Fc Fusion Protein Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

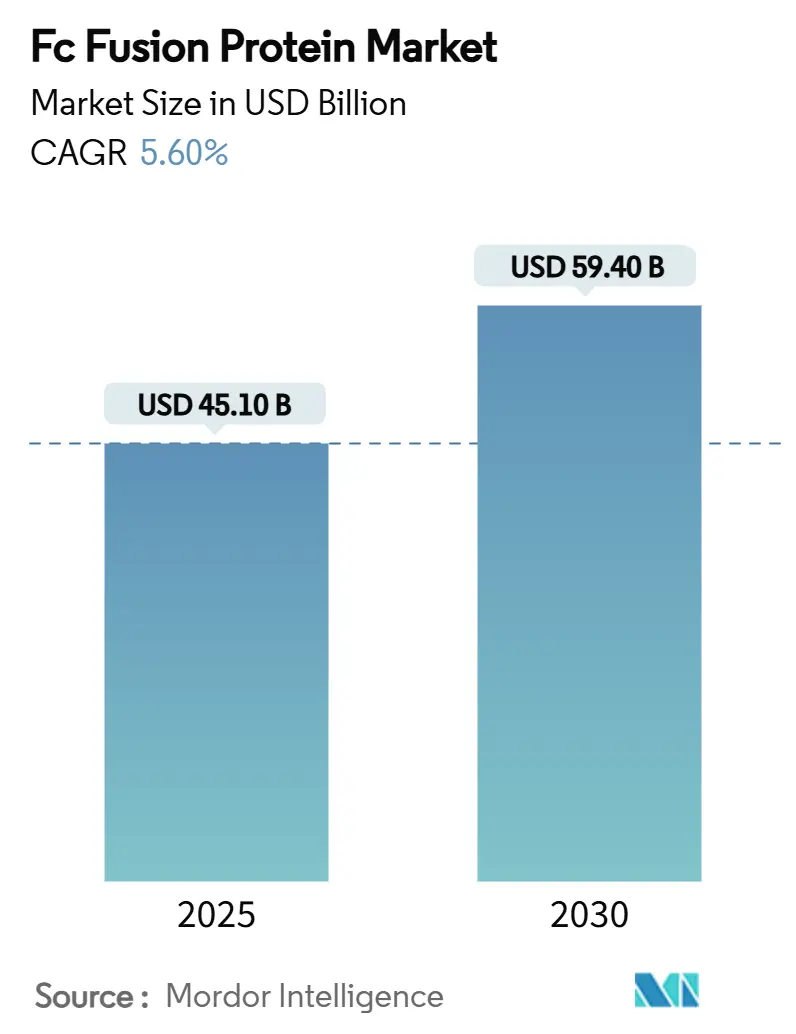

| Market Size (2025) | USD 45.10 Billion |

| Market Size (2030) | USD 59.40 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

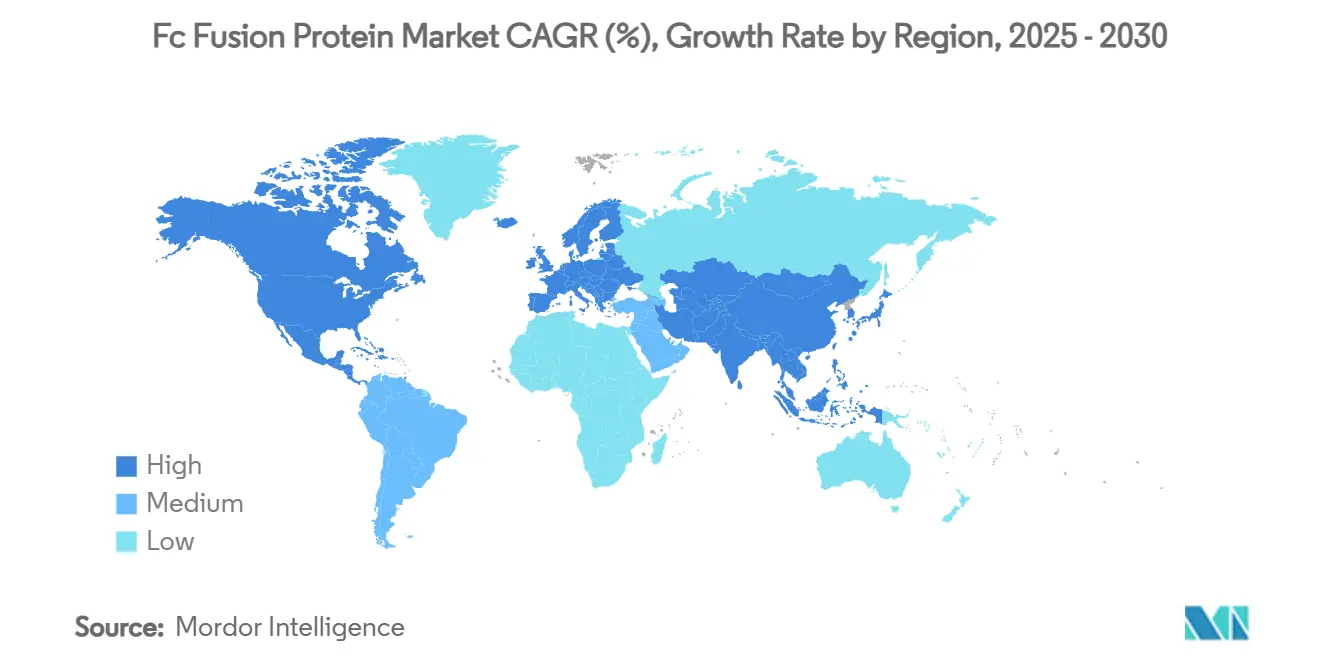

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fc Fusion Protein Market Analysis by Mordor Intelligence

The Fc fusion proteins market size stands at USD 45.1 billion in 2025 and is forecast to reach USD 59.4 billion in 2030, advancing at a 5.6% CAGR. Demand momentum stems from the proven ability of the Fc domain to extend half-life, the rapid uptake of ophthalmology products, and continuous-manufacture cost efficiencies. The pathway from laboratory design to commercial supply has shortened as artificial-intelligence platforms help engineers screen thousands of FcRn mutants in weeks, accelerating lead selection and reducing attrition. Patient preference for at-home therapies sustains the subcutaneous segment, while intravitreal injections gain ground because extended dosing intervals lessen clinic visits. Geographically, North American payers still absorb premium biologic prices, but Asian governments are scaling reimbursement and local production to narrow the affordability gap.

Key Report Takeaways

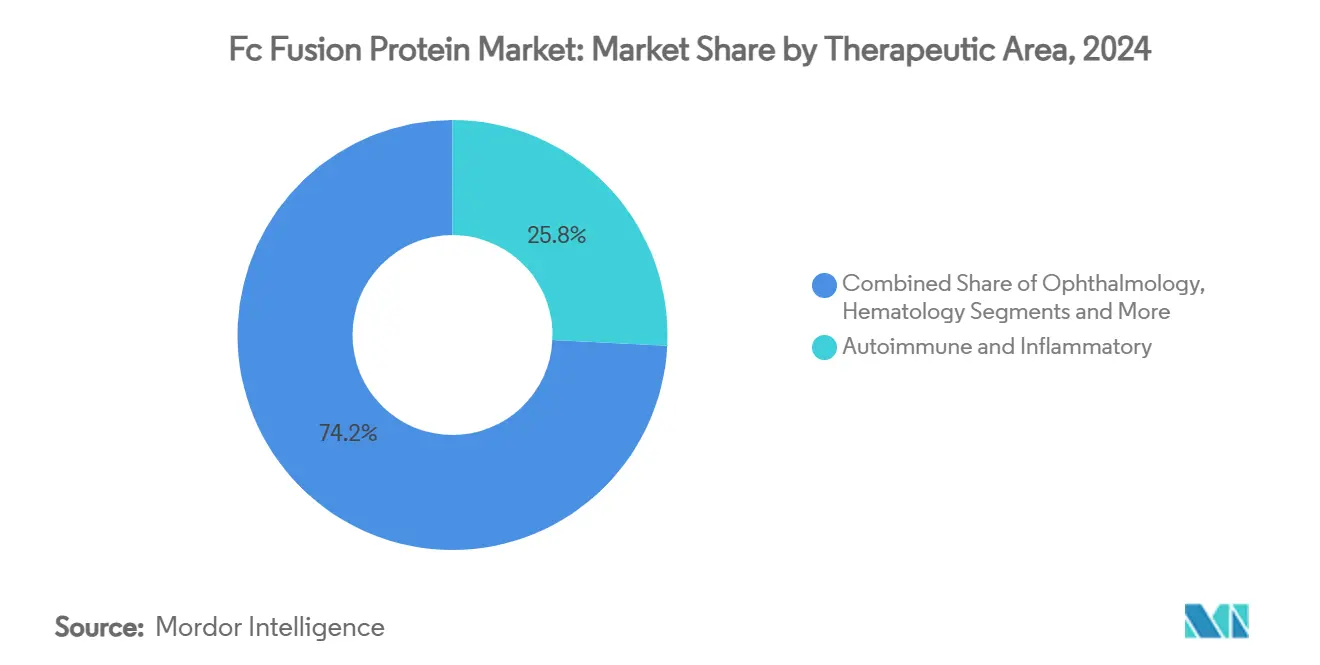

- By therapeutic area, autoimmune and inflammatory disorders held 25.8% of the Fc fusion proteins market share in 2024, whereas ophthalmology is projected to expand at a 6.9% CAGR through 2030.

- By route of administration, subcutaneous delivery accounted for 24.1% of the Fc fusion proteins market size in 2024 and intravitreal delivery is advancing at a 6.9% CAGR through 2030.

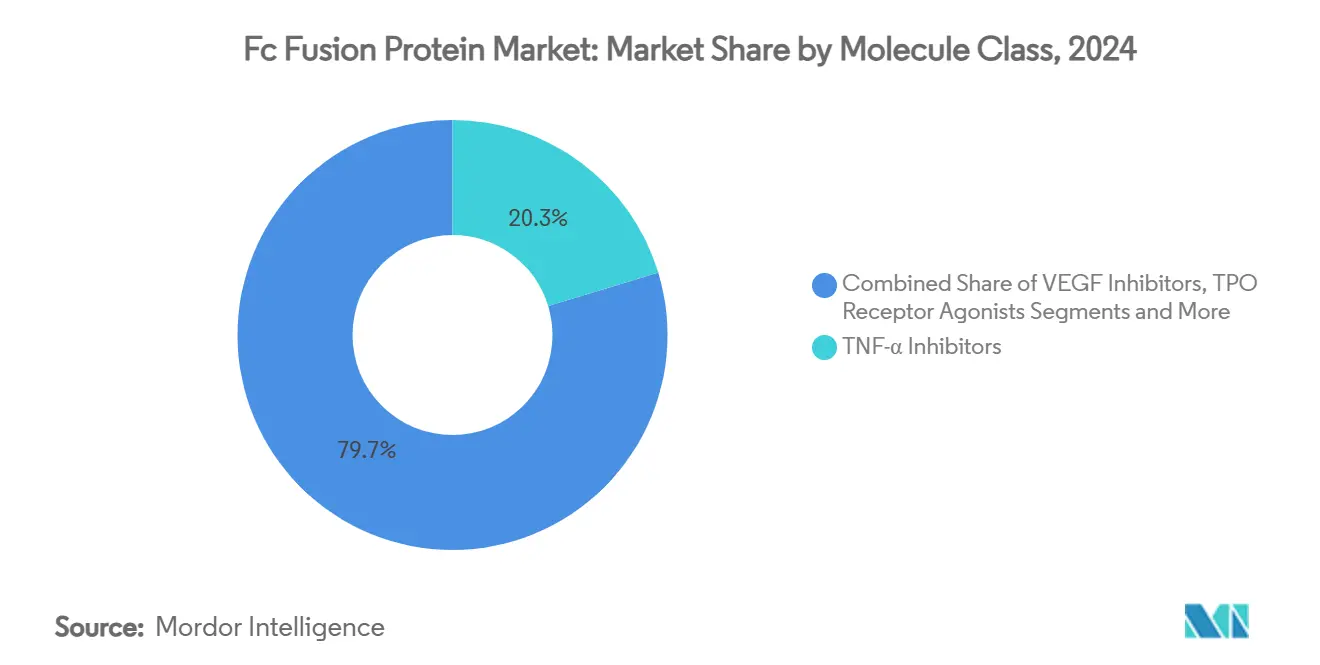

- By molecule class, TNF-α inhibitors commanded 20.3% of the Fc fusion proteins market size in 2024 while VEGF inhibitors record the highest forecast CAGR at 7.4% to 2030.

- By geography, North America led with 40.7% revenue share in 2024 and Asia Pacific is set to rise at an 8.2% CAGR over the same period.

Global Fc Fusion Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of autoimmune & inflammatory disorders | +0.80% | North America, Europe | Long term (≥ 4 years) |

| Rapid uptake of anti-VEGF Fc fusions in ophthalmology | +0.70% | Global, led by developed markets | Medium term (2-4 years) |

| Rising demand for long-acting biologics in chronic care | +0.60% | Global, faster in emerging economies | Long term (≥ 4 years) |

| Breakthroughs in FcRn engineering for weekly dosing | +0.50% | Developed markets | Medium term (2-4 years) |

| Expanding reimbursement for biologics in emerging regions | +0.40% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Continuous-manufacture platforms lowering COGS | +0.40% | Manufacturing hubs worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Autoimmune & Inflammatory Disorders

Rheumatoid arthritis, inflammatory bowel disease, and psoriasis together affect tens of millions of patients worldwide, generating consistent demand for high-potency biologics that can halt disease progression instead of masking symptoms.[1]Daniel M. Czajkowsky, “Fc-Fusion Proteins: New Developments and Future Perspectives,” EMBO Molecular Medicine, europepmc.org The chronic nature of these conditions necessitates lifelong therapy, which stabilizes prescription volumes even when new competitors emerge. Aging populations in Europe and North America further enlarge the patient pool because immunosenescence raises susceptibility to autoimmunity. Commercially, the Fc fusion proteins market benefits from payers’ willingness to fund drugs that reduce hospitalizations and surgery rates over the long term. Pipeline activity supports sustained growth, with multi-specific constructs targeting TNF-α plus IL-17 entering mid-stage trials to tackle refractory patient subsets.

Rapid Uptake of Anti-VEGF Fc Fusions in Ophthalmology

Ophthalmology has become the fastest-moving revenue engine as new Fc fusion products combine dual-target mechanisms with extended injection intervals that lower clinic burden. Sales of faricimab (Vabysmo) surged 108% year-on-year to USD 933 million in Q1 2024 as retina specialists shifted away from monthly injections toward eight-week regimens.[2]Jan Terje Andersen, “Generation of Multivalent Nanobody-Based Proteins with Improved Neutralization,” Bioconjugate Chemistry, doi.org Diabetic macular edema and neovascular age-related macular degeneration are rising in prevalence because of aging and lifestyle changes, magnifying the addressable population. Ophthalmic societies increasingly endorse treat-and-extend protocols, cementing market momentum for agents that can demonstrate comparable vision gains with fewer injections.

Rising Demand for Long-Acting Biologics in Chronic Therapy

Healthcare systems are prioritizing treatments that require infrequent dosing to improve adherence and free clinical capacity. FcRn engineering amplifies IgG recycling, enabling weekly or bi-weekly administration instead of daily shots, which patients perceive as a significant quality-of-life improvement. Economic analyses show that reduced nursing time, lower consumable use, and fewer clinic visits offset higher unit prices, making such regimens attractive for payers as well. The regulatory environment acknowledges these benefits, speeding reviews for half-life–extended molecules that can produce real-world savings.

Breakthroughs in FcRn-Engineering for Weekly/Bi-Weekly Dosing

Protein-design algorithms now evaluate electrostatic surface patches and glycosylation motifs simultaneously, identifying Fc variants with eight-fold higher neonatal Fc receptor affinity without compromising stability. As a result, next-generation fusion constructs achieve trough levels above therapeutic thresholds with fewer administrations.[3]Hemant Rahalkar, “Challenges Faced by the Biopharmaceutical Industry in the Development and Marketing Authorization of Biosimilar Medicines in BRICS-TM Countries,” Pharmaceutical Medicine, springer.com Clinical-stage programs report adherence gains of 15-20 percentage points versus historical cohorts, which translates into better control of disease biomarkers and fewer flares in autoimmune conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost & payer pressure on biologics | -0.40% | Global, more intense in cost-driven systems | Short term (≤ 2 years) |

| Patent cliffs triggering biosimilar erosion | -0.30% | Developed markets | Short term (≤ 2 years) |

| Glycosylation-uniformity challenges in large-scale production | -0.20% | Manufacturing hubs | Medium term (2-4 years) |

| Ocular safety concerns spurring tighter intravitreal rules | -0.20% | Regulatory-stringent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost & Payer Pressure on Biologics

Cost-effectiveness agencies are demanding head-to-head trials and real-world evidence proving superiority over established biosimilars before accepting premium prices. Centralized tenders in Europe and hospital group purchasing in the United States supply strong leverage, forcing manufacturers to adopt outcomes-based contracts that link payment to avoided hospital days or surgical procedures. Administrative complexity and delayed revenue recognition dampen near-term cash flow, discouraging smaller firms from aggressive launch strategies.

Patent Cliffs Triggering Biosimilar Erosion

Etanercept and ustekinumab biosimilars are launching at 30–40% lower list prices across OECD markets, capturing share within 12 months and eroding originator volumes by double digits. Innovators respond with formulation upgrades or new indications, but pricing headwinds remain unavoidable. The scenario underscores the importance of robust pipeline diversification beyond single-target fusions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Area: Autoimmune Dominance and Ophthalmology Surge

Autoimmune and inflammatory disorders delivered 25.8% of the Fc fusion proteins market share in 2024 as decades of clinical practice cemented TNF-α inhibition as standard of care for rheumatoid arthritis, psoriasis, and inflammatory bowel disease. Prescriber familiarity, broad label coverage, and well-established safety monitoring drive repeat prescriptions that anchor overall demand. Ophthalmology, while still smaller in absolute revenue, is set to grow at a 6.9% CAGR, the highest among all therapy areas, because extended-interval anti-VEGF fusions reduce clinic congestion and improve adherence in elderly populations.

Metabolic and endocrine applications remain a niche within the Fc fusion proteins market but serve critical gaps in rare hereditary disorders where enzyme replacement has fallen short. Hematology relies on thrombopoietin receptor agonists that stabilize platelet counts in chronic immune thrombocytopenia, supporting steady albeit moderate expansion. Oncology supportive care and orphan indications sit in the “Others” bracket, providing optionality for pipeline diversification with multi-specific fusions that can ferry cytotoxic payloads directly to tumors.

By Route of Administration: Subcutaneous Convenience Meets Intravitreal Precision

Subcutaneous delivery held 24.1% of the Fc fusion proteins market size in 2024, as at-home self-injection models align with patient lifestyle preferences. Weekly auto-injector formats lower healthcare utilization and facilitate long-term adherence for chronic autoimmune conditions. Pay-per-outcome contracts often require adherence metrics, reinforcing the appeal of user-friendly pens that digitally record dose timing.

Intravitreal injections, although clinically demanding, are advancing at a 6.9% CAGR because retina specialists value the elevated ocular drug concentrations achievable with localized administration. Proprietary syringe designs that minimize injection force and micro-needle innovation are improving patient comfort, while treat-and-extend regimens curtail visit frequency. Intravenous infusions remain indispensable for acute flares and hospital-based therapies, whereas intrathecal and intra-articular experimentation broadens future delivery possibilities, keeping the administration landscape dynamic.

By Molecule Class: TNF-α Maturity Versus VEGF Innovation

TNF-α inhibitors maintained a 20.3% revenue share in 2024 and continue to serve as the anchor franchise for several large biopharma portfolios. Real-world data enable confident switching between reference and biosimilar products, preserving patient outcomes even in cost-containment environments. Biosimilar uptake, however, compresses margins for incumbent brands, necessitating formulation enhancements or label expansions.

VEGF inhibitors will grow fastest at 7.4% through 2030 as next-generation antibodies integrate dual inhibition of VEGF-A and Ang-2 to tackle resistance mechanisms in diabetic retinopathy. TPO receptor agonists fill a hematologic sub-segment that benefits from orphan drug incentives, whereas CTLA-4 fusions offer immune modulation for cytokine storm conditions emerging in severe viral infections. Exploratory multi-specific constructs incorporating checkpoint inhibition or cytokine neutralization foretell a wave of therapeutic complexity that should drive future differentiation in the Fc fusion proteins market.

Geography Analysis

North America captured 40.7% of global revenue in 2024 supported by commercial insurance that absorbs premium list prices and by specialty pharmacies that streamline reimbursement processing. United States hospital systems negotiate volume rebates yet continue to favor novel mechanisms that lower readmission risk, sustaining originator uptake even under biosimilar pressure. Canada tracks more closely to European health technology assessments, but rare-disease frameworks still authorize high-cost fusion therapies for small patient populations.

Asia Pacific represents the most vibrant expansion corridor with an 8.2% CAGR forecast as rising middle-class populations demand cutting-edge biologics and local manufacturers master Fc engineering. China’s reimbursement negotiations have broadened access beyond coastal megacities, and provincial authorities are investing in cold-chain logistics. Japan’s regulatory fast track for breakthrough therapies is shortening time-to-market for domestic innovators, while South Korea leverages contract manufacturing expertise to supply regional demand.

Europe, positioned between mature North America and fast-growing Asia Pacific, prizes real-world performance over list-price innovation. Health services increasingly conduct national tenders that favor suppliers willing to propose volume-based discounts or shared-savings models. Germany and the United Kingdom sustain premium uptake owing to clinician autonomy and robust pharmacovigilance infrastructure, whereas Southern European markets opt for aggressive biosimilar substitution to stabilize budgets. Emerging markets in Latin America and the Middle East follow hybrid strategies, pairing reference products in tertiary hospitals with lower-cost biosimilars in public clinics.

Competitive Landscape

Competition in the Fc fusion proteins market is moderate, with a top tier of global firms—Amgen, Pfizer, Roche, AbbVie, and Regeneron—controlling flagship assets and integrated manufacturing networks. Patent cliffs are drawing Samsung Bioepis, Sandoz, and Celltrion into the arena with biosimilar offerings that underprice reference drugs by 30–40%, rebalancing bargaining power in payer negotiations. In response, originators are refreshing portfolios through acquisitions such as Merck’s USD 1.3 billion purchase of bispecific antibody CN201, which boosts its late-stage immunology pipeline.

Vertical integration is expanding as companies acquire contract development and manufacturing organizations (CDMOs) to secure capacity for complex fusion proteins. Avid Bioservices’ USD 1.1 billion sale to private-equity buyers underscores investor belief in steady biologic production revenues. Continuous-manufacture retrofits across legacy plants are expected to shave per-gram costs, enabling more competitive biosimilar positioning without sacrificing margin.

Technological alliances are proliferating; Generate Biomedicines partnered with Novartis in a USD 1 billion deal to apply generative-AI design to Fc scaffolds, aiming to compress the discovery timeline from years to months. Lonza and Roche have allocated USD 1.2 billion to expand large-scale bioreactor fleets, validating sustained demand outlooks. Market participants that combine proprietary science with manufacturing economics are best placed to maintain leadership in an environment where payer scrutiny and biosimilar entry intensify.

Fc Fusion Protein Industry Leaders

Amgen (Immunex legacy)

Regeneron + Bayer

Bristol-Myers Squibb

Pfizer Inc.

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Merck closed the USD 1.3 billion acquisition of bispecific antibody CN201, adding a late-stage asset for B-cell disorders.

- November 2024: Avid Bioservices agreed to a USD 1.1 billion takeover by GHO Capital Partners and Ampersand Capital Partners to fund CGMP capacity expansion.

- July 2024: Generate Biomedicines secured over USD 1 billion in AI-driven protein-design collaborations with Novartis.

Global Fc Fusion Protein Market Report Scope

| Autoimmune & Inflammatory |

| Ophthalmology |

| Hematology |

| Metabolic & Endocrine |

| Others |

| Subcutaneous |

| Intravitreal |

| Intravenous |

| Others |

| TNF-? Inhibitors |

| VEGF Inhibitors |

| TPO Receptor Agonists |

| CTLA-4 & Co-Stimulation Modulators |

| Next-Gen / Multi-Specific Fusions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Area | Autoimmune & Inflammatory | |

| Ophthalmology | ||

| Hematology | ||

| Metabolic & Endocrine | ||

| Others | ||

| By Route of Administration | Subcutaneous | |

| Intravitreal | ||

| Intravenous | ||

| Others | ||

| By Molecule Class | TNF-? Inhibitors | |

| VEGF Inhibitors | ||

| TPO Receptor Agonists | ||

| CTLA-4 & Co-Stimulation Modulators | ||

| Next-Gen / Multi-Specific Fusions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Fc fusion proteins market in 2025?

The Fc fusion proteins market size is USD 45.1 billion in 2025 with a projected 5.6% CAGR to 2030.

Which therapeutic segment is expanding fastest?

Ophthalmology products are growing at a 6.9% CAGR because extended-interval anti-VEGF fusions lower clinic visits and improve adherence.

Why do payers support longer-acting Fc fusion drugs?

Weekly or bi-weekly dosing cuts nursing time and reduces overall care costs, making such regimens attractive under value-based contracts.

Which region offers the highest growth potential?

Asia Pacific leads with an 8.2% CAGR as reimbursement expansion and local manufacturing boost patient access to advanced biologics.

How are manufacturers tackling biosimilar competition?

Originators pursue pipeline diversification, lifecycle-management upgrades, and continuous-manufacture cost reductions to defend share and margins.

What drives investment in Fc fusion manufacturing capacity?

Rising demand, complex production requirements, and the need for cost-efficient continuous processes spur acquisitions and facility upgrades worldwide.

Page last updated on: