Basalt Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

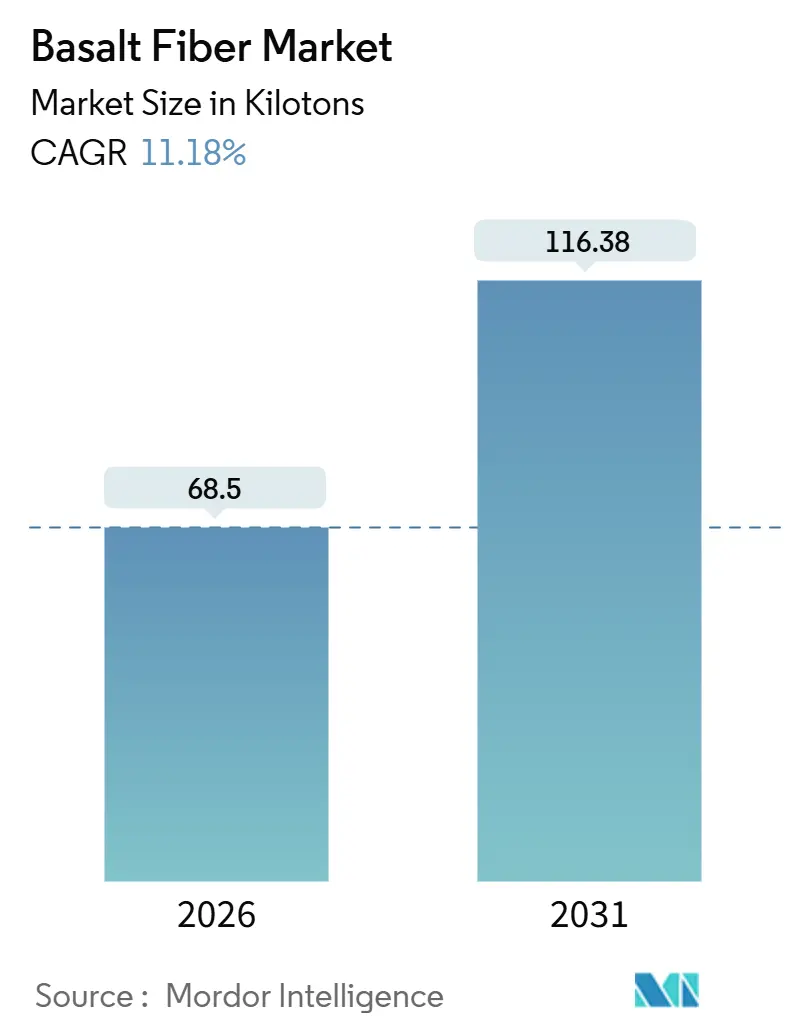

| Market Volume (2026) | 68.5 kilotons |

| Market Volume (2031) | 116.38 kilotons |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basalt Fiber Market Analysis by Mordor Intelligence

The Basalt Fiber Market size is estimated at 68.5 kilotons in 2026, and is expected to reach 116.38 kilotons by 2031, at a CAGR of 11.18% during the forecast period (2026-2031). The surge is tied to infrastructure decarbonization programs, offshore wind construction, and vehicle lightweighting mandates that reward basalt fiber’s superior corrosion and heat resistance. Global producers are scaling capacity to address demand for continuous rovings in turbine blades and automotive body panels, while discrete fiber formats for concrete mixes and insulation gain traction. Regulatory recognition in major codes, coupled with heightened lifecycle-cost scrutiny, is compressing the adoption curve. Intensifying competition and early technical approvals signal a pivotal phase for the basalt fiber market over the next five years.

Key Report Takeaways

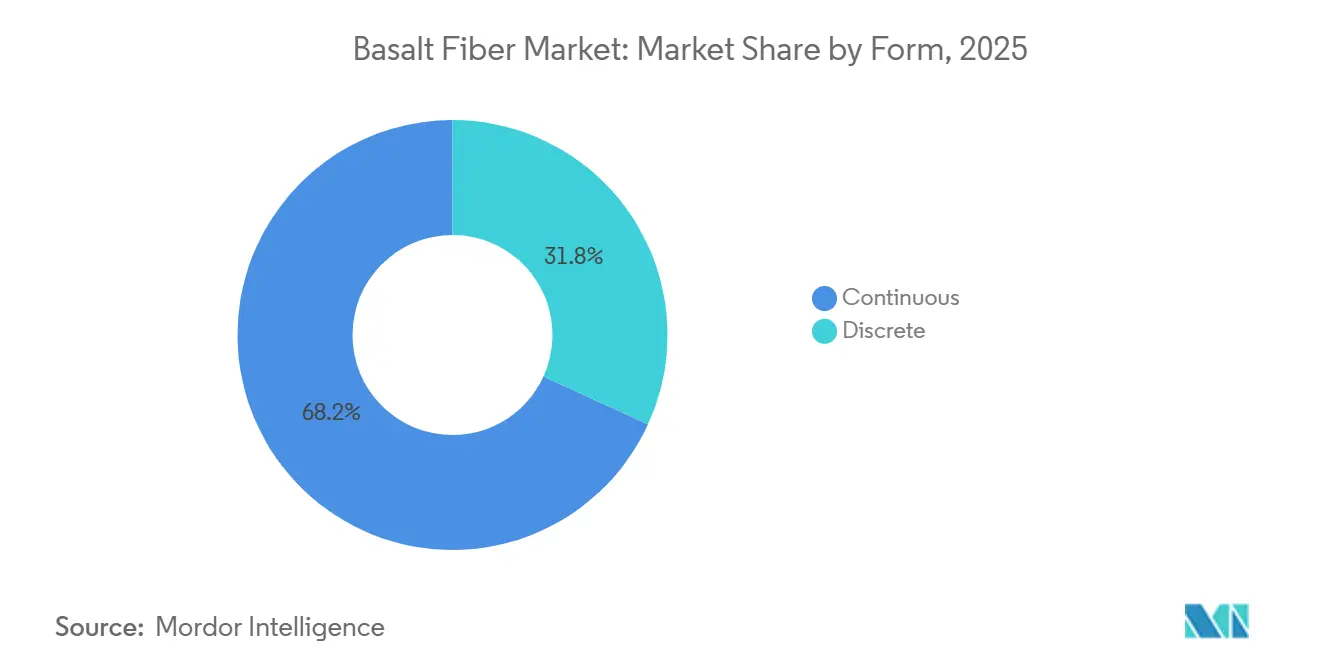

- By form, continuous fibers captured 68.18% of the basalt fiber market share in 2025; discrete fibers are set to post a 13.28% CAGR through 2031.

- By usage, composites accounted for a 72.65% share of the basalt fiber market size in 2025, whereas non-composites are on track for a 13.94% CAGR to 2031.

- By end-use industry, building and construction held 46.89% of the basalt fiber market size in 2025, while energy applications are forecast to expand at a 14.26% CAGR.

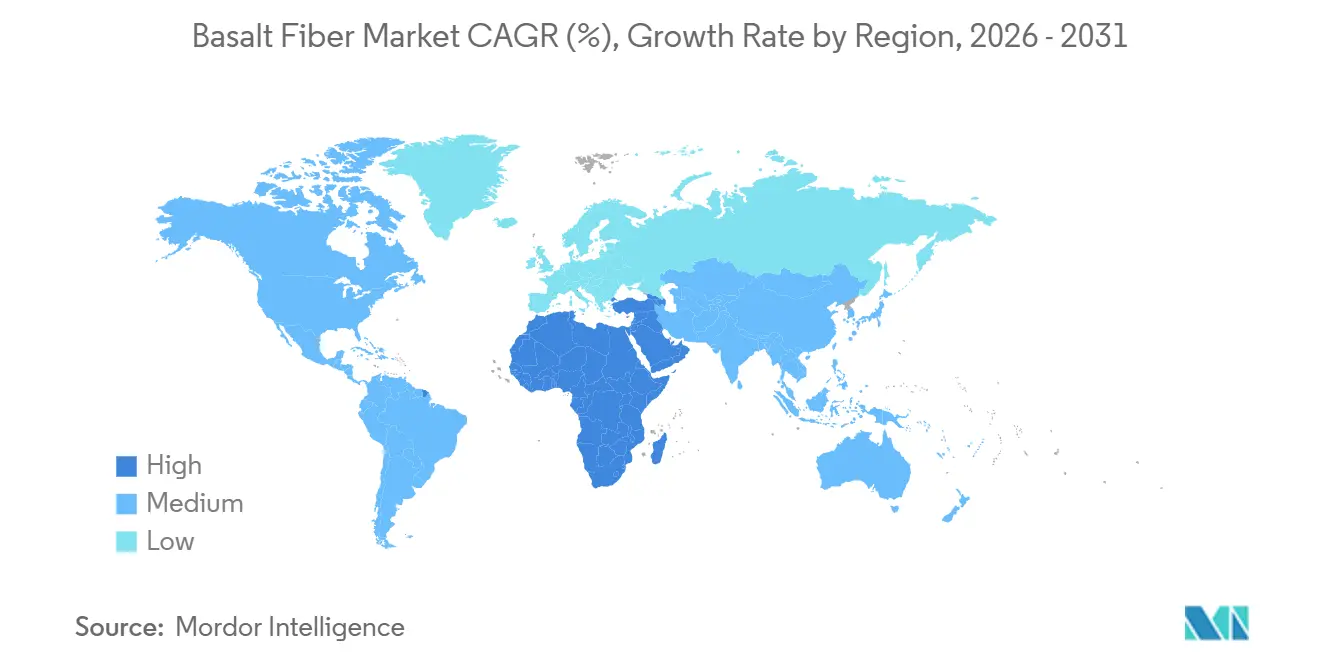

- By region, Asia Pacific led with 48.75% revenue share in 2025; the Middle East and Africa region is projected to progress at a 15.52% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Basalt Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Net-Zero Mandates accelerating basalt rebar | +2.8% | Europe, with spillover to North America | Medium term (2-4 years) |

| Offshore wind-blade build-out needs heat-resistant fabrics | +3.1% | Global, concentrated in Europe, Asia-Pacific, North America offshore zones | Long term (≥ 4 years) |

| Vehicle-lightweighting roadmap in several countries favoring basalt fiber usage | +2.2% | North America, Europe, China | Medium term (2-4 years) |

| GCC desalination expansion driving basalt FRP pipelines | +1.9% | Middle East & Africa, with adoption in Asia-Pacific desalination hubs | Short term (≤ 2 years) |

| LNG platforms requiring cryogenic-tolerant reinforcements | +1.6% | Global, concentrated in Asia-Pacific and Middle East LNG export terminals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Net-Zero Mandates Accelerating Basalt Rebar

The revised EU Net-Zero Industry Act compels project owners to adopt low-GWP reinforcements, placing basalt rebar on specification lists for bridge decks and seawalls. Tensile strengths of 800–1,200 MPa and triple the corrosion resistance of steel lengthen service life to 100 years in chloride-rich environments. EN 13706 now references basalt, removing earlier regulatory gaps[1]European Committee for Standardization, “EN 13706: Fiber-Reinforced Polymer Reinforcement,” cen.eu. France and Germany are piloting basalt rebar in bridge deck overlays and coastal infrastructure, where chloride ingress has historically required steel replacement every 25 years. This regulatory push is compressing payback periods for basalt rebar to under 15 years in high-exposure applications, making it economically viable for public infrastructure budgets constrained by net-zero compliance costs.

Offshore Wind-Blade Build-Out Needs Heat-Resistant Fabrics

Next-generation 15 MW turbines require spar caps that withstand curing exotherms and lightning strikes. Basalt retains strength up to 650°C, outperforming E-glass at 460°C. Flexural strengths of roughly 400 MPa support 120-meter blade spans. The American Bureau of Shipping's guide for floating offshore wind turbines references basalt fiber as a compliant reinforcement for mooring and dynamic cable protection systems, signaling regulatory acceptance that will accelerate adoption in the 80-gigawatt offshore wind pipeline planned for the North Sea and East China Sea through 2030.

Vehicle Lightweighting Roadmap Favoring Basalt Fiber Usage

Automotive lightweighting policies-including the US Corporate Average Fuel Economy (CAFE) standards and the EU's CO₂ emission limits of 95 grams per kilometer, are driving original equipment manufacturers (OEMs) to replace steel and aluminum components with fiber-reinforced composites. Basalt fiber offers a cost-performance balance between glass fiber (lower strength) and carbon fiber (10 times higher cost), making it viable for semi-structural parts such as underbody shields, battery enclosures, and interior panels. Fraunhofer testing showed 30% weight cuts in thermoplastic parts with full crash compliance. US CAFE rules and EU 95 g/km limits intensify the shift, while China’s NEV target drives local capacity expansions.

GCC Desalination Expansion Driving Basalt FRP Pipelines

Saudi Arabia and the United Arab Emirates are expanding desalination capacity by over 5 million cubic meters per day through 2030, and procurement specifications increasingly mandate basalt fiber-reinforced polymer (FRP) pipelines for brine discharge and seawater intake systems to eliminate the corrosion failures that plague steel and glass-reinforced plastic (GRP) in hypersaline environments. Field studies recorded just 18–25% interlaminar shear loss over 7.5 years versus 35–45% for E-glass. Procurement guidelines published by the Saudi Water Authority elevate basalt to preferred status.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Easy availability of substitutes | -2.4% | Global, particularly in cost-sensitive applications | Short term (≤ 2 years) |

| Basalt-ore freight-rate volatility | -1.3% | Global, acute for producers distant from Russian, Ukrainian, and Chinese quarries | Medium term (2-4 years) |

| Abrasive wear on processing equipment raising OPEX | -1.1% | Global, concentrated in regions with aging production infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Easy Availability of Substitutes

Glass fiber maintains a 10-to-1 cost advantage over basalt fiber in non-performance-critical applications such as general-purpose composites and insulation, limiting basalt's penetration into the 7-million-tonne-per-year global glass fiber market. E-glass fiber costs approximately USD 2-3 per kilogram, whereas basalt fiber ranges from USD 20-30 per kilogram, a premium justified only when thermal stability, corrosion resistance, or cryogenic performance is required. Carbon fiber, priced similarly to basalt, offers 30% higher specific strength for aerospace. Steel rebar still holds a 95% share in concrete reinforcement, thanks to entrenched codes and installer familiarity, stalling basalt uptake in price-sensitive regions.

Basalt-Ore Freight-Rate Volatility

Basalt fiber production is concentrated near quarries in Russia (Kamenny Vek), Ukraine (ARMBAS), and China (Zhejiang, Jilin), and freight-rate volatility for bulk basalt ore can swing operating costs by 15-25% annually, compressing margins for producers serving distant markets. Basalt ore is a low-value, high-volume commodity; shipping costs from Russia to Western Europe can exceed USD 50 per tonne when Baltic Dry Index rates spike, effectively doubling the delivered cost of raw material and eroding the price competitiveness of basalt fiber against locally produced glass fiber[2]Baltic Exchange, “Dry Bulk Market Report 2025,” balticexchange.com. Red Sea route disruptions in 2024–2025 lifted freight by 40%, squeezing margins for import-reliant producers and favoring vertically integrated Asian suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Continuous Dominates, Discrete Gains in Concrete

Continuous rovings controlled 68.18% volume in 2025 as turbine blades and auto body panels require unidirectional strength exceeding 4,800 MPa. Discrete fiber volume will expand at a 13.28% CAGR to 2031. The basalt fiber market size for discrete formats is on track to surpass 30 kilotons by 2031, driven by ready-mix concrete mixes that cut on-site labor. Tests show 1% discrete addition lifts flexural strength 25% and shrinks crack width 40% under seismic load. Continuous makers are diversifying into fiber grids for tunnel linings to defend their share.

Project owners in Asia-Pacific and the Middle East favor discrete mixes because they pour faster and meet stricter durability codes. The American Concrete Institute now offers design guidance for both continuous and discrete basalt reinforcement, closing technical gaps. Continuous suppliers leverage economies of scale, producing 6–13 µm filaments suited to high-end aerospace and premium auto parts. As building codes evolve, the basalt fiber market share of discrete formats will keep rising despite the continuous fiber’s entrenched base.

By Usage: Composites Lead, Non-Composites Surge in Infrastructure

Composites absorbed 72.65% of demand in 2025 as epoxy and vinyl-ester laminates dominate wind, auto, and marine builds. The composites portion of the basalt fiber market size is forecast to reach 85 kilotons by 2031, yet non-composites will outpace growth at a 13.94% CAGR. Superior interfacial shear of 40 MPa allows thinner laminates and 10–15% weight savings.

Basalt rebar, insulation mats, and filtration cloth lead non-composites adoption. Florida DOT validation opened US highway projects, and boiler wraps replace ceramic fiber to meet stricter workplace safety rules. The University of Maine’s ARPA-I bridge program seeks a 30% build-time cut, signaling future code shifts. Composites remain growth pillars, but infrastructure mandates will keep non-composites at the forefront of incremental demand for the basalt fiber market.

By End-Use Industry: Construction Leads, Energy Accelerates

Construction consumed 46.89% volume in 2025, anchored by bridge decks, seawalls, and parking structures that need century-long service lives. Energy applications will climb at a 14.26% CAGR to 2031 as 15 MW turbines and LNG terminals deploy basalt for temperature extremes. Automotive OEMs adopt basalt for battery casings and under-floor shields, cutting 30% weight while meeting crash standards.

Industrial users shift to basalt insulation on boilers and petrochemical piping for fire safety, while sports equipment brands integrate mid-tier basalt-carbon hybrids to reduce cost without performance loss. The energy boom in offshore wind and LNG underpins the fastest growth, solidifying a diverse demand base across the basalt fiber market.

Geography Analysis

Asia-Pacific held 48.75% volume in 2025. China leads through Hengdian’s 20,000 tpa plant and additional tank-kiln lines since 2019. Japan and South Korea apply basalt in coastal retrofits, and India’s USD 1.4 trillion infrastructure push fuels rebar demand. Proximity to ore and lower labor costs keep regional pricing competitive.

The Middle East and Africa, advancing at a 15.52% CAGR to 2031, will benefit from desalination and LNG investments. Saudi Aramco lists basalt FRP in corrosive service guidelines. South African mining upgrades and GCC megaprojects extend the order book, solidifying the region as the basalt fiber market’s fastest-growing cluster.

North America leverages the USD 1.2 trillion Infrastructure Act, with the University of Maine’s ARPA-I work aiming to update AASHTO codes. Canada deploys basalt in Arctic builds, and Mexico integrates it in EV battery enclosures. Europe’s EN 13706 standards and net-zero mandates drive coastal and seismic retrofits. South America gains momentum in Brazil’s hydro dam repairs and Argentina’s grain silos, though import costs temper uptake.

Competitive Landscape

The Basalt Fiber market is moderately consolidated. Kamenny Vek leads global capacity, while Zhejiang Shijin, Jilin Tongxin, and Hengdian Group supply more than half of the Asia-Pacific demand. European players such as Basaltex and Deutsche Basalt Faser expand regional plants to cut freight and offer application engineering. Smaller Middle Eastern entrants, including Arab Basalt Fiber and Sudaglass, aim to lock long-term desalination and LNG supply contracts.

Basalt Fiber Industry Leaders

Kamenny Vek

Technobasalt Invest

Zhejiang Shijin Basalt Fiber Co., Ltd.

Sudaglass Fiber Technology

Mafic SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Rock Fiber Inc. and ReforceTech Ltd. have formed ReforceTech Americas, a joint venture to supply eco-friendly, high-performance fiber-reinforced composites for the construction sector. The initiative aims to reduce steel dependency and carbon emissions, offering MiniBars, a basalt fiber-based product.

- October 2024: Basanite Industries, LLC, has been awarded U.S. Patent No. 12,024,885 B2 by the United States Patent and Trademark Office (USPTO). This patent secures protection for Basanite's innovative BasaFlex basalt fiber composite rebar and its proprietary manufacturing process.

Global Basalt Fiber Market Report Scope

Basalt is an igneous rock, and basalt fiber is produced using a blast furnace by melting volcanic rocks. It has superior abrasion and high-temperature resistance and is extensively used as a structural composite.

The basalt fiber market is segmented by form, usage, end-use industry, and geography. By form, the market is segmented into continuous and discrete, by usage, the market is segmented into composites and non-composites, and by end-use industry, the market is segmented into building and construction, automotive, industrial, marine, energy industry, and other (sports, chemical industry, and petroleum industry). The report offers market size and forecasts for 15 countries across major regions. For each segment, market sizing and forecasts are based on volume (tons) for all the above segments.

| Continuous |

| Discrete |

| Composites |

| Non-Composites |

| Building & Construction |

| Automotive |

| Industrial |

| Marine |

| Energy Industry |

| Other (Sports, Chemical Industry, Petroleum Industry) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Continuous | |

| Discrete | ||

| By Usage | Composites | |

| Non-Composites | ||

| By End-Use Industry | Building & Construction | |

| Automotive | ||

| Industrial | ||

| Marine | ||

| Energy Industry | ||

| Other (Sports, Chemical Industry, Petroleum Industry) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the basalt fiber market by 2031?

The basalt fiber market size is forecast to reach 116.38 kilotons by 2031 at an 11.18% CAGR.

Which end-use sector will record the fastest growth through 2031?

Which end-use sector will record the fastest growth through 2031?

How does basalt fiber compare with E-glass in high-temperature uses?

How does basalt fiber compare with E-glass in high-temperature uses?

Why is Asia-Pacific dominant in basalt fiber production?

The region combines abundant ore deposits, large-scale plants such as Hengdian’s 20,000 tpa line, and proximity to construction and automotive customers.

What regulatory change is accelerating basalt rebar uptake in Europe?

What regulatory change is accelerating basalt rebar uptake in Europe?

Page last updated on: