Fifth-party Logistics (5PL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.06 Billion |

| Market Size (2031) | USD 19.61 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

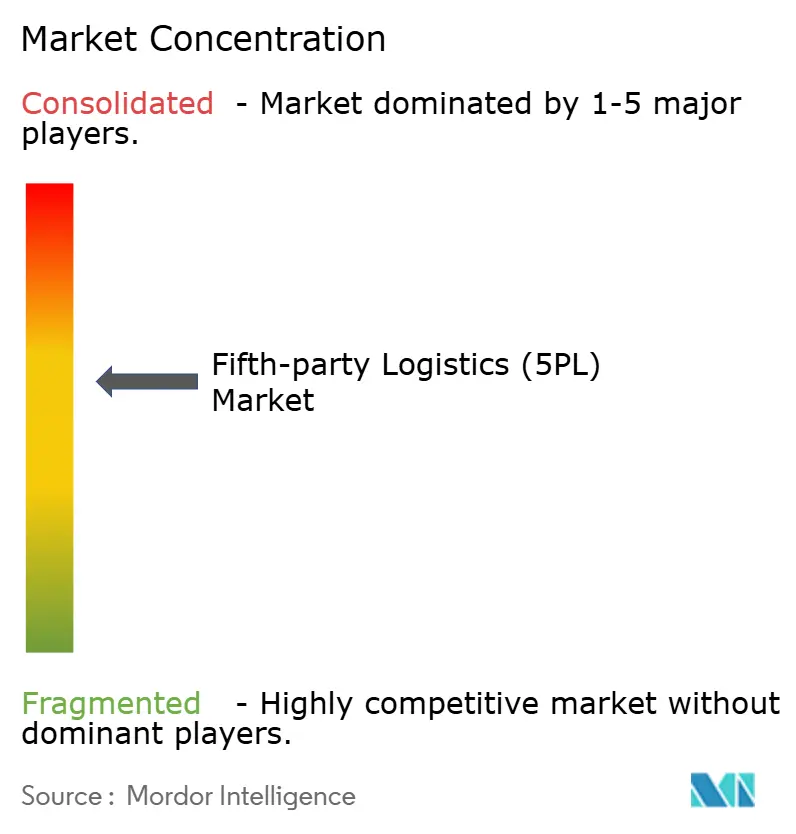

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fifth-party Logistics (5PL) Market Analysis by Mordor Intelligence

The Fifth-Party Logistics market size is expected to increase from USD 10.84 billion in 2025 to USD 12.06 billion in 2026 and reach USD 19.61 billion by 2031, growing at a CAGR of 10.21% over 2026-2031. Direct-to-consumer brands are accelerating outsourcing because they need unified platforms that merge warehousing, transportation, and technology in ways traditional third-party logistics cannot match. Technology-driven orchestration that bundles robotics, blockchain traceability, and embedded finance is creating sticky relationships by lowering customer acquisition costs and improving lifetime value for online brands. Platform providers are also gaining traction with small and medium-sized enterprises that lack the capital and expertise to build proprietary fulfillment networks. At the same time, regulatory mandates such as the European Union Digital Product Passport are pulling blockchain into mainstream logistics workflows, raising the compliance bar for competitors.[1]European Commission, “Digital Product Passport Initiative,” europa.eu

Key Report Takeaways

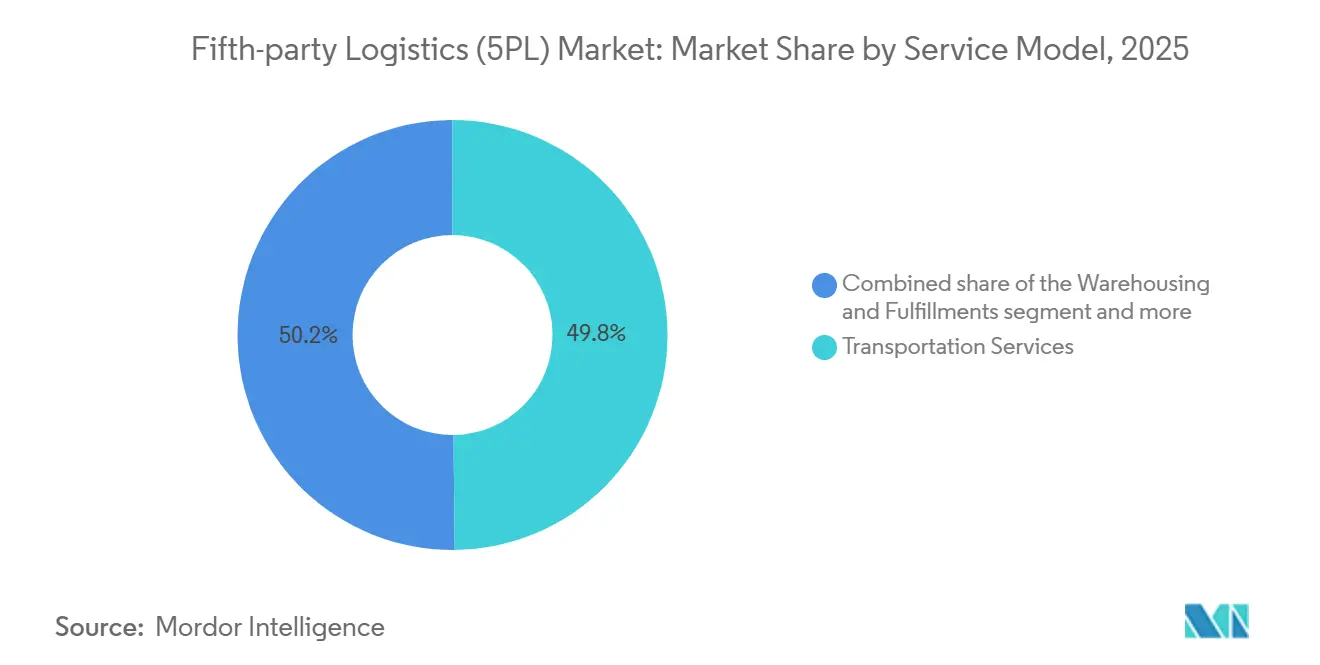

- By service model, Transportation Services held 49.83% of the Fifth-Party Logistics market share in 2025, while Value-Added Services are forecast to expand at a 15.59% CAGR through 2031.

- By end-user industry, E-commerce & Retail led with 37.97% revenue share in 2025; Healthcare & Pharma is projected to grow at a 13.35% CAGR to 2031.

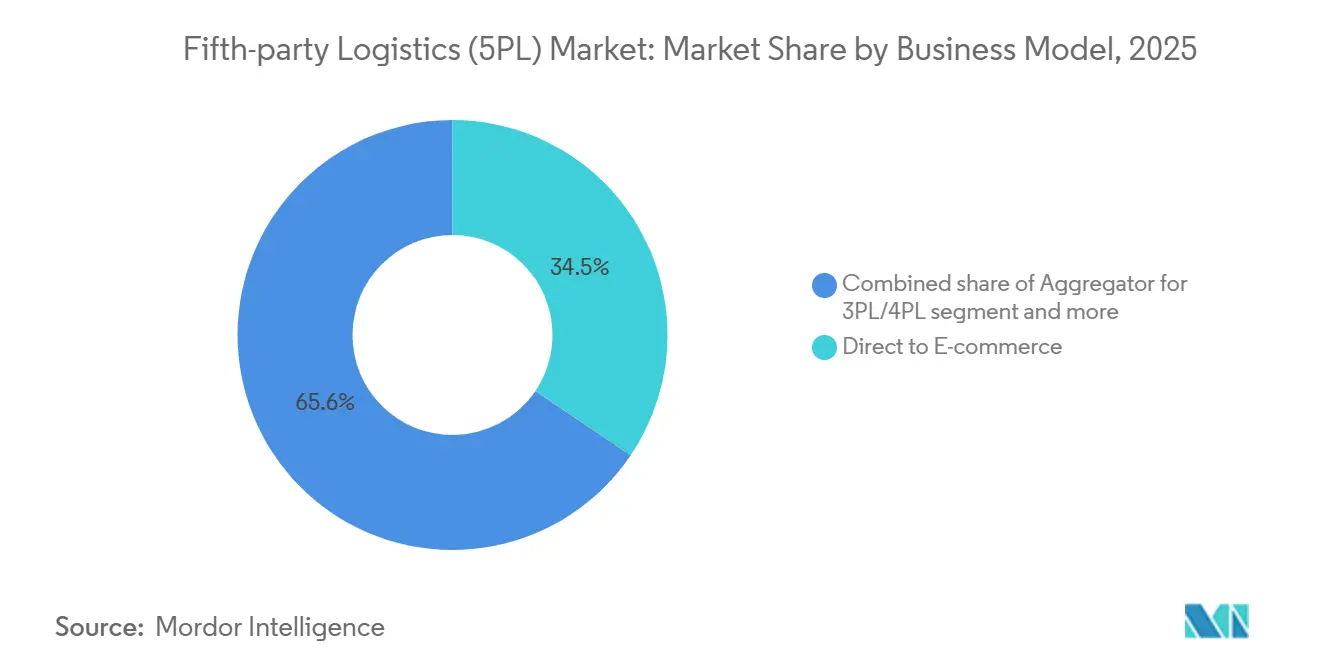

- By business model, the Direct-to-E-commerce approach accounted for 34.45% share of the Fifth-Party Logistics market size in 2025, whereas Platform-based outsourcing is advancing at a 17.08% CAGR during 2026-2031.

- By enterprise size, Large Enterprises captured 63.10% share of the Fifth-Party Logistics market in 2025, but Small and Medium-sized Enterprises are forecast to grow at a 14.03% CAGR through 2031.

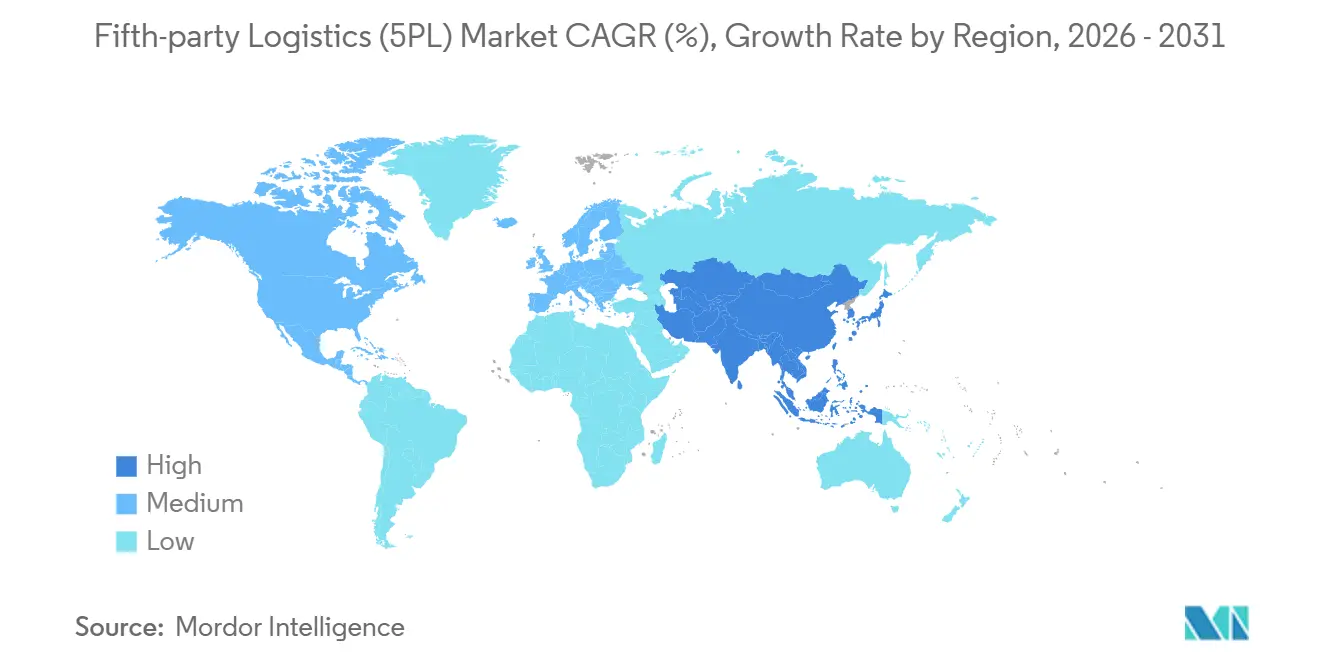

- By Geography, North America commanded 36.72% of market revenue in 2025, while Asia-Pacific is growing fastest at 11.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fifth-party Logistics (5PL) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Direct-to-consumer brand expansion fueling turnkey fulfillment demand | +2.4% | Global with a focus on North America and Europe | Medium term (2-4 years) |

| Heightened omnichannel inventory complexity post-pandemic | +2.0% | North America, Europe, urban Asia Pacific | Short term (≤ 2 years) |

| Supply-chain resilience needs amid geopolitical disruptions | +1.8% | Global | Medium term (2-4 years) |

| Plug-and-play robotics-as-a-service bundled into 5PL contracts | +1.6% | North America and Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Blockchain provenance mandates enhancing outsourcing appeal | +1.5% | Europe and North America, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Embedded finance services within 5PL control-tower platforms | +1.2% | Global, especially emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Direct-to-Consumer Brand Expansion Fueling Turnkey Fulfillment Demand

Digital-first brands are reshaping procurement strategies by insisting on single-source logistics that cover warehousing, shipping, and returns under a single contract. Academic studies show that omnichannel retailers need inventory algorithms that can serve storefronts, online orders, and pickup points simultaneously, a complexity that favors Fifth-Party Logistics market providers. These brands rarely have the scale to build networks on their own, so turnkey 5PL solutions collapse multi-year infrastructure timelines into weeks. Social commerce adoption in the Asia-Pacific further amplifies demand for platforms that blend payments, inventory visibility, and same-day delivery. Superior fulfillment now directly influences customer acquisition costs, making integrated 5PL partnerships a strategic marketing lever.

Heightened Omnichannel Inventory Complexity Post-Pandemic

The pandemic pushed retailers to run physical stores and digital channels in parallel, multiplying the number of stock-placement decisions. Research confirms companies must synchronize many fulfillment nodes to hit service targets without inflating working capital. Off-the-shelf tools are inadequate for balancing seasonality, promotions, and real-time demand sensing. Fifth-Party Logistics market leaders solve this by embedding machine-learning engines inside control towers that continuously reposition goods. Retailers benefit from higher service levels and reduced safety stocks, turning logistics optimization into a margin driver.

Supply-Chain Resilience Needs Amid Geopolitical Disruptions

Trade tensions and natural disasters have exposed risks in single-region sourcing. Thought-leadership from the World Economic Forum shows firms must design networks that can reroute at speed. Fifth-Party Logistics market providers pre-contract capacity in multiple geographies, giving clients fallback options without maintaining redundant headcount. Scenario-planning tools compare costs, lead times, and risks, elevating 5PL partners from tactical vendors to strategic advisers. As nearshoring grows, flexible orchestration is more important than asset ownership.[2]World Economic Forum, “Resilient Supply Chains,” weforum.org

Plug-and-Play Robotics-as-a-Service Bundled into 5PL Contracts

Robotics-as-a-service (RaaS) removes capital hurdles for warehouse automation. Locus Robotics reports 12,000 autonomous units in service and more than 3 billion picks completed, under pay-per-pick agreements that align cost with volume. Fifth-Party Logistics market platforms package these robots inside wider contracts, optimizing fleet utilization across many clients. Integration with warehouse management and labor systems demands technical depth that general robotics vendors cannot supply. Flexible automation is especially valuable during holiday peaks, when labor shortages are acute.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-heavy build-out of global micro-fulfillment networks | −1.2% | Global, especially urban centers | Medium term (2-4 years) |

| Ocean-freight capacity volatility weakening optimization accuracy | −0.9% | Global, trans-Pacific and Europe-Asia routes | Short term (≤ 2 years) |

| Regulatory scrutiny of algorithmic bias in carrier allocation | −0.7% | North America and Europe | Long term (≥ 4 years) |

| Carbon border adjustment compliance burden on 5PL providers | −0.6% | Europe, expanding worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Heavy Build-Out of Global Micro-Fulfillment Networks

Same-day delivery requires micro-warehouses in dense urban areas, but high land prices and the cost of automation equipment push capital requirements beyond the reach of smaller entrants. Break-even analysis shows profitability hinges on high order density, an uncertain variable in many locales. Inventory segregation for multiple clients also drives overhead, eroding utilization rates. These economics encourage consolidation as well-funded providers purchase rivals to secure prime sites. Up-front spending slows expansion pace, trimming overall industry CAGR.

Ocean-Freight Capacity Volatility Weakening Optimization Accuracy

Container schedules remain erratic due to geopolitical reroutes and climate-related canal restrictions, keeping on-time performance below pre-2019 benchmarks. Such swings distort demand-planning algorithms inside the Fifth-Party Logistics market platforms. To maintain service levels, providers carry extra stock or pay for air freight, which raises costs. Real-time re-optimization helps, yet persistent volatility limits the precision that shippers expect from data-driven orchestration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: Value Migration to Technology-Rich Offerings

Transportation Services controlled 49.83% of the Fifth-Party Logistics market share in 2025, yet commoditization pressures are redirecting spending toward Value-Added Services that are accelerating at a 15.59% CAGR through 2031. Clients increasingly view freight movement as a baseline requirement and award contracts based on the provider’s ability to deliver consulting, analytics, and blockchain integration in one bundle. This mix change is expanding the Fifth-Party Logistics market size for advisory functions that once sat outside core logistics budgets. Road transport still dominates last-mile delivery because parcel density supports frequent routes, while multimodal optimization tools shift non-urgent volumes to sea lanes to shrink carbon footprints.

Robotics-as-a-service deployments underscore the pivot. Providers such as DHL integrate fleets of Locus autonomous mobile robots under variable-cost arrangements, improving pick rates for shippers without capital expense. Inventory management modules increasingly embed blockchain to meet Digital Product Passport mandates in Europe. These capabilities boost cross-sell revenue per customer and raise switching costs well above those in traditional rate-based relationships. As advisory and tech income grow faster than trucking revenue, market valuations now hinge on intellectual property and depth of data analytics.

By End-User Industry: Healthcare Complexity Drives Outsourcing Surge

E-commerce & Retail retained 37.97% share of the Fifth-Party Logistics market in 2025 thanks to direct-to-consumer momentum, yet Healthcare & Pharma is projected to climb at a 13.35% CAGR, making it the fastest-growing end-user bloc. Vaccine temperature-control mandates and anti-counterfeit regulations compel full traceability, an area where 5PL platforms that marry blockchain and Internet-of-Things sensors excel. Retailers still dominate by volume, but pharmaceuticals deliver higher revenue per unit because of specialized packaging and compliance tasks. The convergence of social commerce and livestream shopping in the Asia-Pacific increases cross-border parcel counts, reinforcing demand for unified customs documentation and duty-payment automation.

Food & Beverage companies also gravitate to Fifth-Party Logistics market providers for cold-chain orchestration that aligns inventory with fluctuating restaurant and grocery demand. Industrial manufacturers leverage 5PL control towers to coordinate inbound parts with outbound finished goods, reducing dwell times. Across sectors, the thread that unites adopters is rising supply-chain complexity that small internal teams cannot easily master.

By Business Model: Platforms Redefine Competitive Boundaries

The Direct-to-E-commerce model delivered 34.45% of the Fifth-Party Logistics market size in 2025, yet Platform-based, technology-driven outsourcing is racing ahead with a 17.08% CAGR as enterprises move toward API-first integration. Platform architectures give shippers a single pane of glass for carrier booking, inventory positioning, and financial services. Explainable-AI modules help these platforms meet new fairness regulations without sacrificing optimization accuracy. Aggregators that once thrived on manual coordination now face shrinking margins because code-based orchestration scales better than headcount.

Enterprise clients with unusual compliance needs still commission custom orchestration, particularly to navigate Carbon Border Adjustment reporting. However, shared-infrastructure economics let platforms spread robotics fleets and micro-warehouse investments across hundreds of customers, lowering unit costs. Embedded finance services deepen lock-in by tying working-capital flows directly to shipment visibility. Competitive intensity is therefore shifting from freight rates to developer-friendly APIs and fintech innovation.[3]John McDowell, “Supply-Chain Finance Benefits,” Federal Reserve Bank of Atlanta, frbatlanta.org

By Enterprise Size: Platforms Level the Playing Field for SMEs

Large Enterprises captured 63.10% of the Fifth-Party Logistics market share in 2025, but Small and Medium-sized Enterprises (SMEs) are forecast to expand at a 14.03% CAGR through 2031. RaaS and pay-per-use warehouse models give SMEs access to automation that was previously reserved for Fortune 500 budgets. Embedded finance on 5PL portals cuts borrowing costs by up to 300 basis points, letting smaller firms fund inventory builds during holiday peaks. The omnichannel order-management complexity sparked by the pandemic also hits SMEs hardest because they lack data-science teams, pushing them toward turnkey 5PL solutions.

Large corporations still enjoy volume discounts and custom service-level agreements. They rely on Fifth-Party Logistics market partners for geopolitical scenario planning and multi-regional network design as they hedge against single-country disruptions. Yet the capability gap is narrowing fast, suggesting a more even market landscape by 2031.

Geography Analysis

North America held 36.72% of the Fifth-Party Logistics market revenue in 2025, underpinned by mature e-commerce ecosystems and early adoption of robotics-as-a-service, which lowers automation entry costs for warehouse operators. Regulatory scrutiny over algorithmic bias in carrier allocation is strongest in the United States and Canada, prompting leading providers to embed fairness audits and explainable-AI components in their routing engines. Direct-to-consumer brand proliferation is adding parcel density that justifies micro-fulfillment rollout in secondary cities, while embedded finance on logistics platforms is gaining traction among small sellers seeking alternative credit.

Asia Pacific is the fastest-growing region with an 11.97% CAGR through 2031. Cross-border e-commerce corridors linking China, Southeast Asia, and Australia generate high-frequency parcel flows that benefit from unified customs clearance and duty pre-payment features. Government grants for supply-chain digitalization in India and Indonesia encourage mid-tier manufacturers to outsource orchestration to the Fifth-Party Logistics market platforms. Urban congestion fees in major Chinese cities are pushing warehouse operators to adopt autonomous mobile robots that can work in tighter footprints, accelerating RaaS uptake. Nearshoring trends also spur investment in Vietnamese and Thai fulfillment hubs as brands diversify away from single-country sourcing.

Europe maintains steady growth driven by far-reaching sustainability regulations. The Carbon Border Adjustment Mechanism demands granular emissions reporting, prompting importers to enlist 5PL providers with certified calculation engines. The Digital Product Passport program accelerates blockchain deployment across fashion and electronics supply chains. Providers offering packaged compliance plus fulfillment gain an advantage over asset-heavy rivals focused solely on transport. Although South America and the Middle East & Africa lag in infrastructure, select urban centers see pilot projects for shared micro-fulfillment, signaling future catch-up potential as capital becomes available.

Competitive Landscape

Competition is intensifying, but the Fifth-Party Logistics market remains moderately fragmented as asset-heavy incumbents upgrade technology while software-centric entrants scale via platforms. Incumbents such as Kuehne + Nagel and DSV are embedding fintech modules to lock in clients through working-capital solutions announced in 2025. Platform natives differentiate with API libraries that connect shopping carts, order-management systems, and robotics fleets in real time. Investment flows favor providers that can show end-to-end visibility rather than discrete transport assets.

Strategic alliances form around automation. Nippon Express partnered with a robotics manufacturer to create region-specific autonomous mobile robots, aiming for large-scale deployment by 2026. DHL and FedEx continue to expand shared RaaS pools to reach utilization targets that justify subscription pricing. Providers are also acquiring niche blockchain startups to accelerate compliance readiness for European provenance rules. The convergence of logistics and finance is rewriting valuation models, with investors rewarding blended revenue streams that include embedded lending.

Regulatory dynamics are shaping product roadmaps. The EU AI Act forces routing engines to expose decision logic, pushing vendors to build transparent model-management layers. Providers with strong governance credentials can pitch compliance as a service, turning regulation into a moat. Consolidation is expected as capital demands for micro-fulfillment networks rise; smaller regional 5PLs may exit or merge to secure funding for urban warehouse expansions.[4]European Commission, “AI Act Regulatory Framework,” europa.eu

Fifth-party Logistics (5PL) Industry Leaders

Kuehne + Nagel International AG

UPS Supply Chain Solutions

C.H. Robinson Worldwide

DHL Supply Chain (DHL Group)

CEVA Logistics (CMA CGM Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GXO Logistics announced the opening of a new distribution hub in Canada. This move officially deepens the company's global logistics partnership with the global jewelry brand Pandora, providing advanced, multi-tenant inventory orchestration in North America.

- March 2026: DHL Supply Chain announced the construction of a 26,600-square-meter carbon-neutral logistics center in Rheinbach, Germany, scheduled to go on-stream in August 2026. The facility is being built to the "Gold Standard" of the German Sustainable Building Council and is designed modularly to support highly automated e-commerce fulfillment and advanced warehousing processes for flexible enterprise supply chains.

- November 2025: Uber Freight announced an expanded commercial partnership and strategic investment in Better Trucks, an API-first last-mile delivery platform. Through API integration spanning over 50 e-commerce platforms, this alliance enhances Uber Freight's "End-to-End Logistics" ecosystem.

- June 2025: DHL Supply Chain executed a long-term contract with Fortum Battery Recycling to develop customized service logistics solutions for the circular processing of electric vehicle (EV) batteries. This contract illustrates advanced Lead Logistics Partner (LLP) and 5PL orchestration by shifting focus from commodity freight to full-lifecycle asset management.

Global Fifth-party Logistics (5PL) Market Report Scope

| Transportation Services | Road |

| Air | |

| Sea | |

| Multimodal | |

| Warehousing & Fulfillments | |

| Inventory Mangement | |

| Value Added Services (tech, analytics, consulting, etc.) |

| E-commerce & Retail |

| Consumer Packaged Goods |

| Food & Beverage (incl. Cold-chain) |

| Healthcare & Pharma |

| Industrial & Manufacturing |

| Others |

| Direct to E-commerce |

| Aggregator/Integrator for 3PL/4PL |

| Custom Supply Chain Orchestration for Enterprises |

| Platform-based, Technology-driven Outsourcing |

| Others (Government/public sector, alliance-based logistics orchestration, project based events/exhibitions) |

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| Southeast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Model | Transportation Services | Road |

| Air | ||

| Sea | ||

| Multimodal | ||

| Warehousing & Fulfillments | ||

| Inventory Mangement | ||

| Value Added Services (tech, analytics, consulting, etc.) | ||

| By End-user Industry | E-commerce & Retail | |

| Consumer Packaged Goods | ||

| Food & Beverage (incl. Cold-chain) | ||

| Healthcare & Pharma | ||

| Industrial & Manufacturing | ||

| Others | ||

| By Business Model / Client Type | Direct to E-commerce | |

| Aggregator/Integrator for 3PL/4PL | ||

| Custom Supply Chain Orchestration for Enterprises | ||

| Platform-based, Technology-driven Outsourcing | ||

| Others (Government/public sector, alliance-based logistics orchestration, project based events/exhibitions) | ||

| By Enterprise Size | Large Enterprises | |

| Small & Medium Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Southeast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the Fifth-Party Logistics market expected to grow through 2031?

The Fifth-party Logistics (5PL) market is estimated at USD 12.06 billion in 2026 and is projected to reach USD 19.61 billion by 2031, growing at a CAGR of 10.21% over the forecast period.

Which region will add the most incremental revenue?

Asia Pacific leads in growth with an 11.97% CAGR, driven by cross-border e-commerce and supply-chain digitalization programs.

Why are direct-to-consumer brands choosing 5PL providers?

They gain turnkey access to warehousing, transportation, robotics, and embedded finance, which shortens launch times and cuts operating complexity.

What makes healthcare a high-growth end-user segment?

Strict provenance rules and cold-chain needs push pharmaceutical firms toward 5PL partners that integrate blockchain tracking and temperature-controlled logistics.

How does embedded finance change the 5PL value proposition?

Invoice factoring and dynamic discounting embedded in control-tower platforms reduce supplier borrowing costs by up to 300 basis points, deepening client loyalty.

What compliance challenges will 5PL providers face in Europe by 2026?

They must meet Carbon Border Adjustment Mechanism reporting and adhere to the EU AI Act’s transparency rules for optimization algorithms.

Page last updated on: