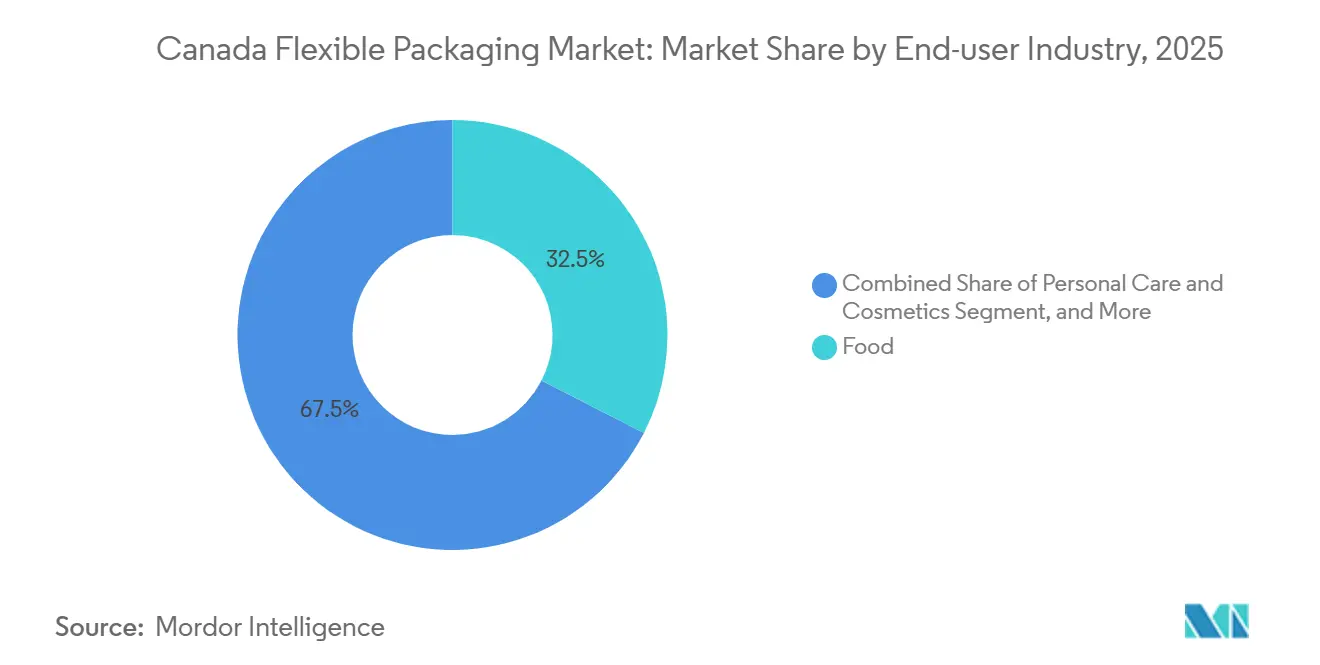

- By end-user industry, food accounted for 32.53% share of Canada flexible packaging market size in 2025, and personal care and cosmetics are advancing at a 5.87% CAGR through 2031.

- By printing technology, flexography commanded 44.72% of Canada flexible packaging market share in 2025, whereas digital printing is projected to expand at a 6.01% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenience and Portion-Control Packaging | +0.9% | National, urban concentration in Toronto, Montreal, Vancouver | Medium term (2-4 years) |

| E-Commerce Growth Accelerating Protective Mailer Adoption | +1.1% | National, strongest in Ontario and British Columbia | Short term (≤ 2 years) |

| Provincial Extended-Producer-Responsibility Rollouts | +1.3% | Ontario, Quebec, British Columbia, Alberta, Atlantic spillover | Long term (≥ 4 years) |

| Converter Investments in Mono-Material Recyclable Films | +0.8% | National, led by Ontario and Quebec clusters | Medium term (2-4 years) |

| Agri-Food Exports Requiring High-Barrier Pouch Solutions | +0.7% | Prairie provinces and Quebec export hubs | Long term (≥ 4 years) |

| Retail Private-Label Premiumization Driving Short-Run Digital Print | +0.6% | National, strongest in major retail markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenience and Portion-Control Packaging

Urban consumers favor single-serve formats that fit busy lifestyles and limit food waste. Between 2018 and 2023, nearly half of new Canadian packaged-food launches arrived in flexible stand-up pouches or sachets, with sauces and snacks leading the count.[1]Agriculture and Agri-Food Canada, “Mintel Global New Products Database Analysis,” agriculture.canada.caSubscription meal-kit providers rely on pre-portioned sachets, and online grocery sales for dairy, snacks, and staple foods posted double-digit annual gains. Converters have answered with vertical form-fill-seal lines offering rapid size changeovers, while premium organic brands adopt bioplastic sachets whose higher material cost is offset by tiny gram-weights. The result is sustained volume growth for lightweight pouches that align with freight savings and consumer convenience.

E-Commerce Growth Accelerating Protective Mailer Adoption

Rising parcel volumes for cross-border trade fuel demand for coextruded polyethylene mailers that cushion goods yet satisfy recyclability labeling. Loblaw and Metro now stipulate that suppliers ship in mailers bearing How2Recycle marks and at least 30% post-consumer recycled polyethylene. Integrated players with captive recycled-resin plants secure those contracts, whereas small converters lacking feedstock access fight on price. The trend has lifted mailer volumes ahead of corrugate, shrinking dimensional weight fees for retailers and creating a durable growth runway for specialty flexible films.

Provincial Extended-Producer-Responsibility Rollouts

Ontario and Quebec already pass full recycling costs to producers, British Columbia’s system is entrenched, and Alberta launched its EPR scheme in 2025, albeit with freezer-bag and cling-film exemptions. Converters serving restrictive provinces rush to design mono-material polyolefin structures that pass sortation tests, while those focused on industrial clients in Alberta continue to use multi-layer laminates. The federal Plastics Registry adds transparency, obliging companies to publish polymer masses and recyclability status, exposing any exaggeration of circularity claims. Early movers with robust data and mono-material lines win retailer preference and shield themselves from escalating EPR fees.

Converter Investments in Mono-Material Recyclable Films

CelluForce’s cellulose-nanocrystal barrier, Amcor’s integration of 218,000 t of post-consumer resin, and Winpak’s recycled-polyethylene supply pact exemplify capex aimed at recyclability. New coextrusion lines, often costing USD 11 million or more, allow converters to laminate barrier coatings onto polyethylene without compromising recyclability streams. These investments raise barriers to entry, accelerate industry consolidation, and shorten payback periods through premium EPR-compliant contracts with national grocery chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Virgin Resin Prices Linked to Crude-Oil Swings | -0.7% | National, acute in Alberta and Saskatchewan | Short term (≤ 2 years) |

| Patchy Film-Recycling Infrastructure Outside Ontario and Quebec | -0.5% | Atlantic and Prairie provinces (ex-Alberta EPR zones), Northern territories | Long term (≥ 4 years) |

| Import Competition from Low-Cost United States and Asian Converters | -0.4% | National, sharpest in commodity films | Medium term (2-4 years) |

| Rising Cost of Sustainability-Compliant Inks and Adhesives | -0.3% | National, food and pharma converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Resin Prices Linked to Crude-Oil Swings

Western Canadian Select crude’s 2025 price slide did not translate into parallel resin savings, as polyethylene and polypropylene producers curtailed output to defend margins.[2]Natural Resources Canada, “Crude Oil Prices,” natural-resources.canada.caConverters locked into fixed-price packaging contracts saw spreads erode when resin prices spiked, then missed out on benefits when crude prices dipped. Aluminum’s 29.9% year-over-year price jump in 2024 compounded costs for metallized coffee and pharma films. To mitigate, converters renegotiate quarterly price escalators, raise recycled-content ratios to hedge volatility, and shorten customer contract tenors.

Patchy Film-Recycling Infrastructure Outside Ontario and Quebec

Ontario and Quebec fund optical sorters capable of isolating flexible polyethylene, but most Atlantic and Prairie municipalities still landfill films. With only 4% of national flexible packaging recycled, designers must assume their packs will traverse regions lacking sortation, forcing down-spec barrier performance to mono-material polyethylene.[3]PRFLEX, “Flexible Plastics Recycling Rate Analysis,” prflex.caThe limited bale volumes that do arise rarely meet minimum loads for mechanical or chemical recycling, depressing bale prices and slowing further infrastructure investment. Until nationwide collection harmonization occurs, converters face higher design constraints and sustained variability in EPR fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyolefins Anchor Volume as Bioplastics Gain Traction

Polyethylene and polypropylene underpinned 65.12% of Canada flexible packaging market share in 2025, serving bread bags, snack pouches, and high-barrier retort structures. CelluForce’s cellulose-nanocrystal coating now enables mono-material polyolefin films to achieve oxygen-barrier levels previously attainable only with aluminum-oxide PET, thereby preserving recycling compatibility. Bioplastics, although niche, are forecast to outpace the Canada flexible packaging market at a 5.77% CAGR as retailers pilot cellulose-acetate wraps for produce to meet a 95% reduction target in single-use fresh-produce packaging. Paper laminates attract dry-goods brands seeking visible sustainability cues, while foil retains a foothold in blister and aseptic packs where an absolute barrier is non-negotiable despite aluminum cost spikes.

The Canada flexible packaging market size for “other plastics,” including polyamide and ethylene-vinyl-alcohol, grows modestly in export-oriented meat and cheese packs demanding sub-1 cc/m²/day oxygen transmission. Still, resin price volatility leads processors to down-gauge these layers or replace them with EVOH-free designs when shelf-life tolerance permits. As EPR fees climb, every gram of non-recyclable barrier invites cost, intensifying the shift toward recyclability-by-design architectures.

By Product Type: Sachets and Stick Packs Accelerate Portion-Control Shift

Bags and pouches dominated 46.63% of Canada flexible packaging market size in 2025, led by stand-up formats featuring press-to-close zippers and slider tracks for snacks, pet food, and frozen produce. The segment’s growth now pivots to sachets and stick packs, rising 6.23% annually as personal-care brands launch single-dose serums and meal-kit players pre-portion sauces. Canada flexible packaging market share captured by these micro-formats benefits from digital press economics that allow vivid graphics on runs as small as a few thousand units without plate costs.

Films and wraps remain indispensable for bakery flow-wrap, produce stretch film, and multi-pack shrink bundles. Modified-atmosphere lidding films for protein trays record mid-single-digit growth, driven by grocers demanding case-ready meats with extended shelf life. Specialty formats such as wicketed bags thrive in high-throughput bakeries where auto-loading offsets labor shortages, further entrenching automation-friendly designs across product lines.

By End-User Industry: Personal Care Outpaces Mature Food Segment

Food applications represented 32.53% of Canada flexible packaging market share in 2025, buoyed by CAD 59.8 billion in processed-food exports that rely on retort, vacuum-skin, and ambient-shelf-life pouches suited for United States and Asian buyers. Meat packing alone accounted for one-quarter of processing sales, sustaining demand for high-barrier films that manage oxygen ingress across long distribution chains. Pet food claims outsized attention, as resealable matte-finish pouches reinforce premium cues for grain-free kibble brands.

Personal care and cosmetics lines, although smaller, post the fastest 5.87% CAGR to 2031, pivoting from rigid jars to lightweight stand-up pouches and sample sachets that travel efficiently in e-commerce parcels. Healthcare and pharma rely on sterile-barrier rollstock for surgical kits and unit-dose pills, expanding in step with Canada’s aging population. Beverage bag-in-box gains traction in wine and juice, trading glass breakage for lower carbon footprints, while agricultural pouches protect seed and fertilizer inputs critical to Prairie growers.

By Printing Technology: Digital Presses Unlock Agile Supply Chains

Flexography retained 44.72% of Canada flexible packaging market share in 2025 as long-run bread and snack film kept eight-color central-impression presses well loaded. Rotogravure serves ultra-high-volume confections and cigarette wraps but loses share when brands prefer SKU proliferation over marathon runs. Digital printing, led by HP Indigo and similar platforms, advances 6.01% annually on private-label momentum. The ability to print serialized QR codes, regional artwork, and seasonal flavors without plates makes digital printing an ideal match for brands that refresh their packaging every few weeks. Canada flexible packaging market size tied to digital remains modest today, yet brand owners cite sub-15-day lead times as a compelling hedge against volatile demand patterns.

Hybrid workflows emerge as converters integrate digital imprint stations inline with flexo units, marrying variable data with cost-efficient process colors. Early adopters win grocery own-brand tenders that treat rapid artwork changes and lower inventory obsolescence as procurement priorities, signaling longer-term erosion of analog share.

Geography Analysis

Ontario and Quebec anchor the Canada flexible packaging market, combining dense populations with clustered food-processing plants and well-funded EPR frameworks. Their optical-sorter networks reward mono-material converters by closing recycling loops and lowering per-unit EPR fees. British Columbia mirrors this structure on a smaller scale, though mountainous terrain inflates collection costs. Alberta’s 2025 EPR launch introduced exemptions for freezer bags and cling film, allowing industrial packs to avoid fees and encouraging converters to focus on multi-layer laminates for oil and chemical clients.

Prairie provinces host export-oriented meat, canola, and pulse processors, driving demand for oxygen-barrier pouches suited to Asia-bound shipments. Manitoba’s Winpak hub expands modified-atmosphere capacity to meet protein processor contracts, leveraging proximity to U.S. Midwest logistics corridors. Atlantic provinces lag in film-sortation investment, resulting in flexible recycling rates that fall below the national 4% average and forcing brands to assume landfill endpoints when selling into those markets.

Currency and trade add complexity. The Canadian dollar’s 2025 slide to USD 0.6964 boosts converter export pricing power but inflates costs of U.S.-dollar-denominated specialty resins and inks. June 2025 trade data showed a 19.4% drop in chemical and plastic exports, highlighting import substitution pressure even as consumer-goods imports rose 2.2%. Regionally tailored supply chains thus replace former national distribution models, Ontario-centric converters invest in mono-material lines, while Western facilities continue multi-layer production targeting performance-driven sectors exempt from stringent EPR fees.

Competitive Landscape

Four landmark deals in 2025 rewrote the rules of competition. ProAmpac’s USD 1.51 billion buyout of TC Transcontinental Packaging deepened its Canadian roster, while Amcor’s all-stock merger with Berry Global forged a USD 23 billion revenue titan integrating 218,000 t of post-consumer resin. Novolex acquired Pactiv Evergreen for USD 6.7 billion, uniting over 250 brands under a foodservice and grocery packaging umbrella. Sealed Air’s pending USD 10.3 billion take-private by CD&R will likely accelerate mono-material tray investments away from quarterly earnings scrutiny.

Scale now underwrites the purchasing of recycled resin, integrated automation systems such as AUTOBAG lines, and proprietary barrier-coating R&D that small independents struggle to match. Digital-printing specialist ePac, operating nine HP Indigo presses across three Canadian cities, fills short-run gaps that megaconverters overlook, while CelluForce’s cellulose-nanocrystal barriers give license to premium recyclable films. Nova Chemicals’ Indiana pyrolysis facility, targeting nearly 50 million kg of recycled polyethylene, exemplifies vertical moves to stabilize PCR supply.

Still, niche opportunities endure. Converters focused solely on high-graphics pet-treat pouches or compostable produce films can differentiate themselves without billion-dollar M&A, provided they secure PCR feedstock through alliances or joint ventures. Retailers armed with EPR fee calculators and recyclability scorecards increasingly favor suppliers offering cradle-to-grave material traceability, putting data management on equal footing with print quality or lead time.

Canada Flexible Packaging Industry Leaders

Amcor PLC

Mondi PLC

Sealed Air Corporation

Winpak Ltd

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Sealed Air agreed to a USD 10.3 billion buyout by Clayton, Dubilier and Rice, aiming for mid-2026 closure.

- October 2025: Cascades divested its Mississauga flexible-packaging plant to Five Star Holding for CAD 31 million (USD 22 million).

- September 2025: CelluForce launched CelluShield cellulose-nanocrystal barrier coating for mono-material polyolefin films.

- September 2025: Nova Chemicals partnered with Charter Next Generation to scale Syndigo recycled polyethylene output above 49.9 million kg.

Canada Flexible Packaging Market Report Scope

Flexible packaging is a method of packaging items that uses non-rigid materials, allowing more cost-effective and customizable solutions. It is a relatively recent approach in the packaging industry that has gained popularity due to its high efficiency and low cost.

The Canada Flexible Packaging Market is Material (Plastics, Paper, Metal Foil, and Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, Sachets and Stick Packs, and Other Product Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, Agriculture and Horticulture, and Other End-User Industries), Printing Technology (Flexography, Rotogravure, Digital Printing, and Other Printing Technologies). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

By End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-user Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Other Product Types | ||

| By End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-user Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the projected value of the Canada flexible packaging market in 2031?

The market is expected to reach USD 12.21 billion by 2031, reflecting a 4.86% CAGR from 2026 to 2031.

Which material segment is growing fastest within Canadian flexible packaging?

Bioplastics and compostable films are forecast to expand at a 5.77% CAGR as retailers pilot cellulose-based solutions for produce.

Why are sachets and stick packs gaining popularity?

Single-dose formats support portion control, lower e-commerce shipping weight, and enable high-impact graphics via digital printing, driving a 6.23% CAGR.

How are EPR regulations influencing packaging design?

Provinces shifting recycling costs to producers push converters toward mono-material films that pass existing sortation tests and minimize EPR fees.

Which printing technology is set to grow fastest?

Digital presses are projected to grow 6.01% annually as private-label brands demand variable data, short lead times, and frequent artwork changes.

What is the main restraint facing Canadian converters today?

Volatile virgin-resin prices linked to crude-oil swings compress margins under fixed-price customer contracts.

Page last updated on: