Membrane Filters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.63 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Membrane Filters Market Analysis by Mordor Intelligence

The Membrane Filters Market size is estimated at USD 8.63 billion in 2026, and is expected to reach USD 12.12 billion by 2031, at a CAGR of 7.03% during the forecast period (2026-2031).

Rising investments in municipal and industrial wastewater treatment, single-use biopharma production lines, semiconductor ultrapure-water upgrades, and direct-lithium-extraction plants are expanding the membrane filters market footprint. Tightening discharge regulations for PFAS and nutrients, paired with incentives for high-recovery desalination in the Middle East, are steering end users toward membranes that combine high selectivity with lower energy consumption. Leading suppliers secure long-term contracts by bundling membranes, housings, skid integration, and cloud-based performance monitoring, while start-ups target niches such as direct nanofiltration, ceramic ultrafiltration, and modular single-use assemblies. Asia-Pacific leads current demand and offers the steepest growth curve, followed by North America and the Gulf states where PFAS compliance deadlines and megascale desalination programs anchor order books.

Key Report Takeaways

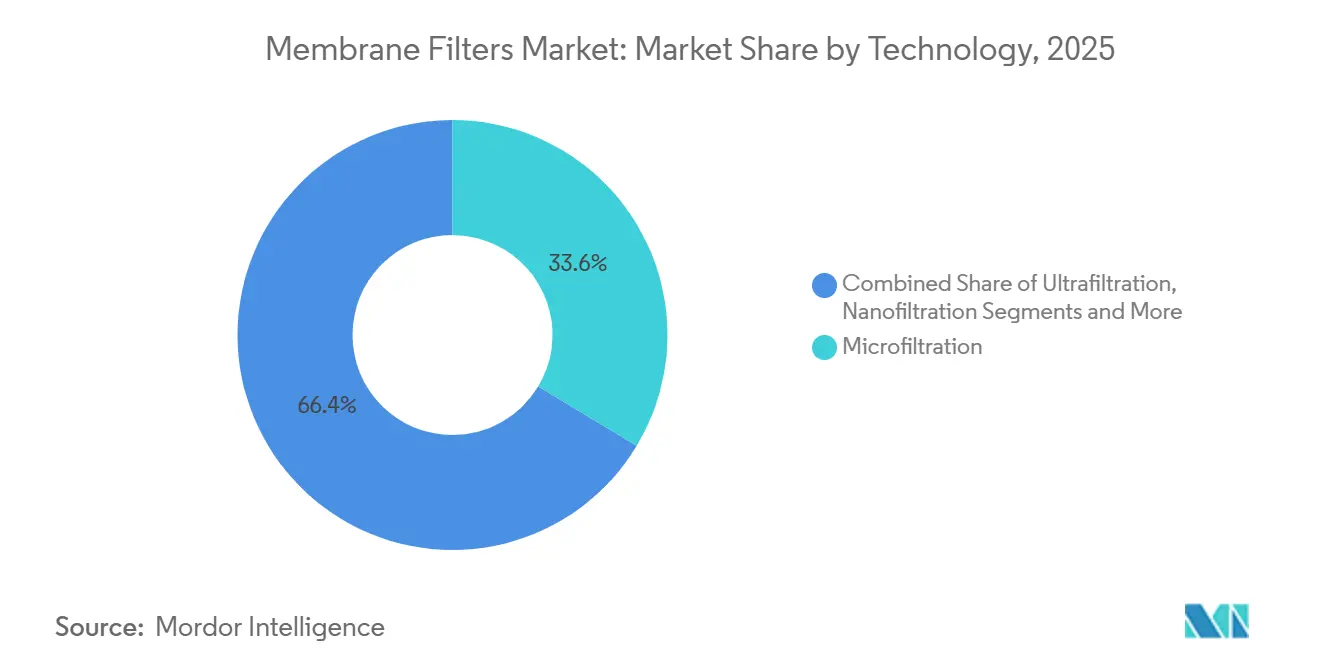

- By technology, microfiltration captured 33.62% of the membrane filters market share in 2025; nanofiltration is projected to expand at a 9.25% CAGR through 2031.

- By material, polyethersulfone accounted for 28.37% of the membrane filters market size in 2025, while ceramic and metallic membranes are advancing at an 8.24% CAGR.

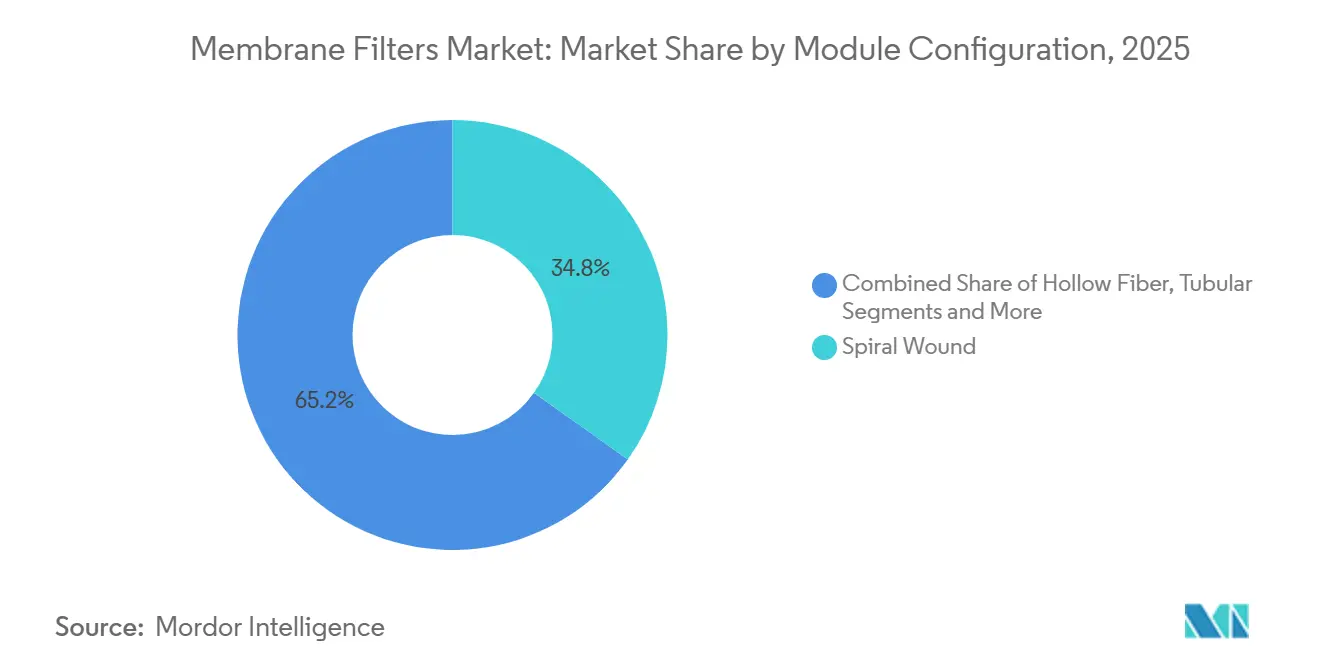

- By module configuration, spiral-wound units held 34.82% share in 2025, and hollow-fiber formats are rising at 7.82% CAGR.

- By application, water and wastewater treatment represented 42.21% revenue in 2025; micro-electronics ultrapure-water systems are forecast to grow at an 8.36% CAGR.

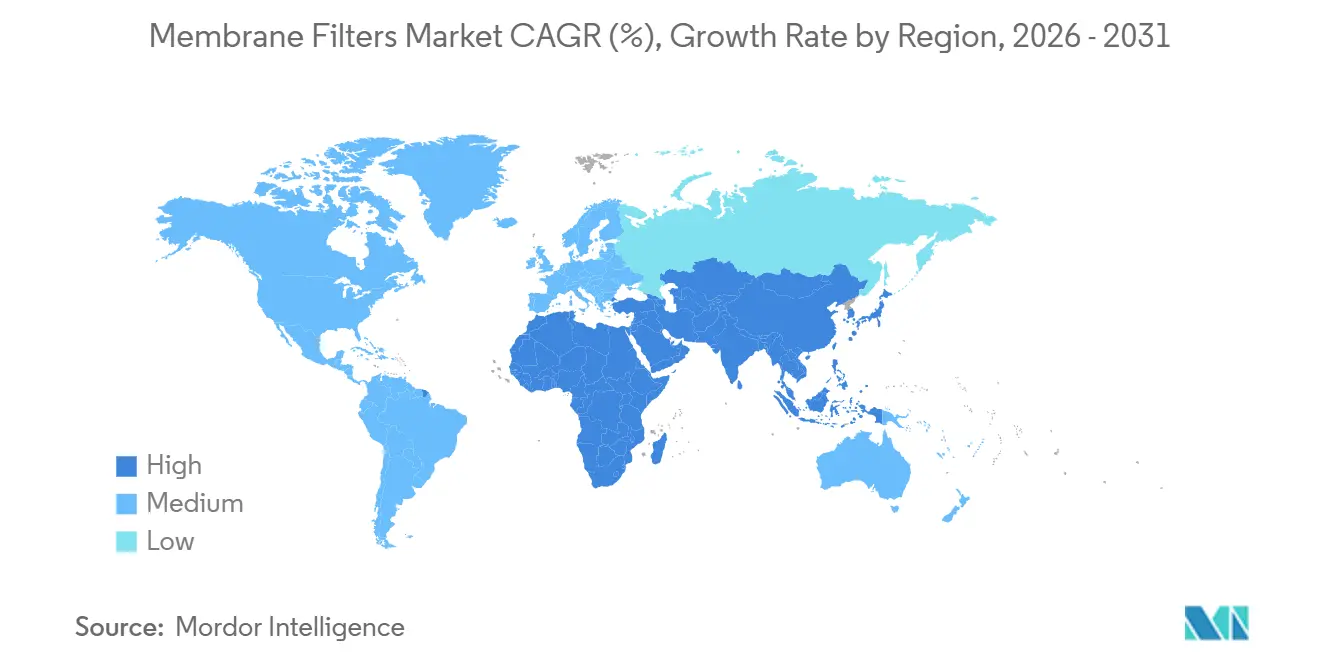

- By geography, Asia-Pacific dominated with 38.14% share in 2025 and is expected to post a 9.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Membrane Filters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict discharge norms for municipal and industrial wastewater | +1.2% | EU, North America, coastal China | Medium term (2-4 years) |

| Rising biopharma production volumes globally | +1.0% | North America, Europe, China, India, South Korea | Short term (≤2 years) |

| Food-grade filtration mandates in emerging economies | +0.6% | India, Southeast Asia, Latin America | Medium term (2-4 years) |

| CAPEX incentives for desalination projects (MENA) | +0.9% | UAE, Saudi Arabia, Qatar, North Africa | Long term (≥4 years) |

| Rapid uptake of single-use tangential-flow skids | +0.8% | North America, Western Europe, APAC biopharma hubs | Short term (≤2 years) |

| Lithium-extraction by direct-lithiation membranes | +0.5% | U.S., Argentina, Chile | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Strict Discharge Norms For Municipal & Industrial Wastewater

Regulators worldwide are lowering allowed contaminant thresholds, compelling utilities and factories to retrofit membrane bioreactors and advanced nanofiltration trains. The U.S. Environmental Protection Agency capped PFOA and PFOS at 4 ppt in April 2024, requiring full compliance by 2029.[1]U.S. Environmental Protection Agency, “Final PFAS National Primary Drinking Water Regulation,” EPA, epa.gov Similar moves by India’s Central Pollution Control Board are pushing tier-2 cities toward membrane upgrades. Project owners now budget for concentrate management options such as thermal oxidation or evaporative crystallization, each costing USD 2 million–10 million per site.

Rising Biopharma Production Volumes Globally

Biologic pipelines outstrip small-molecule launches, and virus filtration, buffer exchange, and sterile polishing rely on 0.1–0.2 µm pore-size membranes. FDA’s Q5A(R2) update in January 2024 reaffirmed virus filtration as a validated step, nudging contract manufacturers toward higher-capacity single-use skids.[2]U.S. Food & Drug Administration, “Q5A(R2) Viral Safety Evaluation,” FDA, fda.gov India’s Production Linked Incentive program earmarked INR 15,000 crore (USD 1.8 billion) to expand domestic biologics capacity, widening the addressable membrane filters market.[3]Government of India, “Production Linked Incentive Scheme for Pharmaceuticals,” Government of India, india.gov.in

Food-Grade Filtration Mandates In Emerging Economies

New hygiene standards for dairy and juice exports in Southeast Asia and Latin America require low-bacterial-count processing, accelerating sales of microfiltration and ultrafiltration cartridges certified under NSF/ANSI 61. Local processors previously relying on plate filters now retrofit hollow-fiber modules to meet export audit requirements.

CAPEX Incentives For Desalination Projects (MENA)

GCC governments back multibillion-dollar seawater reverse-osmosis initiatives. Dubai’s USD 920 million Hassyan plant will deliver 180 million IGD by 2027. NEOM is piloting high-recovery RO exceeding 60% to curb brine discharge. Incentives include 25-year offtake agreements, elevating bid volumes for thin-film-composite spiral-wound membranes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane fouling and cleaning-chemical cost burden | -0.8% | Global, acute in high-solids wastewater and food processing | Short term (≤2 years) |

| Validation delays for GMP upgrades in pharma | -0.5% | North America, Europe, emerging APAC pharma hubs | Medium term (2-4 years) |

| PFAS disposal risk from concentrate streams | -0.6% | North America, Western Europe | Medium term (2-4 years) |

| Supply-chain crunch for high-grade PES resin | -0.4% | Global bottlenecks in specialty-polymer production | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling & Cleaning-Chemical Cost Burden

Flux loss of 30–50% within weeks forces weekly or monthly clean-in-place cycles that cost USD 500–2,000 per module. Over a five-year life, cleaning chemicals can equal initial membrane capital. Ceramic ultrafiltration, such as Nanostone’s CM-151, extends cleaning intervals to three months and achieves 95% recovery, yet higher CAPEX slows adoption.

Validation Delays For GMP Upgrades In Pharma

Regulators mandate re-validation when facilities swap bulk filters for single-use variants. Complex documentation cycles can delay commercial runs by six to nine months, temporarily dampening membrane filters market orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Nanofiltration’s Climb Toward Higher Recoveries

In 2025, microfiltration retained 33.62% share of the membrane filters market. Its broad use in municipal clarification, dairy protein fractionation, and biopharma harvest steps anchors demand, with pore sizes from 0.1 to 10 µm ensuring low pressure drops. Nanofiltration has become the fastest-growing slice at 9.25% CAGR as operators seek divalent-ion and micropollutant rejection while passing monovalent salts. The membrane filters market size allocated to nanofiltration is forecast to widen as direct configurations bypass conventional coagulation and media filters. NX Filtration’s hollow-fiber 1–2 nm pores cut chemical dosing by 80% and lower energy needs by 20%. Reverse osmosis remains mission-critical for seawater desalination and semiconductor ultrapure water, yet the entry of high-recovery NF pretreatment trains allows RO stages to run at lower pressures, extending element life.

Nanofiltration’s momentum spills into wastewater reuse, industrial water loops, and PFAS remediation. U.S. utilities bidding on EPA compliance view NF as a cost-competitive alternative to granular activated carbon when paired with advanced oxidation. In brackish-water desalination, NF lifts overall recovery to >85% by shedding hardness before RO. Growth also tracks lithium brine polishing, where NF removes magnesium and sulfate to protect downstream ion-exchange beads. As cost curves fall, nanofiltration may edge into low-pressure RO domains, eroding microfiltration’s share in pretreatment lines.

By Material: Ceramic Membranes Challenge Polymer Mainstays

Polyethersulfone posted 28.37% revenue share in 2025 owing to 180 °C heat tolerance and pH resilience, serving single-use bioprocess cassettes. The membrane filters market size tied to PES benefits from compatibility with gamma sterilization and long shelf life. Ceramic and metallic membranes, advancing at an 8.24% CAGR, threaten polymer dominance in high-solids or high-temperature fluids. Alumina and silicon-carbide grades survive aggressive caustic washes, facilitating >10-year service life in mining and pulp-and-paper loops. LiqTech’s silicon-carbide units reclaim process water in oil-sands operations that push temperatures beyond 80 °C.

Demand for ceramic units is strongest where downtime penalties dwarf upfront CAPEX—semiconductor fabs and offshore desalination rigs count every minute of outage. Still, polymer films such as PVDF and polysulfone remain cost winners in disposable cartridges where replacement intervals fall under one year. Future material splits will hinge on lifecycle costing models rewarding durability and chemical resistance.

By Module Configuration: Hollow-Fiber Density Cuts Footprint

Spiral-wound modules controlled 34.82% of 2025 sales, fueled by automated roll-stock manufacturing and ease of plant retrofits. Hollow-fiber formats, expanding at 7.82% CAGR, deliver packing densities of up to 9,000 m²/m³, lowering space and skid steel by as much as 40%. DuPont’s 19-capillary Multibore PRO fibers, introduced in 2025, squeeze more surface area into single-use housings for gene-therapy lines. The membrane filters market share for hollow-fiber units is expected to climb further in semiconductor cleanrooms where square-foot rents top USD 3,000 per year.

Tubular modules carve out niches in viscous streams like paint recovery, while plate-and-frame designs fade as gasket complexity and manual servicing deter operators. Capsule and cartridge layouts retain relevance in sterile filtration, benefitting from fast integrity testing and low hold-up volumes. Looking ahead, hybrid modules mixing flat-sheet and fiber inserts may surface to optimize pressure drop and back-washability.

By Application: Ultrapure-Water Demand From Micro-Electronics Accelerates

Water and wastewater treatment represented 42.21% of 2025 revenue, encompassing municipal drinking-water, effluent polishing, and reuse schemes. Yet the micro-electronics segment is on an 8.36% CAGR trajectory, bolstered by silicon-wafer demand for AI data centers and electric vehicles. A single 200 mm wafer consumes up to 7,500 L of ultrapure water, and sub-3 nm nodes require silica below 0.3 ppb. The membrane filters market size dedicated to fabs climbs as chipmakers build plants in Arizona, Dresden, and Hsinchu.

Pharma and biotech remain high-value users owing to GMP validation requirements. Dairy processors, juice bottlers, and breweries add steady volumes but face margin pressure from commodity pricing. Mining and lithium extraction, alongside produced-water treatment in shale plays, emerge as growth pockets for high-durability ceramic stacks.

Geography Analysis

Asia-Pacific held 38.14% of the membrane filters market in 2025 and is poised for a 9.01% CAGR to 2031. China’s domestic-substitution push lifts local ultrafiltration and RO procurement as fabs expand 12-inch capacity at SMIC. India’s INR 15,000 crore incentive scheme spurs sterile cartridge purchases for biologics exports, and South Korea’s advanced nodes chase TOC limits under 1 ppb. Japanese suppliers leverage regional links; Toray opened a Taiwan R&D center in 2025 and delivered an ultrafiltration film that trims CO₂ emissions by 30%.

North America ranks second on the back of EPA PFAS rules, semiconductor reshoring, and early-stage lithium extraction. Intel’s net-positive water drive underpins large multistage RO orders, while ExxonMobil’s Arkansas brine project integrates direct nanofiltration to bypass ponds. Canada modernizes cold-climate membrane bioreactors, and Mexican dairies adopt UF modules to meet export audits.

Europe enforces stringent nutrient and micropollutant caps under the Urban Wastewater Treatment Directive, fueling MBR retrofits. Germany and France anchor biotech demand, and Spain expands desalination for coastal cities. Scandinavia pilots ceramic membranes for pulp-and-paper process water. The Middle East rides mega-desalination: Dubai’s Hassyan and NEOM’s pilot hinge on 99.5% salt-rejection thin-film composites. South America’s lithium triangle adopts membrane routes to cut evaporation.

Competitive Landscape

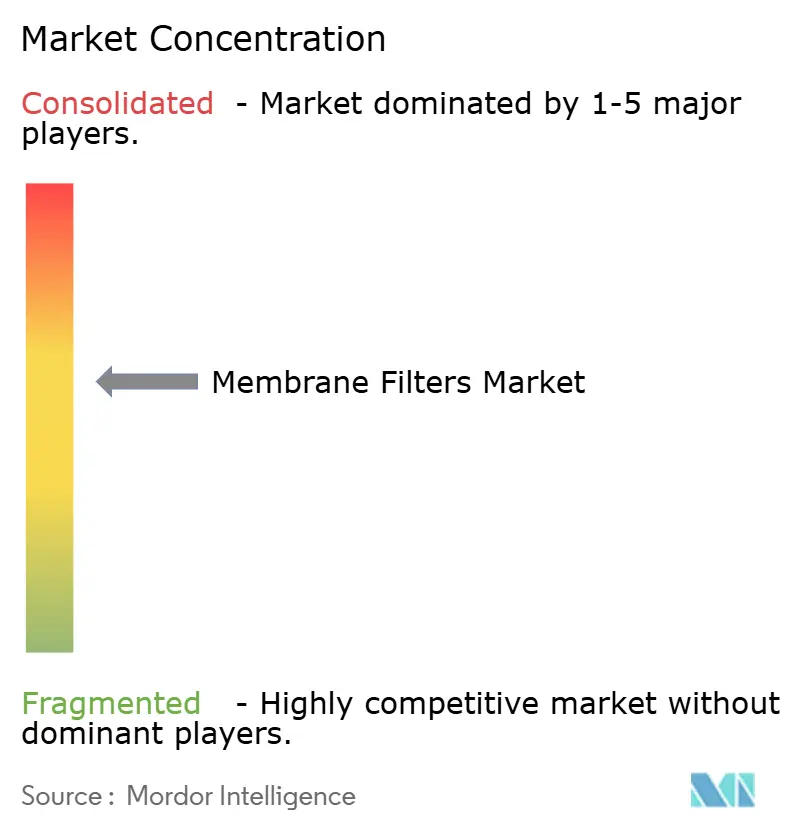

The top suppliers include DuPont, Danaher, Merck KGaA, and others, giving the membrane filters market a medium concentration. Incumbents pair vertical integration with R&D pipelines: Toray’s 2024 RO element doubled urea rejection for chip fabs, and DuPont’s Multibore PRO raised packing density in 2025. Thermo Fisher’s USD 4.1 billion takeover of Solventum’s filtration unit in February 2025 shows ongoing consolidation.

Disruptors mine white space. NX Filtration promotes direct nanofiltration that skips pre-clarification, while Nanostone’s CM-151 ceramic modules prolong cleaning cycles. Repligen scales single-use TFF skids for gene therapy. Partnerships with semiconductor toolmakers emerge as suppliers tailor filter cuts to sub-3 nm lithography steps.

Competition intensifies in biopharma disposables where switching costs are low and validation support is king. Municipal tenders favor vendors with NSF and ISO certifications plus local service crews. Growth opportunities center on ceramic stacks for harsh effluents, hollow-fiber compacts for space-limited fabs, and PFAS-capable NF membranes.

Membrane Filters Industry Leaders

Thermo Fisher Scientific

Merck KGaA

Danaher Corporation

Solventum

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Thermo Fisher closed its USD 4.1 billion acquisition of Solventum’s purification and filtration business, broadening single-use offerings

- April 2025: DuPont debuted Multibore PRO ultrafiltration, integrating 19 capillaries per fiber to cut module footprint by 20%

- April 2025: Monash University researchers produced a graphene-oxide β-cyclodextrin membrane able to capture small PFAS molecules at trace concentrations.

Global Membrane Filters Market Report Scope

As per the scope of this report, a membrane filter is a type of filter that has pores of various maximum diameters for the prevention of passage of microorganisms which has a greater size than the pores. Membrane filtration involves the use of membrane technology for the separation of biomolecules and particles for the concentration of process fluids. Membrane filtration is widely used for the elimination of microorganisms, bacteria, and organic material from water. This filtration can be applied to an infinite number of industries such as chemical processing, food, and dairy.

The Membrane Filters Market is segmented by technology, material, module configuration, application and geography. By Technology, the market is segmented into Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis, Membrane Chromatography, Forward Osmosis, Dialysis/Hemofiltration Membranes, and Others. By Material, the market is segmented into PES, PS, Cellulose-based, PVDF, PTFE, PAN, PP, Ceramic & Metallic, and Others. By Module Configuration, the market is segmented into Spiral Wound, Hollow Fiber, Tubular, Plate & Frame, Capsule/Cartridge. By Application, market is segmented into Water & Wastewater, Food & Beverage, Pharma & Biotech, Chemical & Petrochemical, Micro-electronics, Mining & Metallurgy, Others. By Geography, market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Microfiltration |

| Ultrafiltration |

| Nanofiltration |

| Reverse Osmosis |

| Membrane Chromatography |

| Forward Osmosis |

| Dialysis / Hemofiltration Membranes |

| Others |

| Polyethersulfone (PES) |

| Polysulfone (PS) |

| Cellulose-based |

| Polyvinylidene Fluoride (PVDF) |

| Polytetrafluoroethylene (PTFE) |

| Polyacrylonitrile (PAN) |

| Polypropylene (PP) |

| Ceramic & Metallic |

| Others |

| Spiral Wound |

| Hollow Fiber |

| Tubular |

| Plate & Frame |

| Capsule / Cartridge |

| Water & Wastewater Treatment |

| Food & Beverage Processing |

| Pharmaceutical & Biotechnology |

| Chemical & Petrochemical |

| Micro-electronics |

| Mining & Metallurgy |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Microfiltration | |

| Ultrafiltration | ||

| Nanofiltration | ||

| Reverse Osmosis | ||

| Membrane Chromatography | ||

| Forward Osmosis | ||

| Dialysis / Hemofiltration Membranes | ||

| Others | ||

| By Material | Polyethersulfone (PES) | |

| Polysulfone (PS) | ||

| Cellulose-based | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyacrylonitrile (PAN) | ||

| Polypropylene (PP) | ||

| Ceramic & Metallic | ||

| Others | ||

| By Module Configuration | Spiral Wound | |

| Hollow Fiber | ||

| Tubular | ||

| Plate & Frame | ||

| Capsule / Cartridge | ||

| By Application | Water & Wastewater Treatment | |

| Food & Beverage Processing | ||

| Pharmaceutical & Biotechnology | ||

| Chemical & Petrochemical | ||

| Micro-electronics | ||

| Mining & Metallurgy | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the membrane filters market by 2031?

The membrane filters market is projected to reach USD 12.12 billion by 2031.

Which technology is expected to grow fastest through 2031?

Nanofiltration is forecast to expand at a 9.25% CAGR as operators chase higher recoveries and micropollutant removal.

Why is Asia-Pacific the largest regional buyer?

The region combines rapid semiconductor fab construction, expanding biopharma exports, and aggressive municipal wastewater upgrades, yielding a 38.14% share in 2025.

How are PFAS rules influencing membrane demand in North America?

The EPA’s 4 ppt limit for PFOA and PFOS compels utilities to add nanofiltration or RO units before the 2029 deadline.

What materials are disrupting traditional polymer membranes?

Alumina, silicon-carbide, and other ceramic membranes are gaining traction where foulant loads or high temperatures shorten polymer life cycles.

Page last updated on: