Aircraft Flame-Retardant Films Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

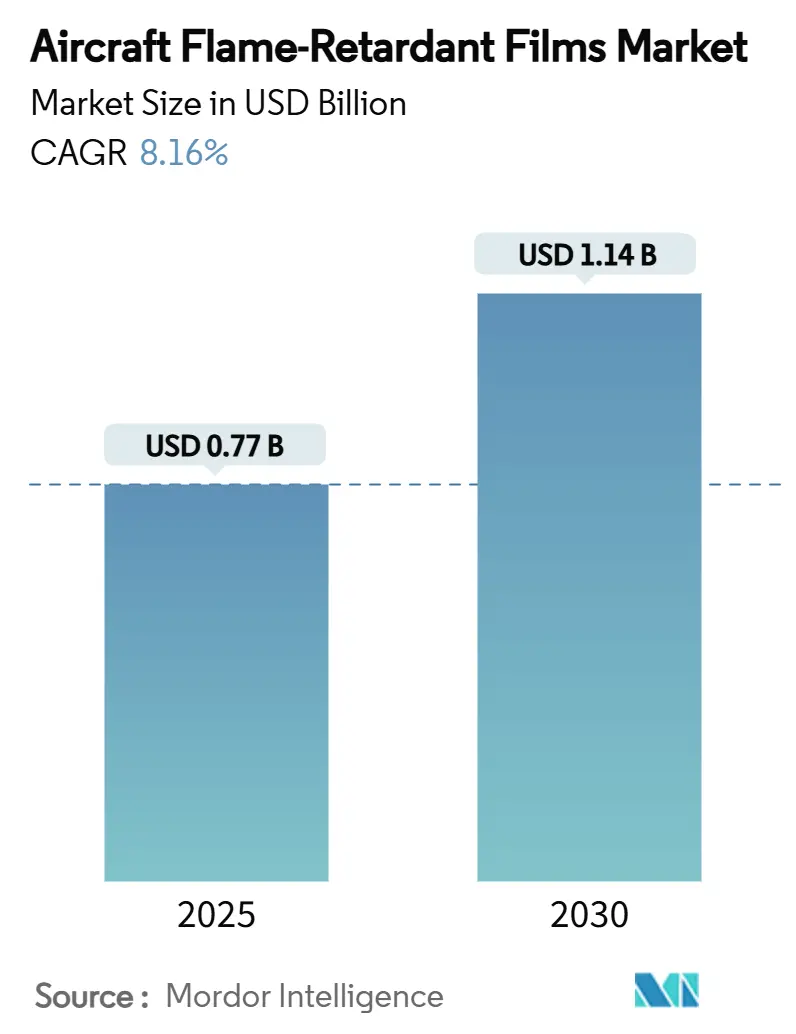

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.14 Billion |

| Growth Rate (2025 - 2030) | 8.16% CAGR |

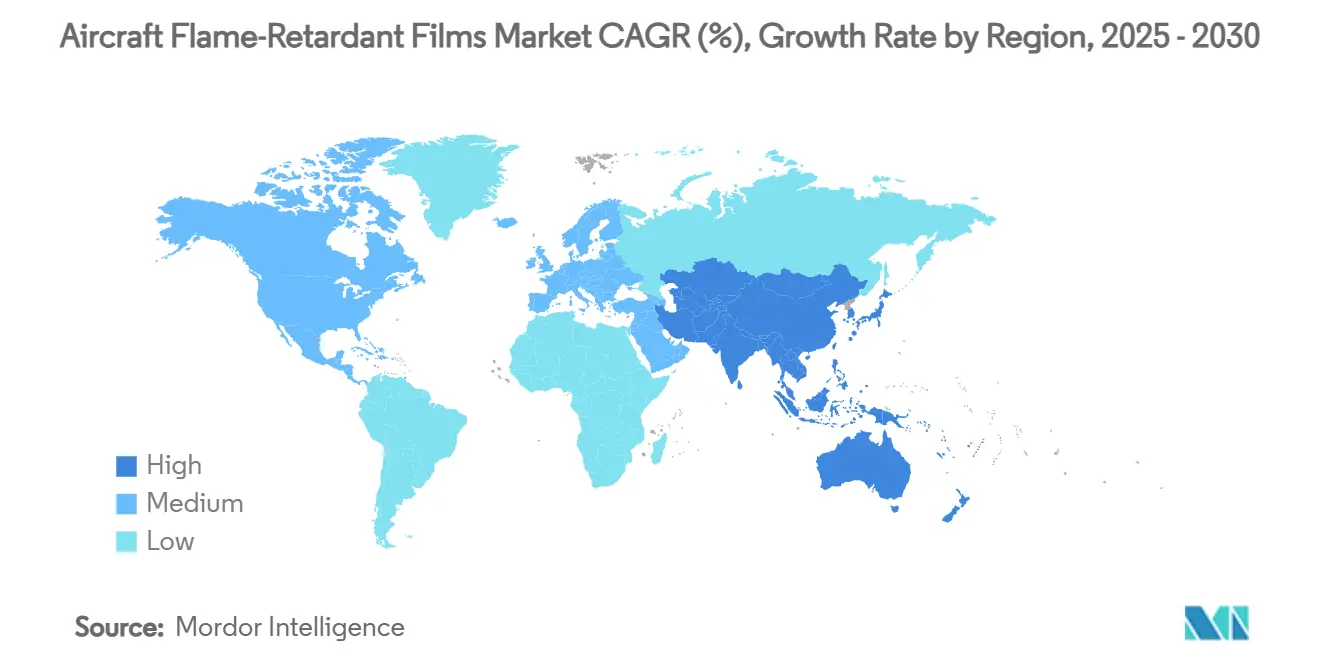

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Flame-Retardant Films Market Analysis by Mordor Intelligence

The aircraft flame-retardant films market size is estimated at USD 0.77 billion in 2025, and is expected to reach USD 1.14 billion by 2030, reflecting a CAGR of 8.16% during the forecast period. This growth outlook mirrors the aviation sector’s rebound, tighter global fire-safety mandates, and continued material-science breakthroughs. Advances in halogen-free polyimides, the widening use of phosphorus-based additives, and the push for lighter cabin components are elevating acceptance of new-generation films. OEM vertical-integration moves, such as Boeing’s agreement to purchase Spirit AeroSystems, underscore how supply-chain realignment reshapes long-term sourcing decisions. Meanwhile, Asia-Pacific’s accelerating aircraft production and retrofit activity ensure that certified film suppliers enjoy a demand tailwind lasting through the decade.

Key Report Takeaways

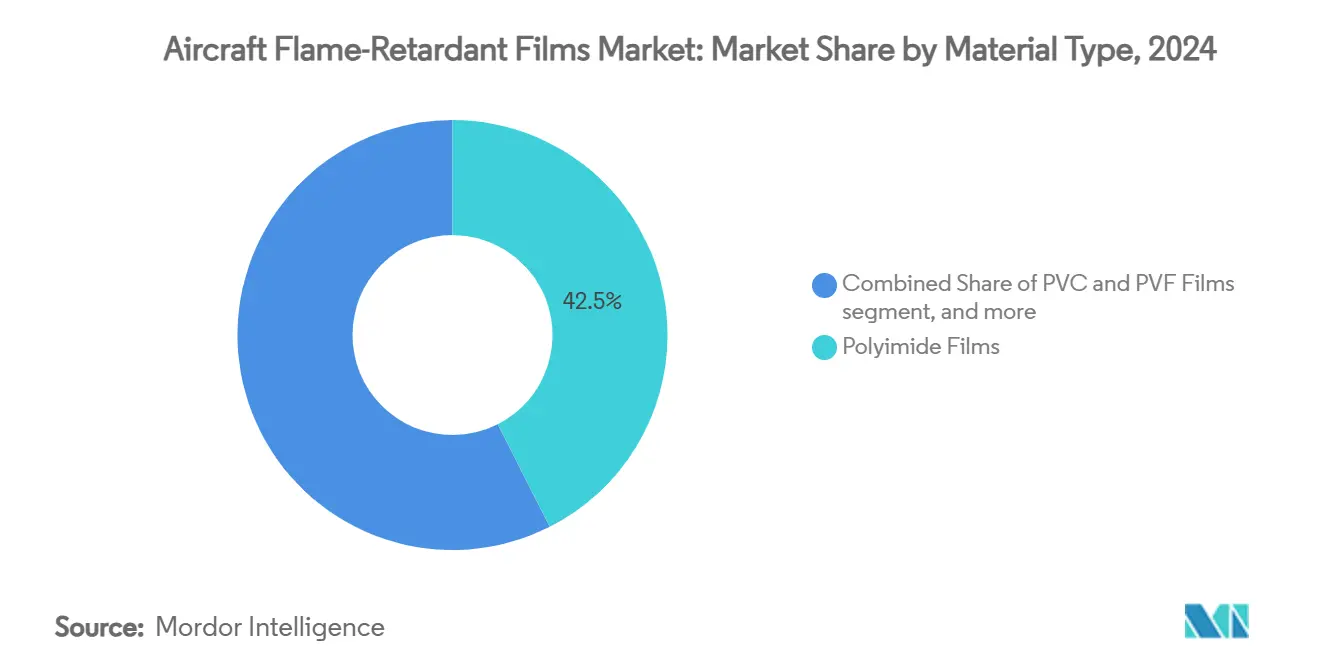

- By material type, polyimide grades held 42.54% of the aircraft flame-retardant films market share in 2024. However, specialty films featuring bio-derived phosphorus recorded the fastest 8.66% CAGR during the forecast period.

- By aircraft type, commercial platforms generated 57.23% revenue share of the aircraft flame-retardant films market and are projected to post the fastest 8.90% CAGR through 2030.

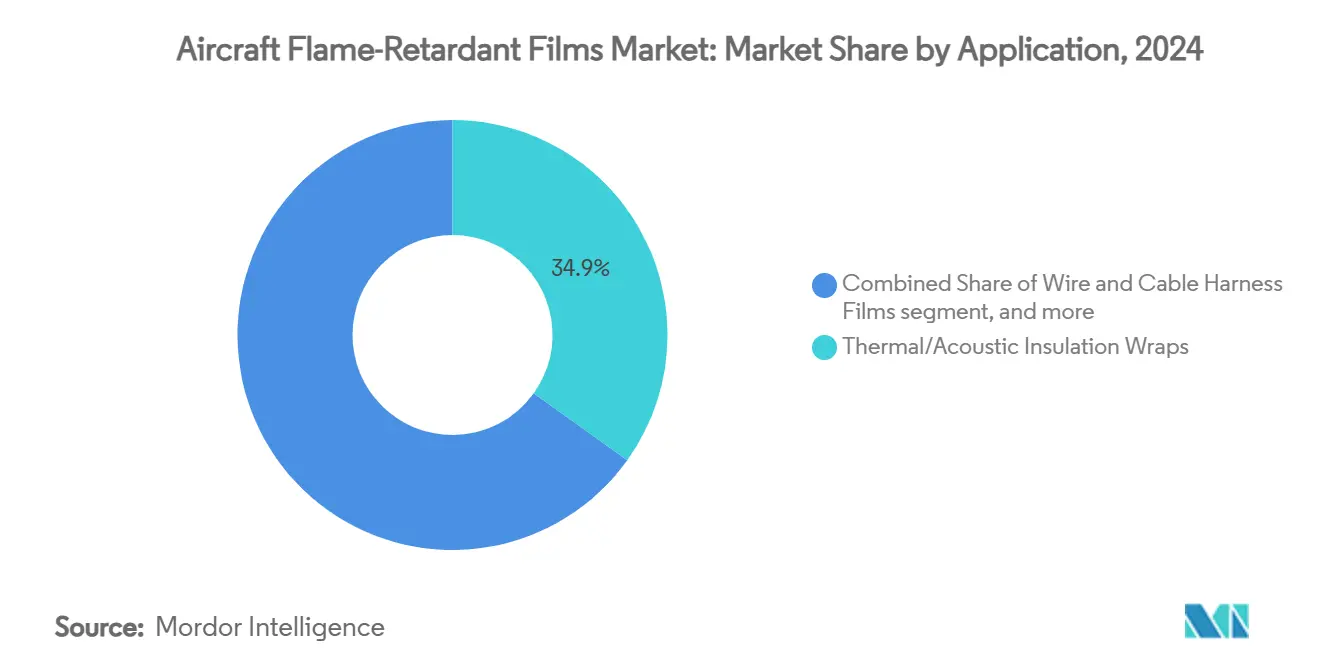

- By application, thermal-acoustic blanket wraps secured 34.89% of 2024 revenue. Yet, wire-and-cable harness wraps are forecasted to record a 9.21% CAGR between 2025 and 2030.

- By fitment channel, OEM deliveries captured 66.28% of the aircraft flame-retardant films market size in 2024. However, the aftermarket channel is forecasted to grow at a 9.11% CAGR as carriers refurbish cabins at 6- to 8-year intervals to keep Net Promoter Scores high and comply with advancing test regimes.

- By geography, North America led with a 37.87% revenue share in 2024, while Asia-Pacific is on track for a 9.32% CAGR to 2030.

Global Aircraft Flame-Retardant Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent international fire safety regulations for aircraft interiors | +2.1% | Global, higher in North America and EU | Long term (≥ 4 years) |

| Growth in global aircraft production and fleet modernization programs | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for lightweight, high-performance interior materials | +1.4% | Global commercial fleets | Medium term (2-4 years) |

| Rising adoption of flame-retardant films in next-generation electric aircraft cabins | +0.9% | North America and EU, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in halogen-free and transparent polyimide films | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Sustainability initiatives driving adoption of recyclable and circular polymer materials | +0.7% | EU first, global follow-on | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent International Fire-Safety Regulations for Aircraft Interiors

Fire-safety mandates leave airlines no flexibility: every interior surface must comply. The FAA’s evolving 14 CFR 25.853 rules now require tougher heat-release and smoke-toxicity thresholds, pushing airlines to adopt high-performance, halogen-free films. EASA mirrored that rigor when it certified the A321XLR, setting precedent for future programs.[1]European Union Aviation Safety Agency, “EASA issues Type Certificate to Airbus A321XLR,” easa.europa.eu OEM-specific standards such as Boeing’s BAC 5034-4 add another layer, forcing suppliers to deliver beyond baseline compliance. The combined effect guarantees long-run demand growth for certified, next-generation film systems.

Growth in Global Aircraft Production and Fleet-Modernization Programs

Airframe output climbed sharply in 2025 as narrowbody lines ramped to meet backlog. Each new fuselage section requires kilometers of flame-retardant insulation and wire-wrap films, making production rates a direct volume driver. Boeing’s bid to internalize Spirit AeroSystems illustrates how OEMs are locking in strategic material flows. Parallel fleet-refresh efforts—in which 10- to 15-year-old jets receive cabin upgrades—bolster aftermarket demand and help smooth cyclical swings in the aircraft flame-retardant films market.

Increasing Demand for Lightweight, High-Performance Interior Materials

Fuel-burn economics still dominate airline profit equations. Replacing older PVF skins with polyimide solutions can trim blanket weight by up to 60%, an excessive incentive for operators to ignore.[2]Victrex, “Polymer Films | High Performance PEEK Films,” victrex.com Composite-rich fuselages rely on compatible films that withstand higher cure temperatures without embrittlement. The need for multifunctional laminates that deliver acoustics, EMI shielding, and fire performance in a single layer keeps R&D pipelines full.

Rising Adoption in Next-Generation Electric Aircraft Cabins

eVTOL prototypes place batteries inches from passenger seats, heightening ignition risk. Design teams specify films offering flame spread, thermal-barrier, and dielectric protection in one material stack.[3]Add Composites, “eVTOL Manufacturing: A Deep Dive,” addcomposites.com The projected USD 39 billion urban-air-mobility segment could add thousands of small-aircraft builds annually by the early 2030s, handing specialty-film suppliers a new, rapidly scaling avenue for revenue.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and procurement costs of specialty flame-retardant films | -1.6% | Global, most acute in cost-sensitive fleets | Short term (≤ 2 years) |

| Volatile raw material supply chains for advanced polymer feedstocks | -1.3% | Global, with Asia-Pacific concentration risk | Short term (≤ 2 years) |

| Regulatory-driven phase-out of legacy halogenated flame retardant materials | -0.8% | EU first, North America following | Medium term (2-4 years) |

| Technical challenges in recycling multi-layered flame-retardant laminate systems | -0.5% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production and Procurement Costs of Specialty Films

Manufacturing colorless, high-temperature polyimides demands capital-intensive reactors running above 300°C, limiting the pool of qualified producers. For airlines operating under tight unit-cost targets, upfront film prices can deter adoption despite clear lifecycle benefits. Lengthy airworthiness qualification cycles further discourage rapid supplier switching, cushioning incumbent pricing power but slowing overall diffusion in the aircraft flame-retardant films market.

Volatile Raw-Material Supply Chains for Advanced Polymer Feedstocks

Geopolitical risk weighs on monomer sourcing. Concentration of specialty diamine production in East Asia exposes Western OEMs to shipping disruptions and export-control shocks. Aerospace primes therefore pursue dual-sourcing and inventory-buffer strategies, but these increase carrying costs and erode near-term profit margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyimide Dominance and PEEK Upside

Polyimide films captured a 42.54% slice of the aircraft flame-retardant films market in 2024 due to their ability to withstand 260°C continuous service while maintaining low smoke density. DuPont’s Kapton grades remain design-office staples on B787 and A350 cabins.[4]DuPont, “DuPont Aerospace,” airframer.com Specialty-film challengers featuring bio-derived phosphorus recorded the fastest 8.66% CAGR and are expected to account for a sizable aircraft flame retardant films market size increment by 2030. PVC and PVF offerings linger in cost-sensitive retrofit use but face shrinking addressable share as halogen regulations tighten. Although commanding price premiums exceeding USD 220 per kg, PEEK delivers unmatched chemical resilience for fuel-system and high-heat zones, thus securing a differentiated growth niche. Commercialized in 2024, transparent polyimide technology enables uniform cabin color palettes while satisfying updated radiant-panel tests, a milestone should spur higher adoption in wide-body refurbishment programs.

Uptake of hybrid multilayer constructions is increasing: producers laminate ultra-thin polyimide skins onto recyclable PET cores to combine weight savings with easier end-of-life processing. Investors are backing vertical-integration projects that bring precursor monomer, film casting, and coating into the same plant to cut lead times. In the aircraft flame-retardant films market, such integrated capacity is projected to add more than 12,000 metric tons by 2030, relieving the chronic supply tension observed after the post-pandemic recovery.

By Aircraft Type: Commercial Jets Lead, eVTOL Adds New Volume

Commercial platforms generated 57.23% of 2024 revenue and are on track for an 8.90% CAGR through 2030, driven by the production ramp of A320neo and B737 MAX families. Each single-aisle delivery installs roughly 4,600 sqm of fire-retardant insulation and decorative films, firmly anchoring volume demand. Military airframes require tighter mechanical-shock tolerance and broader temperature windows, hence sourcing specialized grades, albeit in low volumes. Regional-jet and business-aviation builders increasingly mirror large-airline expectations for cabin feel, amplifying the aircraft flame-retardant films market size across these niches.

Growth prospects widen with the rise of electric regional aircraft and eVTOL vehicles. Prototype certification pathways indicate cabin-material flammability limits similar to Part 25 transport category jets, extending the regulatory umbrella. Early supplier agreements signed in 2025 allow filmmakers to lock in multiyear revenue streams before mass production begins in the late 2020s.

By Application: Thermal Wraps Retain Lead, Harness Protection Accelerates

Thermal-acoustic blanket wraps secured 34.89% of 2024 revenue, reflecting their essential role in fire protection and cabin-noise attenuation. Yet the fastest lift comes from wire-and-cable harness films, forecasted to post a 9.21% CAGR as avionics become denser and electric-propulsion voltages climb. Multi-layer surface laminates, blending scratch resistance with flame performance, are gaining favor in galleys and lavatories where harsh cleaning agents quickly deteriorate older PVC décor shots.

Cargo-liner facings form another steady demand pillar, particularly as express-freight operators retrofit passenger jets for dedicated parcel service. Although smaller in tonnage, seat-cover backings and carpet underlays deliver a high margin because airlines value low-odor, easy-install solutions that keep ground time minimal. Therefore, the aircraft flame-retardant films market share for these specialty sub-segments is set to edge upward through upgraded service-life offerings.

By Fitment Channel: OEM First-Fit Dominance but Aftermarket Upswing

Initial build slots at airframe factories accounted for 66.28% of the aircraft flame-retardant films market size during 2024. Design-freeze decisions made at program launch often lock in a single film supplier for decades, reinforcing OEM streams. However, the aftermarket channel grows 9.11% as carriers refurbish cabins at 6-to 8-year intervals to keep Net Promoter Scores high and comply with advancing test regimes. Predictive maintenance software now tags insulation degradation using cabin-temperature sensor data, prompting more proactive change-outs.

MRO shops increasingly request pre-scored blanket kits that reduce labor by 20%, an innovation that could redirect margin capture toward film producers able to supply turnkey solutions. Boeing’s vertical-integration strategy may tilt future negotiations toward direct purchase agreements, a development that smaller tier-two suppliers are watching closely.

Geography Analysis

North America’s aircraft flame-retardant films market benefits from vertically integrated value chains stretching from polymer research labs to FAA-approved test furnaces. Suppliers headquartered in Delaware, Michigan, and California provide just-in-time delivery to final assembly lines, buffering logistics risk. Retrofit demand remains robust as US carriers plan major cabin upgrades on B737NG and A320ceo fleets to enhance customer comfort while aligning with post-2025 flammability rules. Industry consortia are piloting closed-loop recycling schemes that target a 70% recovery rate for removed blankets, setting a precedent that global regulators will likely emulate.

Asia-Pacific’s acceleration rests on surging intra-regional traffic, which averaged double-digit year-on-year growth in 2025. China’s airframer delivered its first C919 to a foreign carrier, signaling confidence in domestic certification and concurrent FAA and EASA validation efforts. Japanese stalwarts such as Toray ramp high-modulus fiber lines, while Indian conversion shops capture US and EU overflow work, shortening lead times for replacement kits. Local content rules create a competitive advantage for regional film manufacturers that can match Western certification dossiers, spurring joint ventures.

Europe’s share remains anchored by Airbus and a regulatory culture at the vanguard of chemical-safety and circularity mandates. French and German Tier-1s collaborate with universities on solvent-free coating chemistries that cut VOC emissions during film production. The EU Taxonomy has begun influencing airline procurement criteria, rewarding materials with audited end-of-life pathways. As a result, recyclable multi-layer laminates enjoy preferential consideration on A350 cabin-refresh orders scheduled from 2027 onward.

Competitive Landscape

The aircraft flame-retardant films market is moderately concentrated: the top five producers account for more than 55% of global revenue, but certification hurdles give incumbents room to defend share. DuPont keeps pole position through its Kapton and Tedlar franchises, which span thermal, decorative, and EMI-shielding uses. Syensqo leverages Ajedium PEEK film expertise first proven in automotive to secure new aerospace contracts, illustrating cross-sector technology migration. Toray integrates fiber, resin, and film capabilities, partnering with EconCore to roll out recyclable honeycomb-panel systems.

Strategic actions intensified in 2025. DuPont announced a corporate split that could free additional capital for aerospace R&D, potentially accelerating next-gen halogen-free platforms. Honeywell’s decision to spin off its Advanced Materials unit opens M&A possibilities for film specialists seeking scale. At the same time, GE Aerospace earmarked USD 1 billion for US plant upgrades, a portion directed to ceramic-matrix and high-temperature polymer lines expected to benefit film properties for hypersonic and space applications. Emerging Asian suppliers focus on localizing polyimide precursor chemistry, but must still navigate multi-year FAA and EASA qualification gauntlets before penetrating Western OEM bills of material.

Looking forward, white-space opportunity revolves around electric aviation. Film makers that can combine UL94 V-0 dielectric strength with sub-60 g/m² are positioned to command premium pricing. As airlines chart net-zero pathways, sustainability credentials will influence sourcing more than ever, driving competitive differentiation based on end-of-life recoverability and bio-carbon content.

Aircraft Flame-Retardant Films Industry Leaders

DuPont de Nemours, Inc.

Kaneka Corporation

Toray Industries, Inc.

Victrex Manufacturing Limited

Saint-Gobain Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Protechnic announced that its thermoplastic adhesives are compliant with flame-retardant safety standards and are now used in aircraft applications, including seating, cabin dividers with acoustic insulation, and composite reinforcement. This development supports enhanced fire safety and performance in critical aircraft interior components.

- April 2023: tesa SE expanded its flame-retardant product portfolio with tesa® flameXtinct 45020, a new adhesive solution designed for carpet bonding in aircraft interiors. The product features halogen-free and self-extinguishing properties while meeting all aviation industry fire protection standards.

Global Aircraft Flame-Retardant Films Market Report Scope

| Polyimide Films |

| PVC and PVF Films |

| Polyetheretherketone (PEEK) |

| Other Specialty Films |

| Commercial | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| Thermal/Acoustic Insulation Wraps |

| Surface Protection and Decorative Laminates |

| Wire and Cable Harness Films |

| Cargo Liner and Floor Panel Facings |

| Seat-Upholstery/Carpet Backing Films |

| Others |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Material Type | Polyimide Films | ||

| PVC and PVF Films | |||

| Polyetheretherketone (PEEK) | |||

| Other Specialty Films | |||

| By Aircraft Type | Commercial | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military | Combat | ||

| Transport | |||

| Special Missions | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By Application | Thermal/Acoustic Insulation Wraps | ||

| Surface Protection and Decorative Laminates | |||

| Wire and Cable Harness Films | |||

| Cargo Liner and Floor Panel Facings | |||

| Seat-Upholstery/Carpet Backing Films | |||

| Others | |||

| By Fitment Channel | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft flame retardant films market in 2030?

The market is expected to reach USD 1.14 billion by 2030, reflecting an 8.16% CAGR.

Which material currently holds the largest share in aircraft flame-retardant film consumption?

Polyimide films led with 42.54% share in 2024, driven by superior thermal and flame performance.

Why are airlines accelerating aftermarket demand for cabin fire-retardant films?

Refurbishment cycles, tougher post-2025 flammability rules, and predictive-maintenance alerts are prompting faster blanket and wire-wrap replacements.

Which region is growing fastest for certified flame-retardant film demand?

Asia-Pacific is forecasted to post a 9.32% CAGR through 2030 on the back of rising aircraft output and fleet growth.

How will electric aircraft influence future film requirements?

EVTOL and hybrid-electric models need lightweight films that deliver combined flame, thermal, and dielectric protection, opening a new premium niche.

Page last updated on: