Head-Up Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

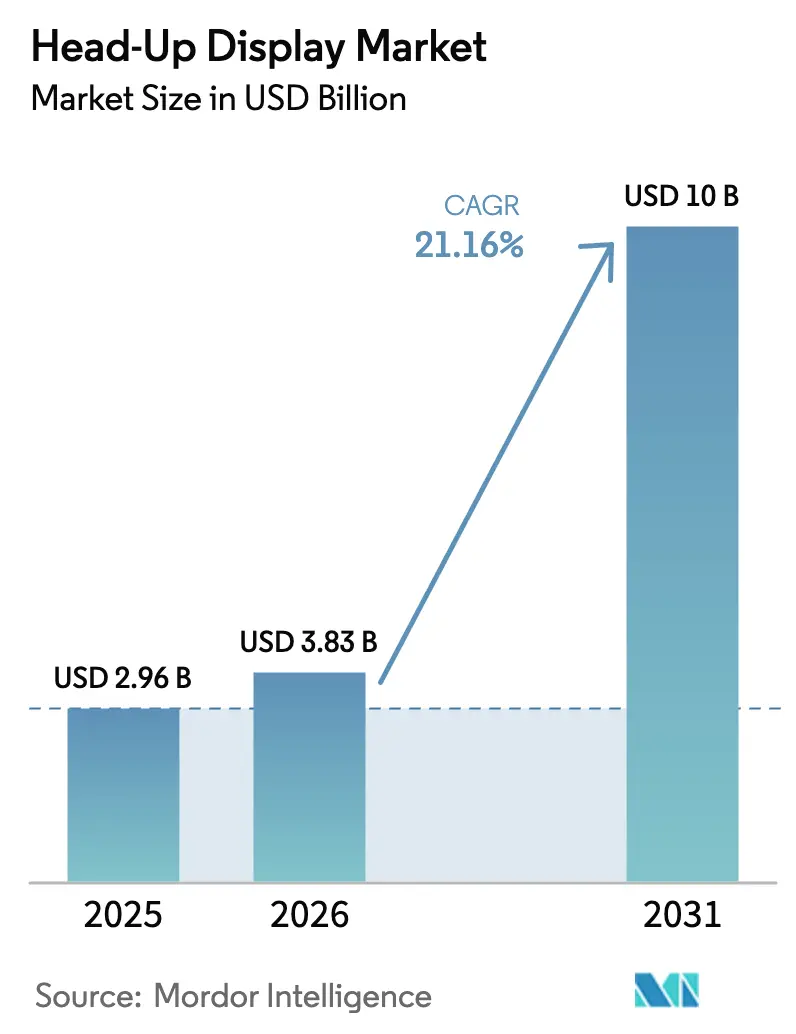

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 10 Billion |

| Growth Rate (2026 - 2031) | 21.16% CAGR |

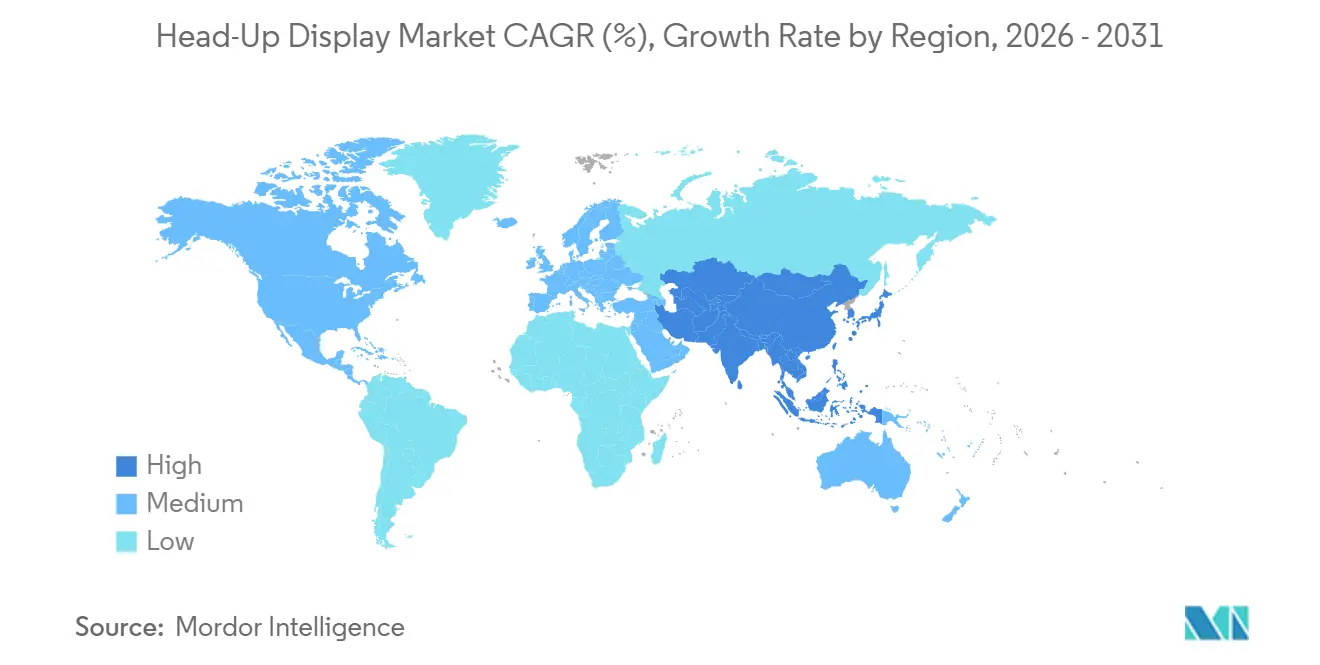

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Head-Up Display Market Analysis by Mordor Intelligence

The Head-Up Display Market size is expected to grow from USD 2.96 billion in 2025 to USD 3.83 billion in 2026 and is forecast to reach USD 10 billion by 2031 at 21.16% CAGR over 2026-2031, underscoring a steep expansion curve for this cockpit technology. This momentum stems from tightening safety mandates, the spread of electric and software-defined vehicle platforms, and a sharp pivot toward subscription-based revenue streams that rely on in-car visualization. Automakers now view windshield-integrated projection as a competitive necessity rather than a luxury option, while tier-1 suppliers race to shorten development cycles through silicon co-design so that advanced displays can cascade from premium to mid-segment trims. Asia-Pacific leads unit volume on the back of China’s new-energy vehicle surge, but North America and Europe set the pace on regulatory pull and software monetization. Competitive pressure is accelerating as holographic optics specialists and semiconductor vendors challenge traditional automotive suppliers for design-win dominance, shaping an ecosystem in which software velocity matters as much as optical performance.

Key Report Takeaways

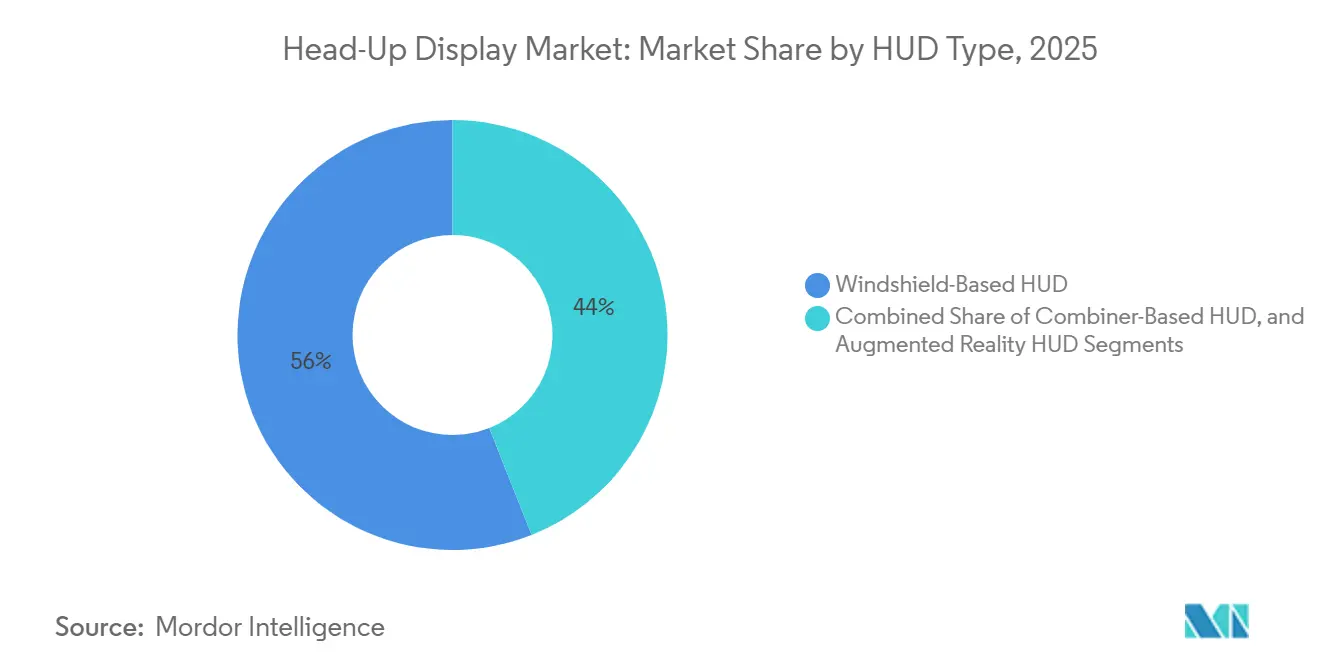

- By HUD type, windshield systems led with 56.00% revenue share in 2025, while augmented reality configurations are forecast to advance at a 19.40% CAGR through 2031.

- By dimension, two-dimensional units held 61.50% of the head-up display market size in 2025, but 3D systems are expected to register a 21.30% CAGR between 2026 and 2031.

- By vehicle class, Passenger cars captured 52.70% sales in 2025; Passenger cars represent the fastest growth at an 18.10% CAGR through 2031.

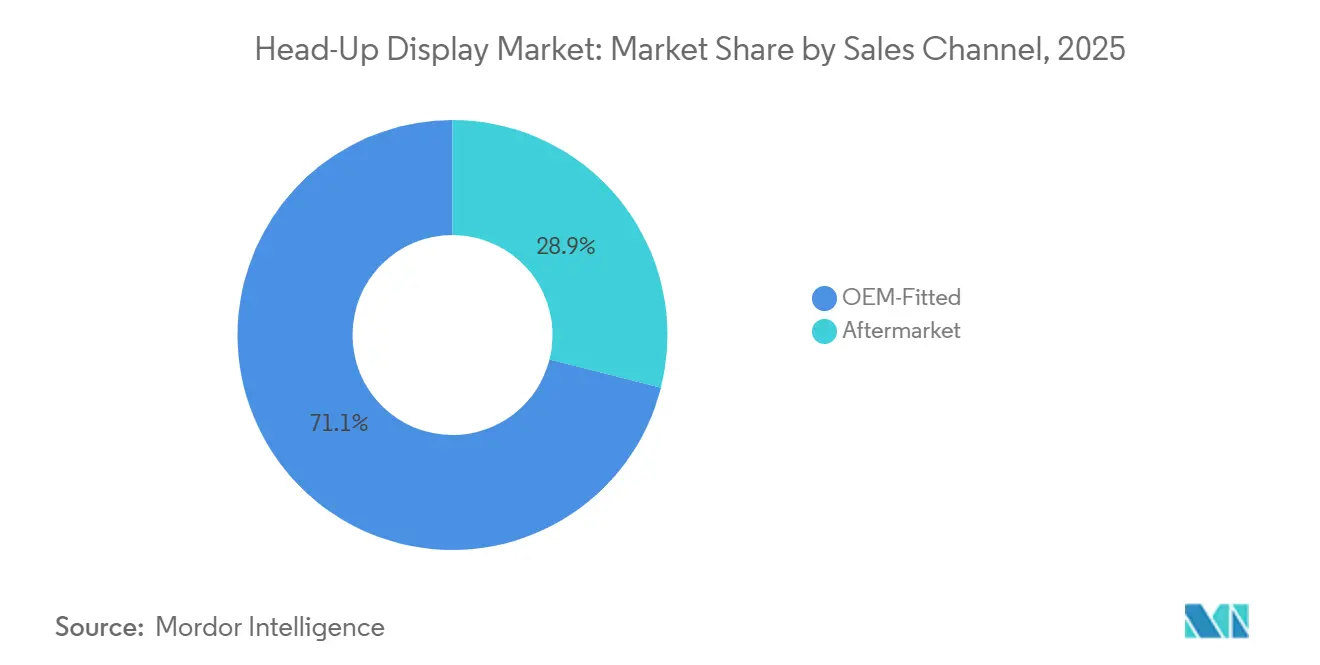

- By sales channel, OEM-fitted installations dominated with 71.20% share in 2025 and will expand at a 15.70% CAGR over the forecast horizon.

- By application, the Automotive sector held the largest share of 43.23% and the Others segment is anticipated to expand at a CAGR of 24.44%.

- By Geography, Asia Pacific retained 38.90% of the head-up display market share in 2025, and the same region is poised to grow at a 12.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Head-Up Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Integration of Augmented Reality HUDs in Mid-Range Vehicles | +4.5% | China, Germany, United States | Medium term (2-4 years) |

| Stringent Safety Regulations Mandating Driver Information Systems | +3.8% | Europe and North America, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Accelerated Adoption of Electric and Software-Defined Vehicles | +4.2% | Global, led by China, Europe, United States | Medium term (2-4 years) |

| Component Cost Reduction through Waveguide and MicroLED Optics | +3.5% | Manufacturing concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Monetization of HUD Software via Subscription-Based Feature Unlocks | +2.1% | North America and Europe | Medium term (2-4 years) |

| Automotive Tier-1 and Semiconductor Co-Design Partnerships Shortening HUD Development Cycles | +2.3% | Germany, United States, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Integration of Augmented Reality HUDs in Mid-Range Vehicles

Chinese and European automakers are pushing AR projection from luxury lines into vehicles priced between USD 30,000 and USD 50,000, resetting buyer expectations in the head-up display market. Waveguide optics now shrink projector volume to under 1 liter, freeing dashboard space and lowering material cost below the USD 300 price point that unlocks mass-market adoption. Xpeng’s G7 launch in June 2025, using Huawei’s AR-HUD, projects an 87-inch virtual image at more than 12,000 nits brightness, proof that premium specifications can arrive early in mid-segment crossovers. Hyundai and Zeiss are developing a full-windshield holographic HUD for mainstream Tucson and Santa Fe models, aiming for 2027 production and signaling that the technology curve will continue to bend toward volume platforms. As attachment rates rise, tier-1 suppliers, in the head-up display market, must balance optical innovation with aggressive cost engineering to secure program awards across multiple price tiers.

Stringent Safety Regulations Mandating Driver Information Systems

UN Regulation 171 specifies handover prompts and driver-availability confirmations that benefit from gaze-aligned visual alerts, making HUDs a compliance accelerant in Level 2 and Level 3 automation programs.[1]UN Regulation 171 Text, UNECE, unece.org In the United States, FMVSS 127 requires collision-warning symbols to reside within a tight sight-line envelope, a target naturally met by windshield projection.[2]FMVSS 127 Final Rule, National Highway Traffic Safety Administration, nhtsa.gov Euro NCAP’s Driver Engagement Protocol, released in March 2025, awards higher ratings to vehicles that display automation status via augmented reality overlays, making safety scoring a competitive marketing lever.[3]Driver Engagement Protocol v1.0, Euro NCAP, euroncap.com These mandates are arriving quickly, forcing OEMs to integrate HUD hardware during base-platform development rather than as an optional afterthought. Suppliers that can certify luminance, ghost-image, and eyebox parameters under ISO/TS 21957 now win preferred-vendor status in new model programs across three continents in HUD market.

Accelerated Adoption of Electric and Software-Defined Vehicles

Energy-efficient cockpit electronics are critical as automakers chase ever-longer driving range, making low-power holographic projection an enabler for battery-electric lineups. Panasonic’s AR HUD uses digital light processing to deliver a 12°×5° field of view at a 10 m virtual distance while staying within stringent EV power budgets. Envisics claims its holographic waveguide cuts power draw in half relative to conventional optics, a figure that translates directly into additional kilometers of range for every charge. Software-defined vehicle architectures, such as GM’s NVIDIA-powered compute domain, update AR graphics over the air and fuse sensor data on a single board, letting HUD content evolve continuously during the vehicle life cycle. Map and location providers like HERE now sell SDKs that overlay live traffic and charger status onto HUD layers, opening persistent subscription revenue opportunities for OEMs. Taken together, electrification and connectivity turn the head-up display market into a frontline for both energy management and digital-service monetization.

Component Cost Reduction through Waveguide and MicroLED Optics

Waveguide combiners and MicroLED light engines cut bill-of-materials cost while improving brightness and lifespan, addressing two historical pain points for OEMs looking to scale HUD adoption. Texas Instruments’ DLP5534-Q1 chipset packages micromirror arrays optimized for AR projection into an automotive-qualified form factor, enabling suppliers to slash projector size by 50%. MicroLED emitters increase optical efficiency at high brightness, reducing thermal load and eliminating bulky cooling ducts that previously limited integration in compact cabins. Asian panel makers are ramping volume production of wafer-level waveguides, and that scale is expected to drop per-unit cost further over the next four years, supporting the long-term CAGR uplift in the head-up display market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent High System Cost for Full-Windshield AR HUDs | -2.8% | Global, most acute in India, South America, Middle East | Medium term (2-4 years) |

| Limited Field of View and Windshield Compatibility Constraints | -1.5% | Global, notably retrofit market | Long term (≥ 4 years) |

| Tariff-Driven Optics and IC Supply Risks in North America | -1.2% | United States and Canada | Short term (≤ 2 years) |

| Growing Competition from Smart Glasses and Mixed Reality Headsets | -0.9% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent High System Cost for Full-Windshield AR HUDs

Full-windshield projection demands holographic optical elements, laser diode arrays, and continuous driver-eye tracking, driving the bill of materials above USD 1,000 and restricting adoption to ultra-luxury models. BMW’s Panoramic Vision, applied as a projection film across the entire windshield, remains an extra-cost option rather than standard equipment, illustrating OEM caution in absorbing these costs. Even with waveguides, production windshields must meet tight distortion limits, raising glass-sourcing expenses and extending validation schedules. The price barrier is especially severe in India, where ADAS penetration was only 8.3% in early 2025, leaving little budget headroom for premium cockpit features. Until component pricing falls sharply, mass-market vehicles will continue to rely on smaller windshield zones or combiner-based solutions.

Growing Competition from Smart Glasses and Mixed Reality Headsets

Apple’s Vision Pro and Meta’s Quest 3 introduce portable AR alternatives that can overlay navigation and diagnostics without permanent vehicle hardware, offering a cross-context experience valued by tech-savvy drivers. Although safety rules currently limit headset use during active driving, early adopters in North America and Europe are experimenting with passenger-side and stationary scenarios, eroding HUD’s exclusivity. Wearables also allow buyers to amortize the cost across home, work, and mobility contexts, challenging the single-purpose value proposition of factory HUDs. Suppliers must therefore emphasize seamless sensor fusion, regulatory compliance, and user comfort in order to defend the HUD market against this emerging substitute technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HUD Type: Windshield Systems Anchor Volume, AR Configurations Lead Growth

Windshield-integrated projection held 56.00% of 2025 revenue share in the head-up display market, as OEMs favored its larger virtual image and cleaner dashboard layout. That dominance will continue, yet the augmented reality subset is forecast to log a 19.40% CAGR through 2031, adding sensor-anchored arrows, hazard framing, and lane cues that elevate situational awareness. The head-up display market size for windshield units will therefore rise in absolute terms even as AR gains mix, creating dual demand streams for both conventional and holographic designs

AR HUD demand is reinforced by BMW’s plan to equip every Neue Klasse vehicle with a 3D overlay option by late 2025, setting a de facto standard for premium interiors. Tier-1 suppliers now quote sub-USD 300 bill-of-materials targets for waveguide designs, enabling mid-segment adoption without sacrificing margin. Combiner-type add-ons will linger in price-sensitive geographies, yet their share will erode as OEMs push integrated solutions that can be updated over the air and calibrated to ADAS sensors.

By Dimension Type: 3D HUD Systems Gain Traction in ADAS-Equipped Vehicles

Two-dimensional imaging retained a 61.50% share in 2025 in the head-up display market, yet 3D HUDs are projected to compound at 21.30% annually as Level 2 and Level 3 automation expand. Depth-separated layers present battery charge, speed, and automation mode close to the driver, while turn arrows and obstacle boxes appear 10-20 m ahead, cutting refocus time.

BMW’s 3D Head-Up Display demonstrates how dual-plane holography works in production, integrating with driver-monitor cameras to adapt imagery as head position shifts. Suppliers must therefore couple optics expertise with real-time gaze tracking and GPU-based rendering. Those that can do so within EV power budgets will earn an outsized share of upcoming model awards, lifting the head-up display market share for 3D solutions over the forecast window.

By Vehicle Class: Passenger Vehicles Drive Volume Growth, Luxury Retains Premium Features

By vehicle class, Passenger cars captured 52.70% sales in 2025; Passenger cars represent the fastest growth at an 18.10% CAGR through 2031 as Chinese and Korean OEMs slot waveguide AR units into crossovers and sedans priced below USD 50,000. This mainstreaming expands the head-up display market by an order of magnitude rather than percentage points because the mid-segment pool is far larger.

Hyundai’s collaboration with Zeiss to bring a film-based holographic HUD to Tucson and Santa Fe illustrates the democratization arc, while premium marques experiment with full-windshield immersion to maintain differentiation. Commercial vehicles represent an adjacent opportunity, especially where fleet managers tie HUD safety overlays to insurance savings, though price sensitivity and long replacement cycles temper near-term volume.

By Sales Channel: OEM Integration Dominates, Aftermarket Constrained by Calibration Complexity

OEM accounted for 71.20% of 2025 revenue and will climb at a 15.70% CAGR as ADAS calibration and software update requirements intensify. Centralized compute architectures make windshield projection a native feature rather than a bolt-on accessory, locking in OEM control over user experience and data pathways.

Aftermarket suppliers still serve older vehicle fleets with compact combiner units, but lack access to factory sensor data and cannot match wide-field AR capabilities, keeping their volumes flat. Fleet operators may adopt portable systems that plug into telematics boxes for driver coaching, yet overall head-up display market size growth remains anchored in OEM build-lines where warranty, regulation, and lifecycle support converge.

By application, Automotive sector dominated the market in 2025

By application, the Automotive sector held the largest share of 43.23% and the Others segment is anticipated to expand at a CAGR of 24.44%.In the automotive sector, head-up displays (HUDs) dominate the market, primarily due to a heightened emphasis on the safety of drivers and passengers, coupled with the integration of Advanced Driver-Assistance Systems (ADAS). This trend is fueled by consumer desires for a more immersive, connected, and safer driving experience. Features such as navigation and speed alerts are now projected directly onto windshields, aiming to reduce driver distraction. Notably, the market is transitioning from premium vehicles to the mid-segment, witnessing substantial growth in both passenger and commercial vehicles.

Initially, HUD technology found its primary applications in the military and aviation sectors. While these segments still play a role, they account for a smaller share of the overall market. In military aircraft, HUDs play a pivotal role, presenting pilots with essential flight data right in their line of sight. This capability significantly boosts situational awareness and operational efficiency. With defense budgets on the rise and ongoing modernization programs, there's a sustained investment in these specialized, high-precision systems. Furthermore, the "Others (Inc.)" category highlights the technology's expanding footprint, encompassing applications in consumer electronics (like wearable HUDs for gaming or industrial purposes) and even in healthcare for surgical assistance.

Geography Analysis

Asia-Pacific held 38.90% of global revenue in 2025 and is forecast to grow at a 12.30% CAGR through 2031, buoyed by China’s electric-vehicle production boom and Japan’s export strength in optoelectronics. Local brands like Xpeng, NIO, and Li Auto embed large AR images to stand out in a hypercompetitive domestic arena, accelerating feature diffusion down the price ladder. South Korea’s display ecosystem supplies waveguides and MicroLEDs at scale, compressing cost curves for regional automakers.

North America benefits from high luxury penetration and early software-defined architectures, although Section 301 tariffs on Chinese optics add 25% landed cost, prompting dual sourcing from Europe and Southeast Asia. U.S. federal rules on collision-warning visualization mandate HUD-friendly sight-line placement, nudging OEMs toward integrated projection. Canada’s parts suppliers align with these programs to keep assembly plants fully utilized despite tariff turbulence.

Europe marries stringent safety scoring with prestige brands that view cockpit digitalization as a hallmark. Euro NCAP’s 2025 engagement protocol rewards AR overlays, pushing Volkswagen, Mercedes-Benz, and BMW to accelerate full-windshield roadmaps. Yet the region also grapples with higher homologation costs for advanced optics. Emerging markets in the Middle East and Africa explore HUD for autonomous shuttle pilots, but harsh climate conditions and price sensitivity keep uptake modest for now.

Competitive Landscape

The competitive field skews toward a handful of entrenched tier-1 suppliers that leverage scale and OEM relationships, yet disruptive entrants wield holographic IP, software platforms, or silicon integration to win new awards. Envisics secured USD 50 million in Series C funding led by Hyundai Mobis, underscoring OEM appetite for waveguide solutions that cut power use by 50% and shrink packaging by 40%. Visteon’s September 2025 pact with FUTURUS positions it to offer windshield, passenger, and AR modules across a single platform, hedging bets on form-factor diversity.

Bosch Ventures’ USD 21 million investment in 4screen reveals a shift toward software monetization, where third-party apps and subscription tiers can populate HUD real estate, turning static hardware into a revenue canvas. Semiconductor vendors such as Texas Instruments move upstream with DLP5534-Q1 chipsets that, when paired with Qualcomm compute, yield turnkey AR solutions, putting pressure on hardware-only suppliers.

Traditional leaders retain advantages in supply security, validation labs, and multi-year sourcing contracts, yet they must accelerate over-the-air feature pipelines to stay relevant. Partnerships that blend optics, compute, and content are becoming the norm, creating a head-up display industry dynamic in which speed of software iteration determines long-term winner status.

Head-Up Display Industry Leaders

Continental AG

Nippon Seiki Co. Ltd.

Denso Corporation

Visteon Corporation

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Continental introduced ScenicView, a full-width windshield display that integrates navigation and ADAS alerts on a single transparent layer, with series production slated for late 2027.

- September 2025: Visteon announced a strategic partnership with FUTURUS to co-develop augmented reality, windshield, and passenger HUD modules for global OEMs.

- August 2025: BMW confirmed Panoramic iDrive with optional 3D HUD for all Neue Klasse models beginning late 2025.

- June 2025: Xpeng launched the G7 SUV featuring Huawei’s AR-HUD projecting an 87-inch virtual image at 12,000 nits.

Global Head-Up Display Market Report Scope

The Head-Up Display (HUD) is a Human-Machine-Interface that relays real-time information related to the vehicle, traffic, and associated environment for an assisted driving experience. A typical HUD consists of a projector unit, a combiner, and a video generator. HUD is being adopted widely in the automotive, military, and civil aviation industries. In the Aviation industry, the HUD helps the pilot in the critical phases of a flight - takeoff and landing.

The Head-up Display Market / HUD Market Report is Segmented by HUD Type (Windshield-Based HUD, Combiner-Based HUD, Augmented Reality HUD, Conventional HUD), Dimension Type (2D HUD, 3D HUD), Vehicle Class (Commercial Vehicles, Passenger Vehicles), Sales Channel (OEM-Fitted, Aftermarket), Application (Automotive, Military and Civil Aviation, and Others)and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Windshield-Based HUD |

| Combiner-Based HUD |

| Augmented Reality HUD |

| 2D HUD |

| 3D HUD |

| Commercial Vehicles |

| Passenger Vehicles |

| OEM-Fitted |

| Aftermarket |

| Automotive |

| Military and Civil Aviation |

| Others (Industrial, Wearable, and other Displays) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By HUD Type | Windshield-Based HUD | |

| Combiner-Based HUD | ||

| Augmented Reality HUD | ||

| By Dimension Type | 2D HUD | |

| 3D HUD | ||

| By Vehicle Class | Commercial Vehicles | |

| Passenger Vehicles | ||

| By Sales Channel | OEM-Fitted | |

| Aftermarket | ||

| By Application | Automotive | |

| Military and Civil Aviation | ||

| Others (Industrial, Wearable, and other Displays) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the head-up display market in 2026?

It stood at USD 3.83 billion in 2026 and is projected to expand rapidly through 2031.

What CAGR is forecast for head-up displays to 2031?

The compound annual growth rate is projected at 21.16% for the 2026-2031 period.

Which region leads 2025 revenue for head-up displays?

Asia-Pacific led with 38.90% of global revenue in 2025.

Why are augmented reality HUDs gaining traction?

They anchor navigation and safety cues directly onto road objects, meeting new safety protocols and improving driver situational awareness.

What limits full-windshield HUD adoption today?

System cost above USD 1,000 per vehicle, windshield manufacturing complexity, and power requirements restrict deployment to ultra-luxury models.

Page last updated on: