Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

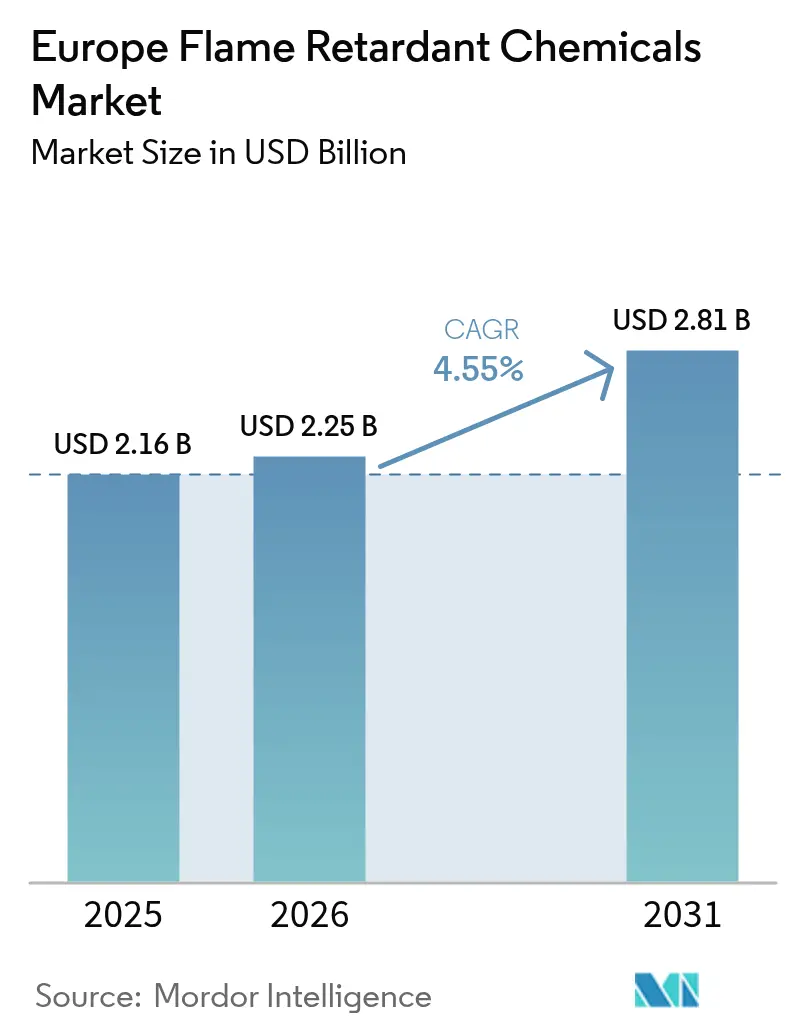

| Base Year Market Size (2025) | USD 2.16 Billion |

| Market Size (2026) | USD 2.25 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

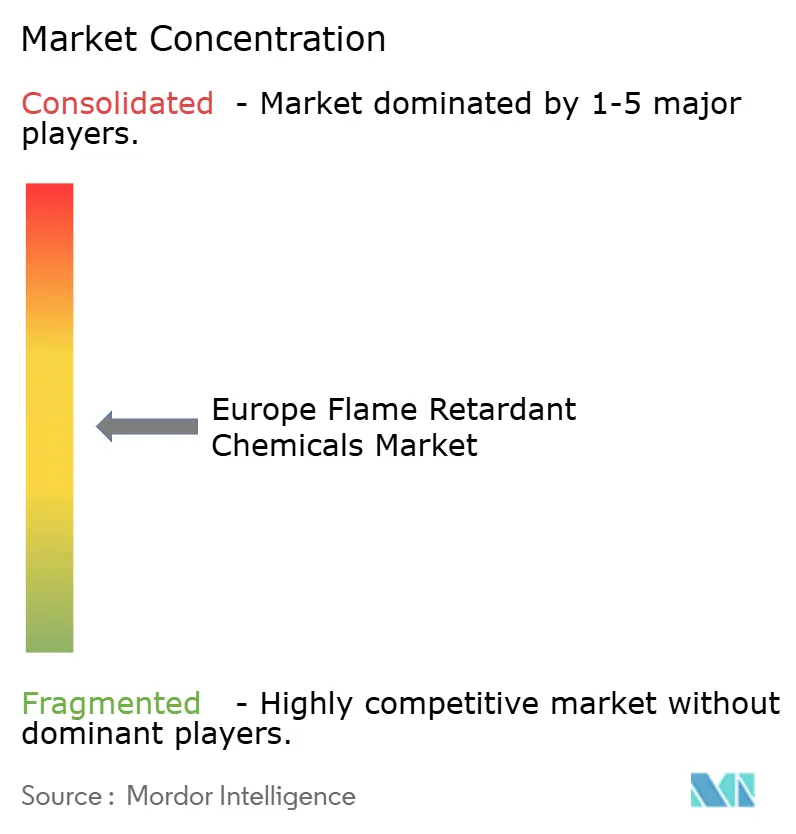

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Flame Retardant Chemicals Market Analysis by Mordor Intelligence

The Europe Flame Retardant Chemicals Market size is projected to expand from USD 2.16 billion in 2025 and USD 2.25 billion in 2026 to USD 2.81 billion by 2031, registering a CAGR of 4.55% between 2026 to 2031. The demand for flame retardant chemicals is driven by Europe's shift toward non-halogenated solutions, increasingly stringent regulations, and growing downstream applications in construction, batteries, and data-center cabling. The transition away from brominated compounds is evident across major applications, while rising antimony prices have highlighted the cost advantages of mineral fillers. Factors such as Germany's retrofit mandates, Spain's gigafactory projects, and the continent-wide expansion of 5G infrastructure are supporting capacity growth among regional producers. Additionally, the introduction of digital product passports under the revised Construction Products Regulation is creating higher entry barriers for offshore suppliers, providing integrated local manufacturers with a competitive advantage. In this context, the flame retardant chemicals market continues to favor suppliers who combine regulatory expertise with application-specific engineering capabilities.

Key Report Takeaways

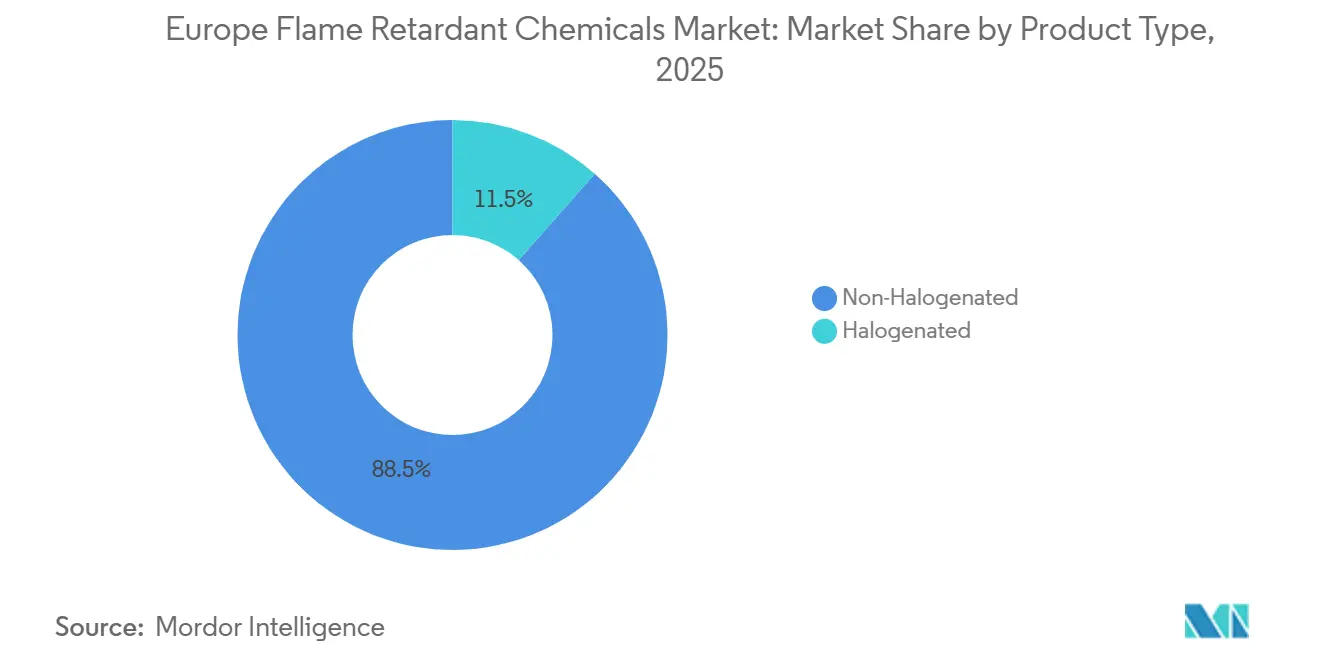

- By product type, non-halogenated solutions led with 88.49% of the flame retardant chemicals market share in 2025; the segment is projected to expand at a 5.79% CAGR through 2031.

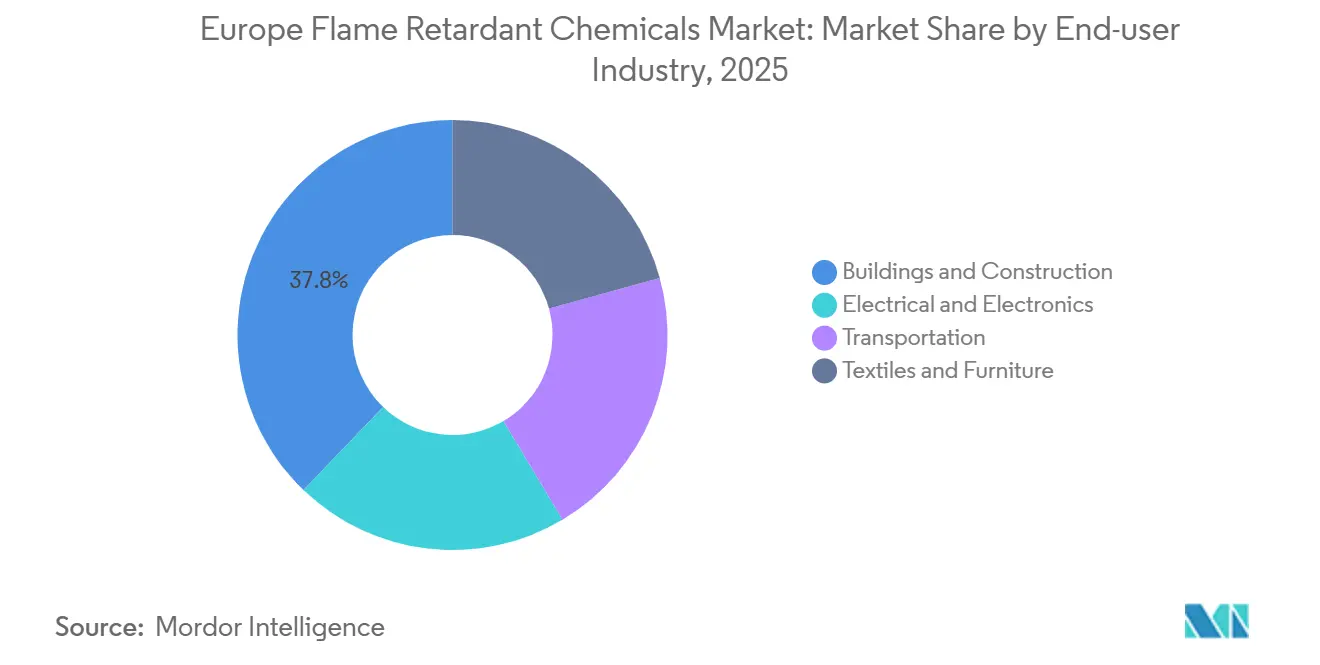

- By end-user industry, buildings and construction accounted for 37.81% of the flame retardant chemicals market share in 2025 and is advancing at a 4.72% CAGR through 2031.

- By geography, Germany captured 30.15% of the flame retardant chemicals market share in 2025 and is projected to post a 5.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flame Retardant Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer electrical and electronics manufacturing | +0.8% | Germany, France, Rest of Europe | Medium term (2-4 years) |

| Stricter fire-safety regulations in construction | +1.2% | Germany, UK, France, Spain | Short term (≤ 2 years) |

| Growth in electric-vehicle battery and charging infrastructure | +0.9% | Germany, France, Spain | Medium term (2-4 years) |

| Shift to circular-economy-compliant FR additives | +0.7% | Germany, France, Italy, Rest of Europe | Long term (≥ 4 years) |

| Surge in 5G cable and data-center installations | +0.6% | Germany, UK, France, Rest of Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Electrical and Electronics Manufacturing

The selective reshoring of electronics production has accelerated following the European Chips Act, which allocated EUR 43 billion in incentives through 2030. This has led to the relocation of printed-circuit-board and connector manufacturing from Asia to Europe[1]European Commission, “European Chips Act Fact Sheet,” EUROPA.EU. New facilities in Germany and France must adhere to IEC 60950 and IEC 62368 standards, which often require phosphorus-based or nitrogen-based formulations. The trend of miniaturization in smart-home and wearable devices has increased heat density, necessitating higher additive loading even as housings become thinner. In response, LANXESS introduced Levagard 2100 at K 2025, a halogen-free compound achieving UL 94 V-0 at a 0.75 mm wall thickness. Concurrently, European OEMs are diversifying supply chains to enhance resilience, benefiting local compounders with just-in-time capabilities. These developments directly support the flame retardant chemicals market by aligning regulatory compliance with regional supply chain security.

Stricter Fire-Safety Regulations in Construction

The revised Construction Products Regulation, effective January 2025, introduced digital product passports and stricter verification requirements, establishing EN 13501-1 Class B-s1,d0 as the practical baseline for insulation and cladding. To meet these standards, non-halogenated fillers like aluminum hydroxide and magnesium hydroxide are now used at concentrations of ≥ 60% by weight in rigid foams. Germany’s Gebäudeenergiegesetz is driving retrofitting activities in a building stock where 75% predates 1990 codes, while Spain’s renewable energy initiatives are increasing demand for rooftop solar and wind sub-structures. Despite Brexit, the UK has adopted similar classifications following post-Grenfell reforms. These converging regulations are pushing the flame retardant chemicals market toward mineral-based solutions that meet low-smoke criteria without encountering REACH authorization challenges.

Growth in Electric-Vehicle Battery and Charging Infrastructure

Although European electric vehicle (EV) production declined by 3% in 2024, battery-cell capacity continues to grow, driving localized demand for phosphorus additives that mitigate thermal runaway under UN Regulation 100.0. Stellantis’s Zaragoza gigafactory is projected to reach 40 GWh by 2027, with each GWh requiring significant volumes of intumescent coatings containing aluminum hydroxide. The bankruptcy of Northvolt removed 60 GWh of planned capacity, redirecting investments toward established players focused on premium safety chemistries. Public charging points exceeded 700,000 in 2024, with cables required to meet EN 50399 Euroclass Cca standards, ensuring the use of halogen-free low-smoke compounds. These factors create sustained demand for flame retardant chemicals in transportation electrification, even amid fluctuations in vehicle production.

Shift to Circular-Economy-Compliant Flame Retardant Additives

Extended Producer Responsibility regulations, fully implemented in 2024, penalize additives that hinder recycling processes. Aluminum and magnesium hydroxide are favored for their ability to withstand melt-reprocessing without toxic leaching, giving them an advantage over brominated systems. ICL’s VeriQuel R100, launched in December 2024, claims a 30% reduction in carbon footprint compared to traditional halogenated options. Clariant has invested CHF 100 million to expand phosphorus production capacity for European customers. The European Commission’s 2028 recycled-content mandate for construction materials is expected to reinforce this trend. As a result, the flame retardant chemicals market is shifting from cost-per-kilogram metrics to life-cycle impact assessments, favoring suppliers that can demonstrate cradle-to-gate sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity concerns over brominated FRs | -0.9% | Germany, France, UK, Rest of Europe | Short term (≤ 2 years) |

| Raw-material price volatility (Al, P, Mg ores) | -0.7% | Germany, Italy, France, Spain | Medium term (2-4 years) |

| Pending EU micro-plastics legislation limiting polymer uses | -0.5% | Germany, France, Italy, UK, Rest of Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicity Concerns Over Brominated Flame Retardants

Delegated Regulation 2025/1482 reduced PBDE thresholds to 350 ppm in November 2025, effectively excluding legacy brominated plastics from recycling streams. In January 2026, ECHA initiated a call for evidence on aromatic brominated chemistries, signaling potential bans by 2027. Retailers such as IKEA have already blacklisted TBBPA, reducing the immediate market for bromine suppliers. Additionally, aquatic toxicity concerns highlighted in the 2024 Water Framework Directive revision have increased public scrutiny. While halogen-free alternatives often require higher loadings, they avoid bioaccumulation risks, making them the preferred choice for new designs.

Raw-Material Price Volatility (Al, P, Mg ores)

Antimony trioxide prices surged by 400% year-on-year to USD 51,500 per ton in early 2025 after China imposed stricter export quotas, significantly impacting compounders reliant on it for brominated systems. Aluminum hydroxide prices have also risen due to a 15% contraction in European alumina capacity caused by ETS carbon costs, necessitating imports from Australia and Guinea. Elevated natural gas prices, still 60% above 2019 levels, have increased phosphorus pentoxide production costs. Nabaltec reported that raw materials accounted for 52% of its revenue in 2025, up from 47% in 2023. This price volatility has compressed margins and extended price renegotiation timelines, limiting the attainable growth of the flame retardant chemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Inorganics Anchor Non-Halogenated Dominance

Non-halogenated solutions captured 88.49% of the flame retardant chemicals market share in 2025 and are projected to grow at a CAGR of 5.79% through 2031. Aluminum and magnesium hydroxide lead this segment due to their ability to suppress smoke and enhance char, meeting EN 13501-1 Class B-s1,d0 standards without requiring REACH authorization. Phosphorus-based additives, such as ammonium polyphosphate and red phosphorus, are particularly favored in engineering polymers, where maintaining filler levels below 25% helps retain tensile strength.

Halogenated chemistries accounted for 11.51% of the market share in 2025 but face increasing challenges from the POPs Regulation and upcoming ECHA restrictions. Brominated compounds remain relevant in applications like printed circuits and aerospace wiring, where 8-12% loadings achieve V-0 ratings without compromising mechanical properties. However, life-cycle assessments and anticipated PFAS regulations are prompting OEMs to redesign products proactively. As a result, most new market demand is shifting toward non-halogenated systems, while bromine suppliers focus on securing regulatory exemptions rather than expanding capacity.

By End-user Industry: Construction Leads, Electronics Innovates

The buildings and construction sector contributed 37.81% of market sales in 2025 and is expected to grow at a CAGR of 4.72% through 2031. Germany's retrofit initiatives are driving demand for treated EPS and mineral wool, while Spain's renewable energy projects are boosting the need for flame-retardant cable management systems. Wire-and-cable products used in buildings must comply with Euroclass Cca standards, necessitating LSZH jackets with magnesium hydroxide and red phosphorus. As municipal codes increasingly align with Class B-s1,d0 standards, the additive loading per square meter of insulation is rising, driving up total tonnage even amid fluctuations in construction output.

The electrical and electronics sector remains a hub of innovation. Standards such as UL 94 and IEC 62368 dictate formulations for multi-year product cycles, while the 43 billion-euro Chips Act ensures the relevance of local sourcing. Miniaturization trends are increasing surface-to-volume ratios, which heightens fire risks and necessitates higher additive dosages. Selective growth opportunities also exist in transportation, textiles, and furniture, particularly as regulatory harmonization advances. For example, EV battery casings are increasingly adopting phosphorus-based systems to meet both safety and recyclability requirements.

Geography Analysis

Germany held a 30.15% share of the flame retardant chemicals market in 2025 and is forecast to grow at a CAGR of 5.69% through 2031. Key drivers include battery-cell manufacturing plants, data-center expansions, and stringent retrofit laws. For instance, Frankfurt added 150 MW of data-center capacity in 2024, with each MW requiring kilometers of LSZH cable that consumes approximately 1.2 kg of mineral flame retardant per meter. Additionally, Stellantis's gigafactory in Spain sources intumescent separators from German suppliers, ensuring that domestic demand for aluminum hydroxide remains above regional averages.

The United Kingdom, despite its separation from EU lawmaking, aligns its BS EN 13501 standards with continental regulations. Post-Grenfell bans on combustible façade elements have significantly increased the use of intumescent coatings and flame-retardant insulation in high-rise retrofits. France is set to benefit from Microsoft's EUR 4 billion data-center project, which will begin shipping cabling in 2026, further driving LSZH demand. Italy's seismic-retrofit programs integrate structural reinforcement with thermal upgrades, embedding mineral additives in dual-purpose panels. Spain's renewable energy projects require flame-retardant junction boxes, increasingly relying on phosphorus-based solutions to meet toxicity standards. The rest of Europe, including the Nordics, Benelux, and Eastern Europe, enforces stricter Class B-s1,d0 codes, resulting in higher per-capita consumption and a broader market footprint.

Competitive Landscape

The flame retardant chemicals market is moderately concentrated, with the top five players, including BASF, Clariant, Albemarle, ICL, and LANXESS, collectively controlling approximately 56% of the market in 2025. Albemarle focuses on defending its brominated product lines through life-cycle studies, while Clariant and ICL are investing in phosphorus-based expansions, such as Clariant's CHF 100 million Daya Bay project scheduled for completion in Q2 2026[2]Clariant AG, “Daya Bay Expansion Announcement,” CLARIANT.COM . Vertical integration provides a competitive edge; for example, Nabaltec processes bauxite into aluminum hydroxide in-house, mitigating risks from raw material price fluctuations, while ICL mines its own phosphate rock.

Patent activity highlights the industry's shift toward innovation. LANXESS filed 12 flame-retardant patents between 2024 and 2025, targeting thin-wall electronics. THOR introduced Aflammit PCO 900, which achieves IEC 60950 compliance at an 18% loading, 30% lower than standard ammonium polyphosphate formulations. While bio-based alternatives using lignin and phytic acid are still in the early stages, they are receiving Horizon Europe grants, indicating potential future disruption. OEM consolidation is also reshaping the competitive landscape, as digital passports enable automakers and construction firms to streamline supplier lists, disadvantaging smaller formulators lacking robust compliance capabilities. Overall, competition increasingly revolves around the ability to align regulatory foresight with low-carbon chemistries, a factor that is becoming critical in determining market share shifts.

Europe Flame Retardant Chemicals Industry Leaders

Albemarle Corporation

ICL

BASF

Clariant

LANXESS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The European Commission formally adopted Delegated Regulation (EU) 2025/1482, which introduced substantial amendments to the provisions concerning brominated flame retardants. These changes were made under the EU Persistent Organic Pollutants (POPs) Regulation (EU 2019/1021).

- April 2025: Mitsubishi Chemical Group Corporation expanded its production capacity for flame-retardant compounds, based on polyolefins and thermoplastic elastomers, at MCPP France SAS. These compounds are used for cable sheathing and other applications.

Europe Flame Retardant Chemicals Market Report Scope

Flame retardants are key chemicals used on materials such as surface coatings, textiles, and plastic, including others, to inhibit or delay the production and spread of fire. The most common elements used as flame retardants are bromine, chlorine, and phosphorous. The compounds of these elements are added to or treat potentially flammable materials and reduce their ability to ignite.

The Europe flame retardant chemicals market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into non-halogenated and halogenated. By end-user industry, the market is segmented into buildings and construction, electrical and electronics, transportation, and textiles and furniture. The report also covers the market size and forecasts for flame retardant chemicals in 5 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Non-Halogenated | Inorganic | Aluminum Hydroxide |

| Magnesium Hydroxide | ||

| Boron Compounds | ||

| Phosphorus-based | ||

| Nitrogen-based | ||

| Others | ||

| Halogenated | Brominated Compounds | |

| Chlorinated Compounds |

By End-user Industry

| Buildings and Construction |

| Electrical and Electronics |

| Transportation |

| Textiles and Furniture |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Rest of Europe |

| By Product Type | Non-Halogenated | Inorganic | Aluminum Hydroxide |

| Magnesium Hydroxide | |||

| Boron Compounds | |||

| Phosphorus-based | |||

| Nitrogen-based | |||

| Others | |||

| Halogenated | Brominated Compounds | ||

| Chlorinated Compounds | |||

| By End-user Industry | Buildings and Construction | ||

| Electrical and Electronics | |||

| Transportation | |||

| Textiles and Furniture | |||

| By Geography | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How large is the Europe flame retardant market?

The Europe flame retardant market stands at USD 2.25 billion in 2026 and is projected to reach USD 2.81 billion by 2031, reflecting a 4.55% CAGR from 2026 to 2031.

Which product is expanding the fastest through 2031?

Non-halogenated solutions, particularly aluminum and magnesium hydroxide, are expected to grow at a 5.79% CAGR through 2031.

Why did Germany lead the market in 2025?

A mix of building-energy retrofits, data-center construction, and battery-cell gigafactories pushes German share to 30.15% in 2025.

How are EU regulations influencing product selection?

EN 13501-1 upgrades, the Construction Products Regulation, and upcoming PFAS restrictions collectively steer buyers toward halogen-free, recyclable chemistries.

Page last updated on: