Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 17.69 Billion |

| Market Size (2031) | USD 25.82 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

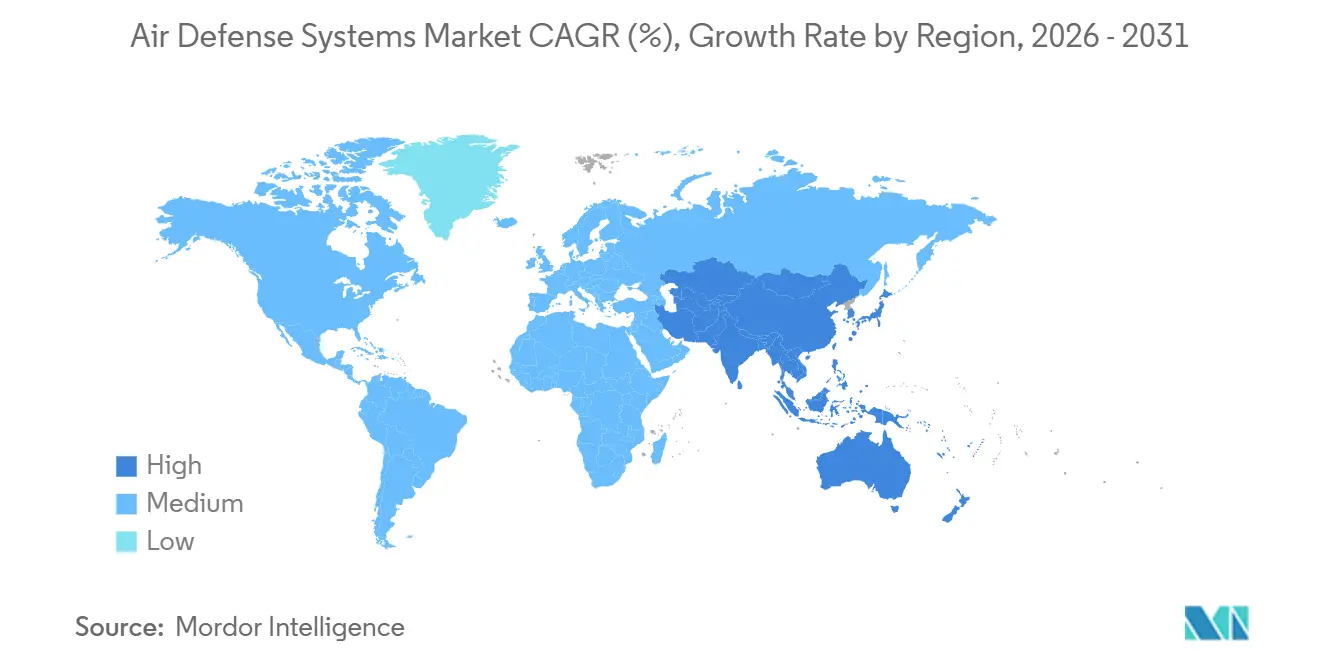

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

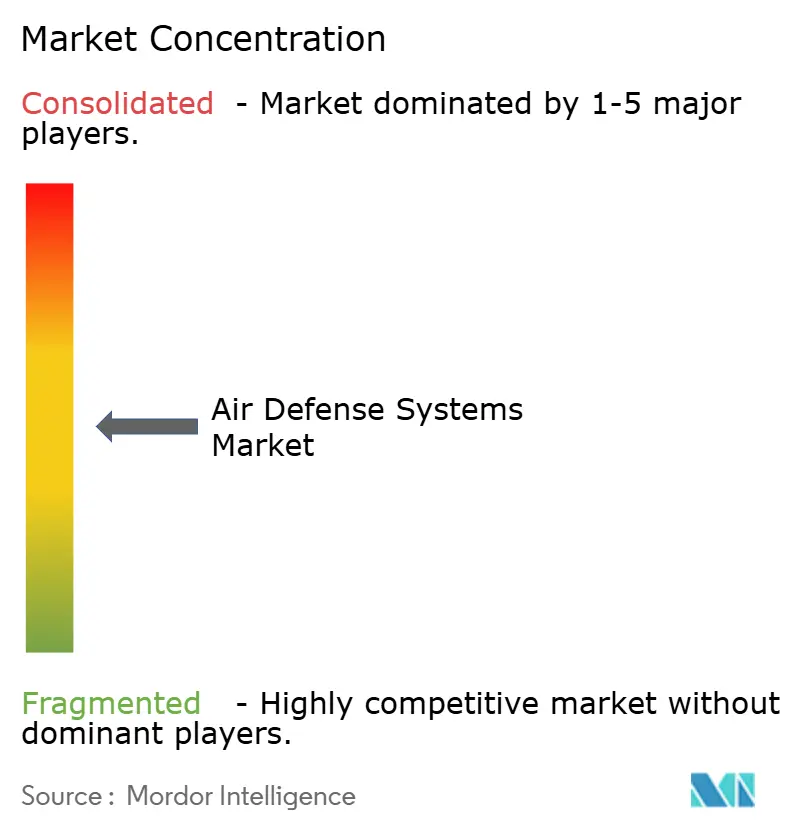

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Defense Systems Market Analysis by Mordor Intelligence

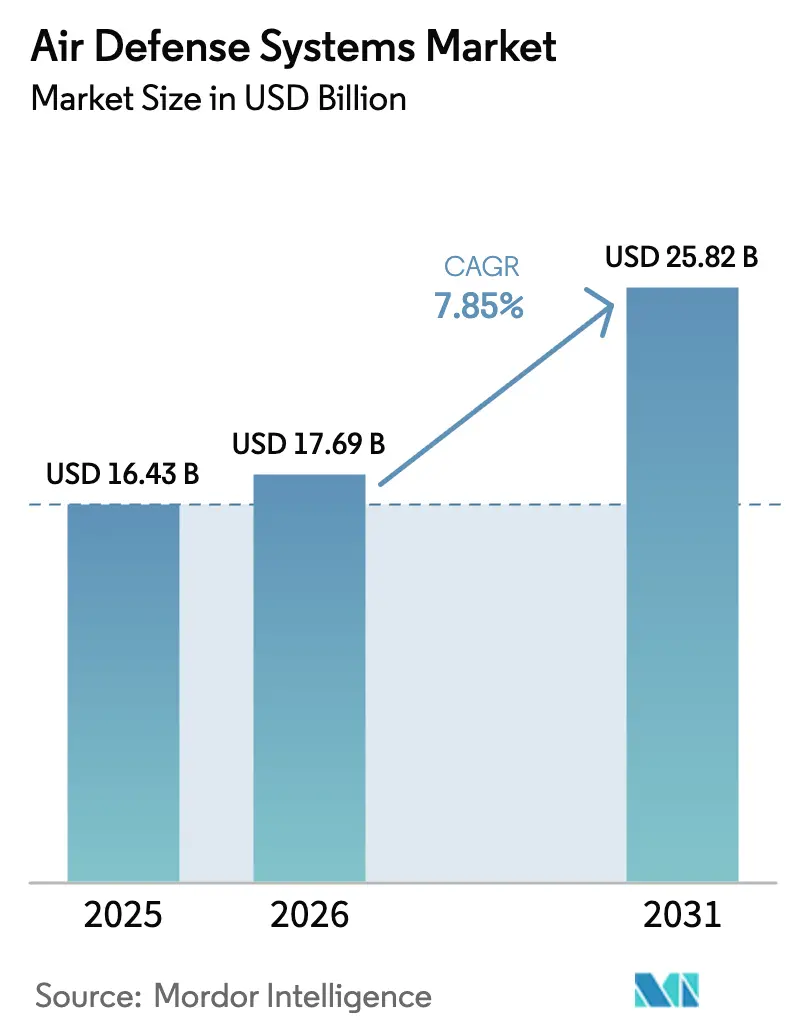

The air defense systems market size is expected to grow from USD 16.43 billion in 2025 to USD 17.69 billion in 2026 and is forecasted to reach USD 25.82 billion by 2031 at a 7.85% CAGR over 2026-2031. Demand is escalating as hypersonic glide vehicles, stealth aircraft, and autonomous drone swarms overwhelm legacy radar networks, prompting governments to accelerate the purchase of network-centric architectures that link land, sea, air, and space sensors in near real-time. NATO states have moved decisively toward layered defense; Poland’s USD 4.75 billion Patriot package and Germany’s USD 3.5 billion Arrow 3 deal illustrate the shift from single-tier batteries to interoperable interceptors that cover short, medium, and exo-atmospheric ranges. Parallel efforts in space are equally pivotal: the Space Development Agency’s 28-satellite Tracking Layer Tranche 0, operational since late 2024, delivers hypersonic tracking coverage beyond the reach of ground radars. On the technology front, the fast-growing directed-energy segment offers sub-dollar shots that redress the unsustainable economics of firing missiles worth hundreds of thousands of dollars at hobby-grade drones. Meanwhile, supply constraints on gallium nitride (GaN) semiconductors and stringent export regimes, such as ITAR and MTCR, temper near-term volume growth.

Key Report Takeaways

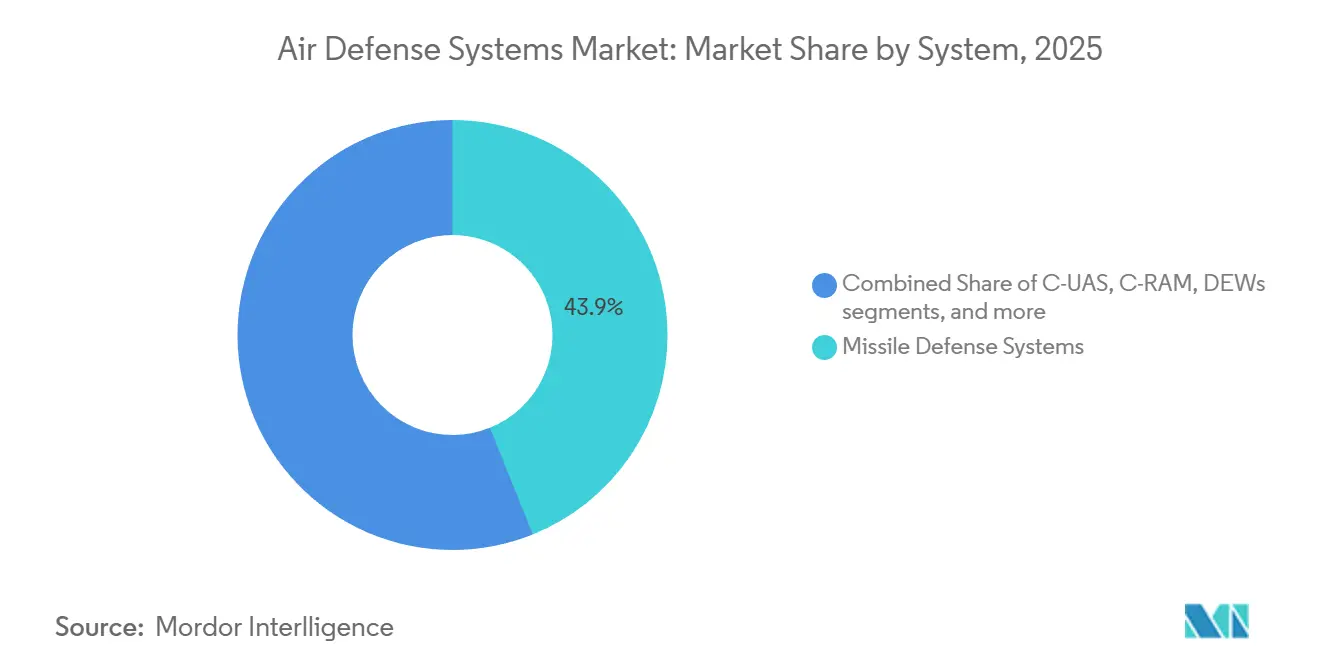

- By system type, missile defense systems held 43.91% of the air defense systems market share in 2025, while directed-energy weapons (DEWs) are projected to advance at an 11.08% CAGR through 2031.

- By platform, land-based solutions commanded 59.75% of the air defense systems market size in 2025; sea-based assets are projected to expand at a 9.0% CAGR between 2026 and 2031.

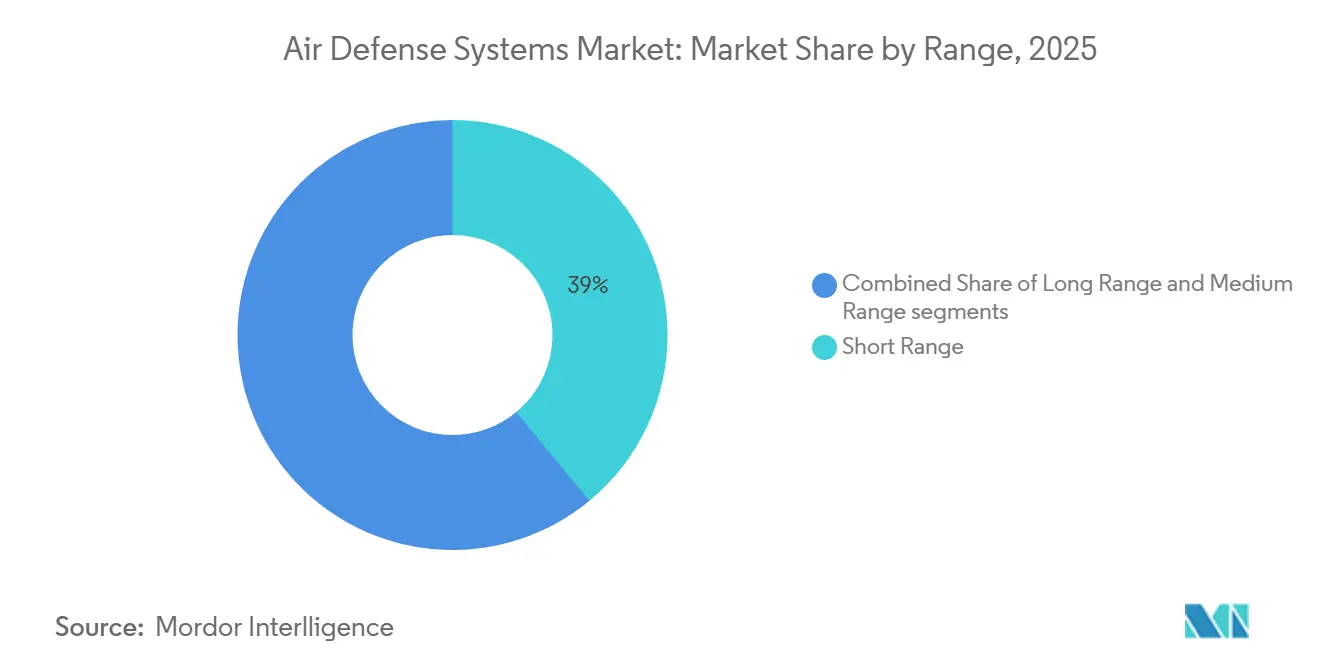

- By range, long-range interceptors accounted for 38% of the air defense systems market size in 2025 and are forecasted to grow at an 8.15% CAGR through 2031, whereas short-range counters will post slower single-digit gains.

- By subsystem, weapon systems held 25.65% of the air defense systems market share in 2025, while fire control systems are projected to expand at an 8.91% CAGR through 2031.

- By technology, kinetic-kill effectors accounted for a 42.45% share of the air defense systems market size in 2025, whereas high-power microwave systems are set to grow at a 9.55% CAGR through 2031.

- By geography, North America led the air defense systems market with a 46.62% share in 2025; the Asia-Pacific region recorded the fastest growth at a 9.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Defense Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of integrated air and missile defense procurement | +1.8% | Global, with concentration in NATO and INDOPACOM | Medium term (2-4 years) |

| Escalating spectrum of airborne threats | +1.5% | Eastern Europe, Middle East, Korean Peninsula | Short term (≤2 years) |

| AI-enabled sensor fusion for stealth detection | +1.2% | North America, Europe, Japan, South Korea, Australia | Medium term (2-4 years) |

| Mobile directed-energy SHORAD adoption | +0.9% | North America, Europe, Middle East | Medium term (2-4 years) |

| GaN-based AESA radar cost decline | +0.7% | North America and Europe lead global adoption | Long term (≥4 years) |

| Higher budgets for counter-UAS and point defense | +1.0% | Global, with spikes in Ukraine and Middle East | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Acceleration of Integrated Air and Missile Defense Procurement

Armed forces are converging once-separate radar, interceptor, and command networks into unified frameworks that share tracks across services and allies. The US Army’s Integrated Battle Command System (IBCS) links Patriot, THAAD, Sentinel, and F-35 sensors via a common software backbone, reducing engagement timelines from minutes to seconds. Europe mirrors this approach: the European Sky Shield Initiative, counting 21 members by late 2024, aligns purchases of IRIS-T SLM, Patriot, and Arrow 3 to avoid duplicative national programs. Contracts now reward integrators that can certify plug-and-play interfaces, raising entry barriers for newcomers lacking legacy protocols. Poland’s USD 4.75 billion Wisla order was explicitly designed to bundle IBCS nodes.[1]Jim Garamone, “Army Deploys IBCS to Europe,” Defense.gov, defense.gov As joint targeting moves toward real-time kill chains, satellite constellations feed birth-to-death tracks directly into ground batteries, completing the multi-domain loop.[2]Sandra Erwin, “SDA Tranche 0 Satellites Begin Operations,” SpaceNews, spacenews.com

Escalating Spectrum of Airborne Threats

Hypersonic glide vehicles, low-observable cruise missiles, and cooperative drone swarms compress reaction time to seconds, forcing the modernization of radar. Russia’s Kinzhal attacks in Ukraine accelerated deliveries of the GaN-based Lower Tier Air and Missile Defense Sensor (LTAMDS), which detects objects with radar cross-sections below 0.01 m². China’s DF-17 spurred Japan to consider THAAD batteries and to co-fund the Hypersonic and Ballistic Tracking Space Sensor program, with prototype satellites slated for 2025. Ukraine’s adaptation of USD 1,000 quadcopters into tank killers revealed the asymmetric payoff of cheap aerial platforms, prompting the US Joint Counter-small UAS Office to vet nine low-cost systems in 2024.

AI-Enabled Sensor Fusion for Stealth Detection

Machine-learning (ML) algorithms now correlate radar, infrared, and electronic support measure returns to classify elusive targets. Northrop Grumman’s IBCS software employed neural networks during Project Convergence 2024, cutting false alarms by 30% in littoral clutter. Palantir’s Apollo platform merges LTAMDS, Sentinel, and space-based IR feeds every two seconds, a five-fold improvement over legacy cycles. Israel’s Iron Dome upgrade fused UAV electro-optical imagery with ELM-2084 radar data, boosting intercept probability against maneuvering rockets by 15%. The primary friction point is bandwidth; current Link 16 data links cannot stream high-resolution synthetic aperture radar, prompting parallel investment in Link 22 and future MDO networks.

Mobile Directed-Energy SHORAD Adoption

Laser and high-power microwave effectors offer unlimited magazines and a potential cost of under USD 1 per shot, a compelling alternative to firing a USD 500,000 missile at a USD 1,000 drone. The US Army deployed four 50-kilowatt Directed Energy Maneuver-SHORAD vehicles to Europe in February 2024, each capable of defeating drones up to 5 kilometers away. The UK's DragonFire laser achieved GBP 10 (USD 13) shots during July 2024 trials, a fraction of the cost of a missile. Israel's Iron Beam, which combines a 100-kilowatt laser with Iron Dome radars, is set to enter service in late 2025 and intercept rockets within a 7-kilometer range for under USD 2 per kill. Atmospheric attenuation and thermal management remain significant challenges; continuous firing requires liquid-cooling units that add approximately 500 kg to the platform's weight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks in GaN radar modules | -0.6% | North America and Europe face acute shortages | Short term (≤2 years) |

| Stringent ITAR and MTCR export controls limiting system sales to emerging nations | -0.5% | Middle East, Southeast Asia, Latin America | Long term (≥4 years) |

| Technical and materials challenges in reliably intercepting maneuvering hypersonic targets, inflating R&D risk | -0.4% | North America, Europe, Japan, South Korea | Long term (≥4 years) |

| Electromagnetic spectrum congestion raising interoperability challenges | -0.3% | NATO and coalition operations worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks in GaN-Based Radar T/R Modules

Reliance on a handful of wafer fabs creates single-point vulnerabilities. Wolfspeed’s Mohawk Valley plant supplies over 40% of the US's defense-grade GaN wafers; any outage would ripple across the LTAMDS, SPY-6, and F-35 lines. Yield rates of roughly 65% for X-band MMICs necessitate that OEMs overbook wafers by 30%, thereby inflating inventory costs. With gallium exports now subject to Chinese quotas, average lead times for 200-mm wafers stretch to 16 weeks, delaying full radar deliveries until 2028 for orders placed in 2026.

Stringent ITAR and MTCR Export Controls Limiting System Sales to Emerging Nations

Category VIII and XI listings under ITAR require State Department licensing for any foreign sale of radar or interceptors. At the same time, the MTCR caps range above 300 kilometers, restricting exports of Patriot PAC-3 MSE and THAAD outside major allies. Ankara’s 2019 ejection from the F-35 program over S-400 procurement underscored the commercial risk of non-compliance. Work-arounds include co-production, such as Lockheed Martin’s PAC-3 MSE partnership with Mitsubishi in Japan, but that path suits only large economies willing to share tooling and intellectual property.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Directed Energy Extends the Engagement Envelope

Directed-energy architectures are projected to register an 11.08% CAGR through 2031, the fastest among major segments, reflecting the operational need for inexpensive, high-rate engagements that lasers and high-power microwave systems provide. The US Navy's 60-kilowatt Layered Laser Defense aboard USS Preble neutralized subsonic cruise missiles at ranges up to 3 kilometers at a cost of less than USD 1 per shot.[3]Valerie Insinna, “US Navy Tests Layered Laser Defense,” Naval News, navalnews.com Missile defense solutions nevertheless retained 43.91% of the air defense systems market share in 2025, underpinned by PAC-3 MSE and THAAD backlogs that extend into 2028 due to shortages of solid-rocket motors.

The air defense systems market continues to pivot toward counter-UAS, C-RAM, and high-power microwave options that promise deep magazines and low costs against saturating drone attacks. Rheinmetall's Skyranger 30, adopted by Germany in 2024, couples 30-mm airburst rounds with radar cueing to defeat quadcopters cost-effectively. The US Marine Corps' procurement of Anduril's integrated counter-UAS suite validated software-defined architectures that can update defenses through code updates rather than hardware swaps.

By Platform: Land Dominance Sustains Mobility Investments

Land configurations secured 59.75% of the air defense systems market in 2025 and are expected to grow at a CAGR of 8.21% through 2031 as armies rediscover the value of mobile SHORAD. The US Army’s IM-SHORAD roll-out of 144 Stryker-mounted launchers combines Stinger, Hellfire, and a 30-mm cannon to protect maneuver forces within an 8-kilometer radius. Europe is emulating this playbook; Boxer-mounted Skyranger turrets provide German brigades with movable drone defense that keeps pace with their armor columns.[4]Mike Yeo, “Germany Picks Skyranger for Boxer,” Rheinmetall, rheinmetall.com

Sea-based capacity benefits from Aegis upgrades; Japan’s Maya-class destroyers feature SPY-1D(V) radars and SM-3 IIA interceptors, expanding the air defense systems market at sea and ensuring regional missile coverage aligns with US assets. Airborne systems, such as the F-35’s Distributed Aperture System, add detection but not yet kinetic response, positioning them as forward sensors rather than shooters.

By Range: Long-Range Demand Accelerates

Long-range batteries are forecast to grow at an 8.15% CAGR through 2031 as hypersonic and exo-atmospheric threats proliferate. Germany’s Arrow 3 deal exemplifies Europe’s first acquisition of an exo-atmospheric layer capable of engagements beyond 100 kilometers in altitude, expanding the market for strategic interceptors. Short-range weapons still dominate numerically. Iron Dome intercepted over 90% of rockets fired in 2024 operations, validating C-RAM for highly populated areas.

Medium-range solutions remain the backbone of NATO airspace, with the Patriot PAC-3 MSE offering up to 160 kilometers of coverage, and Poland’s purchase of eight Wisla batteries highlights the importance of interoperability via IBCS. South Korea’s KM-SAM exports to the UAE demonstrate that sub-50-kilometer systems can succeed commercially when priced 30% below Western incumbents and free of MTCR constraints.

By Sub-System: Fire-Control Software Gains Momentum

Fire-control elements are posting an 8.91% CAGR as neural-network fusion becomes indispensable. IBCS has already trimmed false-alarm rates by 30% and enables cross-domain cueing in under 10 seconds, features that elevate the air defense systems industry to a software-centric paradigm. Weapon subsystems, missiles, guns, and lasers retain a 25.65% share, anchored by Lockheed Martin’s USD 1.7 billion Precision Strike Missile contract that will replace ATACMS by 2029.

Command-and-control is benefiting from Joint All-Domain Command and Control investments, as demonstrated by the US Air Force’s ABMS-linked F-35 sensors, which were able to engage Patriot firing units in 10 seconds during 2024 exercises, significantly tightening the engagement loop. Open-architecture mandates under the Modular Open Systems Approach (MOSA) are fragmenting the subsystem supply base, allowing niche power-supply or cooling vendors to win standalone contracts.

By Technology: High-Power Microwave Moves From Lab to Fleet

High-power microwave concepts are projected to register a 9.55% CAGR through 2031 as navies and armies field prototypes. The US Navy’s at-sea CHAMP trial in January 2026 successfully disabled Group 2-3 drones at distances below 2 kilometers, achieving an 85% success rate and demonstrating readiness for deck deployment. Kinetic-kill effectors still represent 42.45% of the 2025 market, as validated by ongoing production of PAC-3 MSE, THAAD, and SM-3.

EW soft-kill packages such as the Army’s Terrestrial Layer System now accompany maneuver brigades, jamming GPS and data links to neutralize drones without physical destruction. These capabilities also raise legal questions about compliance with international humanitarian law, an area where consensus remains nascent.

Geography Analysis

North America commanded 46.62% of the air defense systems market in 2025 as the US DoD outlays exceeded USD 8 billion for modernization. RTX’s USD 1.2 billion LTAMDS order for 28 radars, to be delivered by 2028, underscores its continuing investment in GaN arrays that track stealth aircraft at a range of 400 kilometers. NORAD upgrades now incorporate NASAMS batteries and Tracking Layer downlinks, expanding continental warning architecture.[5]Gerard O’Dwyer, “NORAD Modernization Steps,” NORAD, norad.mil Canada participates actively, while Mexico’s limited focus is on counter-narcotics C-UAS along the US border.

Asia-Pacific is projected to grow at a 9.76% CAGR through 2031, the highest regional pace. Japan allocated USD 2.3 billion in FY 2025 for ballistic-missile defense upgrades, including THAAD considerations and satellite tracking investments. South Korea’s KM-SAM exports to the UAE and Poland illustrate Seoul’s cost competitiveness in the mid-tier arena. India is scaling its QRSAM line to 200 missiles annually by 2027 to reduce reliance on Russian S-400s. Australia’s NASAMS order and AUKUS collaboration indicate tighter US integration, while China’s opaque HQ-9 exports to Pakistan suggest production volumes exceeding 50 batteries per year.

Europe accelerated procurement under the European Sky Shield Initiative, which enrolls 21 nations committed to interoperable layers. Germany’s Arrow 3 breakthrough diversifies suppliers beyond the United States. The UK’s DragonFire laser will start sea trials in 2027, adding directed-energy depth to naval defenses. France and Italy continue to develop the SAMP/T NG in line with NATO IAMD requirements, aiming to meet the 2028 IOC.

The Middle East remains a hotspot as Saudi Arabia’s THAAD batteries counter Houthi missiles. The UAE modernized its defense capabilities with Patriot and NASAMS while fast-tracking counter-UAS measures following the Red Sea incidents. Israel’s Iron Dome, David’s Sling, and Arrow layers maintained 90% intercept success, and Iron Beam will soon extend that envelope.

South America and Africa remain embryonic segments, as Brazil evaluates NASAMS and RBS 70 NG for Amazon border defense, while South Africa’s Umkhonto-IR supplies naval point defense amid budget constraints.

Competitive Landscape

Market concentration is moderate, with RTX Corporation, Lockheed Martin Corporation, Israel Aerospace Industries Ltd., Thales Group, and Northrop Grumman Corporation capturing about 50% of the market share in 2025, owing to their decades-long integration with legacy command-and-control (C2) systems. RTX’s 2024 revenue climbed 9% to USD 79.8 billion on LTAMDS and Patriot upgrades, while Lockheed Martin’s backlog reached USD 160 billion, ensuring multiyear production visibility. Israel Aerospace Industries disrupted the exo-atmospheric niche with the export of Arrow 3 to Germany, ending an effective US monopoly and demonstrating that allies will diversify suppliers to mitigate single-source risk.

Hanwha Systems exemplifies rising South Korean entrants: its KM-SAM undercuts Patriot by roughly 30% and sidesteps MTCR-related range barriers, enabling penetration into the Middle East. Anduril illustrates how software-centric start-ups can secure USD 640 million counter-UAS awards by layering AI and modular hardware.

Directed-energy adoption remains a competitive wild card. The US Army’s DE M-SHORAD prototypes validated 50-kilowatt lasers against Group 3 drones; however, thermal load and atmospheric effects mean that scale deployment still favors incumbents with power-management expertise. Open-architecture mandates, such as MOSA, erode incumbent lock-in by allowing niche suppliers to bid on subsystem modules, thereby fragmenting future market share. ITAR compliance continues to gatekeep emerging-market sales, preserving the oligopolistic structure in high-end interceptors while creating room for tier-two vendors in short-range segments.

Air Defense Systems Industry Leaders

RTX Corporation

Lockheed Martin Corporation

Israel Aerospace Industries Ltd.

Thales Group

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Saab secured a contract worth approximately USD 220 million from the Swedish FMV. The contract involves the provision of advanced sensors and C2 systems, designed to establish a land-based air defense layer for Swedish Army brigades.

- August 2025: The UK MoD announced the purchase of six new surface-to-air Land Ceptor missile systems to strengthen Britain’s air defences. The Land Ceptor systems will be integrated into Sky Sabre, a sophisticated defense system designed to intercept cruise missiles, aircraft, and drones. This three-year contract will deliver six new MRAD Land Ceptor missile launching systems for the British Army.

- June 2025: At the Paris Air Show, MBDA announced a contract to develop a VSHORAD system for the Italian Army. The missile, named 'FULGUR', addresses a specific operational requirement identified by the Italian Army.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the air defense systems market as all new-build, integrated offensive-intercept solutions, missiles, guns or directed-energy effectors, sold together with the supporting radars, launchers, fire-control and command-and-control nodes that detect, track and neutralize hostile aircraft, missiles, rockets, artillery and unmanned systems. The baseline follows program delivery value rather than multi-year appropriation totals.

Scope exclusion: Upgrades to legacy sensors and stand-alone early-warning radars that are not paired with an effector layer are kept outside the model.

Segmentation Overview

- By System

- Missile Defense Systems

- Anti-Aircraft Gun and SAM Systems

- Counter-Unmanned Aerial Systems (C-UAS)

- Counter-Rocket, Artillery and Mortar (C-RAM)

- Directed Energy Weapons (DEWs)

- By Platform

- Land-Based

- Sea-Based

- Air-Based

- Space-Based Early-Warning Assets

- By Range

- Short Range

- Medium Range

- Long Range

- By Sub-system

- Weapon System

- Fire Control System

- Command and Control (C2) System

- Others

- By Technology

- Kinetic-Kill Effectors

- High-Energy Laser Systems

- High-Power Microwave Systems

- Electronic Warfare (EW) Soft-Kill Solutions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we interview program managers in procurement agencies, retired air-defense officers across North America, Europe, the Middle East and Asia-Pacific, and senior engineers at Tier-1 subsystem suppliers. Their insights refine subsystem cost shares, lead times and adoption of emerging counter-UAS layers, tightening our assumptions before the model is locked.

Desk Research

Mordor analysts first map the global procurement landscape using open-access defense budget papers, Stockholm International Peace Research Institute yearbooks, US DSCA Foreign Military Sales notices, NATO and European Defence Agency expenditure tables, and parliamentary audit reports from major spender nations. Company filings, investor decks and reputable press releases then help link unit orders to contract values. Paid platforms such as D&B Hoovers for prime-contractor financials and Aviation Week for program timelines give additional context on backlog conversion. This list illustrates the primary evidence base; many other credible public and subscription sources were reviewed for clarification and cross-checks.

Market-Sizing & Forecasting

A top-down build begins with annual production plus trade values reconstructed from defense budgets and published contract awards, which are then benchmarked against bottom-up snapshots drawn from sampled supplier roll-ups and channel checks. Key inputs include average battery acquisition cost, interceptor rounds per battery, defense budget growth, regional threat indices, and planned force-structure expansions. Gaps, such as undisclosed classified buys, are bridged with analogous contract ratios validated by experts. A multivariate regression, anchored on defense spending elasticity and intercept density targets, projects demand to 2030; scenario analysis adjusts for sharp budget shocks.

Data Validation & Update Cycle

Our outputs undergo variance screening versus independent series like SIPRI military expenditure data and import/export records. Any anomaly triggers a secondary analyst peer review, followed by lead analyst sign-off. Reports are refreshed annually, with interim revisions issued when material program awards or geopolitical escalations arise.

Why Mordor's Air Defense Systems Baseline Commands Reliability

Published figures often diverge because analysts fold in differing subsystems, apply separate booking or delivery bases, and refresh their models at inconsistent cadences.

Key gap drivers include: some publishers combine life-extension sensor upgrades and multi-year sustainment packages; others restrict coverage to land platforms, omitting sea-based interceptors; still others inflate totals by converting budget authorizations straight to procurement value without slippage allowances. Mordor limits scope to new hardware deliveries across all platforms, applies contract-stage weighting, and revisits each variable annually, yielding a balanced, decision-grade baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 50.86 B (2025) | Mordor Intelligence | - |

| USD 87.63 B (2024) | Global Consultancy A | Adds sensor upgrades and long-term support, uses obligation values not deliveries |

| USD 49.58 B (2024) | Industry Journal B | Excludes sea-based interceptors and counter-UAS layers; limited refresh cadence |

In sum, by aligning scope strictly to deliverable systems, triangulating with both contract data and expert insight, and revisiting assumptions yearly, Mordor Intelligence offers a transparent, reproducible market view that buyers can trust for strategic planning.

Key Questions Answered in the Report

How large is the air defense systems market in 2026?

The air defense systems market size stands at USD 17.69 billion in 2026 and is on track to reach USD 25.82 billion by 2031, expanding at a 7.85% CAGR.

Which region is expanding the fastest?

Asia-Pacific records the highest 9.76% CAGR through 2031, propelled by Japanese, South Korean, and Indian procurement.

What system type is growing most rapidly?

Directed-energy weapons (DEWs) exhibit the fastest 11.08% CAGR thanks to sub-dollar cost per engagement and unlimited magazine depth.

Who are the leading companies?

RTX Corporation, Lockheed Martin Corporation, Israel Aerospace Industries Ltd., Thales Group, and Northrop Grumman Corporation together command more than half of North American orders, while Israel Aerospace Industries and Hanwha Systems are growing in Europe and the Middle East.

What are the main bottlenecks slowing deliveries?

Limited GaN wafer capacity, ITAR/MTCR export controls, and technical hurdles intercepting hypersonic glide vehicles delay some systems until 2028 or later.

How are militaries dealing with drone swarms?

Forces are combining AI-enabled sensors, directed-energy lasers, high-power microwaves, and low-cost interceptors such as the Coyote to create layered counter-UAS defenses.

Page last updated on: