Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

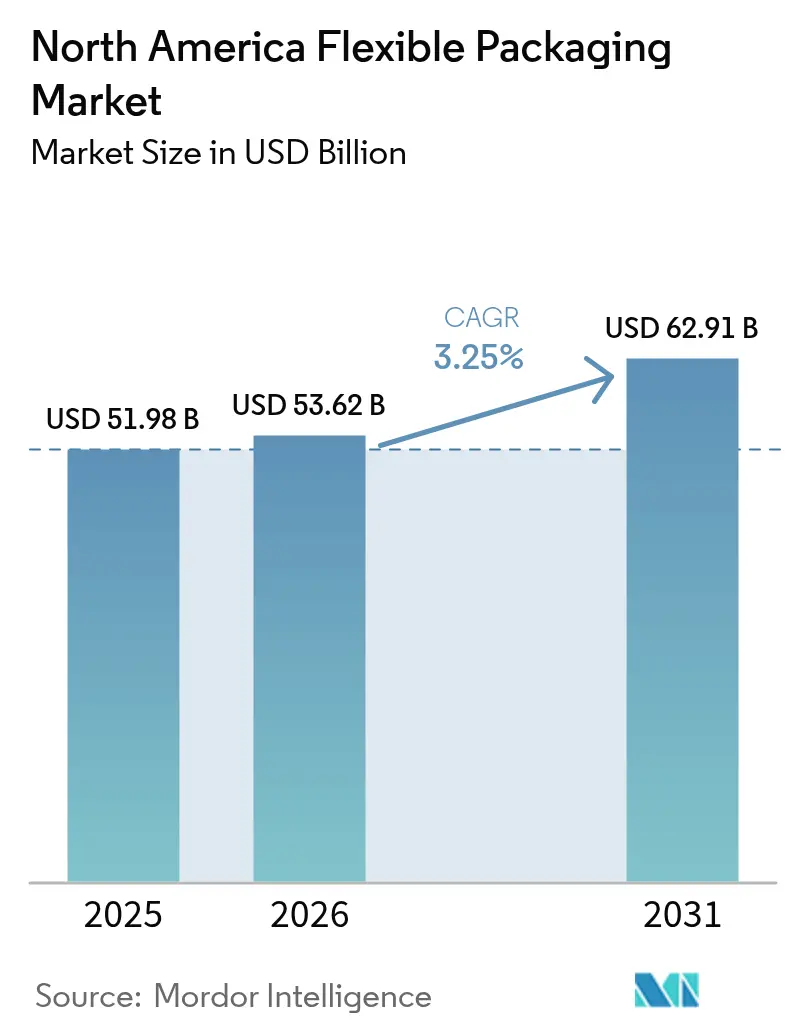

| Base Year Market Size (2025) | USD 51.98 Billion |

| Market Size (2026) | USD 53.62 Billion |

| Market Size (2031) | USD 62.91 Billion |

| Growth Rate (2026 - 2031) | 3.25% CAGR |

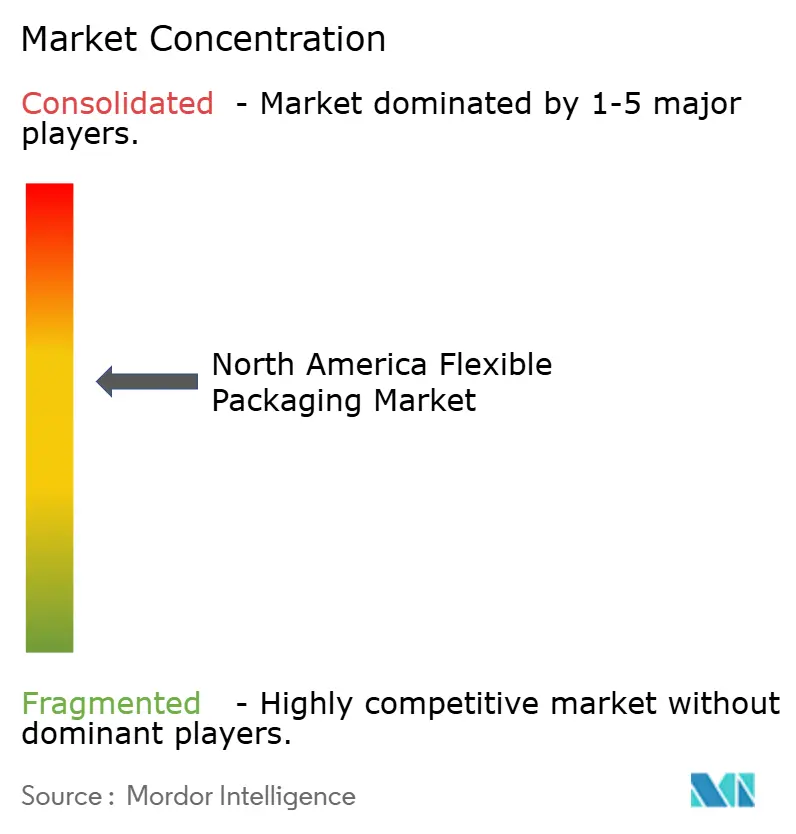

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Flexible Packaging Market Analysis by Mordor Intelligence

The North America flexible packaging market size is projected to expand from USD 51.98 billion in 2025 and USD 53.62 billion in 2026 to USD 62.91 billion by 2031, registering a CAGR of 3.25% between 2026 to 2031. Momentum is shifting from rigid containers to lightweight films, pouches, and wraps that reduce freight costs, satisfy curbside-recyclable pledges, and comply with state-level post-consumer recycled (PCR) mandates. Brand owners are locking multi-year resin contracts as California, New Jersey, Washington, Maine, and Connecticut raise recycled-content thresholds, tightening feedstock supply and elevating PCR premiums. Automation in Amazon and Walmart micro-fulfillment hubs amplifies demand for ultra-thin mailers that can withstand high-speed sortation without tearing. Retailer pressure is accelerating the pivot toward mono-material structures, while nearshoring under USMCA channels investments into Mexico to shorten lead times for U.S. distribution centers. Competitive intensity remains moderate because the top five converters control about 35% of regional capacity, leaving space for mid-tier firms that master thin-gauge extrusion and obtain FDA-cleared recycled resin.

Key Report Takeaways

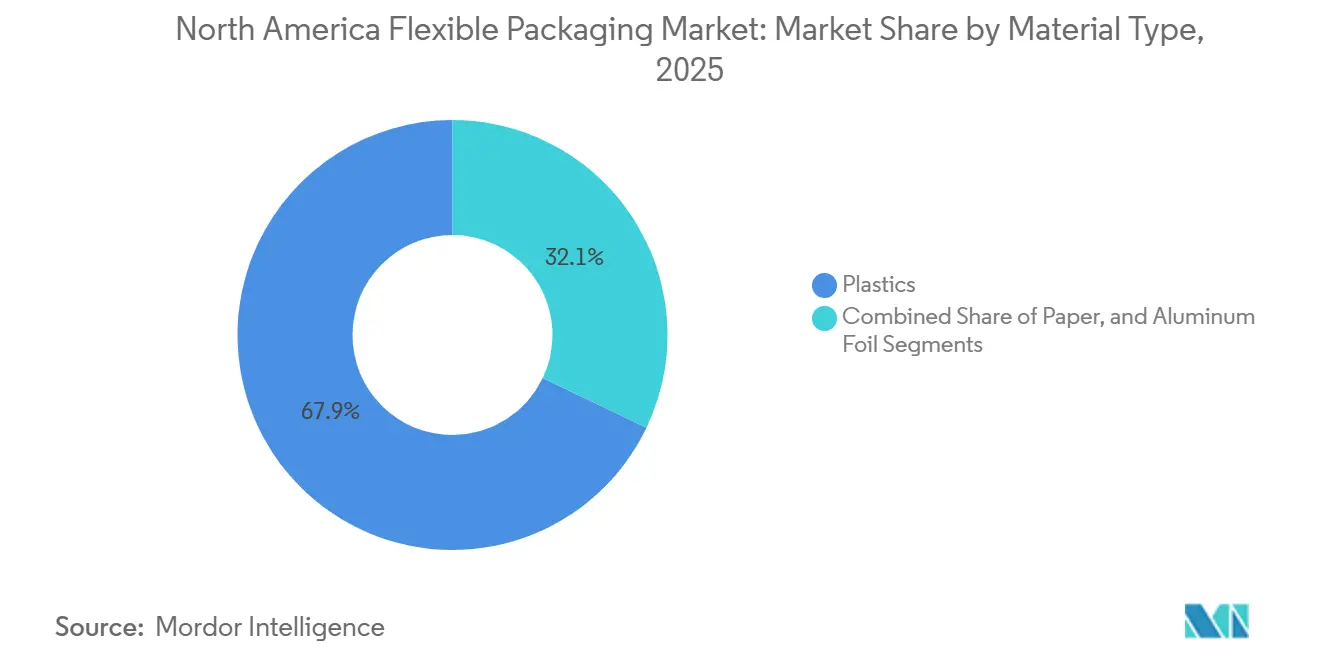

- By material type, plastics led with 67.91% of the North America flexible packaging market share in 2025, whereas paper is forecast to expand at a 3.66% CAGR through 2031.

- By product type, pouches commanded 45.72% revenue share of the North America flexible packaging market size in 2025, while films and wraps hold the fastest projected CAGR at 3.42% to 2031.

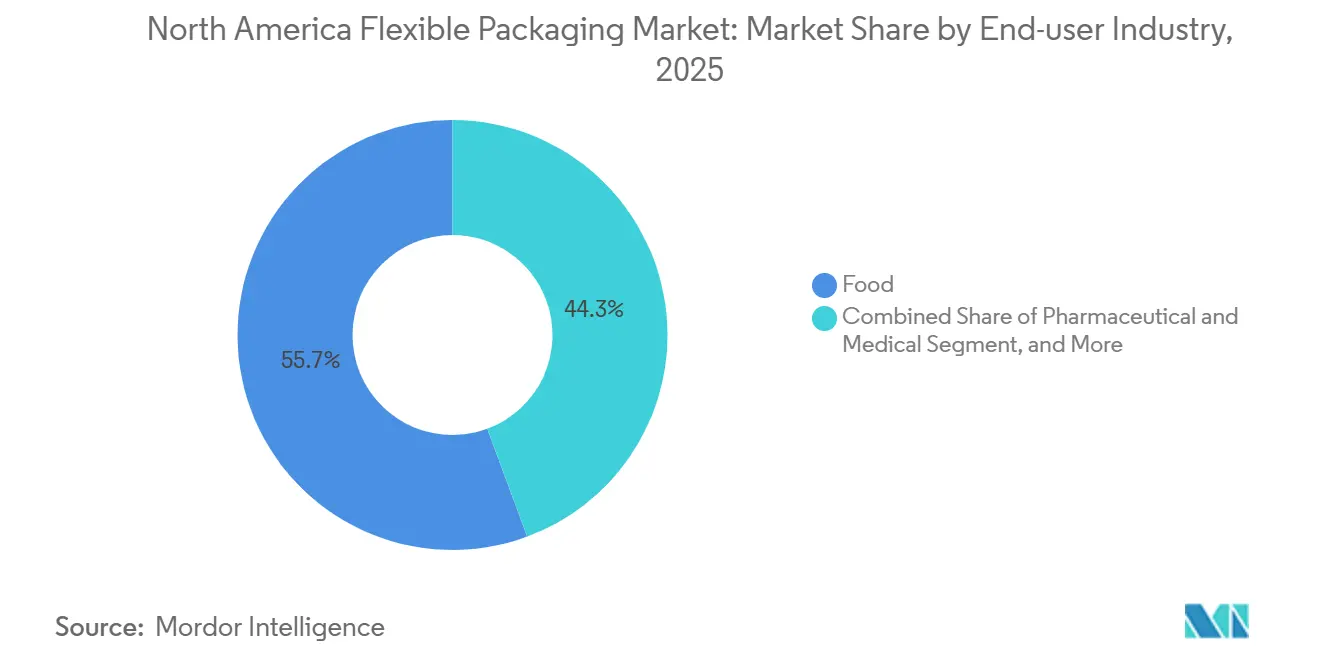

- By end-user industry, food and beverage dominated with 55.66% share in 2025; pharmaceutical and medical applications are advancing at a 3.97% CAGR through 2031.

- By distribution channel, direct B2B accounted for 58.82% revenue in 2025, yet e-commerce and fulfillment will rise at a 4.08% CAGR over 2026-2031.

- By geography, the United States captured 71.84% of 2025 regional revenue, although Mexico is projected to be the fastest-growing country at a 4.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for convenient on-the-go snacking formats | +0.8% | United States, Canada, with spillover to Mexico urban centers | Medium term (2-4 years) |

| Brand-owner shift toward recyclable mono-material structures | +0.7% | United States (California, New York, Washington), Canada (federal plastics strategy) | Long term (≥ 4 years) |

| Premiumisation in pet-food flexibles | +0.4% | United States, Canada | Short term (≤ 2 years) |

| State-level PCR mandates triggering long-term resin off-take contracts | +0.6% | California, New Jersey, Washington, Maine, Connecticut | Long term (≥ 4 years) |

| Automation in micro-fulfilment hubs favouring ultra-thin mailer films | +0.5% | United States (Texas, Ohio, Pennsylvania fulfillment corridors) | Medium term (2-4 years) |

| Retailers' shift to automated micro-fulfilment hubs spurring demand for ultra-thin mailers | +0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Convenient On-the-Go Snacking Formats

Away-from-home food spending reached USD 148.6 billion in 2025 and is on track to climb 39% by 2027, pushing brands to replace rigid canisters with stand-up pouches that fit backpacks and car cup holders.[1]Conagra Brands, “Investor Presentation,” conagrabrands.com Single-serve packs of 28–56 grams represented 42% of salty-snack launches in 2025, up from 31% in 2024, as consumers seek portion control. Flexible structures cut package weight by 60%, saving USD 0.12 per case on cross-country lanes. Resealable zippers appeared on 68% of new snack SKUs in 2025, extending shelf life by 14 days and fetching an extra USD 0.08–0.12 per unit. Quick-service chains such as Chipotle and Panera introduced grab-and-go meal kits in flexible trays, siphoning volumes from rigid formats.

Brand-Owner Shift Toward Recyclable Mono-Material Structures

General Mills pledged to convert its entire North American snack portfolio to all-polyethylene pouches by year-end 2025, eliminating foil and nylon layers that block Store Drop-Off recyclability.[2]General Mills, “Sustainability Commitments,” generalmills.comAmcor’s AmLite all-PE range achieved sub-5 cc/m²/day oxygen transmission without metallization, preserving confectionery shelf life while carrying How2Recycle labels. Kind Snacks cut plastic content by 90% with a paper-based wrapper and earned Climate Pledge Friendly status, tapping consumers who filter Amazon searches by sustainability. California’s SB 54 requires 65% recyclability for plastic packaging by 2032 and fines noncompliance up to USD 500 per ton, compelling national brands to standardize on mono-material designs. Only converters wielding 7- to 9-layer co-extrusion lines can meet barrier targets without reverting to non-recyclable laminates.

Premiumisation in Pet-Food Flexibles

Pet-food producers shifted 34% of dry-kibble volume from paper bags to high-barrier pouches between 2024 and 2025, courting millennial owners who value resealability. Blue Buffalo’s 1.8 kg pouch, launched in 2025, lifted average selling prices 22% while trimming package weight 28%. Purina reported that flexible formats generated 19% of its North American pet-food revenue in 2025, up from 11% in 2024. UFlex opened a USD 45 million pouch facility in Mexico to deliver sub-48-hour lead times to U.S. brands, FT.COM reported. Converters gain insulation from commodity swings because brands accept 15–20% higher costs for premium, resealable pouches.

State-Level PCR Mandates Triggering Long-Term Resin Off-Take Contracts

California’s AB 793 requires food-contact packaging to contain 15% PCR by 2025, increasing to 50% by 2035, with daily penalties of USD 50,000 for infractions. New Jersey, Washington, Maine, and Connecticut enacted parallel rules, spurring Amcor, Sealed Air, and Berry Global to sign 5- to 7-year off-take agreements that secure roughly 120,000 t/y of recycled resin. Only a dozen North American suppliers hold FDA letters of no-objection, driving PCR premiums to USD 400/t over virgin polyethylene. ExxonMobil’s Baytown chemical-recycling line produced 30,000 t of certified circular polymer in 2025, yet costs remain 35% above mechanical recycling. Compliance auditing now adds USD 25,000–50,000 per SKU under ISO 14021 and APR recognition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited curb-side collection for multilayer films | -0.4% | North American municipalities | Long term (≥ 4 years) |

| Polymer-price volatility after geopolitical shocks | -0.6% | Supply chains tied to global markets | Medium term (2-4 years) |

| Scarcity of FDA-grade rPE feedstock | -0.3% | U.S. food-contact converters | Medium term (2-4 years) |

| Extended Producer Responsibility laws impose new fees and reporting burdens | -0.2% | CA, OR, CO, ME, MN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Curb-Side Collection for Multilayer Films

Just 8% of U.S. municipalities accept flexible films curbside, leaving Store Drop-Off programs to capture under 9% of sold volume in 2025.[3]Association of Plastic Recyclers, “Film Design Guide,” plasticsrecycling.org Films snarl optical sorters, prompting many material recovery facilities to landfill entire bales when contamination tops 25%. PFAS bans in 11 states eliminated grease-resistant coatings, narrowing compostable options. Although APR guides endorse PE films thicker than 2.5 mil and free of metal layers, 63% of 2025 pouch launches used aluminum-oxide barriers, rendering them ineligible. Consumer skepticism is rising as 47% of shoppers doubt films get recycled, according to a 2025 McKinsey survey.

Polymer-Price Volatility After Geopolitical Shocks

North American polyethylene spot prices fell 18% in 2024 on Middle East capacity additions, then rebounded when Red Sea tensions spiked, and freight costs rose 42% in Q1 2025. A modeled 25% tariff on Chinese and Mexican imports would raise landed resin costs by USD 310/t, or 27%. Henry Hub gas hovered between USD 2.10 and USD 4.80 per million BTU in 2025, adding uncertainty for ethylene crackers. A 10% resin swing cuts converter revenue 6–8% when utilization is below 65%. Volatility discourages new extrusion lines because ROI models collapse when feedstock shifts by double digits in a quarter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Hold Sway as Paper Gains Pace

Polyethylene, biaxially-oriented polypropylene, cast polypropylene, polyvinyl chloride, and ethylene-vinyl alcohol accounted for 67.91% of the North America flexible packaging market in 2025. Paper-based alternatives are forecast to post a 3.66% CAGR, the quickest growth among materials, as retailers promote curbside-recyclable formats. Polyethylene’s FDA-approved status and heat-seal reliability make it dominant in food contact, whereas biaxially oriented polypropylene serves snacks that need stiffness and clarity. Cast polypropylene thrives in retort pouches that survive 121 °C sterilization with no delamination. Ethylene-vinyl alcohol layers deliver oxygen barriers below 0.5 cc/m²/day, critical for fresh meat and coffee packaging.

Mondi’s PerFORMing paper pouch, introduced in 2025, allows fiber recycling while keeping soups and sauce mixes dry, winning Nestlé and Unilever contracts. Ranpak’s corrugated mailers replaced 18 million bubble mailers across e-commerce channels in 2025. Aluminum foil retained a 6% share, concentrated in coffee and pet food, although sustainability pledges threaten future volume. Biodegradable PLA and cellulose films remain below 3% share, hindered by a lack of composting sites. Retail programs such as Amazon’s Climate Pledge Friendly listed 2,400 SKUs with paper content above 70% in 2025, triple 2024’s tally.

By Product Type: Pouches Dominate while Films Accelerate

Pouches secured 45.72% of 2025 revenue in the North America flexible packaging market, fueled by pet-food premiumization and snack convertibility. Films and wraps are projected to grow at a 3.42% CAGR to 2031, powered by e-commerce mailers and fresh-produce flow-wrap. Bags and sachets remain vital for bulk foods and pharma products that require child-resistant zippers that meet U.S. Pharmacopeia standards. Shrink sleeves and labels offer 360-degree branding but must adopt perforated tear strips to aid bottle recycling under state rules.

Amazon and Walmart ran 340 automated fulfillment centers by 2025, each demanding ultra-thin mailers below 2 mil that survive ISTA 6-Amazon drop tests at scale. Flow-wrap for produce advanced 11% in 2025 as modified-atmosphere films extended shelf life 5–7 days. Printpack’s 1.8-mil mailer cut weight is 40% lower than 3.0-mil incumbents, saving USD 0.04 per unit. Pouches will stay category leader, but films and wraps are closing the gap as online retail climbs from 16% of sales in 2025 to 22% by 2031.

By End-User Industry: Food Leads, Pharma Gains Speed

Food and beverage captured 55.66% of 2025 revenue in the North America flexible packaging market. Frozen-food pouches with steam vents snapped up 23% of new launches, enabling microwave prep directly in the pouch. Dairy relies on high-barrier films to keep yogurt fresh for 60 days, and vacuum-skin formats trimmed meat waste by extending freshness 14 days. Snacks drove zipper adoption across 68% of new SKUs, elevating convenience.

Pharmaceutical and medical applications are poised for a 3.97% CAGR due to FDA serialization requirements under the Drug Supply Chain Security Act, which mandate RFID-enabled pouches. Glenroy’s dual-action zipper pouch passed ASTM D3475 child safety tests, winning contracts from 14 pharma brands. Household-care products such as detergent pods pivoted to stand-up pouches, while industrial uses like powdered adhesives still rely on multi-wall bags.

By Distribution Channel: Direct B2B Rules, E-Commerce Races Ahead

Direct B2B agreements accounted for 58.82% of 2025 revenue in the North America flexible packaging market; converters co-create structures with food and pharma processors, locking in multi-year volume. Retail channels claimed 29% share by stocking private-label pouches that prioritize cost efficiency. E-commerce and fulfillment will post a 4.08% CAGR through 2031 as D2C brands ship straight to consumers, bypassing store shelves.

Warby Parker and Dollar Shave Club swapped corrugated boxes for custom mailers, trimming per-shipment packaging costs by USD 0.22. Amazon certified 4,800 flexible SKUs under its Frustration-Free program in 2025, requiring curbside recyclable designs. 3PLs like ShipBob bundle flexible-pack procurement with fulfillment contracts, shortening supply chains for emerging brands. Retail’s share will erode as online subscription models expand.

Geography Analysis

The United States held 71.84% of the North America flexible packaging market in 2025, anchored by food-processing clusters in California, Texas, Illinois, and Ohio. Seven states enacted Extended Producer Responsibility laws that increased compliance costs by USD 0.02–0.05 per kilogram. Post-consumer recycled content rules in five states locked 120,000 t/y of resin under long-term agreements, raising recycled premiums USD 400/t above virgin grades. Amazon and Walmart fulfillment networks swelled mailer demand for ultra-thin PE films that only eight U.S. converters can supply at scale. Texas attracted USD 1.2 billion in flexible-pack investments between 2024 and 2025 owing to Gulf Coast resin and cross-border logistics.

Canada contributed 18% of 2025 revenue, driven by Quebec and British Columbia EPR rules that add CAD 0.03-0.06 (USD 0.022-0.044) per kilogram in producer fees.[4] Environment and Climate Change Canada, “Provincial EPR Frameworks,” canada.ca Ontario spared flexible packaging from its single-use ban, protecting pouch demand. Transcontinental installed a USD 38 million extrusion line in Montreal in 2025 to serve pharma pouches with child-resistant features TC.TC. Canada’s 2.8% CAGR through 2031 reflects mature demographics yet benefits from growing e-commerce and healthcare spending.

Mexico is forecast to post the fastest 4.01% CAGR as nearshoring and USMCA incentives draw capacity closer to U.S. buyers. UFlex’s USD 45 million Queretaro plant and Amcor’s Monterrey expansion add high-barrier pouch lines optimally located for 48-hour deliveries to Texas and California. Labor costs average USD 4.20 per hour, far below U.S. rates, slicing conversion costs by up to 40%. Domestic food demand remains robust, and tortilla as well as snack producers are adding modified-atmosphere pouches to extend shelf life. Recycling infrastructure lags, with curbside film collection in fewer than 5% of municipalities, posing long-term sustainability challenges.

Regulatory Landscape

North America flexible packaging regulation is increasingly state-led, with EPR, recycled-content, and labeling rules running alongside federal oversight for food-contact materials. California remains the key reference point. SB 54 entered an implementation phase in 2026, and SB 343 tightens conditions for using the chasing-arrows recycling symbol based on specific recyclability criteria, which pressures brands to harmonize national SKU designs.

In food-contact safety, the U.S. FDA finalized a systematic process for post-market assessment of chemicals in food in 2026, changing how food-contact substances are reviewed over time. The FDA also updated 21 CFR Part 176.170 in April 2026 to set a specific migration limit for BPA substitutes (BPS, BPF) in coated paper and paperboard, with compliance timelines beginning in mid-2026 and tied to ISO/IEC 17025-accredited lab testing. On PFAS, the U.S. EPA revised the submission timing for its PFAS Reporting and Recordkeeping Rule in April 2026, shifting the reporting window to start in 2027, while state-level PFAS restrictions continue to affect grease-resistant coatings used in some flexible packaging applications.

Value Chain Analysis

The North America flexible packaging value chain starts with feedstock and substrate suppliers, including PE/PP resins, additives, aluminum foil, and paper. It then moves through film extrusion, coating and lamination, printing, pouch converting, and finishing, before reaching brand-owner filling lines and distribution through direct B2B and e-commerce fulfillment networks. Industry groups such as the Flexible Packaging Association (FPA) and the Advanced Packaging Association (APA) support coordination on design-for-recycling guidance, material selections, and end-of-life initiatives that shape the specifications transmitted by large retailers and consumer brands.

In 2026, shifts in both compliance expectations and production capabilities are changing handoffs across the chain. California SB 54 permanent regulations were approved on May 1, 2026, and the Circular Action Alliance registration milestone (June 1, 2026) reinforced producer data-reporting and stewardship requirements, which cascade into converter documentation, material declarations, and redesign work. On the manufacturing side, ProAmpac finalized the acquisition of TC Transcontinental Packaging (March 2026), PPC Flex completed the acquisition of SUDPACK's US operations (January 2026), and Amcor announced expanded North American PE shrink film capabilities (February 2026), underscoring consolidation and investment in printing, barrier, and mono-material technology as PCR availability and recyclability constraints remain recurring bottlenecks.

Competitive Landscape

The North America flexible packaging market exhibits moderate concentration: Amcor, Sealed Air, Berry Global, Mondi, and ProAmpac together controlled about 35% of capacity in 2025. Amcor’s 2024 purchase of a Texas PCR supplier secured 22,000 t/y of FDA-cleared resin, letting the company guarantee 25% PCR content and meet SB 54 requirements. Sealed Air rolled out machine-vision quality inspection across 12 factories in 2025, slashing defects 18%. Berry Global locked a 7-year deal for 18,000 t/y of recycled PE from a Pennsylvania recycler, limiting spot-market exposure.

Innovation differentiates leaders; converters with in-line corona treatment and digital presses secure 12-15% price premiums on short runs as brands launch limited-edition flavors. Charter Next Generation opened a Columbus, Ohio plant in 2025, just 200 miles from nine Amazon centers, promising 48-hour lead times on ultra-thin mailers. Private-equity-backed Novolex swallowed three Midwest converters in 2024 to broaden reach and integrate corrugated and flexible formats. Patent filings confirm an R&D race: Printpack lodged seven U.S. patents in 2025 for nano-clay-reinforced PE films that combine 40% weight savings with 400 g-force puncture resistance.

Laggards that depend on non-recyclable multilayer laminates face margin pressure as retailers demand How2Recycle-eligible designs. Barriers to entry are rising as 68% of Fortune 500 brands require ISO 9001 and ISO 14001 certification from suppliers. Competitive intensity will climb through 2031 as PCR quotas stiffen and micro-fulfillment automation insists on thinner, tougher films, rewarding converters that co-locate near demand corridors and master advanced extrusion.

North America Flexible Packaging Industry Leaders

Amcor PLC

Mondi PLC

Transcontinental Inc.

American Packaging Corporation

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EPR implementation and recyclability labeling requirements are creating near-term opportunities for converters that can document compliant designs, provide accurate data to producer responsibility organizations, and supply mono-material structures that fit state rules without degrading barrier performance. California SB 54 provides a clear anchor for demand. Permanent regulations took effect May 1, 2026, and the Circular Action Alliance producer registration milestone in June 2026 increases the need for traceable bill-of-materials, recycled-content documentation, and packaging redesign programs, which typically translate into new tooling, qualification, and co-development activity between brand owners and converters.

Recent investment and capacity announcements also signal where short-cycle demand is being targeted. Amcor announced expanded North American printing, lamination, and converting capabilities for the protein market, with equipment installations scheduled through the first half of 2026. ePac Flexible Packaging also announced capacity expansion with a new Phoenix, Arizona site, along with added capacity in Atlanta, Philadelphia, and Vancouver. Together, these moves suggest active buying for faster-turn, high-graphic flexible packaging and for food-oriented structures that meet both performance requirements and evolving compliance expectations. Mexico-focused investments under USMCA and the push for FDA-cleared PCR keep feedstock localization, qualified recycled resin sourcing, and related documentation as actionable opportunity areas for firms that can lock supply and validate food-contact performance.

Recent Industry Developments

- April 2026: Mondi opened a new paper bag production facility in the Pittsburgh, Pennsylvania area, consolidating operations to support e-commerce and industrial demand. The move adds modernized converting capacity closer to major U.S. customer corridors and reinforces paper-based flexible alternatives where curbside-recyclable fiber formats are favored.

- November 2025: Amcor announced an expansion of its North American printing, lamination, and converting capabilities for the protein packaging market, with new equipment installations scheduled through the first half of 2026. This investment targets high-throughput food applications where barrier performance and sustainability claims are increasingly specified by brand owners and retailers.

- April 2024: Amcor completed its all-stock combination with Berry Global. The transaction increased scale across flexible films and related packaging portfolios, supporting broader manufacturing reach and procurement leverage for materials used across North America.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers flexible packaging sold in North America, measured in value, across major flexible materials and pack formats used to pack consumer and industrial products.

Scope exclusions: Rigid packaging formats and packaging machinery are excluded, and upstream resin, paper pulp, or foil raw material sales are not counted as market value.

Segmentation Overview

- By Material Type

- Plastics

- Polyethylene (PE)

- Biaxially-Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Polyvinyl Chloride (PVC)

- Ethylene-Vinyl Alcohol (EVOH)

- Paper

- Aluminum Foil

- Plastics

- By Product Type

- Pouches

- Bags and Sachets

- Films and Wraps

- Shrink Sleeves and Labels

- Other Product Types

- By End-user Industry

- Food

- Frozen Food

- Dairy Products

- Fruits and Vegetables

- Meat, Poultry and Seafood

- Baked Goods and Snacks

- Confectionery

- Other Food

- Beverage

- Pharmaceutical and Medical

- Household and Personal Care

- Industrial and Chemical

- Other End-User Industries

- Food

- By Distribution Channel

- Direct B2B

- E-commerce & Fulfilment

- Retail

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to build the fact base for packaging demand across the United States, Canada, and Mexico before interviews started. We referenced public manufacturing and trade indicators, including US Census Bureau releases, Statistics Canada tables, and Mexico INEGI industrial statistics, to map packaging output and the direction of demand.

To tighten assumptions on end uses and materials, we also used sources such as the US International Trade Commission trade data, industry association publications, and peer reviewed packaging and materials science journals that track film structures, recycling targets, and barrier requirements. Company annual reports, investor presentations, and press releases were used to sanity check capacity additions, plant utilization commentary, and product mix shifts. In a few places, we also checked patterns through paid subscriptions focused on company financials and on import and export shipment-level signals. These desk sources are illustrative only, and many other references were used during data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating pack format demand (pouches, bags and sachets, films and wraps, and shrink sleeves and labels) and pricing behavior by material, since these two points drive the final value the most. We spoke with packaging converters, material suppliers, distributors, and large end users across food, beverage, pharma and medical, household and personal care, and industrial uses, and we ensured coverage across the United States, Canada, and Mexico to align with the regional mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 35% | |

| Smaller Players: 17% | Managers: 53% |

Market-Sizing & Forecasting

Market sizing starts from a top down reconstruction of flexible packaging demand by end use in North America. Packaged food and beverage output, household consumption, and industrial activity are translated into flexible pack usage, and then priced using observed converter level price bands. Once that total is built, we corroborate it with selective bottom up approximations, such as rolling up a sample of converter revenues by geography and checking implied volume using sampled average selling prices per kg and typical pack weights.

The model relied most on packaged food volumes and category mix, share shift toward pouches versus other formats, PCR content adoption timelines that affect material costs and pricing, trade flows for films and laminates, and the split of distribution between direct B2B, e-commerce and fulfillment, and retail. Where the bottom up roll up is incomplete, for example for private firms or missing country splits, the estimate is bridged using peer benchmarks and then corrected through interview feedback.

For forecasting, scenario analysis was used so near term swings in resin and paper pricing, recycling policy timing, and consumer demand could be expressed as clear base, conservative, and upside cases. Assumptions were pressure tested with primary respondents, and only then were growth rates applied back to each format and end use to reach the final regional total.

Data Validation & Update Cycle

Outputs were checked in rounds, first through internal consistency tests across materials, formats, and end uses, and then against independent signals such as trade direction, packaging production trends, and major converter commentary. If an outlier appeared, such as an implied price jump that did not match resin movements or a country mix that did not align with observed demand, we revisited the assumption and re contacted experts for quick confirmation.

Before sign off, another analyst reviews the full model logic and the year by year trend to confirm that growth, pricing, and mix changes move together. Reports are refreshed annually, with interim updates when material events occur, such as policy changes, major capacity additions, or abrupt raw material pricing shifts. Right before delivery, we do a final pass so clients receive the latest view available at that time.

Mordor Intelligence's North America Flexible Packaging Market Market Size Compared With Other Published Estimates

Published market sizes for North America flexible packaging can differ even when the topic sounds the same, because included countries, counted formats, and pricing logic are not always aligned. Differences also show up when a publisher uses an older base year, applies a faster price escalation, or includes rigid categories in a flexible packaging total.

Some external estimates are narrower, for example covering only the United States and Canada, or they are high level on formats and rely on a single growth rate for the full market. In Mordor Intelligence, the total is built for the United States, Canada, and Mexico, and it is counted only for flexible materials and flexible pack formats sold into end user industries. The result is stress tested through price band checks by material and format.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 51.98 B (2025) | |

| Industry Research Publisher A | USD 49.67 B (2025) | The scope is country limited (United States and Canada), which can undercount demand linked to Mexico based manufacturing and cross border packaging supply. The format structure is also summarized more broadly, so mix shifts between pouches and films are less directly reflected in the value build. |

| Regional Consultancy B | USD 45.35 B (2024) | The base year differs, and the growth path is steeper, which makes currency timing and assumed price escalation matter more than observed price bands. The scope also lists a wider set of materials and technology slices, which can lead to overlaps if coatings, additives, or adjacent packaging components get counted beyond finished flexible packs. |

The spread mainly comes from country coverage, the way flexible formats are grouped, and how pricing is carried forward year to year. By keeping the demand pool tied to end use output and then checking implied prices and mix with interviews, the final number remains traceable to practical inputs that can be revisited in each update cycle.

Key Questions Answered in the Report

How large will the North America flexible packaging market be by 2031?

The market is projected to reach USD 62.91 billion by 2031, expanding at a 3.25% CAGR over 2026-2031.

Which product category is growing fastest in regional flexible packaging?

Films and wraps are forecast to post a 3.42% CAGR through 2031, propelled by e-commerce mailer demand.

Why is Mexico the fastest-growing country for flexible packaging?

Nearshoring under USMCA, lower labor costs, and new pouch capacity support Mexico’s projected 4.01% CAGR to 2031.

What material shift is shaping packaging sustainability goals?

Brand owners are moving from multilayer laminates to recyclable mono-material all-polyethylene structures to meet state PCR mandates.

Which end-user segment is expected to outpace overall market growth?

Pharmaceutical and medical applications are set to grow at a 3.97% CAGR as serialization and child-resistant rules tighten.

Page last updated on: