Europe SOC As A Service (SOCaaS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

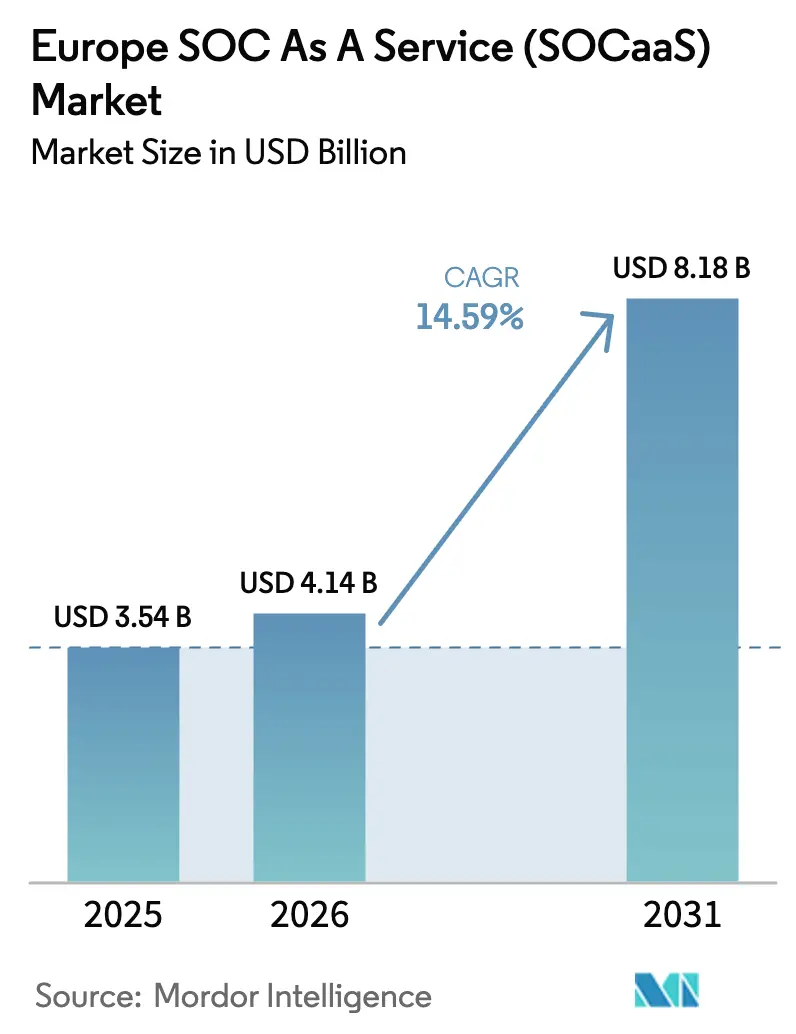

| Base Year Market Size (2025) | USD 3.54 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 8.18 Billion |

| Growth Rate (2026 - 2031) | 14.59% CAGR |

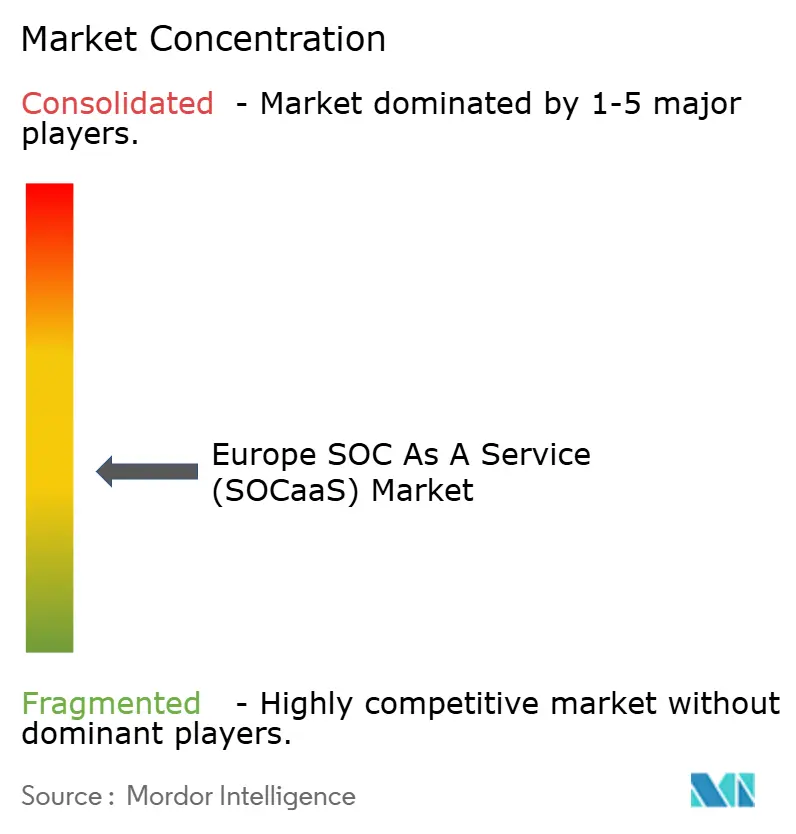

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe SOC As A Service (SOCaaS) Market Analysis by Mordor Intelligence

The Europe SOC As a Service market size is projected to be USD 3.54 billion in 2025, USD 4.14 billion in 2026, and reach USD 8.18 billion by 2031, growing at a CAGR of 14.59% from 2026 to 2031. Rapid adoption of consumption-based security models, the legally binding NIS2 incident reporting timelines, and the spread of generative-AI-driven detection tools are collectively reshaping budget priorities. Enterprises now view outsourced monitoring as an operating expense that scales with business activity rather than a capital project. Telcos and cloud providers bundle extended detection and response into connectivity contracts, squeezing point solution vendors but widening the addressable base of mid-market buyers. Sovereign cloud requirements in Germany and France further stimulate domestic hosting investments, tilting competitive advantage toward providers with in-region data centers. Finally, cyber-insurance underwriters now tie policy issuance to proof of 24x7 monitoring, turning SOCaaS into a prerequisite rather than an optional add-on.

Key Report Takeaways

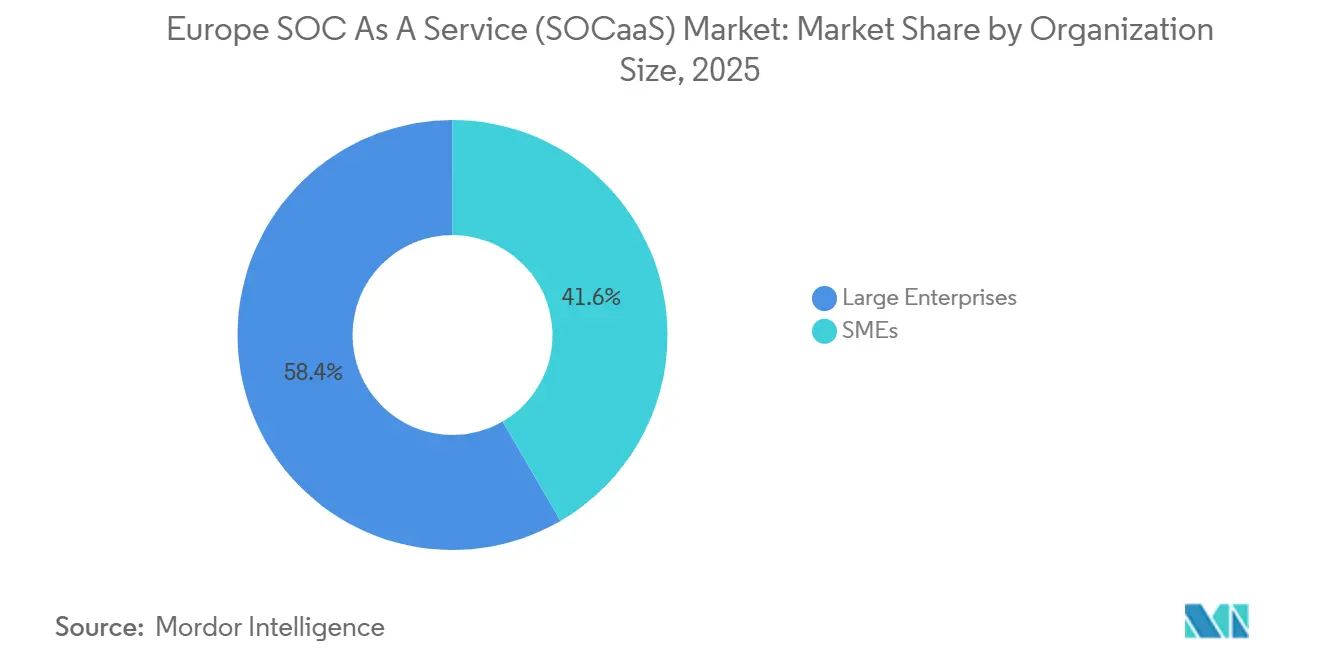

- By organization size, large enterprises led with 58.38% of Europe SOC As A Service market share in 2025, while small and medium-sized enterprises are forecast to grow at a 15.68% CAGR through 2031.

- By end user, banking, financial services, and insurance held 24.53% revenue share in 2025, yet healthcare is advancing at a 15.01% CAGR to 2031.

- By service type, managed detection and response captured 32.27% of the Europe SOC As A Service market size in 2025, and threat intelligence is set to rise at a 15.84% CAGR over 2026-2031.

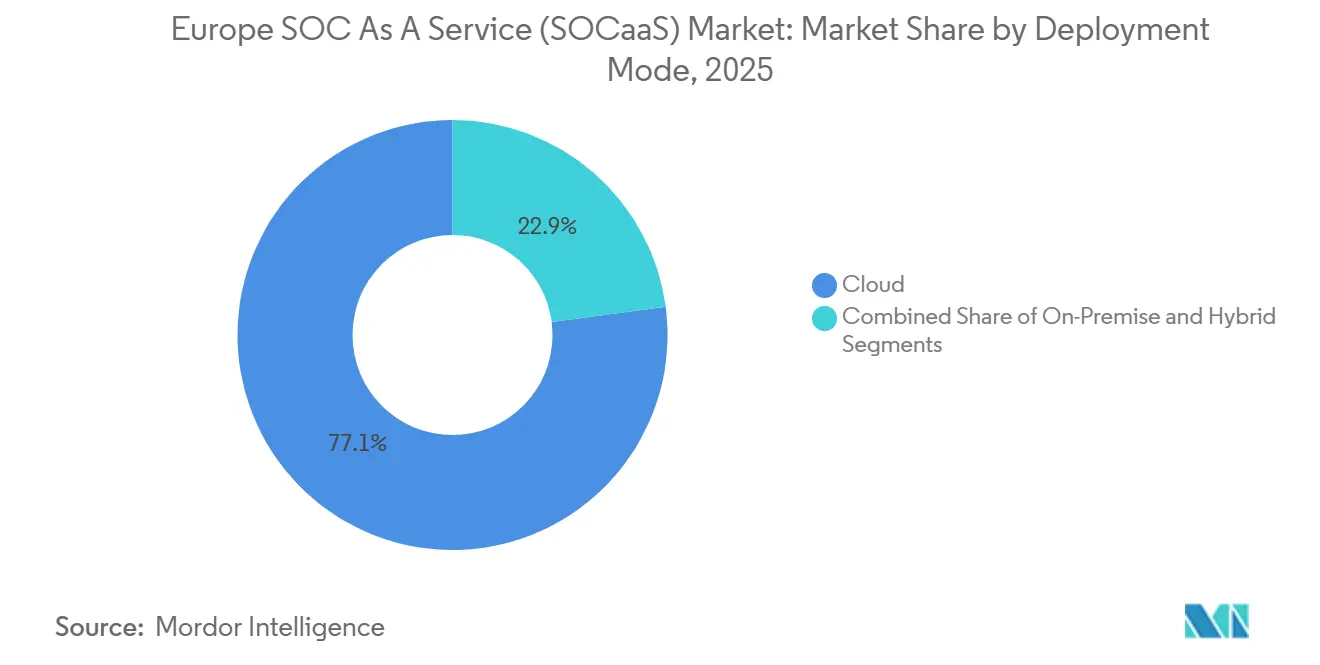

- By deployment mode, cloud implementations accounted for 77.09% of spending in 2025, while hybrid configurations expanded at a 14.89% CAGR across the forecast horizon.

- By security type, network security commanded 29.41% share of the Europe SOC As A Service market size in 2025 and cloud security is projected to climb at 14.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe SOC As A Service (SOCaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Adoption of Pay-per-Use Opex Model | +1.80% | Pan-European, strongest in SME-dense economies such as Italy, Spain, Poland | Medium term (2-4 years) |

| Rapid Cloud Migration Among SMEs | +2.30% | Germany, France, Netherlands, Nordics with high SaaS penetration | Short term (≤ 2 years) |

| Mounting Cyber-Insurance Prerequisites for 24x7 Monitoring | +1.50% | United Kingdom, Germany, France where cyber-insurance adoption exceeds 40% | Medium term (2-4 years) |

| EU NIS2 Directive Amplifying Compliance Demand | +3.10% | All EU member states, acute in critical infrastructure sectors | Short term (≤ 2 years) |

| Generative AI-Powered Threat Hunting Capabilities | +2.00% | Early adopters in Nordics, Germany, United Kingdom | Medium term (2-4 years) |

| Surge in Managed XDR Bundling by Telcos and MSPs | +1.90% | Markets with incumbent telco dominance: Spain, France, Italy | Short term (≤ 2 years) |

| Increasing Availability of Sovereign European Clouds | +1.70% | Germany, France, Netherlands with national data-sovereignty mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU NIS2 Compliance Mandate

NIS2 widened the pool of regulated entities from roughly 2,000 to more than 160,000, compelling even mid-sized utilities, hospitals, and transport operators to maintain continuous monitoring or face fines up to EUR 10 million (USD 10.7 million).[1]European Union Agency for Cybersecurity, “NIS2 Directive Overview,” enisa.europa.eu As few of these organizations can staff an in-house SOC around the clock, providers offering audit ready dashboards and automated incident reporting enjoy a sustained demand floor. German and French regulators reinforce the directive with national data-residency rules, effectively steering contracts toward vendors running data centers inside each country. Compared with the United States three-day reporting allowance, Europe’s 24-hour window increases urgency and justifies premium pricing for AI enhanced detection.

Rapid Cloud Migration Among SMEs

Eurostat recorded that 45% of EU firms with 10-249 employees used cloud services in 2024, up from 38% three years earlier.[2]European Data Protection Board, “EU Cloud Code of Conduct,” edpb.europa.eu This expansion dissolves the traditional perimeter, exposing identity and API layers that legacy firewalls miss. Budget constrained SMEs rarely field a dedicated security professional yet face the same ransomware surge as larger peers. Onboarding to SOCaaS platforms that auto-discover workloads inside Microsoft 365 or Google Workspace therefore offers high protection for a predictable monthly fee. Average total cost of ownership, including tooling and staff, runs roughly one-sixth of an in-house build, creating a clear economic argument.

Generative-AI Threat Hunting

Commercial SOC platforms embedded with large language models let junior analysts query logs in plain English, draft remediation scripts, and summarize incidents for executives. Microsoft Security Copilot pilots show phishing triage falling from 45 minutes to under 5 minutes.[3]Microsoft Investor Relations, “Security Copilot Pilot Results,” microsoft.com Faster triage shrinks attacker dwell time, reducing ransom leverage and regulatory penalties. Providers differentiate by fine-tuning models on European legal texts so that auto-generated reports align with NIS2 and GDPR language, removing hours of manual compliance work. The same models train on fresh threat intelligence every few hours, giving mid-market customers a level of analytical depth once reserved for global banks.

XDR Bundling by Telcos and MSPs

Incumbent telecom operators’ pair extended detection and response with connectivity, software defined wide area networking, and cloud hosting. Telefonica Tech reported 32% cybersecurity revenue growth in 2025 after packaging XDR with SD-WAN across Spain.[4]Telefonica, “Annual Report 2025,” telefonica.com Orange Cyberdefense injects network telemetry from its backbone into correlation engines, spotting anomalies before they cross into customer endpoints. These models let telcos monetize existing infrastructure, drop marginal delivery costs, and undercut standalone security vendors on price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Sovereignty Complexities | -1.20% | Germany, France, Austria with strict localization mandates | Medium term (2-4 years) |

| Scarcity of European SOC-Grade Cyber Talent | -1.50% | Pan-European, acute in Eastern Europe and Southern Europe | Long term (≥ 4 years) |

| Hidden Long-Term TCO in Multi-Tenant SIEM | -0.80% | Cost-sensitive SMEs in Southern and Eastern Europe | Medium term (2-4 years) |

| Integration Friction with Legacy OT Environments | -0.90% | Manufacturing hubs in Germany, Italy, Czech Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber Talent Scarcity

Europe lacked roughly 350,000 cybersecurity professionals in 2025, and median hiring time for a tier-two analyst exceeded four months in major economies. Wage inflation raises provider costs, and some vendors cap new customer intake until staffing pipelines catch up. Solutions include near-shoring to Romania and Bulgaria, heavy automation, and university partnerships like Orange Cyberdefense’s dual-track master’s program targeting 200 graduates per year by 2027. Despite these tactics, limited headcount slows onboarding speed and can constrain service quality during major incident surges.

Data Residency and Sovereignty Rules

German, French, and Austrian regulations compel providers to store logs within national borders and forbid access by non-EU legal entities. Vendors must maintain separate data planes and analyst pools, raising capital requirements and operational complexity. Multinationals operating across several jurisdictions end up stitching together multiple SOC feeds, which can increase mean time to detect. Sovereign cloud initiatives such as Gaia-X promise relief but have slipped behind schedule, so compliance remains a moving target through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Widen Growth Lead

Small and medium-sized enterprises account for a modest portion of total spending today, yet they are forecast to grow at a 15.68% CAGR between 2026 and 2031, overtaking large enterprises in incremental demand. Many SMEs came under NIS2 jurisdiction only in 2024, triggering a scramble for affordable 24x7 monitoring. Arctic Wolf’s fixed-fee bundle at USD 5,000 per month, launched in 2025, removes unpredictable event-volume pricing and resonates with firms managing fewer than 250 users. In contrast, large enterprises that already run internal SOCs primarily outsource burst capacity or specialized functions, which tempers their growth rate. Nonetheless, big firms still represent 58.38% of Europe's SOC As A Service market share in 2025 because their infrastructures span multiple data centers, clouds, and operational technology networks.

Providers deploy separate go-to-market motions. For SMEs, vendors stress time to value, guided setup wizards, and pre-configured playbooks that attach to Microsoft 365 and Salesforce without professional services. For global conglomerates, contracts revolve around bespoke service level agreements, threat intelligence subscriptions, and executive tabletop exercises. As a result, the Europe SOC As A Service market size captured by SMEs is expected to almost triple by 2031, while large enterprise spending roughly doubles.

By End User: Healthcare Accelerates

Banking financial services and insurance entities remain the top spenders, holding 24.53% of revenue in 2025 thanks to the Digital Operational Resilience Act. Yet healthcare is the fastest climber, advancing at 15.01% CAGR through 2031. Ransomware campaigns targeting hospitals rose 210% between 2023 and 2025, forcing clinical networks that historically underinvested in cybersecurity to sign multi-year SOCaaS contracts. Insurance renewals now require documented 24x7 monitoring, driving up funnel conversion.

Meanwhile, manufacturing firms struggle to integrate legacy programmable logic controllers that lack logging, slowing uptake but opening niche demand for OT aware offerings like Fortinet’s 2025 FortiSOC launch. Government buyers expand as national budgets allocate ring fenced funds, but procurement fragmentation across municipalities tempers immediate adoption.

By Service Type: Threat Intelligence Outpaces

Managed detection and response is foundational, securing 32.27% share in 2025. However, threat intelligence subscriptions grow faster at 15.84% because enterprises increasingly seek early warning of industry specific adversaries. IBM X-Force and Thales publish sector tailored feeds that customers ingest directly into SIEM correlation engines. Security monitoring alone, chosen by clients retaining in-house response teams, expands steadily but below the market average.

Incident response retainers sell briskly amid rising ransomware, with per incident fees sometimes exceeding USD 200,000. Managed SIEM demand softens as cloud native stacks reduce infrastructure footprints, though certain heavily regulated banks still prefer provider operated SIEMs for audit familiarity.

By Deployment Mode: Hybrid Picks Up Pace

Cloud deployments dominate, making up 77.09% of the total, underscoring the appeal of scalability and operational expenditure alignment in multi-tenant platforms. These platforms allow businesses to scale their operations efficiently while optimizing costs, making them a preferred choice across various industries. However, hybrid models, which meld on-premises collectors with cloud analytics, are witnessing a robust growth rate of 14.89% CAGR. This growth is driven by the need for flexibility and the ability to balance data processing between local and cloud environments. Industries such as manufacturing, utilities, and transportation are channeling sanitized logs from their operational technology into cloud engines, but only after a local preprocessing step to ensure latency and safety. This preprocessing ensures that sensitive data is handled securely while maintaining real-time operational efficiency.

The introduction of the EU Cloud Code of Conduct certification in 2025 bolsters the confidence of risk officers, facilitating the transition of analytics workloads off-site. This certification provides a standardized framework for data protection and compliance, addressing key concerns for organizations operating in regulated environments. While the trend leans away from pure on-premises adoption, sovereign agencies managing classified data still have a pressing need for air-gapped appliances. These agencies prioritize security and data sovereignty, necessitating solutions that operate independently of external networks. This niche demand is being met by the innovative "portable SOC in a box" solution, which offers a compact and secure option for managing sensitive data in isolated environments.

By Security Type: Cloud Centric Controls Rise

In 2025, network security commanded 29.41% of the spending, but its growth is waning. This shift is largely attributed to the rise of zero trust architectures, which are moving control points away from traditional perimeter firewalls and towards identities and workloads. Zero trust architectures emphasize the principle of "never trust, always verify," requiring continuous authentication and authorization for users and devices, which reduces reliance on perimeter-based security models. Meanwhile, cloud security is making significant strides, boasting a robust 14.96% CAGR. This growth is driven by the increasing adoption of cloud-native applications and the migration of workloads to cloud environments. Key controls like cloud security posture management, container runtime protection, and identity governance are not just standalone measures; they actively feed telemetry into Security Operations Center (SOC) workstreams.

This integration is enhancing the prominence of preventative alerts, overshadowing traditional network anomaly logs. These preventative alerts enable SOC teams to proactively address potential threats, reducing response times and improving overall security posture. Endpoint detection remains a linchpin in the SOC playbook, underscoring the importance of host-level containment and memory forensics. Endpoint detection and response (EDR) solutions are critical for identifying and mitigating threats at the device level, ensuring that compromised endpoints are swiftly isolated to prevent lateral movement within networks. As microservices become ubiquitous and developers increasingly expose APIs, application security is gaining traction. This surge in demand is particularly evident for runtime self-protection monitoring. Runtime application self-protection (RASP) solutions provide real-time protection by detecting and blocking attacks as they occur within applications. The proliferation of APIs, driven by the need for seamless integration and communication between services, has heightened the risk of vulnerabilities, making robust application security measures indispensable for organizations.

Geography Analysis

Germany, the United Kingdom, and France collectively generated more than half of Europe SOC As A Service market revenue in 2025. Germany’s March 2025 procurement rule requiring in-country hosting funnelled contracts to PlusServer and Orange Cyberdefense, while limiting bids from non-European vendors. The United Kingdom’s National Cyber Security Centre earmarked GBP 200 million (USD 253 million) to extend SOCaaS access to local councils, enlarging the public sector pool. France’s ANSSI demanded residency and annual audits, further localizing vendor selection.

The Netherlands and Sweden emerge as innovation hubs. Amsterdam’s dense data center cluster attracts IBM, NTT Security, and Cloudflare SOC investments, and Dutch tax incentives trim setup costs. Stockholm benefits from high fiber penetration and cloud usage, making Nordic midsize enterprises early adopters of AI infused SOC platforms. Spain and Italy ride national recovery and resilience funds amounting to EUR 1.2 billion (USD 1.28 billion) and EUR 900 million (USD 963 million) respectively, channelling grants toward municipal SOC procurement and SME subsidies.

Central and Eastern European markets, including Poland and the Czech Republic, show smaller absolute spending yet record high growth rates as voucher programs and sector guidance close the maturity gap. Poland’s August 2025 cybersecurity voucher covers up to EUR 50,000 (USD 53,500) for SME adoption, and Czech energy regulators publish OT security checklists. As regional digital transformation accelerates, the share of Europe SOC As A Service market size attributed to these economies will edge upward though Western Europe remains dominant.

Competitive Landscape

The Europe SOC as a Service (SOCaaS) market is moderately fragmented, with IBM, SecureWorks, and Fortinet competing beside European specialists such as Orange Cyberdefense, Atos, and Thales Group. Strategic alliances between telecom carriers and security pure plays intensify as bundled connectivity plus SOC propositions resonate with midsized enterprises. Orange Cyberdefense expanded its footprint through a USD 169 million investment in new German and Polish facilities, showcasing the sovereign-cloud model’s appeal.

Technology differentiation orbits around AI-driven automation. IBM leverages Watson to triage high-volume alerts, while Microsoft Sentinel’s cloud-native analytics attract customers favouring tight integration with Azure workloads. Thales augmented its database-security capabilities via its USD 3.6 billion Imperva acquisition, signalling a push toward data-centric monitoring solutions. European vendors promote local processing, multilingual analyst teams, and country-specific certifications to outmanoeuvre U.S. rivals in regulated verticals.

White-space opportunities concentrate in operational-technology and 5G network security, where expertise remains scarce. ETSI’s certification frameworks encourage standardization, but providers able to embed OT protocol parsing and industrial threat-intelligence feeds earn premium margins. As managed security spending converges with connectivity budgets, telecom incumbents may acquire niche providers to capture end-to-end value chains, gradually raising the market’s concentration index without tipping into oligopoly.

Europe SOC As A Service (SOCaaS) Industry Leaders

Thales

Connectwise LLC

Atos SE

Fortinet Inc.

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Orange Cyberdefense opened a Warsaw SOC employing 120 analysts to meet rising Central and Eastern European demand.

- December 2025: IBM Security invested USD 150 million to expand X-Force threat intelligence and embed generative-AI across its European managed detection platform.

- November 2025: Telefonica Tech acquired a Madrid cybersecurity consultancy for EUR 80 million (USD 85.6 million), adding 200 professionals to its Iberian operations.

- October 2025: Thales partnered with OVHcloud to launch a sovereign compliant SOC targeting French public sector and critical infrastructure clients.

Europe SOC As A Service (SOCaaS) Market Report Scope

The Europe SOC As A Service Market Report is Segmented by Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), End User (IT and Telecom, BFSI, Retail and Consumer Goods, Healthcare, Manufacturing, Government, Other End Users), Service Type (Managed Detection and Response, Security Monitoring, Vulnerability Assessment, Incident Response, Threat Intelligence, Managed SIEM, Other Service Types), Deployment Mode (Cloud, On-Premise, Hybrid), Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Other Security Types), and Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Austria, Belgium, Sweden, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Retail and Consumer Goods |

| Healthcare |

| Manufacturing |

| Government |

| Other End Users |

| Managed Detection and Response |

| Security Monitoring |

| Vulnerability Assessment |

| Incident Response |

| Threat Intelligence |

| Managed SIEM |

| Other Service Types |

| Cloud |

| On-Premise |

| Hybrid |

| Network Security |

| Endpoint Security |

| Application Security |

| Cloud Security |

| Other Security Types |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Austria |

| Belgium |

| Sweden |

| Rest of Europe |

| By Organization Size | Small and Medium-Sized Enterprises |

| Large Enterprises | |

| By End User | IT and Telecom |

| BFSI | |

| Retail and Consumer Goods | |

| Healthcare | |

| Manufacturing | |

| Government | |

| Other End Users | |

| By Service Type | Managed Detection and Response |

| Security Monitoring | |

| Vulnerability Assessment | |

| Incident Response | |

| Threat Intelligence | |

| Managed SIEM | |

| Other Service Types | |

| By Deployment Mode | Cloud |

| On-Premise | |

| Hybrid | |

| By Security Type | Network Security |

| Endpoint Security | |

| Application Security | |

| Cloud Security | |

| Other Security Types | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Austria | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of Europe SOC As A Service market by 2031?

The market is forecast to reach USD 8.18 billion by 2031, expanding at a 14.59% CAGR from 2026.

Which user segment is growing fastest in adopting SOCaaS across Europe?

Healthcare organizations lead growth with a 15.01% CAGR as ransomware threats and insurance prerequisites intensify.

Why are SMEs increasingly turning to SOCaaS solutions?

Cloud migration exposes SMEs to new attack surfaces while limited staff and budgets make outsourced 24x7 monitoring a cost effective defense.

How do data residency rules influence provider selection?

Germany and France require in country log storage, pushing buyers toward vendors operating national data centers or sovereign clouds.

Which service type is expected to outpace others through 2031?

Threat intelligence subscriptions are set to grow fastest as firms shift from reactive alert triage to proactive adversary tracking.

Page last updated on: