Europe Vehicle Emission Standards And Impact Analysis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

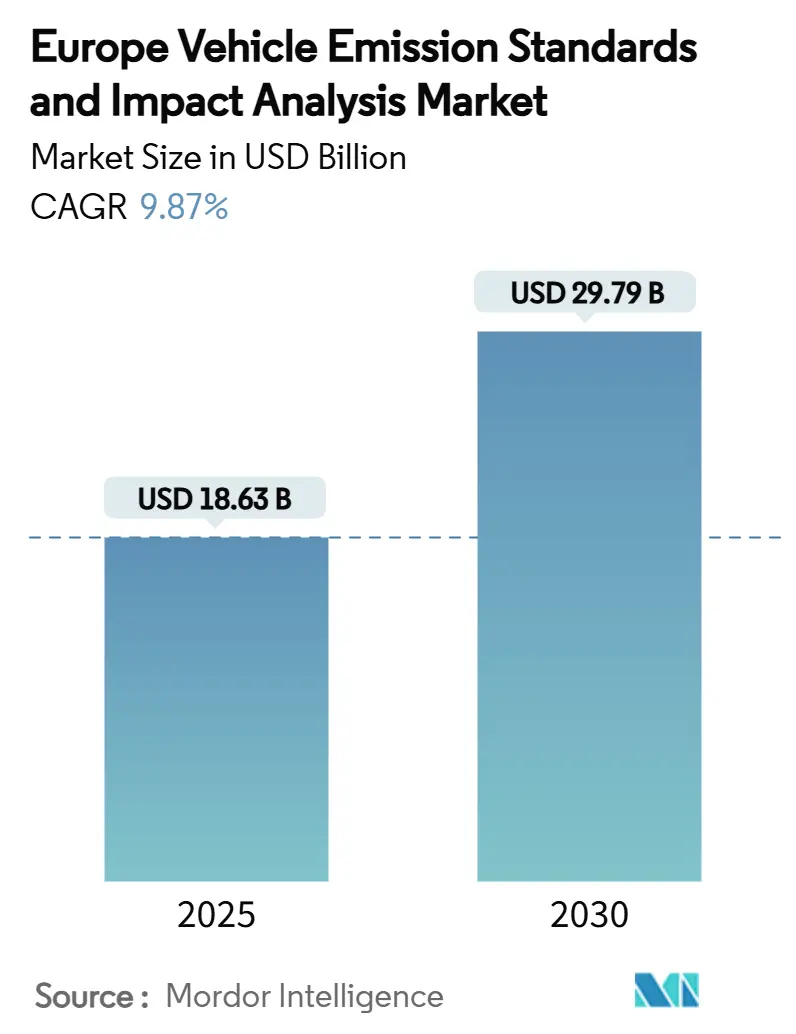

| Market Size (2025) | USD 18.63 Billion |

| Market Size (2030) | USD 29.79 Billion |

| Growth Rate (2025 - 2030) | 9.87% CAGR |

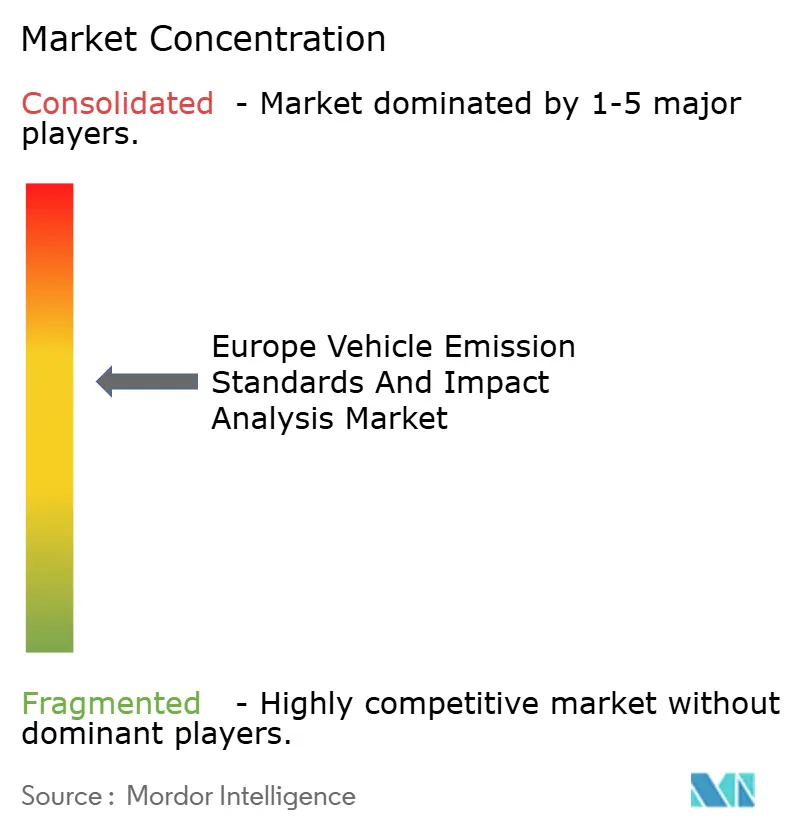

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Vehicle Emission Standards And Impact Analysis Market Analysis by Mordor Intelligence

The European vehicle emission standards and impact analysis market size reached USD 18.63 billion in 2025, and it is projected to expand at a 9.87% CAGR to USD 29.79 billion by 2030, underscoring the accelerating alignment between regulatory convergence and testing innovation. Robust growth reflects the new Euro 7 rules that enter force for light-duty vehicles in November 2026 and extend to all registrations one year later. Stricter pollutant caps, lifetime-long compliance mandates, and compulsory on-board monitoring systems collectively reshape certification protocols for exhaust, brake, and tire particle emissions.

Key Report Takeaways

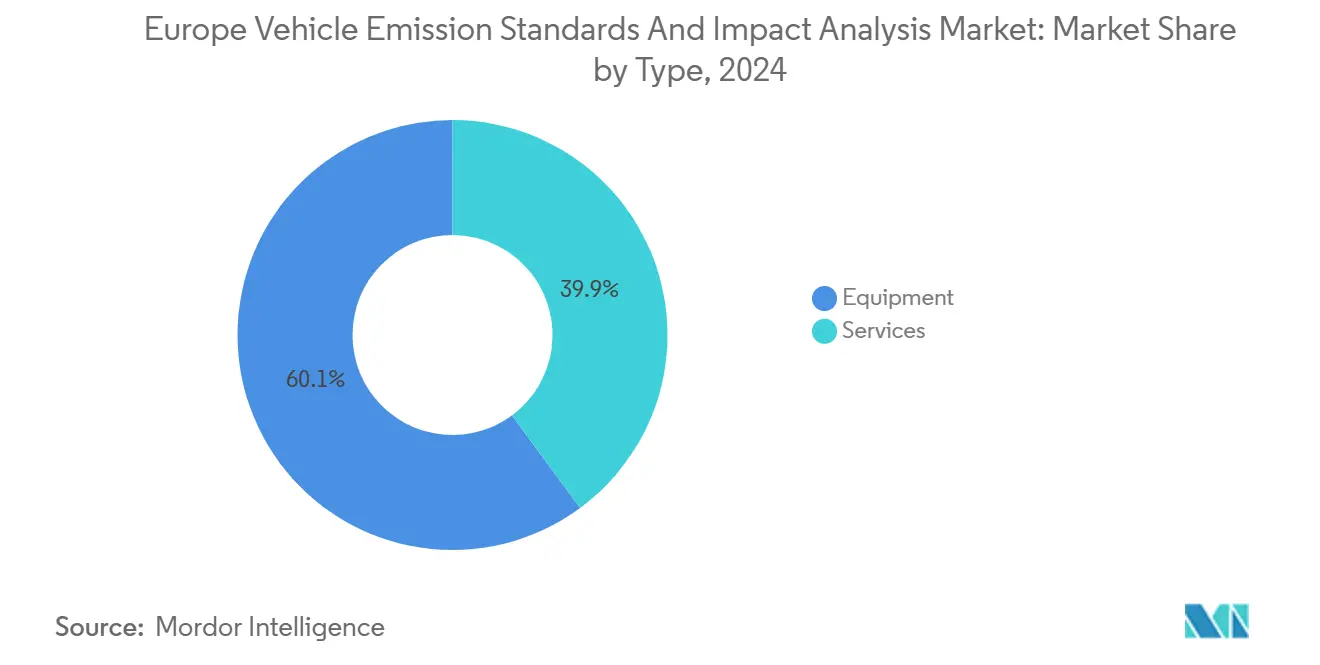

- By type, equipment accounted for 60.12% of the Europe vehicle emission standards and impact analysis market in 2024; services are projected to grow faster than the overall 9.87% market CAGR during 2025–2030.

- By end user, OEMs accounted for 52.14% of the market in 2024 and are expected to post the fastest 11.77% CAGR through 2030, while other end-user groups collectively represent the remaining 47.86% share.

- By geography, Germany captured 26.89% of regional market revenue in 2024, whereas the Netherlands is forecast to record the strongest 12.73% CAGR over the outlook period.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global vehicle emission standards and impact analysis market size report represents that cumulative total.

Europe Vehicle Emission Standards And Impact Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro 7 Standards Enforcement Timeline | +2.8% | EU-wide, with Germany and France leading implementation | Medium term (2–4 years) |

| Stricter OEM Fleet-wide CO₂ Targets and Penalties | +2.1% | EU-wide, particularly Germany, France, Italy | Short term (≤ 2 years) |

| BEV Battery-Durability Rules Influencing Propulsion Mix | +1.6% | Netherlands, Germany, Nordic countries | Medium term (2–4 years) |

| Remote-Sensing Tech for On-Road Compliance (RDE 2.0) | +1.3% | Netherlands, Belgium, Germany, Switzerland | Long term (≥ 4 years) |

| Anti-Subsidy Tariffs Reshaping Import Mix | +0.9% | EU-wide, strongest impact in Germany and France | Short term (≤ 2 years) |

| Blockchain-Based Emission Certification Pilots | +0.4% | France, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Euro 7 Standards Enforcement Timeline

Euro 7 regulations mandate compliance from November 29, 2026, for new light-duty vehicle types, extending to all registrations by November 2027, fundamentally restructuring European emission testing protocols.[1]"European Commission Updates eCall System Regulations for Vehicles," digitalsolutions.applusidiada.com. The standards introduce comprehensive pollutant limits covering traditional exhaust emissions, brake dust, and tire abrasion particles. On-board monitoring systems become mandatory, requiring continuous emission tracking and automatic alerts when vehicles exceed regulatory thresholds. Testing complexity increases substantially as Euro 7 encompasses broader operating conditions, including cold-start scenarios and high-load highway driving that previously escaped rigorous oversight. The regulation's technology-neutral approach allows manufacturers flexibility in compliance strategies while ensuring ultra-low emission performance across diverse real-world conditions.

Stricter OEM Fleet-wide CO₂ Targets and Penalties

Fleet-wide CO₂ targets tighten to 93.6 g/km for passenger cars in 2025, representing a 15% reduction from 2021 baselines, with penalties of EUR 95 per gram for non-compliance creating immediate financial pressure on manufacturers.[2]"ACEA calls for CO2 penalty relief for 2025 for cars and vans," dieselnet.com. German automakers face particularly acute challenges as the weight-based adjustment factor disappears, forcing manufacturers of larger vehicles to accelerate electrification or accept substantial penalty exposure. The regulatory framework eliminates previous flexibility mechanisms while maintaining pooling arrangements that allow manufacturers to share emission credits, creating new market dynamics around compliance trading. Volkswagen and Ford lag behind their 2025 targets, while Volvo Cars has achieved early compliance through aggressive electrification strategies.[3]"The drive to 2025: Carmakers' progress towards their EU CO2 target in H1 2024," transportenvironment.org. The penalty structure's severity transforms compliance from a regulatory obligation to a strategic imperative, driving unprecedented investment in emission testing and validation infrastructure.

BEV Battery-Durability Rules Influencing Propulsion Mix

Euro 7 introduces comprehensive battery durability requirements for electric vehicles, mandating performance retention over extended operational periods and establishing new testing protocols for energy storage systems. Battery electric vehicles must demonstrate consistent performance across temperature extremes, charging cycles, and operational stress scenarios that mirror real-world usage patterns. The regulation requires manufacturers to provide battery health monitoring systems and establish minimum performance thresholds that batteries must maintain throughout their operational lifespan. These requirements reshape propulsion mix strategies as manufacturers balance traditional ICE compliance costs against electric vehicle battery validation expenses. Netherlands leads European implementation with a comprehensive testing infrastructure for battery durability assessment, while Germany develops standardized energy storage system certification protocols.

Remote-sensing Tech for On-road Compliance (RDE 2.0)

Remote sensing technology deployment accelerates across European markets as authorities implement comprehensive emission monitoring systems that identify high-emitting vehicles in real-time traffic conditions. Netherlands, Belgium, Germany, and Switzerland mandate particulate emission testing during periodic technical inspections, utilizing advanced optical remote sensing systems that measure NOₓ, CO₂, and particulate matter concentrations without disrupting traffic flow. RDE 2.0 protocols expand beyond laboratory conditions to encompass diverse driving scenarios, weather conditions, and vehicle loading states that reflect authentic operational environments. European Commission initiatives promote standardized remote sensing methodologies that enable cross-border enforcement cooperation and harmonized compliance verification, which will play a major role in driving the demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Compliance Cost of Euro 7 Retrofits | -1.4% | EU-wide, particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Diesel HDVs Struggle to Meet Real-World NOₓ Limits | -0.8% | Germany, France, Italy, Spain | Medium term (2–4 years) |

| Inventory-vs-Remote-Sensing Data Gaps Create Uncertainty | -0.6% | EU-wide, with acute concern in Germany and Netherlands | Medium term (2–4 years) |

| Catalyst PGM Supply Bottlenecks | -0.7% | Germany, France, South Africa-dependent sourcing chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Compliance Cost of Euro 7 Retrofits

Compliance with Euro 7 standards requires significant investments in advanced aftertreatment systems, such as larger SCR catalysts, cold-start heaters, and upgraded exhaust gas recirculation setups. Extended durability requirements and rising material costs, particularly for platinum group metals, further increase development expenses. Smaller manufacturers, with limited production volumes, face considerable challenges in absorbing these costs, leading to heightened financial pressures and accelerating market consolidation. Additionally, compliance involves extensive testing, certification, and continuous monitoring, which introduce operational and timing challenges. These factors can delay product launches and place additional strain on resources.

Diesel HDVs Struggle to Meet Real-world NOₓ Limits

Heavy-duty diesel vehicles encounter significant challenges in compliance with Euro 7 NOₓ limits under real-world driving conditions, particularly during urban stop-start cycles and high-load highway operations. Current SCR systems demonstrate reduced performance at low exhaust temperatures, highlighting undetected emission control gaps during laboratory testing. Addressing these deficiencies necessitates advanced powertrain integration, including thermal management and mild-hybrid solutions. However, these measures increase vehicle complexity, operational costs, and the likelihood of reliability issues in demanding commercial applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Still Dominates, Services Compound the Complexity

Equipment is estimated to account for 60.12% of spending in 2024, as regulators and OEMs continue to upgrade to Euro-7-ready infrastructure - new chassis and engine dynamometers, PN10-capable particle counters, ammonia and NOₓ analyzers, PEMS fleets, and remote-sensing gantries. Each tightening of CO₂ and pollutant thresholds, and the inclusion of brake and tire particles, forces another round of hardware calibration or replacement, keeping capex-heavy lab modernisation and roadside enforcement kits at the centre of short-term budgets.

Services capture the faster-growing share of value as end users increasingly buy “compliance-as-a-service” rather than just test benches. Type-approval campaigns, RDE route design and execution, remote-sensing programme setup, Euro 7 gap-analysis, and emissions data analytics are bundled into multi-year contracts tied to model refresh cycles. Vendors that combine regulatory interpretation, test execution, and digital reporting platforms steadily convert one-off projects into recurring revenue streams, so service growth outpaces the hardware base even though equipment remains the larger line item through 2030.

By End User: OEMs Take Over Half the Wallet, Agencies and Labs Shape Enforcement

Vehicle manufacturers already anchor this market: OEMs command 52.14% of Europe’s vehicle emission standards and impact analysis spending in 2024 and are also the fastest-growing end-user group, expanding at about 11.77% CAGR through 2030. They are pulling more work in-house—building battery-durability rigs, adding PN10-capable analyzers, and scaling PEMS fleets—because Euro 7, lifetime-compliance mandates, and stricter fleet CO₂ penalties make emissions testing a core product-planning constraint rather than a late-stage regulatory tick box.

Government regulating agencies and independent testing labs together control most of the remaining spend, splitting the roles of rule-setter and neutral executor. National authorities and city governments invest in remote-sensing corridors, upgraded periodic-inspection lines, and digital back-ends that can ingest and compare lab, RDE, and roadside data. Independent labs monetize the rising complexity by acting as overflow and specialist partners - running challenging HDV RDE programmes, validating OEM in-house results, and supporting smaller importers that lack their own facilities. Large fleet operators and public transport agencies are a smaller but growing slice, commissioning impact and compliance studies to plan truck, van, and bus renewal under tightening LEZ and zero-emission targets.

Geography Analysis

Germany anchors the Europe vehicle emission standards and impact analysis market, accounting for 26.89% of regional revenue in 2024. A dense cluster of passenger-car and commercial-vehicle OEMs, Tier-1 suppliers, and major TIC players (like TÜV SÜD, DEKRA, SGS, Applus+, HORIBA) concentrates lab upgrades, type-approval work, and advanced RDE testing in the country. The United Kingdom, France, Italy, and Spain together form a second tier of large, mature markets, where established MOT/ITV/contrôle-technique regimes and expanding low-emission/ultra-low-emission zones maintain consistent demand for both emission-testing equipment and compliance services.

The Netherlands is the fastest-growing geography, projected to expand at a 12.73% CAGR through 2030, reflecting its role as an early adopter of remote-sensing pilots, PN10 implementation, and data-driven on-road enforcement models. Surrounding Western and Northern European markets (Belgium, Switzerland, Nordics, and the rest of BeNeLux) increasingly follow similar approaches, while Central and Eastern European countries move along a convergence path - aligning with Euro 6/6d and Euro 7 timelines but rolling out inspection and lab capacity more gradually. This creates a gradient of opportunity: high-spec, innovation-led projects in Germany and the Netherlands, balanced by more cost-sensitive, capacity-building engagements across the broader “Rest of Europe” bucket.

Coverage of the vehicle emission standards and impact analysis market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Japan and China, each shaped by local operating conditions.

Competitive Landscape

The market exhibits moderate concentration with established testing providers like TÜV SÜD, Dekra SE, and SGS SA maintaining dominant positions through comprehensive service portfolios and regulatory relationships. At the same time, technology innovators including Horiba Ltd., Continental AG, and Robert Bosch GmbH compete through advanced testing equipment and integrated compliance solutions. Strategic positioning increasingly favors companies that combine traditional certification capabilities with emerging technologies like blockchain-based emission tracking and AI-enhanced remote sensing platforms. Market leaders pursue vertical integration strategies, with TÜV SÜD partnering with SEGULA Technologies to offer comprehensive vehicle market introduction services encompassing traditional and electrified powertrains.

White-space opportunities emerge in specialized testing areas, including battery durability validation, onboard monitoring system certification, and remote sensing technology deployment, that require substantial technical expertise and capital investment. Continental AG's spin-off of its Automotive business unit into a separate European company by 2025 reflects broader industry restructuring as suppliers adapt to electrification trends and regulatory complexity.

Emerging disruptors leverage digital technologies and data analytics to offer real-time compliance monitoring and predictive maintenance solutions that complement traditional testing services. The competitive landscape transformation accelerates as Euro 7 implementation creates demand for specialized capabilities that exceed traditional testing provider offerings, potentially reshaping market structure through technology-driven consolidation and partnership formation.

Europe Vehicle Emission Standards And Impact Analysis Industry Leaders

-

TÜV SÜD

-

Dekra SE

-

SGS SA

-

Applus+

-

HORIBA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Hyundai Motor and Kia unveiled the Integrated Greenhouse Gas Information System (IGIS) utilizing blockchain technology for comprehensive carbon emissions management throughout vehicle lifecycles, supporting compliance with international environmental regulations and enhancing operational efficiency.

- October 2024: Ricardo plc secured funding for the SeaChange project, which aims to support the the shipping sector's zero emissions goal by 2050 by developing the Navigating Energy Transitions tool to help ports identify decarbonization pathways and assess future energy requirements.

Europe Vehicle Emission Standards And Impact Analysis Market Report Scope

| Equipment |

| Services |

| Vehicle Manufacturers (OEMs) |

| Component and System Suppliers (Tier-1 / Tier-2) |

| Independent Testing, Inspection, and Certification (TIC) Labs |

| Government and Regulatory Authorities |

| Fleet Operators and Public Transport Agencies |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Type | Equipment |

| Services | |

| By End User | Vehicle Manufacturers (OEMs) |

| Component and System Suppliers (Tier-1 / Tier-2) | |

| Independent Testing, Inspection, and Certification (TIC) Labs | |

| Government and Regulatory Authorities | |

| Fleet Operators and Public Transport Agencies | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe vehicle emission standards market?

The Europe vehicle emission standards market size is USD 18.63 billion in 2025.

How fast will the market grow through 2030?

Revenue is forecast to rise at a 9.87% CAGR, reaching USD 29.79 billion by the decade’s end.

Which country contributes the largest share?

Germany leads with 26.89% of market share, supported by its strong automotive industry and stringent inspection network.

Why is the Netherlands the fastest-growing geography?

Nationwide deployment of optical remote sensing and 10 nm particle counters propels a 12.73% CAGR in the Netherlands.

Which propulsion technology shows the highest growth?

Battery-electric vehicles deliver a 21.96% CAGR, driven by Euro 7 incentives and fleet CO₂ targets.

What segment dominates emission-type spending?

CO₂ certification holds 73.08% of revenue due to direct EUR 95 per gram penalties for non-compliance.

Page last updated on: