Automotive Blockchain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

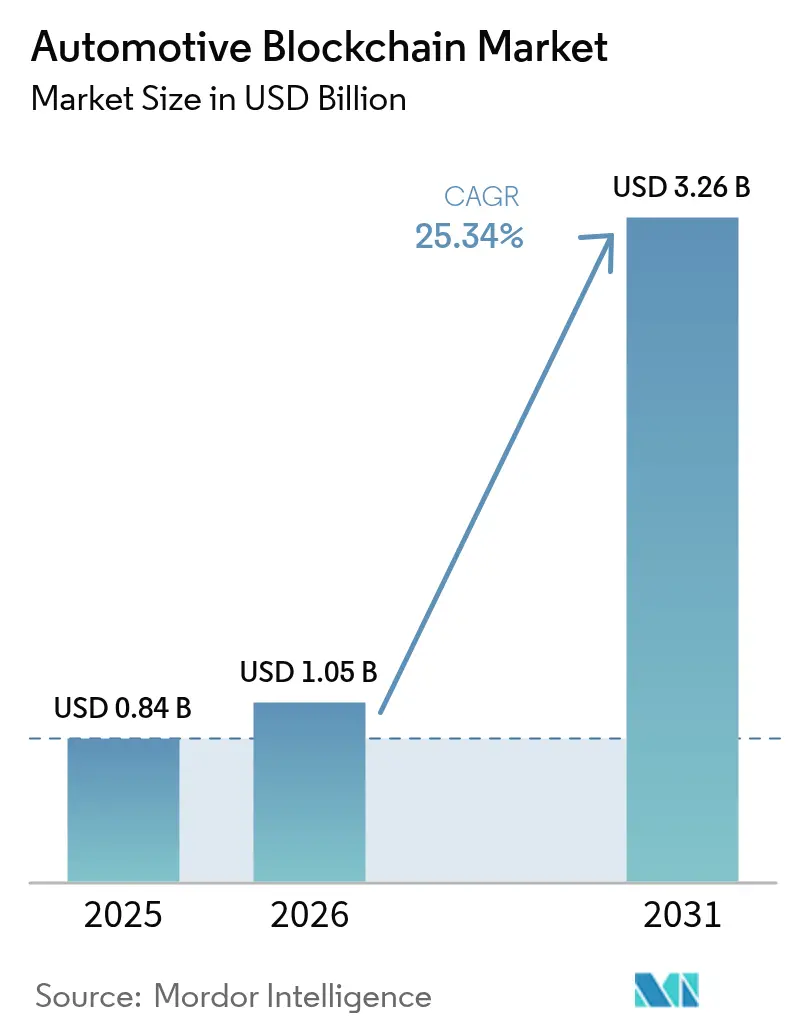

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 3.26 Billion |

| Growth Rate (2026 - 2031) | 25.34% CAGR |

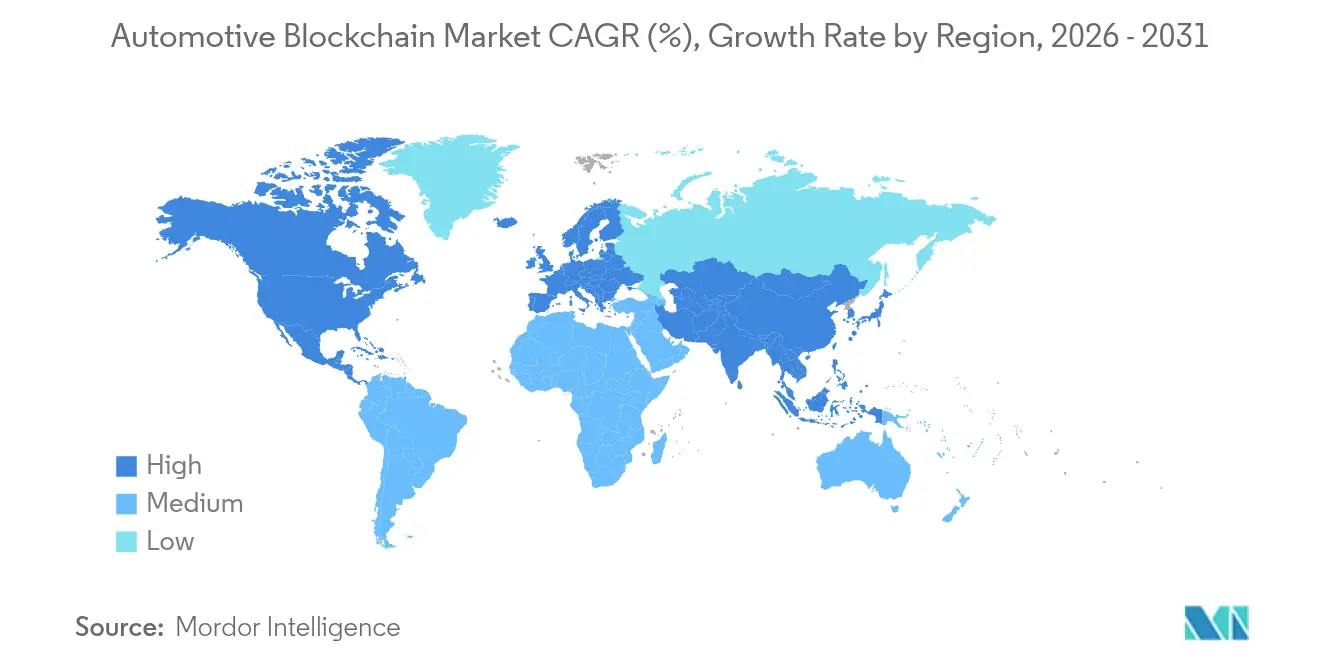

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Blockchain Market Analysis by Mordor Intelligence

The automotive blockchain market size is expected to grow from USD 0.84 billion in 2025 to USD 1.05 billion in 2026 and is forecast to reach USD 3.26 billion by 2031 at 25.34% CAGR over 2026-2031. The expansion mirrors the sector’s broad digitalization, where distributed ledgers solve long-standing gaps in parts provenance, data security, and compliance workflows. Heightened counterfeit-parts exposure, emerging battery-passport mandates, and the shift toward Web3 payment rails are accelerating enterprise pilots into large-scale rollouts. Automakers view the technology as a turnkey layer that links connected-vehicle data with real-time analytics, while regulators increasingly recognize distributed ledgers as the only scalable mechanism for end-to-end traceability. The automotive blockchain market also benefits from cross-industry synergies with energy trading and circular-economy schemes, enabling new revenue sources without overhauling existing hardware.

Key Report Takeaways

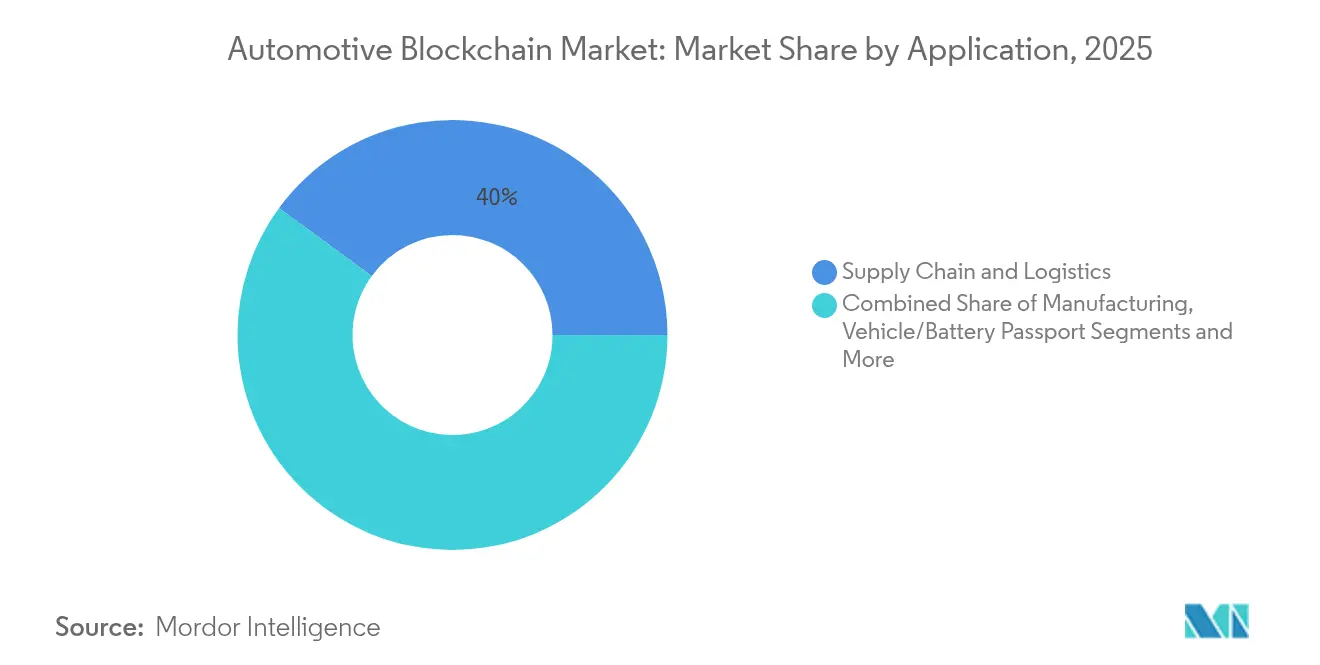

- By application, supply chain and logistics held 39.95% of the automotive blockchain market share in 2025, while vehicle and battery passport solutions are forecast to post a 30.12% CAGR to 2031.

- By end user, OEMs led with 43.72% revenue share in 2025; insurance companies are projected to grow at 28.33% CAGR through 2031.

- By blockchain type, private and permissioned networks commanded 48.22% of the automotive blockchain market share in 2025, whereas hybrid architectures are set for a 29.41% CAGR up to 2031.

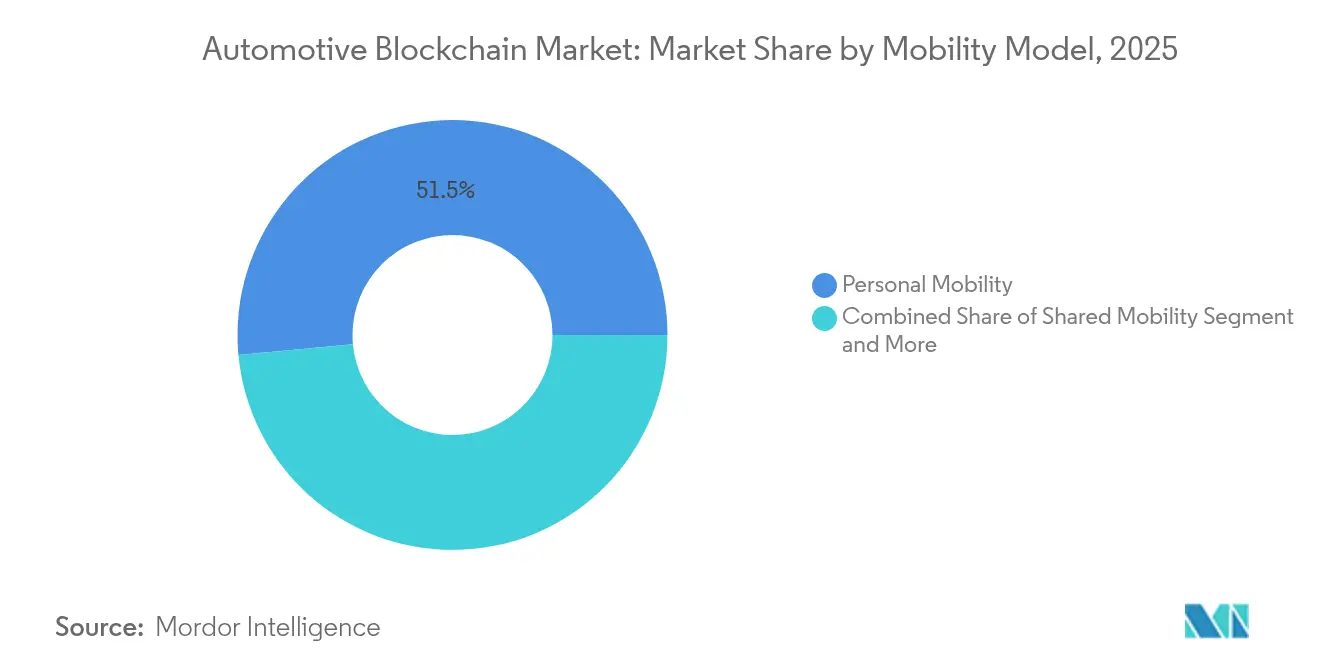

- By mobility model, personal-vehicle use cases accounted for 51.48% of the automotive blockchain market size in 2025, and shared-mobility applications are likely to accelerate at a 33.08% CAGR by 2031.

- By vehicle type, passenger cars represented 64.05% of the automotive blockchain market size in 2025; commercial vehicles are expected to expand at 36.87% CAGR between 2026-2031.

- By geography, North America captured 42.98% of the automotive blockchain market share in 2025, while Asia-Pacific is positioned to grow at 30.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Blockchain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery Passport Regulations for EV Provenance | +5.1% | EU mandatory by 2027, spillover to North America | Short term (≤ 2 years) |

| Supply-chain Transparency and Anti-counterfeit Push | +4.2% | Global, early in North America and EU | Medium term (2-4 years) |

| Connected and Autonomous-Vehicle Data Security Needs | +3.8% | North America and EU leading, APAC following | Long term (≥ 4 years) |

| OTA Software-update Liability Audit Requirements | +3.4% | Global, stricter in EU and North America | Medium term (2-4 years) |

| Web3 Vehicle-Wallet Micropayments Adoption | +2.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Circular-Economy Traceability Incentives | +2.7% | EU leading, gradual in North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Battery Passport Regulations for EV Provenance

The European Union’s 2027 battery passport rule makes blockchain indispensable for tracing every cathode, anode, and cell through a 15-year lifecycle. Volvo’s EX90 passport records cobalt origin, recycled content, and CO₂ output on a public-permissioned chain that meets anticipated EU audits three years early. Consultancy estimates place compliance spending at EUR 10–15 per passport, turning regulation into a service revenue stream for platform providers. Circulor’s selective-disclosure design shields sensitive supplier data while proving provenance to regulators. Spill-over effects reach North America, where California tax credits could hinge on comparable documentation, bolstering the automotive blockchain market penetration among U.S. EV brands.

Supply-chain Transparency and Anti-counterfeit Push

Blockchain-enabled traceability reduces the USD 45 billion annual counterfeit-parts risk by replacing manual paperwork with an immutable data layer that spans thousands of suppliers. Renault’s XCEED platform has already cut compliance-report processing time by 60% [1]“Renault’s XCEED Scales Compliance With Blockchain,” IBM, ibm.com. Catena-X links more than 150 firms into a shared provenance network that converts fragmented supplier exchanges into continuous, verifiable data flows. These initiatives demonstrate that a distributed ledger can preserve competitive confidentiality while revealing tamper-proof part histories to regulators and customers. The result is a structural drop in warranty claims and audit costs, factors that strengthen the automotive blockchain market outlook. Consensus around open standards within Catena-X further lowers onboarding friction for new tier-n suppliers.

Connected and Autonomous-Vehicle Data Security Needs

Connected vehicles create roughly 25 GB of data each hour, exposing OEMs to cyber risks estimated at USD 505 billion in potential losses by 2024. Decentralized authentication verifies data packets in milliseconds, removing central bottlenecks that compromise autonomous-driving safety. BMW’s patent filings confirm investment in blockchain-secured V2V protocols, anticipating regulatory endorsement of distributed trust models for Level 4 autonomy. Immutable logs also simplify incident forensics, a prerequisite as vehicles exchange critical manoeuvre data. As edge-computing costs fall, automakers integrate lightweight nodes directly into electronic control units, embedding blockchain deep inside the software-defined vehicle stack.

OTA Software-update Liability Audit Requirements

ISO 24089 obliges OEMs to document every over-the-air software patch, a task streamlined by immutable block sequencing [2]“ISO 24089: Road Vehicles – Software Update Engineering,” TÜV SÜD, tuvsud.com. Uptane’s security framework, built on blockchain concepts, prevents malicious code injection before an update reaches the vehicle. Regulators demand granular proof that safety-critical functions remain uncompromised, and distributed ledgers supply this audit trail without revealing proprietary firmware. Monthly update cadences make manual tracking impossible, forcing automation that cements blockchain as standard infrastructure. Liability clarity, in turn, lowers recall expenses and insurance premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scalability and Energy-Use Limits of Public Chains | -3.2% | Global, higher in energy-conscious regions | Short term (≤ 2 years) |

| Regulatory Uncertainty for Cross-Border Smart Contracts | -2.8% | Global, affecting multinational operations | Medium term (2-4 years) |

| Shortage of Automotive-Grade Blockchain Talent | -2.4% | Global, acute in North America and EU | Medium term (2-4 years) |

| OEM Intellectual-Property Leakage Concerns | -1.9% | Global, sensitive in competitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scalability and Energy-Use Limits of Public Chains

Ethereum’s 15 tps ceiling and Bitcoin’s 120 TWh annual consumption make public chains ill-suited for millions of vehicle transactions. Layer-2 rollups improve throughput but introduce new attack surfaces that compromise safety-critical workloads. OEMs, therefore, lean on private networks, accepting reduced decentralization in exchange for latency under 500 ms. This trade-off somewhat constrains the public-chain portion of the automotive blockchain market yet accelerates investment in consortium-grade proof-of-stake solutions.

Regulatory Uncertainty for Cross-border Smart Contracts

Divergent rules between the EU’s MiCAR framework and the United States’ state-level statutes create compliance friction that slows multinational deployments. Automakers must tailor smart-contract code to varying data-protection and financial-settlement laws, inflating project timelines. Liability for contract failures remains ambiguous across jurisdictions, exposing firms to unforeseen litigation. Many projects, therefore, segment networks by region, limiting the network-effect benefits that drive blockchain adoption. Harmonized standards are still five to seven years away, so in the interim, the automotive blockchain market relies on legal wrappers and selective-disclosure tooling to mitigate risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Supply Chain Dominance Drives Transparency Revolution

Supply-chain and logistics functions represented 39.95% of the automotive blockchain market in 2025, reflecting industry-wide urgency to authenticate parts and satisfy compliance filings. Immutable provenance records reduce warranty fraud and shorten recall look-up times. Vehicle and battery passports, while smaller today, register the fastest 30.12% CAGR because the 2027 EU mandates guarantee demand. Manufacturing, finance, insurance, and mobility-service niches each leverage the same ledger backbone but diverge in data-type requirements. The application mosaic signals that blockchain flexibility outweighs the additional implementation cost once multipurpose integrations begin.

Continuous data aggregation within supply chains unlocks predictive-maintenance alerts and environmental-footprint dashboards. Battery passport rollouts improve resale values by certifying remaining energy density, which feeds directly into loan underwriting. Insurance telematics delivers granular risk scores, lowering fraud losses and boosting margins. The automotive blockchain market size for vehicle and battery passport solutions is projected to widen as Asian governments consider copy-cat legislation. Supply-chain transparency therefore anchors today’s revenue while regulatory passports fuel future cycles.

By End User: OEMs Lead While Insurance Accelerates Adoption

OEMs held 43.72% of spending in 2025, underpinning the automotive blockchain market through multi-plant deployments that track inbound material and outbound vehicle data. Their leadership stems from direct accountability for recalls and regulatory filings. Insurers, expanding at a 28.33% CAGR, use smart contracts to automate claims and embed real-time risk pricing. Tier-1 suppliers join ledgers to remain preferred partners in OEM scoring programs that reward verified sustainability metrics.

Mobility-service operators rely on transparent smart-contract revenue splits, while dealerships authenticate parts to cut counterfeit incidences. Regulators and authorities view the same network as a compliance console, accessing tamper-proof logs without mandating additional reporting portals. The automotive blockchain market size captured by regulators grows in parallel with digital-title programs. Overall, diverse stakeholder engagement validates distributed-ledger return on investment far beyond the factory gate.

By Blockchain Type: Private Networks Dominate Despite Hybrid Growth

Private, permissioned chains claimed a 48.22% share in 2025 because access controls align with intellectual-property safeguards. These networks enforce deterministic transaction times critical for safety systems. Hybrid models expand at 29.41% CAGR by blending private-chain confidentiality with public-chain auditability. Consortium setups enable industry-wide metadata pools around shared pain points such as counterfeit mitigation. Public-chain uptake remains niche due to throughput limits, yet proof-of-stake upgrades may alter the calculus post-2026.

Interoperability layers bridge private and public instances, enabling single-source regulatory proofs while guarding commercial secrets. Energy-efficient consensus algorithms also reduce scope-3 emissions for sustainability disclosures. Consequently, hybrid adoption increases the automotive blockchain market share for mixed-architecture solutions . In the long term, governance frameworks may converge, making chain type a deployment detail rather than a strategic divider.

By Mobility Model: Personal Vehicles Lead While Shared Services Surge

Personal-vehicle use cases commanded 51.48% of revenue in 2025, mainly from ownership-record tokenization and maintenance-history vaults. Drivers appreciate immutable mile-per-mile service logs that lift resale prices. Shared-mobility platforms are sprinting at 33.08% CAGR because blockchain automates real-time vehicle allocation and revenue splits among operators, owners, and municipalities.

Commercial fleets adopt the technology for automated tolling and carbon reporting. Cross-model convergence appears as ride-sharing fleets adopt battery passports to verify pack health before secondary-life deployment. As urban policies promote usage over ownership, shared services will absorb a growing slice of the automotive blockchain market size, driving stakeholders toward interoperable identity and payment ecosystems.

By Vehicle Type: Passenger Cars Lead While Commercial Fleets Surge

Passenger cars accounted for 64.05% of the automotive blockchain market in 2025, reflecting their installed base and early integration of distributed-ledger tools. OEMs employ blockchain to authenticate parts, record warranty events, and tokenise ownership, creating immutable histories that raise resale values and simplify recall audits. Monthly firmware updates are now hashed, giving regulators tamper-proof confirmation that safety-critical functions remain intact.

Commercial vehicles are set to grow at a 36.87% CAGR through 2031 as logistics operators seek continuous compliance and cost savings. Smart contracts automate customs paperwork, toll reconciliation, and fuel-tax settlements, freeing fleet managers from administration. Immutable telematics logs verify cargo conditions, cutting insurance claims, while blockchain-certified emissions data secures green-freight contracts, accelerating adoption across high-utilization trucks and vans.

Geography Analysis

North America accounted for 42.98% of the automotive blockchain market revenue in 2025 as state authorities digitized 42 million vehicle titles using permissioned ledgers. Federal supply-chain security directives that restrict non-allied components reinforce blockchain as a mandated verification backbone. The region enjoys proximity between automotive OEM headquarters and leading cloud-blockchain providers, accelerating proof-of-concept timelines. Continuous funding from Detroit venture capital further supports start-ups specializing in niche ledger services.

Asia-Pacific is on a 30.18% CAGR trajectory through 2031, anchored by China’s 45% new-EV sales penetration and municipal blockchain development grants. Policies that permit Level 4 autonomy trials in more than 20 cities amplify demand for secure vehicle-to-everything communication protocols. South Korea and Japan have announced national autonomous-mobility roadmaps, channeling funds toward digital identity and compliance solutions. Regional battery-passport pilots ensure that local suppliers remain eligible for EU exports, reinforcing cross-continental market symbiosis.

Europe sustains momentum through binding battery passport rules that make blockchain compulsory by 2027. Germany legalized Level 4 autonomous driving in 2025, necessitating secure, tamper-proof software update records. The continent’s OEMs collaborate within Catena-X to create an open yet confidential data-exchange standard, lowering duplicated investments. Government grants and Horizon-Europe funding anchor research into quantum-safe ledger protocols, positioning Europe as a standards-setter within the automotive blockchain market.

Regulatory Landscape

Automotive blockchain deployments sit at the intersection of cybersecurity, traceability, and data-access rules that increasingly emphasize auditable, tamper-evident records rather than optional reporting. UN Regulation No. 155 (Supplement 3) entered into force on January 10, 2025, tightening type-approval expectations around cybersecurity management systems for vehicles (M, N, and O categories) and reinforcing the need for immutable logging across connected-vehicle software and supplier interfaces.

In Europe, compliance pressure extends from cybersecurity into data governance and product traceability. The EU Data Act becomes effective on September 12, 2025, shaping how vehicle data is accessed and shared, while the EU Digital Product Passport (DPP) Registry went live on July 19, 2026. The registry uses identifiers linked to HTTPS URLs, and blockchain is not mandated, although it can be used to anchor or attest supplemental provenance. Standards activity also influences implementation choices, including SAE AIR7123 (2025) guidance on blockchain-based Digital Authorized Release Certificates (DARC), supporting broader acceptance of distributed-ledger evidence in regulated quality and release workflows.

Value Chain Analysis

The value chain typically starts with standards, governance, and identity layers (consortia and specifications), then moves into platform and infrastructure providers (cloud, permissioned ledgers, DID/VC toolkits), and finally into systems integration and domain applications embedded in OEM and supplier processes. OEMs and Tier suppliers define the data model and access rules, often through permissioned or consortium setups. Technology providers supply ledger frameworks and hosting, while integrators connect blockchain services to ERP/MES, telematics, and compliance systems. Catena-X and related interoperability initiatives underline the importance of shared semantics and onboarding tooling for multi-tier supplier participation.

Downstream, application modules operationalize blockchain records for parts provenance, battery and vehicle passports, carbon accounting, and logistics visibility. In the current landscape, Hyundai and Kia use the Hedera-based IGIS platform for lifecycle emissions tracking, and Renault has scaled its XCEED compliance certification workflow. Newer deployments also show blockchain shifting beyond audit archives into operational logistics networks, including XPENG selecting Vinturas to deploy a private blockchain network for European distribution visibility. Supplier networks and material provenance programs, including permissioned DLT rollouts across broad Tier-1 bases, further reinforce the need for selective disclosure to protect IP and commercial terms.

Competitive Landscape

The market exhibits moderate concentration as legacy IT integrators jostle with blockchain-native scale-ups. IBM leverages its Hyperledger fabric and long-standing automotive contracts, evidenced by Renault’s compliance solution that integrates directly with existing MES systems. Microsoft and Accenture differentiate through cloud-agnostic toolkits that slot seamlessly into OEM ERP landscapes, reducing migration hurdles.

Specialists such as carVertical and Spherity focus on vehicle identity and battery passport micro-services, capturing OEMs that prefer modular architectures over monolithic stacks. Supply-chain giants Bosch and Continental now embed ledger nodes inside electronic control units, baking traceability deep into hardware. The result is a partnership web rather than winner-take-all dynamics, giving mid-tier vendors room to own narrow yet profitable niches.

Web3 entrants, including DIMO and Holoride, explore token-economy models where vehicle data custody yields direct driver rewards. Semiconductor providers such as SEALSQ collaborate with Hedera on quantum-resistant chips, locking in security at the silicon level. Over the next five years, client decision criteria will rotate toward talent availability and domain-specific privacy tooling rather than raw throughput, shaping an automotive blockchain market where integration skill often trumps ledger design.

Automotive Blockchain Industry Leaders

Microsoft Corporation

BigchainDB GmbH

IBM Corporation

Accenture plc

Tech Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-linked digital passports and interoperable data spaces create immediate whitespace for vendors that can package compliance-ready templates, identity, and selective-disclosure controls into deployable modules. The EU Battery Regulation (EU) 2023/1542 requirement for a unique Digital Battery Passport for EV and industrial batteries above 2 kWh starting February 18, 2027 is a concrete catalyst, and the February 2026 guideline from the Industrial Digital Twin Association (IDTA) and Catena-X on implementing a Digital Battery Passport using the Asset Administration Shell (AAS) indicates that standard-aligned implementations are turning into a procurement prerequisite rather than a technical preference.

Cross-border parts movement and supplier collaboration also create opportunities for blockchain-enabled assurance that combines packaging, logistics, and provenance evidence into a single chain of custody. Market activity points to this direction through XPENG and Vinturas implementing a private-blockchain-enabled solution for European supply chain visibility, as well as consortium pilots using blockchain-embedded packaging data to trace auto parts across international borders. In parallel, China-side ecosystem efforts such as the China Association of Automobile Manufacturers (CAAM) Vehicle Data Blockchain Platform (VDBP) highlight a second opportunity track focused on trusted vehicle-data exchange and settlement, where platforms compete on interoperability with OEM data governance and regulator-facing auditability rather than on public-chain decentralization.

Recent Industry Developments

- July 2026: Volvo Group began testing a proprietary cryptocurrency to support blockchain-based supplier transactions. The effort targets faster and more controlled settlement and reconciliation across multi-party supplier workflows, extending blockchain use from traceability into transactional supplier operations.

- June 2026: Accenture entered an engineering partnership with Coretura, a Daimler Truck and Volvo Group venture, to develop a software-defined commercial vehicle platform. The collaboration strengthens the ecosystem around secure software and data lifecycle management in commercial vehicles, where immutable audit trails and governed data sharing are increasingly central to compliance and operations.

- December 2024: Hyundai Motor Company and Kia Corporation launched the Integrated Greenhouse Gas Information System (IGIS), a blockchain-powered platform for lifecycle carbon emissions management. By anchoring emissions and LCA data with distributed-ledger integrity controls, the platform supports auditable sustainability reporting across multi-tier supply chains and accelerates broader adoption of blockchain-based compliance workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from blockchain solutions and related services that are implemented for automotive use cases, where distributed ledgers are used to record, share, and verify vehicle, parts, and transaction data across stakeholders.

Scope exclusions: Cryptocurrency trading, general enterprise blockchain spend not tied to automotive workflows, and purely experimental pilots without a commercial rollout are excluded.

Segmentation Overview

- By Application

- Manufacturing

- Supply Chain and Logistics

- Financing and Payments

- Insurance and Usage-Based

- Mobility Services

- Vehicle/Battery Passport

- Others

- By End User

- OEMs

- Tier-1 Suppliers

- Mobility-as-a-Service Providers

- Insurance Companies

- Vehicle Owners/Drivers

- Dealerships and Service Centers

- Regulators and Authorities

- By Blockchain Type

- Public Blockchain

- Private/Permissioned Blockchain

- Consortium Blockchain

- Hybrid Blockchain

- By Mobility Model

- Personal Mobility

- Shared Mobility

- Commercial and Logistics Fleet

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping the demand pool and the operating environment where blockchain is actually adopted in automotive programs. We referenced public source types such as NHTSA vehicle safety publications, US DOT logistics and freight indicators, Eurostat transport statistics, UNECE vehicle regulation frameworks, and WIPO patent databases to understand activity levels and where traceability and data integrity requirements are rising.

Next, we reviewed company filings, investor decks, press releases, and association websites to identify common commercialization patterns, pricing hints, and where spending is counted as software versus services. Where needed, a paid subscription for company financials and intelligence was used selectively to cross-check business mix statements and avoid double counting adjacent digital programs. The sources listed here are illustrative only, and many other public references were reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with solution providers, automotive ecosystem participants, and domain specialists who track connected vehicle data flows and supply chain traceability needs. Because this is a global market, we checked inputs across APAC, EMEA, and the Americas so adoption timing, pricing assumptions, and realistic deployment scale could be aligned before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 22% | Managers: 50% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the addressable automotive digitalization and traceability spend is reconstructed through adoption signals, then filtered to blockchain-specific deployments that are monetized in the market. The totals are cross-checked with selective bottom-up approximations, such as sampled program-level budgets, typical annual contract values, and an ASP times volume check for active deployments. This helped adjust for over-reporting in early stage announcements.

Key inputs in the model include connected vehicle penetration and data sharing intensity, supply chain traceability requirements for critical parts and batteries, number of vehicles produced and traded (used as a proxy for documentation and provenance needs), the share of workflows moving to smart contract based automation, and the services-to-software mix seen in commercial rollouts. When direct volume points were not available, gaps were handled using comparable deployment cohorts by region and by use case maturity, and then reviewed with interview feedback.

For forecasting, we used scenario analysis because adoption depends heavily on regulatory timing, OEM platform decisions, and the pace of ecosystem onboarding. Assumptions on adoption curves and price realization were stress-tested with expert views, and the final forecast reflects a base case that can be reproduced with transparent inputs.

Data Validation & Update Cycle

Outputs were validated through consistency checks against independent signals, such as vehicle production trends, cross-border trade activity, and the pace of connected services rollouts. Any sharp step changes in the model were flagged, reviewed, and then re-tested with an additional round of expert follow-ups when needed.

Before sign-off, the full model goes through multi-step analyst review so assumptions, math, and scope boundaries are aligned end to end. The report is refreshed annually, and interim updates are triggered when material events shift the adoption outlook, such as major regulatory moves or widely scaled deployments. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Automotive Blockchain Market Estimate Compared With Other Published Estimates

Published market sizes for automotive blockchain can look different even when everyone is discussing the same theme, since the counted revenue boundary is not always the same. In our checks, the biggest swings usually come from what is treated as blockchain revenue versus broader connected vehicle software, and how services, pilots, and platform spending are treated.

Vehicle production and cross-border parts movement indicators, along with observed adoption of traceability workflows, are the signals that tie Mordor Intelligence's estimate to a commercial automotive demand pool instead of including general blockchain spending that only touches the sector indirectly. Differences also come from base case choices, where some sources apply aggressive adoption curves out to 2034 or 2035, and from currency timing when multi-region revenues are converted and summed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.84 B (2025) | |

| Global Consultancy A | USD 0.96 B (2025) | Uses a broader inclusion of automotive digital trust and data integrity programs, which can pull in adjacent connected vehicle security and data platform spend beyond blockchain-specific implementations. |

| Industry Publisher B | USD 0.86 B (2025) | Counts a wider set of application areas, including financial services and mobility solutions, and may treat early stage pilots and bundled services as full market revenue earlier in the adoption cycle. |

The spread across sources is explainable once the inclusion rules are made explicit, especially around adjacent connected vehicle software and how early deployments are monetized. With clear scope filters, practical adoption variables, and repeatable cross-checks, the estimate stays transparent and easier to reconcile with real automotive activity over time.

Key Questions Answered in the Report

How large is the automotive blockchain market today and in 2031?

The automotive blockchain market size stands at USD 1.05 billion in 2026 and is projected to reach USD 3.26 billion by 2031 on the back of multi-segment adoption.

What is driving the rapid growth of the automotive blockchain market?

Surging demand for supply-chain transparency, mandatory battery-passport rules effective in 2027, and rising use of Web3 vehicle-wallets are the primary catalysts behind the 25.34% CAGR forecast through 2031.

Which application segment leads the automotive blockchain market?

Supply-chain and logistics applications dominate with 39.95% revenue share in 2025, supported by counterfeit parts mitigation and compliance automation.

Why are insurance companies adopting blockchain faster than other end users?

Blockchain enables real-time usage-based pricing and automated claims processing, underpinning a 28.33% CAGR for insurance adoption through 2031.

Page last updated on: