Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

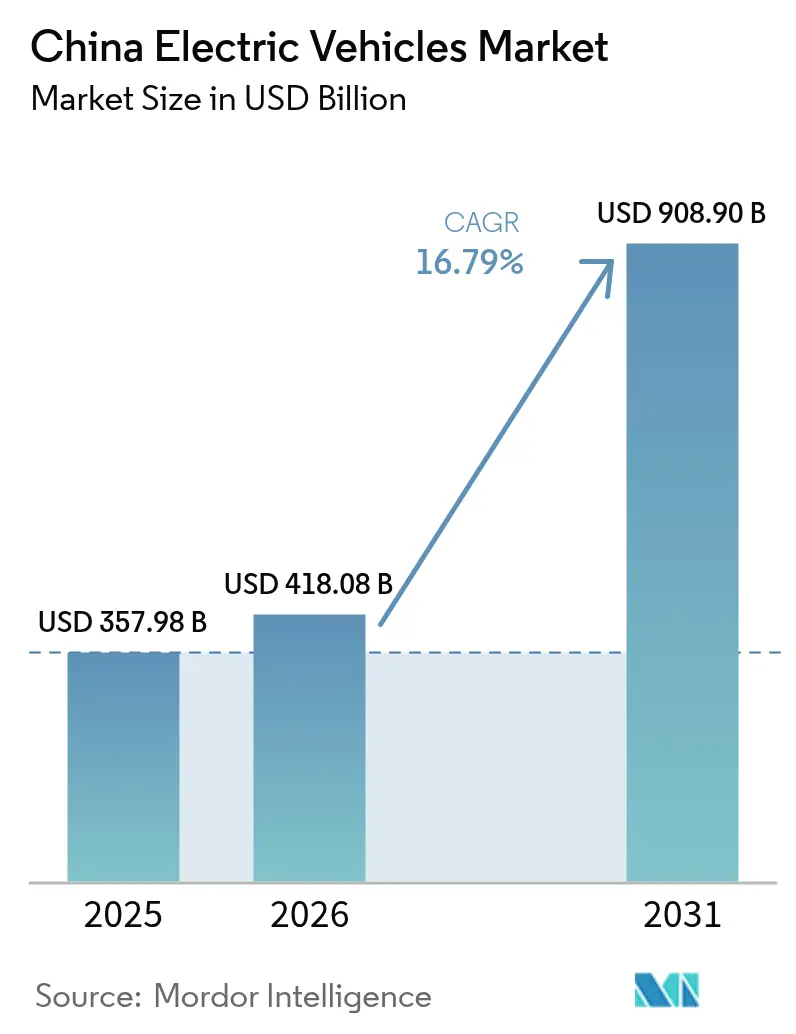

| Base Year Market Size (2025) | USD 357.98 Billion |

| Market Size (2026) | USD 418.08 Billion |

| Market Size (2031) | USD 908.9 Billion |

| Growth Rate (2026 - 2031) | 16.79% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Electric Vehicles Market Analysis by Mordor Intelligence

The China Electric Vehicles Market size in 2026 is estimated at USD 418.08 billion, growing from 2025 value of USD 357.98 billion with 2031 projections showing USD 908.9 billion, growing at 16.79% CAGR over 2026-2031. Battery cost parity, a nationwide charging and battery-swap build-out, and tier-2/3 city PHEV momentum reinforce volume expansion. Automakers are also accelerating vertical integration and battery chemistry innovation to secure falling margins amid price wars. Infrastructure investment and cost-competitive LFP batteries position the Chinese electric vehicle market for further penetration into price-sensitive rural segments.

Key Report Takeaways

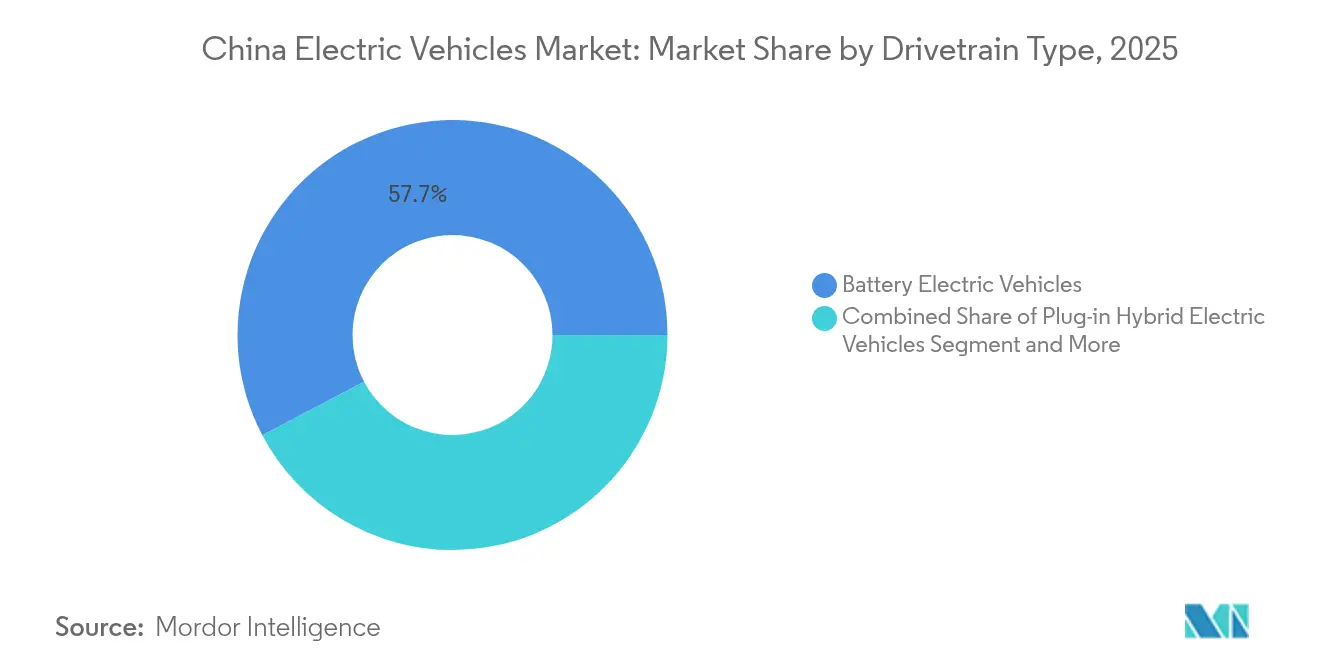

- By drivetrain type, battery electric vehicles held 57.72% of the China electric vehicle market share in 2025, while plug-in hybrids are forecast to advance at a 20.88% CAGR through 2031.

- By vehicle type, passenger cars captured 87.60% revenue share in 2025; light commercial vehicles are expanding at an 18.20% CAGR to 2031.

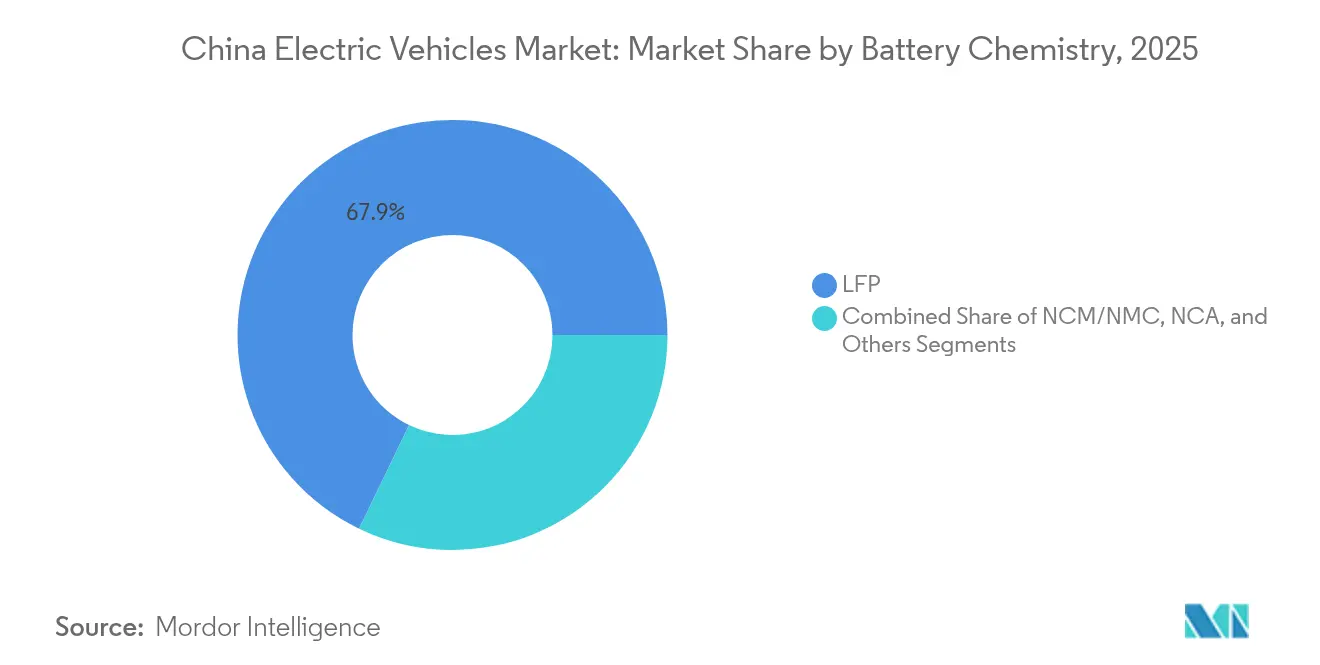

- By battery chemistry, LFP commanded a 67.85% share in 2025, whereas the other sub-segments are on track for a 33.20% CAGR through 2031.

- By price band, the USD 10,000 - 20,000 segment led with a 46.15% share in 2025; vehicles over USD 50,000 are projected to grow at a 21.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Electric Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PHEV Growth in Tier-2/3 Cities | +4.1% | Tier-2/3 cities, rural areas | Short term (≤ 2 years) |

| LFP Cost Parity With Small ICE Cars | +3.8% | National, strongest in price-sensitive segments | Short term (≤ 2 years) |

| NEV Tax Exemptions Extended to 2027 | +3.2% | National, with stronger impact in tier-2/3 cities | Medium term (2-4 years) |

| Fast-Charge & Battery-Swap Corridor Expansion | +2.8% | National, concentrated in major transportation corridors | Long term (≥ 4 years) |

| E-Freight Quotas Driving LCV Demand | +1.9% | Major metropolitan areas, logistics hubs | Medium term (2-4 years) |

| V2G Tariffs Unlock Grid Revenue | +1.5% | Pilot cities, expanding to provincial level | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended NEV Purchase-Tax Exemptions to 2027

Tax-free status worth USD 1,390-4,175 per vehicle cushions the post-subsidy transition and keeps entry-level pricing competitive. Tier-2/3 customers react strongly to this saving, and one-third of 2024 NEV sales leveraged the exemption plus trade-in incentives. Predictable policy horizons let automakers schedule capacity ramps and mid-cycle refreshes, particularly for mid-market crossovers driving the volume of China's electric vehicles.

Nationwide Fast-Charging & Battery-Swap Corridor Build-Out

Public charging points rose drastically over the past few years, while CATL and Sinopec are placing 500 battery-swap stations capable of two-minute exchanges. Highway coverage now spans 60% of service areas, and 57% of chargers remain clustered within 15 cities, signalling headroom in western provinces. The twin-track infrastructure strategy addresses commuter top-up needs and fleet uptime demands, underpinning confidence in the Chinese electric vehicle market.

PHEV Surge in Tier-2/3 Cities on Fuel-Savings Appeal

PHEV deliveries jumped over 80% in 2024 as consumers embraced BYD Qin L-level pricing below USD 16,700. Dual-fuel flexibility mitigates limited charging access and lowers the total cost of ownership. Research shows buyers outside tier-1 metros rank operating savings above environmental factors, making PHEVs the pragmatic bridge toward full electrification.

Municipal E-Freight Quotas Boosting Electric LCV Demand

Cities restrict diesel van access during peak hours, propelling electric LCV registrations exceeding 38,000 units in 1H 2024. Battery-swap vans leverage CATL’s two-minute module change to maximise route density. Fleet operators benefit from battery-as-a-service contracts that transfer residual-value risk, solidifying the Chinese electric vehicle market’s commercial pillar.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy Phase-Out Slows Upgrade Cycles | -2.7% | National, stronger impact in price-sensitive segments | Short term (≤ 2 years) |

| Lithium Price & Export Volatility | -1.8% | Global supply chain, domestic battery production | Medium term (2-4 years) |

| NEV Quality Concerns Impacting Loyalty | -1.6% | National, stronger impact on premium segments | Short term (≤ 2 years) |

| Provincial Caps on Underused Chargers | -1.2% | Provincial level, particularly in oversupplied regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Phase-Out of Central Subsidies Slowing Upgrade Cycles

The December 2022 subsidy sunset trimmed purchase incentives by RMB 1,670-2,780, elevating price sensitivity in mid-market sedans. Automakers countered with rebates and regional trade-in schemes, yet replacement intervals lengthened. As battery input costs drop, reliance on direct subsidies is expected to fade, restoring natural replacement rhythms within the Chinese electric vehicle market.

Lithium-Carbonate Price & Export-Control Volatility

An 80% price plunge to roughly USD 13,000/ton relieved near-term cost pressure but highlighted sourcing risk, with China importing 83.65% of its lithium feedstock. Export-control threats from Australia and Chile complicate multi-year procurement contracts, pushing cell makers toward sodium-ion and iron-rich chemistries less exposed to lithium swings.[1]“Lithium-Carbonate Price & Export-Control Volatility,” Oxford Institute for Energy Studies, oxfordenergy.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drivetrain Type: PHEV Momentum Challenges BEV Leadership

Battery electric vehicles led 2025 deliveries with a 57.72% share, anchoring the China electric vehicle market size for that year. Plug-in hybrids, however, are forecast to post a 20.88% CAGR to 2031, narrowing the gap as infrastructure diffuses inland. Dual-fuel flexibility makes PHEVs the preferred bridge tech for drivers facing sparse chargers.

Continued BEV cost erosion keeps fully electric models appealing in subcompacts and taxi fleets, yet PHEV growth in family SUVs and rural sedans diversifies the powertrain mix. Manufacturers, therefore, hedge across architectures, while solid-state programs target the post-2030 premium BEV wave.

By Vehicle Type: Commercial Electrification Accelerates

Passenger cars captured 87.60% of China's electric vehicle market share in 2025, but light commercial vans are rising on an 18.20% CAGR trajectory. Municipal zero-emission quotas, hub-and-spoke logistics, and battery-swap economics make electric LCVs a reliable fleet asset.

SUVs show 14.85% CAGR as consumers trade up for cabin space, and bus operators refresh diesel fleets under local low-emission mandates. Commercial adoption reinforces battery demand curves and broadens China's electric vehicle market size beyond private mobility.

By Battery Chemistry: Sodium-Ion Disruption in Sight

LFP retained 67.85% dominance in 2025, cementing cost leadership for the Chinese electric vehicle market. Other sub-segments are scaling at 33.20% CAGR, with CATL sodium-ion battery prototypes hitting 160 Wh/kg. Abundant raw sodium and simplified supply chains hedge lithium exposure, suiting entry-level hatchbacks and delivery vans.

NCM chemistry maintains its foothold in performance sedans, yet faces cost headwinds. Solid-state roadmaps aiming for 500 Wh/kg by 2027 could recalibrate density benchmarks in luxury crossovers and intercity coaches.

By Price Band: Mid-Market Strength Amid Premium Uptake

The USD 10,000-20,000 price bracket captured 46.15% of total EV sales volume in 2025, highlighting it as the most concentrated segment of China's electric vehicle market. Meanwhile, the above-USD 50,000 category is expanding at a 21.50% CAGR, driven by demand from urban commuters and ride-share programs. EVs priced between USD 30,000-50,000 are growing at a 14.20% CAGR, supported by rising interest in advanced driver-assistance features and premium branding.

Price compression, average retail tags fell 19% in two years, reflects capacity expansion and battery cost declines. Makers now align trim ladders carefully to defend branding while satisfying price-sensitive contexts.

Geography Analysis

Eastern and southern provinces remain powerhouses, yet penetration drifted marginally as hinterland sales accelerated. Tier-1 cities reached NEV penetration above 70%, sustained by dense infrastructure, restrictive license-plate quotas for ICE cars, and affluent buyers. The Chinese electric vehicle market now gains incremental volume in tier-2/3 locales, where PHEVs bridge charging gaps and rural promotion campaigns seed adoption.

Infrastructure is still uneven; 57% of chargers cluster in 15 megacities. Government programs fund corridor coverage, and county-level battery-swap rollouts by NIO promise availability across 2,844 counties. High-speed rail access unexpectedly boosts EV confidence by shortening intercity journey times that otherwise magnify range anxiety.

Export manufacturing concentrates in coastal hubs, shipping 1.284 million NEVs to 160 markets in 2024. Interior provinces court supply-chain investments, integrating battery, motor, and electronics plants into local industrial revitalisation. Varied provincial incentives, from parking rebates to electricity discounts, shape localised adoption curves but collectively extend the China electric vehicle market reach nationwide.

Regulatory Landscape

China's EV regulatory environment is tightening around eligibility, efficiency, and safety compliance while maintaining national incentives through a clearer technical filter. Starting January 1, 2026, new NEV models seeking purchase-tax exemption must meet updated technical requirements, including passenger-car energy consumption limits referenced in GB 36980.1-2025, and aligned requirements tied to newer national standards such as GB 19578-2024, GB 20997-2024, and GB 30510-2024. This links fiscal benefits more directly to measurable vehicle performance and standard compliance rather than simple drivetrain classification.

On the manufacturing side, the Ministry of Industry and Information Technology (MIIT) released revised Road Motor Vehicle Production Enterprise and Product Access Review Requirements in January 2026 to streamline access procedures while maintaining entry barriers for non-compliant products. In parallel, national standards updates raise the compliance baseline: GB 18384-2025 (electric vehicle safety requirements) and GB/T 38775.9-2025 (wireless charging system communication protocols) are implemented starting July 1, 2026. Regulatory pressure also increases through credit targets, with NEV credit percentage requirements set at 48% for 2026 and 58% for 2027, reinforcing OEM portfolio electrification and compliance investment.

Value Chain Analysis

China's EV value chain is characterized by deep vertical integration at leading OEMs and battery makers, with a dense midstream ecosystem spanning cells, packs, drive motors, power electronics, and software stacks. Battery supply remains a core determinant of cost and availability, with LFP at the center of mass-market competitiveness, and major players such as BYD (FinDreams) and CATL holding dominant positions across power batteries and related electrification modules. At the component level, supplier installation rankings through January to November 2025 show rising OEM self-supply, with automakers such as Tesla and Leapmotor appearing among top suppliers in selected electrification categories, signaling a continued shift of value capture from tier suppliers toward OEM-controlled designs.

Downstream, distribution and infrastructure are increasingly intertwined with the vehicle proposition through fast-charging corridors and battery swapping, supporting both consumer adoption and commercial uptime. Export logistics and overseas channel build-out are also reshaping the chain: China produced about 70% of the world's electric cars and over 80% of global battery cell output in 2025, and CAAM reported that monthly vehicle exports exceeded 1 million units for the first time in 2026, with NEVs accounting for over half (523,000 units). Policy and cost conditions are feeding back into the chain as well, including an April 2026 announcement of reduced export tax rebates, which affects export economics and encourages further manufacturing efficiency, localization of key inputs, and higher value-added configurations (for example, integrated e-drive systems and advanced charging architectures).

Competitive Landscape

Roughly 90 brands contest the arena, but the top 10 capture the majority of sales, indicating moderate consolidation pressure. BYD leads from the forefront, leveraging end-to-end battery-to-car integration and 30% promotional discounts to defend its share. SAIC-GM-Wuling retains micro-EV leadership, Tesla sustains premium mindshare, and Huawei’s platform strategy lets multiple partners deploy Harmony cockpit software rapidly.

Three playbooks dominate. First, vertically integrated players such as BYD internally manage cells, packs, and semiconductors. Second, technology alliances—Huawei-Seres and Xiaomi-BAIC—share electronics stacks, shortening the time to launch. Third, modular vehicle platforms allow legacy makers like Geely to amortise R&D across sub-brands.

Margins have tightened to 5%, the lowest in a decade, magnifying the survival stakes. Differentiation leverages fast-charge breakthroughs, 2-minute battery swaps, and Level-2+ driver assistance standardisation. Rising defect rates flagged by J.D. Power propel quality-control investments, advantaging firms with mature supply-chain monitoring. Choco-Swap, CATL’s open battery-swap standard, allied with 100 partners, illustrates how ecosystems play can create fresh revenue pools beyond unit sales and influence the future structure of the Chinese electric vehicle market.[3]“Choco-Swap Ecosystem Launch,” Contemporary Amperex Technology Co. Limited, catl.com

China Electric Vehicles Industry Leaders

BYD Company Ltd

SAIC Motor Corporation Limited

Geely Auto Group

Tesla Inc.

Changan Automobile

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Infrastructure-led differentiation is opening a new competitive lane beyond vehicle pricing, particularly around ultra-fast charging and integrated energy services. BYD's March 2026 unveiling of its 2nd Generation Blade Battery and FLASH charging technology, alongside a stated target of 20,000 domestic flash-charging stations by end-2026, highlights the opportunity for OEMs and charging-network partners to monetize high-throughput corridors, raise utilization, and reinforce brand stickiness in dense urban clusters. Similar whitespace remains in less-served geographies as charging is still concentrated, with 57% of chargers clustered in 15 cities, creating room for inland rollout strategies that pair PHEVs as a bridge with expanding fast-charge and swap coverage.

Battery-chemistry diversification is another opportunity area, driven by lithium exposure and the need to keep entry price bands competitive while improving range and charging performance. The market is already anchored by LFP (67.85% share in 2025), but 2026 product signals show parallel tracks: Chery's March 2026 Rhino Battery S-series announcement (including a solid-state concept with 1,500 km range) supports premium range-and-performance positioning, while SAIC's May 2026 launch of the MG 4X with semi-solid-state battery technology indicates nearer-term commercialization routes. Policy also creates targeted whitespace in certain subsegments: a July 2026 Ministry of Finance/MIIT announcement stated that from January 1, 2027, annual vehicle and vessel tax exemptions will end for plug-in hybrids, range-extended hybrids, and commercial battery-electric vehicles (while passenger BEVs and fuel-cell vehicles remain exempt), encouraging OEMs and fleet operators to reassess model mix, total-cost-of-ownership packaging, and battery-as-a-service or swap-based operating models for commercial applications.

Recent Industry Developments

- July 2026: BYD announced a restructuring of its overseas brand operations, consolidating Dynasty and Ocean under the BYD brand while aligning Denza and Fang Cheng Bao under shared operations and keeping Yangwang independent. The move simplifies go-to-market execution across regions and supports scale efficiencies in marketing, retail, and aftersales as Chinese EV makers prioritize exports and overseas presence.

- April 2025: CATL and Sinopec initiated construction of 500 battery-swap stations designed for two-minute exchanges. The build-out expands swap availability for high-uptime use cases such as fleets and logistics, strengthening battery-as-a-service economics and reinforcing swapping as a parallel refueling pathway alongside fast charging.

- December 2024: CATL unveiled the Choco-Swap ecosystem with nearly 100 partners, targeting 30,000 swap sites by 2030. By promoting an open standard and partner-led rollout, the initiative supports interoperability and accelerates network effects that can influence vehicle platform choices and residual-value assumptions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the China electric vehicles market is measured as the value of electric vehicle sales within China, counted at the vehicle level in USD, and aligned to annual registration and sales activity for passenger and commercial EVs.

Scope exclusions: This sizing does not include charging infrastructure, standalone batteries, or wider mobility services unless they are embedded in the vehicle selling price.

Segmentation Overview

- By Drivetrain Type

- Battery Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Fuel-cell Electric Vehicles

- By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV

- MPV

- Commercial Vehicles

- Light Commercial Vehicles

- Buses & Coaches

- Medium & Heavy Trucks

- Passenger Cars

- By Battery Chemistry

- LFP

- NCM/NMC

- NCA

- Others

- By Price Band

- Less than USD 10,000

- USD 10,000 - 20,000

- USD 20,000 - 30,000

- USD 30,000 - 50,000

- Over USD 50,000

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting structure of the model and to keep assumptions tied to trackable data series. We rely on public statistical releases and policy updates to understand how EV registrations, model mix, and supply conditions are changing each year, and then the demand pool is rebuilt from those signals.

Key references include sources such as the China Association of Automobile Manufacturers (CAAM), China Passenger Car Association (CPCA), and Ministry of Industry and Information Technology (MIIT) notices and catalogs. We also review definitions and benchmark data from organizations such as the International Energy Agency (IEA) and UNECE when they help us cross-check EV terminology and penetration patterns. In addition, company annual reports, investor presentations, and reputable press coverage are used for practical context, and a paid subscription for company financials and intelligence supports quick consistency checks on revenue and pricing narratives. The sources listed here are illustrative only, and many other public references were also used to collect data, validate assumptions, and clarify definitions.

Primary Interviews and Surveys

Primary work is used to confirm what the numbers mean on the ground, especially when pricing, mix shifts, or policy timing makes the secondary trail look inconsistent. We speak with OEM and supplier-side roles, channel and fleet stakeholders, and industry advisors across China, and we also validate how China-made EVs are being priced and reported when exports affect model assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | |

| Mid tier: 50% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where annual China EV sales volumes are reconstructed using registration and industry shipment series, which are then converted to value using an average selling price (ASP) curve that is updated for mix and price band movement. To keep the number realistic, we corroborate totals through selective bottom-up approximations, such as sampling model-level pricing, applying typical discount ranges seen in the market, and checking implied revenue patterns against aggregated OEM and supplier financial signals.

A few inputs that matter most in this market include NEV penetration in total light vehicle sales, the passenger versus commercial split, BEV versus PHEV mix changes, battery chemistry shifts that influence vehicle pricing, and the pace of price cuts across mass and premium bands. Where data gaps exist for smaller commercial formats or niche drivetrains, proxy shares are derived from observed registrations and then re-tested in expert discussions before finalizing.

Forecasting is run using scenario analysis supported by a simple regression overlay, where unit growth and ASP movement are linked to variables like total auto demand, policy direction, charging availability trends, and battery cost direction. Assumptions are kept straightforward so the forecast can be re-run quickly when a policy change or a price reset materially shifts the market path.

Data Validation & Update Cycle

Outputs are validated by comparing implied unit volumes and ASPs against independent signals, such as annual registration totals, public delivery statements, and broad pricing movements across major vehicle categories. When a jump in value is observed, it is traced back to a unit change, a mix shift, or an FX conversion effect, and then the underlying inputs are adjusted if the explanation does not hold.

Before sign-off, the model is reviewed in multiple analyst passes, and re-contact triggers are used when a key input moves outside expected bounds, such as a sharp ASP reset or an unexpected penetration swing. Reports are refreshed annually, with interim updates for material events, and before delivery an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's China Electric Vehicles Ev Market Outlook Market Size Compared With Other Published Estimates

Published market sizes for China EVs can look far apart because the boundaries are not always the same, and pricing plus currency timing can be handled differently. Even when the same year is quoted, the number can shift if one source uses list prices, another uses transaction price averages, and a third adds ecosystem revenue that sits outside vehicle sales.

The largest gap drivers in this market are whether plug-in hybrids are counted in the same way, whether exports are blended into a China market view, and how the ASP is updated during periods of rapid price cuts. When FX conversion is taken at a different point in the year, USD values can move meaningfully, so refresh timing matters. By re-checking ASP movements and FX timing close to publication and reconciling totals back to unit and registration signals, Mordor Intelligence arrives at a vehicle-sales-only value that will not match broader ecosystem tallies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 357.98 B (2025) | |

| Advisory Firm A | USD 380.00 B (2025) | Often expands scope beyond vehicle sales by attributing parts of charging, services, and other ecosystem value to EVs, and may also blend in export-linked revenue, which lifts the total versus a vehicle-only view. |

| Data Publisher B | USD 377.72 B (2025) | Commonly combines EVs with charging infrastructure in one value pool, where category roll-ups can inflate totals if vehicle revenue and infrastructure spend are not separated consistently year to year. |

Taken together, the spread mostly comes from scope and refresh timing rather than a disagreement on China EV adoption itself. Our model stays traceable because unit volumes, mix, and ASP steps are shown clearly, and the total is cross-checked against independent demand and pricing signals before final sign-off.

Key Questions Answered in the Report

What is the current size of the Chinese electric vehicle market?

The Chinese electric vehicle market was USD 418.08 billion in 2026 and is projected to reach USD 908.9 billion by 2031.

Which drivetrain segment is growing fastest?

Plug-in hybrid electric vehicles are expected to record a 20.88% CAGR through 2031, the highest among powertrains.

How dominant is BYD in China’s electric vehicle landscape?

BYD held majority of national EV sales in 2024, leading a top-five cohort that collectively controls about majority of the market.

What role do battery-swap stations play?

Battery-swap networks from CATL, NIO, and partners promise two-minute exchanges that minimise downtime, which is especially valuable for logistics fleets.

Why are PHEVs popular in tier-2 and tier-3 cities?

They offer fuel savings and long-range flexibility where public charging remains sparse, aligning with cost-conscious buyers outside major metros.

Page last updated on: