Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 5.78 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aramid Fiber Market Analysis by Mordor Intelligence

Aramid Fiber Market size in 2026 is estimated at USD 4.52 billion, growing from 2025 value of USD 4.30 billion with 2031 projections showing USD 5.78 billion, growing at 5.04% CAGR over 2026-2031. Increasing penetration in automotive, aerospace, telecom, and advanced personal protective equipment elevates demand, while the fiber’s strength-to-weight ratio and thermal stability anchor long-term relevance. Material‐lightweighting targets in electric mobility, the build-out of 5G networks, and rising investment in hypersonic and space programs continuously widen commercial opportunities. At the same time, feedstock price swings, mainly for MPD and PPD, keep margins under pressure, prompting vertical-integration moves by large producers. Intellectual-property constraints further shape competitive dynamics, cementing the position of incumbents that can finance R&D and navigate cross-licensing frameworks.

Key Report Takeaways

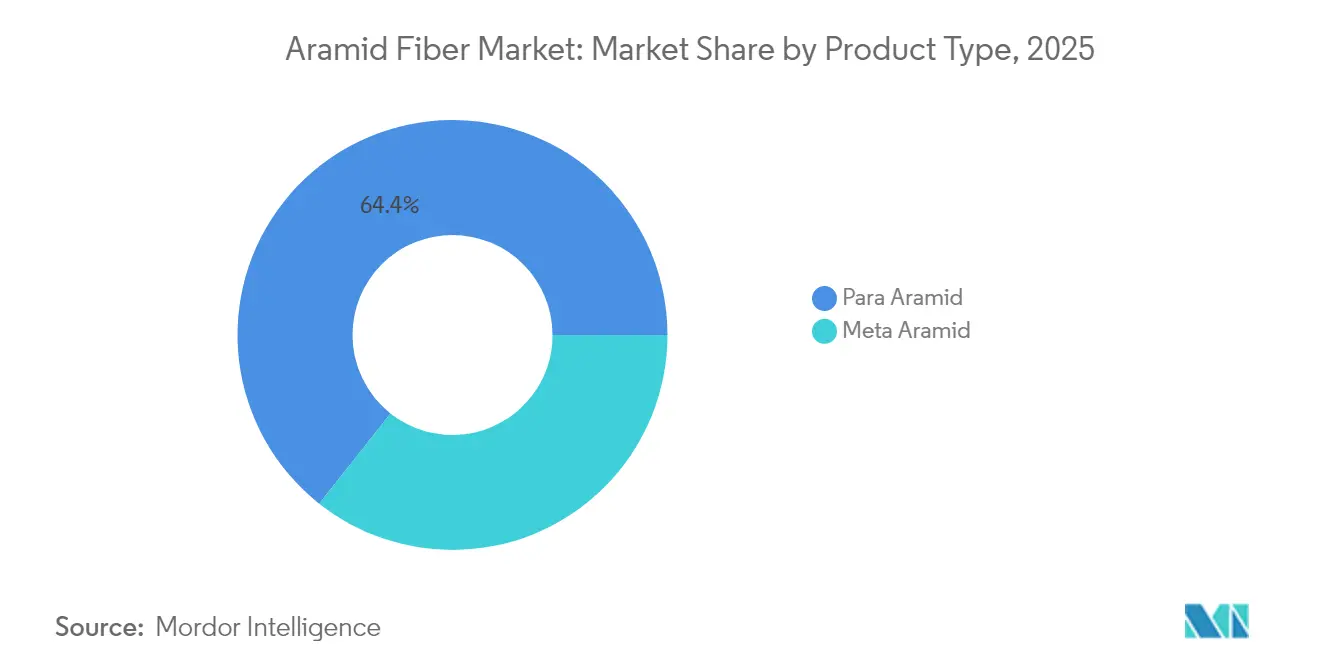

- By product type, para-aramid led with 64.35% of aramid fiber market share in 2025, while meta-aramid is set to expand at a 5.28% CAGR to 2031.

- By spinning process, wet spinning commanded 59.40% of the aramid fiber market size in 2025 and is tracking a 5.71% CAGR through 2031.

- By application, security and protection equipment captured 36.40% revenue share in 2025; optical-fiber cables are forecast to grow at a 5.35% CAGR to 2031.

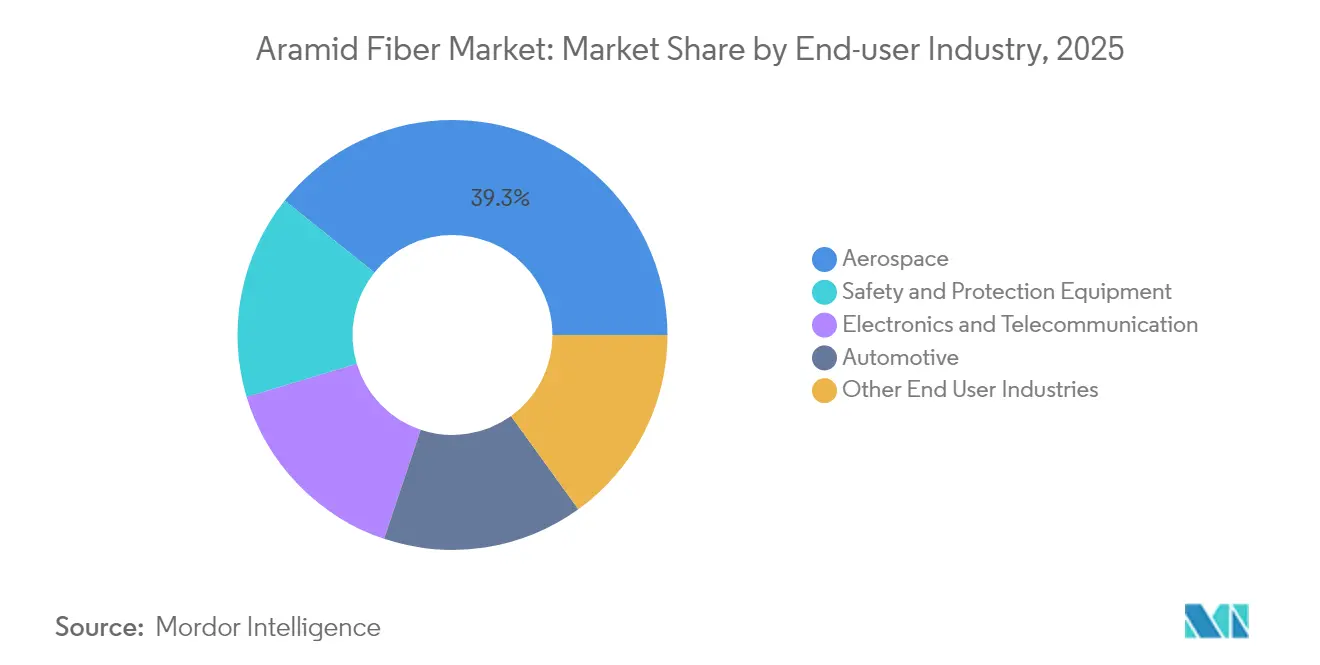

- By end-user industry, aerospace and defense held 39.25% share of the aramid fiber market size in 2025 and is advancing at a 5.86% CAGR through 2031.

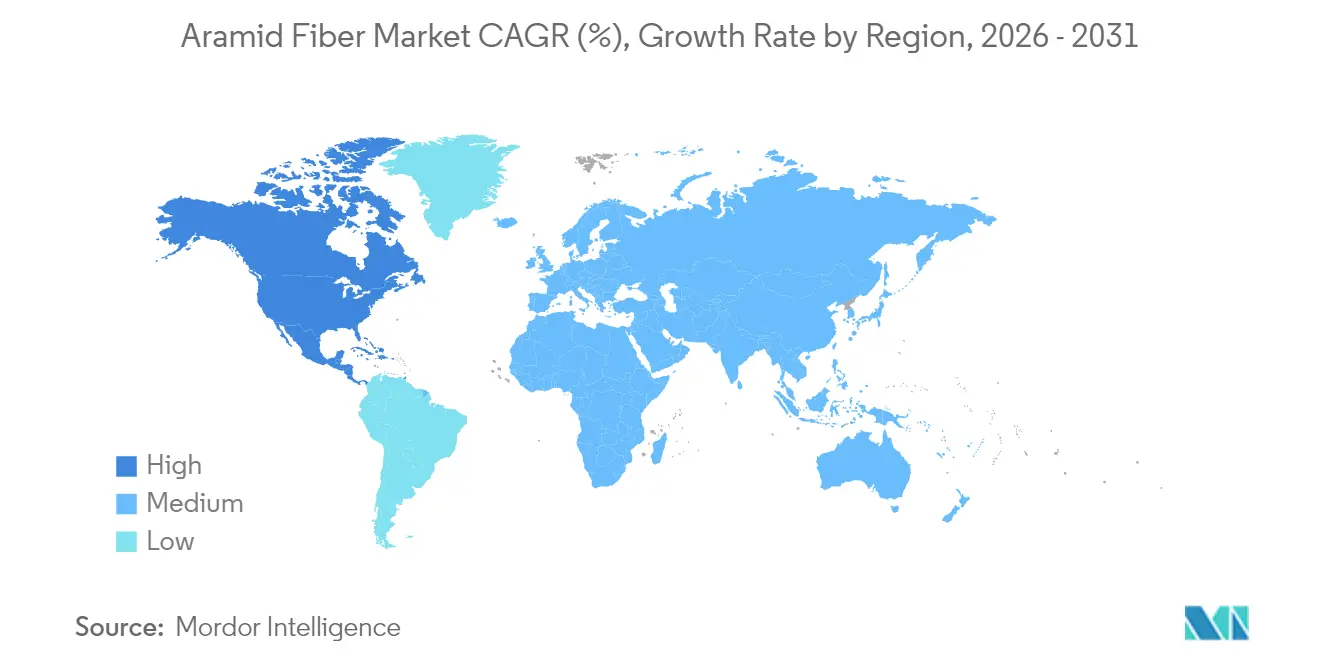

- By geography, Europe accounted for 34.65% share in 2025, whereas North America records the fastest regional CAGR at 5.21% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aramid Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating PPE safety mandates | +1.2% | Asia-Pacific with spillover global | Medium term (2-4 years) |

| EU Green-Deal push for lightweight EV tires | +0.8% | Europe, North America | Long term (≥ 4 years) |

| 5G roll-out surge for optical-fiber cables | +1.1% | Southeast Asia, Global | Short term (≤ 2 years) |

| Increase in defense spending by many countries | +1.0% | North America, Europe, Asia | Medium term (2-4 years) |

| Hypersonic & space defense investments | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating PPE Safety Mandates Across Asian Manufacturing Hubs

Growing enforcement of industrial‐safety rules in China, India, and emerging Southeast Asian economies is lifting orders for aramid-reinforced gloves, helmets, and heat-resistant workwear. Industrial helmets made with aramid composites show 37% higher impact resistance than ABS counterparts, a performance gap that accelerates factory adoption. Cut-resistant gloves incorporating para-aramid deliver Level 5 protection with 30% less weight, improving comfort for continuous wear. Fire-retardant workwear formulated with meta-aramid maintains structural integrity at 425 °C, aligning with stricter foundry and petrochemical safety codes. Manufacturers supplying this region therefore raise allocation for aramid yarns and fabrics, strengthening the growth profile of the aramid fiber market.

EU Green-Deal Push for Lightweight EV Tires Reinforced with Aramid

European automakers accelerate tire redesign programs that shave vehicle mass to extend electric-car range. Aramid-reinforced tire carcasses cut weight by up to 25%, a saving directly linked to the Green Deal’s transport decarbonization targets [1]U.S. Department of Energy, “2024 VTO Annual Merit Review Results Report – Materials Technology,” energy.gov. Every kilogram trimmed offers a 0.7 km range gain, motivating OEMs to substitute polyester or steel cords with aramid. Compounders are commercializing aramid-filled rubber mixes that lower rolling resistance yet keep durability, reinforcing demand for the aramid fiber market in Europe and soon North America.

5G Roll-out Surge Elevating Demand for Aramid-Reinforced Optical-Fiber Cables

Operators racing to deploy 5G macro-cells and dense fiber backbones specify cables with higher tensile and rodent-resistance thresholds. Aramid composite rods supply three times the tensile strength of steel reinforcements at one-fifth the mass, ideal for long pulls in humid terrains [2]Utilities Technology Council, “Underground Fiber Report,” utc.org . Providers such as HFCL confirm rising usage of aramid elements in both underground and aerial designs. Flame-retardant, zero-halogen aramid yarns also protect data-center-to-tower links, bringing an incremental lift to the aramid fiber market.

Hypersonic & Space Defense Investments Raising Meta-Aramid Thermal-Shield Consumption

Defense agencies in the United States, Europe, and China are funding thermal-protection systems that withstand extreme aero-heating. Meta-aramid reinforced EPDM shields exhibit ablation rates as low as 0.015 mm/s, outperforming legacy ablators in solid-rocket motors. Composite studies confirm that aramid survives combined thermal and mechanical loads better than glass or carbon fibers in ultra-high-speed regimes. The specialized nature of hypersonics therefore feeds premium demand segments within the aramid fiber market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MPD & PPD feedstock price volatility | –1.0% | Global, import-dependent regions | Short term (≤ 2 years) |

| Patent cross-licensing barriers | –0.6% | Global, emerging markets | Long term (≥ 4 years) |

| High production costs | –0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MPD & PPD Feedstock Price Volatility

Surging crude-oil swings and regional supply disruptions elevate MPD and PPD cost curves, compressing producer margins and unsettling long-term contracts. The U.S. Department of Commerce lists aromatic diamines among chemically critical inputs subject to geopolitically concentrated production, heightening supply-security risks [3]U.S. Department of Commerce & Homeland Security, “Assessment of the Critical Supply Chains,” bis.doc.gov . Manufacturers counter by exploring bio-based intermediates and closed-loop recovery of aramid scrap, yet near-term volatility still shaves growth momentum within the aramid fiber market.

Patent Cross-Licensing Barriers Deterring New Para-Aramid Entrants

Extensive intellectual-property estates held by DuPont, Teijin, and a handful of peers block fast follower entry. U.S. courts upheld a 20-year ban on a challenger’s Kevlar-like product, illustrating the potency of enforcement tactics. Capital-intensive spinning assets and steep learning curves further discourage aspirants. These hurdles lock market power among incumbents, constraining broader competitive expansion and limiting the aramid fiber market’s addressable producer base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Para-Aramid Dominance and Meta-Aramid Acceleration

The para-aramid segment held a commanding 64.35% aramid fiber market share in 2025, supported by ballistic protection, aerospace, and friction-material demand. Para-aramid yarns deliver tensile strength near 3.8 GPa, sustaining their position in body armor and aviation honeycombs. Defense-budget uplifts in the United States and renewed interest in lightweight automotive composites ensure stable volume pipelines for para-aramid within the aramid fiber market. Significant investments, such as a 3,000-ton capacity addition at Toray’s South Korea site, underscore the scale of capital allocation toward this fiber class.

Meta-aramid, while smaller in base, stages the fastest trajectory at a 5.28% CAGR through 2031. Advanced wet-spun filaments now reach 1,255 MPa tensile strength and retain over 90% strength after prolonged UV exposure, unlocking outdoor applications like transmission-line covers. Embedded in fire-retardant fabrics, insulation papers, and filtration bags, meta-aramid addresses thermal stability demands in electronics, industrial safety, and environmental protection. The aramid fiber market size for meta-aramid is forecast to expand steadily because of expanding semiconductor capacity across Asia and EU green-transition projects, setting a competitive dynamic where material attributes, not only price, decide customer conversion.

By Spinning Process: Wet Spinning Leadership and Dry-Jet Wet Niche Strength

Wet spinning captured 59.40% of aramid fiber market share in 2025 and continues to out-pace the headline market with a 5.71% CAGR. The process offers homogeneous polymer coagulation, producing uniformly dense fibers that achieve high dielectric stability, a prerequisite for electrical papers and filtration media. Upgraded solvent-recycling modules reduce emissions and cost, supporting adoption even among sustainability-minded end-users. The aramid fiber market size for wet-spun output is projected to widen in line with electrification and filter-media demand growth.

Dry-jet wet spinning remains indispensable for para-aramid where chain orientation drives extreme tensile metrics. Lab runs of polyimide analogues display tensile strength up to 2.72 GPa and modulus above 114 GPa, confirming pathway headroom for future para-aramid enhancement. Although overall share is smaller, the process anchors high-end ballistic yarn supply, aligning with the needs of defense ministries and premium sports-equipment brands. Continuous line upgrades aimed at throughput efficiency and solvent-capture technology will safeguard its niche contribution to the aramid fiber market.

By Application: Security & Protection Scale and Optical-Fiber Velocity

Security and protection equipment represented 36.40% of aramid fiber market size in 2025. Military and law-enforcement procurement of next-generation vests, helmets, and vehicle armor underpins baseline tonnage. Fire-brigade turnout gear and industrial PPE add civil demand streams, reinforcing volume stability across economic cycles. Continuous R&D produces lighter, more breathable multilayers, extending comfort and wearer compliance, which stimulates repeat purchases.

Optical-fiber cables, although smaller, post the highest growth at 5.35% CAGR. Aramid yarns and rods in cables handle tensile loading during pull-through and resist water ingress, enabling lower total-cost deployment in rural and subterranean corridors. With regulators mandating broader 5G coverage, telcos budget for extensive backbone reinforcement, accelerating the segment’s contribution to the aramid fiber market. Secondary applications such as friction materials for premium brake pads and aerospace composites maintain specialized but profitable niches aware of the fiber’s superior fatigue resistance and thermal endurance.

By End-User Industry: Aerospace & Defense Premium and Diversified Industrial Uptake

Aerospace and defense captured 39.25% of the aramid fiber market size in 2025, reflecting usage in aircraft panels, honeycomb cores, ballistic armor, and rocket-motor thermal shields. The sector also commands the fastest CAGR at 5.86%, supported by hypersonic weapon prototypes and commercial-space launch cadence. Aramid fiber composites translate to payload savings and extended flight ranges, hard to match with metal or lower-performance polymers.

Safety and protection equipment forms the second pillar, riding on evolving regulatory benchmarks worldwide. Electronics and telecommunications stake a rising claim, with printed-circuit reinforcement and flexible battery insulation opening incremental tonnage. Electric-vehicle platforms lean on aramid in battery pack separators and structural inserts to extend driving range. Industrial filtration, from flue-gas treatment to hot-gas filtration, leverages chemical resistance and dimensional stability. These diverse offtake routes secure demand continuity and buffer the aramid fiber market against single-industry shocks.

Geography Analysis

Europe anchors the global aramid fiber market with 34.65% revenue in 2025. Stringent worker-safety laws, ISO-aligned flame standards, and the European Union’s Green Deal propel high-value adoption in automotive and industrial settings. Germany, with its export-oriented automotive base, leads regional volume expansion, while France and the Netherlands specialize in advanced filtration and aerospace laminates. Government incentives for electric-vehicle battery plants further stimulate polymer-composite uptake.

North America posts the fastest CAGR at 5.21% for 2026-2031. Federal defense appropriations feed continuous demand for para-aramid ballistic materials, whereas NASA and private launch providers channel investments into meta-aramid thermal shields. U.S. telecom carriers renew aerial fiber backbones across hurricane-prone corridors, specifying aramid strength members to mitigate storm damage. Canada follows similar trends with a public-safety focus, particularly in mining and energy infrastructure.

Asia-Pacific represents the next frontier of scale for the aramid fiber market. China escalates domestic output to cut reliance on imports and targets self-sufficiency in para-aramid by mid-decade. Massive construction of smart factories, EV battery plants, and renewable infrastructure multiplies demand for lightweight, heat-resistant materials. Japan and South Korea refine high-tech deployment in semiconductors and 5G hardware, requiring dielectric stability and mechanical resilience that aramid delivers. India’s Make-in-India defense program and updated occupational-safety codes build local PPE and armor consumption, adding depth to regional growth.

Competitive Landscape

The aramid fiber market is consolidated in nature, with DuPont leading North America's para-aramid segment through patents and large-scale manufacturing, while Teijin maintains a global edge with integrated supply chains and balanced portfolios. Entry barriers include expertise in continuous polymerization, solvent-recovery systems, and high-strength spin-drawing technology. Strategic priorities focus on circularity and input diversification. Chinese players are enhancing backward integration and patent portfolios, while investments like Toray's KRW 500 billion Gumi expansion and Sinochem's capacity growth reflect confidence in demand. Future alliances target high-margin niche materials, such as nanoporous aramid aerogels for thermal management and additive manufacturing of powdered aramid composites, which could reshape competitive dynamics without disrupting traditional yarn production.

Aramid Fiber Industry Leaders

TEIJIN LIMITED

DuPont

Yantai Tayho Advanced Materials Co., Ltd.

Kolon Industries, Inc.

HS HYOSUNG ADVANCED MATERIALS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teijin Limited has begun implementing Digital Product Passport (DPP) technology for its aramid and carbon fibers, using Circularise B.V.'s traceability system. This initiative aligns with Europe's ESPR mandate, enhances supply chain transparency, and reinforces Teijin's commitment to sustainability and compliance with evolving regulations.

- May 2024: Toray Industries Inc. plans to invest USD 365 million to expand facilities at the Gumi National Industrial Complex, enabling Toray Advanced Materials Korea to increase dry-spinning aramid fiber production at Gumi Plant 1 to 3,000 tons annually, raising the company’s total production capacity to 5,000 tons.

Global Aramid Fiber Market Report Scope

Aramid fiber is a man-made, high-performance organic fiber that is manufactured from aromatic polyamides. The key characteristics of aramid fiber include high strength, good resistance to heat, abrasion, and organic solvents, non-conductivity, and low flammability. It is mainly used for applications such as composites, ballistics, optical fiber cables, protective clothing against heat and chemicals, and others. The aramid fiber market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into para-aramid and meta-aramid. By end-user industry, the market is segmented into safety and protection equipment, aerospace, automotive, electronics and telecommunications, and other end-user industries. The report also covers the market size and forecasts for the aramid fiber market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Product Type

| Para Aramid |

| Meta Aramid |

By Spinning Process

| Wet Spinning |

| Dry Jet Wet Spinning |

By Application

| Security and Protection Equipment |

| Frictional and Brake Materials |

| Optical Fiber Cables |

| Aerospace Components |

| Automotive Composites |

| Electrical Insulation |

| Others (industrial filtration, rubber and tire reinforcement) |

By End User Industry

| Safety and Protection Equipment |

| Aerospace |

| Automotive |

| Electronics and Telecommunication |

| Other End User Industries |

Geography

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Para Aramid | |

| Meta Aramid | ||

| By Spinning Process | Wet Spinning | |

| Dry Jet Wet Spinning | ||

| By Application | Security and Protection Equipment | |

| Frictional and Brake Materials | ||

| Optical Fiber Cables | ||

| Aerospace Components | ||

| Automotive Composites | ||

| Electrical Insulation | ||

| Others (industrial filtration, rubber and tire reinforcement) | ||

| By End User Industry | Safety and Protection Equipment | |

| Aerospace | ||

| Automotive | ||

| Electronics and Telecommunication | ||

| Other End User Industries | ||

| Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Aramid Fiber Market?

The Aramid Fiber Market stands at USD 4.52 billion in 2026 and is projected to reach USD 5.78 billion by 2031.

Which region is growing fastest in Aramid Fiber Market demand?

North America shows the highest regional growth, advancing at a 5.21% CAGR for 2026-2031, driven by defense and aerospace investment.

Why is wet spinning dominant in aramid fiber production?

Wet spinning accounts for 59.40% of the aramid fiber market share because the process yields fibers with uniform density and excellent thermal resistance, essential for electrical insulation and filtration applications.

What application segment is growing quickest?

Optical-fiber cables are the fastest-growing application, benefiting from 5G infrastructure roll-outs and posting a 5.35% CAGR through 2031.

Page last updated on: