Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

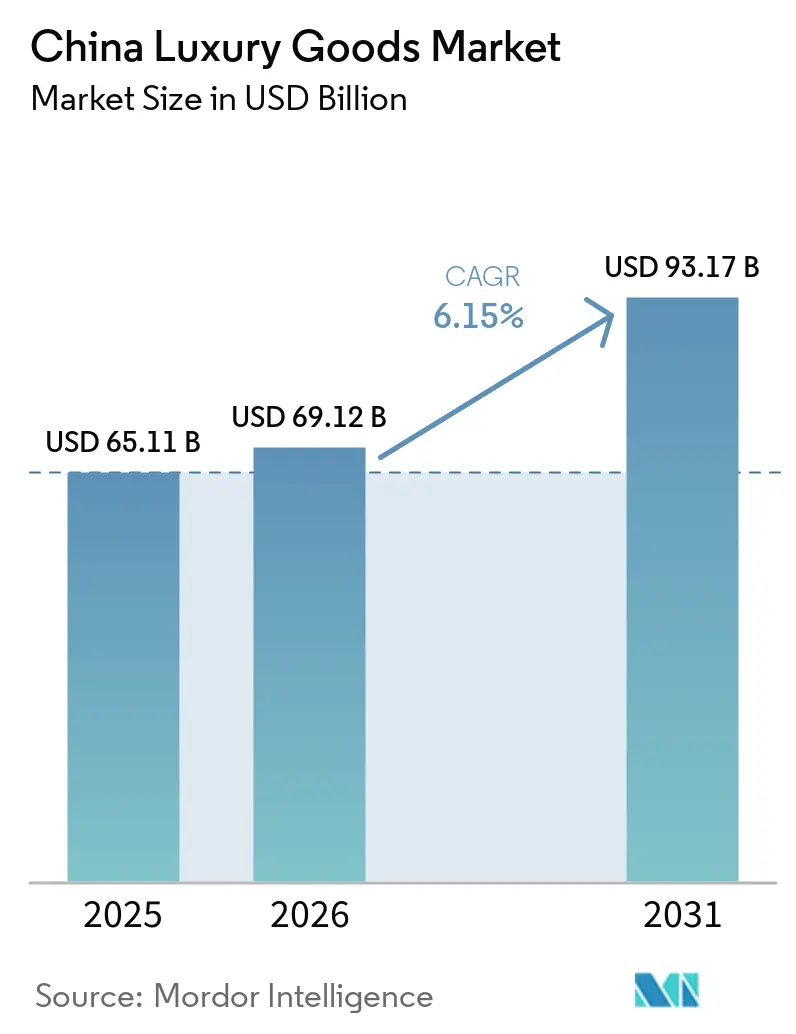

| Base Year Market Size (2025) | USD 65.11 Billion |

| Market Size (2026) | USD 69.12 Billion |

| Market Size (2031) | USD 93.17 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Luxury Goods Market Analysis by Mordor Intelligence

The China Luxury Goods Market size was valued at USD 65.11 billion in 2025 and estimated to grow from USD 69.12 billion in 2026 to reach USD 93.17 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031). The market growth is driven by a growing middle-class population, increasing disposable incomes, and evolving consumer preferences toward premium products. Chinese millennials and Gen-Z consumers have emerged as key demographics, demonstrating strong brand loyalty and embracing digital shopping experiences. The market encompasses traditional luxury categories such as fashion, accessories, and jewelry, while witnessing substantial growth in emerging segments like luxury experiences, personalized services, and sustainable luxury products. International luxury brands are expanding their physical presence through flagship stores and boutiques while developing comprehensive online channels to capitalize on e-commerce demand. The market benefits from government policies promoting domestic consumption and reduced import tariffs on luxury goods. Companies are focusing on product innovation in terms of raw materials and design, while meeting growing demand for sustainable high-end materials. The expansion of e-commerce platforms and digital retail channels, combined with aggressive marketing strategies by established brands, continues to shape the market landscape.

Key Report Takeaways

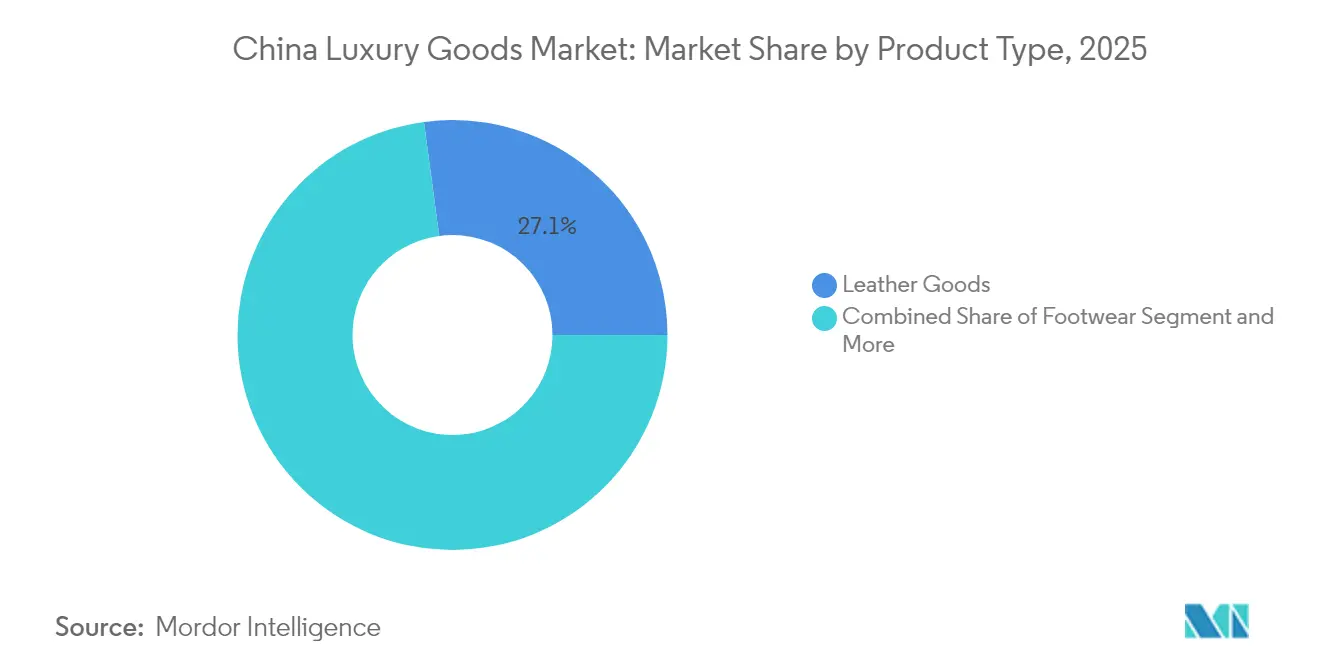

- By product type, leather goods held 27.12% of the China luxury goods market share in 2025, whereas beauty and personal care is poised to grow the fastest at a 5.52% CAGR through 2031.

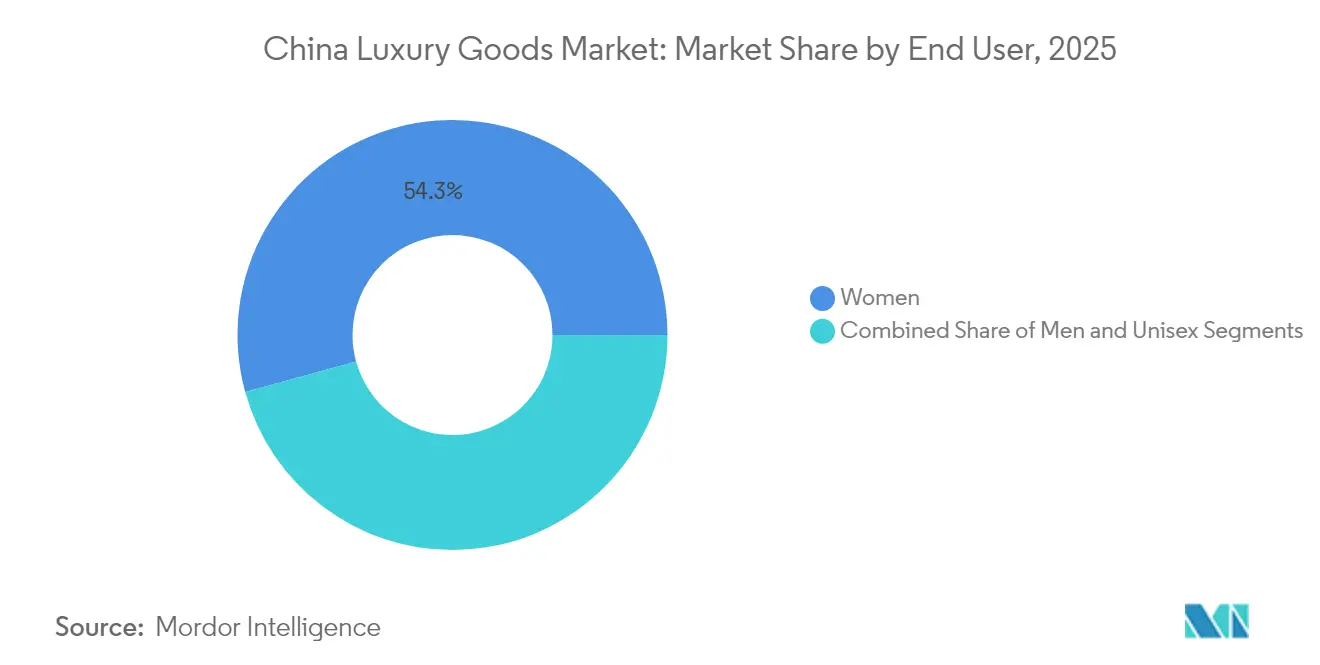

- By end user, women accounted for 54.28% of the China luxury goods market size in 2025, while the men’s segment is expanding at a 5.72% CAGR between 2026-2031.

- By distribution channel, offline stores captured 78.95% of China luxury goods market share in 2025, yet online channels are projected to scale at a 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic expansion by foreign brands | +1.8% | Tier 1 dominance with widening Tier 2-3 presence | Medium term (2-4 years) |

| Growing demand for sustainable high-end materials | +1.2% | Coastal provinces lead nationwide adoption | Long term (≥4 years) |

| Aggressive marketing by reputed brands | +1.5% | Digital-first regions nationwide | Short term (≤2 years) |

| Product innovation in raw material and design | +1.7% | Major metropolitan areas | Medium term (2-4 years) |

| Rapid expansion of e-commerce and digital retail | +2.1% | Strongest in Tier 2-3 cities | Short term (≤2 years) |

| Government policies that spur domestic spending | +1.4% | National; duty-free hubs such as Hainan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strategic expansion by foreign brands

International luxury brands are strategically expanding their presence in China through multiple initiatives, including increasing their retail footprint in tier-1 and emerging tier-2 cities. These companies are strengthening their digital presence through omnichannel strategies while developing China-exclusive collections through collaborations with local designers and artists. The establishment of regional headquarters and distribution centers in China enables these brands to improve their operational efficiency and market responsiveness. The companies are also implementing localized marketing campaigns and advanced customer relationship management systems to better understand and serve Chinese consumers. This concentrated focus on the Chinese market reflects its significant growth potential and increasing consumer sophistication. In December 2024, Balenciaga demonstrated this commitment by launching its largest global flagship store in China, featuring a minimalist, futuristic design that echoes the brand's raw architecture concept. These strategic expansions position luxury brands to capitalize on the evolving luxury goods market.

Growing demand for sustainable high-end materials

The increasing focus on sustainability in China's luxury market has emerged as a significant growth driver, particularly among younger consumers who are actively reshaping consumption patterns. Chinese luxury consumers demonstrate a strong preference for environmentally responsible products and show willingness to pay premium prices for sustainable offerings. This market evolution has prompted luxury brands to adapt their strategies by incorporating sustainable materials and establishing transparent supply chains. The transformation is exemplified by initiatives such as Kering's February 2024 collaboration with Tsinghua University and Institut Français de la Mode (IFM) to launch a Massive Open Online Course focused on sustainable fashion practices[1]Source: Kering, “Kering Collaborates with Tsinghua University and IFM to Launch Sustainable Fashion MOOC,” kering.com. The integration of environmental responsibility into luxury products has become fundamental to Chinese consumers' perception of quality and exclusivity, making sustainability a crucial factor in purchasing decisions within the country's luxury goods market landscape.

Rapid expansion of e-commerce platforms and digital retail channels

The rapid expansion of e-commerce platforms and digital retail channels in China significantly drives the luxury goods market growth, with consumers increasingly preferring online platforms like Tmall Luxury Pavilion, JD.com for luxury purchases. These digital platforms enhance the shopping experience through personalized services, virtual try-ons, and exclusive online collections. The integration of social commerce and livestreaming has enabled luxury brands to connect with younger consumers through real-time interactions, driving sales growth. According to the National Bureau of Statistics of China, online retail sales grew by 9.8% in the first half of 2024, highlighting the accelerated digital transformation of China's luxury retail landscape[2]Source: National Bureau of Statistics of China, “Total Retail Sales of Consumer Goods Increased by 9.8 Percent in the First Half of 2024,” stats.gov.cn. The government's support for digital commerce infrastructure has created an environment where luxury brands can effectively reach consumers across all city tiers, eliminating traditional geographic barriers to luxury consumption. This digital transformation of luxury retail in China represents a fundamental shift in how luxury brands engage with consumers and is expected to remain a key driver of market growth.

Government policies promoting domestic consumption and reducing import tariffs on luxury goods

The Chinese government has implemented comprehensive policies to stimulate domestic luxury consumption, with the Central Economic Work Conference emphasizing expanding demand and fostering new growth areas. The Ministry of Commerce's declaration of 2024 as the 'Year of Promoting Consumption' includes visa-free travel initiatives and enhanced support for duty-free shopping, particularly in Hainan. The establishment of International Consumption Centre Cities demonstrates a systematic approach to developing luxury retail infrastructure, with focused development of premium shopping destinations in Beijing, Shanghai, and other major cities. These policy initiatives aim to capture luxury spending that previously occurred overseas, reducing the outflow of purchasing power to international markets. According to China International Import Expo, duty-free sales in South China's Hainan Province grew by about 25% year-on-year to reach 43.76 billion yuan in 2023, driven by domestic travel recovery and local government stimulus measures[3]Source: China International Import Expo, “Hainan Duty-Free Sales Surge in 2023,” ciie.org. The government's coordinated efforts continue to strengthen China's position as a primary market for luxury consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -1.3% | Manufacturing hubs and tourist districts | Medium term (2-4 years) |

| Lesser demand from price-sensitive consumers | -1.5% | Lower-tier cities, younger cohorts | Short term (≤2 years) |

| Economic uncertainty and possible slowdown | -1.8% | Export-oriented regions | Short term (≤2 years) |

| Rising competition from premium domestic labels | -1.1% | Beauty, fashion, jewelry segments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

The widespread availability of counterfeit luxury goods poses a significant challenge to China's luxury market, with the country accounting for approximately 80% of global counterfeit production, according to World Trademark Review[4]Source: World Trademark Review, “China: Multi-Pronged Approach Proves Best Fit to Tackle Rise in Counterfeits,” worldtrademarkreview.com . China's extensive manufacturing capabilities and established distribution networks facilitate the production and sale of fake luxury items. Despite government efforts to combat counterfeiting through stricter regulations and enforcement measures, the market continues to be flooded with replicas of high-end brands. These counterfeit products impact the revenue of legitimate luxury brands and affect consumer trust and brand value. The presence of sophisticated counterfeits, often manufactured using similar materials and techniques, makes it difficult for consumers to distinguish between authentic and fake products. The lower price points of counterfeit goods attract price-sensitive consumers, particularly in tier-2 and tier-3 cities, leading to reduced sales of authentic luxury products. Furthermore, digital marketplaces facilitate grey market channels and parallel distribution networks, which undermine official sales networks and disrupt brand pricing strategies.

Lesser demand from price sensitive consumers

Economic uncertainty and inflationary pressures in China have significantly impacted consumer behavior in the luxury goods market, particularly affecting price-sensitive consumers and the emerging middle class. Despite rising disposable incomes, Chinese consumers are displaying increased caution in their spending patterns, prioritizing essential purchases and investment-oriented items over luxury goods. This shift is notably evident among young consumers aged 25-34, who are adopting more strategic purchasing behaviors, with many turning to gold products as a long-term savings strategy, as reported by the China Gold Association in 2024. The high price points of international luxury brands pose a substantial barrier, especially in lower-tier cities, leading consumers to either postpone high-value purchases or opt for more affordable domestic luxury alternatives. This price consciousness among potential consumers has created challenges for luxury brands, compelling them to reassess their pricing strategies and value propositions to maintain their market position in China.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product type: Leather Goods Lead while Beauty Accelerates

The China luxury market is dominated by leather goods, which holds a 27.12% share in 2025. This dominance stems from leather goods' perceived investment value and status symbol significance. The segment's strength is supported by China's established manufacturing infrastructure, expanding middle-class population, and rising disposable incomes. The market continues to grow through e-commerce integration and the established presence of domestic and international brands. Beauty and personal care is emerging as the fastest-growing segment with a projected CAGR of 5.52% (2026-2031), while watches and jewelry maintain substantial market share due to their value retention during economic uncertainty.

The guochao movement has significantly influenced luxury segments, particularly in clothing and apparel through the revival of traditional Hanfu clothing. Companies such as Shisanyu and Xiannixiaozhu have established themselves through their Hanfu designs. In response to increasing national pride and cultural confidence, luxury brands are incorporating Chinese design elements into their products. This cultural integration extends across all luxury categories, influencing product development in leather goods, beauty products, and other segments.

By Distribution channel: Online Growth Challenges Offline Dominance

Offline stores dominate the luxury watch market with a 78.95% share, as physical retail locations continue to serve as essential brand ambassadors by providing personalized experiences and allowing customers to interact directly with high-end products. These brick-and-mortar stores create immersive shopping environments that align with Chinese consumers' preferences for experiential luxury retail, maintaining their position as the primary sales channel. Physical stores remain crucial as they enable customers to experience the craftsmanship, quality, and prestige associated with high-end timepieces firsthand.

The integration of online and offline channels has become crucial, with the online segment growing at a CAGR of 6.18% (2026-2031). E-commerce platforms like Tmall and JD.com have established themselves as significant players through strategic brand partnerships and efficient delivery systems, while livestreaming has emerged as an innovative channel that combines entertainment, education, and sales to appeal to Chinese consumers. This omnichannel approach enables luxury watch brands to maintain their premium positioning while expanding their reach across multiple consumer touchpoints.

By End user: Women Dominate while Men's Segment Grows Faster

Women command a dominant 54.28% share of China's luxury market in 2025, driven by their increasing economic independence and elevated social status. Their purchasing decisions, particularly in high-end fashion, accessories, and cosmetics, are shaped by brand reputation, quality, and social status considerations, amplified by social media influence. While women prioritize refinement and brand heritage, men's luxury consumption focuses on projecting elite status, with the segment growing at a CAGR of 5.72% (2026-2031) as they diversify beyond traditional categories like watches and leather goods.

The evolving luxury market landscape in China reflects shifting gender dynamics and consumption patterns. The emergence of a unisex segment, driven by younger consumers embracing gender-fluid fashion trends, has prompted luxury brands to develop gender-inclusive product ranges and marketing strategies. This adaptation ensures brands remain relevant and responsive to the changing preferences of Chinese luxury consumers across gender segments. The market's transformation underscores the importance of understanding and catering to diverse consumer preferences while maintaining brand authenticity and exclusivity.

Geography Analysis

China's luxury market exhibits distinct regional characteristics, with Tier 1 cities maintaining their dominance while expanding into emerging markets. The government's establishment of International Consumption Centre Cities has created concentrated luxury hubs in Beijing, Shanghai, Guangzhou, and Shenzhen. Shanghai K11's 94% occupancy rate in 2024 and Guangzhou K11 Art Mall's 40% increase in foot traffic, according to New World Development report, demonstrate this trend. The National Bureau of Statistics reported urban retail sales of 20,455.9 billion yuan in the first half of 2024, up 3.6% year-on-year, with luxury goods contributing significantly to this growth in major metropolitan areas.

The expansion into Tier 2 and Tier 3 cities presents growth opportunities, driven by increasing purchasing power and government policies promoting consumption across urban centers. These cities benefit from digital commerce infrastructure that enables luxury brands to reach consumers regardless of their location, transforming the traditional city-tier hierarchy in luxury consumption. This geographic diversification strategy allows luxury brands to capture emerging consumer segments while maintaining their presence in established markets.

Hainan Province has become a vital part of China's luxury market through its duty-free shopping policies. The Ministry of Commerce has implemented visa-free travel initiatives and expanded duty-free shopping opportunities in the region. The Central Economic Work Conference's strategy to boost domestic demand includes measures to position Hainan as a competitive luxury shopping destination. These initiatives create a framework for geographical diversification of luxury consumption, allowing different regions in China to target specific market segments based on their unique economic and cultural characteristics. The strategic development of China's luxury market across various regions, from established Tier 1 cities to emerging markets and specialized zones like Hainan, demonstrates a comprehensive approach to market expansion that aligns with both consumer demands and government economic objectives.

Competitive Landscape

The China Luxury Goods Market exhibits moderate fragmentation, characterized by established international players competing with emerging domestic brands. The market dynamics showcase a strategic shift toward localization and cultural relevance, with international brands prioritizing store upgrades in key Chinese cities while domestic players strengthen their position through expanded retail presence and enhanced product offerings. This trend is exemplified by Rolex's October 2024 opening of its first directly operated boutique in China, enabling the brand to deliver consistent premium experiences and maintain greater control over brand presentation.

White-space opportunities have emerged at the intersection of technology and luxury, with Chinese consumers demonstrating willingness to pay premium prices for innovative features, including AI personalization. Digital engagement through platforms like Weixin has become essential for creating personalized shopping experiences and building customer relationships. The integration of technology serves as a critical competitive differentiator in the market.

The market landscape continues to transform through the rise of domestic brands leveraging the guochao trend, which celebrates Chinese cultural identity. These emerging disruptors have gained significant traction among younger consumers who increasingly favor local brands. Success in this evolving market increasingly depends on brands' ability to combine luxury heritage with technological innovation while maintaining cultural relevance to Chinese consumers.

China Luxury Goods Industry Leaders

LVMH Moet Hennessy Louis Vuitton SE

Chanel SA

Rolex SA

Hermès International SA

Prada Holding S.P.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tiffany opened its largest flagship store in China, a three-story space in Chengdu that expands the jeweler’s regional footprint.

- January 2025: Burberry launched a capsule line with artist Qian Lihuai, featuring open reticular weave gabardine designs incorporating the Burberry Check.

- November 2024: Manolo Blahnik debuted its first mainland China boutique, unveiling a capsule inspired by traditional aesthetics alongside core collections.

- May 2024: LVMH and Alibaba deepened cooperation to apply AI and cloud tools across Tmall Luxury Pavilion operations for improved consumer insight.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China luxury goods market as the value of new, premium-priced personal products, apparel, footwear, leather goods, jewelry, watches, eyewear, and prestige beauty, sold to final consumers within mainland China. Valuations exclude automobiles, real estate, upscale services, second-hand trading, and tourist purchases made outside the country.

Scope exclusion: Luxury experiences, cars, yachts, art, and duty-free sales outside the mainland stay outside our remit.

Segmentation Overview

- By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal Care

- By End User

- Men

- Women

- Unisex

- By Distribution Channel

- Offline Stores

- Online Stores

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview brand merchandisers, mall landlords, cross-border daigou agents, and logistics partners across Beijing, Shanghai, Shenzhen, Chengdu, and Hainan. These conversations validate average selling prices, online penetration rates, and inventory turns, while quick pulse surveys among Gen Z shoppers test sentiment around new-season collections and resale habits.

Desk Research

We begin with public domain cornerstones such as monthly retail sales releases from the National Bureau of Statistics, China Customs export-import sheets, and demographic income tables issued by the National Development and Reform Commission, which anchor spending pools. Trade bodies, including the China Chain Store & Franchise Association and the Gems & Jewelry Trade Association of China, supply category shipment or store count snapshots that fill important gaps. Company filings, IPO prospectuses, and Hong Kong exchange disclosures enrich brand-level price bands, while trusted media like Jing Daily and WWD trace product launches and channel shifts.

To refine inputs, we tap paid repositories when warranted. Dow Jones Factiva lets analysts quantify press-reported store rollouts, D&B Hoovers provides revenue splits for key players, and Questel flags recent patents that signal premium material innovation. The sources named illustrate our approach; many additional references underpin each datapoint collected, cross-checked, and stored in Mordor's internal library.

Market-Sizing & Forecasting

A top-down model reconstructs domestic spend from retail turnover, discretionary income per urban household, and luxury share of wallet, which are then stress-tested with sampled ASP times volume roll-ups for flagship brands to ensure bottom-up reasonableness. Key variables include per-capita disposable income, premium mall floor space, cross-border duty-free receipts, online luxury penetration, and counterfeit seizure trends; each signals shifts in demand or price realization. We forecast through a multivariate regression that links these drivers to historical sales and projects five scenarios before selecting the consensus path endorsed by interviewees. Where brand roll-ups under-report smaller city sales, calibrated uplift factors bridge the gap.

Data Validation & Update Cycle

Outputs face three rounds of analyst review, variance checks against Statista retail indices and customs totals, and anomaly resolution calls with field sources. Reports refresh every twelve months, with interim updates triggered by policy changes on import duties, pandemic restrictions, or currency swings.

Why Mordor's China Luxury Goods Baseline Stands Out

Published estimates often diverge because firms adopt different product baskets, price-mix assumptions, and refresh cadences.

Key gap drivers include whether grey-market daigou flows are counted, if services and automobiles creep into definitions, the treatment of VAT adjustments, and how quickly macro shocks are incorporated. Mordor's scope limits the basket strictly to personal goods bought inside China, and our annual refresh, as seen in the July 2025 edition, captures post-pandemic repatriation faster than peers.

In sum, our disciplined scope, driver-based model, and fast refresh give decision-makers a balanced baseline they can trace to transparent variables and replicate with publicly available data; qualities that, we believe, set Mordor Intelligence apart.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 65.11 B (2025) | Mordor Intelligence | - |

| USD 55.4 B (2022) | Regional Consultancy A | Older base year; excludes online channels |

| USD 40.77 B (2024) | Trade Journal B | Omits beauty and eyewear categories |

| USD 316.34 B (2024) | Global Consultancy C | Adds automobiles and luxury travel to basket |

In sum, our disciplined scope, driver-based model, and fast refresh give decision-makers a balanced baseline they can trace to transparent variables and replicate with publicly available data; qualities that, we believe, set Mordor Intelligence apart.

Key Questions Answered in the Report

What is the current size of the China luxury goods market?

The market is valued at USD 69.12 billion in 2026 and is projected to reach USD 93.17 billion by 2031 at a CAGR of 6.15% during 2026-2031.

Which product category holds the largest share in China’s luxury sector?

Leather goods lead with 27.12% of China luxury goods market share in 2025, reflecting strong investment appeal.

How fast is the online channel growing within China’s luxury landscape?

Online sales of luxury items are advancing at a 6.18% CAGR from 2026-2031, making it the fastest-growing distribution channel.

What demographic currently contributes most to luxury spending?

Women account for 54.28% of luxury purchases in 2025, although men’s spending is rising at a 5.72% CAGR.

What role do government policies play in the luxury market’s growth?

Reduced import tariffs, duty-free expansion, and the designation of International Consumption Centre Cities channel overseas spending back into domestic stores.

Page last updated on: