Flat Carbon Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

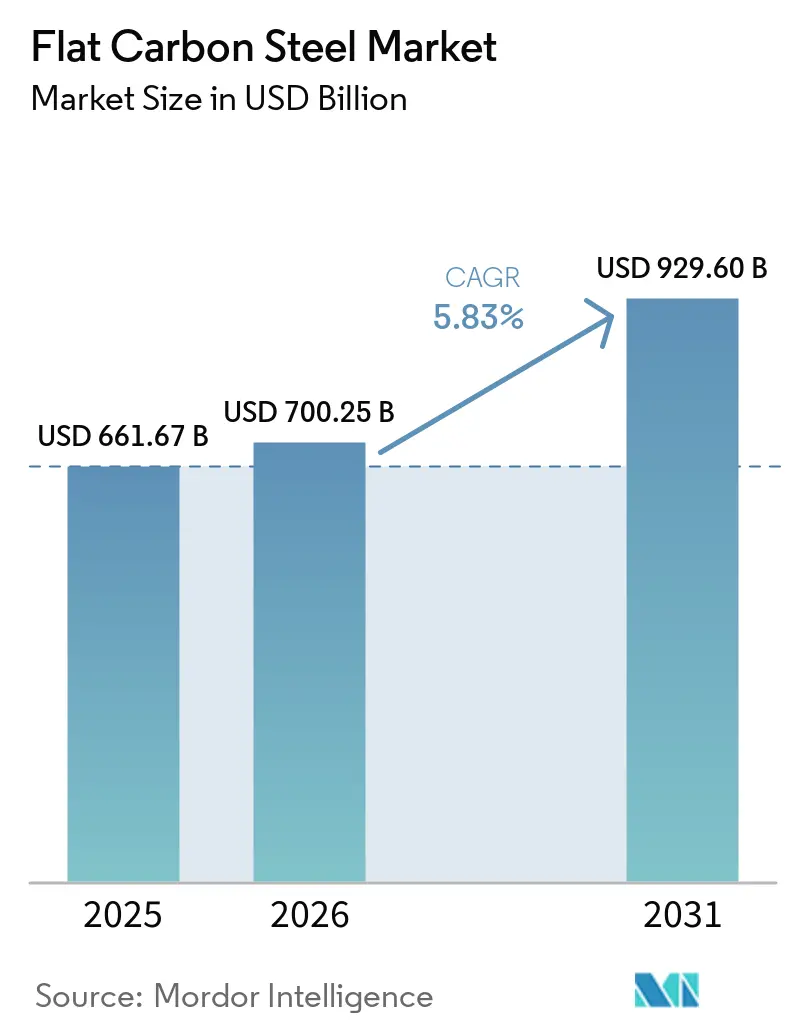

| Market Size (2026) | USD 700.25 Billion |

| Market Size (2031) | USD 929.60 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

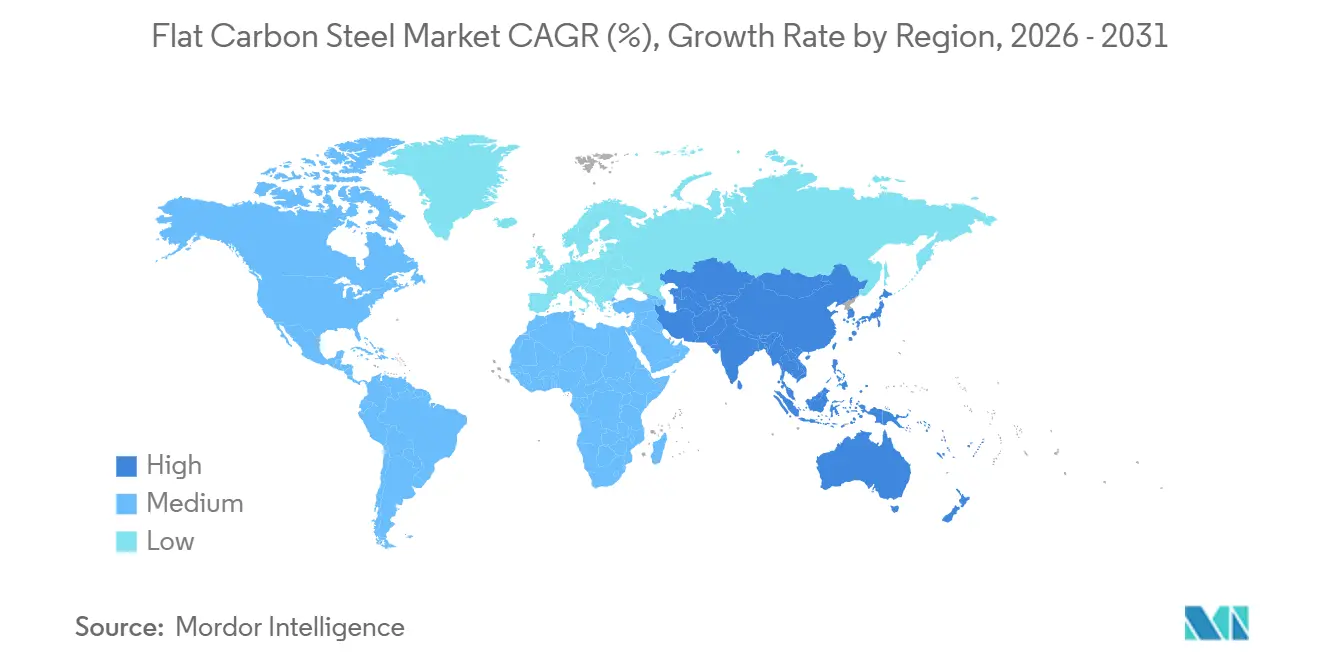

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flat Carbon Steel Market Analysis by Mordor Intelligence

The Flat Carbon Steel Market size is projected to be USD 661.67 billion in 2025, USD 700.25 billion in 2026, and reach USD 929.60 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031. The transition toward value-added, low-carbon flat products is progressing due to factors such as automotive electrification, offshore wind tower construction, and the implementation of carbon-border regulations, which are influencing demand patterns. The Asia-Pacific region is experiencing growth, while North America and Europe are focusing on investments in scrap-based furnaces. Meanwhile, China's capacity-swap policy is encouraging mills to upgrade to premium coil production. Tight raw material markets and increasing carbon fees are driving a gradual shift from blast furnaces to electric arc furnaces (EAF) and hydrogen-based direct reduced iron (hydrogen-DRI) technologies. Additionally, the adoption of digital-twin roll shops and converter models is reducing waste to below 1% and improving throughput, enabling mills to produce thinner gauges for appliances and electric vehicle (EV) stampings.

Key Report Takeaways

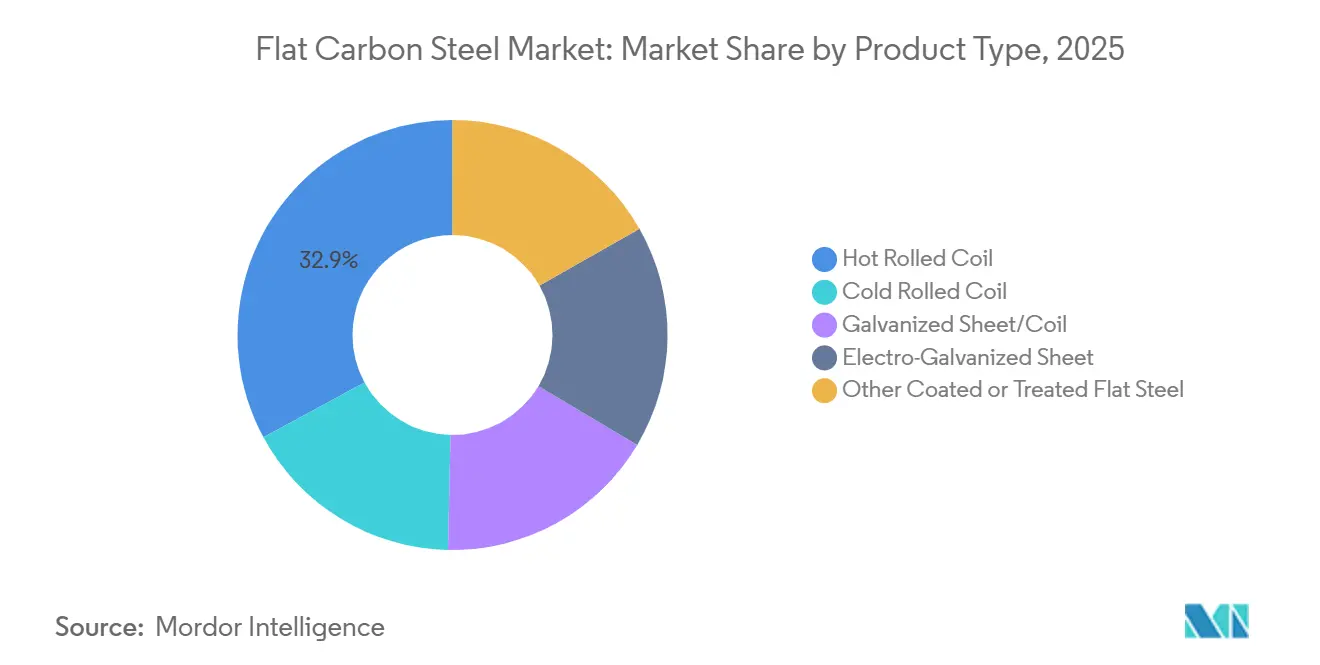

- By product type, hot rolled coil led with 32.89% of flat carbon steel market share in 2025, while galvanized sheet or coil posted the highest 6.47% CAGR outlook through 2031.

- By thickness, medium-gauge (2-10 mm) commanded 41.92% share of the flat carbon steel market size in 2025, whereas light-gauge (less than 2 mm) is projected to advance at a 6.62% CAGR to 2031.

- By production route, basic oxygen furnace accounted for 75.21% of the flat carbon steel market size in 2025; hydrogen-DRI + EAF is expected to expand at a 6.37% CAGR through 2031.

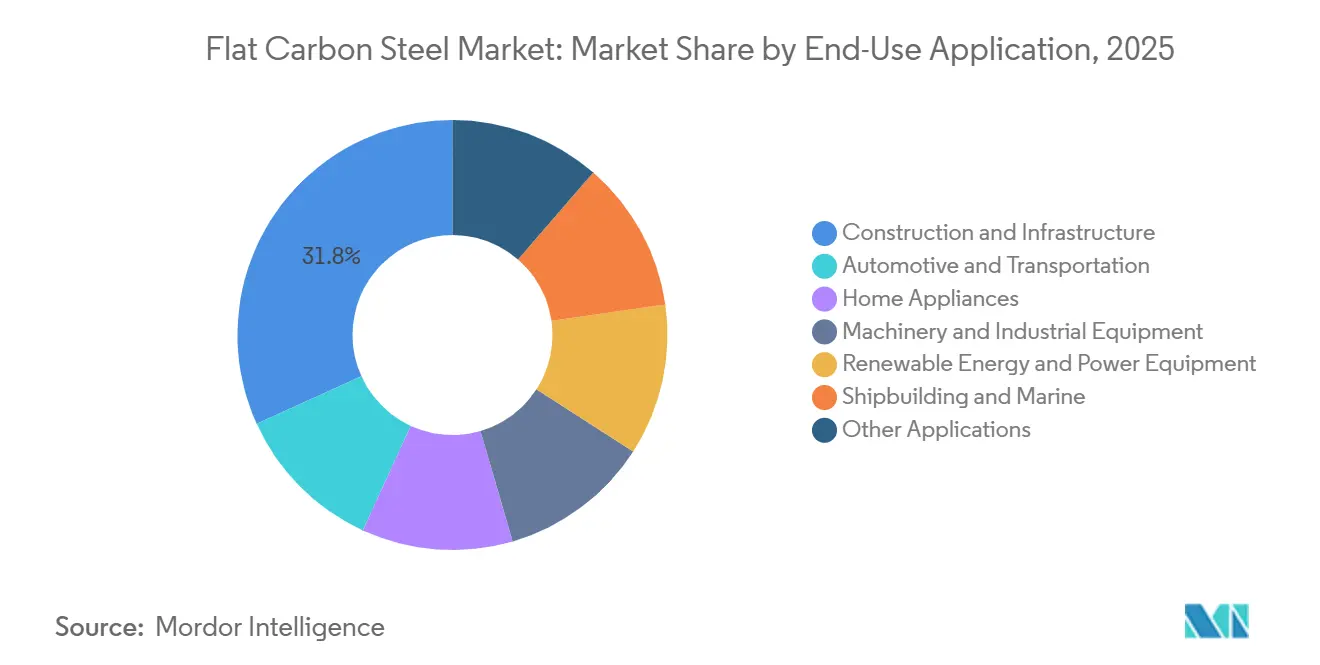

- By end-use application, construction and infrastructure represented 31.78% of flat carbon steel market share in 2025, but renewable energy and power equipment is the fastest-growing end-use application at 6.25% CAGR through 2031.

- By geography, Asia-Pacific contributed 44.37% of 2025 revenue and is forecast to post a 6.72% CAGR, through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Flat Carbon Steel Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand in automotive and shipbuilding | +1.2% | Global, APAC core (China, South Korea, Japan) | Medium term (2-4 years) |

| Global infrastructure and appliance build-out | +1.5% | APAC (India, ASEAN), North America, Middle East | Medium term (2-4 years) |

| Cost-efficient high-strength grades in construction | +0.8% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Offshore-wind tower build-out (heavy-gauge plate) | +0.9% | Europe (UK, Nordic), APAC (Taiwan, Japan), North America (U.S. East Coast) | Long term (≥ 4 years) |

| OEM Scope-3 goals driving 'green flat steel' | +1.0% | Europe, North America, select APAC markets | Medium term (2-4 years) |

| Digital-twin yield optimisation (scrap-cut) | +0.5% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand in Automotive and Shipbuilding

Automotive electrification maintains steel content at approximately 1,200 kilograms per vehicle, including up to 100 kilograms of electrical steel, sustaining cold-rolled coil demand despite a plateau in unit production. Asian shipyards face three-year backlogs for liquefied natural gas (LNG) carriers, requiring high-toughness plate grades and premium coatings, which support pricing for shipbuilding steel[1]Min Joo Kang and Rico Luman, “Asia's Shipbuilding Renaissance,” ingwb.com. In 2024, India added 65 million white goods, increasing galvanized coil volumes, though thinner gauges reduced per-unit steel usage. China's focus on improving scrap quality following the Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships is raising feed costs for electric arc furnace (EAF) mills supplying automotive stampers. South Korea's Hyper-Gap Vision 2040 program is driving demand for advanced plate in liquefied carbon dioxide (CO₂) carriers and dual-fuel ships.

Global Infrastructure and Appliance Build-Out

U.S. construction starts reached an annualized USD 1.24 trillion in January 2026, with nearly USD 20 billion attributed to just three megaprojects, introducing volatility to the flat carbon steel market. India's INR 1,110 million (USD 11.82 million) infrastructure pipeline supports a projected 252 million tons of finished steel demand by fiscal year (FY) 2034. The Association of Southeast Asian Nations (ASEAN)'s USD 3.1 trillion development program is boosting regional coil flows under the Regional Comprehensive Economic Partnership (RCEP) while reducing reliance on Chinese imports. Heating, ventilation, and air conditioning (HVAC) shipments declined by 20% in 2025 to 7.7 million units, negatively impacting sheet volumes for cabinets and ducts. In the Middle East, demand remains steady at approximately 50 million tons, driven by projects like NEOM and Vision 2030, which drive heavy plate and structural beam consumption.

Offshore Wind Tower Build-Out

Tower foundations for offshore wind require a 50-100 millimeter plate at 120-180 tons per megawatt, creating significant demand for heavy-gauge mills. Taiwan's 15 gigawatt (GW) target necessitates 1.7 million tons of plate by 2035, while the United Kingdom will require up to 25 million tons by 2050. The United States plans for 70 GW of capacity, which will demand 22 million tons over 20 years, though permitting delays are shifting some orders to Europe and Asia. Supplier qualification under Det Norske Veritas (DNV) and International Organization for Standardization (ISO) standards narrows the pool, supporting price premiums that enhance earnings before interest, taxes, depreciation, and amortization (EBITDA) margins over commodity coil. A single 15 megawatt (MW) turbine foundation can require 1,800-2,700 tons of plate, encouraging long-term framework agreements.

OEM Scope-3 Goals Driving Green Flat Steel

Automakers such as BMW, Volvo, and Nissan are incorporating low-carbon steel clauses in sourcing contracts, paying premiums of 10-20% for hydrogen-based steel. SSAB's Luleå pilot is scaling commercial production using renewable hydrogen to achieve near-zero emissions, supported by Nordic hydro power. Thyssenkrupp is testing 70% hydrogen injection and aims for green hydrogen costs below USD 2 per kilogram to achieve cost parity with traditional blast furnaces. The European Union (EU) Carbon Border Adjustment Mechanism, effective January 2026, is expected to increase the landed cost of high-carbon imports by up to 15%. North American automakers are aligning with Securities and Exchange Commission (SEC) climate-disclosure rules, requiring mill-level Scope 3 emissions tracking to secure financing.

Restraints Impact Analysis of Flat Carbon Steel Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile iron-ore and coking-coal prices | -0.7% | Global, acute in import-dependent regions (Europe, Japan, South Korea) | Short term (≤ 2 years) |

| Stringent carbon-emission regulations | -0.5% | Europe (CBAM), North America (state-level mandates), select APAC markets | Medium term (2-4 years) |

| Persistent global over-capacity | -0.9% | Global, concentrated in China and CIS | Long term (≥ 4 years) |

| Scarce prime scrap for EAF decarbonisation | -0.4% | North America, Europe, and select APAC markets are expanding EAF capacity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Iron-Ore and Coking-Coal Prices

U.S. metallurgical coal exports are projected to rise to 53.4 million short tons by 2026, affecting global coke supplies and increasing furnace costs[2]U.S. Energy Information Administration, “Short-Term Energy Outlook 2026,” eia.gov. Disruptions in Brazilian mining operations and port delays in Australia have caused significant monthly fluctuations in iron-ore prices, impacting mill working capital. Spot coking coal prices increased following shipping disruptions in the Middle East, further widening the cost difference between blast furnace (BF) and electric arc furnace (EAF) production routes. Additionally, blast furnace producers are facing increasing carbon fees, while EAF mills are dealing with scrap price increases, with busheling reaching USD 422.50 per gross ton. Higher diesel and power tariffs have also increased freight and melting costs, reducing profit margins across the Flat carbon steel industry.

Persistent Global Over-Capacity

Despite China reducing crude steel output to 960.81 million tons by 2025, latent capacity continues to exceed domestic demand by 50-100 million tons. To address this, mills are shifting production from rebar to hot-rolled coil and targeting export markets at prices 30% lower than Western benchmarks, which impacts the Flat carbon steel market. Section 122 tariffs at 10% in the United States and quota restrictions in the European Union have fragmented trade flows, creating regional price differences of USD 200-300 per ton. Political challenges have slowed the closure of excess capacity, prompting mills to focus on value-added coatings to avoid commodity pricing pressures. Persistent over-capacity sustains spot price fluctuations and discourages new greenfield blast furnace investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Flat Carbon Steel Market Segment Analysis

By Product Type:

Galvanized Coil Surges on Corrosion StandardsGalvanized sheet and coil are projected to grow at a rate of 6.47% by 2031. Hot rolled coil accounted for 32.89% of the flat carbon steel market share in 2025, supported by demand for structural beams, ship plates, and automotive panels. The market size for galvanized products is expected to expand alongside Asia’s shipbuilding recovery and India’s growing appliance industry. Cold-rolled coil, while essential for automotive stampings, faces substitution challenges due to gauge-thinning alternatives. Electro-galvanized sheet maintains a small but steady niche in automotive exposed panels. Other coated flat steel products benefit from growth in food packaging and solar-roof initiatives.

Mills with in-house galvanizing and continuous annealing lines have a competitive advantage as customers prioritize certified coating weights. China’s sufficient plate capacity enables shipyards to demand higher standards, creating challenges for new market entrants. ArcelorMittal has invested EUR 500 million (USD 585.5 million) in a French electrical-steel line to supply electric vehicle (EV) motors and diversify into silicon grades. Premium ship plates command higher prices due to requirements for liquefied natural gas (LNG) containment and cryogenic properties. Appliance manufacturers pay a premium for tighter thickness tolerances, which digital-twin mills can reliably produce.

By Thickness:

Light-Gauge Leads Energy-Efficient AppliancesLight-gauge coil under 2 millimeters (mm) is expected to grow at 6.62%, driven by the adoption of 0.4-0.6 mm panels in refrigerators and washing machines without compromising rigidity. Medium-gauge steel held a 41.92% share of the flat carbon steel market in 2025, owing to its versatility in beams, automotive chassis, and offshore monopiles. The market benefits from digital roll models that reduce gauge spreads to below 0.5%, enabling appliance original equipment manufacturers (OEMs) to source niche widths domestically. Ultra-thin strips below 0.8 mm support applications in packaging and EV laminations.

Heavy plates over 10 mm are essential for wind towers and shipbuilding but remain capacity-constrained, giving pricing power to qualified mills. U.S. utility projects are driving medium-gauge demand, while multifamily housing supports light-gauge steel for studs. Although Chinese overcapacity pressures mid-gauge margins, quality improvements are opening export opportunities. Data indicates that appliances produced in Asia require fewer kilograms of steel per unit, but rising production volumes offset material reductions, sustaining tonnage growth.

By Production Route:

Hydrogen-DRI Investment AcceleratesElectric arc furnaces (EAF) are capturing a growing share of production as mills focus on reducing emissions and securing green-premium contracts. Basic oxygen furnaces retained a 75.21% share in 2025, reflecting slower modernization among older mills. Hydrogen-DRI combined with EAF is projected to grow at 6.37% through 2031, driven by European Union (EU) Carbon Border Adjustment Mechanism (CBAM) penalties and OEM Scope 3 emissions requirements. The flat carbon steel market is becoming more resilient as mills diversify raw materials, blending scrap with DRI pellets.

ArcelorMittal’s EUR 1.3 billion (USD 1.52 billion) Dunkirk EAF will operate on low-carbon electricity, achieving emissions of 0.6 tons of carbon dioxide (CO₂) per ton of steel, demonstrating that large-scale plants can meet CBAM thresholds. In the U.S., projects worth USD 6 billion are targeting Gulf Coast gas hubs for DRI feedstock. Scrap shortages have pushed busheling prices above USD 420 per gross ton, encouraging direct reduction imports from the Middle East. India has set a long-term capacity target of 500 million tons, supported by blended financing for green furnace projects.

By End-Use Application:

Renewables Overtake Growth ChartsThe renewable energy and power equipment market is projected to grow at a rate of 6.25% annually, driven by demand for offshore wind components, solar frames, and grid hardware, which dominate heavy-plate consumption. Construction and infrastructure are expected to account for a 31.78% share in 2025. Automotive production remains stable; however, high-strength thin coils are gaining market share as electric vehicle (EV) manufacturers prioritize lightweight materials. In 2024, the appliances segment is expected to produce 820 million white goods, with galvanized and pre-painted coils accounting for 70-80% of the steel used.

The machinery segment is closely linked to industrial capital expenditures and upgrades in the power sector. In Asia, shipbuilding continues to demand premium-grade plates despite intense competition among shipyards. The packaging industry relies on tin-free and aluminized coils that comply with food safety regulations. As a result, the flat carbon steel market is shifting its focus toward specialized grades rather than raw tons.

Geography Analysis

APAC Flat Carbon Steel Market

Asia-Pacific accounted for 44.37% of the flat carbon steel market in 2025 and is projected to grow at a rate of 6.72% through 2031. This growth is supported by India's INR 1,110 million (USD 11.82 million) infrastructure pipeline and the expansion of manufacturing in ASEAN countries, which sustains demand for steel coils. China's 1.5:1 capacity-swap rule reduced crude steel output to 960.81 million tonnes, yet the country remains the lowest-cost supplier, stabilizing regional prices. India's per-capita steel consumption stands at 93 kg, significantly below the global average of 219 kg, indicating substantial growth potential for the flat carbon steel market. Meanwhile, Japan and South Korea are focusing on high-value products such as ship plates and automotive electrical steel, supported by government-backed innovation funds.

North America Flat Carbon Steel Market

North America emphasizes decarbonization and reshoring efforts. Nippon Steel's USD 14.9 billion acquisition of U.S. Steel includes an additional USD 11 billion capital plan aimed at modernizing hot-strip mills and increasing DRI capacity. Construction starts reached an annualized USD 1.24 trillion in January 2026, though growth depends on sporadic megaprojects. Section 122 tariffs have increased utilization rates to 79.1%, but they also raise costs for downstream fabricators. Canada and Mexico benefit from near-shoring vehicle assembly operations but remain vulnerable to shifts in U.S. policies.

Europe, South America, Middle East and CIS Flat Carbon Steel Market

Europe is navigating carbon regulations and high energy costs. ArcelorMittal's Dunkirk EAF and Mardyck electrical steel line highlight the transition to scrap-based, low-carbon steel production. Steel demand in the EU and UK is expected to recover by 3.2% in 2026, driven by offshore wind projects requiring up to 25 million tonnes of steel plate. Germany and France are investing in grid upgrades and electric vehicle value chains. Meanwhile, CIS steel supply is being redirected to Asia due to sanctions. South America's growth is tied to Brazilian iron ore exports and local construction activities. In the Middle East, efforts to achieve self-sufficiency are evident, with Emirates Steel Arkan increasing capacity to 5.5 million tonnes. Gulf mills are positioning themselves to export green-premium steel plates to Europe, benefiting from CBAM relief measures.

Competitive Landscape

The flat carbon steel market is fragmented. Nippon Steel's acquisition of U.S. Steel secures access to premium automotive grades and pipeline plate, with 48 specialists deployed to implement Japanese process control methods, aiming to increase EBITDA by USD 3 billion. ArcelorMittal has committed EUR 1.8 billion (USD 2.10 billion) to its Dunkirk and Mardyck facilities, combining decarbonization efforts with the expansion of electrical steel production to support EV motor manufacturing. The adoption of digital twins provides early adopters with a competitive advantage by reducing gauge deviation and scrap rates to below 1%.

Opportunities for growth are concentrated in areas such as DNV-certified heavy plate for wind towers, green flat products with verified carbon intensity of less than or equal to 0.6 tons CO₂, and pre-painted coil for energy-efficient appliances. Middle Eastern mills utilize low-cost natural gas for direct reduced iron (DRI) production and renewable energy to export to Europe under CBAM credits. JSW and JFE have launched a 4.5 million-tonne joint venture in Odisha and plan to double capacity, highlighting India's growing influence in the market. However, scrap shortages limit the expansion of electric arc furnaces (EAF), prompting integrated mills with proprietary DRI facilities to secure metallic inputs.

Regional plate manufacturers are enhancing their capabilities in monopile production to meet offshore wind demand. Service centers are consolidating to achieve scale, as demonstrated by Worthington Steel's USD 2.4 billion acquisition of Kloeckner Metals, which expands slitting and painting capacities. Competitive differentiation now hinges on low-carbon intensity, processing capabilities, and digital quality assurance rather than production volume alone.

Flat Carbon Steel Industry Leaders

POSCO

China BaoWu Steel Group Corp. Ltd.

ARCELORMITTAL

NIPPON STEEL CORPORATION

JFE Steel Corporation

- *Disclaimer: Major Players sorted in no particular order

Flat Carbon Steel Market Companies Covered in this Report

- AM/NS India

- ARCELORMITTAL

- BlueScope Steel Limited.

- China BaoWu Steel Group Corp. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hyundai Steel

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- Severstal

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- voestalpine Stahl GmbH

Recent Industry Developments in Flat Carbon Steel Market

- January 2026: Worthington Steel acquired Kloeckner Metals Corporation for USD 2.4 billion to expand its processing capabilities in North America. This acquisition is expected to strengthen Worthington Steel's position in the flat carbon steel market by increasing its ability to process and distribute flat carbon steel products efficiently across the region.

- December 2025: JFE Steel Corporation and JSW Steel Limited formed a 50:50 joint venture in Odisha with an initial production capacity of 4.5 million tons of flat carbon steel. The venture plans to expand this capacity to 10 million tons to address the growing demand from the automotive and infrastructure sectors.

Global Flat Carbon Steel Market Report Scope

Flat carbon steel is a metal alloy primarily composed of iron and carbon, commonly formed into sheets, plates, or strips. Recognized for its strength and cost efficiency, it is widely utilized in construction, automotive, and machinery industries. It is typically classified based on carbon content into low, medium, or high categories.

The flat carbon steel market is segmented by product type, thickness, production route, end-use application, and geography. By product type, the market is segmented into product type hot rolled coil, cold rolled coil, galvanized sheet/coil, electro-galvanized sheet, and other coated or treated flat steel. By thickness, the market is segmented into ultra-thin (less than 0.8 mm), light-gauge (less than 2 mm), medium-gauge (2-10 mm), and heavy-gauge (greater than 10 mm). By production route, the market is segmented into basic oxygen furnace (BOF), electric arc furnace (EAF), and hydrogen-DRI + EAF. By end-use application, the market is segmented into construction and infrastructure, automotive and transportation, home appliances, machinery and industrial equipment, renewable energy and power equipment, shipbuilding and marine, and other applications. The report also covers the market size and forecasts for flat carbon steel in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

Segmentation Overview

| Hot Rolled Coil |

| Cold Rolled Coil |

| Galvanized Sheet/Coil |

| Electro-Galvanized Sheet |

| Other Coated or Treated Flat Steel |

| Ultra-Thin (Less than 0.8 mm) |

| Light-Gauge (Less than 2 mm) |

| Medium-Gauge (2-10 mm) |

| Heavy-Gauge (Greater than 10 mm) |

| Basic Oxygen Furnace (BOF) |

| Electric Arc Furnace (EAF) |

| Hydrogen-DRI + EAF |

| Construction and Infrastructure |

| Automotive and Transportation |

| Home Appliances |

| Machinery and Industrial Equipment |

| Renewable Energy and Power Equipment |

| Shipbuilding and Marine |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Hot Rolled Coil | |

| Cold Rolled Coil | ||

| Galvanized Sheet/Coil | ||

| Electro-Galvanized Sheet | ||

| Other Coated or Treated Flat Steel | ||

| By Thickness | Ultra-Thin (Less than 0.8 mm) | |

| Light-Gauge (Less than 2 mm) | ||

| Medium-Gauge (2-10 mm) | ||

| Heavy-Gauge (Greater than 10 mm) | ||

| By Production Route | Basic Oxygen Furnace (BOF) | |

| Electric Arc Furnace (EAF) | ||

| Hydrogen-DRI + EAF | ||

| By End-Use Application | Construction and Infrastructure | |

| Automotive and Transportation | ||

| Home Appliances | ||

| Machinery and Industrial Equipment | ||

| Renewable Energy and Power Equipment | ||

| Shipbuilding and Marine | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is current market size of Flat Carbon Steel Market?

The Flat Carbon Steel Market size is projected to be USD 661.67 billion in 2025, USD 700.25 billion in 2026, and reach USD 929.60 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

Which region drives demand growth after 2026?

Asia-Pacific leads with a forecast 6.72% CAGR through 2031, fueled by India’s infrastructure and ASEAN manufacturing.

What segment records the fastest growth rate?

Galvanized sheet and coil are expected to grow at 6.47% as appliance and marine corrosion standards tighten.

Why is offshore wind important to steel plate demand?

Each megawatt of offshore wind requires 120-180 tons of 50-100 mm plate, creating a long-term order backlog for qualified mills.

Page last updated on: