Extended Reality (XR) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

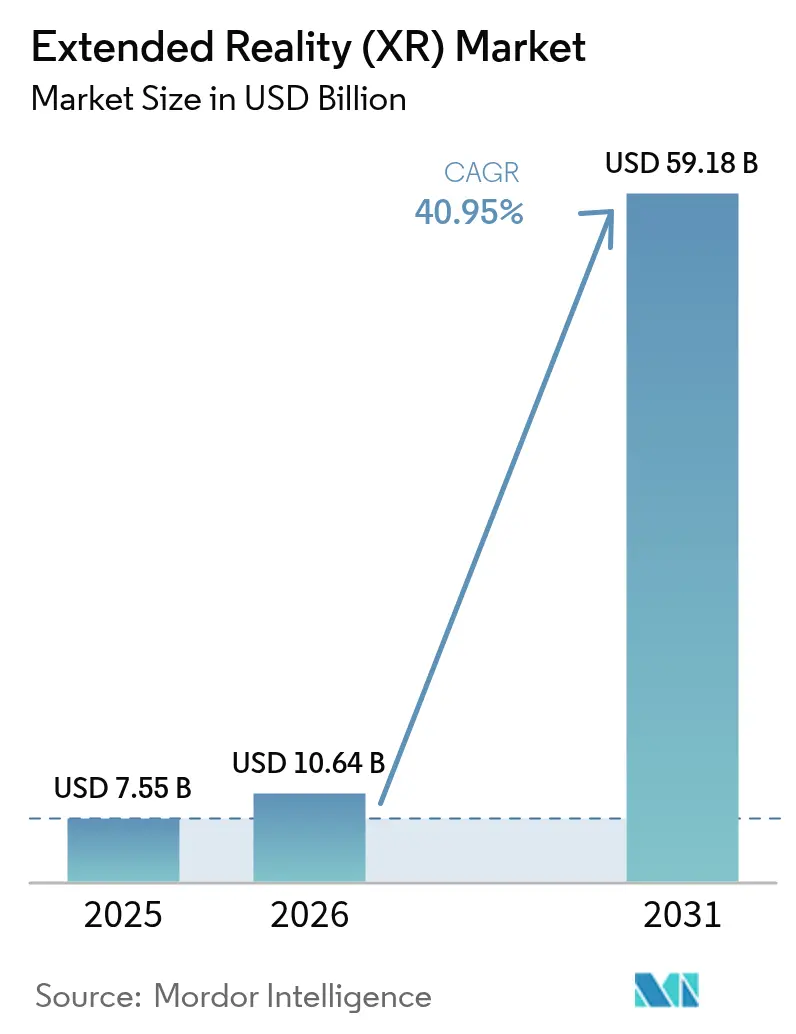

| Market Size (2026) | USD 10.64 Billion |

| Market Size (2031) | USD 59.18 Billion |

| Growth Rate (2026 - 2031) | 40.95% CAGR |

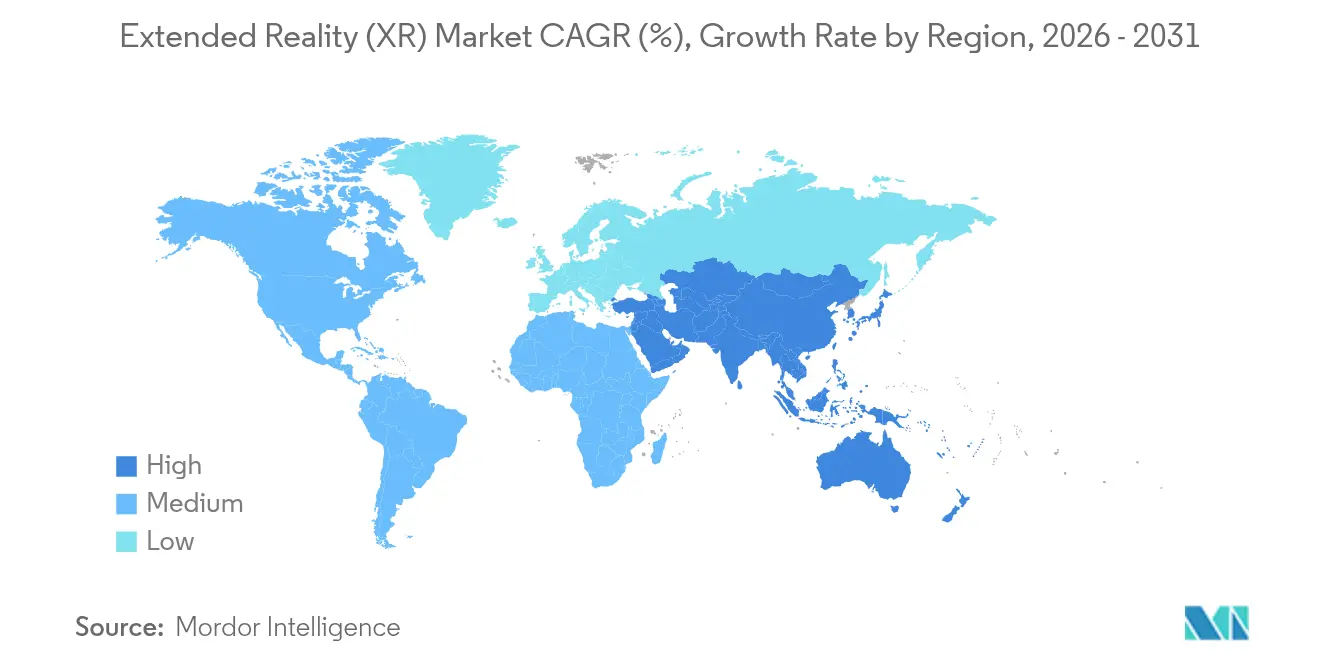

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extended Reality (XR) Market Analysis by Mordor Intelligence

Extended Reality market size in 2026 is estimated at USD 10.64 billion, growing from 2025 value of USD 7.55 billion with 2031 projections showing USD 59.18 billion, growing at 40.95% CAGR over 2026-2031. Rapid enterprise adoption across manufacturing, healthcare, and defense now outpaces consumer entertainment, turning XR from a gaming novelty into a mission-critical productivity tool. Five-generation mobile networks paired with edge computing have erased latency barriers, making millisecond-accurate visualization practical on factory floors and in surgical suites. Artificial intelligence embedded in spatial computing personalizes training content while real-time analytics close feedback loops, further raising measurable returns. Government funding in the United States and China, coupled with open standards such as OpenXR, is accelerating ecosystem maturity and reducing vendor lock-in worries. Supply chain constraints and component price inflation remain headwinds but continue to ease as new semiconductor capacity and alternative material sourcing enter production.

Key Report Takeaways

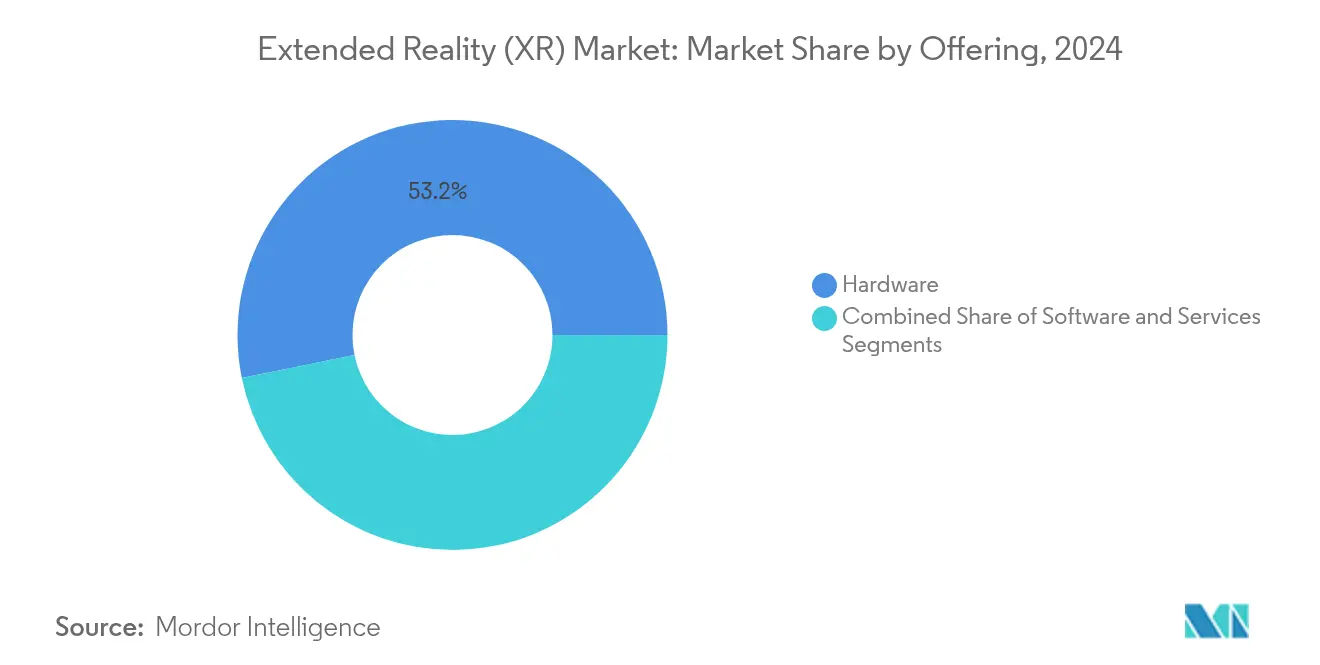

- By offering, Hardware led with 52.38% revenue share in 2025; Services is forecast to advance at a 41.35% CAGR through 2031.

- By device type, Head-Mounted Displays held 41.95% of Extended Reality market share in 2025 while Spatial and Holographic Displays are set to grow at 42.20% CAGR to 2031.

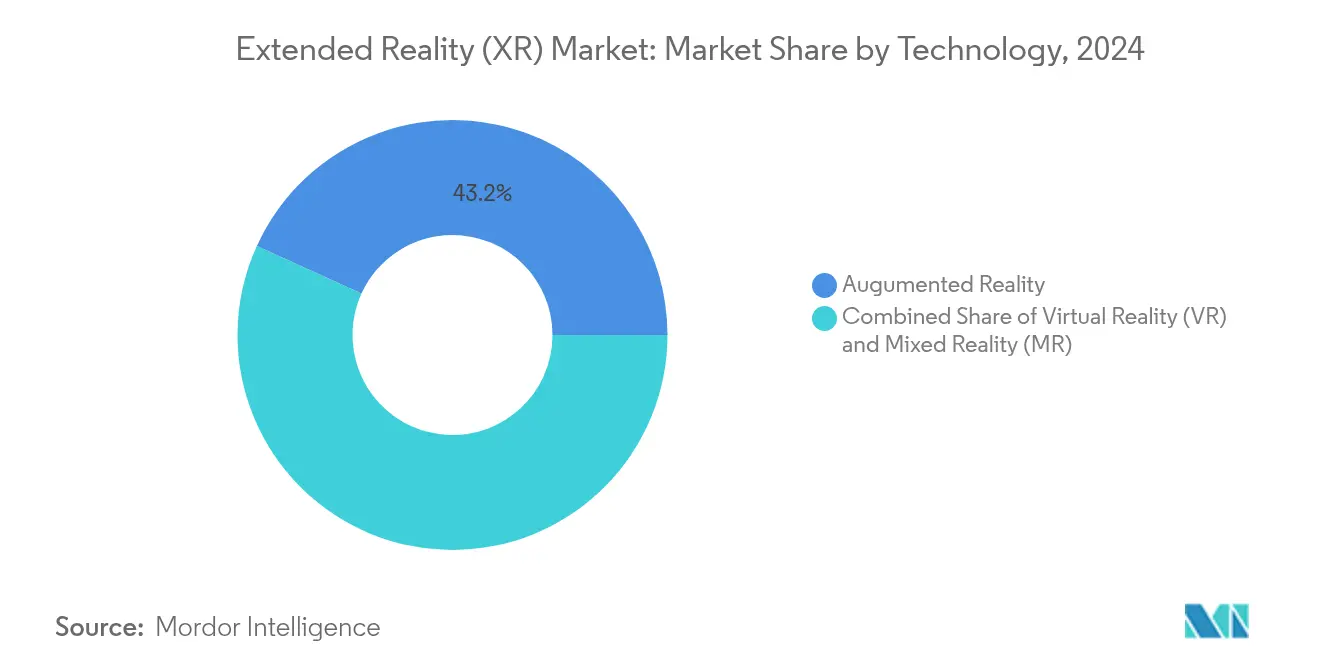

- By technology, Augmented Reality commanded 42.55% share of the Extended Reality market size in 2025 and is expanding at 41.65% CAGR to 2031.

- By end user, Gaming and Entertainment retained 38.30% share in 2025; Healthcare and Life Sciences is progressing at a 41.10% CAGR through 2031.

- By geography, North America held 36.45% revenue share in 2025, whereas Asia-Pacific posts the fastest regional CAGR at 41.20% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Extended Reality (XR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding 5G coverage and edge computing synergy | +8.2% | Global, with early gains in South Korea, China, US urban centers | Medium term (2-4 years) |

| Increased integration of XR into digital twin and Industry 4.0 frameworks | +6.8% | North America and EU, expanding to Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Rising enterprise demand for immersive remote-training | +7.1% | Global, particularly strong in healthcare and aerospace sectors | Short term (≤ 2 years) |

| Mass-market smartphone integration of spatial sensors | +5.4% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Government funding for metaverse-related RandD | +4.9% | China, US, Germany with targeted industry initiatives | Long term (≥ 4 years) |

| Adoption of open XR standards lowering vendor lock-in | +3.8% | Global, with faster adoption in enterprise segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding 5G Coverage and Edge Computing Synergy

Sub-20 ms latency now enables multi-user VR collaboration without tethered backpack PCs, as trials by Ericsson, AT&T, Dreamscape, and Qualcomm have shown. China Steel Corporation’s 5G-enabled virtual factory tours integrate live data from 85 production nodes, proving value for heavy industry. [1]China Steel Corporation, “5G Immersive Factory Tour,” csc.com.tw DHL smart-glasses pilots illustrate logistics gains from real-time pick guidance. Device weight drops as compute moves to the network edge, boosting shift-length comfort. Telcos therefore place micro-data-centers within 50 km of users to sustain immersive throughput.

Increased Integration of XR into Digital Twin and Industry 4.0 Frameworks

Pegatron’s PEGAVERSE builds five virtual factories on NVIDIA Omniverse for remote diagnostics and scenario testing, lowering downtime and travel.[2]NVIDIA, “Pegatron Deploys Omniverse for Virtual Factories,” nvidia.com BASF’s AR-enabled plant planning links sensor data with immersive visualization to streamline hazard identification. Siemens and Sony priced the SRH-S1 engineering headset at USD 4,750 to deliver pixel-accurate design collaboration. OpenUSD alignment lets disparate CAD, PLM, and IoT feeds merge into a single spatial layer. Platform vendors thus monetize subscription-based visualization rather than one-off license fees.

Rising Enterprise Demand for Immersive Remote Training

The U.S. Marine Corps installed 81 driver-training simulators that replace live vehicle use, trimming both risk and cost. Endovascular neurosurgery programs employ patient-specific 3D models to enhance procedural outcomes. Howden combines Microsoft HoloLens with PTC Vuforia to upskill field technicians, saving on travel and downtime. Adaptive AI now calibrates lesson complexity in real time, delivering 90% knowledge retention. The main bottleneck is bespoke content creation, spurring demand for service providers fluent in regulatory standards.

Mass-Market Smartphone Integration of Spatial Sensors

Apple’s WebXR support and Google’s Android XR toolkit embed spatial computing directly into mobile operating systems. XREAL’s USD 199 Beam Pro couples AR glasses with Google Play apps, with 400,000 units sold since 2017. IKEA’s smartphone AR furniture placement reduces returns and lifts purchase confidence. Cloud AI delivers instant object recognition, enabling location-based marketing while heightening GDPR scrutiny over biometric capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront costs of high-fidelity optics and processors | -4.2% | Global, particularly affecting SME adoption rates | Medium term (2-4 years) |

| User motion-sickness and ergonomic limitations | -3.1% | Global, with higher impact in consumer applications | Short term (≤ 2 years) |

| Data-privacy gaps in eye- and hand-tracking analytics | -2.8% | EU and California leading regulatory scrutiny | Long term (≥ 4 years) |

| Fragmented content-authoring tool ecosystem | -2.4% | Global, affecting enterprise deployment scalability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs of High-Fidelity Optics and Processors

Gallium and germanium shortages have inflated optics prices by up to 25%. Meta’s Reality Labs has accumulated USD 60 billion losses since 2020 while selling USD 1.1 billion in Q4 2024 XR hardware, underscoring profitability challenges. Smaller firms hesitate without capital or clear ROI. Cloud-rendered XR lightens devices yet introduces latency trade-offs that limit usage to well-served 5G zones.

User Motion-Sickness and Ergonomic Limitations

Up to 40% of users still report discomfort in full-immersion VR sessions. RayNeo’s Air 3s micro-OLED headset cuts weight and attains TÜV-certified eye comfort for all-day wear. [3]ETX View, “RayNeo Air 3s Launch Details,” etxview.com Predictive algorithms fed by biometric signals promise further relief, as Wearable Devices’ neural wristband demonstrates. Mixed-reality pass-through optics meet workplace safety requirements by preserving situational awareness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Revenue Models Accelerate Enterprise Adoption

Hardware controlled 53.2% of revenue in 2024, yet Services is set to grow fastest at 42.5% CAGR. Subscription bundles that combine devices, software, and managed support convert capex into opex, a structure favored by finance departments. The shift drives predictable recurring income for suppliers and lowers barrier-to-entry for customers. Meta’s platform pivot illustrates this movement, exploring enterprise-grade subscriptions alongside hardware refreshes.

Managed training and simulation services command premium rates thanks to specialized content needs. Vertex Solutions alone shipped more than 500 military-grade simulators worldwide, highlighting vertical expertise. As these contracts often span multi-year periods, vendors capture higher lifetime value. Hardware makers therefore partner with integrators rather than compete head-on, reflecting a maturing services-led Extended Reality market.

By Device Type: Spatial Displays Challenge HMD Dominance

Head-Mounted Displays captured 42.7% revenue in 2024 but growth now shifts to Spatial and Holographic Displays, which head toward a 43.1% CAGR. Shared viewing walls overcome hygiene and comfort limits found in personal headsets, supporting collaborative engineering reviews and customer demonstrations. Samsung’s Project Moohan exemplifies next-generation standalone units optimized for industrial deployment.

Glasses-free solutions also emerge, with Distance Technologies raising EUR 10 million (USD 11.73 million) to transform vehicle windows into dynamic mixed-reality canvases. Smartphone-tethered handheld devices remain common in field maintenance, while head-up displays secure niche positions in aviation and automotive cockpits. Longer term, smart contact lenses such as XPANCEO’s prototype could push the Extended Reality market into invisible wearables.

By Technology: AR Convergence Drives Cross-Platform Integration

Augmented Reality led with 43.2% share in 2024 and is forecast for 42.7% CAGR, reflecting its blend of digital overlays with uninterrupted real-world visibility. Virtual Reality now concentrates on high-fidelity training and design reviews, illustrated by Alaska Airlines adopting full-motion 737 simulators. Mixed Reality occupies the middle ground, dynamically switching between immersive and see-through modes.

OpenXR standardization, now supported by 13 major vendors, allows one code base to target multiple devices, slimming development costs. New Spatial Entities Extensions further streamline plane detection and anchors for enterprise apps. Qualcomm’s on-glass generative AI showcases context-aware overlays that anticipate user needs, positioning silicon roadmaps around XR-optimized neural processing.

By End User: Healthcare Acceleration Surpasses Gaming Growth

Gaming and Entertainment retained 38.3% share in 2024; however, Healthcare and Life Sciences is growing at 42.9% CAGR as hospitals quantify shorter procedure times and higher retention in surgeon training. Apple Vision Pro hosts Medical Veyond Metaverse scenarios for patient education and operating-room rehearsal.

Industrial firms deploy digital twins for remote troubleshooting, with Howden reducing engineer travel through mixed-reality guides. Retail innovations such as virtual showrooms quadruple consumer confidence and cut return rates. Defense agencies use immersive simulators to lower live-fire costs while expanding scenario diversity, reinforcing steady demand in the Extended Reality market.

Geography Analysis

North America’s installed base expands through steady healthcare, aerospace, and defense procurement. Infinite Reality closed USD 350 million in new capital and bought Landvault for USD 450 million, underscoring investor optimism in spatial computing platforms. The US Defense Innovation Unit fielded 225 immersive trainers across Air Force sites, further entrenching enterprise XR usage. Regulatory support for alternative certification in aviation spurs equipment orders as simulator fidelity approaches physical cockpit standards.

Asia-Pacific scales fastest. China alone launched more than 100 VR projects in 2024. South Korea readies Samsung’s Project Moohan release, leveraging the country’s near-universal 5G coverage. India’s public-private incubator with Meta and HCLTech cultivates grassroots application developers. Wide manufacturing bases feed continuous proof-of-value pilots, making APAC pivotal to hardware volume economics. Europe positions itself as the responsible innovation hub. Distance Technologies’ EUR 10 million (USD 11.73 million) seed illustrates appetite for automotive-grade mixed-reality surfaces. BASF, Siemens, and Sony collaborate on engineering headsets that comply with strict CE safety norms. The EU’s privacy regime shapes data-handling architectures, influencing global vendors to build GDPR-ready analytics modules.

Competitive Landscape

Competition is moderate. Meta, Apple, Microsoft, Google-Samsung, and Sony supply platform-level ecosystems, while Varjo and Magic Leap specialize in high-fidelity or industrial niches. OpenXR compliance expanded from 7 to 13 large vendors in 2024, lowering switching costs for enterprises. Proprietary hardware alone no longer guarantees lock-in; integrated service portfolios and vertical content libraries now differentiate suppliers.

Meta recorded 40% sales growth in 2024 yet posted a USD 4.97 billion Q4 loss, reflecting scale-heavy R&D commitments. Apple priced Vision Pro at USD 3,500, betting on premium elasticity among professional buyers. Microsoft bundles HoloLens with Dynamics 365 Guides, leveraging SaaS incumbency. Varjo’s photorealistic optics serve aviation and automotive design centers that pay for sub-arcminute resolution. Start-ups such as Wearable Devices and XPANCEO pursue neural-input and smart-lens breakthroughs that could reset form-factor expectations.

Hardware commoditization shifts value toward cloud orchestration, digital-twin integration, and AI-augmented analytics. Vendors that fuse these layers will secure recurring revenue and fend off margin erosion in the Extended Reality market.

Extended Reality (XR) Industry Leaders

Qualcomm Technologies Inc.

Accenture PLC

SoftServe Inc.

SphereGen Technologies LLC

Northern Digital Inc. (Roper Technologies Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snap unveiled Specs smart glasses, claiming 8 billion daily Lens uses across 4 million AR effects.

- June 2025: Khronos released Spatial Entities Extensions to formalize cross-platform plane detection and anchors.

- May 2025: XREAL announced Project Aura for Android XR at Google I/O, tightening ties with Google’s spatial platform.

- April 2025: Meta’s Reality Labs posted USD 4.2 billion Q1 loss on USD 412 million sales, citing new tariff pressures.

- March 2025: Samsung showcased Haean smart glasses aimed at industrial workflows.

Global Extended Reality (XR) Market Report Scope

Extended reality (XR) is an umbrella term encompassing augmented and virtual reality, covering a full spectrum of real and virtual environments. XR experience also caters to business issues and creates innovative solutions to increase efficiency and productivity to meet critical client needs. Implementing XR provides enterprises with a platform that helps people perform their jobs more effectively.

The extended reality market is segmented by solution (consumer engagement and business engagement), application (virtual reality (VR), augmented reality (AR), and mixed reality (MR)), end-user industry (education, retail, industrial & manufacturing, healthcare, media & entertainment, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the market size and forecasts for all the above segments in value (USD).

| Hardware |

| Software |

| Services |

| Head-Mounted Displays (Tethered, Stand-alone) |

| Head-Up Displays |

| Handheld and Mobile Devices |

| Others |

| Virtual Reality (VR) |

| Augmented Reality (AR) |

| Mixed Reality (MR) |

| Gaming and Entertainment |

| Healthcare and Life Sciences |

| Industrial and Manufacturing |

| Retail and E-commerce |

| Education and Training |

| Aerospace and Defense |

| Architecture, Engineering and Construction |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Hardware | ||

| Software | |||

| Services | |||

| By Device Type | Head-Mounted Displays (Tethered, Stand-alone) | ||

| Head-Up Displays | |||

| Handheld and Mobile Devices | |||

| Others | |||

| By Technology | Virtual Reality (VR) | ||

| Augmented Reality (AR) | |||

| Mixed Reality (MR) | |||

| By End-user Industry | Gaming and Entertainment | ||

| Healthcare and Life Sciences | |||

| Industrial and Manufacturing | |||

| Retail and E-commerce | |||

| Education and Training | |||

| Aerospace and Defense | |||

| Architecture, Engineering and Construction | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Extended Reality market?

The market reached USD 10.64 billion in 2026 and is forecast to grow to USD 59.18 billion by 2031 at a 40.95% CAGR.

Which factors are driving rapid enterprise adoption of XR?

Sub-20 ms latency from 5G plus edge computing, AI-powered adaptive training, and growing government funding together create strong, measurable returns for manufacturers, healthcare systems, and defense organizations.

Which region will expand the fastest through 2031?

Asia-Pacific is projected to post a 41.20% CAGR thanks to large-scale 5G rollouts, China’s Three-Year Metaverse Action Plan, and aggressive manufacturing digitization programs.

What is the biggest hurdle to wider XR deployment?

High upfront costs for premium optics and processors, amplified by ongoing semiconductor supply constraints, remain the primary barrier—especially for small and mid-size enterprises.

How does 5G improve XR performance?

5G networks shift heavy processing to the network edge, delivering real-time visuals with millisecond precision while allowing lighter, more comfortable devices suitable for full-shift use.

Page last updated on: