Market Overview

| Study Period | 2021 - 2031 |

|---|---|

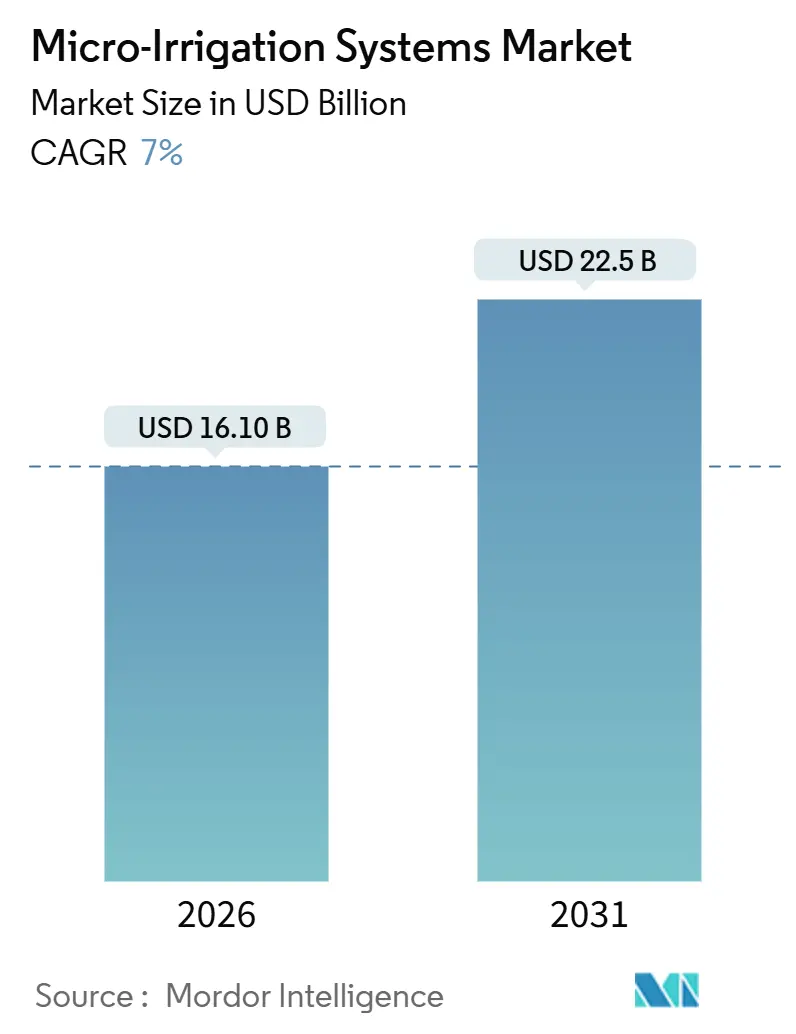

| Market Size (2026) | USD 16.10 Billion |

| Market Size (2031) | USD 22.5 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

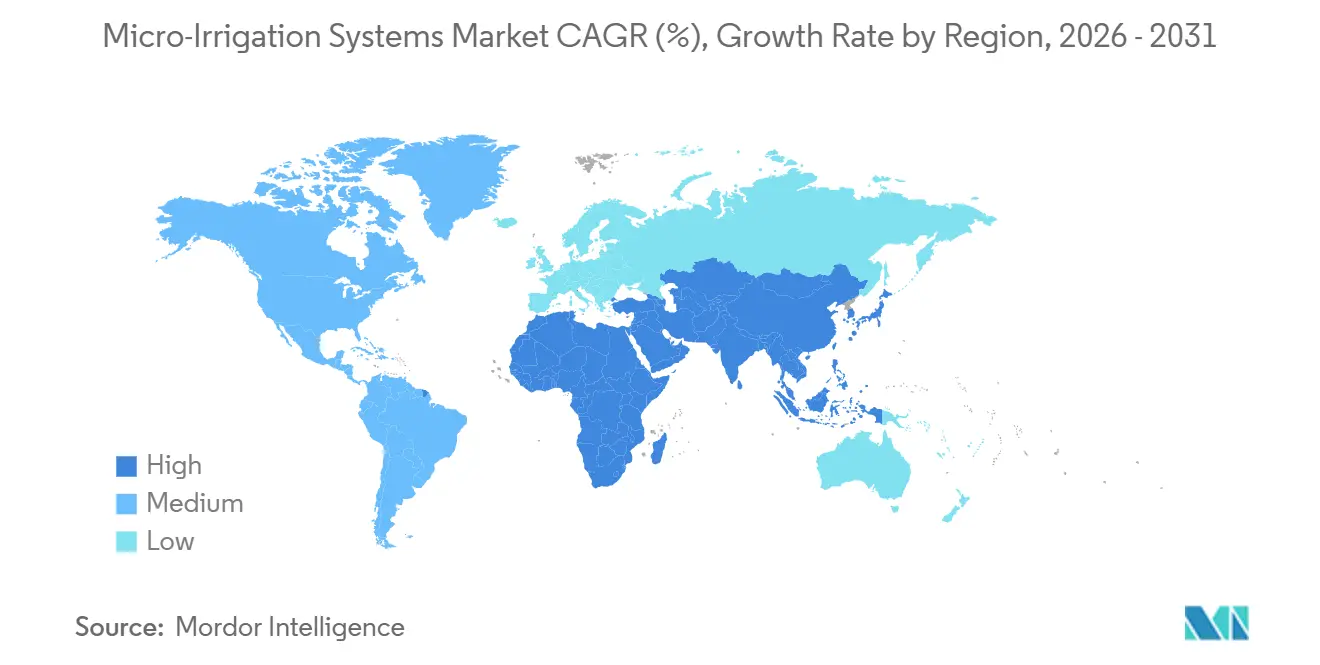

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro-Irrigation Systems Market Analysis by Mordor Intelligence

The micro irrigation systems market size stood at USD 16.1 billion in 2026 and is projected to reach nearly USD 22.5 billion by 2031, registering a 7% CAGR. Adoption is climbing because climate volatility is shrinking freshwater reserves, and growers must squeeze more yield from every cubic meter of water[1]Source: Food and Agriculture Organization, “Water Scarcity,” FAO.org. Precision delivery reduces consumption by 30-50% compared to flood irrigation and often increases output by 20-40%, resulting in higher gross margins when commodity prices are stable. Governments in India, China, and Saudi Arabia now subsidize up to 55% of capital costs, shortening payback periods for smallholders. Subsidies increasingly bundle sensors and controllers, nudging demand toward digital integration. Meanwhile, patent filings for self-flushing and pressure-compensating emitters increased in 2024 and 2025, indicating a shift in the industry from traditional metal and plastic engineering to data-driven reliability.

Key Report Takeaways

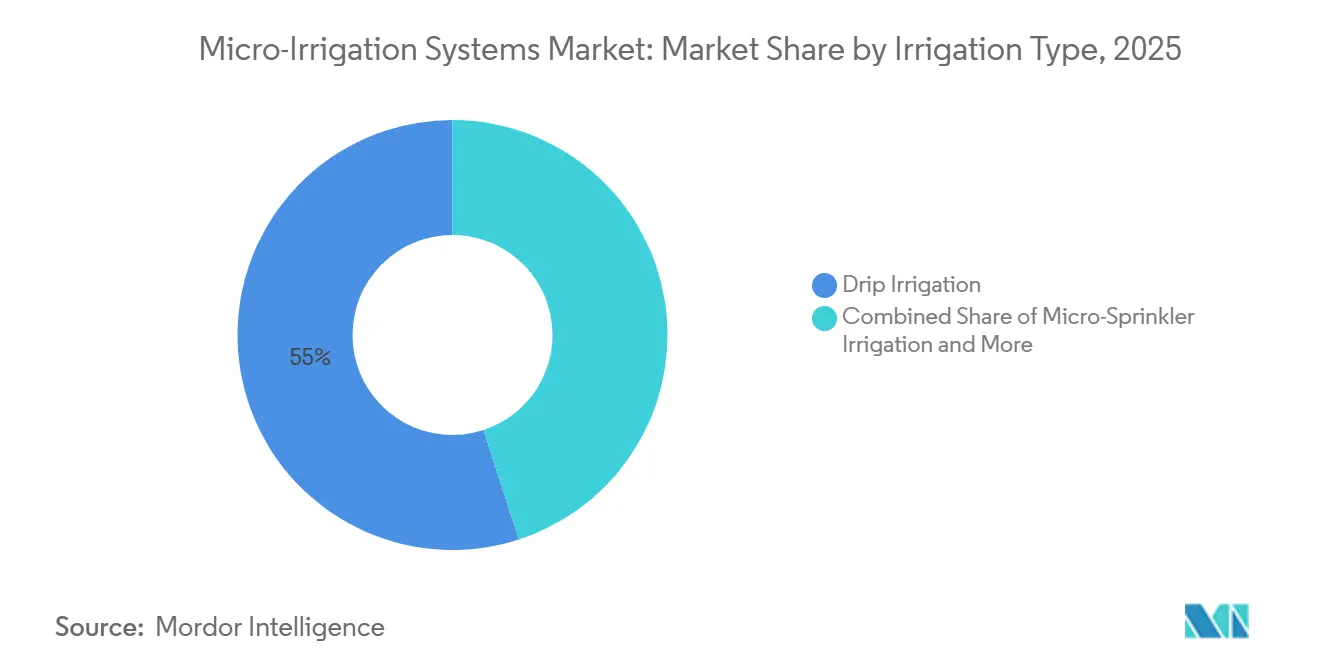

- By irrigation type, drip systems accounted for 55% of the micro irrigation systems market share in 2025, while subsurface drip is forecast to expand at a 9% CAGR through 2031.

- By component, drippers and emitters accounted for 34% of the micro irrigation systems market size in 2025, and controllers and sensors are anticipated to grow at an 11.2% CAGR through 2031.

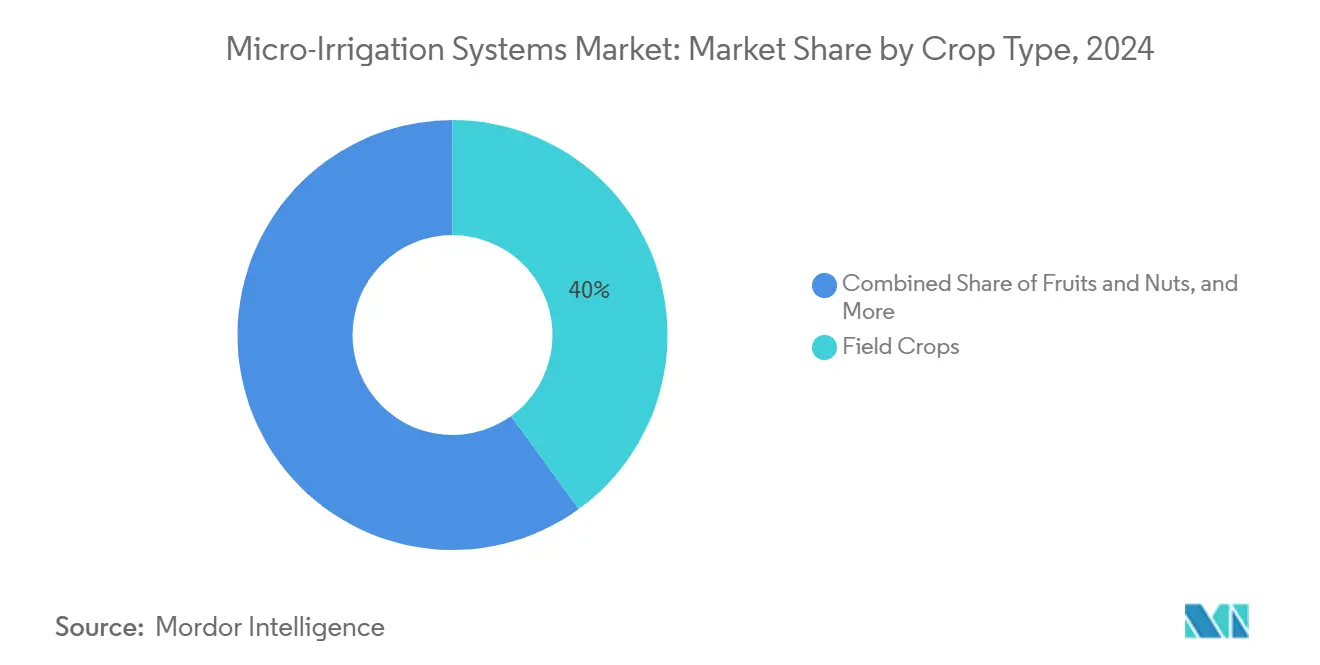

- By crop, field crops captured 40% of the micro irrigation systems market share in 2025, and the vegetable segment is projected to record an 8.4% CAGR through 2031.

- By end user, large commercial farms accounted for 52% of the micro irrigation systems market size in 2025, and greenhouses are projected to grow at the fastest rate, with a 10.5% CAGR from 2026 to 2031.

- By geography, the Asia-Pacific region constituted 45% of the 2025 revenue, while the Middle East is the fastest-growing region, with a 9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro-Irrigation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for water-efficient agriculture | +1.8% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Intensifying water scarcity and drought frequency | +2.1% | Global, peak in Middle East and North Africa | Long term (≥ 4 years) |

| Need to maximize crop yield per drop | +1.5% | Global | Medium term (2-4 years) |

| Rising adoption of precision agriculture and smart farming tools | +1.2% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Solar-powered micro-irrigation packages gaining traction | +0.7% | Africa, South Asia, Middle East | Medium term (2-4 years) |

| Pay-as-you-go micro-irrigation financing models for smallholders | +0.6% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Water-Efficient Agriculture

Public funding is compressing payback periods and expanding adoption among farmers lacking collateral. India’s Pradhan Mantri Krishi Sinchayee Yojana allocated INR 40 billion (USD 480 million) in fiscal 2025 to subsidize up to 55% of the system costs for smallholders, covering an additional 500,000 hectares[2]Source: Government of India, “Per Drop More Crop,” pmksy.gov.in. China disbursed CNY 15 billion (USD 2.1 billion) in grants to drought-prone provinces[3]Source: Ministry of Agriculture and Rural Affairs China, “Water-Saving Irrigation Plan,” moa.gov.cn. Saudi Arabia’s Vision 2030 allocates 50% of its capital expenditure to date palm and vegetable growers. These incentives reduce the effective cost of capital, making investments viable even during periods of commodity price slumps. Requirements now emphasize sensor bundles, which accelerate digital penetration. Subsidy momentum is likely to continue as countries pursue food security goals under tightening water budgets, supporting long-term demand for micro irrigation systems.

Intensifying Water Scarcity and Drought Frequency

Seventeen countries have already withdrawn more than 80% of their renewable freshwater resources, creating structural pressure to switch from gravity flood to pressurized precision delivery. Morocco, following its worst drought in 30 years, now mandates the use of drip irrigation in new orchards and vows to phase out flood irrigation systems by 2028. California’s regulators tightened pumping rights in the Sacramento–San Joaquin Delta in 2025, catalyzing conversions to subsurface drip irrigation in almond and pistachio orchards. Water-productivity gains are decisive, as drip-irrigated vegetables consume 3,000 m³ per hectare, versus 8,000 m³ for flood-irrigated wheat, yet deliver triple the gross margin. This economic arbitrage is reshaping crop choices across arid zones, propelling the micro irrigation systems market through the decade.

Need to Maximize Crop Yield per Drop

Precision water and nutrient delivery reduces plant stress and disease while raising marketable output. Punjab field trials showed that drip-irrigated cotton achieved an 18% higher lint yield and a 35% lower water use than furrow-irrigated plots, thereby boosting water productivity by 28%. Israeli research on tomato processing cut blossom-end rot by 40%, validating the quality premium associated with precise moisture control. Such gains are particularly important in high-value horticulture, where retailers pay for consistency. As climate swings increase mid-season drought risk, precision irrigation acts as yield insurance, reinforcing growers’ willingness to invest. Consequently, agronomic performance continues to elevate the micro irrigation systems market beyond purely water scarcity narratives.

Rising Adoption of Precision Agriculture and Smart Farming Tools

Low-cost sensors, cloud analytics, and cellular IoT connectivity now turn static hardware into live decision-support platforms. Netafim’s NetBeat covers more than 100,000 hectares, automatically adjusting schedules based on real-time soil moisture data. John Deere’s 2024 purchase of European telemetry assets signals that machinery makers will bundle precision water delivery with autonomous tractors. Economic benefits are compelling as a 500-hectare almond ranch cut water use by 12%, nitrogen by 15%, and eliminated 80 hours of monthly valve-adjustment labor in 2025. Policy changes also exist in the European Union's 2023-2027 direct payments, which tie digital farm management adoption. These factors jointly accelerate sensor penetration, fueling both hardware shipments and subscription revenues across the micro irrigation systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation cost for small farmers | -1.4% | Global, peak in South Asia and Sub-Saharan Africa | Short term (≤ 2 years) |

| Emitter clogging and maintenance complexity | -0.9% | Middle East, North Africa, South Asia | Medium term (2-4 years) |

| Shortage of skilled micro-irrigation technicians | -0.5% | Africa, South Asia, South America | Long term (≥ 4 years) |

| End-of-life plastic tubing waste management issues | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Cost for Small Farmers

Turnkey drip systems run USD 1,200–1,800 per hectare, equal to 6–12 months of net farm income for landholdings under 2 hectares in South Asia or East Africa. Even after a 50% subsidy, growers must divert scarce liquidity from essentials such as seed and fertilizer. Land-tenure uncertainty further depresses the willingness to invest because farmers fear losing plots before recouping their capital. Modular kits lower entry thresholds, but they sacrifice hydraulic efficiency and complicate maintenance. In sub-Saharan Africa, agriculture accounts for less than 5% of bank lending, unsecured interest rates exceed 20%, limiting credit uptake. Unless financing innovations spread swiftly, sticker shock will continue to slow penetration in the micro irrigation systems market.

Emitter Clogging and Maintenance Complexity

Sediment, algae, and mineral precipitates obstruct emitter orifices, cutting discharge uniformity and raising downtime. Egyptian cotton fields, where source water exceeded 500 ppm total dissolved solids, averaged 12% emitter clogging per season, resulting in USD 80 per hectare in additional maintenance costs. Filtration helps, but it requires routine backwashing, which smallholders often skip. Chlorination tackles bio-clogging yet introduces safety issues and pump corrosion. Poorly maintained systems underperform, undermining grower confidence and repeat sales. Manufacturers are deploying self-flushing designs and herbicide-impregnated laterals, however, these upgrades cost 15–20% more, which slows adoption in price-sensitive tiers of the micro irrigation systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Subsurface Systems Gain Permanent-Crop Favor

Drip technology accounted for about 55% of the 2025 revenue in the micro irrigation systems market, supported by its versatility across row crops, orchards, and vegetables. Subsurface drip irrigation outpaces all categories at a 9% CAGR through 2031, spurred by permanent-crop growers who value evaporation cuts and reduced equipment traffic. In 2025, a University of California trial reported 22% lower evapotranspiration in subsurface-drip almonds, resulting in a savings of 180 m³ per hectare. Although subsurface installation adds USD 300–500 per hectare, lower upkeep and 15-year lifespans tip the cost-benefit in favor of buried tape. Policy levers amplify the shift as California’s Sustainable Groundwater Management Act ties pumping caps to proven water efficiency. Meanwhile, Israel mandates subsurface systems in new Negev orchards, pairing loans with technical assistance. This steady regulatory drumbeat solidifies subsurface drip as a best-practice standard, expanding its share of the micro irrigation systems market.

Surface micro-sprinklers remain key in citrus, avocado, and frost-prone orchards, but their growth is hindered due to higher evaporation rates. Bubbler irrigation is primarily used in nurseries and public landscapes, yielding modest volumes. Nonetheless, innovation continues as Valmont’s 2024 low-pressure tape operates at just 4–6 psi, appealing to Midwest corn and soybean growers facing energy-price volatility.

By Component: Controllers and Sensors Drive Digital Transition

Controllers and sensors are projected to grow the fastest at an 11.2% CAGR through 2031, reflecting a shift from hardware sales to data services. Drippers and emitters dominate the market, accounting for 34% of revenue, due to their pressure-compensating and anti-siphon designs, which are essential for uniform discharge across slopes. Tubing faces intense price pressure from Chinese extrusion lines, prompting high-end suppliers to shift toward UV-stabilized, premium products. Filters and fertigation systems perform optimally where water quality issues and nutrient regulations intersect, particularly in high-intensity vegetable production areas. Pumps, valves, and accessories complete the system architecture, with energy-efficient upgrades capturing an incremental share.

Digitization economics resonate across farm sizes. A 200-hectare Spanish tomato complex recouped its USD 45,000 sensor retrofit investment in 18 months by reducing water usage by 14%, fertilizer usage by 10%, and labor costs by 87%. As capacitance probes drop below USD 80 and IoT modules under USD 50, cooperative buying circles in India and Africa pool equipment to share data. Vendors now subsidize sensors to lock customers into subscription dashboards, increasing customer lifetime value in the micro irrigation systems industry.

By Crop Type: Vegetables Accelerate Amid Protected-Cultivation Boom

Field crops accounted for 40% of 2025 revenue, led by conversions of cotton, sugarcane, and maize. However, vegetables are estimated to expand at an 8.4% CAGR through 2031 as protected cultivation proliferates in North Africa, the Middle East, and Southeast Asia. Morocco added 15,000 hectares of greenhouses between 2023 and 2025 under Plan Maroc Vert, nearly all of which are equipped with drip irrigation systems for exporting tomatoes. Saudi Arabia’s National Agricultural Development Company commissioned 8,000 hectares of controlled-environment vegetable units using desalinated water. Greenhouse tomatoes yield 400–500 metric tons per hectare, compared to 80–100 metric tons in open fields, thereby boosting the return on investment. Adjacent vertical farms and hydroponic systems create new demand for micro-tubing and fertigation pumps tailored to recirculating loops, widening product scope within the micro irrigation systems market.

Orchards and vineyards show stable mid-single-digit growth through sensor retrofits and subsurface upgrades. Plantation crops, such as oil palm and coffee, exhibit a gradual uptake, constrained by fragmented ownership. Turf and ornamental landscaping experience incremental growth where municipal water restrictions drive drip adoption, particularly in southwest United States and Australia.

By End User: Greenhouses Lead Controlled-Environment Surge

Large commercial farms accounted for 52% of 2025 revenue, benefiting from economies of scale and technical capacity. Smallholders number in the millions but account for a smaller share of the micro irrigation systems market size because per-hectare spending is lower and often subsidy-dependent.

Greenhouses are projected to be the fastest-growing end user, with a 10.5% CAGR through 2031. The Netherlands operates 10,000 hectares of high-tech glasshouses with drip-fertigation yields topping 600 metric tons per hectare in tomatoes, a model now exported to China and the Gulf states. Cannabis legalization in North America catalyzes additional greenhouse builds, each relying on drip to meet the crop’s high water and nutrient needs. Recirculating fertigation, which captures drainage for reuse, bolsters compliance with European nitrate limits, adding value and complexity to system design. Landscape and turf customers utilize drip irrigation to reduce maintenance visits and comply with drought ordinances, particularly on golf courses in the Arabian Peninsula.

Geography Analysis

The Asia-Pacific region contributed 45% of the 2025 revenue and remains the anchor of the micro irrigation systems market. India aims to equip 10 million hectares with micro-irrigation by 2026, supported by federal and state subsidies that cover up to 55% of the costs. China invested CNY 20 billion (USD 2.8 billion) to expand coverage in the Yellow River and Tarim River basins, countering groundwater depletion. Domestic manufacturers, such as Jain Irrigation and Chinadrip, supply cost-competitive components, ensuring local service networks and spare part availability. Japan, South Korea, and Australia post high penetration but smaller absolute volumes due to limited arable land.

The Middle East is projected to post a 9% CAGR through 2031, the fastest worldwide. Saudi Arabia’s Vision 2030 targets domestic vegetable output and offers 50% capital subsidies, while the United Arab Emirates aims for a 50% rise in local food production under its Food Security Strategy 2051. Israel exports subsurface drip know-how to neighbors under regional water-sharing agreements, elevating the innovation baseline. High salinity in desalinated water accelerates emitter wear, but research centers in Riyadh and Tel Aviv are trialing corrosion-resistant polymers.

Europe is expanding at a high growth rate as Spain, Italy, and Greece retrofit vineyards and olive groves to comply with the Common Agricultural Policy's water-efficiency metrics. Germany and France invest in protected horticulture to mitigate labor costs and nitrate runoff. North America is experiencing significant growth, led by California and Arizona, where groundwater regulations are tightening. South America posts a strong growth, fueled by conversions in Brazilian sugarcane and Argentine coffee. Africa’s growth is driven by donor-funded smallholder kits in Kenya, Ethiopia, and Senegal, yet penetration remains low, indicating untapped potential for the micro irrigation systems market.

Regulatory Landscape

Public policy and compliance requirements continue to shape adoption and vendor qualification in the micro-irrigation systems market. In India, the Per Drop More Crop (PDMC) scheme under PMKSY supports large volumes through state-led procurement and subsidy workflows. Installed components are required to conform to Bureau of Indian Standards specifications, which affects product design, labeling, and approved-vendor participation across states.

Regulatory pressure also comes through water quality and environmental oversight. In the United States, California's State Water Resources Control Board administers the Irrigated Lands Regulatory Program (ILRP), which requires commercial irrigated operations to obtain regulatory coverage and implement practices that protect water quality. The US FDA Produce Safety Rule (Subpart E) sets agricultural water microbial criteria and monitoring obligations for covered produce, which can increase demand for filtration, fertigation controls, and traceable, managed irrigation practices. In Africa, Kenya's Irrigation Act (2019) and the February 2026 Guidelines for Promotion, Development and Management of Irrigation formalize licensing, quality assurance, and provider oversight for irrigation schemes, raising the importance of compliant system integrators and documented standards in project execution.

Competitive Landscape

The top five suppliers, Netafim Ltd. (Orbia Advance Corporation), Rivulis Irrigation Ltd. (Temasek Holdings), The Toro Company, Rain Bird Corporation, and Hunter Industries, captured a major share of 2025 revenue, confirming moderate concentration. Israeli firms command premium pricing due to decades of research and development (R&D) focused on pressure-compensating emitters. Indian and Chinese competitors win government tenders on price and customizability. Hardware commoditization is driving all players to integrate digital layers. Netafim offers the NetBeat platform. In 2025, The Toro Company acquired AgriTech Innovations for machine-learning scheduling, and Rivulis bundles remote diagnostics into its T-Net service tier.

White-space battles are unfolding in sub-Saharan Africa and Southeast Asia. Vendors deploy pay-as-you-go financing and mobile money integration to break affordability barriers, extending their reach beyond traditional dealer networks. N-Drip’s gravity-fed system eliminates pumps and filtration, gaining traction in off-grid regions and challenging incumbents designed for pressurized lines.

Regulatory compliance differentiates established brands in Europe and North America, where plastic take-back mandates and ISO-9261 uniformity standards raise entry barriers. In December 2025, Hunter Industries’ ISO 9001 certification in Mexico, for instance, improved its position for EU tenders. Patent intensity is shifting toward digital intelligence, with filings for machine-learning irrigation schedulers and self-cleaning emitters climbing in 2025. This evolving landscape underscores the race to secure recurring software revenue streams inside the micro irrigation systems market.

Micro-Irrigation Systems Industry Leaders

The Toro Company

Netafim Ltd. (Orbia Advance Corporation)

Rivulis Irrigation Ltd. (Temasek Holdings)

Rain Bird Corporation

Hunter Industries

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity is concentrated in government-program execution and the formalization of subsidy delivery, especially in Asia-Pacific. India’s PMKSY remains a central scaling mechanism, with cumulative PDMC coverage reaching 96.97 lakh hectares by March 2025. The government also announced a target to bring an additional 100 lakh hectares under micro-irrigation during 2025-26 to 2029-30. The Micro Irrigation Fund (MIF) at NABARD, with an Rs 10,000 crore corpus, supports state infrastructure beyond base subsidy norms. Cumulative loans sanctioned total Rs 4,853.50 crore, and Rs 4,074.63 crore has been released as of October 31, 2025, which broadens the addressable pipeline for system supply, installation services, and aftersales.

Opportunity also extends into affordability and risk-sharing approaches that reduce upfront barriers for smallholders and emerging-market growers. The June 2026 collaboration between Rivulis, DLL, and the AGRI3 Fund highlights de-risked procurement of drip systems and could support conversion in areas where credit is limited. Demand-side pull is also building from controlled-environment agriculture and water stewardship programs, which increase project-led volumes and raise requirements for digital control, fertigation integration, and documented performance. Netafim's collaboration with Amazon India, announced in February 2026, positions micro-irrigation as part of measurable corporate water-saving programs, supporting deployments that bundle hardware with monitoring and management services.

Recent Industry Developments

- June 2026: The Toro Company launched the RXC residential irrigation controller alongside Oasis irrigation management software, enabling remote management with Wi-Fi modules. The release strengthens Toro's connected-controls stack and supports recurring software-led value capture around irrigation scheduling and monitoring.

- May 2026: Netafim (Orbia Advance Corporation) announced a strategic co-marketing and sales partnership with GrowGeneration Corporation to provide integrated fertigation and irrigation support for controlled-environment agriculture customers. The tie-up expands channel reach into greenhouse and indoor cultivation users where precision irrigation and nutrient delivery are sold as a system solution.

- September 2025: Rivulis opened a new micro-irrigation factory in North America to shorten lead times and support regional demand. The added manufacturing footprint improves service levels for large-scale farm and protected-cultivation projects and reinforces Rivulis's competitive position in a market where delivery reliability and local support influence tender wins.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the global value of micro irrigation systems used to apply low-volume water near the crop root zone, mainly through drip and micro-sprinkler type setups, plus the core hardware required to run these systems in farms and protected cultivation.

Scope exclusions: Large mechanized pivot systems, flood irrigation hardware, and standalone fertigation tanks are excluded from this sizing.

Segmentation Overview

- By Irrigation Type

- Drip Irrigation

- Micro-sprinkler Irrigation

- Subsurface Drip Irrigation

- Bubbler Irrigation

- By Component

- Drippers and Emitters

- Tubing and Drip Lines

- Filters and Fertigation Systems

- Valves and Pressure Regulators

- Controllers and Sensors

- Pumps and Accessories

- By Crop Type

- Field Crops

- Orchard and Vineyards

- Plantation Crops

- Vegetables

- Turf and Ornamental

- By End User

- Smallholder Farms

- Large Commercial Farms

- Greenhouses

- Landscape and Turf

- Others

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the base structure of the model and to keep assumptions linked to measurable farming activity. We referenced public sources such as FAOSTAT for crop and harvested area signals, World Bank and IMF indicators for macro and farm income context, and UN Comtrade for trade direction checks on irrigation-related equipment where the harmonized classifications are usable.

To translate activity into addressable demand, we also reviewed irrigation and agronomy association publications, agriculture ministry program notes on micro irrigation subsidies, peer reviewed water management studies, and a set of company annual reports and investor presentations to understand product mix. In a few instances, paid subscriptions were used for company financial intelligence, patent lookups, and shipment level import and export visibility to test whether adoption trends were consistent with supply signals. These desk sources are not exhaustive, and additional public references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm what is actually being bought and installed, and to test desk assumptions on pricing, replacement cycles, and adoption barriers. We spoke with system manufacturers, component suppliers, distributors, installers, and farm level users across key demand regions, then reconciled differences by use case (open field versus protected cultivation) and crop water needs. Where the desk record was thin, these discussions helped tighten penetration rates and a more realistic ASP movement by region and component type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 22% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 22% | Managers: 41% | Americas: 23% |

Market-Sizing & Forecasting

The core sizing starts from a top-down demand pool view where irrigated area, crop mix, and water scarcity pressure are used to reconstruct likely micro irrigation adoption by region, then translated into system demand through penetration and replacement assumptions. After that is built, we corroborated the totals with selective bottom-up approximations, mainly using sampled price points for key components, distributor channel checks, and a limited roll up of supplier revenues where product exposure is clear.

A few variables mattered most for keeping the model realistic, such as irrigated and harvested area trends by major crops, the share of protected cultivation, subsidy coverage and timing, typical system life and replacement frequency, and observed shifts in component pricing (filters, valves, tubing, controllers) by region. For forecasting, we used scenario analysis supported by expert views, where the main scenarios flex adoption speed, subsidy continuity, and drought intensity, then apply sensible price progression rather than a single flat ASP assumption. When bottom-up visibility was incomplete for smaller, unlisted participants, gaps were handled by applying region-specific channel multipliers, then checking that implied per-hectare spend stayed within primary-validated ranges.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, including area under irrigation indicators, trade movement where relevant, and the implied equipment spend per hectare for the crops that drive the most micro irrigation use. Variances were investigated through anomaly checks, followed by a second analyst review that re-runs the model with altered inputs to see which assumptions are most sensitive.

The report is refreshed annually, and interim updates are triggered when there are material events such as major subsidy rule changes, abnormal drought seasons, or sharp currency and input cost shifts that affect pricing. Before delivery, a fresh pass is completed so the final numbers reflect the latest available signals and any re-contacts needed to clear open questions.

Mordor Intelligence's Global Micro Irrigation Systems Market Market Sizing Compared With Other Published Estimates

Published market sizes for micro irrigation systems can look far apart because each study draws the line in a different place on what counts as the market and how pricing is applied. Differences usually show up around included hardware, whether installation or service value is counted, and the year and exchange rate choices used to convert local prices into USD.

By tracking component-level scope boundaries and refreshing currency timing and price checks through interviews, Mordor Intelligence keeps the estimate focused on micro irrigation system hardware used in open-field and protected cultivation, instead of blending in broader irrigation equipment or adjacent farm infrastructure. Another common gap comes from how adoption is modeled, since some estimates project aggressive penetration jumps without anchoring them to subsidy budgets, irrigated area growth, and practical replacement cycles that buyers described.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.10 B (2026) | |

| Industry Publisher A | USD 15.25 B (2025) | Uses a different base year and a longer horizon, and the scope detail is less explicit on what system components are included or excluded, which can shift the counted value and growth rate. |

| Global Consultancy B | USD 13.50 B (2025) | Starts from a lower 2025 base and may apply a broader application view without clearly separating system hardware from adjacent irrigation categories, which can compress or expand the total depending on what gets bundled. |

The spread across the three values is mainly explained by base-year choice, boundary setting around included equipment, and how adoption and pricing are stepped forward year to year. When the scope is kept tight to micro irrigation hardware and the key drivers are checked against area, subsidy, and replacement signals, the final market total becomes easier to trace and repeat.

Key Questions Answered in the Report

What is the anticipated value of the micro irrigation systems market in 2031?

It is forecast to approach USD 22.5 billion by 2031, growing at a 7% CAGR from 2026 levels.

Which region will expand fastest through 2031?

The Middle East will post the highest regional CAGR at 9% as Gulf nations pair desalination with precision farming.

Why are controllers and sensors the fastest-growing component?

Prices of soil-moisture probes and IoT modules have fallen sharply, and growers seek data-driven scheduling that reduces labor and input costs.

How do subsidies influence adoption?

Programs in India, China, and Saudi Arabia cover up to 55% of system costs, shortening payback periods and making drip viable for smallholders.

What is the main technical barrier for small farmers?

High upfront capital of USD 1,200–1,800 per hectare and limited access to affordable credit delay investment among holdings under 2 hectares.

How is plastic waste from drip lines being addressed?

European regulations push manufacturers toward take-back schemes, and pilots like Netafim’s Spain program recycle used lines into non-food products.

Page last updated on: