High-Performance Fibers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.35 Billion |

| Market Size (2031) | USD 28.43 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

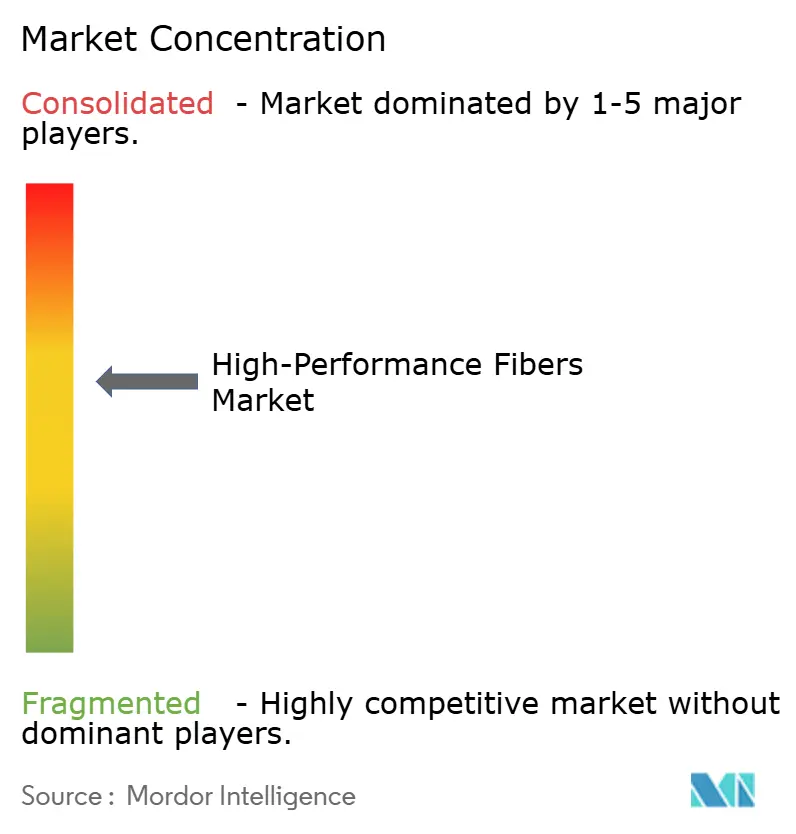

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Performance Fibers Market Analysis by Mordor Intelligence

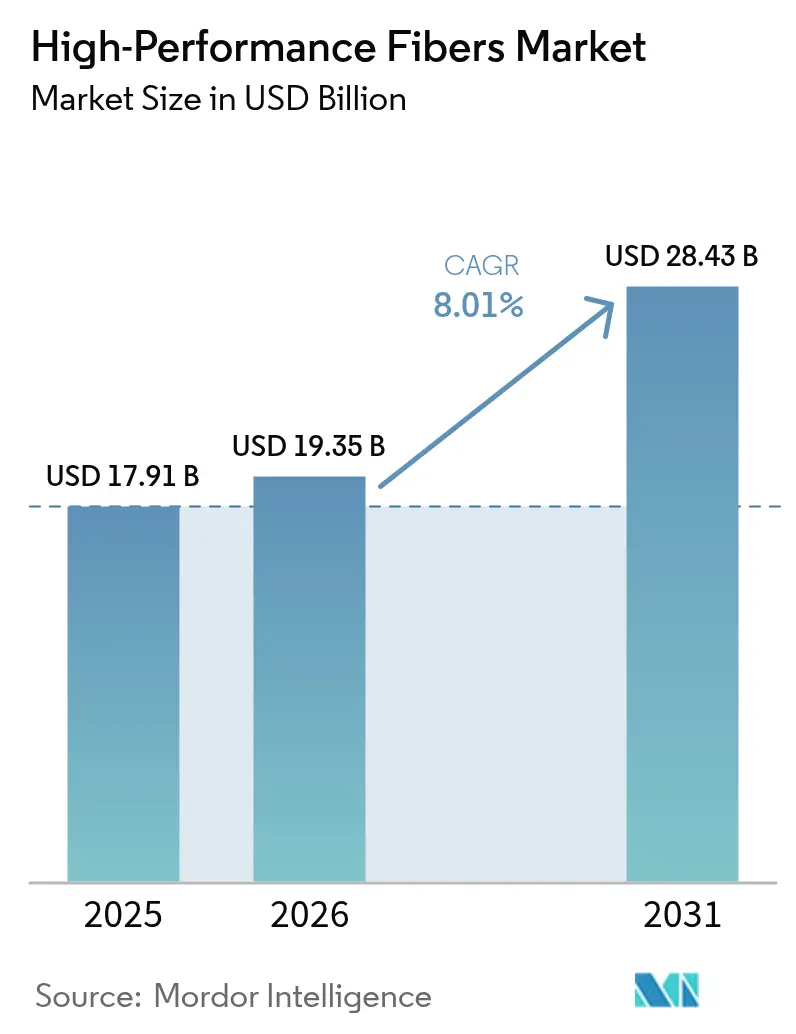

The High-Performance Fibers Market size was valued at USD 17.91 billion in 2025 and estimated to grow from USD 19.35 billion in 2026 to reach USD 28.43 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). Uptake is accelerating as carbon, aramid, glass, and specialty fibers move from niche aerospace uses to mainstream roles in renewable-energy hardware, zero-emission vehicles, and data-rich telecom networks. Commercial wind-turbine blades that now exceed 100 m lengths, Type-IV hydrogen pressure vessels, and 5G fiber-optic cabling all require materials with exceptional strength-to-weight ratios and thermal stability. Aggressive capacity additions in China have pressured average selling prices, yet rising volumes and new applications continue to lift revenue. Policymakers’ decarbonization mandates, combined with supply-chain localization initiatives in North America and Europe, further anchor long-term growth.

Key Report Takeaways

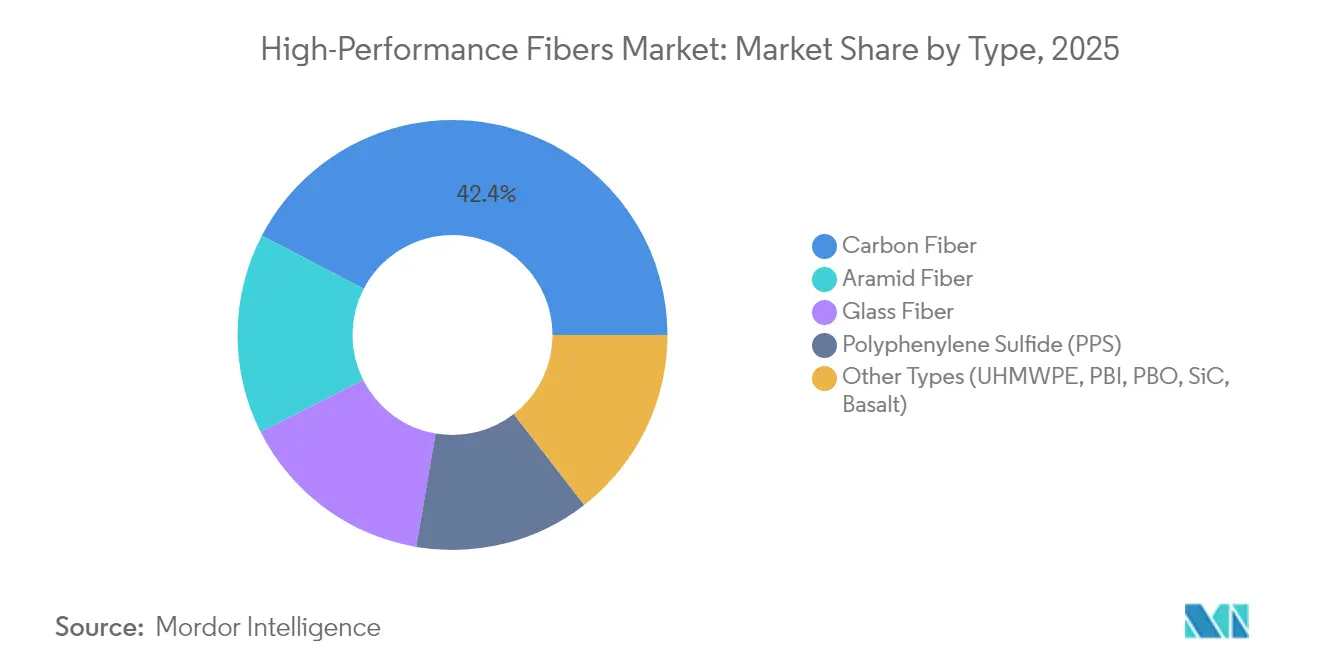

- By type, carbon fiber led with 42.35% revenue share in 2025; its segment is advancing at a 8.88% CAGR through 2031.

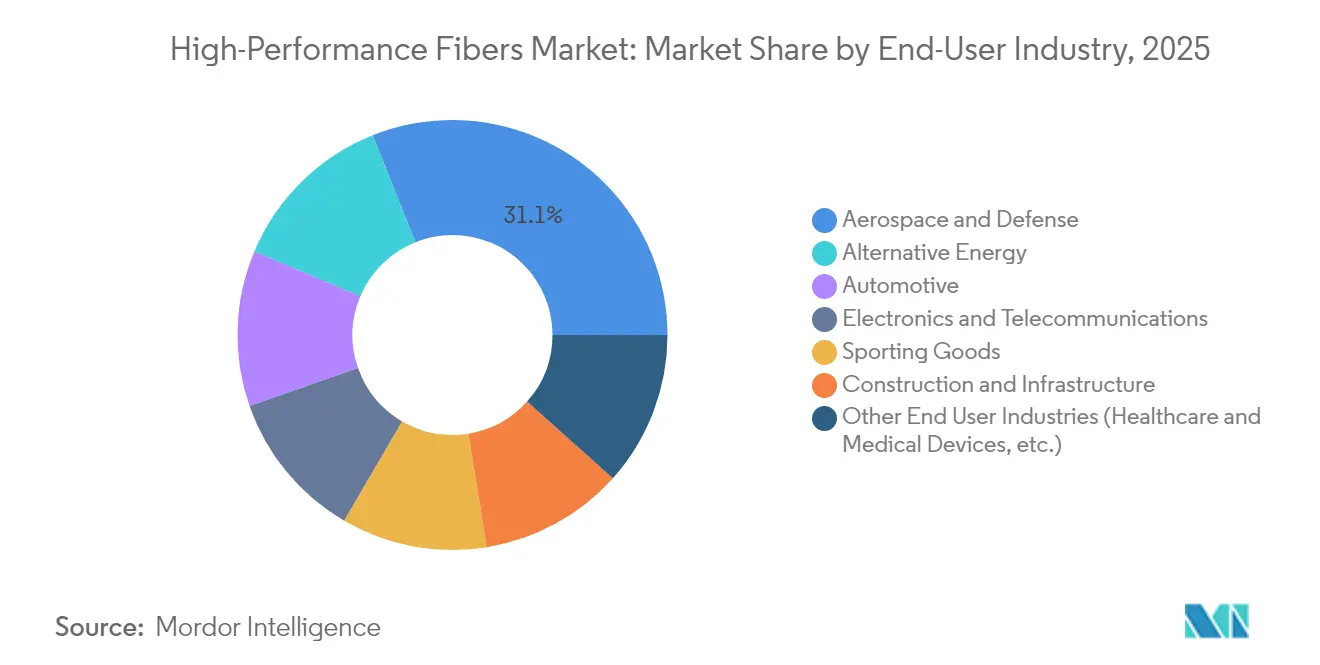

- By end-user industry, aerospace & defense held 31.05% of the high-performance fibers market share in 2025, while alternative energy is forecast to expand at an 8.61% CAGR to 2031.

- By geography, Asia-Pacific accounted for 40.10% of the high-performance fibers market size in 2025 and is rising at an 8.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-Performance Fibers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Lightweight Offshore-Wind Blades | +1.8% | Global, concentrated in Europe & APAC | Medium term (2-4 years) |

| High Demand from Aerospace and Defense Industry | +1.5% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Commercial Rollout of Type-IV Hydrogen Pressure Vessels | +1.2% | Global, early adoption in Japan & Europe | Medium term (2-4 years) |

| 5G Fiber-Optic Cabling Shift to Aramid Yarn | +0.9% | Global, led by North America & APAC | Short term (≤ 2 years) |

| High Demand for Sporting and Protective Products | +0.7% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Lightweight Offshore-Wind Blades

Turbine blades topping 100 m now consume far greater volumes of carbon fiber than earlier models, and automated fiber placement is lowering production costs, allowing wind to surpass aerospace as the single largest volume outlet for some manufacturers. Hybrids that combine carbon and glass are being adopted to balance stiffness, corrosion resistance, and lightning-strike protection. Chinese and European blade makers with captive fiber lines gain cost advantages during rapid capacity build-outs in the North Sea and East China Sea.

High Demand from Aerospace and Defense Industry

Modernization of fighter fleets, uncrewed aerial systems, and space-launch vehicles keeps defense budgets invested in ultra-high-modulus carbon and ceramic fibers. Commercial aviation recovery has renewed orders for composite-rich wide-body platforms, while “more-electric” aircraft architectures introduce electromagnetic-shielding requirements that favor hybrid carbon-aramid lay-ups.

Commercial Rollout of Type-IV Hydrogen Pressure Vessels

The hydrogen economy's emergence is creating unprecedented demand for Type-IV pressure vessels that rely entirely on composite overwraps for structural integrity, with automotive applications leading commercial deployment. Honda’s CR-V e:FCEV and similar fuel-cell vehicles store hydrogen solely in carbon-fiber overwrapped tanks, tripling fiber footage per vehicle compared with Type-III vessels. European truck and rail operators are piloting 700-bar tanks for long-haul routes, spurring demand for tow-preg lines able to guarantee burst strengths above 1,600 bar.

5G Fiber-Optic Cabling Shift to Aramid Yarn

Operators replacing steel strength members with dielectric aramid reduce cable weight by 70%, easing aerial installation and improving bend performance in dense urban ducts. Small-cell architectures that require thousands of short links per square kilometer multiply volume demand for specialty aramid yarns produced in Japan, the United States, and China. [1]Teijin Aramid press office, “Aramid Yarn for 5G Cables,” Teijin Aramid, teijinaramid.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain | -1.1% | Global, concentrated impact in Asia-Pacific | Short term (≤ 2 years) |

| Limited Recycling Infrastructure for Multi-Material Composites | -0.8% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Chinese Over-Capacity Driving Price Compression | -0.9% | Global; strongest in Asia-Pacific and export-oriented hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain

Polyacrylonitrile price swings of 30–40% in 2024 curtailed margins for independent spinners lacking backward integration. Toray and domestic Chinese majors that control precursor capacity insulated themselves from spikes, while several Western producers postponed expansion plans pending more stable feedstock visibility. Bio-based acrylonitrile pilot projects in the United States could diversify inputs, yet commercial output remains years away.

Limited Recycling Infrastructure for Multi-Material Composites

Pyrolysis plants can recover carbon fiber at only 70–80% of virgin tensile strength, restricting reuse to non-structural panels. Complex hybrid laminates with metals or thermoplastics raise separation costs, slowing investment in large-scale facilities. The European Union’s extended-producer-responsibility rules may hasten design-for-recycling guidelines, but current economics favor landfilling blade scrap, a practice at odds with corporate sustainability pledges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbon Fiber Drives Innovation Across Applications

Carbon fiber captured 42.35% of the high-performance fibers market share in 2025 and is forecast to climb at a 8.88% CAGR to 2031, underpinned by automotive lightweighting mandates and renewable-energy infrastructure roll-outs. Asia-based producers such as Zhongfu Shenying are injecting fresh capacity—USD 866 million for 30,000 t/y in Jiangsu—to penetrate cost-sensitive industrial segments. Aramid continues to dominate ballistic and telecom applications; Teijin’s industrial-scale recycling plant in the Netherlands now reprocesses aramid yarn into new fiber, lowering lifecycle emissions. Glass fiber remains the low-cost mainstay for construction and standard automotive panels, while polyphenylene sulfide (PPS) enjoys double-digit growth as electric-vehicle battery packs require thermal and chemical resilience. UHMWPE and ceramic fibers fill niche roles in cryogenic storage and hypersonic platforms, respectively.

Rapid cost erosion across industrial-grade carbon is reshaping procurement strategies. Automakers are locking multiyear contracts to assure supply, while wind OEMs negotiate tolling arrangements that exchange volume commitments for price ceilings. Material formulators are coupling carbon tow with low-viscosity epoxy resins to meet high-throughput blade production targets. Concurrently, the high-performance fibers market is witnessing growing venture investment in lignin-derived carbon to ease PAN dependence and improve environmental credentials. Although still pre-commercial, pilot lines have produced 35+ Msi modulus fibers suitable for sporting-goods laminates, signaling potential to disrupt incumbent supply chains later in the decade.

By End-user Industry: Alternative Energy Challenges Aerospace Dominance

Aerospace & defense retained 31.05% of the high-performance fibers market size in 2025, reflecting high certification hurdles that limit new entrants. Airbus and Boeing are extending composite fuselage adoption to narrow-body replacements, boosting per-aircraft fiber volume from 35 tons on current programs to 50 tons on next-generation designs. Defense ministries in the United States, France, and Japan are allocating record budgets for stealth drones and hypersonic missiles, each reliant on ceramic and carbon-carbon composites capable of surviving >2,000 °C flight conditions.

The alternative-energy segment is the fastest mover, advancing at an 8.61% CAGR to 2031 as offshore wind and green-hydrogen projects scale. Blade OEMs are designing 25 MW turbines for floating platforms, each requiring 350–500 tons of carbon and glass fiber. Simultaneously, electrolyzer and hydrogen-tank manufacturers favor carbon over metal for corrosion resistance and weight savings. Electric-vehicle battery enclosures, pressure-plate springs, and structural members further widen use cases, spreading demand across thermoset and thermoplastic matrices. Sporting goods, infrastructure, and medical sectors provide a stable base load consumption but face slower, mid-single-digit growth due to market maturity and regulatory constraints.

Geography Analysis

Asia-Pacific dominates with 40.10% of the high-performance fibers market share in 2025, propelled by China’s renewable-energy deployment and aggressive vehicle-electrification timelines. Beijing’s Five-Year Plan backs >100 GW/year of offshore-wind additions, doubling fiber usage in large-diameter blades. Domestic producers have broken Western monopoly on T1000-class carbon, enabling local OEMs to meet defense and aerospace specifications for advanced fighter jets. Japan’s Toray and Teijin continue to command premium niches, while South Korea channels PPS and glass fiber into battery housings and electronic substrates.

North America, supported by the Inflation Reduction Act and Buy-American policies, is prioritizing domestic carbon-fiber output. New lines in Washington State, Alabama, and Quebec will add >15,000 t/y by 2027, mitigating reliance on Asian precursors and aligning with national-security objectives for fighter programs and space launchers. Mexico’s growing EV assembly capacity is pulling aramid and glass imports south of the border, prompting regional converters to co-locate near final assembly hubs.

Europe's market evolution emphasizes sustainability and circular economy principles, with regulatory frameworks that increasingly favor bio-based and recyclable fiber solutions over conventional materials. The region's wind energy sector drives significant carbon fiber demand, while automotive applications focus on lightweight solutions that support emission reduction targets . German automakers validate thermoplastic carbon architectures that allow easier re-melt, while Nordic energy developers test bio-based epoxy matrices in offshore prototypes. Regional growth lags Asia’s pace yet commands higher average selling prices due to stringent quality and environmental standards.

Emerging demand in South America and the Middle East remains opportunistic, tied to infrastructure and renewable-energy megaprojects but tempered by currency volatility and skills shortages.

Value Chain Analysis

The high-performance fibers value chain starts with upstream petrochemical and specialty-chemical inputs (notably acrylonitrile for PAN-based carbon fiber precursor and solvents/additives used in gel-spinning and fiber finishing), then moves through precursor production, fiber spinning (carbon, aramid, glass, PPS, UHMWPE, and specialty grades), and downstream conversion into yarns, fabrics, nonwovens, UD tapes, and prepregs. The final transformation happens at composite part and component fabricators serving aerospace and defense, wind blades, hydrogen Type-IV pressure vessels, electronics and telecom cabling, construction reinforcement, and protective products.

Key bottlenecks remain in (i) precursor and energy-intensive stabilization and carbonization steps, which constrain carbon-fiber output and increase exposure to feedstock volatility, and (ii) lengthy qualification and certification cycles in aerospace, which slow supplier switching and tie up capacity in approved grades. The chain is increasingly shaped by vertical integration (Tier-1 players controlling precursor through prepreg) and by qualification-led pull-through at the materials-to-prepreg interface, where programs such as NCAMP help standardize material datasets and shorten adoption timelines for certified composite systems.

Competitive Landscape

Roughly 20 global players control 70% of installed spinning and conversion capacity, giving the high-performance fibers market a moderately concentrated profile. Tier-1 incumbents such as Toray Industries Inc., Mitsubishi Chemical Group, and Teijin Ltd. leverage fully integrated PAN or PPTA precursor supply chains to prepreg roll to secure cost and quality advantages over mid-tier rivals. Competitive differentiation increasingly revolves around sustainability metrics. Teijin Ltd.’s closed-loop aramid recycling recovers >85% of fiber tensile strength, enabling integration into new telecom cables without performance sacrifice. European producers are trialing bio-based epoxy routes, while North American start-ups explore lignin-carbon blends.

High-Performance Fibers Industry Leaders

Toray Industries Inc.

Teijin Ltd.

Mitsubishi Chemical Group

Owens Corning

DuPont

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is opening where end users need certified, application-ready materials rather than commodity fiber, particularly in aerospace and defense prepregs and thermoplastic composites, as well as in telecom cabling that substitutes dielectric aramid yarns for steel strength members. NCAMP-driven qualification activity also creates a practical commercialization pathway for new resin systems and fiber-reinforced prepregs, supporting suppliers that can deliver consistent specifications and documentation across multi-site supply chains.

On the supply side, new capacity and capability additions are creating room for localized and specialty-grade growth, alongside cost-competitive industrial volumes. In June 2026, Toray Advanced Materials Korea completed an expansion of its second meta-aramid fiber line at Gumi, taking total capacity to 5,400 tons per year. In March 2026, China Jushi began an electronic-grade glass fiber plant in Huaian with 100,000 tons per year of fiber capacity and 390 million meters of electronic cloth, which aligns with demand for higher-performance reinforcement in electronics and telecommunications. Process innovation also points to manufacturing-footprint and energy-efficiency opportunities, including FH Aachen work on plasma-based PAN stabilization that cuts stabilization energy consumption and reduces equipment length requirements, a lever for regions pursuing supply-chain localization and lower-carbon production of carbon-fiber precursor and fiber.

Recent Industry Developments

- May 2026: Toray Advanced Composites expanded NCAMP qualifications for its Toray Cetex TC1225 low-melt PAEK thermoplastic composite system to include T700 uni-directional tape prepreg. The broader qualification set supports faster material selection and certification workflows for aerospace and defense programs, strengthening pull-through for qualified high-performance fiber composite systems.

- March 2026: Teijin Carbon introduced an expanded Tenax Next carbon fiber product line, including pelletized grades and a recycled-carbon-fiber/polycarbonate (rCF/PC) non-woven fabric. The lineup targets industrial processing routes and circular-material requirements, widening downstream conversion options beyond traditional thermoset composite formats.

- August 2024: Renegade Materials Corp., part of Teijin Limited, received NCAMP certification for an epoxy thermoset prepreg on quartz fabric, described as a first for this material category. The certification expands the menu of qualified reinforcement-resin combinations used in high-performance applications, supporting adoption in programs that require standardized qualification data.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The high performance fiber market is defined as demand and revenues for fibers engineered for high strength, stiffness, and heat or chemical resistance, then used in advanced composites, protective materials, and specialty textiles across end users.

Scope exclusions: We exclude finished end products (for example, complete protective gear or molded composite parts) and focus on the fiber and fiber-based intermediate material value.

Segmentation Overview

- By Type

- Carbon Fiber

- Composite Materials

- Carbon Fiber Reinforced Polymer (CFRP)

- Reinforced Carbon Carbon (RCC)

- Textiles

- Microelectrodes

- Catalysis

- Composite Materials

- Aramid Fiber

- Meta-Aramid

- Para-Aramid

- Glass Fiber

- Polyphenylene Sulfide (PPS)

- Other Types (Ultra-High Molecular Weight Polyethylene (UHMWPE), Polybenzimidazole (PBI), Poly(p-phenylene-2,6-benzobisoxazole)(PBO), Silicon Carbide (SiC), Basalt)

- Carbon Fiber

- By End-user Industry

- Aerospace & Defense

- Automotive

- Sporting Goods

- Alternative Energy

- Electronics & Telecommunications

- Construction & Infrastructure

- Other End User Industries (Healthcare & Medical Devices, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research began with building the demand context and setting the rules for what to count as high performance fiber revenue. We relied on public sources such as USGS materials statistics, the US International Trade Commission trade datasets, UN Comtrade, OECD industry indicators, and the World Bank macro series to anchor production, trade flows, and end use activity trends.

Next, company annual reports, investor presentations, and press releases were reviewed to track capacity changes, product mix shifts, and regional exposure. These sources were then used to sanity check growth rates against shipment and channel movement patterns.

We also used paid database subscriptions for company financials and intelligence, patent databases, and an import and export shipment-level database to cross-check expansion timing and the direction of shipments. These sources are illustrative, and other public references were also reviewed to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what is actually being purchased, how pricing moves by grade, and where substitution is happening between fiber families in real projects. We spoke with a mix of raw material suppliers, fiber producers, compounders, converters, distributors, and downstream users, and we gathered input across major consuming regions so the assumptions did not over-index on a single geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 47% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 14% | Managers: 56% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was first constructed using a top-down approach, where end use demand pools were rebuilt from proxy indicators and then converted into fiber value using usage intensity and price ranges. Because the same fiber can flow into composites, protective textiles, and industrial reinforcement, we treated the demand drivers separately and combined them at the end.

To keep the model practical, inputs were selected that can be tracked and explained, including aerospace and defense build rates, automotive lightweighting activity, wind energy installations, industrial filtration and insulation activity, and import and export patterns for technical fibers and related intermediates. Price assumptions were guided by typical grade mix and by expected movement in energy and feedstock costs, then rechecked with interview feedback to avoid overstating ASP growth.

Results were corroborated with selective bottom-up approximations, including supplier revenue disclosures, regional channel checks, and sampled volume times ASP calculations where public data allowed it. Where coverage gaps existed, we used conservative ranges and then tightened them through callbacks. For forecasting, scenario analysis was run around key variables such as capacity additions, end market cycles, and pricing normalization, and the final outlook was selected only after it matched the direction of consensus from practitioners.

Data Validation & Update Cycle

Validation was done by checking the model against independent signals such as trade direction, capacity announcements, and the pace of downstream programs. Where variance appeared too large to be realistic, the underlying driver was isolated and re-tested so the final total was not overly sensitive to one assumption.

Before sign-off, the work is reviewed in steps, starting with logic checks, followed by year-on-year movement checks, and then a final consistency review across regions and applications. The study is refreshed annually, and interim updates are triggered when there are material events such as large plant ramps, meaningful price shocks, or demand disruptions. A fresh pre-delivery review is then completed so clients receive the latest updated view.

Mordor Intelligence's High Performance Fiber Market Size Compared Against Other Published Estimates

Published market sizes for high performance fiber can differ even when they appear to cover the same topic, because the counting rules are not always the same. Differences usually come from what is included as fiber revenue versus finished composite parts, the year used as the starting point, and how pricing is carried forward across grades.

In this study, the main gap driver is scope and timing. Values are anchored to fiber and intermediate material revenues and to a defined base year before growth is applied, then checked against capacity and trade signals. This modeling choice is applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.35 B (2026) | |

| Industry Publisher A | USD 17.90 B (2024) | Uses an earlier base year and a longer horizon, and may blend broader technical fiber revenues with adjacent advanced materials, which can shift the starting value and the implied price path. |

| Global Publisher B | USD 17.46 B (2024) | Applies a performance-threshold definition and reports in USD millions with its own scope for types and applications, which can pull in or leave out certain fiber families and alter currency timing assumptions. |

Across the three figures, the spread is largely explained by base-year selection and what is counted as fiber revenue versus nearby materials or downstream products. By keeping inputs traceable to end use activity, trade, and capacity signals, each step can be explained and the estimate updated cleanly when market conditions change.

Key Questions Answered in the Report

What is the current size of the high-performance fibers market?

The high-performance fibers market size is valued at USD 19.35 billion in 2026 and is projected to reach USD 28.43 billion by 2031, growing at an 8.01% CAGR.

Which fiber type commands the largest share?

Carbon fiber leads with 42.35% of the high-performance fibers market share in 2025, supported by expanding applications in wind-turbine blades and hydrogen storage systems.

Which end-user industry is expanding the fastest?

Alternative energy is the fastest-growing end-user segment, advancing at an 8.61% CAGR as wind and green-hydrogen projects scale globally.

Why is Asia-Pacific the dominant regional market?

Asia-Pacific holds 40.10% of global revenue due to integrated supply chains, China’s renewable-energy build-out, and Japan’s advanced-materials expertise.

What is the biggest supply-chain challenge facing producers?

Volatility in polyacrylonitrile precursor supply and limited recycling infrastructure are the main bottlenecks, collectively trimming the forecast CAGR by nearly 2%.

Page last updated on: