Multirotor Unmanned Aerial Systems (UAS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

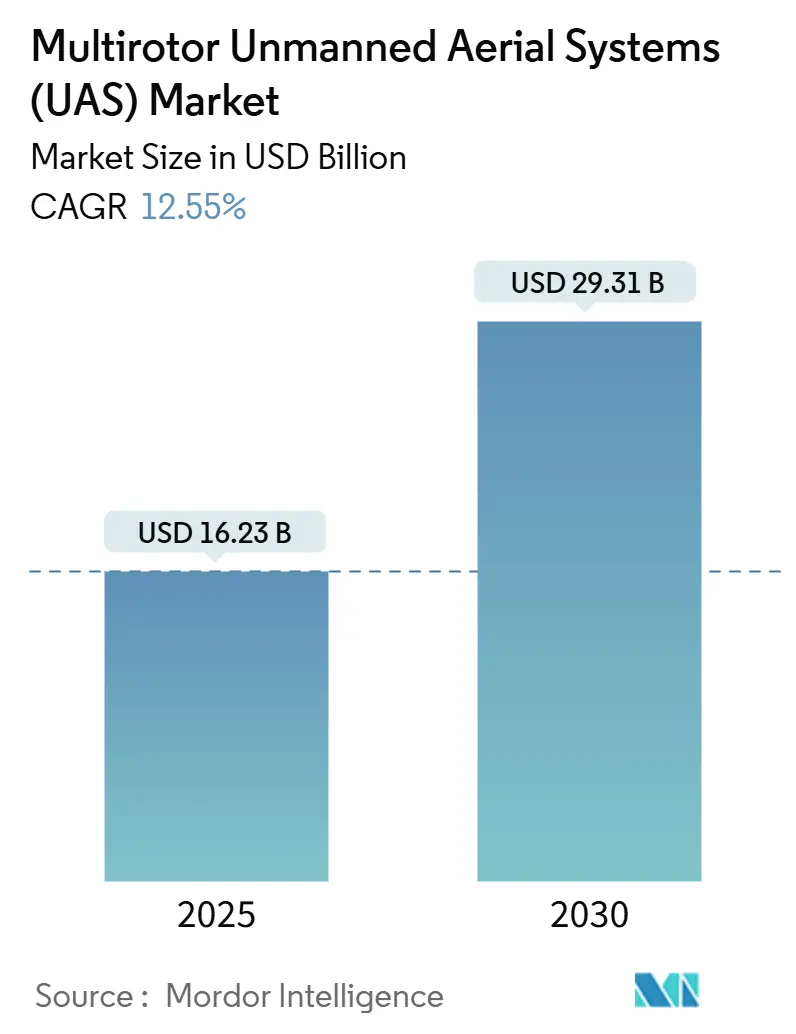

| Market Size (2025) | USD 16.23 Billion |

| Market Size (2030) | USD 29.31 Billion |

| Growth Rate (2025 - 2030) | 12.55% CAGR |

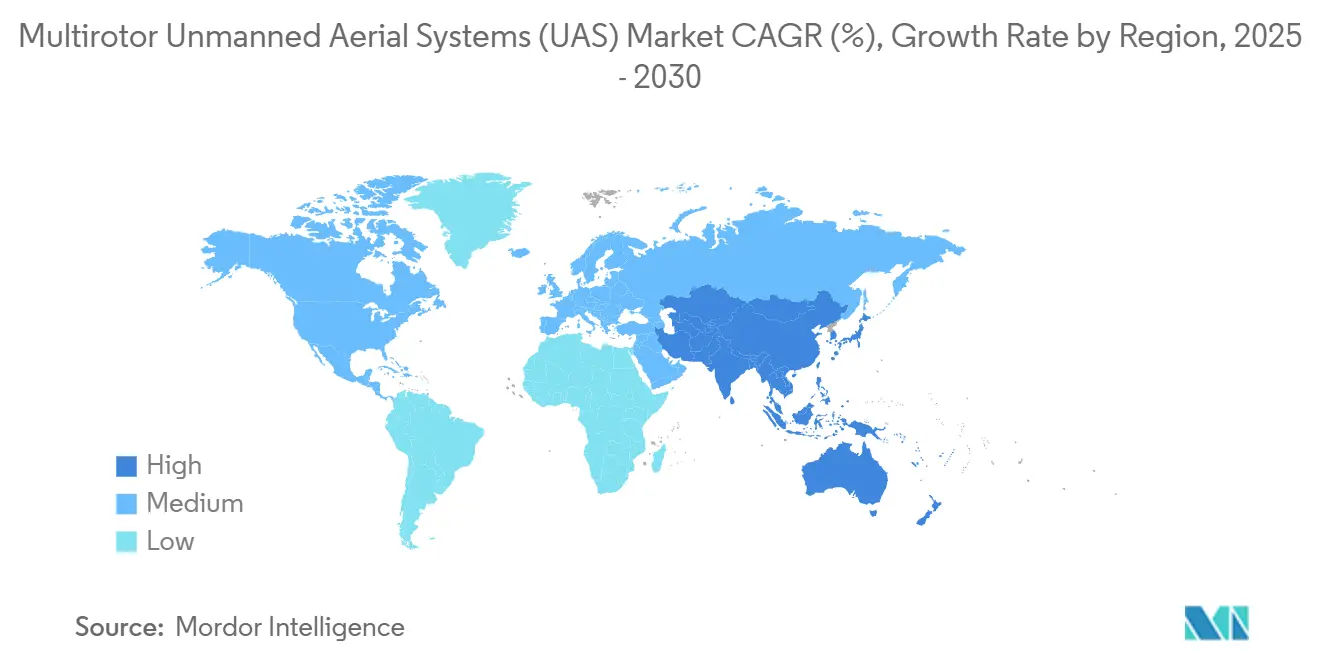

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multirotor Unmanned Aerial Systems (UAS) Market Analysis by Mordor Intelligence

The multirotor unmanned aerial systems (UAS) market size stood at USD 16.23 billion in 2025 and is projected to reach USD 29.31 billion by 2030, advancing at a 12.55% CAGR during the forecast period. Rapid gains in lithium-ion energy density, edge-AI autopilot sophistication, and the steady rollout of beyond-visual-line-of-sight (BVLOS) rules combine to reposition multirotors as essential infrastructure across commercial, industrial, and defense settings. Quadcopters remain the volume leader, yet octocopters and larger configurations are drawing investment because enterprises want heavier payloads and in-flight redundancy for risk-sensitive missions. Global demand tilts toward real-time aerial data streams that drop directly into enterprise software stacks, accelerating orders for integrated sensor suites and cloud-connected flight-management platforms. At the same time, sanctions-driven supply-chain reforms are pushing manufacturers to onshore key electronics, which is reshaping cost structures and competitive strategy.

Key Report Takeaways

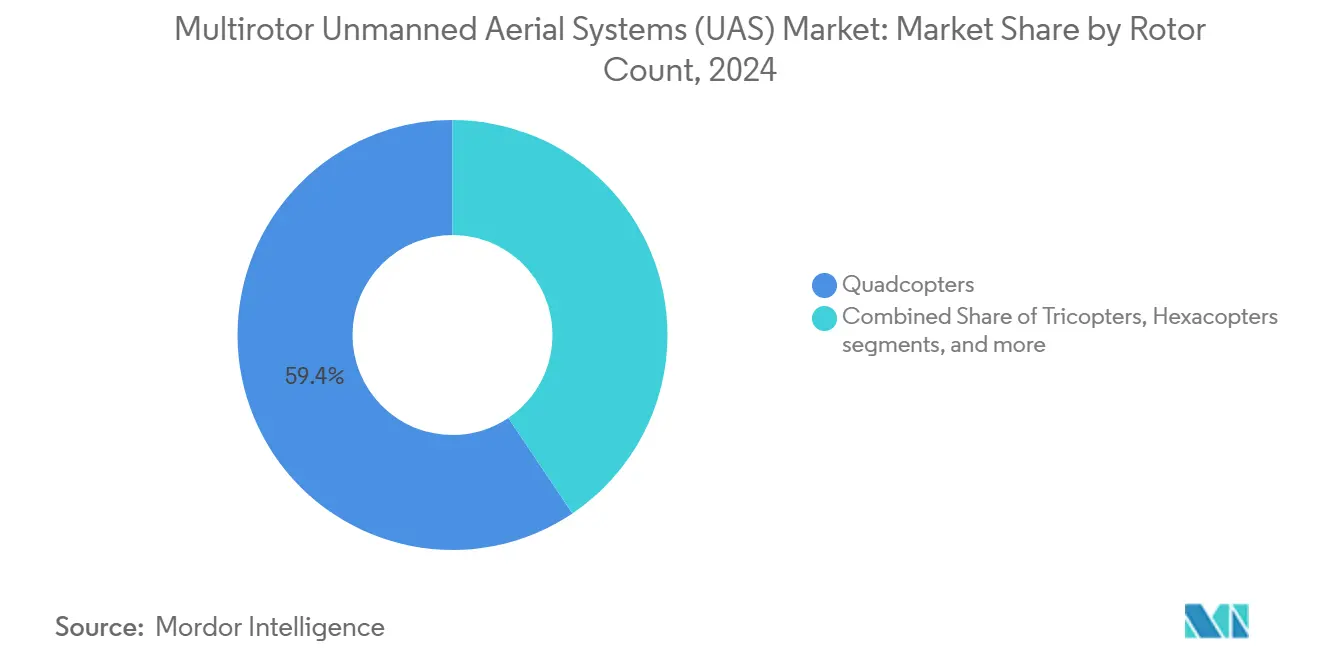

- By rotor count, quadcopters held 59.42% revenue share in 2024, while octocopters and larger systems are expanding at an 18.88% CAGR through 2030.

- By application, surveillance accounted for 31.67% of 2024 revenue; delivery and logistics are forecasted to post a 22.81% CAGR to 2030.

- By end-user industry, commercial and industrial enterprises led with a 43.78% share in 2024, whereas defense and homeland security spending is growing at a 20.81% CAGR.

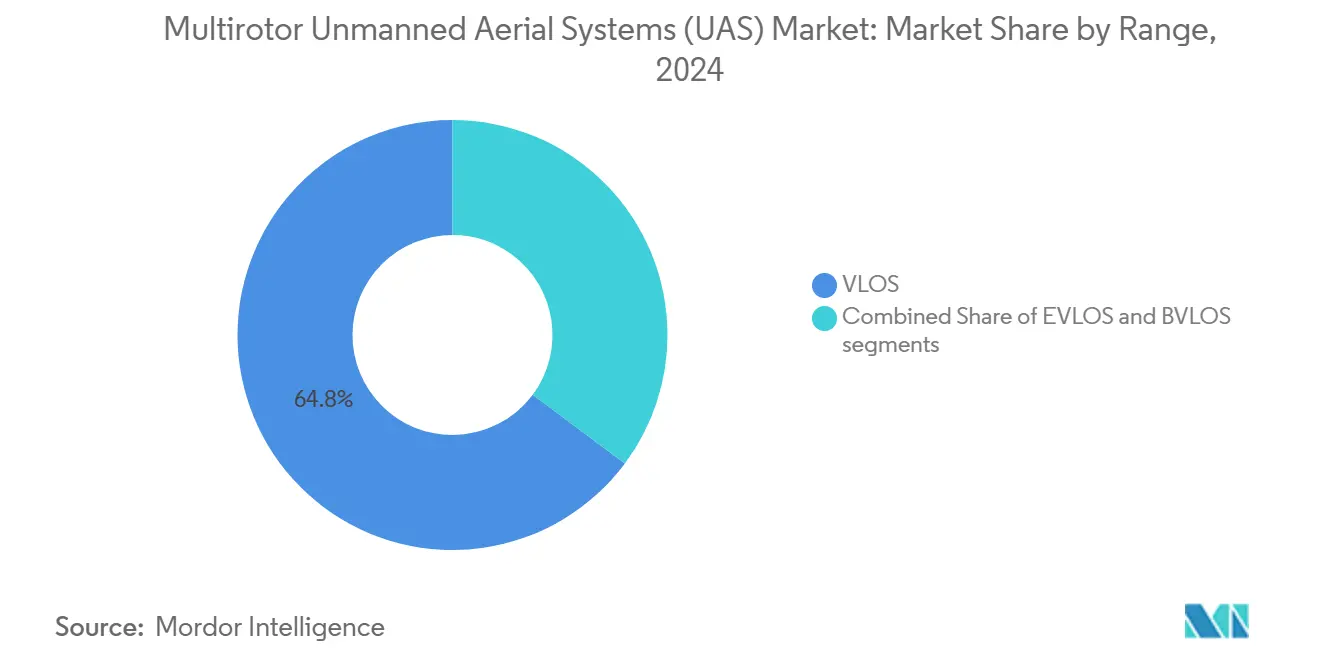

- By range, VLOS operations represented 64.81% of flights in 2024, yet BVLOS missions are advancing at a 19.45% CAGR.

- By payload, sensor packages captured a 39.55% share in 2024, and EW payloads are registering a 24.82% CAGR through 2030.

- By geography, North America dominated with 42.45% revenue share in 2024, while Asia-Pacific is forecasted to log the fastest 20.11% CAGR to 2030.

Global Multirotor Unmanned Aerial Systems (UAS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cross-industry demand for real-time aerial data | +3.20% | North America, EU, global spillover | Medium term (2-4 years) |

| Precision-agriculture ROI from rotary-wing spray drones | +2.80% | Asia-Pacific core, Latin America spillover | Short term (≤ 2 years) |

| Defense shift to low-cost ISR and loitering multirotors | +2.10% | North America, EU, Middle East | Long term (≥ 4 years) |

| Battery-energy-density gains unlock heavier payloads | +1.90% | Global | Medium term (2-4 years) |

| Edge-AI autopilots enabling BVLOS approvals | +1.70% | North America, EU | Long term (≥ 4 years) |

| Swarm-as-a-service business models for security events | +1.40% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cross-Industry Demand for Real-Time Aerial Data

Utilities confirmed 40% cost savings in 2024 after substituting helicopters with multirotors for transmission-line inspections, showing how the multirotor UAS market can immediately trim OPEX.[1]IEEE Transactions on Power Delivery, “Drone Inspection Cost Reduction,” ieee.org Fifth-generation cellular networks stream high-definition video to cloud-AI dashboards in seconds, allowing field crews to close maintenance work orders on the same day. Insurers are writing policies that require drone-based risk surveys, effectively mandating adoption for large commercial real-estate portfolios. Manufacturers rely on thermal-imaging multirotors to flag overheated machinery before failure, embedding drones into predictive-maintenance loops. As a result, enterprises now budget for fleets and software licenses under core operations line items rather than R&D headings, signaling that procurement behavior has moved past experimentation.

Precision-Agriculture ROI from Rotary-Wing Spray Drones

Agricultural operators documented 30–35% reductions in agro-chemical use when shifting to variable-rate multirotor spraying in 2024, yet maintained baseline yields.[2]Wiley Editors, “Precision Agricultural Drones,” onlinelibrary.wiley.com National regulators in China, India, and Brazil now certify drone-applied chemicals at parity with tractor boom sprayers, cutting procedural delays that once grounded pesticide flights. Farm-services firms run subscription fleets that let smallholders order acreage-based spraying on demand, widening the addressable market. Autonomous battery-swap stations enable a single pilot to manage multiple aircraft, which slashes labor costs in labor-scarce rural zones. Combining chemical savings and higher labor productivity delivers sub-18-month payback periods, a threshold that unlocks bank financing for equipment leases across emerging-market farms.

Defense Shift to Low-Cost ISR and Loitering Multirotor

Attritable multirotors are rewriting defense aviation economics because commanders accept mission success without platform recovery.[3]Defense One Staff, “Attritable Drone Strategies,” defenseone.com Battlefront footage from Ukraine showed off-the-shelf quadcopters modified with thermal cameras performing night ISR at a fraction of the hourly cost of manned aircraft. Integrating digital radio jammers converts standard frames into focused electronic-warfare nodes that blind adversary GPS links. Swarm-planning software synchronizes dozens of airframes, producing blanket reconnaissance coverage even if several are lost. Defense ministries, therefore, insert multirotor squadrons into force-modernization roadmaps, often using rapid contracting paths that bypass decade-long fighter-jet procurement cycles.

Battery-Energy-Density Gains Unlock Heavier Payloads

NMC 811 cells jumped from 280 Wh/kg to roughly 350 Wh/kg between 2024 and 2025, lifting average multirotor endurance by 22% on identical payloads. Prototype solid-state packs nearing 400 Wh/kg are undergoing certification trials for pipeline-inspection drones that once required gas-electric hybrids. Field data show hybrid battery-fuel-cell stacks stretching flight times to 150 minutes under 5 kg payloads, opening cross-border power-line inspection missions that once defaulted to helicopters. Engineers now bundle micro-radiators into battery bays, stabilizing cell temperatures from −20 °C to 55 °C to satisfy Arctic resource firms and Gulf-state utilities. Larger energy budgets create capacity headroom for multi-spectral and LiDAR combinations that improve data quality without upping sortie counts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented global air traffic and counter-UAS rules | -2.30% | EU, Asia, global impact | Long term (≥ 4 years) |

| Cell-chemistry supply bottlenecks for Li-ion packs | -1.80% | North America acutely, global spillover | Short term (≤ 2 years) |

| RF-spectrum congestion impacting C2 links | -1.50% | Global, severe in dense urban areas | Medium term (2-4 years) |

| Insurance-premium spikes after urban crash incidents | -1.20% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Air-Traffic and Counter-UAS Rules

Operators planning cross-border drone service networks face an alphabet soup of certification forms, air-risk assessments, and remote-ID hardware specifications that shift by jurisdiction.[4]International Civil Aviation Organization, “Global UAV Regulation Map,” icao.int Facilities near critical infrastructure must coordinate with multiple agencies, sometimes receiving contradictory NOTAM directives that force mission cancellations. Insurance actuaries inflate premiums when legal liability is opaque, eroding the ROI calculus that otherwise favors BVLOS operations. Disparate counter-UAS laws mean authorities can mandate immediate landings without unified digital protocols, inserting operational uncertainty. Harmonization talks proceed slowly because national security agencies guard sovereign airspace privileges, suggesting the restraint will linger through the decade.

Cell-Chemistry Supply Bottlenecks for Li-Ion Packs

Lithium carbonate (Li2CO3) spot prices spiked 61% in early 2025 on South American export curbs, squeezing battery-pack margins for mid-tier airframe builders. Cobalt supply tightened after political unrest disrupted Congolese mines, and buyers pivoted to nickel-rich chemistries that require new production tooling. Asian cell plants hit COVID-related shutdowns, delaying shipments into US ports by as much as 10 weeks. Smaller drone companies lacked volume to secure priority allocations, forcing expensive spot-buy deals or redesigns around off-spec cells that underperformed in cold weather. These shocks slowed rollouts of new multirotor models, especially in agriculture, where seasonal spraying windows are unforgiving.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rotor Count: Quadcopters Hold Volume Leadership Yet Redundancy Drives Growth

Quadcopters commanded 59.42% of the multirotor UAS market share in 2024, thanks to simple four-motor architectures, low bill-of-materials costs, and mature flight-controller ecosystems.[5] IEEE Robotics and Automation Letters, “Quadcopter Market Dynamics,” ieee.org Enterprise buyers favor quads for short-haul visual inspection routes where lightweight optical sensors suffice. However, the multirotor UAS market size tied to octocopters and heavier platforms is forecast to climb at 18.88% CAGR through 2030 as utilities, defense agencies, and logistics carriers demand lift capacity for payloads above 20 kg. Robust eight-motor or twelve-motor layouts deliver motor-out fault tolerance that regulators increasingly require for operations over people. In 2025, large-coil wind-farm inspections began shifting to hexacopters because losing one motor no longer ends the mission.

Higher rotor counts also unlock multi-sensor stacks—thermal, LiDAR, high-zoom EO—that exceed typical quadcopter payload ceilings. Engineering advances have trimmed the power penalty once associated with more rotors, using carbon-fiber props and field-oriented motor controllers that boost efficiency. Insurance underwriters factor in redundancy when pricing coverage, which narrows the premium differential versus quadcopters. Component suppliers now mass-produce eight-in-one ESC boards, cutting assembly labor for octocopter builders. These cost and reliability trends explain why octocopters headline procurement tenders for bridge-deck scanning, offshore rig inspection, and heavy-lift logistics in disaster zones.

By Application: Surveillance Maintains Lead While Delivery Accelerates

Surveillance generated the most significant revenue slice at 31.67% in 2024, anchored by law-enforcement patrols, border-security overwatch, and infrastructure perimeter monitoring. Real-time object-detection analytics transform introductory video feeds into actionable alerts, enabling a single officer to triage incidents across multiple zones. Municipal agencies cite a 15% cut in patrol vehicle mileage after shifting routine checks to quadcopters outfitted with 30× zoom cameras. Delivery and logistics, meanwhile, posted a 22.81% CAGR and are set to eclipse mapping revenues by 2027 as BVLOS waivers proliferate. Retailers pilot same-day drone drops within 10 km radii, shaving two hours off curbside delivery windows during peak demand periods.

Emergency-response agencies blend infrared sensors and loudspeakers to locate and direct wildfire evacuees, showing cross-pollination between surveillance and public-safety missions. Construction-site mapping remains a durable mid-tier application, feeding progress-tracking dashboards that automate payment milestones. Film and broadcast segments decelerated because affordable consumer drones saturated hobbyist cinematography, though niche growth continues in live sports coverage. Multispectral crop-health scans now layer into agronomic decision support, but the volume expansion lies in fully autonomous chemical application flights. Over the forecast, integrated payload bays that toggle between camera, speaker, and delivery box will increase platform utilization rates, amplifying ROI for fleet operators.

By End-User Industry: Enterprises Cement Lead, Defense Budgets Accelerate

Commercial and industrial enterprises controlled 43.78% of 2024 revenue, underscoring the transition from pilot projects to embedded workflows inside utilities, insurance, telecom, and energy verticals. CEOs green-lit multi-year fleet programs once internal audits verified maintenance and inspection savings exceeded deployment costs within two fiscal years. The defense segment is forecast to grow at a 20.81% CAGR due to attractive ISR and EW procurements prioritizing swarming tactics. Federal contracts for loitering quadcopters stipulate US-sourced components, prompting the reshoring of PCB assemblies and secure-link radios. Recreational demand plateaued because regulatory caps on flight ceilings and mandatory remote-ID modules raised entry barriers for hobbyists.

Insurance underwriters emerged as power users, dispatching drones to validate roof conditions before issuing commercial property cover, compressing claims cycles by 70% versus ladder inspections. Mining companies use heavy-lift hexacopters to haul core samples from pit floors to labs, shortening assay turnaround from days to hours. Compliance frameworks such as ISO 21384 spur consistent training and maintenance records, a prerequisite for enterprise-wide scaling. Together, these dynamics lock the multirotor UAS industry into mainstream operational budgets rather than discretionary tech spending.

By Range: VLOS Dominates but BVLOS Scaling Up

Visual-line-of-sight sorties accounted for 64.81% of commercial flights in 2024 because most jurisdictions still restrict uncrewed craft beyond the pilot’s eyesight. However, the multirotor UAS market size attached to BVLOS missions is projected to rise at a 19.45% CAGR as detect-and-avoid radars, redundant command links, and real-time traffic-management integrations clear regulatory hurdles. Utilities lead early adoption because transmission corridors often lack ground obstacles, easing safety-case preparation. Extended VLOS, where observers hand off the aircraft along linear routes, serves as a stepping-stone for pipeline and railway operators seeking incremental range.

Cellular-LTE and emerging 5G NTN satellite links now blanket many rural zones, providing the low-latency control paths BVLOS requires. Regulators accept automated contingency-landing protocols that trigger when links degrade below threshold, assuaging public-safety concerns. Urban BVLOS will likely lag until unmanned traffic management (UTM) grids mature, but suburban delivery corridors already launch daily flights. Each incremental waiver embeds operational data that shortens subsequent approval cycles, reinforcing the feedback loop that expands BVLOS revenue opportunities inside the broader multirotor UAS market.

By Payload: Sensors Rule, Electronic Warfare Surges

Sensor suites held 39.55% revenue share in 2024, with thermal, multispectral, and LiDAR modules leading orders for inspection, mapping, and agricultural analytics. The multirotor UAS market size tied to electronic-warfare payloads is set for a 24.82% CAGR because defense buyers seek GPS-jamming and communications-denial kits that can ride on cost-effective quadcopters. Optical zoom cameras now ship with AI edge chips that auto-label anomalies, trimming post-flight analytics labor. LiDAR units dropped below USD 8,000 in 2025, broadening adoption for crack detection on bridges and dams. Swappable bay designs allow operators to flip between imaging and RF payloads within minutes, maximizing fleet utilization.

Miniaturized synthetic-aperture radar emerges as the next payload frontier because it penetrates foliage and smoke, essential for wildfire and search missions. Self-contained radios relay data through meshed drone-to-drone hops, extending range without ground repeaters. Defense ministries validate that disposable quadcopters carrying 300 g jammers can neutralize million-dollar missile batteries, a cost-exchange that shifts procurement math. In civil markets, telecom firms position portable LTE pod payloads above disaster zones to restore connectivity, illustrating how payload diversification multiplies addressable use cases.

Geography Analysis

North America maintained 42.45% revenue dominance in 2024 as FAA Part 108 standardized pilot certification, remote-ID, and low-altitude traffic-management interfaces. State agencies accelerated bridge and road inspections via quadcopters, generating fleet contracts that cascade through regional resellers. The US Department of Defense (DoD) spending on ISR and EW drones further concentrates demand, while venture-backed startups exploit a mature capital ecosystem to commercialize edge-AI navigation systems. Original-equipment manufacturers (OEMs) benefit from well-developed aerospace supply chains that absorb inflationary shocks better than offshore rivals.

Asia-Pacific is projected to record the fastest 20.11% CAGR as lower manufacturing costs and expanding agricultural modernization drive bulk orders.[6]Reuters Correspondents, “Asia-Pacific Drone Growth,” reuters.com China channels provincial subsidies into precision-spray operations, lifting annual quadcopter shipments past 120,000 units in 2025. India pilots federal-level crop-insurance programs that reimburse farmers using drone-derived yield data, stimulating fleet rentals for smallholders. Southeast Asian utilities mandate aerial inspections of transmission towers after typhoons, a policy that translates into predictable call-outs for service providers. With regional dominance in lithium-ion (Li-ion) cell production, Asia-Pacific suppliers offer bundled airframe-battery packages that compress lead times for domestic and export customers.

Europe represents a high-regulation but high-value opportunity because EASA achieved pan-EU rules, yet member-state nuances complicate cross-border operations. Environmental directives steer investment toward emissions monitoring, while stringent privacy laws add compliance costs for surveillance flights. Defense ministries allocate modernization budgets for low-signature ISR drones suited to urban peacekeeping missions. Eastern European border-security requirements have accelerated orders for loitering multirotors with EW payloads. For commercial fleets, GDPR drives demand for onboard encryption and local data processing, prompting suppliers to push AI inference models to the edge.

Competitive Landscape

The multirotor UAS market features moderate concentration because the top five vendors control a significant share of global sales, leaving ample room for regional specialists. Legacy aerospace primes leverage certification expertise to dominate defense orders, yet consumer-electronics-trained firms like DJI pioneer rapid hardware iterations that resonate with enterprise buyers seeking cost-effective platforms. Supply-chain shocks and geopolitical scrutiny over Chinese electronics persuaded Western brands to vertically integrate key flight-controller and radio-frequency (RF) modules in 2025. Leading vendors now purchase chip-design houses and battery-pack assemblers to secure IP ownership and mitigate export-control risk.

Software has overtaken airframe geometry as the primary differentiation lever. Autonomy stacks ingest sensor fusion data to run onboard route re-planning, while cloud APIs feed enterprise resource-planning suites for automated work-order creation. Subscription pricing models convert once-off hardware sales into recurring revenue, aligning with CFO preferences for operational expenditure outlays. Drone-as-a-service startups win contracts by bundling aircraft, pilots, data analytics, and maintenance under per-flight-hour pricing, eroding the incumbents’ hardware margin advantage. Meanwhile, insurers assess reliability metrics from real-world flight logs, favoring platforms with granular health-monitoring telemetry.

Mergers and acquisitions intensified; DDC–Volatus created a North American service giant, while Patria’s Nordic Drones buyout embedded specialized rotor-craft R&D inside a defense portfolio. Capital markets remain enthusiastic: Skydio’s USD 170 million Series E and DeltaQuad’s EUR 42.60 million (USD 49.95 million) Series B highlight investor confidence in software-heavy autonomy strategies. Sanctions on select Chinese drone makers redirect purchase orders to US and European alternatives, yet those suppliers face scale-up challenges amid battery-cell shortages. Competitive advantage rests on balancing secure supply chains, AI-rich autonomy, and service-based revenue streams.

Multirotor Unmanned Aerial Systems (UAS) Industry Leaders

SZ DJI Technology Co., Ltd.

AeroVironment, Inc.

Autel Robotics Co., Ltd.

Skydio, Inc.

Yuneec International (Advanced Technology Labs AG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Patria and Swedish company ACC Innovation agreed to jointly develop a military variant of the Thunder Wasp GT quadcopter drone for a NATO member country.

- January 2025: Performance Drone Works (PDW) secured USD 15.3 million in contracts from the US Army to deliver its C100 quadcopter, a Group 2 Small Uncrewed Aircraft System (sUAS), supporting the Army's 'Transformation in Contact' initiative.

- October 2024: The Royal Australian Navy contracted Red Cat Holdings to supply 12 FlightWave Edge 130 Blue military-grade tricopters.

- January 2024: The UAE-based Edge Group signed a contract with the country's Ministry of Defence (MoD) to supply 200 HT-100 and HT-750 unmanned helicopters.

Global Multirotor Unmanned Aerial Systems (UAS) Market Report Scope

| Tricopters |

| Quadcopters |

| Hexacopters |

| Octocopters and Others |

| Surveillance |

| Mapping and Surveying |

| Aerial Photography and Cinematography |

| Delivery and Logistics |

| Precision Agriculture |

| Emergency and Disaster Response |

| Defense and Homeland Security |

| Commercial and Industrial Enterprises |

| Consumer/Recreational |

| Visual Line of Sight (VLOS) |

| Extended Visual Line of Sight (EVLOS) |

| Beyond Visual Line of Sight (BVLOS) |

| Imaging and Mapping Systems |

| Sensors |

| Communications and Datalinks |

| Electronic Warfare (EW) Systems |

| Other Payload Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Rotor Count | Tricopters | ||

| Quadcopters | |||

| Hexacopters | |||

| Octocopters and Others | |||

| By Application | Surveillance | ||

| Mapping and Surveying | |||

| Aerial Photography and Cinematography | |||

| Delivery and Logistics | |||

| Precision Agriculture | |||

| Emergency and Disaster Response | |||

| By End-User Industry | Defense and Homeland Security | ||

| Commercial and Industrial Enterprises | |||

| Consumer/Recreational | |||

| By Range | Visual Line of Sight (VLOS) | ||

| Extended Visual Line of Sight (EVLOS) | |||

| Beyond Visual Line of Sight (BVLOS) | |||

| By Payload | Imaging and Mapping Systems | ||

| Sensors | |||

| Communications and Datalinks | |||

| Electronic Warfare (EW) Systems | |||

| Other Payload Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the multirotor unmanned aerial systems market and how fast will revenue expand to 2030?

The multirotor UAS market was valued at USD 16.227 billion in 2025 and is projected to reach USD 29.31 billion by 2030, reflecting a 12.55% CAGR.

Which rotor configuration currently accounts for the largest share of global shipments?

Quadcopters lead, holding 59.42% of 2024 revenue.

Which mission type is projected to record the fastest revenue growth by 2030?

Delivery and logistics flights are forecast to post a 22.81% CAGR.

Which geographic region shows the most rapid growth outlook through 2030?

Asia-Pacific is projected to expand at a 20.11% CAGR.

Which payload category is accelerating quickest within defense procurement?

EW payloads are advancing at a 24.82% CAGR.

What key regulatory barrier most heavily suppresses long-term growth?

Fragmented global air-traffic and counter-UAS rules are estimated to cut the overall CAGR by 2.3%.

Page last updated on: