Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

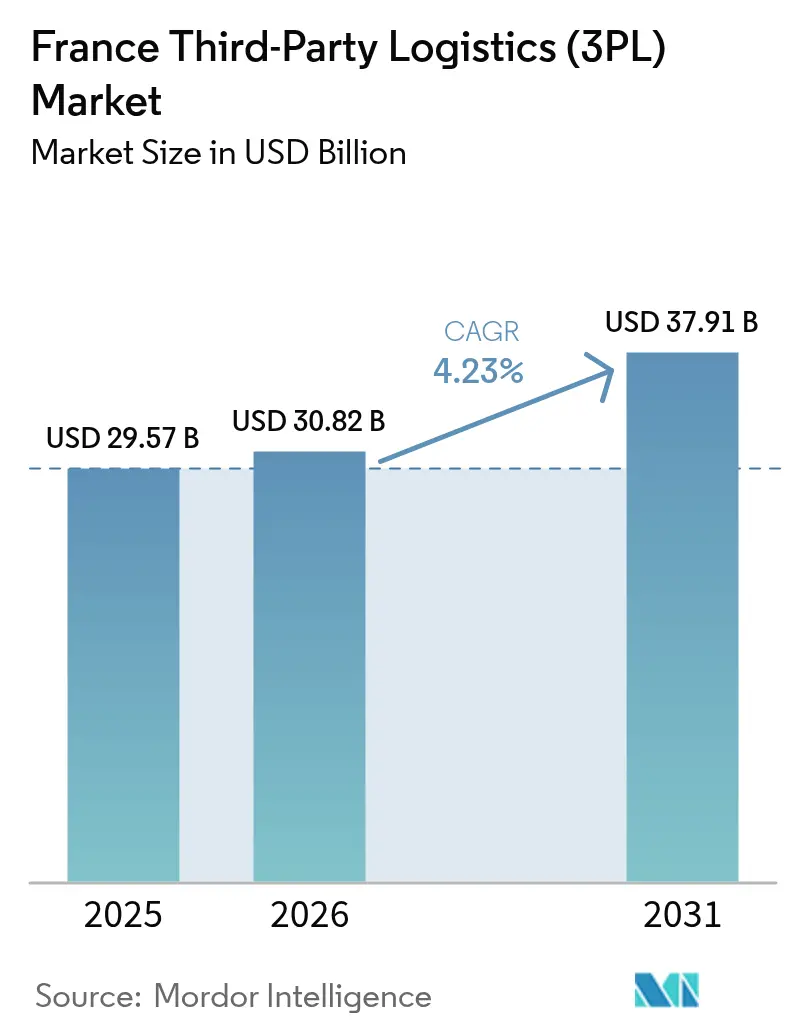

| Base Year Market Size (2025) | USD 29.57 Billion |

| Market Size (2026) | USD 30.82 Billion |

| Market Size (2031) | USD 37.91 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

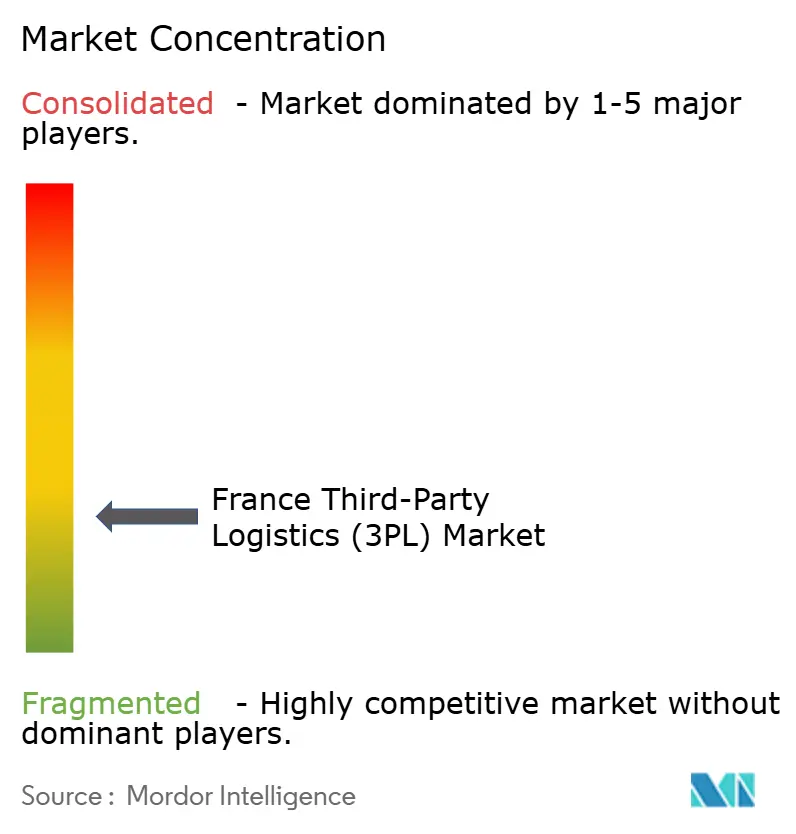

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The France Third-Party Logistics market size is expected to grow from USD 29.57 billion in 2025 to USD 30.82 billion in 2026 and is forecast to reach USD 37.91 billion by 2031 at 4.23% CAGR over 2026-2031.

The moderate expansion is underpinned by France’s role as a continental gateway, rising omnichannel fulfillment needs, and tighter carbon-reporting mandates that are reshaping fleet decisions. Domestic Transportation Management dominates with a 43.2% share, yet Value-Added Warehousing & Distribution is accelerating fastest at a 7.2% CAGR as shippers demand integrated inventory, personalization, and returns capabilities. The automotive industry remains the single-largest user of 3PL services, while life sciences and healthcare lead in growth as cold-chain compliance widens. Asset-light operators hold a slim majority of activity, but hybrid models are scaling swiftly as providers blend owned automation hubs with subcontracted line-haul capacity. Competitive intensity stays high: traditional champions face margin compression, driver shortages exceed 50,000 vacancies, and new environmental taxes start in March 2025, yet more than 80% of logistics firms still expect favorable conditions by 2030[1]Claire Dubois, “Portrait Sectoriel: Transport-Logistique,” France Travail, francetravail.gouv.fr.

Key Report Takeaways

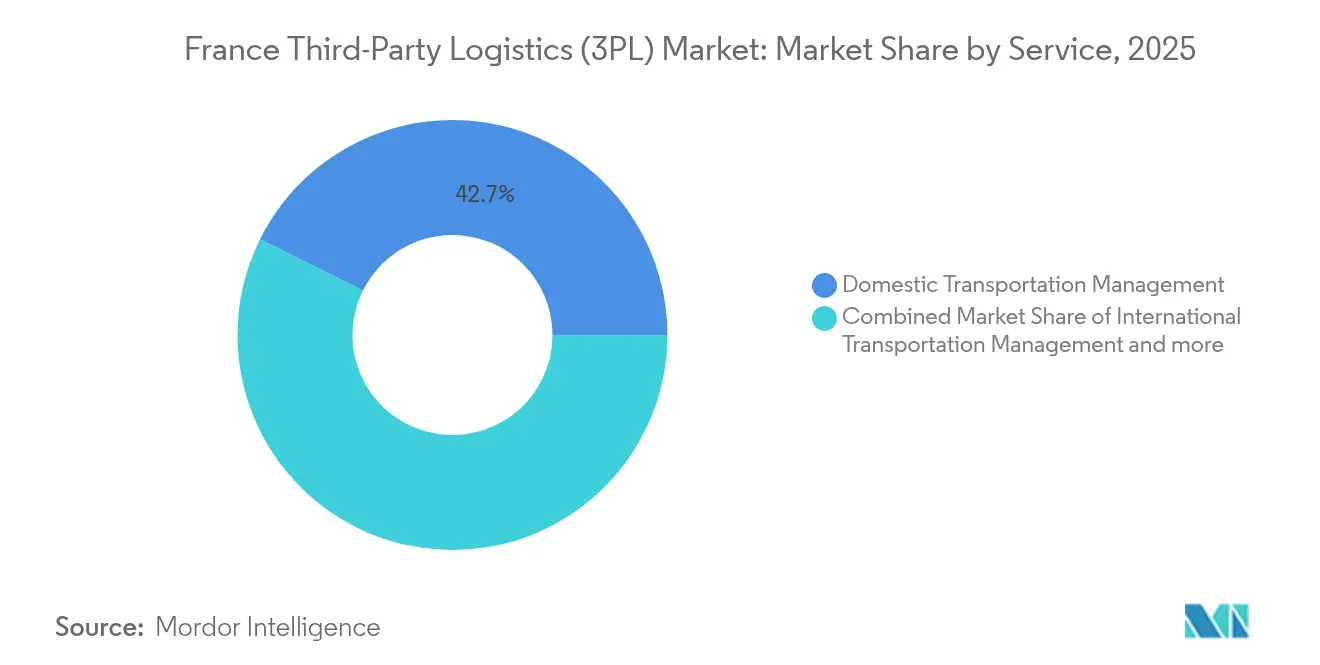

- By service, Domestic Transportation Management captured 42.65% of France third-party logistics market share in 2025, while Value-Added Warehousing & Distribution is projected to grow at a 6.85% CAGR through 2031.

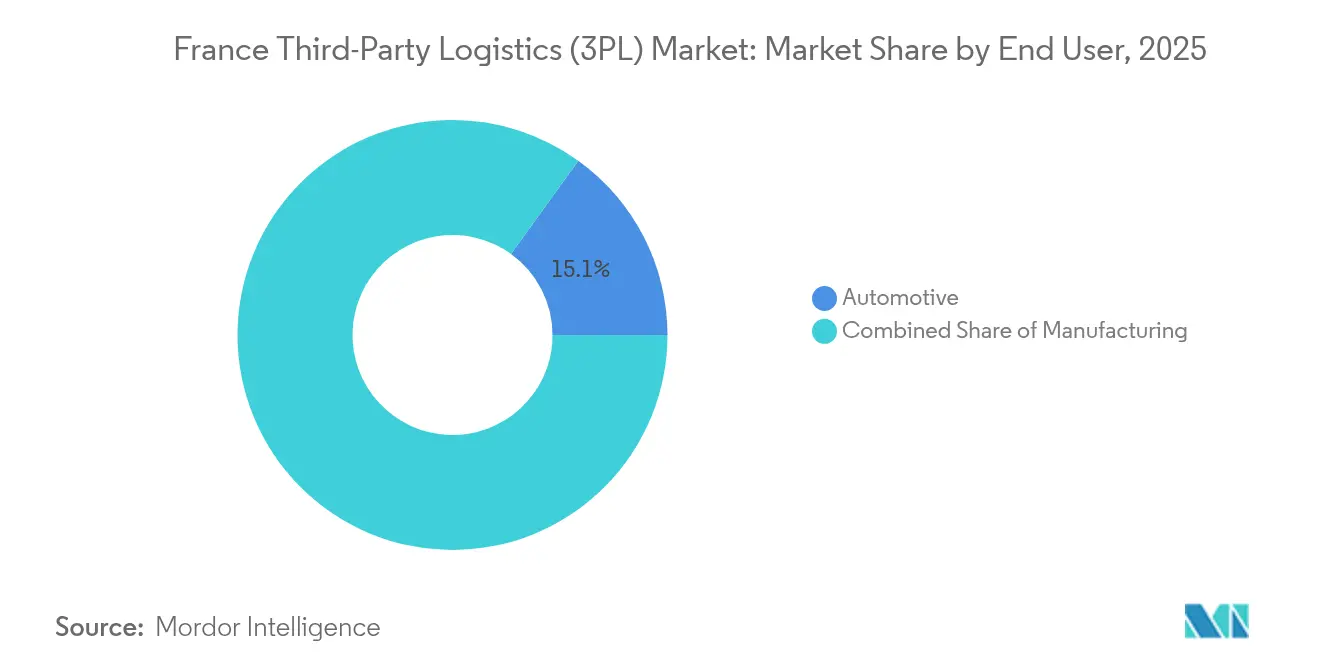

- By end user, automotive accounted for 15.05% of the France third-party logistics market size in 2025, whereas life sciences & healthcare is advancing at a 6.42% CAGR over 2026-2031.

- By logistics model, asset-light providers held a 49.70% share of the France third-party logistics market size in 2025, yet hybrid models record the fastest momentum with a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce fulfilment demand | 1.8% | Global, with concentration in Paris, Lyon, Marseille urban areas | Medium term (2-4 years) |

| Growing intra-EU cross-border trade | 1.2% | Northern France corridors, Calais-Dunkerque axis | Long term (≥ 4 years) |

| Outsourcing focus of French manufacturers | 0.9% | Industrial regions, automotive clusters in eastern France | Medium term (2-4 years) |

| Expansion of cold-chain in pharma & food | 1.1% | National, with early gains in Lyon, Strasbourg, Marseille | Short term (≤ 2 years) |

| 5G-enabled warehouse automation pilots | 0.7% | Major logistics hubs, Paris region priority | Long term (≥ 4 years) |

| Rail-freight revitalisation boosting intermodal 3PL | 0.5% | APAC core, spill-over to Eastern France corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Fulfillment Demand

France’s rapid online retail migration is stretching last-mile capacity, prompting 3PLs to redesign city-center networks around electric vans, micro-hubs, and parcel lockers rather than pure speed. Seventy percent of French online shoppers now prefer low-emission delivery options, pushing providers to balance sustainability and service costs. The resale economy’s climb toward a €14 billion valuation by 2030 intensifies reverse logistics and inspection needs, steering retailers toward value-added warehouse solutions instead of basic transport. Fashion continues to post the deepest online penetration, yet grocery and homeware categories are closing the gap, further lifting demand for temperature-controlled urban facilities. Together, these shifts explain why warehousing and distribution services outpace core trucking within the France third-party logistics market.

Growing Intra-EU Cross-Border Trade

Post-Brexit rerouting places France at the center of mainland trade flows, supported by multimodal investments that connect Northern manufacturing belts to Mediterranean ports. The mandatory ELO digital envelope, effective September 2025, automates customs paperwork for roll-on/roll-off freight, trimming wait times and encouraging smaller 3PLs to add international lanes[2]Pierre-Yves Gahinet, “Présentation du Dispositif ELO,” French Customs, douane.gouv.fr. New corridors stemming from the India–Middle East–Europe initiative will designate French ports as the first continental landing points, raising long-haul forwarding and customs brokerage demand. Government strategy papers for 2025-2026 earmark funding for smart-border technology and low-carbon truck parking along the A1 and A16 highways. As near-shoring expands, shippers increasingly request integrated warehousing in Calais and Lille that can service both domestic and Benelux markets within 24 hours.

Outsourcing Focus of French Manufacturers

Automotive and aerospace OEMs continue to hand off logistics tasks once deemed core, redirecting capital toward electrification and advanced composites. Logistics Service Providers now operate “control towers” that manage multimodal flows, supplier coordination, and carbon dashboards across dozens of plants. Groupe Blondel’s new centralized platform for Mecachrome illustrates the trend, targeting a 45% carbon cut by 2028 through optimized truck loading and alternative fuels. Falling road-transport EBIT—down to 1.4% in 2023—encourages manufacturers to tap 3PL economies of scale instead of operating private fleets. Specialized providers respond by embedding engineering teams capable of line-side delivery and sequencing, thereby blurring the line between logistics contractor and tier-1 supplier within the France third-party logistics market.

Expansion of Cold-Chain in Pharma & Food

Biotechnology breakthroughs and personalized medicines push France’s pharmaceutical logistics bill past €3.5 billion, with cold-chain already one-fifth of the total and heading higher. CEVA’s new Strasbourg campus and Omer-Decugis’s planned 20,000 m² platform at Dunkirk each add critical temperature-controlled capacity. The food sector mirrors this growth as consumer demand for fresh and organic produce rises, requiring 3PL operators to integrate smart packaging, real-time temperature alerts, and HACCP documentation. Investment in dual-fuel reefers and photovoltaic-powered cross-docks gains momentum, enabling providers to meet stricter ATP regulations without sacrificing payload. Cold-chain know-how is becoming a premium differentiator, especially for hybrid 3PL models that retain ownership of highly specialized assets while outsourcing primary haulage.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortage & mounting labour costs | -1.5% | National, acute in Paris and Lyon metropolitan areas | Short term (≤ 2 years) |

| Stringent carbon-emissions compliance costs | -0.8% | National, with higher impact on fleet-intensive operators | Medium term (2-4 years) |

| Urban consolidation-zone truck restrictions | -0.4% | Major urban centers: Paris, Lyon, Marseille, Lille | Medium term (2-4 years) |

| Post-Brexit volatility at Calais & Channel ports | -0.6% | Northern France, Calais-Dunkerque corridor | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Driver Shortage & Mounting Labor Costs

Unfilled truck positions surpass 50,000 nationwide, constraining capacity even as demand rebounds. Warehouses feel parallel stress, with 72% of operators citing recruitment difficulties and 85% flagging retention challenges. The financial strain shows in insolvency filings—486 logistics firms entered administration during Q1 2024 alone, a level unseen since the 2008-2009 crisis. Fuel volatility and limited pricing power compress already thin margins, especially for smaller operators that lack automation capital. These pressures invite accelerated robotics adoption, but payback periods remain lengthy for asset-heavy fleets unless complemented by densification and route-optimization software.

Stringent Carbon-Emissions Compliance Costs

January 2025 introduces €3,000 fines for late emissions declarations, while March adds an annual fleet tax pegged to low-emission vehicle ratios for operators with 100-plus trucks. From 2027, transport firms will enter the SEQE-UE 2 carbon trading scheme, exposing them to cap-and-trade price swings. GEODIS’s pledge to amplify its electric fleet tenfold by 2030 illustrates the scale of capital reallocation away from network expansion and into decarbonization. Asset-light operators that charter subcontracted trucks can shift some responsibility downstream, but shippers increasingly demand end-to-end carbon auditing, limiting the pass-through effect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Leadership Meets Warehousing Innovation

Domestic Transportation Management contributed 42.65% of France third-party logistics market share in 2025, buoyed by dense motorway coverage and sustained road-freight preference. Yet the segment’s mid-single-digit growth is eclipsed by Value-Added Warehousing & Distribution, whose 6.85% CAGR echoes rising SKU counts, omnichannel order profiles, and shrinking delivery windows. International Transportation Management remains vulnerable to geopolitical uncertainty, though the ELO customs envelope and fresh rail links to Spain and Italy are expected to lift volumes from 2026 onward.

The France third-party logistics industry is shifting from transactional trucking to integrated lifecycle stewardship. Retailers request kitting, personalization, and returns grading inside warehouses, embedding 3PLs deeper into the downstream customer experience. This service layering underpins incremental fees and fortifies long-term contracts, offsetting margin squeezes in pure line-haul. Meanwhile, intermodal volumes benefit as government subsidies rekindle rail; MEDLOG’s Paris hub plans to process one million TEUs per year by 2027, supporting emission-cutting objectives and enhancing regional capacity balance.

By End User: Automotive Dominance Faces Healthcare Momentum

Automotive generated 15.05% of the France third-party logistics market size in 2025, reflecting the complexity of just-in-time component flows and tier-1/2 supplier clustering in eastern regions. Assembly-plant shifts to electric vehicles and battery modules add hazardous-goods rules that only seasoned 3PLs can navigate. Nevertheless, life sciences & healthcare posts a brisk 6.42% CAGR as biologics, cell therapies, and vaccine platforms demand validated cold-chain lanes and GDP-compliant facilities.

E-commerce keep climbing on the back of urban micro-fulfillment and resale loops, while food & beverages track parallel growth through chilled and frozen expansion. The France third-party logistics industry sees technology & electronics and consumer goods adapting to circular-economy mandates, necessitating re-processing centers able to triage returns for refurbishment or recycling. Energy & utilities, led by hydrogen and offshore wind components, adds niche oversized-cargo opportunities that reward 3PLs owning specialized trailers and route-planning tools.

By Logistics Model: Asset-Light Supremacy Meets Hybrid Acceleration

Asset-light configurations captured 49.70% of France third-party logistics market share in 2025, offering cash-flow resilience by leasing fleet and facilities. Rising carbon fees further tilt preference toward variable-cost models that transfer capex and compliance to subcontractors. Yet hybrid solutions, blending owned cold-chain depots or automated mezzanines with outsourced trunking, expand fastest at 7.18% CAGR as shippers demand visibility and ESG control without full capital burden.

Large 3PLs now segment portfolios: core verticals such as pharma, perishables, and aerospace receive dedicated, owned infrastructure, while commoditized dry freight leverages brokerage networks. Smaller contenders replicate the formula through asset-share alliances, pooling specialized warehousing yet avoiding full fleet ownership. The France third-party logistics industry expects hybrid penetration to widen once emission-reporting granularity forces precise asset-level disclosures.

Geography Analysis

Paris-Île-de-France anchors the country’s logistics ecosystem through Charles de Gaulle air cargo and a 35-million-consumer catchment reachable within two hours. Warehouse vacancy sits below 3%, fueling a record EUR 4 billion of logistics real-estate investment in 2024. Urban consolidation regulations drive up demand for electric van depots and rooftop solar integration, reinforcing the shift toward value-added city-fringe facilities.

Northern corridors from Calais to Lille remain vital for UK flows despite Brexit turbulence, servicing 38 daily ferry routes. The France third-party logistics market size for the region is poised to lift once the ELO system streamlines border checks from September 2025. Eastern clusters around Metz and Mulhouse thrive on automotive and machinery exports into Germany, while new hydrogen transport lanes emerge from Alsace chemical plants. Southern gateways like Marseille-Fos connect North Africa and the Middle East, with CEVA’s headquarters overseeing a global network from the port city.

Western France, notably Nantes and Cholet, attracts food distribution platforms that service Atlantic coastal tourism centers. Inland, Lyon consolidates life-science logistics due to a dense biotech base and proximity to Alpine cold-chain routes. Government rail-freight incentives are funneled to these corridors, with national targets to double tonnage by 2030, offering modal diversification benefits to 3PLs. Overall, regional specialization enhances the France third-party logistics market’s resilience by spreading exposure across multiple growth levers.

Competitive Landscape

The France third-party logistics market is fragmented. GEODIS, once the clear leader, slipped to seventh place domestically after a 15% revenue slide to EUR 11.6 billion in 2023, prompting its Ambition 2027 plan focused on digital control towers and an electric fleet expansion[3]Sylvie Charles, “Ambition 2027: GEODIS Strategic Plan,” GEODIS, geodis.com. DHL leverages global scale, winning Sanofi’s three-site contract that includes GDP-certified warehousing and secondary distribution, reinforcing its healthcare stronghold. Kuehne+Nagel, posting CHF 24.8 billion turnover in 2024, is integrating IMC Logistics and City Zone Express to widen U.S. and Southeast Asian routes funneling into France.

Portfolio reshaping continues: Modalis entered hydrogen logistics via its Air Flow acquisition, while CEVA invested in a Strasbourg pharma campus and a Côte d’Ivoire decarbonized maritime lane. Retailer–3PL joint ventures such as METRO and ID Logistics’ Cholet facility illustrate cross-sector collaboration, uniting food-service demand with green building certification. Technology adoption accelerates—55% of providers rate generative AI favorably and 58% are ramping robotics—yet only 29% intend to deploy at scale within 12 months, pointing to a future competitive wedge between digital frontrunners and laggards.

France Third-Party Logistics (3PL) Industry Leaders

DSV

DHL Supply Chain

Kuehne + Nagel

CEVA Logistics

UPS Supply Chain Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kuehne+Nagel reported CHF 24.8 billion turnover for 2024 and opened an automated fulfillment center in Italy serving Southern and Eastern Europe.

- March 2025: French Customs confirmed the ELO digital envelope becomes mandatory 1 September 2025 for roll-on/roll-off traffic.

- February 2025: Logicor forward funded a 12,850 m² Beaucaire warehouse slated for Q1 2026 completion with EV charging and green tech.

- February 2025: France introduced an annual fleet tax for operators with 100-plus vehicles to accelerate low-emission adoption.

France Third-Party Logistics (3PL) Market Report Scope

A comprehensive background analysis of the France 3PL Market, covering the current market trends, restraints, technological updates and detailed information on various segments and competitive landscape of the industry.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

How large is the France third-party logistics market in 2026?

The market is valued at USD 30.82 billion in 2026 and is projected to reach USD 37.91 billion by 2031.

Which service segment is expanding fastest?

Value-Added Warehousing & Distribution is growing at a 6.85% CAGR through 2031 as retailers demand integrated inventory and returns management.

What is driving life sciences logistics demand?

Growth stems from cold-chain requirements for biologics and vaccines, prompting specialized facilities such as CEVA’s new Strasbourg hub.

How are environmental regulations affecting 3PL costs?

From 2025, fleet taxes and emissions-reporting fines compel operators to invest in electric vehicles and emissions auditing, raising compliance outlays.

Page last updated on: