Fixed-Wing Unmanned Aerial System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

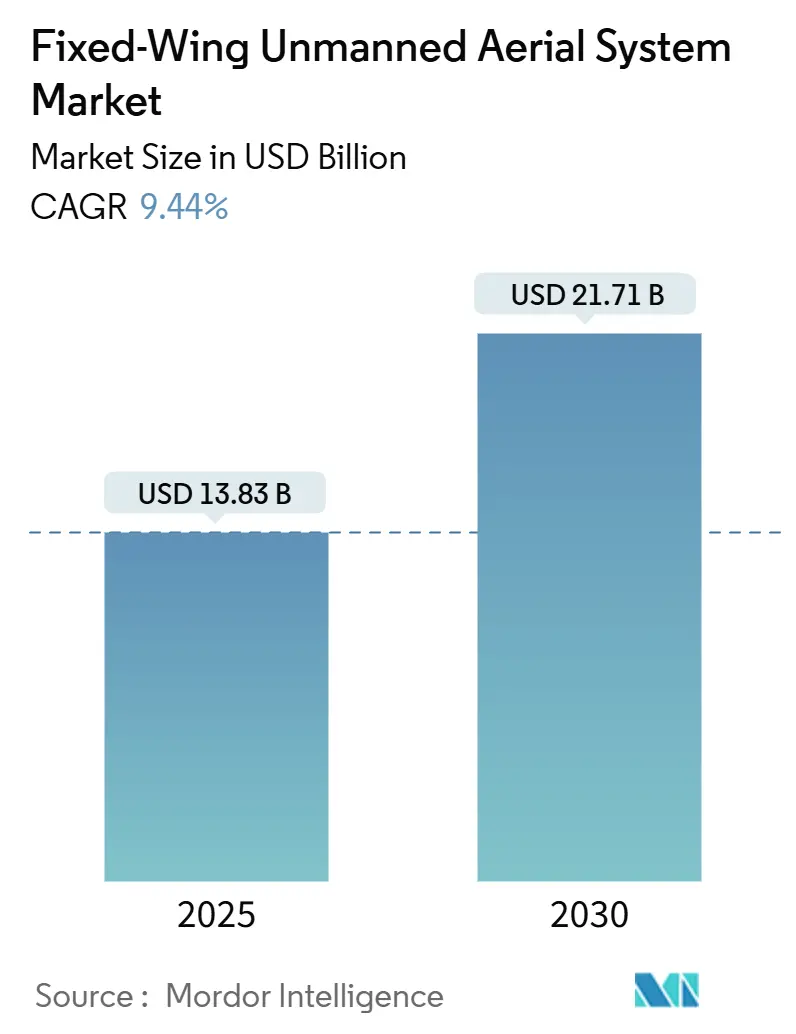

| Market Size (2025) | USD 13.83 Billion |

| Market Size (2030) | USD 21.71 Billion |

| Growth Rate (2025 - 2030) | 9.44% CAGR |

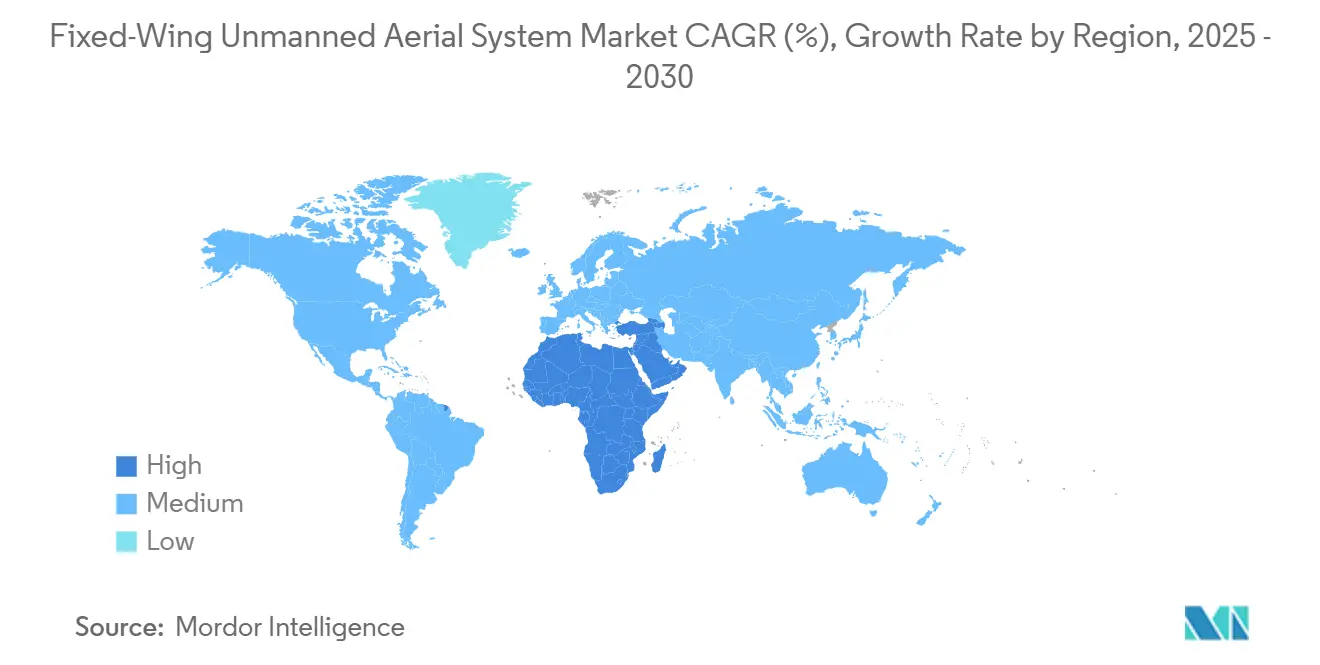

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fixed-Wing Unmanned Aerial System Market Analysis by Mordor Intelligence

The fixed-wing unmanned aerial system (UAS) market size is valued at USD 13.83 billion in 2025 and is projected to reach USD 21.71 billion by 2030, reflecting a 9.44% CAGR over the forecast period. Accelerating defense procurement programs, widening commercial adoption in agriculture and long-range logistics, and steady progress on global beyond-visual-line-of-sight (BVLOS) regulations sustain this expansion. Fixed-wing airframes deliver higher endurance and payload capacity than multirotor designs. This performance edge underpins their rapid uptake for intelligence, surveillance, and reconnaissance (ISR) and high-altitude pseudo-satellite (HAPS) missions. Simultaneously, new hydrogen and hybrid fuel-cell propulsion architectures offer 2–3x endurance gains, reshaping platform economics. On the commercial side, FAA Part 108 and EASA design-verification frameworks are lowering the cost and time of certification, incentivizing infrastructure inspection, corridor mapping, and long-range cargo pilots. Mid-term opportunities lie in AI-enabled swarm autonomy and multi-sensor data-fusion payloads, while supply-chain exposure to advanced composites and wide bandgap electronics remains a headwind.

Key Report Takeaways

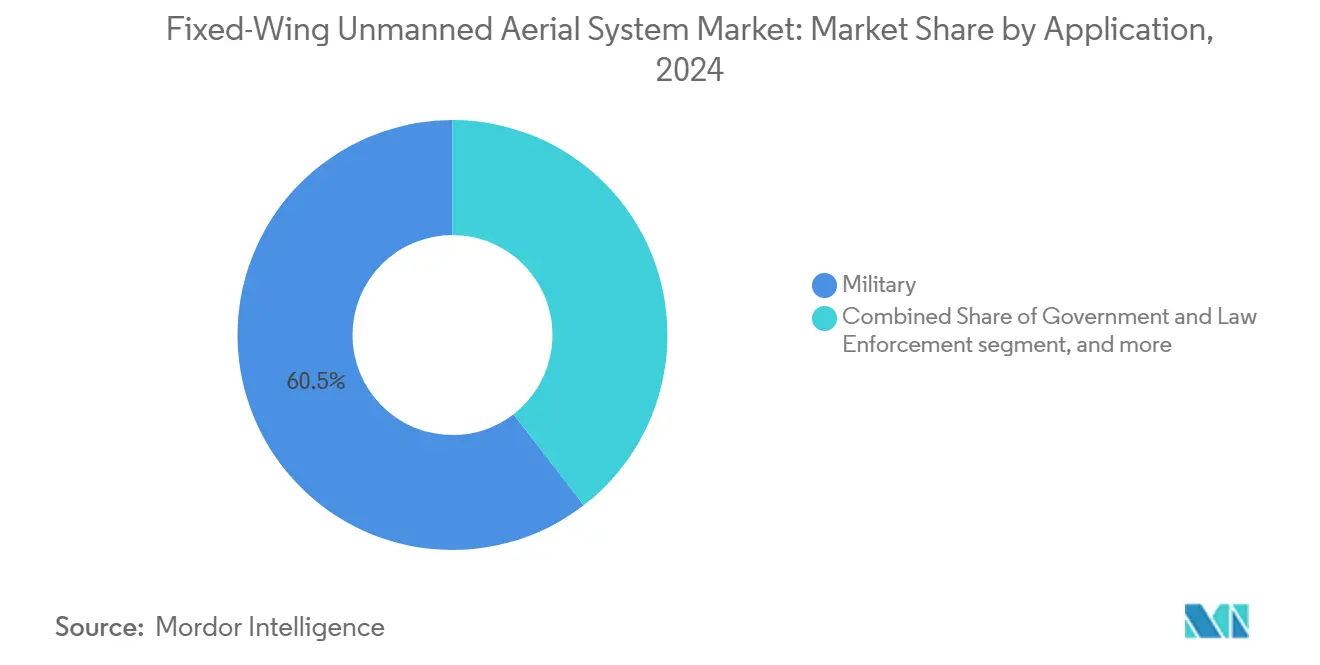

- By application, military operations accounted for a 60.45% share of the fixed-wing UAS market in 2024, while commercial uses are forecast to expand at a 13.50% CAGR through 2030.

- By mode of operation, remotely piloted platforms held 65.10% of the fixed-wing UAS market share in 2024; fully autonomous systems are expected to grow at a 14.55% CAGR to 2030.

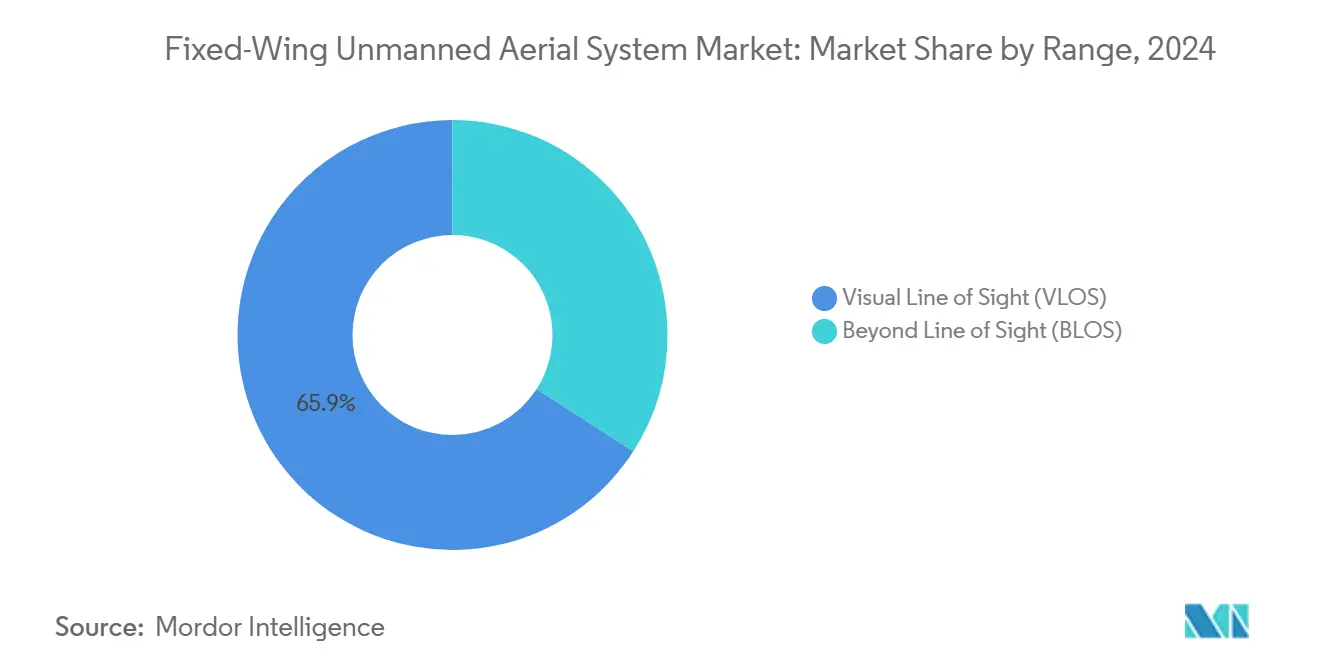

- By range, BVLOS flights represented 65.90% of the fixed-wing UAS market size in 2024, whereas VLOS missions will record the fastest 12.65% CAGR between 2025 and 2030.

- By MTOW, aircraft above 200 kg generated 55.87% of fixed-wing UAS market revenue in 2024; sub-25 kg platforms are projected to advance at 13.40% CAGR through 2030.

- By geography, North America commanded 34.50% of the fixed-wing UAS market size in 2024, while the Middle East and Africa region is poised for a 12.00% CAGR to 2030.

Global Fixed-Wing Unmanned Aerial System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging defense procurement amid geopolitics | 2.8% | Global, concentrated in NATO allies and Indo-Pacific | Short term (≤ 2 years) |

| Rapid commercial adoption for large-area mapping and logistics | 2.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Regulatory progress on BVLOS/type certification | 1.9% | Global, led by FAA and EASA frameworks | Medium term (2-4 years) |

| Hydrogen and hybrid fuel-cell propulsion breakthroughs | 1.2% | North America and EU, early adoption in defense | Long term (≥ 4 years) |

| High-altitude pseudo-satellite (HAPS) demand for 5G and EO | 0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| AI-enabled swarm autonomy increasing operator coverage | 0.5% | Global, defense-led with commercial spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Defense Procurement amid Geopolitics

Escalating geopolitical tension prompts record defense budgets and accelerated approval cycles for fixed-wing UAS, extending reconnaissance reach and delivering precision strikes without risking crews. The US allocated USD 10.12 billion to counter-UAS lines through 2029, directing nearly half of that to kinetic interceptors that complement long-endurance ISR platforms.[1]Source: Institute for Defense and Government Advancement, “The U.S. Counter-Unmanned Aerial Systems Market Report 2024-2029,” idga.com European allies are following suit; Greece inserted unmanned patrol aircraft into its 2025-2028 plan, and multiple NATO members now fund dual-use hydrogen demonstrators promising 20-hour station times. Taiwan’s unprecedented 100,000-unit procurement underscores the shift toward distributed swarms able to saturate contested airspace.[2]Source: Redwire Corporation, “Redwire Announces Acquisition of Edge Autonomy,” stocktitan.com Collectively, these programs create multi-year backlogs, boost tier-two supplier revenue, and stabilize investment in autonomy, command links, and anti-jamming payloads across surveillance and strike sets.

Rapid Commercial Adoption for Large-Area Mapping and Logistics

Commercial operators are pivoting to fixed-wing drones because superior lift-to-drag ratios translate into longer flight times, broader coverage, and lower cost per acre than multirotor craft. Rotor Technologies’ Sprayhawk treats 240 acres every hour with a 110-gallon tank, cutting crop-dusting cycles by 35% and demonstrating payload capacities once reserved for piloted aircraft. Beyond agriculture, utilities dispatch BVLOS patrols that log 300 km daily, replacing manned helicopters and reducing inspection budgets by 40%. FAA Section 44807 exemptions climbed 27% year over year, while EASA issued record SAIL III approvals, signaling regulator confidence in fixed-wing safety cases. Growing e-commerce pushes middle-mile delivery trials in Australia, Brazil, and Japan, attracting venture capital to hybrid-propulsion startups seeking scalable logistics corridors across remote and peri-urban regions.

Regulatory Progress on BVLOS/Type Certification

Global regulators converge on performance-based requirements that make routine BVLOS operations commercially viable. The FAA’s forthcoming Part 108 will codify detect-and-avoid thresholds, remote pilot training, and shielded-operations concepts, eliminating the need for labor-intensive waivers. Europe already employs EASA’s Design Verification Report route, enabling SAIL IV missions without full type certificates and cutting lead times to six months. Germany’s urban BVLOS authorization for the ZERC platform showcases confidence in redundant navigation, power, and command architectures. As insurance carriers embed DVR references into premium schedules, operators face lower risk pricing, while financiers clarify asset utilization rules. Harmonized frameworks pave the path for regional drone corridors, stimulating surveys, railway mapping, and offshore wind-farm monitoring in Europe and North America.

Hydrogen and Hybrid Fuel-Cell Propulsion Breakthroughs

Propulsion innovation is unlocking endurance and sustainability gains that favor fixed-wing airframes. Prototype 70-kg hydrogen fuel-cell stacks achieve 2.8 kW kg⁻¹ power density, doubling mission duration versus piston engines while eliminating lead-avgas maintenance cycles. Thales’ UAS100 hybrid demonstrator flew 600 km on nine kilograms of hydrogen, trimming lifecycle CO2 by 35% compared with avgas counterparts.[3]Source: Thales, “UAS100 Long-Range Surveillance Drone,” thalesgroup.com Defense evaluators see 15% mission-cost savings through reduced refueling infrastructure and lower acoustic signatures, which are valuable for covert ISR. Commercial fleet managers value the ability to service multi-field agriculture or mapping sorties without landing to swap batteries. Venture investment exceeds USD 900 million across North America and Europe, funding membrane advances, storage, and lightweight composite tanks to accelerate production readiness from 2026 onward for civilian operators globally.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent air-space integration and DAA requirements | -1.8% | Global, most restrictive in dense airspace regions | Medium term (2-4 years) |

| Supply-chain bottlenecks in composites and SiC/GaN electronics | -0.9% | Global, concentrated impact on high-tech components | Short term (≤ 2 years) |

| High acquisition/lifecycle costs of MALE/HALE platforms | -1.2% | Global, acute in cost-sensitive commercial markets | Short term (≤ 2 years) |

| Rising cyber and electronic warfare (EW) threats to UAV systems | -0.6% | Global, elevated in contested environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Air-Space Integration and DAA Requirements

Integrating fixed-wing drones into controlled airspace hinges on detect-and-avoid (DAA) performance equal to human see-and-avoid. Current multilayer suites combine active radar, ADS-B, LiDAR, and EO/IR sensors, adding 12–18% weight and 8–12% drag, eroding endurance margins and payload capacity. The Hong Kong SUPER demonstrator negotiated forested terrain at 45 mph without GPS, yet LiDAR computation consumed 22% of onboard power. Complexity inflates unit prices and certification timelines; many operators restrict sorties to Class G skies, limiting revenue. Harmonized standards remain under development, causing regional fragmentation and insurance uncertainty. Until low-size-weight-and-power chips and algorithmic certification frameworks mature, achieving economical BVLOS approval in dense terminal areas will remain the market’s most persistent brake for high-value logistics, passenger eVTOL handoffs, and urban mapping flights.

Supply-Chain Bottlenecks in Composites and SiC/GaN Electronics

Advanced composites and wide-bandgap semiconductors underpin airframe stiffness and power-conversion efficiency, yet both supply chains remain fragile. Military-grade carbon-fiber prepreg relies on precursor resins restricted by recent Chinese export controls, forcing Western primes to re-qualify alternative materials and elevating airframe cost by 18%. Lead times for silicon-carbide and gallium-nitride modules necessary for hybrid propulsion doubled to 26 weeks in 2024, delaying HALE block upgrades and complicating inventory forecasts. Smaller manufacturers lack volume leverage, absorbing spot-market surcharges that compress margins or push price increases downstream. Scarcity also slows certification, because every material substitution triggers new structural-test campaigns. Unless regional foundries and composite-tow plants scale quickly, component volatility will constrain rollout schedules and dampen revenue visibility for integrators across defense and commercial sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Military ISR Sustains Revenue Momentum

Military programs contributed 60.45% of the fixed-wing UAS market revenue in 2024. Defense allocations continue to anchor fixed-wing UAS spending, with ministries channeling multi-year funds toward medium-altitude. These long-endurance fleets deliver persistent maritime, border, and battlefield visibility. Workhorse airframes such as the MQ-9A Reaper and RQ-4 Global Hawk form the backbone of joint intelligence architectures, streaming real-time electro-optical, radar, and signals data to distributed operations centers. Procurement managers now specify open-system avionics, AI mission computers, and satellite-resilient datalinks that support rapid sensor swaps and seamless teaming with crewed aircraft. Meanwhile, serial production of loitering munitions like Helsing’s HX-2, which carries a 10 kg warhead 100 km and resists electronic attack, adds substantial unit volume and diversifies revenue across strike, suppression, and decoy missions for allied contingency operations worldwide over decades.

Commercial and public-service operators represent a smaller revenue base today, yet they outpace defense growth by embracing fixed-wing endurance advantages for mapping, inspection, and delivery tasks. The market expands at a 13.5% CAGR as farms, utilities, and parcel carriers shift from crewed aircraft to autonomous sorties capable of covering 400 km in one flight. FAA Category 3 approvals granted to Percepto in 2024 removed over-people restrictions for industrial sites, prompting chemical plants, solar farms, and refineries to schedule weekly BVLOS missions that cut inspection costs by 40%. Border forces in Australia, Greece, and Mexico adopt compact surveillance platforms for coastal interdiction, while Mediterranean navies test unmanned search grids. These non-military users validate dual-use payloads, create data analytics ecosystems, and attract sustained venture investment.

By Mode of Operation: Autonomy Converts the Installed Base

Remotely piloted aircraft dominate current deployments, commanding 65.10% market share because regulators still require human oversight for higher-risk sorties in populated or contested zones. Ground control stations provide triple-redundant Ku-band, LTE, and UHF links, letting crews reroute aircraft around pop-up airspace restrictions or unexpected weather systems within seconds. Mature military and commercial training pipelines supply certified operators, and modular console designs enable one crew to supervise multiple airframes when bandwidth allows. This man-in-the-loop paradigm supports time-sensitive targeting and humanitarian drops where ethical rules demand rapid judgment. Nevertheless, constant video streaming inflates operating costs, and encrypted links must evolve to counter increasingly sophisticated electronic-warfare jamming and cyber intrusion attempts from near-peer adversaries during dynamic and highly contested air campaigns.

Fully autonomous systems are projected to grow 14.55% annually, driven by edge processors that fuse LiDAR, radar, and computer-vision inputs without relying on high-latency datalinks. Retrofit guidance kits such as Auterion’s plug-and-play module upgrade legacy fleets to self-navigate, land on rough strips, and execute cooperative swarm behaviors for area search or saturation attack. The US Air Force validated the approach under AFWERX Autonomy Prime, demonstrating 80% design-to-build cycle reduction via digital twins and model-based certification. As regulators finalize machine-learning assurance frameworks and standardized failsafe logic, autonomous sorties will expand into wildfire monitoring, linear-asset inspection, and reconnaissance corridors where EW denies reliable communications. Lower crew costs and simplified logistics underpin compelling operator economics, driving faster worldwide uptake by 2030.

By Range: BVLOS Remains the Workhorse

BVLOS missions supplied 65.90% of the fixed-wing UAS market size in 2024. BVLOS flights dominate revenue because fixed-wing lift-to-drag ratios deliver multi-hour endurance crucial for patrolling pipelines, railways, and shipping lanes over sparsely populated regions. Operators routinely fly 300-km transects that, on a single fuel or battery cycle, something multirotor fleets cannot match without mid-route changes. Germany’s urban BVLOS waiver for the ZERC platform proved that redundant navigation hardware and detect-and-avoid logic can satisfy regulators even in complex airspace. Insurers now apply premium discounts when Design Verification Reports accompany risk assessments, reducing mission cost. Satellite-to-cellular hybrid modems will soon stream gigabit payload data, enabling near-real-time anomaly detection, precision geotagging, and predictive maintenance scheduling across energy corridors and transcontinental logistics routes as automated cloud analytics turn vast frames into instant operational insights for operators.

Though smaller today, VLOS operations are projected to advance 12.65% annually as compact, hand-launch aircraft empower agronomists, miners, and filmmakers to gather localized data efficiently. Foam-core wings bearing multispectral sensors capture crop vigor indices across 500-hectare fields in one pass, replacing ATV-mounted cameras and reducing fuel consumption. University programs leverage VLOS platforms to train pilots before progressing to BVLOS certifications, broadening the talent pipeline. Pending FAA Part 108 is expected to keep VLOS requirements simple, preserving a low-barrier entry for startups. Many enterprises will therefore field hybrid fleets of VLOS drones for spot checks and BVLOS craft for extended corridor surveillance, balancing cost, regulatory complexity, and mission duration while enabling incremental hardware upgrades that smoothly transition airframes to future autonomous beyond-visual missions seamlessly.

By MTOW: Heavy Airframes Capture Budget Outlays

Airframes above 200 kg capture 55.87% of market value because militaries, coast guards, and disaster-response agencies insist on large bays housing synthetic-aperture radar, communications relays, and electronic-intelligence suites. High-thrust diesel, turbine, or hybrid engines lift these platforms to altitudes exceeding 40,000 ft, affording regional coverage without aerial refueling. New coastal-patrol variants carry 400-lb sensor modules that stream fused intelligence to real-time command posts. Acquisition budgets cover lifecycle sustainment, hardened ground stations, and encrypted satellite links, justifying premium unit pricing. Fleet managers value podded payload modularity, rotating between ISR, signals, and communications roles as priorities shift during multi-year deployments, maximizing asset utilization and capital efficiency across diversified mission sets while facilitating future hybrid-fuel retrofits that extend sortie duration and range.

Sub-25 kg craft is the fastest-growing category, projected at 13.40% CAGR, propelled by lenient regulations and breakthroughs in lightweight materials. Flexible solar sheets weighing one-fourth of the total mass recharge lithium-sulfur (Li-S) packs during flight, stretching endurance for environmental monitoring, wildlife counts, and small-parcel delivery missions. Midweight 25–200 kg platforms fill niche utility roles; Rotor Technologies’ Airtruck, with 2,500 lb MTOW and 1,000-lb payload, delivers construction supplies and island-hop cargo where helicopters are cost-prohibitive. Together, lighter classes foster entrepreneurial entry, diversify mission profiles, and push component suppliers to miniaturize hydrogen fuel-cells, gallium-nitride inverters, and advanced composites, driving economies of scale that will eventually spill over into heavier defense-grade platforms, enhancing global supply-chain resilience and broadening technology access for emerging civil operators worldwide.

Geography Analysis

North America generated 34.50% of the fixed-wing UAS market size in 2024, due to the US’s USD 886 billion defense budget and early FAA performance-based rulemaking. Canada’s Industrial & Technological Benefits policy promotes domestic avionics suppliers through offset agreements with prime contractors. Regulatory transparency encourages commercial trials; utilities in Texas operate weekly BVLOS patrols of 2,000-mile transmission corridors, cutting helicopter charter hours by 45%.

Europe ranks second, benefitting from EASA’s harmonized DVR process and multinational defense collaboration. Germany’s Bundeswehr ordered additional EURO-MALE airframes, while France advanced its hydrogen UAV demonstrator under the HEMERA program. Commercial adoption is snowballing: Spain’s national rail administrator completed the first 350 km BVLOS track inspection using a hybrid-electric craft certified under SAIL III provisions.

Although smaller today, the Middle East and Africa region will post the fastest 12% CAGR through 2030 as governments invest in border security and critical infrastructure surveillance. Egypt finalized a coastal ISR contract for medium-altitude systems with 24-hour endurance, and South Africa designated three unmanned corridors for humanitarian cargo pilots. Vast desert expanses and limited legacy infrastructure favor fixed-wing efficiency.

Competitive Landscape

The market is moderately concentrated. The key players hold a strong market position, while a second tier of agile specialists scales innovative propulsion and autonomy stacks. Established primes The Boeing Company, Lockheed Martin Corporation, and Northrop Grumman Corporation leverage program-of-record incumbency and broad sustainment networks. They increasingly acquire niche capabilities rather than design in-house; Airbus’ purchase of Aerovel integrates rotary-wing launch/recovery know-how for shipborne ISR fleets.

Pure-play UAV manufacturers capitalize on shorter innovation cycles. General Atomics added a hydrogen demonstrator wing to its SkyGuardian line, promising 30-hour endurance without mid-sortie refuel. Tekever raised USD 300 million in Series B funding, reaching a USD 1.33 billion valuation and scaling West Wales Airport production for AR3 16-hour endurance platforms. Edge Autonomy’s Stalker and Penguin portfolios extend reach via Redwire’s USD 925 million acquisition, combining ISR airframes with space-based downlink infrastructure.

Technology disruptors pivot around autonomy. Helsing’s Resilience Factory achieves 1,000 HX-2 strike drones monthly, embedding neural network target recognition on-board to reduce latency. Start-ups in Silicon Valley and Tel-Aviv refine swarm-mesh comms that maintain encrypted links across 20 shipborne assets, a capability the US Navy is evaluating for distributed maritime ops.

Fixed-Wing Unmanned Aerial System Industry Leaders

Northrop Grumman Corporation

General Atomics

The Boeing Company

AeroVironment, Inc.

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Karshak Drones launched SHARK HAWK, a fixed-wing VTOL drone that combines autonomous operation with VTOL capabilities. The drone features a 2.55-meter wingspan, CubePilot flight controller, and carbon-glass composite airframe, enabling operation without runways in remote areas.

- February 2025: The Kalashnikov Concern introduced its SKAT 350M multifunctional UAV to the Middle East market. Designed for reconnaissance and ground operation support, it performs efficiently in extreme weather and wide temperature ranges. With a four-hour flight capability, it is durable, reliable, and proven effective through its deployment in the SMO zone.

Global Fixed-Wing Unmanned Aerial System Market Report Scope

| Military | Intelligence, Surveillance and Reconnaissance (ISR) |

| Combat Operations | |

| Others | |

| Government and Law Enforcement | Border Management |

| Maritime Security | |

| Others | |

| Commercial | Inspection and Monitoring |

| Delivery and Logistics | |

| Agriculture | |

| Surveying and Mapping | |

| Others |

| Remotely Piloted |

| Fully Autonomous |

| Visual Line of Sight (VLOS) |

| Beyond Line of Sight (BLOS) |

| Less than 25 Kg |

| 25 to 200 Kg |

| More than 200 Kg |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Military | Intelligence, Surveillance and Reconnaissance (ISR) | |

| Combat Operations | |||

| Others | |||

| Government and Law Enforcement | Border Management | ||

| Maritime Security | |||

| Others | |||

| Commercial | Inspection and Monitoring | ||

| Delivery and Logistics | |||

| Agriculture | |||

| Surveying and Mapping | |||

| Others | |||

| By Mode of Operation | Remotely Piloted | ||

| Fully Autonomous | |||

| By Range | Visual Line of Sight (VLOS) | ||

| Beyond Line of Sight (BLOS) | |||

| By MTOW | Less than 25 Kg | ||

| 25 to 200 Kg | |||

| More than 200 Kg | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 valuation of the fixed-wing unmanned aerial system market?

The fixed-wing UAS market stands at USD 13.83 billion, with a projected rise to USD 21.71 billion by 2030, reflecting a 9.44% CAGR over the forecast period.

Which segment is forecast to grow fastest through 2030?

Fully autonomous platforms will expand at a 14.55% CAGR as AI guidance kits retrofit the installed base.

Which region leads current revenue?

North America holds 34.50% of 2024 revenue due to high defense outlays and early BVLOS regulation.

How large is the military share today?

Military programs represent 60.45% of 2024 revenue, driven by ISR and loitering-munition demand.

What propulsion innovation is reshaping endurance?

Hydrogen and hybrid fuel-cell systems extend MALE endurance to 30 hours, cutting mission costs by 15%.

Page last updated on: