Glass Fiber Reinforced Polymer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

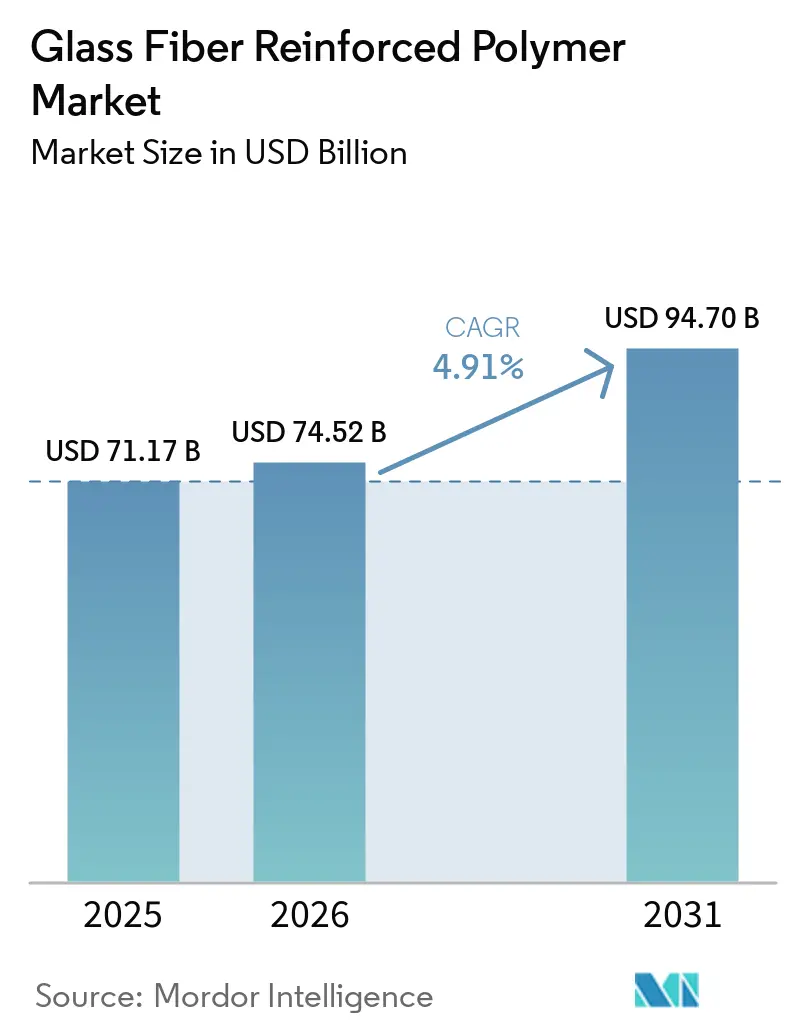

| Market Size (2026) | USD 74.52 Billion |

| Market Size (2031) | USD 94.70 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

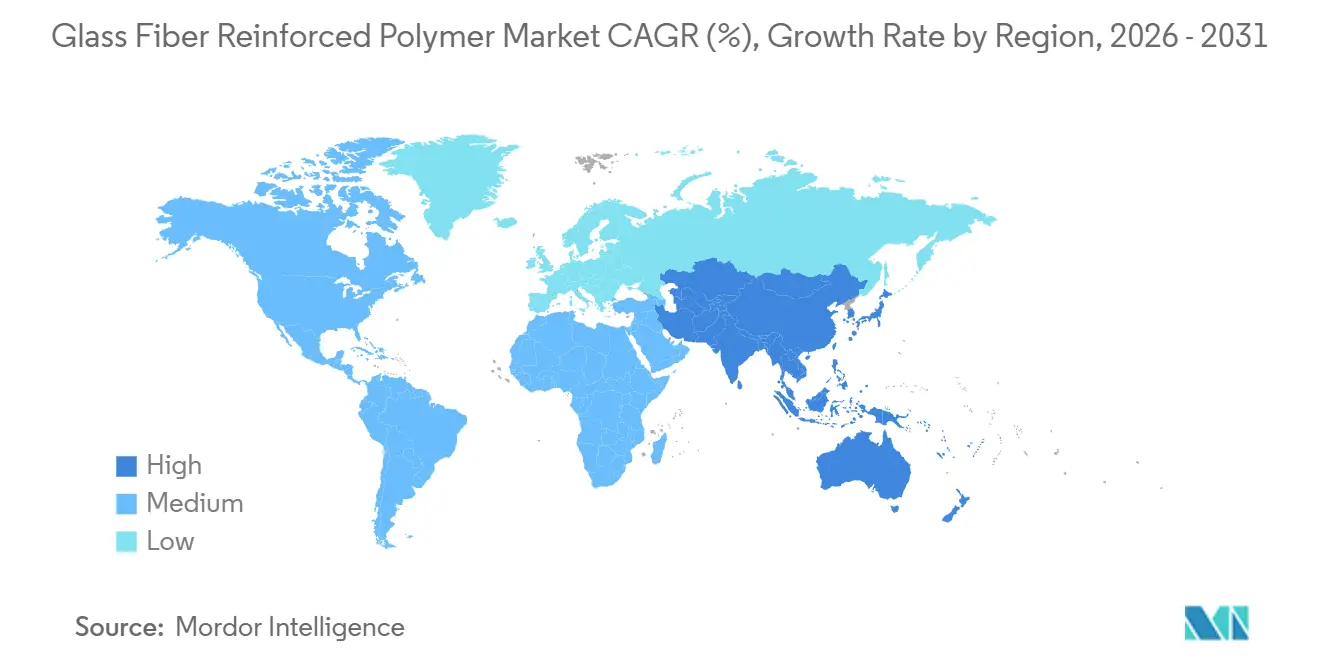

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Fiber Reinforced Polymer Market Analysis by Mordor Intelligence

The Glass Fiber Reinforced Polymer Market size is expected to grow from USD 71.17 billion in 2025 to USD 74.52 billion in 2026 and is forecast to reach USD 94.70 billion by 2031 at a 4.91% CAGR over 2026-2031. Robust demand stems from automotive electrification, offshore-wind capacity additions, and hydrogen infrastructure, all of which favor composites that deliver superior strength-to-weight ratios compared with metals. Polyester resin preserves cost leadership in high-volume construction and infrastructure, while epoxy gains share in aerospace and 700-bar pressure-vessel applications that reward fatigue resistance. Carbon-fiber price deflation and stricter occupational-health rules compress margins, so producers are automating molding lines and integrating downstream to capture more value.

Key Report Takeaways

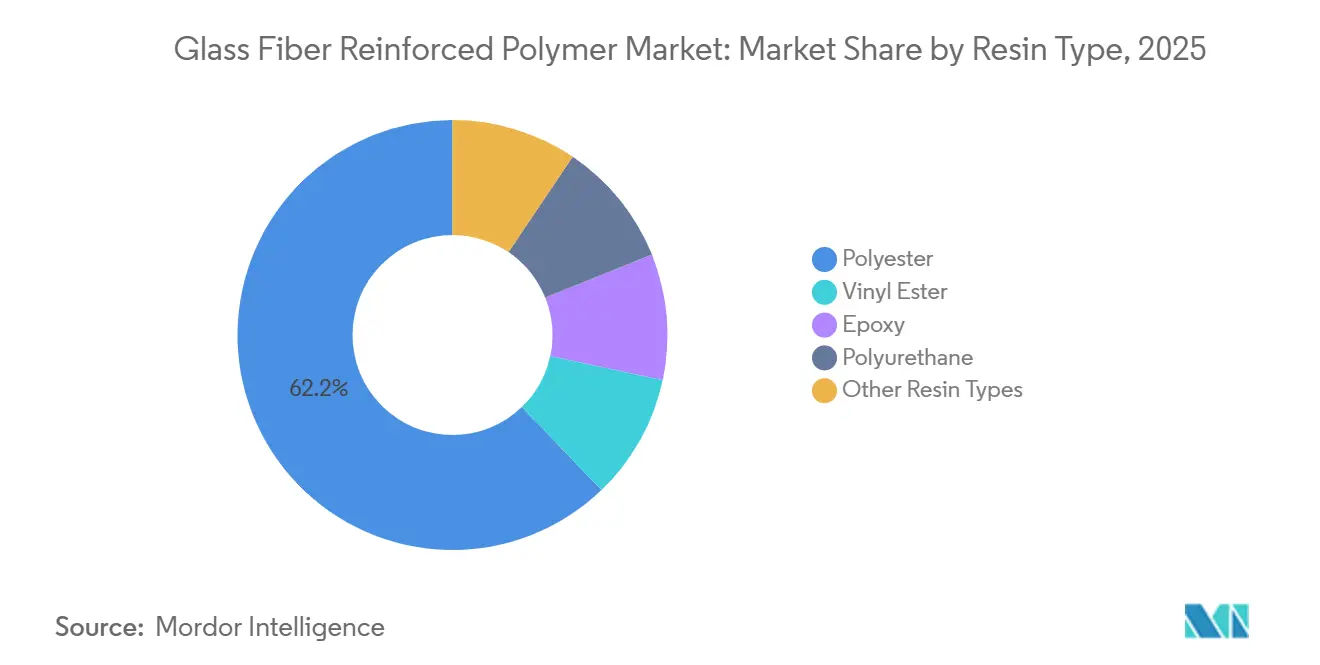

- By resin type, polyester commanded 62.19% share of the glass fiber reinforced polymer market size in 2025; epoxy is projected to grow fastest at 5.08% CAGR from 2026 to 2031.

- By process, compression molding accounted for 31.05% of the Glass fiber reinforced polymer market size in 2025; injection molding is expanding at a 4.97% CAGR to 2031.

- By fiber form, rovings accounted for 41.08% of the glass fiber reinforced polymer market size in 2025, while continuous filament mats will post the quickest 5.12% CAGR to 2031.

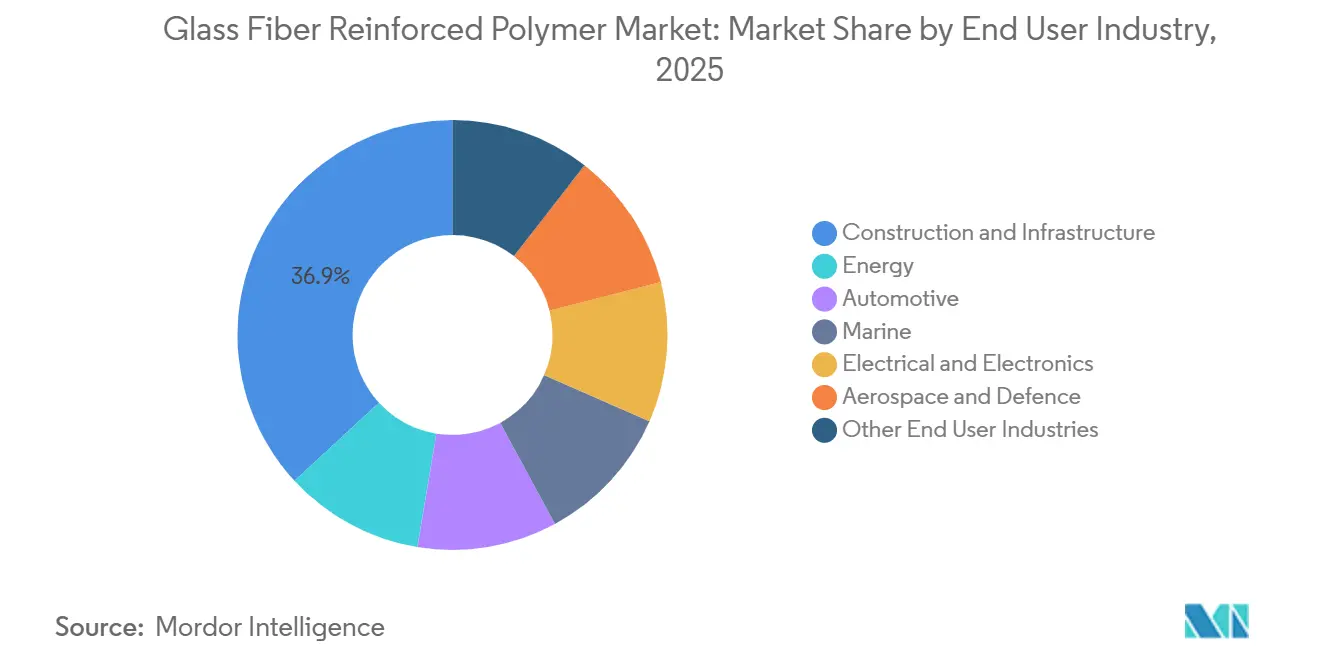

- By end-user industry, construction and infrastructure led with 36.86% of the glass fiber reinforced polymer market share in 2025, while wind energy is forecast to expand at a 5.22% CAGR through 2031.

- By geography, Asia-Pacific captured 48.97% of the glass fiber reinforced polymer market share in 2025 and will remain the fastest-growing region at 4.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Fiber Reinforced Polymer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from the automotive sector | +1.2% | Global, with concentration in China, Germany, United States | Medium term (2-4 years) |

| Expanding use in wind-turbine blade manufacturing | +1.5% | APAC core, North America, Europe offshore installations | Long term (≥ 4 years) |

| Rising aerospace lightweighting initiatives | +0.8% | North America and Europe, spillover to Middle East | Medium term (2-4 years) |

| Surge in hydrogen-storage pressure-vessel production | +0.6% | Europe, Japan, South Korea, California | Long term (≥ 4 years) |

| Rehabilitation of aging offshore oil and gas pipelines | +0.5% | North America Gulf Coast, North Sea, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand from the Automotive Sector

Battery-electric vehicle programs are laser-focused on weight savings, with every kilogram counting. Participants in the glass fiber reinforced polymer market are supplying components like underbody shields, battery casings, and seat frames, enabling an extended range for each kilogram saved. European OEMs chose glass-mat thermoplastic composites for new BEV platforms, a significant increase from the ratio in 2023. Parts made from injection-molded glass fiber reinforced polymer are now replacing stamped steel in door panels and liftgates, leading to a reduction in assembly time. Tier 1 suppliers are now colocating resin-infusion cells adjacent to final-assembly lines, a strategic move that benefits local fiber producers. In response to axle-load regulations, Chinese truck manufacturers have turned to GFRP cargo boxes, resulting in an impressive annual volume increase.

Expanding Use in Wind-Turbine Blade Manufacturing

In 2025, the addition of offshore capacity will spur an incremental demand for glass fiber, as blades exceeding 100 m in length require significant amounts of glass fiber per MW. The adoption of vacuum-assisted resin-transfer molding is enhancing fiber volume fraction, with a preference for continuous-filament mats over woven rovings. As owners target 30-year lifetimes, epoxy penetration in offshore blades surged in 2025. Thanks to U.S. production-tax credits, blade manufacturing plants have been established in Texas and New Jersey. Furthermore, with EU blade-recycling mandates set to kick in 2025, there's a heightened research and development focus on thermoplastic-epoxy hybrids, potentially challenging polyester's cost advantage.

Surge in Hydrogen-Storage Pressure-Vessel Production

Type IV tanks utilize polymer liners reinforced with carbon and glass fiber overwraps, with glass contributing to the hoop strength[1]SAE International, “Hydrogen Storage Standards,” sae.org. Global output of Fuel Cell Electric Vehicles (FCEVs) requires glass fiber. California's energy grid expanded by adding hydrogen storage, with each MWh incorporating glass fiber. Tank manufacturers are increasingly backward-integrating to secure high-strength E-glass grades exceeding 3,400 MPa tensile strength.

Rehabilitation of Aging Offshore Oil and Gas Pipelines

Operators incur annual corrosion losses. However, with the installation of GFRP liners, pipeline life can be extended by 20-25 years. In 2025, firms undertook the rehabilitation of lines in the Gulf of Mexico, a figure that has doubled since 2023. While vinyl ester is adept at resisting hydrogen sulfide, the IMO's five-year integrity check guidelines further enhance the appeal of retrofitting.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing cost | -0.4% | Global, acute in high-labor-cost regions (North America, Western Europe) | Short term (≤ 2 years) |

| Availability of high-performance substitutes | -0.3% | Premium automotive, aerospace segments in developed markets | Medium term (2-4 years) |

| Stricter occupational-health regulations on glass-fiber dust | -0.2% | North America, European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Cost

In 2025, European gas prices led to an inflation in production costs for glass-melting furnaces. While manual lay-up boasts a throughput that lags behind automated compression-molding, the adoption of a six-axis robotic cell poses a challenge for SMEs. Additionally, the volatility of styrene monomer further squeezes polyester margins.

Availability of High-Performance Substitutes

In 2025, standard-modulus carbon fiber prices dropped, making it only a few times the cost of E-glass. This price shift allowed carbon fiber to capture a significant portion of the composite volume. In a strategic move, VW rolled out flax-fiber door skins in its ID-series BEVs, successfully redirecting demand away from traditional glass. Meanwhile, basalt fiber capacity surged in 2025, marking a robust annual growth rate, and in the process, began to chip away at the market share traditionally held by alkali-rich concrete applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Gains in High-Value Niches

Polyester maintained 62.19% of the Glass fiber reinforced polymer market share in 2025 because its lower cure temperature and raw material cost suit high-volume infrastructure. Epoxy captured fast-growing aerospace, wind-blade, and hydrogen-tank niches, expanding at a 5.08% CAGR. Vinyl ester secured a share in chemical-resistant pipeline repairs, while polyurethane is witnessing growth in automotive interiors that necessitate short cure cycles. Specialty resins like PEEK, known for maintaining mechanical integrity at high temperatures, are pivotal for aircraft ducts.

As Type IV vessel orders surge, the rising demand for epoxy is propelling the Glass Fiber Reinforced Polymer market, especially in high-performance segments. Simultaneously, Polyester is safeguarding its commodity volumes by leveraging automated molding cells, significantly reducing labor time per part. Suppliers are diversifying their portfolios, enabling customers to weigh upfront costs against factors like fatigue life, corrosion resistance, and recyclability requirements.

By Process: Injection Molding Automates Complexity

In 2025, compression molding captured 31.05% share of the market volume, as SMC achieved under-hood thermal and mechanical targets in just 2-3 minute cycles. Injection molding, advancing at 4.97% CAGR, penetrates thin-wall electronics housings. While manual hand lay-up continues to cater to marine prototypes, it's gradually losing ground as the automotive and wind sectors shift towards automated methods.

The market for glass fiber reinforced polymers, particularly in injection molding, reaps benefits from reduced cycle times and maintaining scrap levels at minimal levels on six-sigma lines. Continuous processes like pultrusion and filament winding hold a notable market share, driven by the demand from utilities, drive shafts, and pressure vessels for constant cross-sections and material yield exceeding 95%.

By Fiber Form: Continuous Filament Mat Rises

In 2025, rovings accounted for 41.08% of the demand for filament-wound and pultruded parts. Meanwhile, chopped-strand mat captured a notable share of the market in hand lay-up and SMC applications. Continuous filament mat (CFM) is climbing 5.12% CAGR as wind-blade skins and automotive panels migrate to vacuum-infusion, raising the Glass fiber reinforced polymer market size for CFM lines. Biaxial and triaxial stitched fabrics, boasting greater strength than woven rovings, are carving out a niche for weavers in super-yacht hulls and aerospace panels.

Direct-roving technology not only slashes costs but also accelerates custom-blend lead times. This advantage allows major players to safeguard their margins while accommodating smaller orders. As a result, the focus of competitive advantage has shifted from mere furnace tonnage to the nimbleness of textile engineering.

By End-User Industry: Wind Energy Outpaces Legacy Sectors

Construction and infrastructure dominated with 36.86% of volume because corrosion-free rebar and bridge decks cut lifetime maintenance fivefold. Automotive, driven by the adoption of underbody shields in BEVs, accounted for a significant portion of the market. Wind energy, though smaller, is the fastest-growing at 5.22% CAGR, expanding steadily and utilizing an additional amount of glass for every 100-meter blade. Aerospace and defense, holding a notable market share, commands premium pricing, resulting in a disproportionate uplift in the market size of glass fiber reinforced polymers relative to tonnage.

Healthcare, consumer goods, and electronics together comprise a modest but rising share as additive manufacturing standardizes patient-specific devices and smart-luggage shells. The portfolio rebalances toward applications where fatigue life and design freedom justify material premiums.

Geography Analysis

Asia-Pacific supplied 48.97% of the 2025 volume and will grow 4.99% CAGR. This surge is largely attributed to China's impressive output in wind-blade production and India's upgrades to GFRP-rebar highways. Notably, Chinese companies dominate the scene with substantial capacity, constituting a significant share of the global total. Meanwhile, Japan is incorporating GFRP into its regional jets, and South Korea is utilizing glass-fiber epoxy insulation in its LNG carriers, ensuring compliance with the IMO's 2025 thermal standards.

North America benefited from U.S. offshore wind incentives, generating a notable surge in fiber demand for 2025. In Canada, GFRP-lined oil-sands pipelines are set to enjoy a doubled service life. Simultaneously, Mexico's automotive sector, particularly in Guanajuato, has seen a boost in Tier 1 exports, thanks to molded battery enclosures.

Europe was spearheaded by an offshore wind base that utilized significant amounts of fiber[2]WindEurope, “European Offshore Wind Statistics 2025,” windeurope.org. Germany has integrated GFRP into a considerable portion of its 2025 BEV platforms, while the U.K. has set a precedent by mandating composite rebar for coastal bridges exceeding a specific value. South America and the MEA region collectively accounted for a notable share, driven by Brazil's Serra Branca wind projects and Saudi Arabia's ambitious hydrogen corridors.

Competitive Landscape

The glass fiber reinforced polymer market is moderately consolidated. White-space niches are emerging in the industry, such as marine drive shafts that reduce rotational mass and hydrogen pipelines that utilize liners to minimize permeation losses. Companies are capturing a share of the technical-textile market by customizing biaxial fabrics in smaller batch sizes than the larger incumbents typically accept. Additionally, six-sigma injection-molding cells, equipped with viscosity control, have managed to reduce scrap rates, effectively halving the time required for part qualification.

Glass Fiber Reinforced Polymer Industry Leaders

Owens Corning

China Jushi Co. Ltd

Chongqing Polycomp International Corp. (CPIC)

Johns Manville

Nippon Electric Glass Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Owens Corning plans to invest in a new fiberglass insulation line in Kansas, scheduled to commence operations in 2027, while evaluating strategic alternatives for its global glass reinforcements business. This move is expected to influence the glass fiber-reinforced polymer market by driving innovation and expanding product offerings.

- March 2024: At CHINAPLAS 2024, BASF and Jiangsu Worldlight New Material Co., Ltd unveiled a new polyurethane photovoltaic module frame. This innovative frame, crafted from glass fiber-reinforced polyurethanes, boasts an impressive 85% reduction in carbon footprint when compared to traditional aluminum frames.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the glass fiber reinforced polymer market as all virgin composite items where continuous or chopped glass fibers are blended with thermoset or thermoplastic resins and shipped as molded parts, panels, pipes, sheets, profiles, and reinforcing bars to automotive, energy, marine, construction, and electronic buyers. According to Mordor Intelligence, only factory-built volumes that move through organized supply chains are counted.

Scope Exclusions: Hybrid laminates, recycled GFRP scrap, and aftermarket repair kits are outside our scope.

Segmentation Overview

- By Resin Type

- Polyester

- Vinyl Ester

- Epoxy

- Polyurethane

- Other Resin Types (PEEK Resin, Phenolic Resin, etc.)

- By Process

- Manual Process

- Compression Molding

- Sheet Molding Compound Process

- Glass Mat Thermoplastic Process

- Continuous Process

- Injection Molding

- By Fiber Form

- Rovings

- Chopped Strands Mats

- Continuous Filament Mats

- Woven Rovings/Fabrics

- By End User Industry

- Energy

- Automotive

- Marine

- Construction and Infrastructure

- Electrical and Electronics

- Aerospace and Defence

- Other End User Industries (Healthcare, Consumer Goods)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Asian and North American fabricators, resin formulators, civil engineers, and wind-farm buyers. Their insights on average selling prices, installation wastage, and resin-mix changes filled gaps left by secondary work and grounded model assumptions.

Desk Research

We began with credible public datasets that map real production and trade. International Energy Agency wind tables, UN Comtrade codes 7019 and 3926, Eurostat composite output, USGS fiberglass surveys, and Japan Glass Fiber Association yearbooks supplied baseline tonnage and flow patterns. Company filings captured through Dow Jones Factiva and cost curves from D&B Hoovers tied weight to value, while Questel patents tracked resin blend shifts. These sources are illustrative; many others informed validation.

Market-Sizing & Forecasting

We launch with a top-down reconstruction. Regional glass-fiber output is netted for exports, scrap, and resin ratios, then allocated to end uses through penetration curves confirmed in interviews. Targeted bottom-up checks, supplier revenue roll-ups, and sampled price-times-volume pairs fine-tune totals. Key drivers modeled include annual wind-turbine additions, housing starts, passenger-car assembly, resin-to-fiber spreads, and infrastructure stimulus outlays. Forecasts blend multivariate regression with ARIMA smoothing; missing splits are bridged with weighted industry averages cleared by experts.

Data Validation & Update Cycle

Each run passes variance screens and peer review before sign-off. Reports refresh yearly, with interim updates triggered by tariff changes or large capacity additions. A final analyst pass just before release ensures clients receive the latest view.

Why Mordor's Glass Fiber Reinforced Polymer Baseline Commands Reliability

We recognize that published GFRP estimates seldom align because firms choose different product sets, pricing decks, and refresh rhythms.

Values drift when studies drop thermoplastic grades, treat freight as value, or skip customs reconciliation. By pairing clear scope with dual-angle modeling and annual refresh, we avoid those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 71.17 B (2025) | Mordor Intelligence | - |

| USD 64.5 B (2025) | Global Consultancy A | Pipes excluded, single global price |

| USD 50.72 B (2024) | Industry Database B | Thermoplastics omitted, limited customs data |

| USD 39.8 B (2024) | Trade Journal C | Focus on construction and transport only |

These contrasts show that our transparent scope, balanced cross-checks, and timely updates give decision-makers a dependable baseline they can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What was the Glass fiber reinforced polymer market size in 2026?

Global consumption is USD 74.52 billion in 2026 and is projected to reach USD 94.70 billion by 2031, reflecting a 4.91% CAGR.

Which segment is growing fastest?

Wind-energy blades will expand at a 5.22% CAGR as offshore capacity accelerates.

Why is epoxy resin gaining share?

Epoxy offers superior fatigue resistance and low permeability, making it standard for aerospace structures and 700-bar hydrogen tanks.

Which region leads consumption?

Asia-Pacific accounted for 48.97% of the 2025 volume and will stay dominant thanks to Chinese wind projects and Indian infrastructure retrofits.

Page last updated on: