Military Aircraft Avionics Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 24.06 Billion |

| Market Size (2031) | USD 30.38 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Aircraft Avionics Market Analysis by Mordor Intelligence

The military aircraft avionics market size is estimated at USD 24.06 billion in 2026 and is projected to reach USD 30.38 billion by 2031, growing at a 4.78% CAGR. The growing demand for AI-enabled sensor fusion that processes data at the edge, the mandatory adoption of open-systems architecture, and the rapid fielding of power-efficient avionics for unmanned platforms are shaping procurement priorities in every major air arm. Suppliers are racing to embed zero-trust cyber controls that satisfy DO-326A and EUROCAE ED-202A while still meeting weight and power budgets. At the same time, on-shoring of RF and microelectronics capacity is redrawing supply chains and moderating the impact of semiconductor disruptions. These intersecting forces reinforce a momentum that offsets the long certification cycles typical of the military aircraft avionics market.

Key Report Takeaways

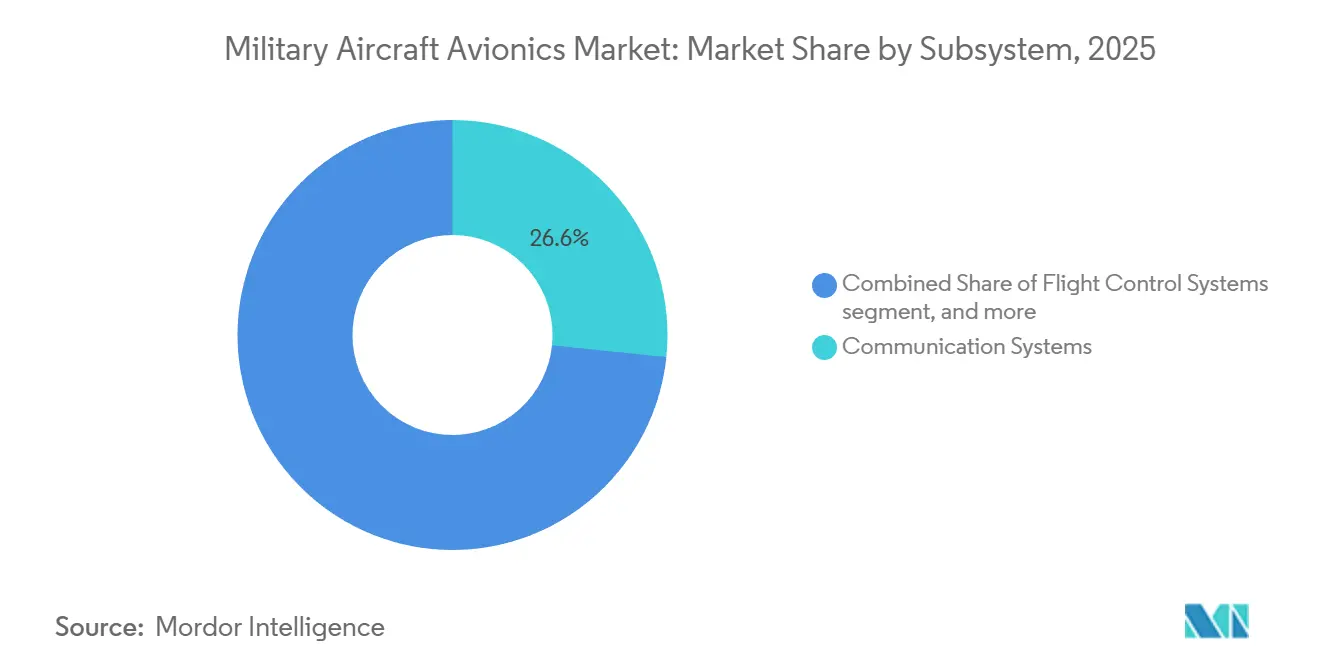

- By subsystem, communication systems led the military aircraft avionics market with a 26.64% market share in 2025 and are forecasted to expand at a 6.03% CAGR through 2031.

- By aircraft type, fixed-wing combat aircraft accounted for 41.21% of the military aircraft avionics market size in 2025, whereas unmanned aerial vehicles (UAVs) are projected to advance at a 9.81% CAGR through 2031.

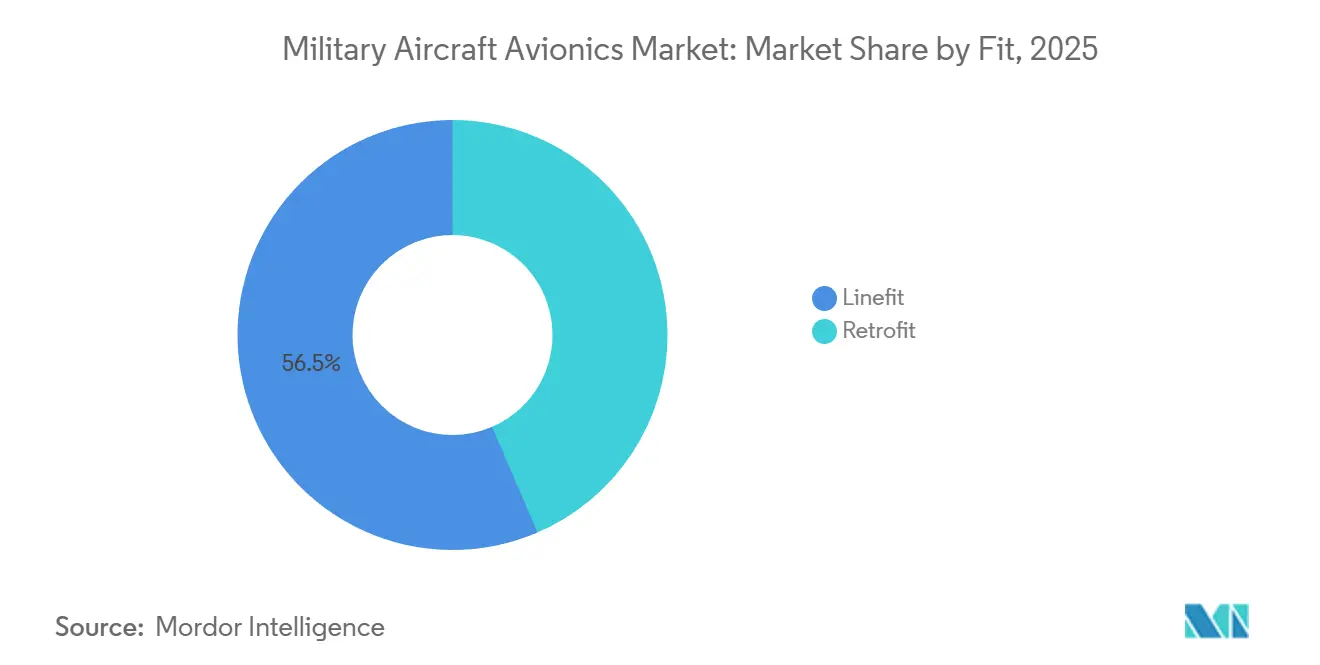

- By fit, linefit installations captured 56.47% of the military aircraft avionics market in 2025; however, retrofit applications are growing at the fastest rate, with a 6.67% CAGR.

- By geography, North America held 30.47% of the military aircraft avionics market in 2025, while Asia-Pacific is registering the highest regional CAGR at 5.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Aircraft Avionics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global defense spending and modernization of military aircraft fleets | +1.20% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Accelerated integration of AI-enabled sensor fusion and edge analytics | +0.90% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Proliferation of UAV platforms driving demand for lightweight avionics | +1.10% | Middle East, Asia-Pacific | Short term (≤ 2 years) |

| Mandates for open-systems architecture by DoD and NATO | +0.70% | North America, Europe, allied APAC | Long term (≥ 4 years) |

| Strategic on-shoring and localization of RF and microelectronics | +0.50% | North America, Europe, India, Japan | Long term (≥ 4 years) |

| Emergence of zero-trust cybersecurity standards for avionics certification | +0.40% | Global, early adoption in North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Defense Spending and Modernization of Military Aircraft Fleets

Military expenditure reached USD 2.44 trillion in 2024 and continued to rise in 2025 as 41 nations spent more than 2% of GDP on defense, extending fleet life cycles and expanding the upgrade pipeline.[1]Stockholm International Peace Research Institute, “Military Expenditure Database 2024,” sipri.org The US Department of Defense (DoD) earmarked USD 33.1 billion for aircraft procurement in fiscal year 2026, prioritizing F-35 Block 4 and Next Generation Air Dominance capability increments. Germany allocated EUR 8 billion (USD 9.37 billion) for Eurofighter Typhoon enhancements, which include new mission computers, AESA radar, and electronic-warfare suites. India, Japan, and South Korea are channeling resources into indigenous fighters that must incorporate domestic avionics to circumvent export controls, reinforcing a long-term demand stream. These budgets lengthen platform service lives to 40 years and create an 8-to-10-year retrofit cadence that underpins the 6.67% retrofit CAGR in the military aircraft avionics market.

Accelerated Integration of AI-Enabled Sensor Fusion and Edge Analytics

DARPA flight trials in 2024 showed autonomous dogfighting algorithms fusing radar, electro-optical, and electronic-support data in under 20 milliseconds, proving real-time edge processing viability.[2]DARPA, “Air Combat Evolution Program Results,” darpa.mil RTX Corporation fielded an AI-accelerated mission computer on the F/A-18E/F that runs convolutional neural networks while drawing less than 60 watts, a power envelope compatible with legacy wiring. Shifting from centralized to distributed architectures has cut avionics bus bandwidth by up to 70% and improved survivability in jammed environments. Lockheed Martin’s Sikorsky unit embedded predictive maintenance analytics in the CH-53K, resulting in a 35% increase in mission-capable rates. Suppliers therefore co-design hardware and software on integrated modular avionics cards, accelerating technology refresh cycles inside the military aircraft avionics market.

Proliferation of UAV Platforms Driving Demand for Lightweight Avionics

US procurement of 1,200 Group 3 and Group 4 UAVs in 2025 pushed annual unmanned shipments 42% higher than 2024 levels.[3]U.S. Department of Defense, “Fiscal Year 2026 Budget Request,” defense.gov Northrop Grumman’s MQ-4C Triton uses a 180-kilogram modular avionics suite that is 40% lighter than comparable crewed-aircraft systems, showing the benefits of carbon-fiber enclosures and gallium-nitride (GaN) power amplifiers. Turkey’s Bayraktar TB3 consolidates cockpit, autopilot, and payload control into a 12-kilogram stack, freeing payload for sensors or weapons. Middle East deployments of attritable drones priced under USD 2 million are expanding the demand for small, rugged mission computers that can survive 9-G loads. Lightweight designs, therefore, broaden the addressable market for military aircraft avionics beyond crewed platforms.

Mandates for Open-Systems Architecture by DoD and NATO

A 2024 DoD memorandum requires new aircraft programs to comply with the Modular Open Systems Approach, utilizing published interfaces and government-owned data to reduce lifecycle costs by 30%. NATO adopted the Future Airborne Capability Environment standard in 2025, enabling software portability across disparate platforms. Lockheed Martin reduced the unit upgrade cost of the F-35 Technology Refresh 3 from USD 18 million to USD 11 million by replacing proprietary processors with commercial GPUs that are compliant with the Sensor Open Systems Architecture. BAE Systems released interface-control documents for the multinational Tempest fighter, reducing technology insertion cycles from 10 years to 3 years. These mandates open the military aircraft avionics market to new entrants that supply modular subsystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising R&D and integration costs associated with advanced avionics systems | -0.80% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Persistent supply chain disruptions in semiconductors and specialized chips | -0.60% | North America, Europe | Medium term (2-4 years) |

| Power limitations in legacy wiring harnesses hindering avionics retrofits | -0.30% | North America, Europe | Long term (≥ 4 years) |

| Export control barriers affecting encryption and EW technologies | -0.40% | Global, impacts non-allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising R&D and Integration Costs Associated with Advanced Avionics Systems

Non-recurring engineering charges for next-generation flight-control suites now exceed USD 50 million per platform, 35% higher than the 2020 levels, reflecting the adoption of AI processors, GaN RF front ends, and DO-178C Level A validation.[4]Honeywell International, “2025 Annual Report,” honeywell.com Exhaustive DO-178C and DO-254 testing consumes up to half of total budgets and pushes complex projects to five-year development cycles. Smaller OEMs are exiting or consolidating, as shown by TransDigm’s 2024 purchase of Cobham’s avionics arm for USD 9.5 billion. Cross-functional expertise in real-time operating systems and partitioning kernels commands salary premiums of 25% and is tightening talent supply outside North America and Western Europe. High costs encourage incremental upgrades over clean-sheet avionics, tempering near-term growth in the military aircraft avionics market.

Persistent Supply Chain Disruptions in Semiconductors and Specialized Chips

Lead times for radiation-hardened FPGAs doubled to 52 weeks in 2025, forcing primes to carry 18 months of inventory that ties up working capital and erodes margins. Taiwan Semiconductor Manufacturing Company dedicates less than 5% of advanced nodes to defense-grade runs, creating allocation risk as commercial buyers outbid military volumes. In 2024, US export rules added 140 Chinese firms to the Entity List, blocking high-performance AI silicon shipments exceeding 600 TOPS and fragmenting global supply chains. Mercury Systems recorded USD 120 million in deferred revenue due to shortages that delayed F-35 and F/A-18 mission-computer deliveries by six months. Dual sourcing and board redesigns mitigate risk but add up to 15% to material costs and extend qualification by a year, restraining expansion of the military aircraft avionics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Subsystem: Communication Systems Anchor the Network-Centric Pivot

The communication systems segment accounted for 26.64% of the military aircraft avionics market share in 2025 and is forecasted to grow at a 6.03% CAGR through 2031. L3Harris won a USD 1.2 billion contract in 2025 to supply AN/ARC-210 software-defined radios (SDRs) across multiple US fighter fleets, reflecting demand for simultaneous voice, data, and video links. Navigation systems are integrating jam-resistant M-Code GPS as the US Space Force declared initial operational capability in 2024. Flight-control subsystems are increasingly relying on model-based tools that reduce software defects by 40%, thereby speeding up DO-178C certification. Health-management platforms highlight maintenance savings, with Honeywell analytics predicting failures 150 flight hours in advance.

Line-replaceable units (LRUs) are consolidating into large-format touchscreens that reduce cockpit-panel weight by 30%, as seen in Elbit Systems’ CockpitNG for India’s Tejas Mk2. These shifts sustain premium pricing while lowering lifecycle costs, ensuring that communication-heavy architectures dominate the military aircraft avionics market. Continued upgrades to Link 16, SATCOM, and SDRs ensure long-term visibility for vendors that control waveform libraries and cryptographic keys, providing a competitive edge.

By Aircraft Type: UAVs Set the Growth Pace

Fixed-wing combat airframes accounted for 41.21% of the military aircraft avionics market size in 2025, driven by 156 F-35 deliveries.[5]Lockheed Martin, “F-35 Production Statistics 2025,” lockheedmartin.com Despite this mass, UAVs are expanding at a 9.81% CAGR through 2031, driven by ISR and counter-drone missions that can tolerate higher attrition rates. Northrop Grumman’s MQ-4C Triton and General Atomics’ MQ-9B together generated 22% of UAV avionics revenue in 2025, each employing open-architecture mission computers that simplify sensor swaps. Non-combat fixed-wing aircraft such as transports and tankers are adopting civil-derivative flight decks, leveraging commercial economies of scale.

Helicopter programs, including Poland’s AW149, add synthetic vision and helmet displays that improve low-visibility operations. Attritable UAVs priced below USD 2 million demand ruggedized yet low-cost avionics, prompting suppliers to modularize designs for platforms ranging from 25 kilograms to 15 tons. The breadth of this unmanned demand will keep UAVs at the forefront of the military aircraft avionics market through the forecast period.

By Fit: Retrofit Accelerates as Airframes Age

Linefit installations captured 56.47% of the military aircraft avionics market in 2025, driven by ongoing production of the F-35, F-15EX, and Rafale. Retrofit demand, however, is climbing at a 6.67% CAGR as operators stretch service lives to 40 years and refresh mission systems every decade. The USD 4.2 billion F-16 Viper program will retrofit 608 jets with AESA radar, modern computers, and Link 16, underscoring the scale of the retrofit. Europe is following a similar path through the Eurofighter Phase 4 Enhancement, which spans 500 aircraft and adds the Common Radar System Mark 2.

Power limits in legacy wiring harnesses create trade-offs that slow adoption of full-suite upgrades, yet the imperative to keep fleets interoperable sustains retrofit volume. Because obsolescence cycles for commercial processors now run four to five years, retrofit will remain the faster-growing slice of the military aircraft avionics market.

Geography Analysis

North America accounted for 30.47% of revenue in 2025, primarily due to the US procurement budget and the F-35 ramp, with avionics content exceeding USD 12 million per jet. The Asia-Pacific region is the fastest-growing, with a 5.65% CAGR, driven by programs such as India’s Light Combat Aircraft (LCA) Mk2, Japan’s F-X, and South Korea’s KF-21, which target 60% local avionics content. Europe captured 24% of the revenue in 2025, sustained by the Future Combat Air System (FCAS) and Tempest initiatives, which will embed open architectures from inception.

Middle East buyers accelerate UAV acquisitions, exemplified by Saudi Arabia’s 300 Wing Loong II order, while Australia continues F-35A procurement and Wedgetail upgrades, anchoring demand in Oceania. China’s domestic programs, notably the J-20 and Y-20, are estimated to represent 12% of global demand but remain insulated behind export controls. Fragmented supply chains and industrial-sovereignty policies will keep Asia-Pacific at the center of incremental capacity expansion in the military aircraft avionics market.

Competitive Landscape

The top five suppliers, RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, L3Harris Technologies Inc., and Thales Group, control roughly 62% of the military aircraft avionics market through vertical integration of sensors, processors, and software. Open-systems mandates are lowering entry barriers, enabling Mercury Systems, Elbit Systems, and Leonardo to win subsystem awards with MOSA-compliant hardware that slots into prime architectures without proprietary interfaces. Strategic moves focus on AI and software, such as RTX Corporation’s 2024 purchase of a machine-learning firm to accelerate sensor-fusion algorithms and BAE Systems’ alliance with Palantir to embed data analytics in mission planners.

White-space opportunities are emerging in attritable UAV avionics, where subsystems must balance 9-G survivability with price points fit for expendable platforms. Technology remains the decisive lever: suppliers invest in GaN RF, neuromorphic processors, and quantum-secure encryption, which future-proofs designs against evolving threats. Patent activity underscores this shift; L3Harris filed 142 avionics-related patents in 2024, with a focus on adaptive waveform generation and cognitive electronic warfare. As open standards proliferate, differentiation moves from hardware enclosures to the software stack, reshaping competitive dynamics across the military aircraft avionics market.

Military Aircraft Avionics Industry Leaders

Lockheed Martin Corporation

Northrop Grumman Corporation

RTX Corporation

Thales Group

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Collins Aerospace, a part of RTX Corporation, has signed a multi-decade agreement with the Royal Netherlands Air and Space Force to establish a Netherlands-based avionics service center that will support the European F-35 and CH-47F fleets.

- September 2025: Mercury Systems has been awarded a USD 12.3 million development contract to provide a Communication Management Unit avionics subsystem for a new US military aircraft, aimed at streamlining cockpit communications for an upcoming fleet.

- April 2025: The US Air Force awarded Indra Air Traffic Inc. a contract worth up to USD 198.36 million to design, deploy, and sustain man-portable Tactical Air Navigation (TACAN) systems through 2032.

Global Military Aircraft Avionics Market Report Scope

The military aircraft avionics market encompasses electronic systems, software, and embedded processing units integrated into military aircraft to facilitate flight control, navigation, communication, mission management, surveillance, and health monitoring. The report focuses on key avionics subsystems, including flight control, communication, navigation, monitoring, and health management, as well as other mission-critical electronics. It examines global demand influenced by defense modernization initiatives, the increasing use of UAVs, mandates for open-systems architecture, and cybersecurity considerations. Additionally, the report assesses the competitive dynamics, regulatory frameworks, and technological advancements that shape the development of military avionics systems.

The military aircraft avionics market is segmented by subsystem, aircraft type, fit, and geography. By subsystem, the market is segmented into flight control systems, communication systems, navigation systems, monitoring and health-management systems, and other subsystems. By aircraft type, the market is segmented into fixed-wing combat aircraft, fixed-wing non-combat aircraft, helicopters, and unmanned aerial vehicles (UAVs). By fit, the market is segmented into fit and retrofit. The report also covers the market sizes and forecasts for the military aircraft avionics market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Flight Control Systems |

| Communication Systems |

| Navigation Systems |

| Monitoring and Health-Management Systems |

| Other Subsystems |

| Fixed-wing Combat Aircraft |

| Fixed-Wing Non-Combat Aircraft |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Subsystem | Flight Control Systems | ||

| Communication Systems | |||

| Navigation Systems | |||

| Monitoring and Health-Management Systems | |||

| Other Subsystems | |||

| By Aircraft Type | Fixed-wing Combat Aircraft | ||

| Fixed-Wing Non-Combat Aircraft | |||

| Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the military aircraft avionics market?

The military aircraft avionics market size is USD 24.06 billion in 2026 and is projected to reach USD 30.38 billion by 2031.

Which subsystem segment is growing fastest?

Communication systems are expanding at a 6.03% CAGR due to widespread installation of wideband SATCOM, Link 16, and software-defined radios (SDRs).

Why are unmanned aerial vehicles (UAVs) important for avionics suppliers?

UAVs require lightweight, power-efficient avionics and are posting a 9.81% CAGR, making them the most dynamic aircraft-type opportunity.

How significant is retrofitting compared with new-build installations?

Retrofit demand is rising at 6.67% annually as air forces extend aircraft service lives and refresh mission systems every decade.

Which region shows the highest growth through 2031?

Asia-Pacific leads regional growth with a 5.65% CAGR, underscored by large indigenous fighter programs in India, Japan, and South Korea.

What impact do zero-trust cybersecurity standards have on avionics development timelines?

Adoption of DO-326A and EUROCAE ED-202A adds 12–18 months to certification because suppliers must implement continuous authentication, network micro-segmentation, and hardware roots of trust, yet the extra effort sharply reduces cyber-attack surface and is becoming mandatory on new programs.

Page last updated on: