Americas Fighter Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

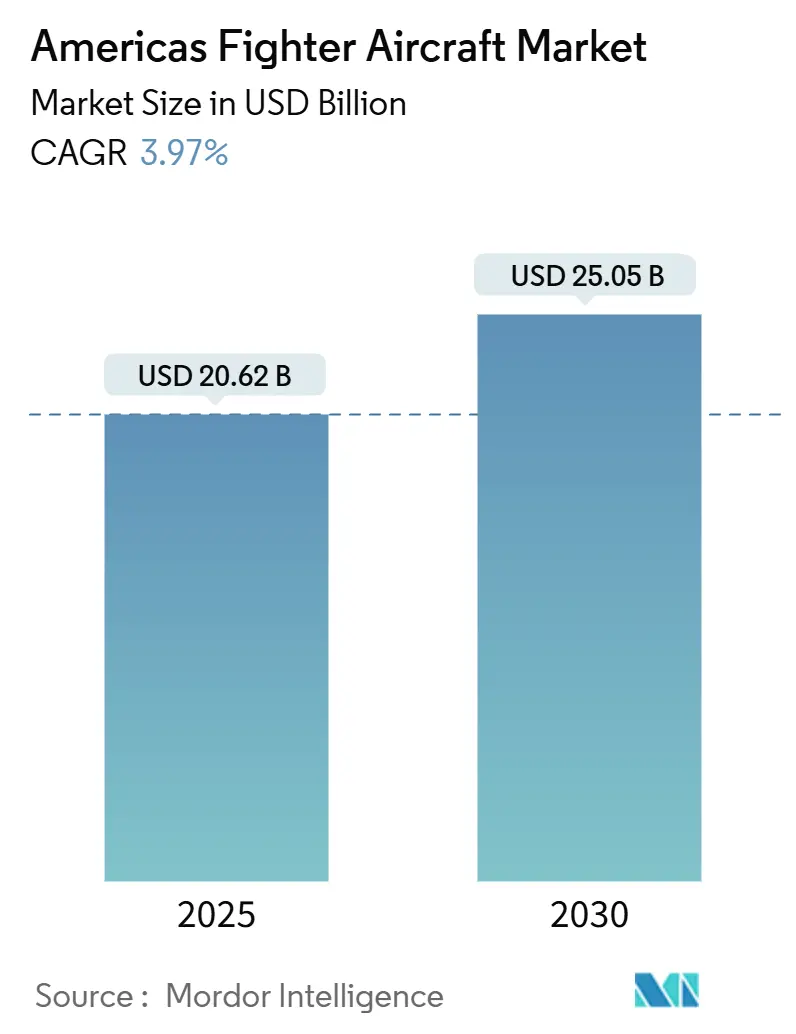

| Market Size (2025) | USD 20.62 Billion |

| Market Size (2030) | USD 25.05 Billion |

| Growth Rate (2025 - 2030) | 3.97% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

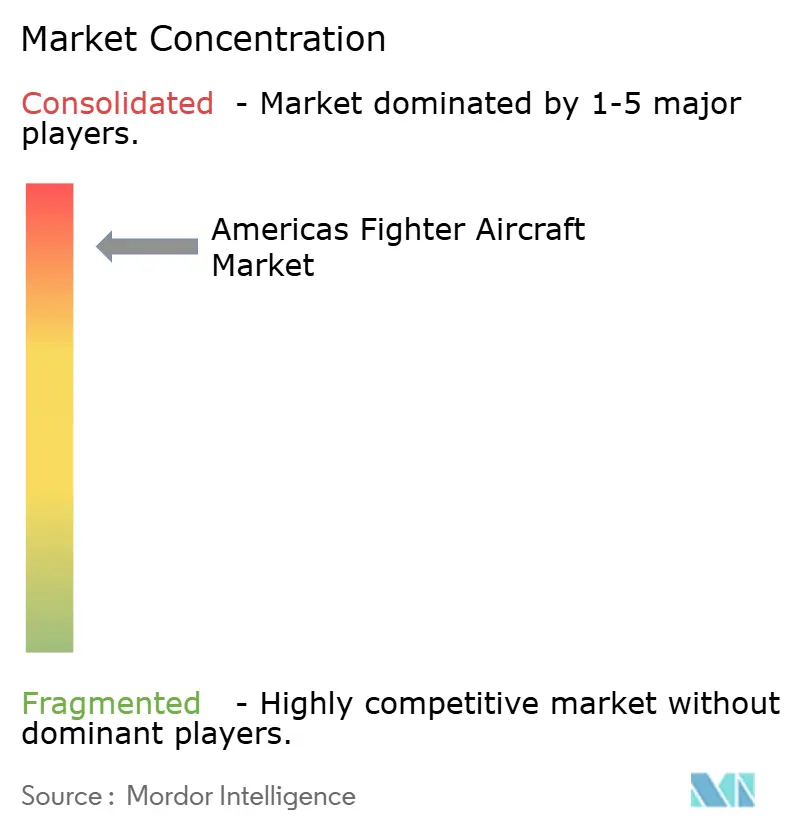

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Fighter Aircraft Market Analysis by Mordor Intelligence

The Americas fighter aircraft market size reached USD 20.62 billion in 2025 and is forecasted to expand to USD 25.05 billion by 2030, reflecting a 3.97% CAGR. The steady climb is anchored in sustained fleet recapitalization programs, widening 5th-generation adoption, and the need to keep sizable legacy fleets mission-ready. Geopolitical friction, particularly in the Arctic and South Atlantic, continues to spur procurement, while industrial offset mandates channel work into domestic supply bases across Brazil, Mexico, and Colombia. Growing interest in collaborative combat aircraft, use of artificial intelligence, and tighter joint-all-domain networks also reinforce the upward trajectory of the Americas fighter aircraft market. Remote operational concepts that rely on distributed basing, alongside surging demand for light-attack and advanced trainer aircraft, broaden the competitive opportunity set for prime and emerging manufacturers alike.

Key Report Takeaways

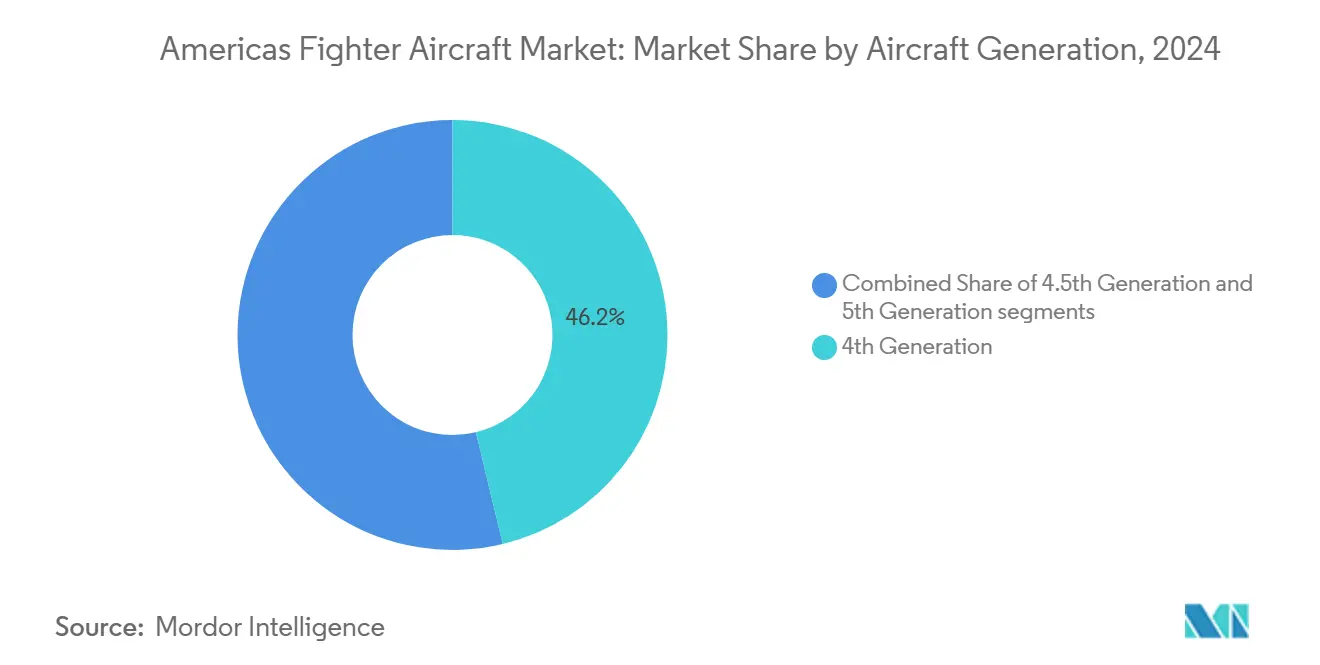

- By aircraft generation, 4th-generation platforms captured 46.24% of the market share, while 5th-generation platforms are advancing at a 7.88% CAGR, the highest among all categories.

- By take-off and landing, conventional take-off and landing (CTOL) captured 83.75%, vertical take-off and landing (VTOL) is advancing at a 5.23% CAGR, the highest among all categories.

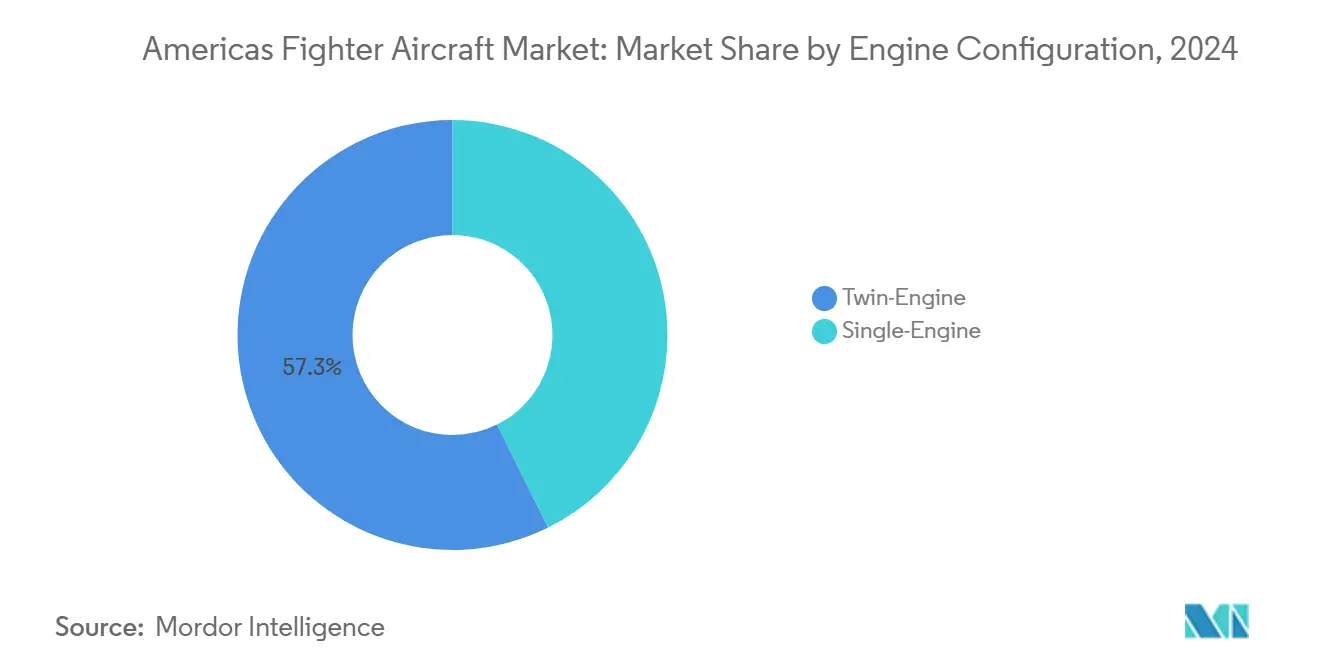

- By engine configuration, twin-engine fighters captured 57.34% of the Americas fighter aircraft market size in 2024, and single-engine fighters are advancing at a 4.56% CAGR during the forecast period.

- By mission role, multi-role aircraft accounted for 60.21% of the Americas fighter aircraft market size in 2024, and close-air-support/strike platforms are poised for a 4.87% CAGR through 2030.

- By end user, the Air Force commanded 88.42% of the Americas fighter aircraft market share in 2024, while Naval Aviation is advancing at a 5.11% CAGR to 2030.

- By geography, North America led with 76.55% of the Americas fighter aircraft market share in 2024; South America is projected to register the fastest 4.66% CAGR through 2030.

Americas Fighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5th-generation fighter procurement programs | +1.2% | North America primary, South America emerging | Medium term (2-4 years) |

| Sustainment and modernization of legacy fighter fleets | +0.8% | Global, concentrated in North America | Long term (≥ 4 years) |

| Geopolitical tensions and increasing defense budgets in the region | +1.0% | Global, with emphasis on North America and Brazil | Short term (≤ 2 years) |

| Industrial offset programs supporting domestic aerospace capabilities | +0.5% | South America focus, selective North America | Medium term (2-4 years) |

| Rising demand for advanced trainer and light-attack platforms | +0.4% | South America primary, US SOCOM secondary | Medium term (2-4 years) |

| Integration of joint all-domain command and control (JADC2) networks | +0.6% | North America primary, allied interoperability focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5th-Generation Fighter Procurement Programs

Boeing’s selection for the Next Generation Air Dominance (NGAD) contract, valued at USD 18-20 billion, signals a decisive pivot toward 6th-gen-ready, air-superiority designs that leapfrog the current 5th-generation benchmark. Canada’s contested F-35 review shows how political oversight shapes procurement cadence, yet interoperability imperatives continue to weigh in favor of 5th-generation adoption. Early sea-based operations aboard USS Abraham Lincoln illustrated the operational flexibility of stealth multirole aircraft in contested maritime theaters.[1]Stew Magnuson, “New U.S. Navy Aircraft to Change Middle East Ops,” National Defense, nationaldefensemagazine.org South American air forces, led by Colombia’s Gripen selection, are increasingly bundling industrial offsets—such as renewable-energy factories and water-infrastructure projects—into procurement deals, underscoring how defense buys are now instruments of broad industrial strategy.

Sustainment and Modernization of Legacy Fighter Fleets

Lockheed Martin’s USD 270 million integration of an Infrared Defensive System on the F-22 exemplifies the lifecycle-extension ethos that underpins large portions of the Americas fighter aircraft market. Chile’s USD 177 million F-16 M6.6 tape upgrade reinforces how incremental sensor and datalink enhancements keep legacy assets relevant while avoiding full fleet replacement costs. These upgrades generate long-term revenue for OEMs and guarantee operator readiness levels without disrupting budgets.

Geopolitical Tensions and Increasing Defense Budgets in the Region

Argentina’s broader USD 750 million military aviation allocation and Brazil’s USD 23.7 billion defense outlay reveal how regional governments channel higher discretionary spending into air-power capability. North American appropriations continue to favor procurement and RDT&E accounts that bolster the Americas fighter aircraft market. Higher budgets fast-track modernization timelines, though questions about long-term fiscal headroom linger as social spending competes for resources.

Industrial Offset Programs Supporting Domestic Aerospace Capabilities

South America is leaning on offsets to accelerate industrialization. Colombia’s Gripen package includes solar-panel plants and desalination initiatives, interweaving defense and socioeconomic goals. Mexico’s aerospace manufacturing hub at Tijuana, strengthened by ICON Aircraft’s USD 150 million near-shoring investment, enhances component resilience for the broader Americas fighter aircraft market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary constraints and fiscal austerity across key economies | -0.7% | Global, particularly South America | Short term (≤ 2 years) |

| Supply chain disruptions impacting critical fighter components | -0.5% | Global, concentrated in North America | Medium term (2-4 years) |

| Environmental regulations limiting supersonic flight training | -0.3% | North America primary, selective global | Long term (≥ 4 years) |

| Pilot shortages and workforce retention challenges | -0.4% | North America focus, emerging South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budgetary Constraints and Fiscal Austerity Across Key Economies

Despite the surge in defense budgets, many South American air arms still face rigid fiscal ceilings. Mexico’s delay in fighter recapitalization illustrates how sovereign debt loads and social-program pressures push modernization to the right. High fly-away and lifecycle costs of 5th-generation platforms deter smaller economies, steering choices toward upgraded fourth-gen solutions that temper capability against affordability.

Supply Chain Disruptions Impacting Critical Fighter Components

Casting and forging bottlenecks have stretched titanium lead times to nine months, while specialized alloy backlogs hover at 70-80 weeks, creating ripple effects across F-16, F-35, and NGAD lines.[2]Laura Juliano et al., “Fixing Aerospace’s Supply Chain for Casting and Forging,” Boston Consulting Group, bcg.com Engine delivery delays at GE Aerospace underscore the fragility of single-point suppliers. Workforce attrition among skilled machinists and engineers compounds recovery timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Generation: 5th-Generation Momentum Accelerates

The Americas fighter aircraft market size for 4th-generation assets equaled 46.24% of total revenue in 2024. 5th-generation platforms, however, are expanding at a 7.88% CAGR as operators increasingly prioritize stealth, sensor fusion, and network-centric capability. The F-35's operational success—from its inaugural carrier deployment to theater ISR missions—affirmed the platform's versatility. Boeing's NGAD win further cements the pivot toward advanced systems that survive inside high-threat air defense bubbles.

Legacy 4th-generation fleets remain integral for sovereignty patrols and cost-effective readiness. Chile's M6.6 upgrade keeps its F-16 fleet interoperable with allied Link-16 networks. Argentina's acquisition of Danish F-16 AM/BM aircraft underscores the enduring value proposition of proven airframes, particularly when bundled with comprehensive sustainment packages.

By Take-off and Landing: Conventional Dominance with VTOL Growth

CTOL variants generated 83.75% of 2024 revenue, reflecting existing runway infrastructure and well-established doctrine across the Americas fighter aircraft market. VTOL platforms, spearheaded by the F-35B, are moving higher at a 5.23% CAGR as distributed operations doctrine gains traction within US Marine Corps expeditionary units and select South American navies.

VTOL’s growth is also tied to humanitarian assistance and disaster-relief missions, where flexible basing proves decisive. Still, the category’s adoption outside major operators remains capped by higher acquisition and maintenance overheads. Future propulsion advances aimed at lowering thermal signature and improving fuel efficiency could widen VTOL adoption beyond niche requirements.

By Engine Configuration: Twin-Engine Reliability Preferred

Twin-engine fighters accounted for a 57.34% revenue share in 2024. They are favored for maritime strike and Arctic air-sovereignty missions where redundancy is critical. Single-engine designs post a 4.56% CAGR as improved reliability and lower cost entice South American buyers. Korea Aerospace Industries’ FA-50 single-seat variant targets nations wanting an F-16-class punch without two-engine sustainment burdens.

As 5th-generation propulsion tech migrates down the cost curve, the performance gap between single- and twin-engine platforms will narrow, potentially shifting future fleet-mix decisions.

By Mission Role: Multi-Role Versatility Drives Demand

Multi-role aircraft captured 60.21% of 2024 revenue, underscoring the operator's need for air-to-air and precision-strike versatility within shrinking fleet sizes. Close-air-support/strike aircraft clock a 4.87% CAGR on the back of low-intensity conflict requirements and demand for cost-effective kinetic options. The A-29 Super Tucano's passage of 600,000 total flight hours and 22-air-force user base is emblematic of that pull.

Air-superiority-specific variants remain essential for peer-threat deterrence, yet procurement preferences lean toward aircraft that can swing between missions without specialized fleets.

By End User: Air Force Dominance with Naval Growth

Air Force customers form 88.42% of demand in 2024, mirroring the sheer size of land-based operations. Naval aviation is on a 5.11% CAGR trajectory as carrier air-wing recapitalization accelerates. The F-35C’s carrier integration signals a generational upgrade in deck-launched capability, while Brazil’s naval missile programs hint at future sea-based fighter initiatives.

Marine and Army aviation retain smaller yet mission-critical slices of the Americas fighter aircraft market, chiefly for expeditionary support and high-tempo close-support needs.

Geography Analysis

North America commanded 76.55% revenue in 2024 thanks to sustained US Department of Defense programs such as NGAD, rolling F-35 block upgrades, and Canada’s CAD 16 billion drone-integration initiative for its fighter fleet. Continued F-35 production and the emergent F-47 program underpin regional momentum through 2030. Mexico’s growing MRO footprint, highlighted by L3Harris securing F-35 depot work, improves regional sustainment economics and mitigates supply-chain risk for North American operators.

South America, though smaller, is the fastest-growing slice of the Americas fighter aircraft market at a 4.66% CAGR. Argentina’s USD 266 million F-16 transfer package kicks off a broader fleet update.[3]Source: Xavier Dolan, “Lockheed to Transfer F-16 to Argentina,” GovCon Exec, govconexec.comBrazil’s USD 23.7 billion defense budget underwrites indigenous programs, including an armed ISR variant of the C-390 and new anti-ship missiles. Colombia’s Gripen deal spotlights industrial offsets as a force multiplier for local economies, while Peru’s multi-vendor fighter evaluation shows how competitive the regional landscape has become.

Looking ahead, South American share is expected to inch upward as more countries retire Cold-War airframes and harness defense as a tool for industrial development. Still, North America’s absolute spending power ensures it remains the anchor of the Americas fighter aircraft market for the foreseeable future.

Competitive Landscape

The competitive arena is heavily concentrated, with Lockheed Martin Corporation, The Boeing Company, and Northrop Grumman Corporation operating entrenched product lines, deep government relationships, and sizeable classified technology portfolios. Boeing’s NGAD award underscores the value of proven integration capability and digital-engineering proficiency in securing marquee contracts. Strategic tech alliances—such as Boeing’s 2025 accord with Palantir to infuse AI into mission-system architectures—herald emerging cross-industry ecosystems that can upend traditional value chains.

Mid-tier players are carving niches in light-attack and advanced trainer segments. Korea Aerospace Industries’ KF-21 and FA-50 lines and Embraer’s A-29 evolution cater to operators balancing performance and affordability. Supply-chain resilience is now a competitive differentiator, prompting primes to near-shore component production and vertically integrate critical cast-and-forge operations.

Intellectual property depth around sensor fusion, autonomous teaming, and open systems architecture becomes the next battleground. The Americas fighter aircraft market, therefore, favors incumbents with capital to fund long-cycle R&D yet leaves space for specialized suppliers of AI algorithms, electronic warfare (EW) payloads, and advanced propulsion materials.

Americas Fighter Aircraft Industry Leaders

Lockheed Martin Corporation

The Boeing Company

Saab AB

Northrop Grumman Corporation

Dassault Aviation SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Boeing secured a contract from the US Air Force to design, build, and deliver the nation's next-generation fighter aircraft, the NGAD platform.

- April 2024: Argentina signed a USD 300 million agreement with Denmark to acquire 24 F-16 fighter jets from the Royal Danish Air Force.

Americas Fighter Aircraft Market Report Scope

| 4th Generation |

| 4.5 Generation |

| 5th Generation |

| Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) |

| Vertical Take-off and Landing (VTOL) |

| Single-Engine |

| Twin-Engine |

| Air-Superiority |

| Multi-Role |

| Close-Air-Support/Strike |

| Air Force |

| Naval Aviation |

| Marine/Army Aviation |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

| By Aircraft Generation | 4th Generation | |

| 4.5 Generation | ||

| 5th Generation | ||

| By Take-off and Landing | Conventional Take-off and Landing (CTOL) | |

| Short Take-off and Landing (STOL) | ||

| Vertical Take-off and Landing (VTOL) | ||

| By Engine Configuration | Single-Engine | |

| Twin-Engine | ||

| By Mission Role | Air-Superiority | |

| Multi-Role | ||

| Close-Air-Support/Strike | ||

| By End User | Air Force | |

| Naval Aviation | ||

| Marine/Army Aviation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation and growth outlook for the Americas fighter aircraft market?

The Americas fighter aircraft market is valued at USD 20.62 billion in 2025 and is projected to reach USD 25.05 billion by 2030, growing at a 3.97% CAGR.

Which aircraft generation is seeing the fastest uptake across the region?

5th-generation fighters exhibit the highest growth, registering a 7.88% CAGR through 2030 as countries shift toward stealth and sensor-fusion capabilities.

Why does North America dominate regional demand?

Extensive US and Canadian procurement programs, including NGAD and F-35 block upgrades, give North America 76.55% of 2024 revenue.

How are supply chain disruptions affecting fighter production?

Long titanium and alloy lead times, plus engine delivery delays, are extending production schedules and prompting near-shoring and vertical-integration strategies.

What role do industrial offsets play in South American procurement?

Offsets such as renewable-energy plants and MRO centers are increasingly bundled into deals, enabling technology transfer and local economic development alongside aircraft acquisition.

Page last updated on: