Filter Integrity Test Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

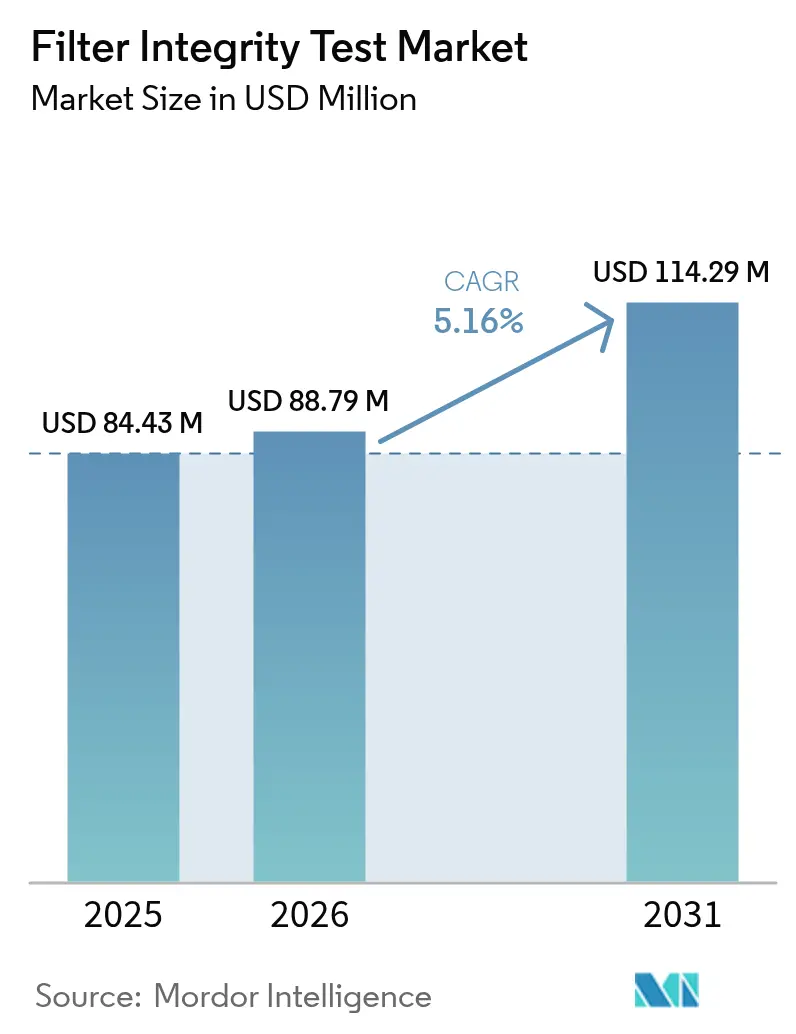

| Market Size (2026) | USD 88.79 Million |

| Market Size (2031) | USD 114.29 Million |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

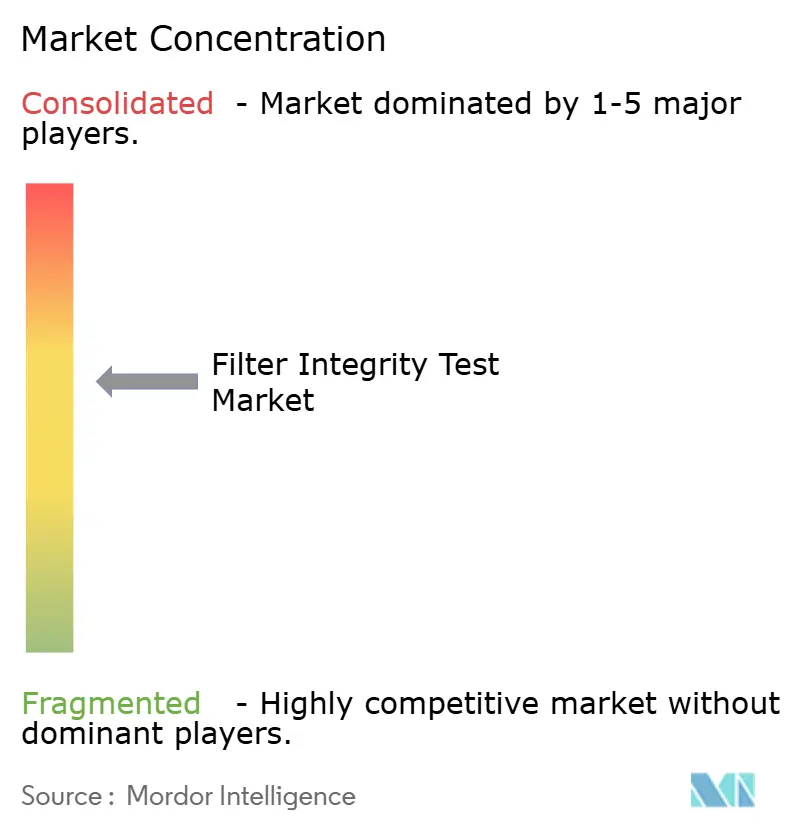

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Filter Integrity Test Market Analysis by Mordor Intelligence

The filter integrity test market size in 2026 is estimated at USD 88.79 million, growing from 2025 value of USD 84.43 million with 2031 projections showing USD 114.29 million, growing at 5.16% CAGR over 2026-2031. Intensifying regulatory oversight over sterile manufacturing, rapid bioprocess capacity build-outs, and widespread digitalization of quality control workflows underpin this steady expansion. Heightened investments in cell- and gene-therapy facilities demand more sophisticated validation protocols, while the pivot toward single-use filtration assemblies amplifies testing volumes. Automated systems that generate tamper-proof audit trails are increasingly preferred because they minimize human error, uphold data integrity, and accelerate batch-release timelines. In parallel, emerging acoustic test technologies promise non-destructive, high-sensitivity defect detection that strengthens contamination-control strategies in advanced therapeutics manufacturing.

Key Report Takeaways

- By product type, automated systems led with 56.88% revenue share in 2025 and are advancing at a 7.52% CAGR through 2031.

- By test type, bubble point testing held 40.75% of the Filter Integrity Test market share in 2025, while water intrusion testing records the fastest 7.12% CAGR to 2031.

- By mechanism, pressure-based methods commanded 61.72% share in 2025, whereas acoustic technologies expand at an 8.05% CAGR through 2031.

- By filter type, liquid filters accounted for 67.90% of the Filter Integrity Test market size in 2025 and are forecast to grow 7.27% annually to 2031.

- By application, liquid filtration integrity testing captured 60.98% share in 2025 and is progressing at an 8.34% CAGR to 2031.

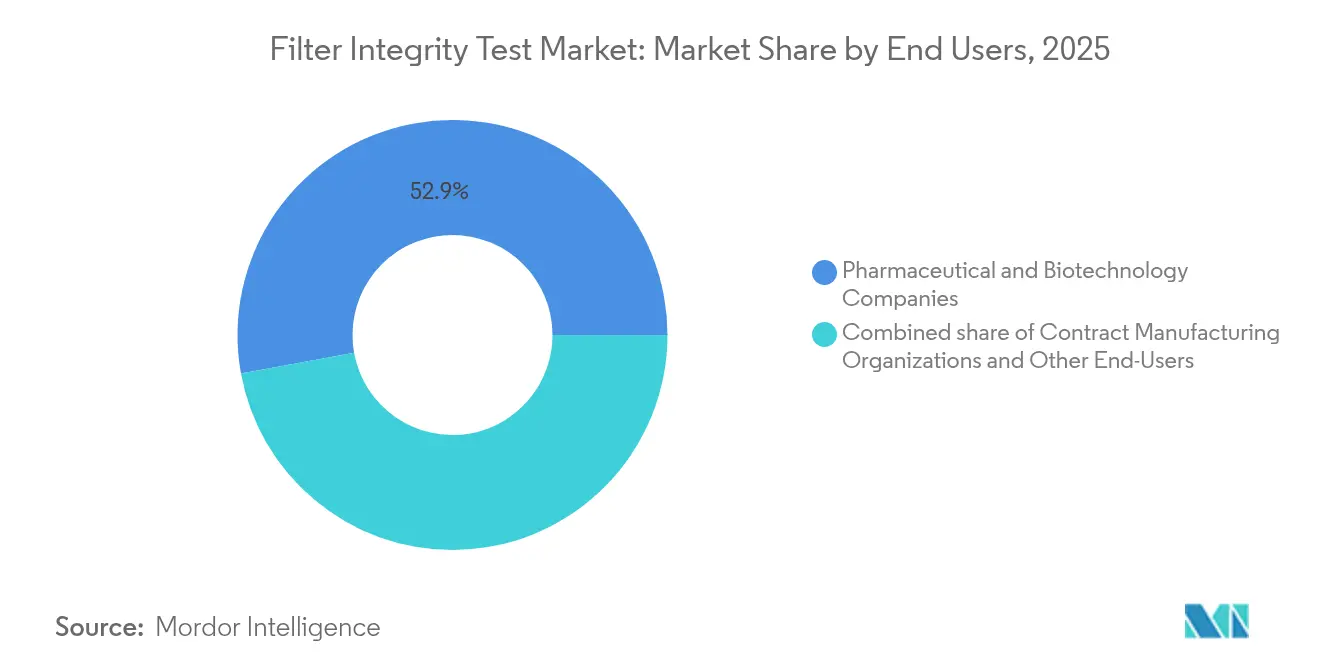

- By end user, pharmaceutical and biotechnology firms contributed 52.86% demand in 2025; contract manufacturing organizations post the highest 8.55% CAGR through 2031.

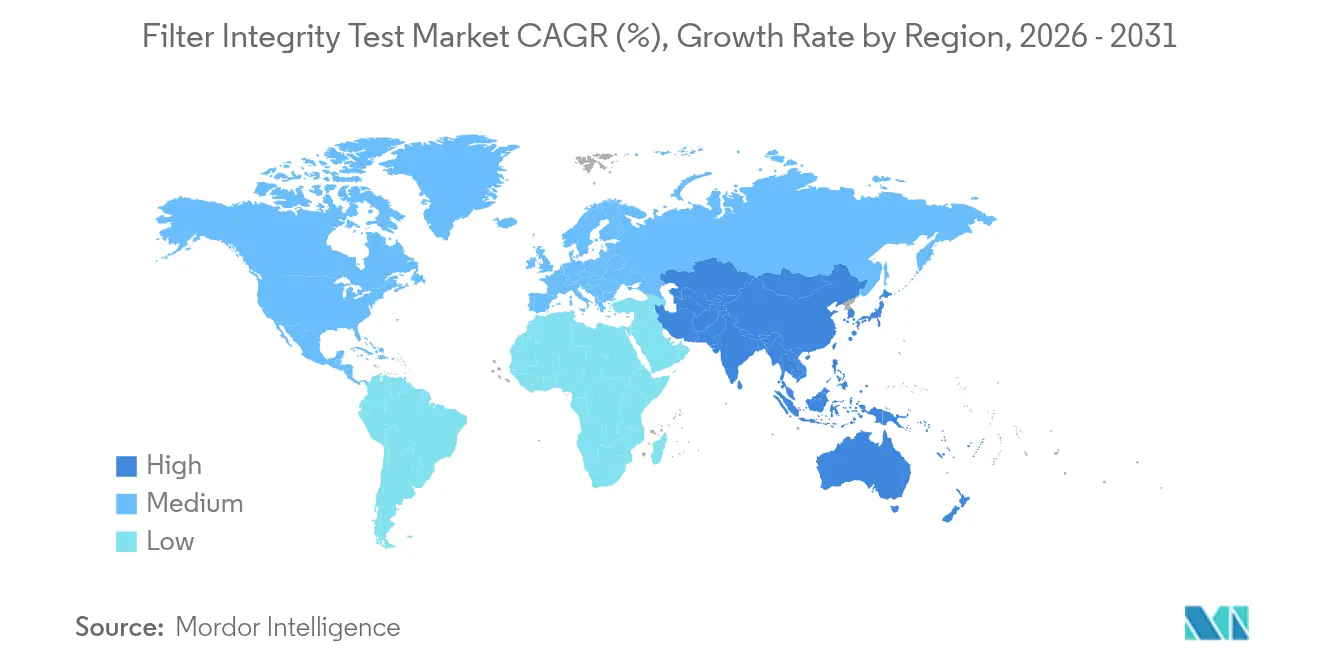

- By geography, North America retained leadership with 39.10% share in 2025, whereas Asia-Pacific is projected to record a 6.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Filter Integrity Test Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global biopharmaceutical capacity | +1.2% | APAC, North America, EU | Medium term (2-4 years) |

| Regulatory mandates for sterile compliance | +0.9% | North America, EU, Global | Short term (≤ 2 years) |

| Rising adoption of single-use filtration | +0.8% | Developed markets, Global | Medium term (2-4 years) |

| Food and beverage safety investments | +0.5% | EU, Global | Long term (≥ 4 years) |

| Expansion of high-potency & advanced therapies | +0.7% | North America, EU, APAC | Long term (≥ 4 years) |

| Digitalization of quality control analytics | +0.6% | Developed markets, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Global Biopharmaceutical Production Capacity

Surging construction of large-scale bioreactors amplifies demand for Filter Integrity Test market solutions as firms validate ever-greater filtration surface areas. More than 16.5 million L of active capacity now spans 1,500+ facilities worldwide, with APAC adding the largest blocks of stainless-steel and single-use suites[1]“Global Forecast: Filter Integrity Test Equipment to 2030,” BioProcess International, bioprocessintl.com. Chinese producers report that 90% plan to export globally within a decade, mirroring 100% of surveyed Indian peers. High-profile projects such as Samsung Biologics’ USD 1.46 billion fourth plant in Incheon and Fujifilm Diosynth’s USD 3.2 billion expansions in Denmark and North Carolina illustrate the multi-site build-outs that each require hundreds of automated testers. These installations emphasize throughput, driving preference for self-diagnosing systems capable of parallel test execution and instant electronic release.

Regulatory Mandates for Sterile Manufacturing Compliance

Regulators elevate integrity testing from best practice to explicit requirement, tightening timelines for market authorization. EMA Annex 1 now obliges Pre-Use Post-Sterilization Integrity Testing for sterile drug filters, materially increasing test frequency in European plants. U.S. FDA guidance on data integrity for bioequivalence studies stipulates complete, accurate, contemporaneous electronic records, spurring upgrades to 21 CFR Part 11-compliant instruments[2]U.S. Food and Drug Administration, “Data Integrity and Compliance with Drug CGMP,” federalregister.gov. Harmonized microbial limits, such as the FDA’s ≤ 10 CFU/100 mL bioburden threshold before final filtration, institutionalize routine verification cycles across biologics and vaccine lines.

Rising Adoption of Single-Use Filtration Systems

Disposable assemblies reshape the Filter Integrity Test market by introducing sealed, gamma-irradiated filter capsules that cannot undergo repeated wetting-drying cycles. FDA endorsements during COVID-19 response highlighted their role in rapid scale-up. Yet integrity verification must occur once, pre-use, without compromising sterility. Automated testers with low internal volume and remote-connectivity firmware execute short, non-destructive assessments while logging full results directly into Manufacturing Execution Systems. Suppliers integrate inline sensors to enable point-of-use leak detection, reducing operator intervention and accelerating release.

Digitalization of Quality Control and Process Analytics

Manufacturers accelerating toward Pharma 4.0 embed integrity testers into plant-wide data lakes so quality metrics update dashboards in real time, a shift that adds +0.6% to projected CAGR. Edge-enabled instruments now push JSON outputs directly to MES and LIMS platforms, shaving hours off deviation investigations and facilitating continuous-quality-verification strategies approved by regulators. Artificial-intelligence algorithms overlay live diffusion curves with historian baselines to flag drift before it triggers an out-of-spec result, letting maintenance teams rotate filter housings proactively. Suppliers bundle cyber-security hardening and encrypted time-stamps to meet 21 CFR Part 11 and EU Annex 11 clauses, ensuring electronic records remain tamper-evident. Together these features reduce manual data handling, cut transcription errors, and support real-time release testing, reinforcing the commercial case for automated platforms across both legacy and greenfield sites within the Filter Integrity Test market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of automated instruments | -0.8% | Emerging markets, Global | Short term (≤ 2 years) |

| Limited skilled GMP testing workforce | -0.6% | APAC, Global | Medium term (2-4 years) |

| Data-integrity risks in legacy software | -0.4% | Mature markets, Global | Medium term (2-4 years) |

| Environmental concerns over single-use waste | -0.3% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Automated Test Instruments

Cutting-edge integrity testers that conform to EMA Annex 1 can exceed USD 100,000 per unit, discouraging smaller facilities from immediate adoption. Instruments such as the explosion-proof Sartocheck 5 Plus bundle risk-management software, auto-fail-safe logic, and encrypted audit-trails, but the upfront cash outlay remains substantial. Leasing models and pay-per-test service contracts have emerged to lower entry barriers, although uptake in price-sensitive regions still lags.

Limited Skilled Workforce for GMP Integrity Testing

Accelerated facility builds, specifically in Asia-Pacific, outpace the availability of certified QC analysts versed in Annex 1, ICH Q9, and 21 CFR Part 11. Retirements in North American plants compound shortages. ISPE benchmarking highlights elevated overtime rates in microbiology labs, raising data-integrity risk profiles[3]International Society for Pharmaceutical Engineering, “Talent Shortage Survey,” ispe.org. Companies respond with digital SOP platforms and augmented-reality training that halve onboarding time yet require capital and cultural change.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automated Systems Drive Market Evolution

Automated testers captured 56.88% of Filter Integrity Test market share in 2025 on the back of universal data-integrity mandates. They are simultaneously the fastest-growing at a 7.52% CAGR through 2031 as firms phase out manual rigs that lack electronic record keeping. Leading platforms integrate pre-programmed PUPSIT cycles, remote diagnostics, and predictive maintenance alerts, boosting equipment uptime and batch-release velocity. Manual devices persist in pilot plants and low-volume nutraceutical operations where budget constraints outweigh compliance pressure. Nevertheless, falling sensor costs and cloud-native analytics narrow the total-cost-of-ownership gap, accelerating the switch to automation during facility refurbishments. Across global installations, automated instruments now represent the default specification for any greenfield biologics expansion.

Second-generation units embed artificial-intelligence algorithms that recognize atypical diffusion curves, auto-flagging potential membrane damage before a catastrophic breach can contaminate product. Suppliers validate firmware under GAMP 5 to streamline 510(k) approvals for devices shipped into regulated U.S. lines. This evolution positions automated systems as the linchpin of enterprise-wide electronic Quality Management Systems, cementing their dominance in the filter integrity test market.

By Test Type: Water Intrusion Testing Gains Momentum

Bubble point remains the gold-standard hydrophilic membrane assay with 40.75% share; however water intrusion testing (WIT) leads growth at a 7.12% CAGR. WIT verifies hydrophobic filters without the wetting and drying steps that jeopardize sterility, making it indispensable for cell- and gene-therapy suites running multi-product campaigns. Enhanced algorithmic baselining compensates for humidity fluctuations, broadening WIT’s deployability across climate zones. Diffusion/forward-flow protocols retain relevance for validating low-surface-area filters in high-potency drug manufacture, while pressure-hold tests confirm mechanical stability under surge conditions. Over the forecast horizon, WIT adoption is poised to eclipse diffusion in new hydrophobic filter installations, reinforcing its status as the segment’s growth engine within the Filter Integrity Test market size.

By Mechanism : Acoustic Technologies Reinforce Non-Destructive Testing Goals

Pressure-based techniques commanded 61.72% of Filter Integrity Test market share in 2025 because regulators have long accepted their reliability and straightforward validation protocols. In day-to-day biopharmaceutical operations they remain the default choice for hydrophilic and hydrophobic membranes alike, especially in high-throughput vaccine-fill suites where cycle time is tightly controlled. Continuous software refinements now let modern pressure rigs auto-compensate for temperature drift, tightening test repeatability margins and shortening engineer sign-off loops. The 61.72% dominance nonetheless masks a subtle shift in customer wish-lists: manufacturers want methods that probe microscopic defects without wetting membranes or exposing sterile assemblies to external gases.

That preference fuels the 8.05% CAGR logged by acoustic/sonic approaches through 2031, positioning them as the most dynamic slice of the Filter Integrity Test market. Ultrasonic bubble-detection arrays and resonance-frequency scans supply contact-free verification, a feature prized in cell-therapy plants that cannot tolerate even trace contaminants. Vendors pair these probes with cloud dashboards that trace resonance signatures batch-by-batch, enabling predictive analytics that spot gradual membrane fatigue weeks before yield dips. Marker-based and visualization methods hold niche roles—such as fluorescent dyes for academic method development—but their combined footprint stays modest because they lack the throughput and data-integrity automation of pressure and acoustic platforms. Over the forecast horizon, suppliers are expected to embed dual-mode heads that let operators toggle between pressure and acoustic modes, allowing one instrument to satisfy legacy compendial tests while future-proofing against next-generation non-destructive standards.

By Filter Type : Liquid Filtration Remains the Volume Engine

Liquid filters generated 67.90% of the Filter Integrity Test market size in 2025 due to the pharmaceutical sector’s near-universal use of sterile liquid processing for injectables, monoclonal antibodies, and mRNA therapeutics. Each aseptic fill line may deploy up to five sequential sterile liquid filters, a configuration that amplifies integrity-test counts and cements liquids as the segment’s revenue anchor. Rising titres in fed-batch and perfusion bioreactors raise viscosity, prompting manufacturers to install larger surface-area cartridges that—once sterilized—require bubble-point or diffusion confirmation before every lot release. Regulatory guidelines insisting on Pre-Use Post-Sterilization Integrity Testing intensify test frequency and sustain the 7.27% CAGR forecast for liquid filters through 2031.

Air and gas filters play a smaller but indispensable role in maintaining Grade A laminar-flow zones, venting bioreactors, and protecting lyophilizers from airborne bioburden. Although this niche commands fewer units, it demands high-sensitivity instruments capable of detecting sub-micron breaches that could trigger costly batch losses. Device makers respond with modular test modules that switch seamlessly between liquid and gas modes, letting QC teams consolidate equipment fleets while meeting both liquid- and air-filtration protocols. Long term, environmental monitoring initiatives inside isolators may divert a fraction of budget toward real-time, in-line aerosol particle sensors, yet liquid filtration will continue to deliver the bulk of absolute unit growth for the Filter Integrity Test market.

By End Users : CDMOs Shape Outsourcing-Led Growth

Pharmaceutical and biotech license-holders generated 52.86% of 2025 demand, reflecting their legal accountability for product sterility and their entrenched investment in on-site QC laboratories. These firms standardize on automated testers that interface with electronic batch records, limiting reviewer cycle times and reducing FDA Form 483 observations tied to paper data. However, contract manufacturing organizations are expanding fastest, posting an 8.55% CAGR that reshapes buying power dynamics within the Filter Integrity Test industry. Multi-client campuses in China, India, and the United States scale up single-use processing suites to woo advanced-therapy sponsors, and every added cleanroom bay requires its own fleet of integrity testers compliant with Annex 1 PUPSIT clauses.

CDMOs’ business model relies on audit readiness across a spectrum of international guidelines, so they gravitate to platforms offering one-click retrieval of 21 CFR Part 11 audit trails and harmonized SOP libraries. Food-and-beverage processors, medical-device assemblers, and specialist micro-electronics fabs round out the customer base but each has unique validation scripts centred on HACCP, ISO 13485, or IEST standards. Suppliers increasingly package sector-specific firmware and calibration kits, enabling a single tester chassis to pivot among end-market verticals by swapping test recipes. This configurability helps vendors defend margins while addressing the heterogenous workflow needs of an outsourcing-heavy marketplace.

By Application : Liquid Filtration Integrity Testing Dominates Regulatory Workflows

Liquid filtration integrity testing represented 60.98% Filter Integrity Test market share in 2025 and is growing at an 8.34% CAGR because injectable-drug manufacturers must certify sterility for every lot released to the public. Annex 1 expressly labels pressure monitoring a critical process parameter, obliging QC teams to confirm acceptable diffusion limits under worst-case flow and pressure settings for each filter train. Modern auto-testers store individual membrane serial numbers and tie result files directly to batch IDs, giving Qualified Persons immediate visibility for disposition decisions.

Air-filtration integrity checks, while fewer per plant, are mission-critical in freeze-drying, lyophilization, and aseptic isolator applications where airborne spores threaten product sterility. Failures here often force terminal sterilisation or outright batch discard, so operators rely on hypersensitive acoustic modules fine-tuned for low-flow vent filters. Looking forward, integrators plan to co-locate integrity analytics with real-time pressure and conductivity sensors, forming closed-loop control networks that can trigger automated hold-points if mid-batch filter stress exceeds validated envelopes. Such digital twins will extend the leadership of liquid filtration in the Filter Integrity Test market while giving air-side applications a more predictive QA toolset.

Geography Analysis

North America led the Filter Integrity Test market with 39.10% share in 2025, anchored by stringent FDA oversight and continuous biologics pipeline funding. Mandated data-integrity audits catalyze replacement cycles toward 21 CFR Part 11-ready instruments. Biotech clusters across Massachusetts and North Carolina embed automated testers into digitally native “factory-of-the-future” footprints, raising regional penetration rates. High vaccine-fill volumes sustain recurrent service contracts that boost aftermarket revenue streams.

Europe follows closely, propelled by EMA Annex 1’s compulsory PUPSIT clause that elevates test counts per filter to an all-time high. Investments such as Merck KGaA’s €62 million Darmstadt QC facility expand local capacity for on-site calibration, shortening downtime for German and Swiss manufacturers. Sustainability discourse intensifies R&D into recyclable polymer housings and bio-based membranes, offering longer-term differentiation to European suppliers.

Asia-Pacific is the fastest-growing region with a 6.41% CAGR projected through 2031 as China, India, and South Korea race toward global GMP parity. Large-scale CDMO campuses in Shanghai, Hyderabad, and Daejeon standardize on automated testers to satisfy prospective U.S. and EU regulators. Government incentives covering up to 40% of equipment expenditures accelerate adoption, positioning APAC to narrow the installed-base gap with mature markets. Simultaneously, rising semiconductor fabrication in Singapore and Taiwan opens adjacent revenue channels for ultrapure-water filter testing, broadening geographic demand diversity across the Filter Integrity Test market.

Competitive Landscape

The Filter Integrity Test industry displays moderate concentration, with the top five vendors controlling roughly 55% of global revenue. Strategic M&A reinforces scale advantages: Thermo Fisher’s USD 4.1 billion purchase of Solventum’s filtration assets augments its chromatography and testing portfolio and deepens end-to-end biologics workflows. Danaher combined Cytiva and Pall into a USD 7.5 billion bioprocess entity, unifying media, filtration, and integrity-test offerings and pledging USD 1.5 billion for capacity expansions across 13 sites.

Technology differentiation centers on embedded analytics, AI-driven anomaly detection, and Ethernet-enabled edge connectivity. New patents cover acoustic resonance methods that can detect micro-cracks below 2 µm without wetting agents.

Vendors pair hardware with cloud-based compliance dashboards offering real-time audit readiness, an increasingly decisive factor in CDMO purchasing. Smaller specialists emphasize service responsiveness and filter-specific calibration libraries to remain competitive. Overall, pricing remains stable as quality-assurance imperatives outweigh cost savings in purchasing decisions.

Filter Integrity Test Industry Leaders

Merck KGaA

3M

Sartorius AG

Meissner Filtration Products Inc.

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher acquired Solventum’s purification and filtration business for USD 4.1 billion, adding high-flux membranes and integrity testers aimed at biologics manufacturing.

- October 2024: Asahi Kasei Medical released the Planova FG1 virus-removal filter offering seven-fold higher flux for biologics processing.

- August 2024: Donaldson bought a 49% stake in Medica S.p.A. for €62 million (USD 67 million) to access hollow-fiber technology for medical devices and water purification.

- July 2024: IDEX acquired Mott Corporation for USD 1 billion, strengthening its presence in sintered porous filtration for semiconductor and energy applications.

- June 2024: Pall opened a USD 150 million plant in Singapore dedicated to lithography and wet-etch filtration for semiconductor production.

Global Filter Integrity Test Market Report Scope

As per the scope of the report, a filter integrity test is used to check the integrity of filters. It is performed before and after the filtration process. The Filter Integrity Test Market is Segmented by Product Type (Manual and Automated), Test Type (Diffusion Test, Bubble Point Test, Pressure Test, and Other Test Types), Application (Air Filters and Liquid Filters), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Manual |

| Automated |

| Bubble Point Test |

| Diffusion / Forward-Flow Test |

| Pressure / Hold Test |

| Water Intrusion Test |

| Other Tests Types |

| Pressure-based |

| Marker-based |

| Visualization |

| Acoustic / Sonic |

| Liquid Filters |

| Air / Gas Filters |

| Pharmaceutical and Biotechnology Companies |

| Contract Manufacturing Organizations |

| Other End Users |

| Liquid Filtration Integrity |

| Air Filtration Integrity |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Manual | |

| Automated | ||

| By Test Type | Bubble Point Test | |

| Diffusion / Forward-Flow Test | ||

| Pressure / Hold Test | ||

| Water Intrusion Test | ||

| Other Tests Types | ||

| By Mechanism | Pressure-based | |

| Marker-based | ||

| Visualization | ||

| Acoustic / Sonic | ||

| By Filter Type | Liquid Filters | |

| Air / Gas Filters | ||

| By End Users | Pharmaceutical and Biotechnology Companies | |

| Contract Manufacturing Organizations | ||

| Other End Users | ||

| By Application | Liquid Filtration Integrity | |

| Air Filtration Integrity | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Filter Integrity Test market by 2031?

The Filter Integrity Test market is set to reach USD 114.29 million by 2031, expanding at a 5.16% CAGR.

Which test type is growing fastest in upcoming years?

Water intrusion testing is the fastest-growing test type, posting a 7.12% CAGR through 2031.

Why are automated integrity testers gaining traction?

Automated systems generate electronic audit trails, cut human error, and now account for 56.88% market share with a 7.52% growth rate.

Which region will expand quickest?

Asia-Pacific is forecast to grow at a 6.41% CAGR thanks to large-scale biopharmaceutical capacity expansion and GMP harmonization.

How are sustainability concerns affecting integrity testing?

EU and North American regulations focusing on plastic waste spur R&D into recyclable filter housings and bio-based membranes, influencing future equipment specifications.

Who recently invested heavily in filter technology capacity?

Danaher earmarked USD 1.5 billion to expand Cytiva and Pall manufacturing across 13 locations, underscoring confidence in long-term demand.

Page last updated on: