Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

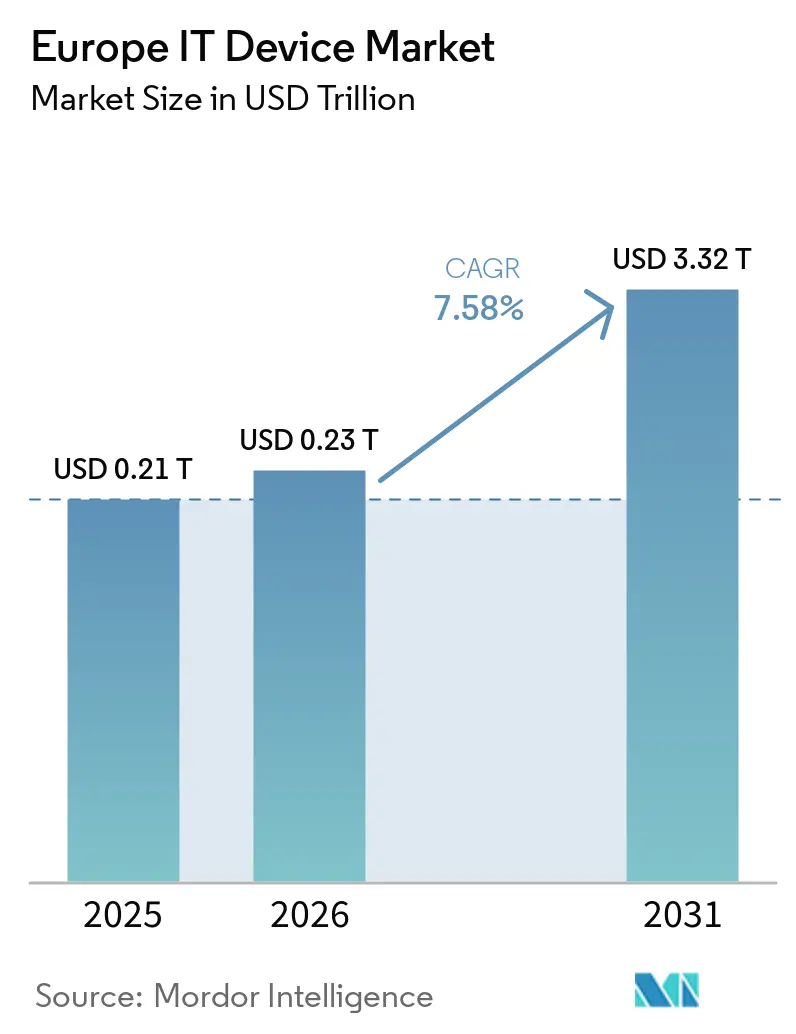

| Base Year Market Size (2025) | USD 0.21 Trillion |

| Market Size (2026) | USD 0.23 Trillion |

| Market Size (2031) | USD 3.32 Trillion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IT Device Market Analysis by Mordor Intelligence

The Europe IT device market size is projected to expand from USD 0.21 trillion in 2025 and USD 0.23 trillion in 2026 to USD 3.32 trillion by 2031, registering a 7.58% CAGR between 2026 and 2031. Hybrid-work norms, government digitalization grants, and an emerging preference for edge-centric architectures are sustaining device refresh demand even as pandemic-era emergency spending fades. Employers are standardizing dual-location computing setups that include lightweight laptops, external monitors, and ergonomic peripherals, while households gravitate toward mid-range 5G smartphones and large-screen tablets that support streaming and learning. Vendors are localizing assembly lines inside the European Union to reduce tariff exposure and comply with sovereignty rules, a shift that shortens lead times for education and enterprise tenders. At the same time, the refurbished-device channel, rising right-to-repair rules, and longer software-support windows are placing structural limits on unit growth, pushing OEMs to emphasize circular-economy services and premium features.

Key Report Takeaways

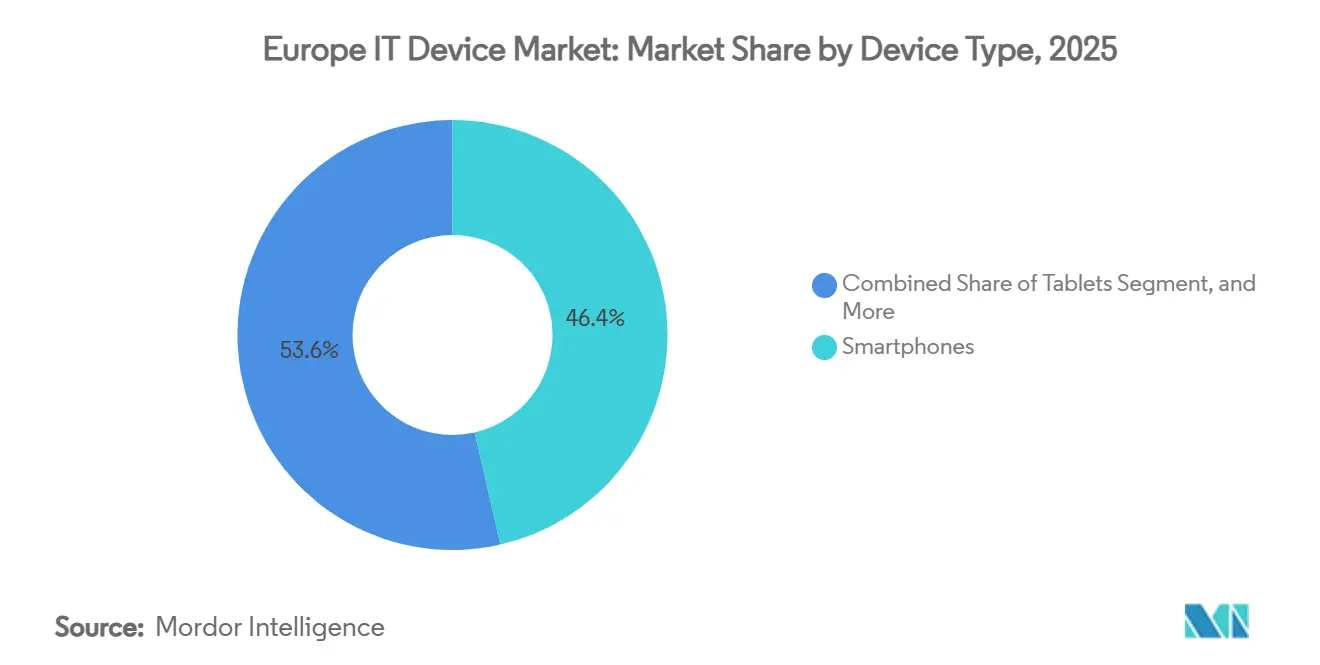

- By device type, smartphones led with a 46.43% share of the Europe IT device market in 2025, while tablets are forecast to grow at an 8.58% CAGR through 2031.

- By end-user industry, the consumer segment accounted for 54.19% of the Europe IT device market size in 2025; education is advancing at an 8.38% CAGR to 2031.

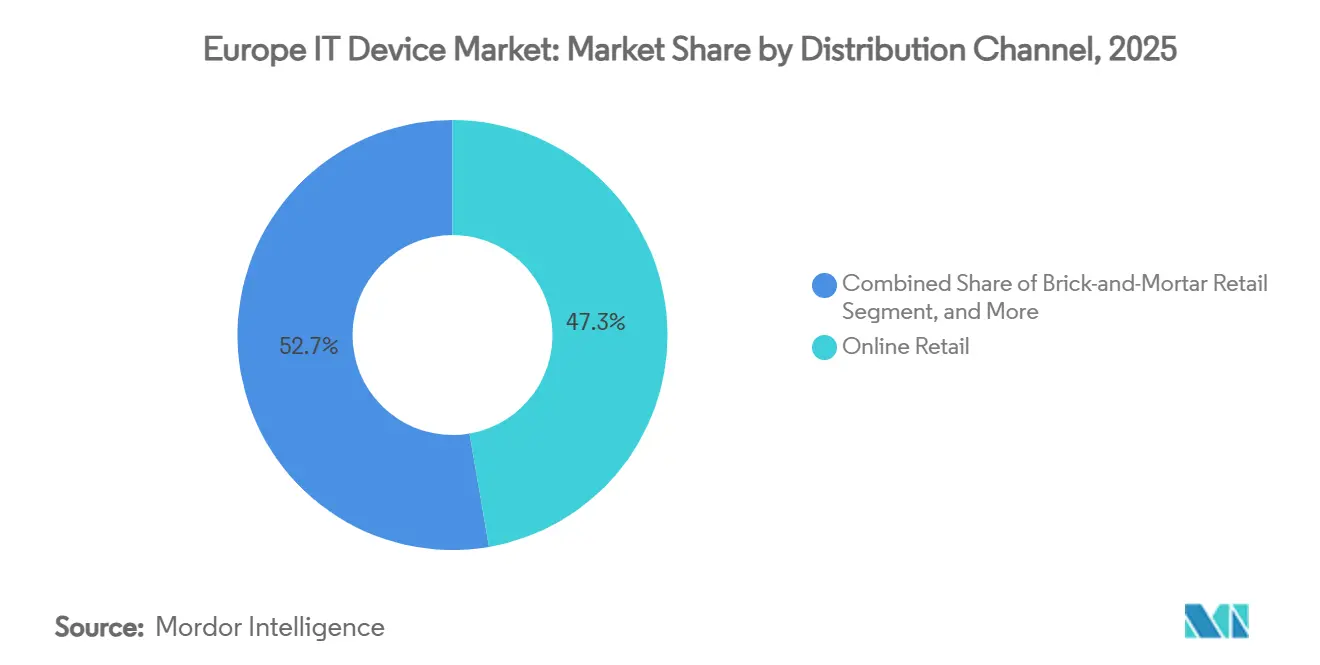

- By distribution channel, online retail accounted for 47.29% of revenue in 2025 and is projected to post an 8.47% CAGR through 2031, overtaking brick-and-mortar by 2027.

- By operating system, Android retained 63.98% share of shipments in 2025, whereas ChromeOS is expanding fastest at an 8.69% CAGR over 2026-2031.

- By geography, Germany held 21.68% of the Europe IT device market in 2025, while Spain recorded the highest projected growth at an 8.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe IT Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G Networks Accelerating Smartphone Refresh Cycles | +1.5% | Pan-European, with concentrated deployment in Germany, UK, France, Nordic region | Short term (≤ 2 years) |

| Government-Led Digitalisation Programmes Across the EU | +1.3% | EU-wide, with flagship initiatives in Spain, Italy, Poland, and Baltic states | Medium term (2-4 years) |

| Rising Adoption of Hybrid Work Models Boosting Mobile Computing Demand | +1.2% | Western Europe core (Germany, France, UK, Benelux), spill-over to Central Europe | Medium term (2-4 years) |

| Growth of E-Commerce Channels Enhancing Device Accessibility | +1.0% | Pan-European, strongest in Nordic region, Netherlands, Germany | Short term (≤ 2 years) |

| Emergence of AI-Enabled Edge Devices in Smart Manufacturing | +0.8% | Germany, France, Italy, Czech Republic (manufacturing hubs) | Long term (≥ 4 years) |

| EU Right-to-Repair Legislation Encouraging Modular Design | +0.6% | EU-wide, with early compliance in France, Netherlands, Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of 5G Networks Accelerating Smartphone Refresh Cycles

Europe hosts 79 standalone 5G commercial networks, a footprint that enables low-latency use cases such as warehouse automation and augmented-reality field service. German operators finalized nationwide SA coverage in 2025, triggering enterprise upgrades to ruggedized 5G handsets capable of network slicing. Premium consumers in urban corridors adopt mmWave-ready flagships, while mid-tier users wait for prices to fall, creating a bifurcated refresh curve. The RedCap specifications in 3GPP Release 18 extend 5G capability to wearables and IoT nodes ETSI.ORG. Peripheral makers, therefore, see incremental demand for compatible smartwatches and barcode scanners that sync with those networks.

Government-Led Digitalization Programs Across The EU

The Digital Europe Program earmarked EUR 1.3 billion (USD 1.47 billion) for supercomputing, AI, and cybersecurity grants between 2025-2027. Spain channels EUR 3.75 billion (USD 4.24 billion) of that pool into rural connectivity and SME device subsidies under its España Digital 2026 plan. Poland, Italy, and the Baltic states run similar co-funded schemes that specify EU-assembled laptops and tablets, providing volume opportunities for Lenovo’s Polish factory and Dell’s Irish plant. These mandates anchor multi-year procurement pipelines and create predictable demand visibility for the Europe IT device market.

Rising Adoption Of Hybrid Work Models Boosting Mobile Computing Demand

Hybrid arrangements covered 44% of European workers in 2024, up from 37% in 2022.[1]Eurofound, “European Working Conditions Telephone Survey 2024,” eurofound.europa.eu Employers now issue ultralight laptops and secondary monitors so staff can hot-desk in the office and plug-and-play at home. Zero-trust security rollouts favor hardware with TPM 2.0 and biometric sensors, benefiting premium enterprise lines from Microsoft, Dell, and Lenovo. Logitech posted a 23% jump in European webcam and headset sales in 2025, reflecting higher peripheral attach rates. Updated EU ergonomic guidelines further codify employer responsibility to fund compliant equipment, cementing device procurement as a routine operating expense.

Growth Of E-Commerce Channels Enhancing Device Accessibility

73% percent of Europeans aged 16-74 shopped online in 2024, and IT devices ranked among the top three product categories. Amazon’s 45 fulfillment centers enable same-day delivery in 75 metro areas, eroding the immediacy advantage of physical stores. Apple and Samsung blend web ordering with two-hour in-store pickup across major capitals, driving omnichannel convenience. The Digital Services Act requires transparent product ranking, empowering price-comparison engines that commoditize mid-tier phones. As margins narrow, OEMs lean on trade-in credits and direct-to-consumer financing to maintain share in the Europe IT device market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthening Smartphone Replacement Cycles in a Maturing Market | -0.9% | Western Europe (Germany, France, UK, Benelux, Nordic) | Medium term (2-4 years) |

| Semiconductor Supply Chain Volatility | -0.7% | Pan-European, acute in automotive and industrial IT segments | Short term (≤ 2 years) |

| Growth of Refurbished Device Sales Cannibalising New Units | -0.6% | Western and Northern Europe, emerging in Southern Europe | Medium term (2-4 years) |

| Heightened Compliance Costs Under EU Sustainability Rules | -0.5% | EU-wide, disproportionate impact on smaller OEMs and importers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthening Smartphone Replacement Cycles In A Maturing Market

Upgrade intervals widened to 33-40 months in 2025, up from 24-30 months in 2019, as performance gains flattened and devices crossed the EUR 1,000 (USD 1,130) threshold in many markets.[2]European Environment Agency, “Circular Economy and E-waste,” eea.europa.eu Seven years of software support for iOS 18 and One UI 7 removes security obsolescence as a trigger to buy new models. EU rules that cap interest rates on bundled handset plans have weakened carrier subsidies, shifting decisions from monthly cashflow to lifetime cost. Collectively, these forces subtract nearly 1 percentage point from the projected CAGR of the Europe IT device market.

Semiconductor Supply Chain Volatility

Only 9% of global fabrication capacity was in Europe in 2025, exposing OEMs to Asia-centric shocks. Dutch chipmaker Nexperia extended microcontroller lead times to 26 weeks in 2025, double pre-pandemic norms. While the EUR 43 billion (USD 49 billion) EU Chips Act aims to double regional share by 2030, new German and Austrian fabs will not reach high-volume output until after 2027. Interim redesigns and dual-sourcing inflate bill-of-materials by up to 12%, curbing margin headroom for vendors in the Europe IT device market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Tablets Surge On Education Mandates

Tablets are expected to post an 8.58% CAGR over 2026-2031, the quickest clip among form factors, as ministries enforce one-to-one ratios in classrooms. Smartphones, though still dominant with a 46.43% share of the Europe IT device market in 2025, are experiencing slower unit growth as saturation in Western Europe tempers annual upgrades. Laptops retain their role as the hybrid-work workhorse, benefiting from larger battery envelopes and AI-optimized chipsets. Desktops and workstations occupy specialized niches such as computer-aided design and quantitative finance, where thermal budgets and multi-monitor arrays matter more than portability.

In education tenders, Android and iPadOS tablets compete on depth of mobile device management, while ChromeOS-based detachables win budget-sensitive bids through lower licensing costs. France shipped 130,000 student tablets under its Territoires Numériques Éducatifs program in 2025. Spain procured 500,000 devices the same year, mostly sub-EUR 300 (USD 339) Chromebooks fitted with offline-capable curricula. These deployments lift peripheral attach rates, prompting monitor and stylus makers to tailor classroom bundles for the Europe IT device market.

By End-User Industry: Education Leads Growth Trajectory

The education vertical is forecast to record an 8.38% CAGR through 2031, outstripping all other user groups. The consumer segment retained 54.19% of the Europe IT device market in 2025, buoyed by smartphone cycles and gaming laptops, yet its growth rate is plateauing as ownership nears full penetration in Northern Europe. Enterprise demand remains resilient thanks to Windows 11 hardware prerequisites, zero-trust projects, and ESG disclosure software that requires higher compute headroom. Government agencies, although beneficiaries of EU recovery funds, advance at a steadier clip due to protracted tendering processes.

ESF Plus allocates EUR 99.3 billion (USD 112 billion) for digital skills from 2021-2027, focusing on enhancing digital literacy and fostering technological adoption across vocational schools. This funding supports the procurement of laptops, tablets, and other essential IT devices, ensuring that students and educators have access to modern tools for effective learning. Additionally, Italy’s Piano Scuola 4.0 allocates EUR 2.1 billion (USD 2.38 billion) to transforming traditional classrooms into smart classroom environments. This initiative includes investments in interactive displays, advanced teaching aids, and comprehensive teacher training programs to facilitate the integration of technology into education. These structured programs provide a steady demand for IT devices, creating pipeline visibility and offering stability to the Europe IT device market, even during periods of fluctuating consumer demand.

By Distribution Channel: Online Retail Dominates And Accelerates

Online platforms captured 47.29% share in 2025 and are on track for an 8.47% CAGR, overtaking physical electronics chains by 2027. Marketplace algorithms, rapid fulfillment, and transparent pricing diminish the need for showroom visits. Conversely, value-added resellers keep relevance in enterprise and government accounts where financing, imaging, and lifecycle services matter. Direct OEM web-stores, armed with trade-in engines and build-to-order configurators, squeeze intermediary margins yet unlock higher engagement metrics.

E-commerce penetration in the Netherlands reached 52% of device sales in 2025, underscoring consumers' growing preference for online platforms over traditional retail channels. Amazon’s Frustration-Free Packaging initiative reduced packaging waste by 30%, appealing to environmentally conscious buyers and aligning with the European Union's circular economy objectives. This initiative not only enhanced Amazon's brand image but also set a benchmark for sustainability practices in the industry. Concurrently, logistics advancements, such as Samsung’s partnership with DHL Express, enabled next-day delivery coverage across 90% of postal codes in the Netherlands. These improvements have effectively minimized delivery speed as a competitive differentiator, shifting the focus of competition toward value-added services and loyalty programs. This trend underscores the growing importance of customer retention strategies and eco-friendly practices in the European IT device market.

By Operating System: ChromeOS Gains Education And SME Traction

ChromeOS is projected to grow 8.69% annually to 2031, riding on bulk Chromebook orders from schools and subscription-priced SME bundles. Android, with 63.98% shipment share in 2025, retains leadership on the back of smartphone dominance, but its growth curve bends downward in mature economies. Windows remains entrenched in enterprise desktops and notebooks, thanks to Active Directory and legacy app dependencies. iOS/iPadOS serves premium tiers, leveraging the broader Apple ecosystem, while Linux sustains developer and privacy niches.

Europe accounted for 32% of worldwide Chromebook shipments in 2025, with education dominating the segment, accounting for 78% of regional volume. Spain, as a significant contributor, ordered 180,000 Chromebooks during the year, focusing on devices priced below EUR 300 to meet budget constraints and educational needs. Similarly, the Netherlands distributed 50,000 Chromebooks specifically for vocational training programs, underscoring the importance of affordable, efficient devices for skill development. Google’s zero-touch enrollment feature, combined with automatic updates, has proven to be a key driver for adoption among cost-sensitive small and medium-sized enterprises (SMEs). These SMEs, often lacking dedicated IT staff, find the operating system’s simplicity and ease of management highly appealing, further solidifying its presence and integration within the Europe IT device market.

Geography Analysis

Germany’s sizeable automotive and industrial base pairs with a strong SME sector, reinforcing a steady pipeline for rugged handhelds, CAD-capable laptops, and edge servers. Corporate buyers fast-track device refreshes to support private 5G factory networks and real-time quality analytics, cushioning the Europe IT device market from consumer cyclicality. Local manufacturing outposts in Bavaria and Saxony benefit from reduced logistics latency, shaving weeks off the delivery time for custom-configured workstations.

Southern Europe shows a different trajectory. Spain’s public-private España Digital 2026 plan not only funds network coverage but also earmarks subsidies for device upgrades across tourism, logistics, and agriculture. Tablet shipments spike in Andalusia and Castilla-La Mancha, where distance learning bridges road-access gaps. Italy’s recovery plan steers investment toward digital classrooms and smart-city pilots, seeding demand for sensor-rich tablets and IoT gateways that local governments can monitor via EU sovereign cloud services.

Nordic nations and the Netherlands sustain the highest e-commerce penetration, making them early adopters of direct-to-consumer launches. Finland and Sweden favor sustainable devices with verified repairability scores, rewarding OEMs that disclose modular design roadmaps. Poland and Romania leverage GDP growth and rising disposable income to boost consumer smartphone ownership, while domestic IT-services clusters in Warsaw and Cluj-Napoca pull enterprise-class notebook orders into the Europe IT device market.

Competitive Landscape

The Europe IT device market is moderately concentrated. The top five brands, Apple, Samsung, Lenovo, HP, and Dell, collectively held a moderate share of 2025 revenue, leaving ample room for challenger brands and niche specialists. Chinese vendors such as Xiaomi, OPPO, and Realme use sub-EUR 300 smartphones to erode mid-tier share in Spain and Poland, whereas Apple defends the premium segment through ecosystem lock-in and first-party trade-ins. Sustainability messaging is now a frontline differentiator: Fairphone advertises modular parts and transparent supply chains, while Dell integrates recycled plastics and offers carbon-offset bundles.

Strategic investments underscore a shift toward local production. Lenovo is spending EUR 150 million (USD 162 million approximately) to lift Hungarian notebook capacity by 30%, trimming lead times for corporate and education accounts. Dell’s USD 200 million outlay in Łódź includes new-build lines and a circular-economy refurbishment center, aligned with EU ecodesign rules. Samsung’s R&D hub in Poland focuses on AI chipsets and 6G wireless, preparing the brand for next-gen devices that emphasize on-device inference workloads.

At the ecosystem level, Microsoft’s Surface Laptop 6 moves to ARM silicon to extend battery life and run Copilot AI features offline, a direct nod to GDPR-driven data residency concerns in European enterprises. Logitech’s acquisition of lighting specialist Litra signals diversification into creator peripherals, a segment growing alongside Europe’s freelance workforce. Such maneuvers illustrate how vendors are broadening their portfolios to capture wallet share as unit growth moderates in the European IT device market.

Europe IT Device Industry Leaders

Apple Inc

Samsung Electronics Co., Ltd.

HP Inc.

Lenovo Group Limited

Dell Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Microsoft shipped the first Copilot-optimized Surface Laptop 6 units to German enterprise customers under early-adopter agreements.

- February 2026: Lenovo announced a EUR 150 million (USD 170 million) capacity expansion at its Ullo, Hungary plant, boosting annual laptop output by 30%.

- January 2026: Apple released the iPhone 16 line with on-device generative AI and shipped the first units across Europe.

- December 2025: HP and Deutsche Telekom launched bundled 5G data and an Elite Dragonfly laptop offer for German SMEs.

Europe IT Device Market Report Scope

The Europe IT Device Market encompasses the production, distribution, and utilization of electronic computing and connected hardware devices across residential, commercial, educational, and government sectors within Europe. These devices enable digital communication, computing, and productivity applications and include smartphones, laptops and notebooks, tablets, desktops and workstations, and peripheral devices.

The Europe IT Device Market Report is Segmented by Device Type (Smartphones, Laptops and Notebooks, Tablets, Desktops and Workstations, and Peripherals), End-User Industry (Consumer, Enterprise, Government, and Education), Distribution Channel (Online Retail, Brick-and-Mortar Retail, Value-Added Resellers, and Direct Sales), Operating System (Android, Windows, iOS/iPadOS, ChromeOS, and Linux), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Device Type

| Smartphones |

| Laptops and Notebooks |

| Tablets |

| Desktops and Workstations |

| Peripherals (Monitors, Keyboards, Mice, Printers) |

By End-user Industry

| Consumer |

| Enterprise |

| Government |

| Education |

By Distribution Channel

| Online Retail |

| Brick-and-Mortar Retail |

| Value-Added Resellers |

| Direct Sales (OEM Web-stores) |

By Operating Systems

| Android |

| Windows |

| iOS / iPadOS |

| ChromeOS |

| Linux |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Device Type | Smartphones |

| Laptops and Notebooks | |

| Tablets | |

| Desktops and Workstations | |

| Peripherals (Monitors, Keyboards, Mice, Printers) | |

| By End-user Industry | Consumer |

| Enterprise | |

| Government | |

| Education | |

| By Distribution Channel | Online Retail |

| Brick-and-Mortar Retail | |

| Value-Added Resellers | |

| Direct Sales (OEM Web-stores) | |

| By Operating Systems | Android |

| Windows | |

| iOS / iPadOS | |

| ChromeOS | |

| Linux | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe IT device market by 2031?

The market is forecast to reach USD 3.32 trillion by 2031, expanding at a 7.58% CAGR from 2026.

Which device category is growing fastest in Europe?

Tablets lead growth, supported by education mandates and expected to post an 8.58% CAGR over 2026-2031.

How big is online retail's role in device distribution?

Online channels captured 47.29% of sales in 2025 and should surpass 50% by 2027 as they grow at an 8.47% CAGR.

Why is ChromeOS gaining traction among European buyers?

Bulk Chromebook purchases by schools and cost-sensitive SMEs favor ChromeOS because of low total ownership costs and zero-touch enrollment.

Which country shows the quickest market growth through 2031?

Spain is set to expand at an 8.29% CAGR thanks to its España Digital 2026 program that subsidizes connectivity and device upgrades.

Page last updated on: