Enterprise Augmented Reality Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

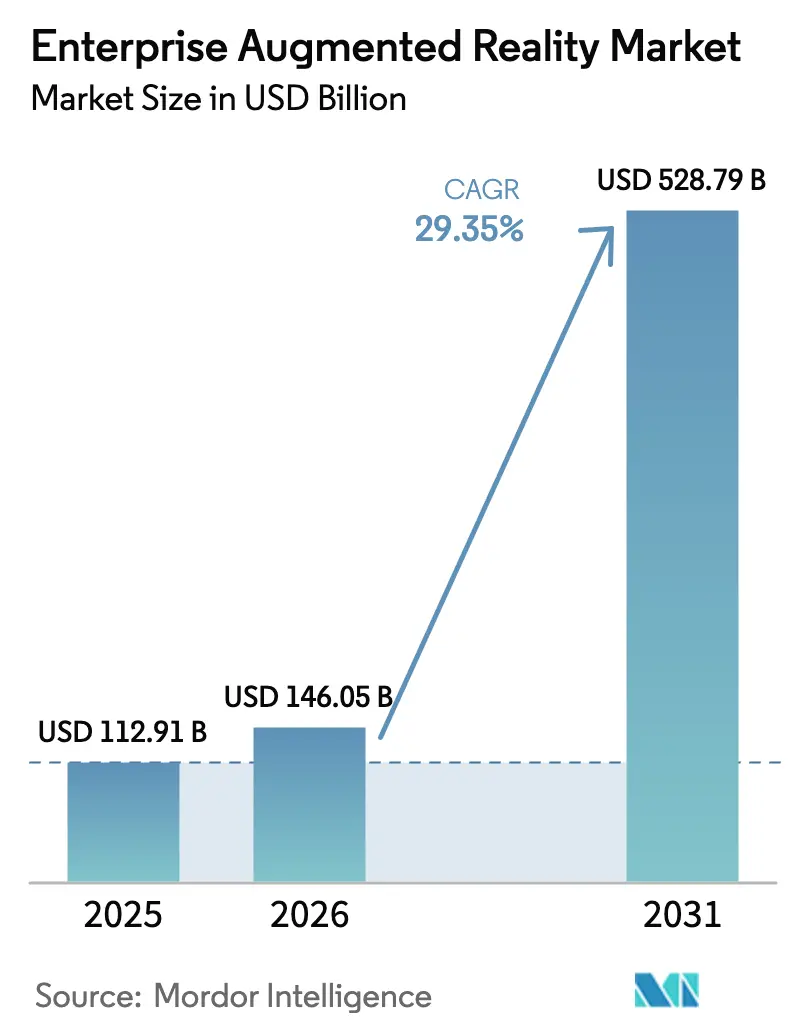

| Market Size (2026) | USD 146.05 Billion |

| Market Size (2031) | USD 528.79 Billion |

| Growth Rate (2026 - 2031) | 29.35% CAGR |

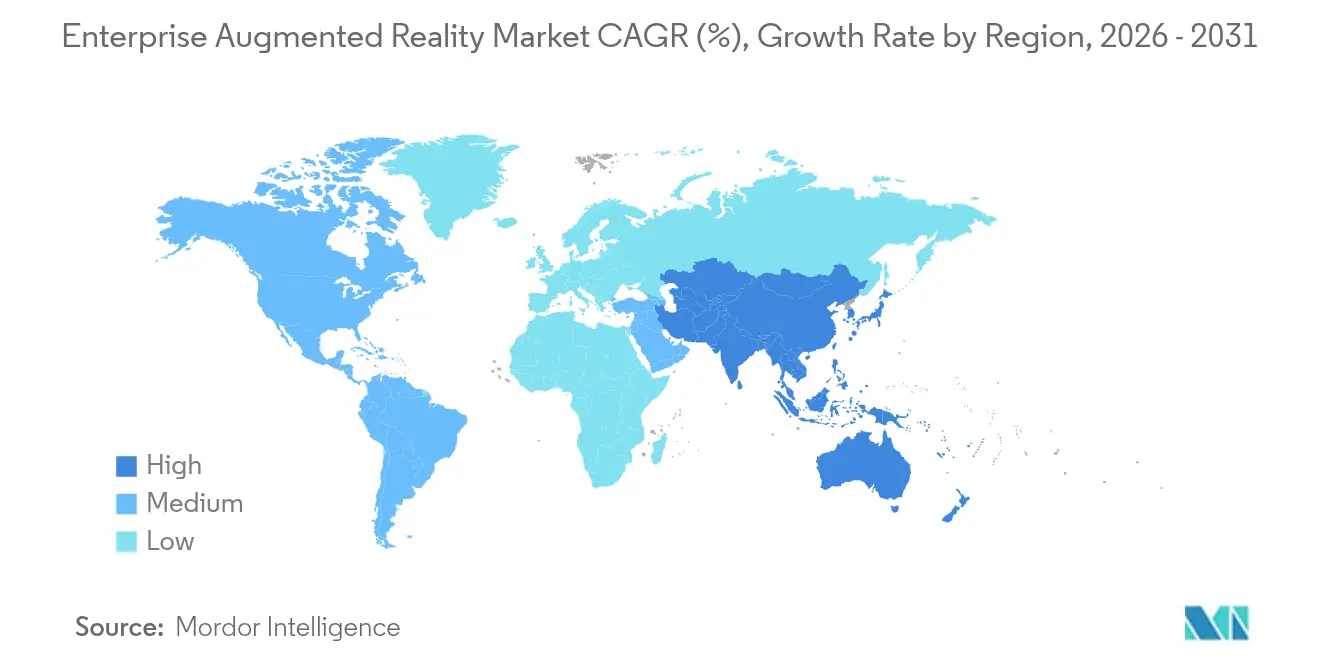

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

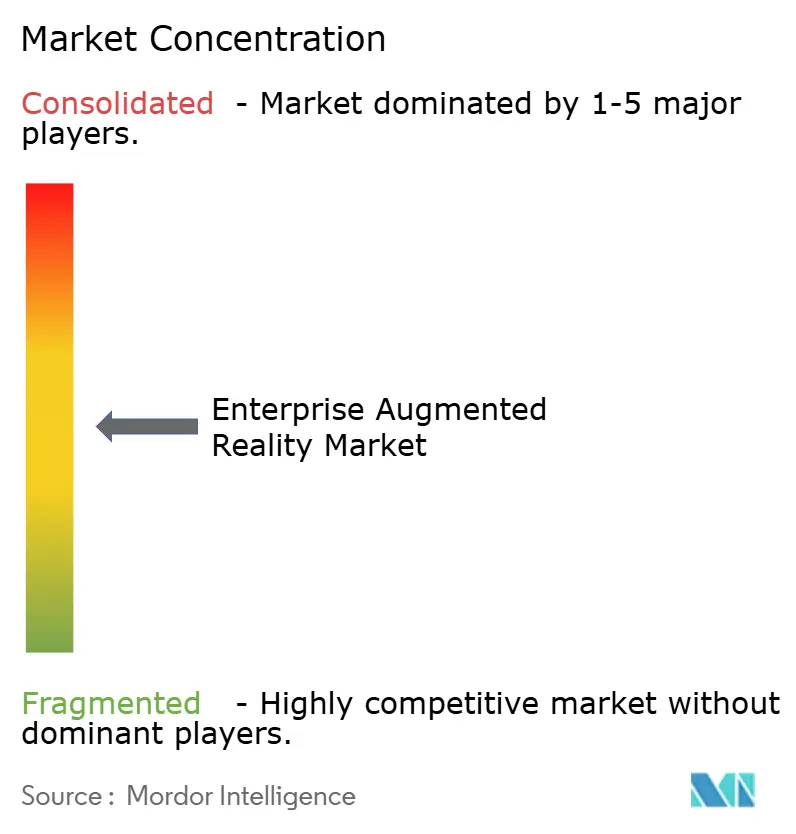

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Augmented Reality Market Analysis by Mordor Intelligence

The enterprise augmented reality market size was valued at USD 112.91 billion in 2025 and estimated to grow from USD 146.05 billion in 2026 to reach USD 528.79 billion by 2031, at a CAGR of 29.35% during the forecast period (2026-2031). Hardware currently delivers 62.3% of global revenue, yet service-centric business models are expanding fastest as enterprises shift capital from devices to outcome-based engagements. The acceleration is powered by widespread 5G roll-outs, AR-cloud architectures, and RISC-V chipsets that lower total cost of ownership while providing the ultra-low latency required for mission-critical use cases. Discrete manufacturers and energy operators are scaling proven pilots into plant-wide deployments because real-time visual guidance consistently trims errors, downtime, and training cycles. Competitive intensity remains moderate; platform players are deepening software ecosystems while newer entrants leverage cost-efficient optics and proprietary SLAM stacks to secure design wins.

Key Report Takeaways

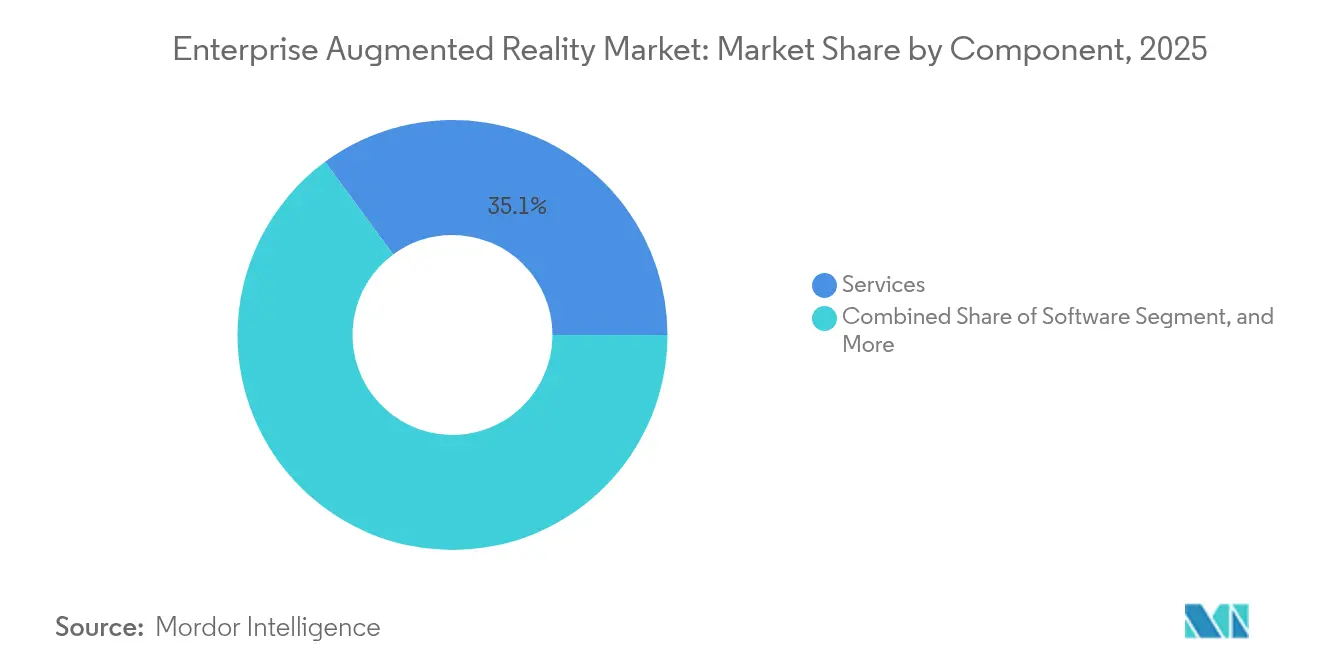

- By component, Hardware held 61.45% of the enterprise augmented reality market share in 2025, while Services is forecast to grow at 33.20% CAGR through 2031.

- By device type, Head-mounted displays led with 51.85% revenue share in 2025; Projection/Spatial systems are projected to expand at a 36.10% CAGR to 2031.

- By deployment, On-premise implementations represented 61.90% of 2025 spending; Cloud/AR-as-a-Service is forecast to rise at 34.90% CAGR to 2031.

- By application, Remote Assistance & Collaboration accounted for 27.15% of the enterprise augmented reality market size in 2025; Workflow & Quality Control is advancing at a 35.80% CAGR to 2031.

- By end-user industry, Industrial Manufacturing captured 30.05% share of the enterprise augmented reality market size in 2025, while Energy & Utilities is expected to post a 32.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Augmented Reality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid ROI-proof industrial pilot programs | +4.2% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Smartphone-class RISC-V processors slashing device BOM | +3.8% | Global, led by APAC manufacturing hubs | Medium term (2-4 years) |

| Mainstream shift to head-mounted AR for frontline work | +5.1% | North America & EU industrial corridors | Medium term (2-4 years) |

| 5G/Private-LTE enabling ultra-low-latency AR streaming | +4.7% | Global, with early deployment in developed markets | Long term (≥ 4 years) |

| ESG-linked capex credits for AR training gear | +2.3% | EU & North America, expanding to APAC | Long term (≥ 4 years) |

| OSHA digital-twin mandates for high-risk plants | +3.1% | North America, with spillover to global operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid ROI-proof Industrial Pilot Programs

Enterprises move beyond proofs of concept because pilot projects consistently deliver hard savings and productivity lifts. Ford’s Dearborn engine plant documented measurable quality gains after equipping technicians with HoloLens 2, training 25 workers initially and planning to scale to 100 by year-end.[1]Kelly Tyko, “Ford Expands HoloLens Use for Quality Checks,” Axios, axios.com Similar warehouse programs pushed order-picking accuracy to 99.9% at Coca-Cola operations.[2]Tom Huddleston, “AR Headsets Boost Warehouse Productivity,” Business Insider, businessinsider.com These publicly reported successes shorten internal approval cycles and justify multi-site roll-outs, accelerating the enterprise augmented reality market’s penetration curve.

Smartphone-class RISC-V Processors Slashing Device BOM

Open-source RISC-V chipsets provide smartphone-level compute at materially lower bill-of-materials. XREAL’s X1 processor removed the need for tethered devices, letting the firm price its smart glasses at USD 499–599 and still sustain gross margins.[3]Kif Leswing, “XREAL One Series Launches with New Chip,” CNBC, cnbc.com Lower costs broaden the addressable user base and allow fleet-sized procurements, a critical lever for scaling the enterprise augmented reality market in cost-sensitive industrial segments.

Mainstream Shift to Head-mounted AR for Frontline Work

Improved ergonomics, larger FoV, and all-day battery life have made head-mounted AR practical for frontline technicians. Peer-reviewed research indicated productivity jumps of up to 15% without compromising worker safety. As wearables integrate seamlessly with PPE and corporate IT, hands-free workflows replace handheld screens, lifting adoption barriers and deepening per-user consumption of AR content.

5G/Private-LTE Enabling Ultra-low-latency AR Streaming

Edge-to-cloud rendering over dedicated 5G slices reduces on-device compute and unlocks photorealistic overlays. Google Cloud’s Immersive Stream for XR showcases download-free experiences that run on thin clients. Nuclear facilities in the Czech Republic now run latency-sensitive AR inspections over private 5G, improving safety in constrained environments. Reliable sub-20 ms round-trip times are pivotal for real-time guidance and digital twins, underpinning long-term growth of the enterprise augmented reality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-compute security gaps | -2.8% | Global, with heightened concern in regulated industries | Short term (≤ 2 years) |

| Legacy MES/PLM integration costs | -3.4% | North America & EU manufacturing centers | Medium term (2-4 years) |

| Short-staffed optical-waveguide supply chain | -2.1% | Global, concentrated in APAC production hubs | Medium term (2-4 years) |

| Growing patent-troll litigation on SLAM IP | -1.7% | North America & EU legal jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Edge-compute Security Gaps

Distributing processing across headsets, on-premise gateways, and cloud nodes widens the attack surface, a concern for plants handling proprietary processes or hazardous materials. Many IT teams lack AR-specific security playbooks, resulting in delayed roll-outs until zero-trust architectures are proven. Compliance audits add further overhead, temporarily dampening some demand curves within the enterprise augmented reality market.

Legacy MES/PLM Integration Costs

Brownfield factories often run decades-old MES and PLM suites that were never architected for spatial data. Retrofitting those systems to stream work instructions into AR devices can exceed hardware budgets and demands scarce integration talent. Without standardized APIs, CIOs face vendor lock-in and multi-year roadmaps, slowing conversion of intent into purchase orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Transformation

The Services segment is projected to expand at 33.20% CAGR from 2026-2031, overtaking pure product revenue as firms lean on integrators for rollout, user training, and uptime SLAs. Services partners convert early hardware pilots into plant-wide deployments, a trend that underpins the enterprise augmented reality market’s shift toward outcome-based contracting. Innovations such as AI-generated work instructions automate content creation and cut deployment cycles.

The component mix evolution signals maturation: once fleets of headsets are installed, value migrates to analytics, refresh cycles, and continuous improvement consulting. Vendors are bundling software subscriptions with on-site change-management to lock in recurring revenue and deepen client intimacy, reinforcing long-run stickiness across the enterprise augmented reality market.

By Device Type: Projection Systems Emerge

Head-mounted units retained 51.85% share in 2025, but projection and spatial systems are sprinting at 36.10% CAGR as factories deploy shared 3D workspaces for collaborative tasks. Projection eliminates wearability concerns and is favored for operator training bays, additive-manufacturing cells, and quality cabins where teams gather around a common reference. Industry 4.0 pilots confirm that spatial setups shorten design reviews and cut rework loops.

Lightweight optics research is simultaneously reducing headset weight to under 200 g, widening suitability for shift-long use. Enterprises therefore adopt a multimodal toolkit: individual technicians wear head-mounted displays, while supervisors engage with large-scale projection, collectively accelerating device diversity across the enterprise augmented reality market.

By Deployment: Cloud Services Surge

On-premise solutions accounted for 61.90% of 2025 revenue because CIOs initially favored tight data custody. However, cloud-native offerings are growing at 34.90% CAGR as hyperscalers launch GPU-accelerated XR services with enterprise controls. Google Cloud’s Immersive Stream delivers zero-install sessions across multisite fleets, slashing local hardware spend.

Infinite Reality’s USD 3 billion investment and Zappar acquisition underscore momentum toward vertically integrated cloud plus content ecosystems. As bandwidth costs fall and zero-trust postures mature, cloud will capture an outsized share of incremental dollars in the enterprise augmented reality market.

By Application: Workflow Control Accelerates

Remote Assistance & Collaboration represented 27.15% of 2025 demand, yet Workflow & Quality Control is pacing at a 35.80% CAGR as manufacturers embed AR into takt-time operations. Real-time overlay of torque specs, part numbers, and IoT sensor data slashes errors before first pass yield. Automotive OEMs such as BMW run mixed-reality reviews that compress design-to-tooling cycles.

Design, training, and maintenance continue to show robust gains, but the pivot to line-side quality control elevates AR from supportive to indispensable. The enterprise augmented reality market’s growth therefore tilts toward process-critical licenses where downtime impacts are measurable and C-suite visibility is high.

By End-User Industry: Energy & Utilities Lead Growth

Industrial Manufacturing held 30.05% share in 2025, yet Energy & Utilities is forecast for 32.40% CAGR because digital twins and remote inspections mitigate risk in hazardous plants. Czech nuclear operators’ success with 5G-enabled AR strengthens the case for similar adoption in oil, gas, and chemical complexes.

Automotive, aerospace, and healthcare add scale through assembly guidance, cabin configuration, and surgical visualization respectively. Retail, logistics, and agriculture remain in earlier phases but exhibit clear ROI in pick accuracy and agronomic scouting, indicating continued whitespace for the enterprise augmented reality market.

Geography Analysis

North America delivered 35.75% of 2025 revenue on the back of mature IT budgets, defense-grade mandates, and OSHA’s inclusion of UL 8400 AR/VR equipment safety standards. Microsoft’s collaboration with Anduril on the Integrated Visual Augmentation System illustrates government pull-through into commercial sectors. The region’s robust developer ecosystem accelerates bespoke application creation, reinforcing leadership across the enterprise augmented reality market.

Asia-Pacific is the fastest-growing theatre at 31.10% CAGR. China alone is expected to ship 2.75 million smart-glasses units in 2025, more than doubling year on year. XREAL’s 51% share of global AR eyewear shipments highlights regional ascendancy in optics manufacturing. Government incentives tied to factory digitalization and 5G coverage blanket industrial corridors, pulling local integrators and hyperscale cloud providers into tight alignment.

Europe posts steady gains, anchored by Industry 4.0 roadmaps, ESG-linked capex, and stringent worker-safety directives. Automotive clusters in Germany and France adopt collaborative AR to de-risk model transitions, while offshore wind farms deploy spatial twins for maintenance sequencing. The continent emphasizes interoperability standards, giving rise to cross-vendor consortia that could shape global frameworks and influence procurement across the enterprise augmented reality market.

Competitive Landscape

The enterprise augmented reality market is moderately fragmented, with incumbents leveraging platform depth while newcomers pursue cost disruption. Microsoft couples HoloLens hardware with Azure Digital Twins and Power Platform plugins, offering CIOs an end-to-end stack. PTC fortifies share via Vuforia Engine 11, embedding AR authoring into existing PLM workflows. Google’s optics partnership with Magic Leap signals its intent to internalize display IP and derisk supply dependencies.

Challengers such as XREAL, Rokid, and RealWear exploit agile hardware iterations and vertical bundles. RealWear’s acquisition of Almer Technologies broadens its industrial headset line while adding TeamViewer’s remote-support channels. Patent suits around SLAM and waveguides introduce uncertainty that can stunt capital formation; accordingly, firms with large IP arsenals or captive component fabs are better shielded. Supply-chain tightness in high-index glass and micro-LED emitters has fostered strategic investments like Vuzix’s USD 5 million infusion from Quanta Computer to ramp waveguide output.

Strategic collaboration is the dominant playbook. Cloud hyperscalers provide rendering back-ends, while ISVs overlay sector-specific logic. System integrators bundle change-management and KPI accountability. As pilots scale, winning vendors will combine device diversity, security certifications, and analytics benchmarks to capture an increasing slice of enterprise augmented reality market spending.

Enterprise Augmented Reality Industry Leaders

Atheer Inc.

Dynabook Americas Inc.

Epson Corporation

ThirdEye Gen Inc.

Lenovo Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: HMS confirmed its SiNGRAY G2 headset will ship with frontline.io’s XR platform, integrating device management and workflow authoring to accelerate industrial rollouts.

- June 2025: Vuzix secured a USD 5 million investment from Quanta Computer aimed at scaling waveguide production and embedding AI vision modules for next-gen devices.

- June 2025: Wyr.ai partnered with Vuzix to co-launch an inspection suite that merges computer vision defect detection with AR overlays for quality engineers.

- April 2025: Lumus became optical-engine supplier to Holochip for a U.S. Navy AR program, signaling defense traction for reflective waveguide tech.

Global Enterprise Augmented Reality Market Report Scope

Augmented reality is an interactive experience in a real-world environment where the objects that reside in the real world are enhanced by computer-generated perceptual information, sometimes across multiple sensory modalities, including visual and auditory.

Global Enterprise Augmented Reality Market is Segmented by End-user Applications (Retail and E-commerce, Education (E-learning), Industrial, Automotive and Aerospace, Professional Services, and Other End-user Applications) and Geography.

| Hardware |

| Software |

| Services |

| Head-mounted / Smart-glasses |

| Handheld / Mobile AR |

| Projection / Spatial |

| Others (HUD, Helmet-mounted) |

| Remote Assistance and Collaboration |

| Training and Simulation |

| Maintenance and Inspection |

| Design and Visualization |

| Sales and Marketing |

| Workflow and Quality Control |

| Industrial Manufacturing |

| Automotive and Aerospace |

| Energy and Utilities |

| Healthcare |

| Retail and E-commerce |

| Logistics and Warehousing |

| Other End-user Industries (Public Safety, Agriculture) |

| On-premise |

| Cloud / AR-as-a-Service |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Device Type | Head-mounted / Smart-glasses | |

| Handheld / Mobile AR | ||

| Projection / Spatial | ||

| Others (HUD, Helmet-mounted) | ||

| By Application | Remote Assistance and Collaboration | |

| Training and Simulation | ||

| Maintenance and Inspection | ||

| Design and Visualization | ||

| Sales and Marketing | ||

| Workflow and Quality Control | ||

| By End-User Industry | Industrial Manufacturing | |

| Automotive and Aerospace | ||

| Energy and Utilities | ||

| Healthcare | ||

| Retail and E-commerce | ||

| Logistics and Warehousing | ||

| Other End-user Industries (Public Safety, Agriculture) | ||

| By Deployment | On-premise | |

| Cloud / AR-as-a-Service | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the enterprise augmented reality market?

The enterprise augmented reality market stands at USD 146.05 billion in 2026 and is projected to reach USD 528.79 billion by 2031.

Which component segment is growing fastest?

Services is expanding at 33.20% CAGR as firms rely on integrators and outcome-based contracts for large-scale deployments.

Why is Asia-Pacific the fastest-growing region?

Manufacturing expansion, government digitalization incentives, and cost-efficient optics production are driving a 31.10% CAGR in Asia-Pacific.

How will 5G influence AR adoption?

Dedicated 5G and private-LTE networks provide sub-20 ms latency that supports cloud-rendered AR, enabling photorealistic overlays without heavy on-device processing.

Which industry vertical shows the highest forecast growth?

Energy & Utilities is predicted to grow at 32.40% CAGR as operators deploy AR for safety-critical digital twins and remote inspections.

What are the main barriers to enterprise AR scale-up?

Edge-compute security gaps and costly integration with legacy MES/PLM systems remain the two largest restraints on rapid expansion.

Page last updated on: