Middle East And Africa Fighter Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 5.28 Billion |

| Market Size (2030) | USD 6.71 Billion |

| Growth Rate (2025 - 2030) | 4.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Fighter Aircraft Market Analysis by Mordor Intelligence

The Middle East and Africa fighter aircraft market size stood at USD 5.28 billion in 2025 and is forecasted to reach USD 6.71 billion by 2030, advancing at a 4.91% CAGR. Robust investment in next-generation platforms, greater emphasis on counter-UAS capabilities, and stringent offset rules that embed local industry are steering the region toward sustained fleet modernization. Regional defense outlays rose 21.8% between 2021 and 2024, while Saudi Arabia directed USD 78 billion—21% of its 2025 budget—toward defense, underscoring how secure oil revenues and heightened geopolitical risks keep procurement momentum strong. Air forces now weigh the trade-offs between proven 4th-generation airframes and stealth-enabled 5th-generation jets, with sensor fusion, data-link integration, and electronic warfare (EW) suites increasingly viewed as minimum performance baselines. Meanwhile, cost-efficient single-engine designs are improving mission-ready rates, and vertical-take-off models are expanding naval reach as Gulf states reinforce maritime choke points. Competitive dynamics are shifting as Turkey and South Korea introduce indigenous designs with compelling price-to-performance ratios, challenging incumbent Western suppliers.

Key Report Takeaways

- By aircraft generation, 4th-generation fighters led with 51.23% of the Middle East and Africa fighter aircraft market share in 2024. In contrast, 5th-generation platforms are projected to post the fastest 7.89% CAGR through 2030.

- By take-off and landing mode, CTOL aircraft accounted for 84.56% revenue share in 2024; VTOL platforms are set to expand at a 6.66% CAGR to 2030.

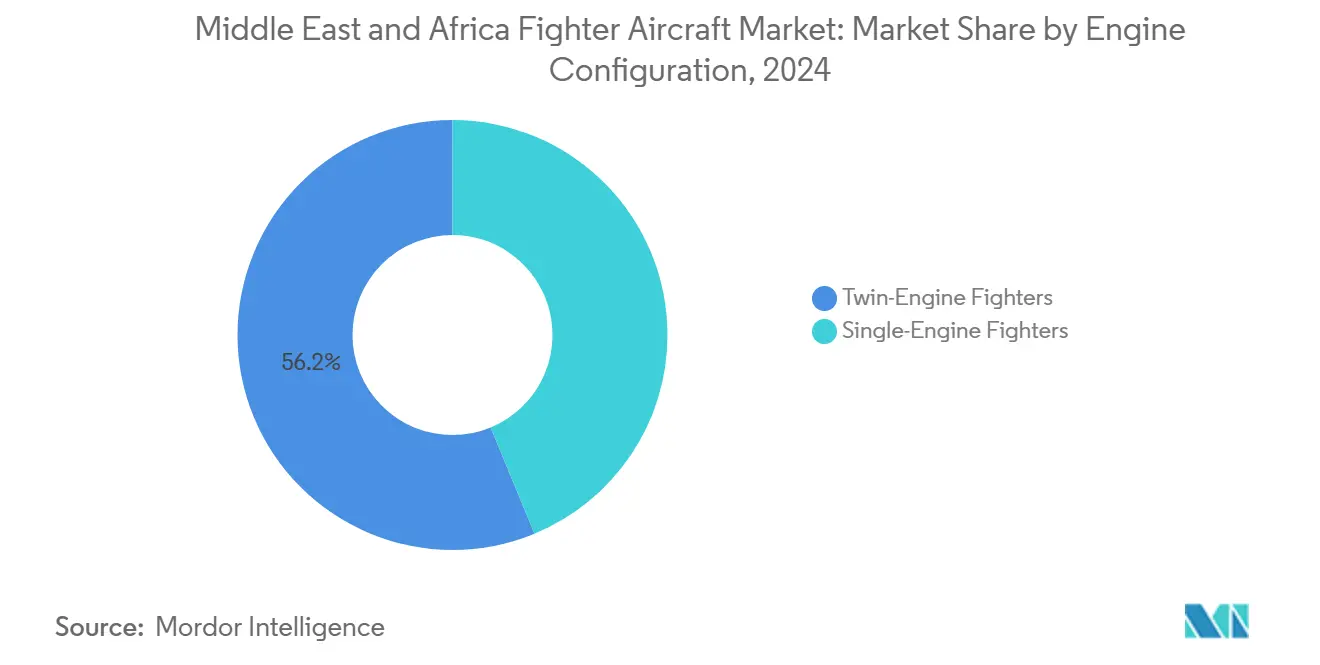

- By engine configuration, twin-engine fighters captured 56.23% of 2024 sales, while single-engine models are forecasted to grow at a 6.45% CAGR between 2025 and 2030.

- By mission role, multirole aircraft held 52.87% share of the Middle East and Africa fighter aircraft market size in 2024; close-air-support and strike variants are advancing at a 5.24% CAGR during the same horizon.

- By end user, air forces represented 78.61% of spending in 2024, but naval aviation shows the highest projected CAGR at 5.87% through 2030.

- By geography, the Middle East represented 72.45% of spending in 2024 and shows the highest projected CAGR at 5.62% through 2030.

Middle East And Africa Fighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in regional defense spending across key Gulf and African states | +1.2% | GCC states, Egypt, South Africa | Medium term (2-4 years) |

| Competitive push for 5th-generation fighter fleet modernization | +0.8% | Saudi Arabia, UAE, Israel, Qatar | Long term (≥ 4 years) |

| Offset and industrial participation requirements driving procurement commitments | +0.6% | Saudi Arabia, UAE, Egypt, Morocco | Medium term (2-4 years) |

| Expanding demand for multirole fighter integration with counter-UAS capabilities | +0.4% | Gulf states, Israel | Short term (≤ 2 years) |

| Emergence of regional flight-training hubs serving allied and partner nations | +0.3% | UAE, Jordan, Egypt, Morocco | Long term (≥ 4 years) |

| Indigenous stealth fighter programs attracting export interest and political support | +0.2% | Turkey, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Regional Defense Spending Across Key Gulf and African States

Sustained revenue from hydrocarbons allows Gulf governments to finance new squadrons while underwriting maintenance, training, and mission-system upgrades. Saudi Arabia boosted 2025 defense allocations by 15% to USD 73 billion, channeling funds into F-15SA avionics refreshes and guided-munitions stockpiles. The UAE committed USD 19.8 billion to procure Rafale jets and to bankroll stealth-fleet negotiations, reinforcing its status as an early adopter of advanced combat airframes. Egypt’s dollar-denominated procurements benefit from favorable export-credit terms, widening the customer base for 5th-generation solutions. Despite cyclical oil-price swings, such spending ensures predictable demand for airframe OEMs and electronic-warfare suppliers. Defense ministries now view technology transfer and sovereign MRO capacity as intrinsic to budget approvals.

Competitive Push for 5th-Generation Fighter Fleet Modernization

Operational lessons from Israel’s F-35I Adir sorties in contested zones highlight how low-observable airframes exploit sensor fusion to suppress integrated air defenses.[1]First-name Last-name, “F-35I Adir Operations,” Israel Defense Forces, idf.il The UAE’s parallel F-35 request signals a consensus that regional deterrence increasingly hinges on stealth, seamless data-linking, and shared battlespace awareness. Turkey’s KAAN prototype achieved first flight in 2025, offering a domestic 5th-generation option that sidesteps foreign export controls while courting Egypt as a partner customer.[2]First-name Last-name, “KAAN Fighter Aircraft Program,” Turkish Aerospace Industries, tusas.com Fast-rising pilot interest in helmet-mounted cueing, internally carried standoff weapons, and agile software upgrades will likely accelerate platform obsolescence cycles, nudging air forces to retire fourth-generation fleets sooner than initially planned.

Offset and Industrial Participation Requirements Driving Procurement Commitments

Defense ministries exploit aircraft buys to seed aerospace ecosystems, shifting offsets from basic assembly into advanced subsystem fabrication. Saudi Arabia’s THAAD localization relocated missile-pallet production to Riyadh, anchoring a long-term missile-sustainment hub. Morocco’s Maintenance Aero Maroc venture now services F-16 and C-130 fleets from multiple North African operators, reducing turnaround times and building avionics diagnostics expertise region-wide. Bidders unable to demonstrate credible job creation or intellectual-property hand-offs lose strategic tenders even when cost or performance metrics favor their platforms. These requirements favor countries willing to co-develop and coproduce rather than merely export.

Expanding Demand for Multirole Fighter Integration with Counter-UAS Capabilities

Drone incursions over energy infrastructure, ports, and troop concentrations prompted air forces to integrate low-cost interception packages into existing fighters. The Advanced Precision Kill Weapon System allows F-15E crews to engage class II drones at a fraction of the cost of radar-guided missiles, preserving high-value munitions for manned threats. Software-defined radios now fuse UAS telemetry with airborne early-warning tracks, enabling real-time handoff between ground-based lasers and fighter escort. Procurement specifications increasingly insist on native counter-UAS modes, elevating multirole platforms that can pivot between air-superiority and base defense within a single sortie. Such flexibility compresses the need for dedicated interceptor squadrons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints linked to fluctuations in hydrocarbon revenue streams | –0.7% | Gulf states, Algeria, Angola, Nigeria | Short term (≤ 2 years) |

| Lengthy compliance timelines tied to US and EU export-control regulations | –0.5% | US and European platform buyers | Medium term (2-4 years) |

| Infrastructure limitations, including runway capacity and hardened airbase availability | –0.4% | Sub-Saharan Africa, secondary Gulf sites | Long term (≥ 4 years) |

| Shortages of skilled maintenance personnel to support advanced fighter platforms | –0.3% | Africa-wide, select Gulf states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Linked to Fluctuations in Hydrocarbon Revenue Streams

When crude prices dip below the USD 70–80 per-barrel fiscal break-even, defense ministries defer tranche payments and stretch fleet upgrades. Algeria postponed Su-30MK upgrades during 2024’s price dip, compelling aircrews to log fewer annual hours. Nigeria faced competing social-infrastructure bills that crowded out its multirole-fighter line item. Such price-linked austerity unavoidably blunts procurement momentum and may intensify capability gaps precisely when regional tensions peak. OEMs respond with bridge financing, yet higher interest costs ultimately shrink purchase quantities.

Lengthy Compliance Timelines Tied to US and EU Export-Control Regulations

Complex fighter transfers must pass US ITAR and third-party‐technology release gauntlets that typically add 12 to 18 months to delivery schedules. European equivalents covering AESA radars and EW suites impose parallel reviews. Protracted approvals trigger cost escalations, strain inventory planning, and prompt some buyers to consider alternative suppliers with less restrictive regimes. Egypt’s FA-50 deal avoided lengthy US export-clearance hurdles, illustrating how compliance risk alters sourcing decisions. While safeguards protect sensitive technologies, slow approvals reduce strategic flexibility for importers facing emergent threats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Generation: 5th-Generation Momentum Challenges Fourth-Generation Dominance

4th-generation fighters dominated 51.23% of 2024 deliveries, making them the biggest revenue pool within the Middle East and Africa fighter aircraft market. Operators appreciate the lower acquisition cost and extensive in-theater sustainment footprint that legacy F-16 and Typhoon fleets enjoy. However, from 2025 to 2030, the 5th-generation cohort is tracking a 7.89% CAGR, illustrating how stealth and sensor fusion now outweigh pure kinetic performance in procurement calculus.

As network-centric doctrines mature, fourth-generation jets risk relegation to permissive-airspace tasks such as close air support or homeland defense. Turkey’s KAAN program anchors an indigenous supply chain that may narrow 5th-generation cost premiums, accelerating adoption in cash-constrained North African markets. Meanwhile, avionics retrofit kits keep 4th-generation units relevant, extending service life until fifth-generation inventory reaches sustainment economies of scale across the Middle East and Africa fighter aircraft industry.

By Take-off and Landing: Conventional Platforms Dominate While VTOL Gains Naval Traction

CTOL aircraft generated 84.56% of the 2024 Middle East and Africa fighter aircraft market size, aided by the region’s ample runway networks across GCC air bases. Yet VTOL and STOVL types are charting a 6.66% CAGR, a pace that underscores how Gulf navies intend to project air power from amphibious assault ships and forward logistics hubs.

USS Abraham Lincoln’s 2024 deployment proved that F-35B dets can sortie against land targets from the Red Sea without carrier support, a template the Gulf states aim to emulate. Still, VTOL proliferation will hinge on specialized pilot training and International Civil Aviation Organization (ICAO) compliance standards that many regional regulators are only now drafting for fighter operations.

By Engine Configuration: Twin-Engine Reliability Preferred Despite Single-Engine Efficiency Gains

Twin-engine fleets held 56.23% of 2024 shipments, retaining market leadership thanks to perceived survivability over open water and hot-and-high terrain. Ongoing reliance on two-engine redundancy sustains elevated maintenance budgets but reassures commanders tasked with extended maritime patrols.

Single-engine designs nonetheless record a 6.45% CAGR, buoyed by the F-35A’s combat credibility and power-plant mean-time-between-failures exceeding 6,000 hours. Lower fuel burn and logistics simplicity attract defense ministries rebalancing toward cost-per-flight-hour metrics. The pivot is unlikely to erase twin-engine dominance before 2030, but it will impact future basing and MRO investments in the Middle East and Africa fighter aircraft industry.

By Mission Role: Multirole Versatility Drives Market Leadership

Multi-role jets amassed 52.87% of 2024 spending, highlighting how decision-makers prioritize platforms able to switch seamlessly between air superiority, ground attack, and maritime strike tasks without reconfiguration downtime. Flexibility maximizes fleet utility, which is critical for air forces constrained by limited squadron counts.

Close-air-support/strike variants post the highest growth at 5.24% CAGR, reflecting intensifying asymmetric conflicts where precision engagement of dispersed insurgent cells is paramount. Software-reconfigurable cockpits now permit pilots to load counter-UAS overlays mid-mission. This evolution keeps multi-role fighters at the forefront of operational planning within the Middle East and Africa fighter aircraft market.

By End User: Air Force Dominance Faces Naval Aviation Challenge

Air forces consumed 78.61% of 2024 budgets, leveraging entrenched command structures and existing airfield infrastructure to field large inventories quickly. Nevertheless, naval aviation is on a 5.87% CAGR trajectory as Red Sea and Hormuz Strait security imperatives redefine maritime strategy.

Future acquisition rounds already earmark carrier-capable or VTOL fighters to equip Gulf amphibious assault ships, blurring air-land-sea boundaries. As joint commands proliferate, interoperability protocols will place equal emphasis on data-link convergence and deck-handling standards, anchoring naval aviation as a decisive growth node in the Middle East and Africa fighter aircraft market.

Geography Analysis

The Middle East commands the largest share of regional procurement, powered by GCC hydrocarbon wealth and acute threat perceptions. Saudi Arabia invested USD 78 billion in defense during 2025, channeling funds into F-15SA sensor refresh and exploring 5th-generation procurement paths. The UAE complements a standing Rafale fleet with F-35 discussions, demonstrating its intent to keep qualitative superiority irrespective of fleet size. Qatar’s Eurofighter deliveries and Israel’s expanding F-35I squadrons amplify stealth presence, while joint training annexes foster cross-border tactical alignment.

Israel’s operational validation of 5th-generation effectiveness shapes neighborhood buying rationales, accelerating adoption curves among states previously content with 4.5th-generation updates. Turkey’s KAAN prototype injects a non-Western supply option that could circumvent protracted US Foreign Military Sales (FMS) timelines, appealing to countries such as Egypt eager for strategic autonomy. Export-clearance lag nonetheless remains a gating factor, compelling interim life-extension packages for legacy fighters.

Africa presents a mosaic of smaller, budget-sensitive fleets. Egypt broke from traditional suppliers by ordering FA-50 light fighters, citing lower cost-per-flight-hour and fast delivery.[3]First-name Last-name, “FA-50 Golden Eagle Program,” Korea Aerospace Industries, koreaaero.com Nigeria focuses on affordable strike aircraft suited to counter-insurgency, whereas South Africa reviews modernization strategies for its aging Gripen inventory. Morocco, aiming to field North Africa’s first fifth-generation capability, is in exploratory talks for F-35 acquisitions, leveraging its NATO partnership status to secure advanced technology pathways. Infrastructure gaps—from runway length to hardened shelters—continue restraining large-frame fighter deployments across much of Sub-Saharan Africa.

Competitive Landscape

The Middle East and Africa fighter aircraft market is moderately consolidated, with US primes leading installed fleets yet facing fresh challengers. Lockheed Martin Corporation generated USD 808 million in Middle East aeronautics revenue during 2024, sustained by F-16V upgrades and F-35 unit deliveries.[4]First-name Last-name, “Form 10-K for Lockheed Martin Corp,” Lockheed Martin Corporation, lockheedmartin.com The Boeing Company capitalizes on F-15EX enhancements, while Eurofighter consortium members deliver Typhoon capability-sustainment packages.

Emergent competition stems from Korean Aerospace Industries’ FA-50 success in Egypt and Turkish Aerospace Industries’ KAAN program, each pairing attractive price points with robust technology-transfer commitments. Such offerings align with regional offset mandates, tilting tender evaluations beyond performance metrics. MRO remains a white-space revenue pool; Morocco’s Maintenance Aero Maroc hub now draws multi-country contracts, setting a benchmark for localized sustainment models that can reduce downtime and boost fleet availability.

OEMs increasingly bundle advanced munitions, data analytics, and sovereign training packages to cement long-term annuity streams. Artificial intelligence-enabled predictive maintenance and integrated counter-UAS suites are emerging differentiators, while suppliers are slow to localize component manufacture and face procurement headwinds. The competitive tableau is expected to evolve as indigenous programs mature and export customers demand deeper industrial partnerships.

Middle East And Africa Fighter Aircraft Industry Leaders

Lockheed Martin Corporation

United Aircraft Corporation

Turkish Aerospace Industries, Inc.

Dassault Aviation SA

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Turkish Aerospace Industries (TUSAŞ) is expanding flight testing and increasing prototype production of the Kaan aircraft. The company plans to deliver the first aircraft to the Turkish Air Force by the end of 2028.

- June 2024: Israel's Defense Ministry finalized a USD 3 billion agreement with the United States to acquire a third F-35 fighter jet squadron. A delegation signed the letter of agreement for 25 Lockheed Martin-manufactured advanced stealth fighters, with deliveries scheduled from 2028 onwards at three to five units annually.

- November 2024: The Israeli Defence Ministry signed an agreement with The Boeing Company to acquire 25 F-15 fighter jets.

Middle East And Africa Fighter Aircraft Market Report Scope

| 4th Generation |

| 4.5th Generation |

| 5th Generation |

| Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) |

| Vertical Take-off and Landing (VTOL) |

| Single-Engine Fighters |

| Twin-Engine Fighters |

| Air-Superiority |

| Multi-Role |

| Close-Air-Support/Strike |

| Air Force |

| Naval Aviation |

| Marine/Army Aviation |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Aircraft Generation | 4th Generation | |

| 4.5th Generation | ||

| 5th Generation | ||

| By Take-off and Landing | Conventional Take-off and Landing (CTOL) | |

| Short Take-off and Landing (STOL) | ||

| Vertical Take-off and Landing (VTOL) | ||

| By Engine Configuration | Single-Engine Fighters | |

| Twin-Engine Fighters | ||

| By Mission Role | Air-Superiority | |

| Multi-Role | ||

| Close-Air-Support/Strike | ||

| By End User | Air Force | |

| Naval Aviation | ||

| Marine/Army Aviation | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa fighter aircraft market in 2030?

It is projected to reach USD 6.71 billion by 2030, reflecting a 4.91% CAGR over 2025-2030.

Which fighter generation is growing fastest in the region?

5th-generation platforms show the highest momentum, advancing at 7.89% CAGR through 2030 due to stealth and sensor-fusion advantages.

Why are VTOL fighters gaining interest among Gulf states?

Gulf navies seek vertical-take-off jets to operate from amphibious ships and dispersed maritime bases, driving a 6.66% CAGR for VTOL configurations.

How do offset requirements influence aircraft procurement?

Governments now favor bids that include technology transfer and local manufacturing, turning offsets into decisive evaluation criteria.

What challenges slow fighter deliveries to the region?

US and EU export-control reviews can add 12 to 18 months to delivery schedules, raising cost and delaying operational availability.

Page last updated on: