Fiber Reinforced Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

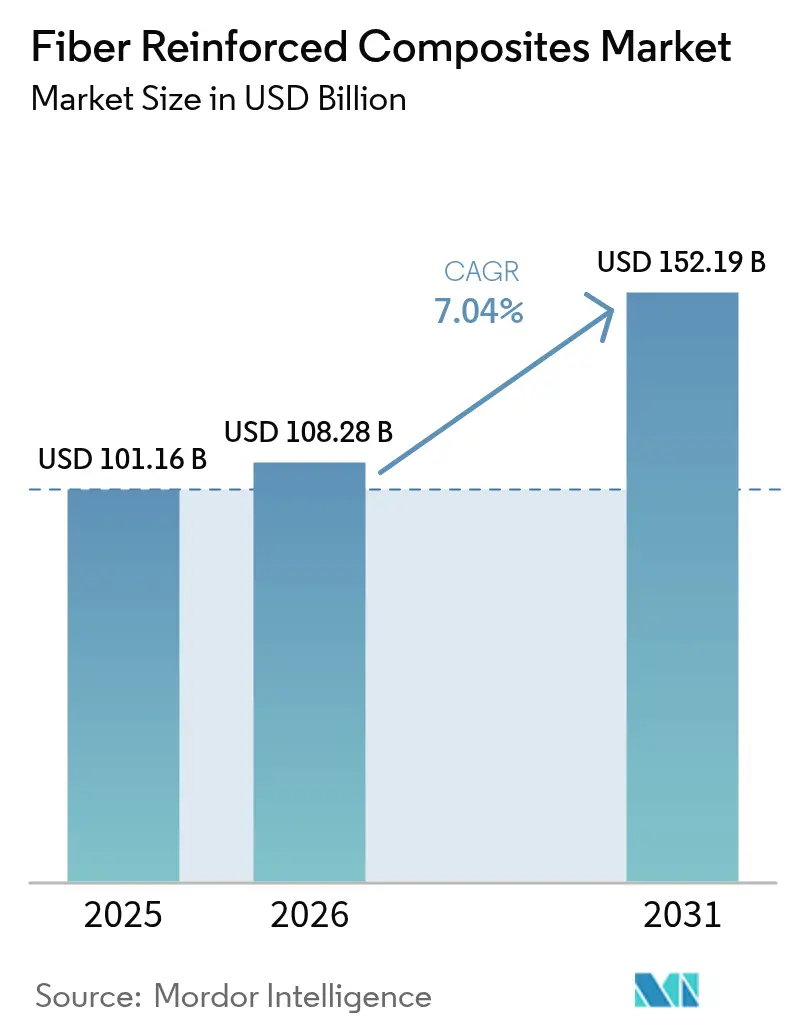

| Market Size (2026) | USD 108.28 Billion |

| Market Size (2031) | USD 152.19 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Reinforced Composites Market Analysis by Mordor Intelligence

The fiber reinforced composites market size was valued at USD 101.16 billion in 2025 and estimated to grow from USD 108.28 billion in 2026 to reach USD 152.19 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). Robust demand originates from aviation programmes that allocate more than 50% of structural weight to composites, notably the Boeing 787 and Airbus A350 platforms[1]CompositesWorld Editors, “Aerospace drives 50% composite content in new programmes,” compositesworld.com. Automakers pursuing Corporate Average Fuel Economy compliance and electric-vehicle range gains accelerate adoption of lightweight carbon laminates, while the wind sector’s push toward 100-meter blades further enlarges the fiber reinforced composites market[2]Federal Register, “Corporate Average Fuel Economy Standards for MY 2027-2032,” federalregister.gov. Process automation deepens competitiveness, with automated fiber placement lines resolving labour shortages and consistency challenges. Regionally, Asia-Pacific leads on the back of China’s large-scale manufacturing capacity, although local overcapacity pressures linger even as India’s nascent aerospace ecosystem scales.

Key Report Takeaways

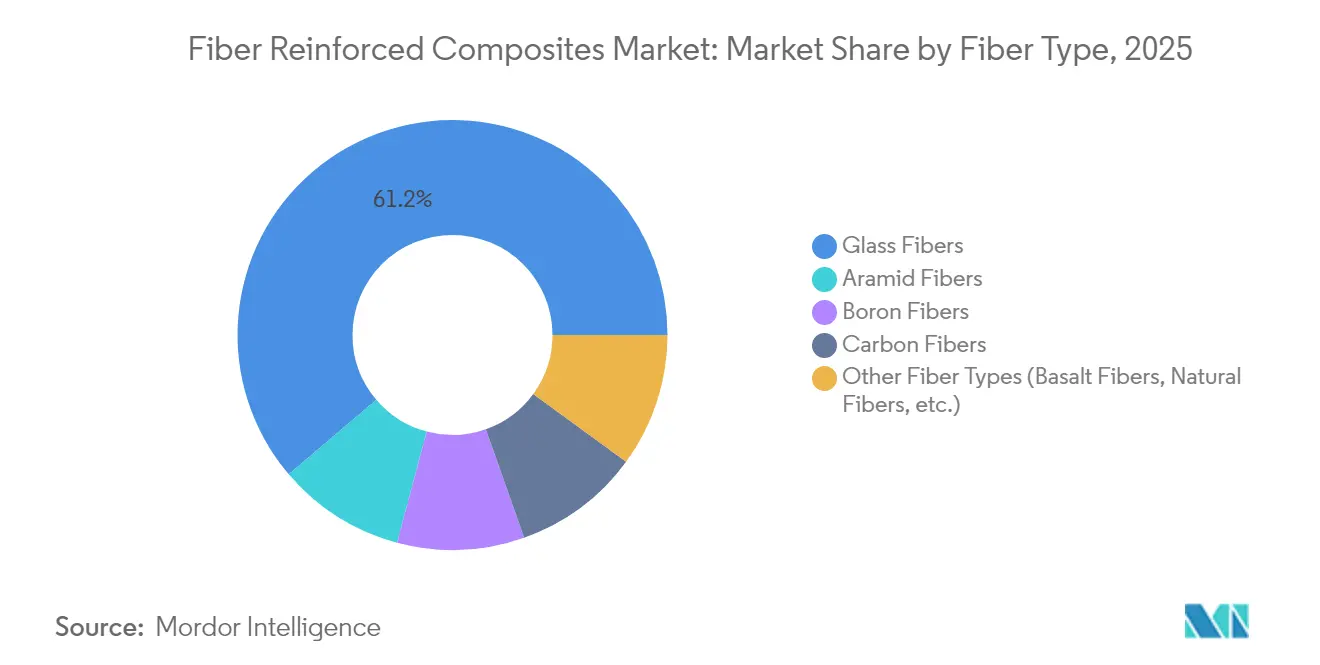

- By fiber type, glass fibers led with 61.22% revenue share in 2025; carbon fibers are poised to expand at an 7.86% CAGR through 2031.

- By matrix, polymer systems accounted for 69.78% share of the fiber reinforced composites market size in 2025, while metal matrix composites will increase at a 7.31% CAGR through 2031.

- By manufacturing process, lay-up methods held 25.64% of the fiber reinforced composites market share in 2025, whereas automated fiber placement is forecast to grow at an 7.92% CAGR to 2031.

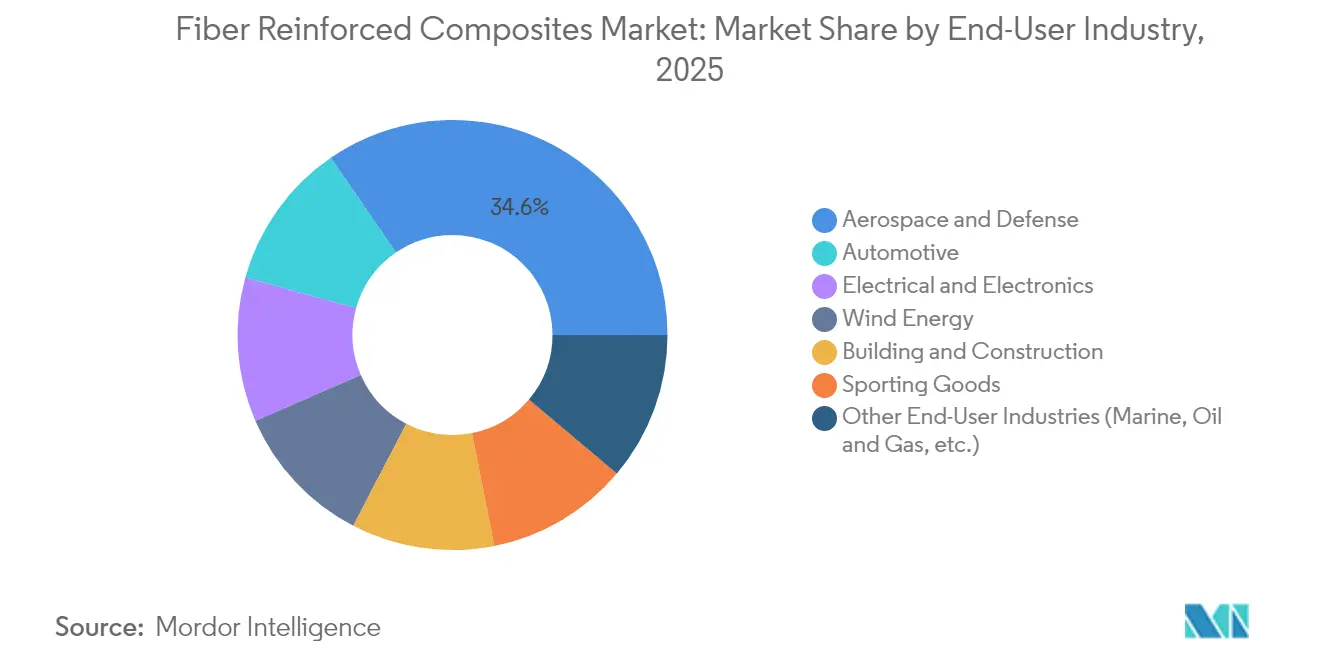

- By end-user industry, aerospace and defense captured 34.58% share in 2025; automotive applications represent the fastest growth at a 7.74% CAGR to 2031.

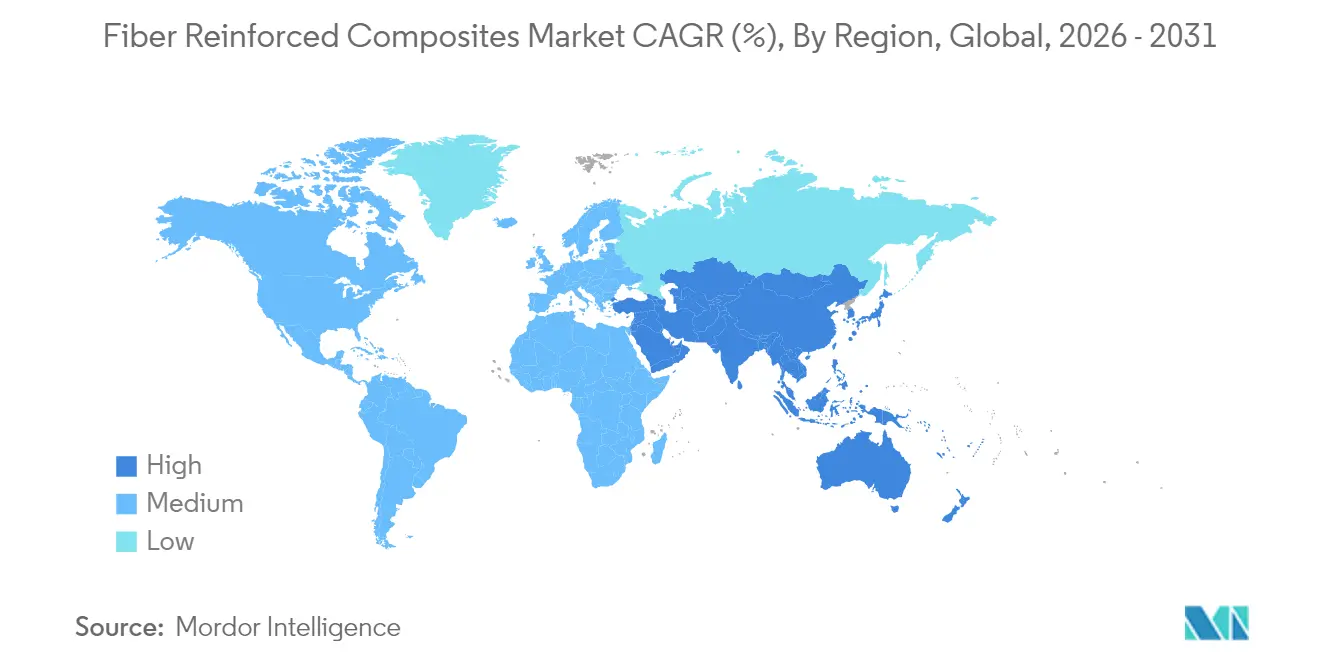

- By geography, Asia-Pacific dominated with a 40.46% share in 2025 and is set to climb at an 8.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fiber Reinforced Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aerospace composite demand | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Wind-turbine blade length upsizing | +1.2% | Global, led by Europe & China | Long term (≥ 4 years) |

| Automotive lightweighting mandates | +1.5% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Infrastructure rehab with FRP rebar | +0.8% | North America & Asia-Pacific | Long term (≥ 4 years) |

| Rapid-layup thermoplastic UD tape lines | +0.9% | Global manufacturing hubs | Medium term (2-4 years) |

| Carbon-capture derived acrylonitrile feedstock | +0.3% | Europe & North America early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace Composite Demand

Commercial programmes target 50% composite content to secure 15–20% fuel-burn reductions, and eVTOL designs push that ratio even higher. Hexcel’s commercial aerospace revenue jumped 21.3% in 2024 on wide-body build rates, yet supply chain tightness tempers near-term deliveries. NASA’s HiCAM effort aims to multiply output rates for thermoset and thermoplastic fuselages, signaling a structural demand uplift. Parallel R&D on fully composite cryogenic tanks for liquid-hydrogen propulsion opens new sub-segments for the fiber reinforced composites market. Together, these shifts cement aerospace as a medium-term growth catalyst.

Wind-Turbine Blade Length Upsizing

Blade lengths now exceed 100 meters, demanding carbon spar caps to retain stiffness without weight penalties. The U.S. Big Adaptive Rotor project underscores this trajectory, while hybrid natural-synthetic fibre blends improve lifecycle sustainability. New polyurethane-carbon pultrusion lines from Dow achieve 90% in-line cure, boosting throughput for oversized laminates. Global capacity is forecast to reach 981 GW by 2030, yet recycling end-of-life blades remains unresolved, inviting circular-economy innovation.

Automotive Lightweighting Mandates

EPA rules for model years 2027-2032 and parallel CAFE targets oblige 2% annual efficiency gains, making carbon composites integral to battery-electric platforms. AFP adoption has lowered cycle times and enabled General Motors to shave mass from body-in-white structures. Ford’s composite C-brace on the 2022 Bronco Raptor validated crash and stiffness benefits under off-road abuse. Battery enclosures now capitalise on composites’ weight and thermal-runaway resistance, further expanding the fiber reinforced composites market.

Infrastructure Rehab with FRP Rebar

Corrosion-free CFRP rebar outperforms steel at one-quarter the weight, translating to thinner covers and extended bridge lifecycles. Valley Metro documented 23% total savings and a 110-day schedule cut on its light-rail extension using FRP reinforcement asce.org. Self-sensing cement enhanced with carbon fibres delivers gauge factors near 40, allowing embedded monitoring of structural health. Transportation regulators across North America and Asia-Pacific are mainstreaming GFRP bar specifications, sustaining long-term demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw-material & processing costs | -1.40% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Difficulties in Recycling | -0.80% | Europe & North America regulatory pressure | Medium term (2-4 years) |

| Performance defects due to water absorption and low fire resistance | -0.60% | Global, critical in marine & aerospace applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material & Processing Costs

Energy-intensive carbonisation drives elevated input costs, although lignin-based precursors from the University of Manchester suggest 3–5 × savings potential. Traditional AFP systems list at USD 3–6 million, but modular leasing models lower the entry barrier. SGL Carbon’s 35.2% sales drop in fiber units shows sensitivity to volatile commodity pricing. Recycled carbon fibre, requiring far less energy, can relieve some pressure while preserving mechanical properties.

Difficulties in Recycling

End-of-life turbines and aircraft could yield 840,300 tonnes of CFRP waste annually by 2050, versus sub-100,000 tonnes recycling capacity today. Acetolysis methods depolymerise epoxy-amine matrices at room temperature, fully recovering fibre quality. Ambient-air pyrolysis keeps 73.3% tensile strength after 500 °C treatment, making industrial adoption feasible. EU directives push OEMs toward such solutions, prompting OEM partnerships like Boeing’s carbon-fibre reclamation network.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Carbon Drives Innovation Despite Glass Dominance

In 2025, glass fibers dominated the market with a 61.22% share, driven by cost efficiencies and robust supply chains in the construction, automotive, and wind energy sectors. While holding a smaller share, carbon fibers are projected to grow at a CAGR of 7.86% through 2031, supported by increasing demand in the aerospace and high-performance automotive industries. Aramid fibers, known for their impact resistance and thermal stability, are primarily used in protective equipment and aerospace components. Despite their higher costs, Boron fibers are utilized in specialized aerospace applications. The adoption of natural fibers is increasing through hybrid composites that combine synthetic and natural fibers, offering environmental benefits while maintaining performance. For example, bamboo and sisal fibers are used in wind turbine blades.

Advancements in manufacturing are transforming fiber production economics. The CARBOWAVE project has introduced microwave-assisted carbon fiber production, reducing energy consumption by up to 70%, potentially altering cost structures and environmental impacts. Saudi Arabia has established the first industrial-scale facility for graphene-enriched carbon fiber production, targeting aerospace, automotive, and construction applications, with projected revenues exceeding USD 1.6 billion by 2030. Basalt fibers are emerging as a sustainable alternative, offering superior mechanical properties and environmental resistance compared to natural fiber composites. Additionally, their cost advantages over carbon fibers make them suitable for offshore wind applications requiring durability in harsh environments.

By Matrix: Polymer Dominance Faces Advanced-Material Challenge

In 2025, polymer systems accounted for 69.78% of the revenue, while metal matrix options are projected to achieve a 7.31% CAGR, highlighting their sustained importance in the fiber-reinforced composites market, particularly for aerospace thermal-management applications. Ceramic matrix composites developed by GE enhance jet engine operating temperatures, improving fuel efficiency by up to 20%. Additionally, carbon-carbon materials are critical for components exposed to hypersonic re-entry and fusion reactors, where endurance at 2,000 °C is essential.

Rapid-cycle thermoplastics, such as polycarbonate, PEKK, and PEEK, are gaining traction due to their recyclability and capability for one-minute press molding. Covestro has introduced continuous-fiber polycarbonate panels targeting the consumer electronics sector. Furthermore, NREL has demonstrated a bio-based epoxy that reduces greenhouse gas emissions by 40% compared to petrochemical-based resins while maintaining production cost efficiency. Mitsubishi Chemical has also developed a ceramic composite capable of withstanding temperatures of 1,500 °C, meeting JAXA specifications for launch vehicles and creating new revenue opportunities in the defense and space sectors.

By Manufacturing Process: Automation Transforms Traditional Methods

In 2025, lay-up maintained a 25.64% market share, while automated fibre placement experienced significant growth, recording an impressive 7.92% CAGR. This trend highlights the increasing focus on labor productivity within the fiber-reinforced composites market. Engel and Fill have successfully developed thermoplastic tape cells, achieving one-minute takt times across 30 tapes and incorporating camera-based quality validation. Meanwhile, pultrusion lines utilizing polyurethane resin systems have achieved a notable 90% in-line cure rate, significantly enhancing output for wind-blade spar caps.

Additive manufacturing is transforming the industry by integrating continuous fibre deposition with in-situ thermoset curing. This advancement not only reduces material waste but also expands design possibilities. In a significant development, the University of Delaware's capillary-fed process secured funding from NASA to advance heat-shield applications in spacecraft. Additionally, injection-compression lines, combining SABIC's Digital Composites platform with Airborne automation, are scaling up composite applications in laptops and vehicle trims. On another front, Cygnet Texkimp's robotic filament winding is effectively supporting 10-meter structures at steep lay-up angles, enabling advancements in hydrogen storage and yacht mast programs.

By End-User Industry: Aerospace Leadership Meets Automotive Growth

Aerospace and defense commanded 34.58% of 2025 turnover and remain the technical vanguard, yet automotive volumes will rise fastest at 7.74% CAGR, driven by battery-electric platforms requiring aggressive mass-offsetting strategies. Wind-energy purchasing eased in 2024 due to logistics bottlenecks, but the long-term pivot to 15-MW offshore turbines ensures a stable call on carbon spar cap supply.

In civil infrastructure, FRP rebar and stay-in-place formwork enhance bridge durability, bolstered by transportation authorities approving non-corroding reinforcement. Electronics miniaturisation benefits from high dielectric strength laminates, and sports equipment remains a steady niche for premium fibres. TPI Composites surpassed the 100,000-blade milestone, applying machine-learning cures that shorten cycle times by 25%.

Geography Analysis

Asia-Pacific generated 40.46% of 2025 sales and is set to post an 8.16% CAGR, ensuring that the fiber reinforced composites market remains anchored in the region. China’s HRC invested USD 33.8 million in Changshu to expand serial thermoset and thermoplastic part output, while India’s Kineco Exel now supplies pultruded carbon planks to Vestas from its Goa site. Taiwan’s Swancor has localised resin plate supply for offshore projects, deepening the regional value chain.

North America leverages an entrenched aerospace base and fuel-economy regulation to maintain demand. GKN Aerospace doubled assembly capacity in Chihuahua, Mexico, adding 200 jobs to serve Gulfstream and HondaJet programmes. Safran expanded LEAP engine capacity in Querétaro, underscoring Mexico’s rise as a composites manufacturing node. MIT researchers developed “nanostitching” with carbon nanotubes, lifting interlaminar shear by 62% and hinting at further light-weighting gains. Europe champions recycling mandates and low-carbon material innovation. The Clean Sky 2 FRAMES project validated xenon flashlamp AFP heating for PEEK and PEKK wingskins, while Strata and Solvay opened the first MENA prepreg plant for Boeing 777X parts in Al Ain, UAE. Brazil’s composites turnover rose 5.6% to USD 560 million in 2024, pointing to latent growth potential across South America.

Competitive Landscape

The fiber reinforced composites market is moderately fragmented. Toray Industries, Hexcel, Owens Corning, and Mitsubishi Chemical Group lead on scale and vertical integration, but mid-tier entrants leverage automation or sustainability niches to differentiate. Hexcel recorded a 21.3% sales lift in commercial aerospace, reflecting volume recovery amid supply-chain knots. Owens Corning divested its glass-reinforcement unit to Praana Group for USD 755 million to sharpen its focus on building products, signalling ongoing portfolio realignment.

Technology-based disruptors attract capital: Boston Materials secured USD 13.5 million for its Z-axis Fibre architecture, with Mitsubishi Chemical’s venture arm joining the round. Saudi graphene-enhanced fibre lines illustrate sovereign diversification into advanced materials, aiming to capture electronics casings and EV battery housings. Automation investments remain pervasive, as OEMs converge on AFP, high-speed RTM, and Digital Composites lines to ensure repeatability and cost parity with aluminium stampings.

Fiber Reinforced Composites Industry Leaders

TORAY INDUSTRIES, INC

Hexcel Corporation

Solvay

SGL Carbon

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Owens Corning finalized the sale of its glass fiber reinforcements business to Praana Group for USD 755 million. Concurrently, Praana Group aims to enhance operational efficiencies within the glass fiber sector, leveraging the increasing global demand for clean energy.

- September 2024: Hexcel Corporation introduced its new HexForce 1K woven reinforcement fabric. This lightweight fabric, developed using Hexcel's proprietary HexTow AS4C 1K carbon fiber, facilitates the production of high-strength, lightweight composite materials. The HexForce 1K fabric is designed for diverse industrial applications, including golf shafts, hockey sticks, and automotive components.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fiber-reinforced composites market as the total value of carbon, glass, aramid, basalt, and other fibers combined with polymer, metal, or ceramic matrices that are manufactured into intermediate or finished parts for aerospace, automotive, wind energy, construction, electrical, sporting, and other industrial uses.

Scope exclusion: one-off repair kits, pure resin systems, and recycled composite scrap traded as waste are left outside this assessment.

Segmentation Overview

- By Fiber Type

- Carbon Fibers

- Glass Fibers

- Aramid Fibers

- Boron Fibers

- Other Fiber Types (Basalt Fibers, Natural Fibers, etc.)

- By Matrix

- Polymer Matrix Composites

- Metal Matrix Composites

- Ceramic Composites

- Carbon-Carbon Composites

- Hybrid Composites

- By Manufacturing Process

- Lay-Up (Hand/Spray)

- Filament Winding

- Pultrusion

- Resin Transfer Molding

- Automated Fiber Placement & Tape Laying

- Compression & Injection Molding

- 3D Printing / Additive Manufacturing

- By End-user Industry

- Aerospace & Defense

- Automotive

- Wind Energy

- Building & Construction

- Electrical & Electronics

- Sporting Goods

- Other End-user Industries (Marine, Oil and Gas, etc.)

- By Geography (Value)

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- South Africa

- Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview plant managers, procurement heads, material scientists, and regional distributors across North America, Europe, Asia-Pacific, and the Middle East. These conversations validate utilization rates, price realizations, and adoption hurdles, filling gaps that published statistics alone cannot close.

Desk Research

We start with public data from tier-1 bodies such as the American Composites Manufacturers Association, Eurostat, the US Geological Survey, and China's National Bureau of Statistics, which help us frame production, trade, and end-use demand. Industry-specific datasets from WSTS for electronics, Global Cement Directory for construction panels, and Asia Metal for fiber precursor pricing feed our baseline assumptions. Company 10-Ks, investor decks, patent filings via Questel, and curated press in Dow Jones Factiva supply cost trends, expansion plans, and technology diffusion signals. This list is illustrative; many additional sources were tapped to complete and cross-check secondary facts.

Market-Sizing & Forecasting

A top-down production and trade reconstruction gives the first pass market value, which is subsequently stress tested with selective supplier roll-ups and average selling price × volume checks. Key fingerprints guiding the model include aircraft build rates, light vehicle composite penetration, average blade length in onshore turbines, resin-to-fiber cost spreads, and regional construction floor space additions. Forecasts rely on a multivariate regression that links those drivers to historical demand, with scenario inputs refined through expert consensus. Where bottom-up estimates miss minor end uses, we adjust by indexing against adjacent material spend patterns.

Data Validation & Update Cycle

Outputs go through variance screens, peer review, and senior sign-off. We refresh every year and trigger interim updates when large capacity additions, regulatory changes, or price shocks occur, so clients always receive our latest view.

Why Mordor's Fiber Reinforced Composites Baseline Is Dependable

Published figures often diverge because studies pick different fiber sets, treat recycled feedstock inconsistently, and convert currencies at varied dates.

Key gap drivers include some publishers limiting scope to polymer matrices, others applying uniform ASP growth without segment nuance, or adopting multi-year update cycles that lag new aerospace build schedules. Mordor's model applies current exchange rates, keeps metal and ceramic matrices in scope, and rolls forward driver data quarterly before release.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 101.16 B (2025) | Mordor Intelligence | - |

| USD 105.22 B (2025) | Global Consultancy A | Excludes metal and ceramic matrices, older currency base |

| USD 110.75 B (2024) | Industry Association B | Inflates by counting repair kits and recycled scrap |

| USD 60.36 B (2024) | Trade Journal C | Focuses on thermoplastics only, limited geography |

External publications place the 2024-2025 market anywhere between USD 60 billion and USD 111 billion, underlining how scope and update cadence shape outcomes. Taken together, the comparison shows that Mordor's disciplined variable selection and timely refresh create a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the Fiber Reinforced Composites market?

The Fiber Reinforced Composites Market is valued at USD 108.28 billion in 2026 and is projected to rise to USD 152.19 billion by 2031.

Which region leads the fiber reinforced composites market?

Asia-Pacific held 40.46% share in 2025 and is advancing at an 8.16% CAGR through 2031.

Which end-use sector generates the highest demand?

Aerospace and defense applications led with 34.58% revenue share in 2025, owing to high composite content in new aircraft programmes.

What major restraint could slow market growth?

High raw-material and processing costs currently reduce the CAGR forecast by 1.40 percentage points, despite ongoing cost-reduction initiatives.

How are composites being recycled?

Emerging chemical depolymerization and optimized pyrolysis techniques now recover up to 93.5% of fiber modulus, although global recycling capacity still lags projected waste volumes.

Page last updated on: