Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

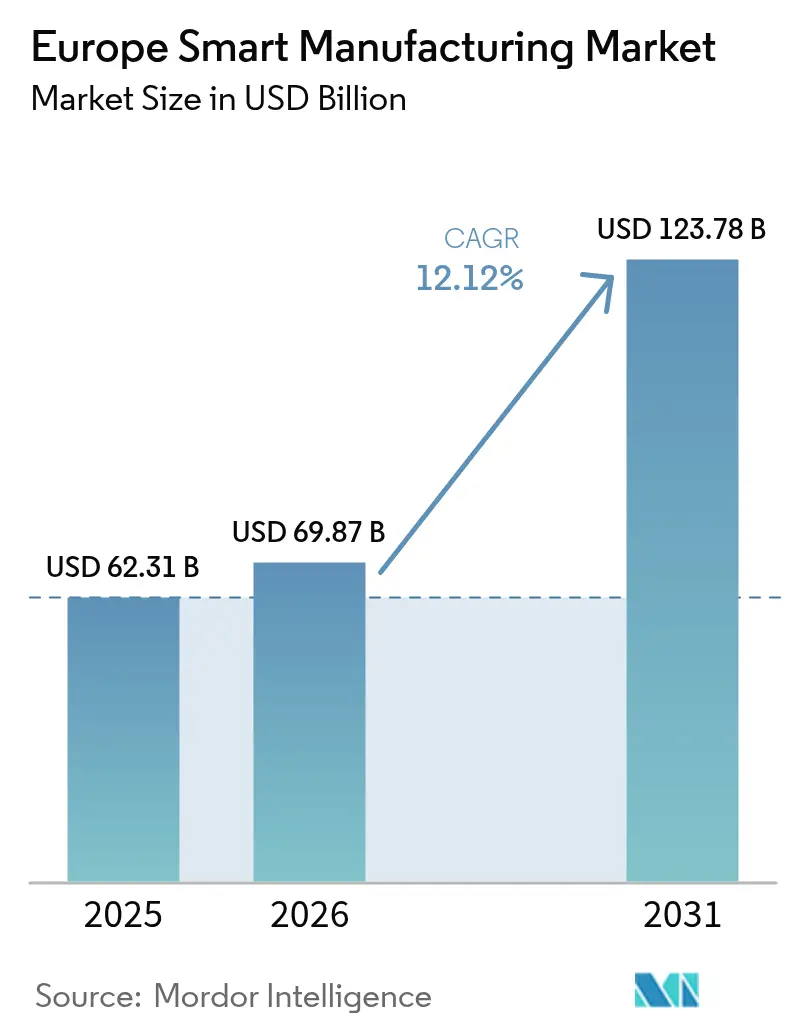

| Base Year Market Size (2025) | USD 62.31 Billion |

| Market Size (2026) | USD 69.87 Billion |

| Market Size (2031) | USD 123.78 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Smart Manufacturing Market Analysis by Mordor Intelligence

Europe smart manufacturing market size in 2026 is estimated at USD 69.87 billion, growing from 2025 value of USD 62.31 billion with 2031 projections showing USD 123.78 billion, growing at 12.12% CAGR over 2026-2031. Intensifying labor-cost inflation, high-profile public funding such as the EUR 200 billion (USD 213 billion) InvestAI program, and escalating regulatory pressure under the Cyber Resilience Act collectively accelerate adoption of connected production technologies. Industrial robotics continues to anchor plant-floor automation, while edge AI and digital-twin deployments unlock real-time process insights that magnify asset utilization. Enterprises pursue platform-based ecosystems that fuse control hardware, IIoT connectivity, and analytics software so they can curb energy consumption and comply with net-zero mandates. The competitive field tightens as incumbents absorb AI specialists, and governments link fiscal incentives to local data-sovereignty safeguards, turning the Europe smart manufacturing market into a strategic pillar of economic resilience.

Key Report Takeaways

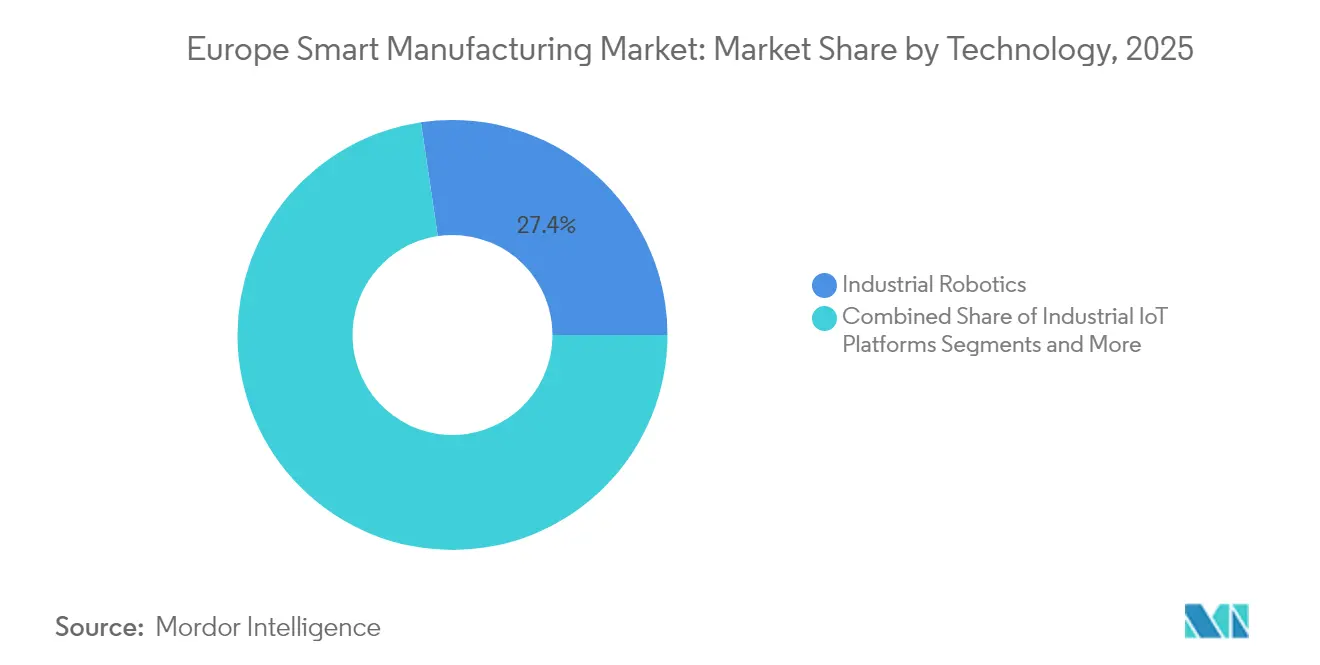

- By technology, industrial robotics led with 27.35% of Europe smart manufacturing market share in 2025; digital twin & simulation is projected to scale at a 16.2% CAGR to 2031.

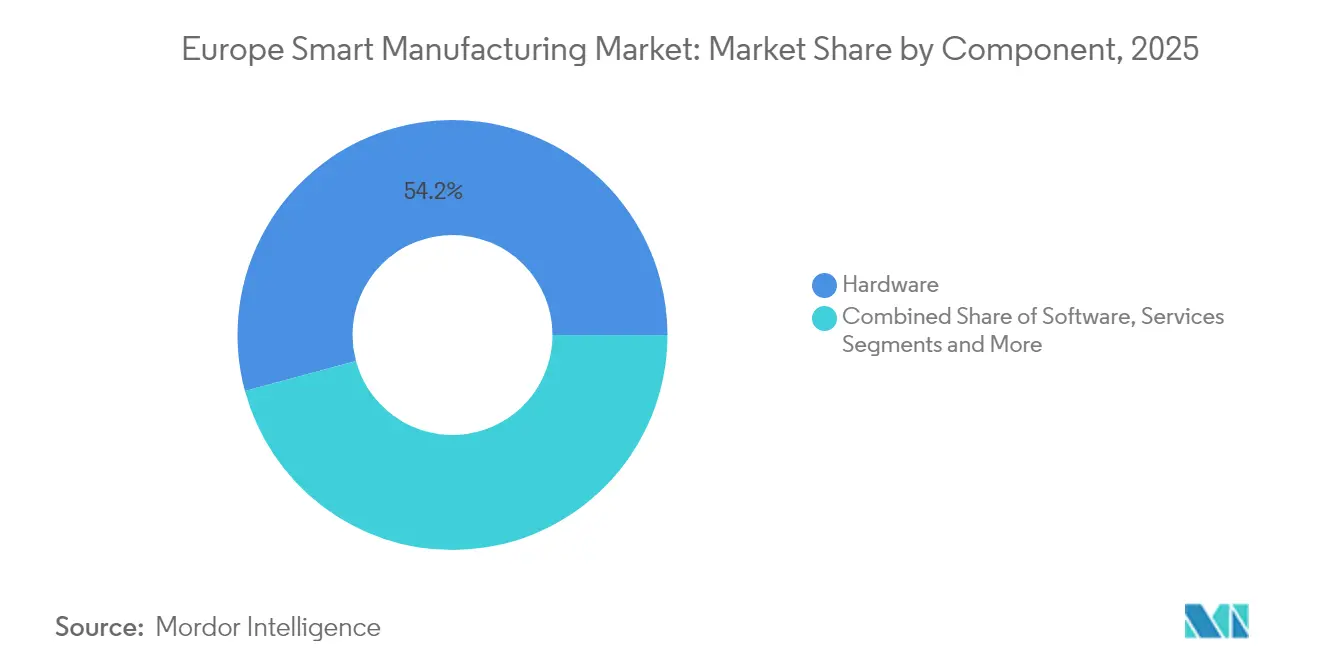

- By component, hardware captured 54.20% revenue share of the Europe smart manufacturing market size in 2025, while edge-computing devices are advancing at a 14.1% CAGR through 2031.

- By end-user industry, automotive retained 22.55% share of the Europe smart manufacturing market in 2025, whereas electronics & semiconductors shows the fastest 14.5% CAGR to 2031.

- By country, Germany held 23.75% of Europe smart manufacturing market size in 2025, and Poland is expanding at a 12.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Smart Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Industry-4.0 funding schemes | +2.10% | Germany, France, Netherlands, spillover to CEE | Medium term (2-4 years) |

| Rising labor-cost pressure driving factory automation | +3.20% | Nordic and Western Europe | Short term (≤ 2 years) |

| Rapid adoption of IIoT connectivity | +2.80% | Germany, UK, Netherlands, expanding to Poland and Czech Republic | Medium term (2-4 years) |

| Net-zero mandates accelerating energy-optimization solutions | +1.90% | EU-wide, early uptake in Germany and Scandinavia | Long term (≥ 4 years) |

| Edge-AI quality-inspection deployment in SMEs | +1.40% | Germany, Italy, France, emerging in CEE | Medium term (2-4 years) |

| Industrial-grade 5G private-network roll-outs | +1.10% | UK, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Industry-4.0 Funding Schemes

Robust European funding unlocks unprecedented capital for digital transformation. Germany’s Manufacturing-X program supplies EUR 150 million (USD 160 million) to create interoperable industrial data spaces, while the broader InvestAI architecture mobilizes EUR 200 billion (USD 213 billion) across AI infrastructure. SME access to matching grants lowers entry barriers; the UK’s Made Smarter pilot has already funnelled GBP 22 million (USD 28 million) into 350 technical projects that generated 1,600 new jobs. Venture momentum follows public outlays, illustrated by Germany’s 67% jump in AI-enabled manufacturing start-ups and hyperscaler commitments from AWS, Microsoft, and Apple. These capital flows position the Europe smart manufacturing market as a credible alternative to Asian contract manufacturing while defending regional technology sovereignty. [1]BMWK, “Manufacturing-X Funding Programme”, Federal Ministry for Economic Affairs and Climate Action, bmwk.de

Rising Labor-Cost Pressure Driving Factory Automation

Average EU hourly labor costs climbed 5% year over year to EUR 33.5 (USD 35.7) in 2024, widening the delta between Western Europe and lower-wage regions. Luxembourg tops the bloc at EUR 55.2 (USD 58.8) per hour, sharpening competitive urgency for automation among premium producers. Employers also confront an acute talent gap: 75% of firms surveyed across 21 countries report difficulty filling skilled roles. These intertwined pressures convert automation from a discretionary efficiency lever into an existential requirement, accelerating replacement of repetitive tasks with robotics and computer-vision systems across the Europe smart manufacturing market. [2]European Commission, “Data Space for Manufacturing (deployment)”, hadea.ec.europa.eu

Rapid Adoption of IIoT Connectivity

Private 5G networks and low-cost retrofit modules deliver the bandwidth and determinism necessary for large-scale machine-data capture. Ericsson’s deployment at CIMPOR’s Portuguese cement plant illustrates closed-loop control that slices emissions and maintenance downtime simultaneously. In the UK, over a dozen lighthouse installations use 5G to orchestrate autonomous guided vehicles and real-time analytics. Brownfield equipment integration is eased by plug-and-play IoT nodes that convert RS-232 outputs to MQTT protocols, allowing legacy assets to feed enterprise data lakes. This connectivity lattice underpins predictive maintenance and fosters the decentralised data governance demanded inside the Europe smart manufacturing market. [3]Ericsson, “Ericsson and Vodafone deploy private 5G at CIMPOR Portugal”, ericsson.com

Net-Zero Mandates Accelerating Energy-Optimization Solutions

EU climate policy drives capital toward electrified process heat and AI-enabled energy management. Siemens’ Fürth plant cut energy consumption per throughput by 64% while lifting output 145%, validating the triple bottom-line effect. Real-time MES and EMS integration empowers operators to modulate power draw against fluctuating electricity prices, embedding sustainability into cost-baseline decisions. Automotive OEMs replicate the model through automated in-plant driving systems that shave logistics time and battery usage. Consequently, carbon compliance becomes a built-in advantage within the Europe smart manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-sovereignty concerns | -1.80% | Germany and France, EU-wide | Short term (≤ 2 years) |

| High brown-field integration CAPEX | -2.30% | Germany, UK, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Sovereignty Concerns

The Cyber Resilience Act enforces risk-tiered conformity assessments and may levy penalties up to EUR 15 million (USD 16 million) or 2.5% of global turnover. Overlapping GDPR and NIS 2 rules escalate documentation workloads, especially for SMEs with limited cyber teams. Fear of extraterritorial data transfer slows migration to hyperscale platforms hosted outside the EU, compelling suppliers to offer sovereign clouds or edge-analytics appliances. These compliance costs elongate deployment cycles and temper the near-term growth pace of the Europe smart manufacturing market

High Brown-Field Integration CAPEX

Europe’s installed base of heterogeneous machine controllers demands bespoke retrofit solutions. Studies show upgrade budgets can reach 50% of new-equipment outlays, stretching payback periods beyond typical investment committees’ thresholds. Integration complexity magnifies skill-gap pain points, with 66% of Polish SMEs still operating without robots despite automation intentions. Financially constrained mid-caps may defer projects, ceding ground to digitally native rivals and diluting the achievable CAGR for the Europe smart manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Robotics Drives While Digital Twins Accelerate

Industrial robotics held 27.35% of Europe smart manufacturing market share in 2025, supported by automotive final-assembly automation and standardized welding cells. FANUC’s expansion in Spain signals pursuit of underserved Southern European clusters, while its explosion-proof collaborative paint robot opens hazardous-environment applications. Digital twin & simulation platforms are scaling at a 16.2% CAGR, embedding physics-based models alongside AI to forecast asset behaviour and shrink commissioning intervals. Simulation convergence with MES unlocks closed-loop optimisation, positioning digital twins as the fastest lever inside the Europe smart manufacturing market.

Automation control systems (PLC, SCADA, DCS) experience replacement demand as plants migrate to Ethernet-based fieldbuses. AI-augmented HMI layers such as Honeywell’s Experion Operations Assistant surface contextual recommendations that cut alarm fatigue. MES penetration quickens through acquisitions like Valmet–FactoryPal, enriching OEE dashboards with prescriptive insights. Additive manufacturing maintains a niche foothold in spare-parts fulfillment, where geometry complexity outweighs volume economics. This broadening toolset cements diversified revenue streams across the Europe smart manufacturing market.

By Component: Hardware Dominance Meets Edge Computing Growth

Hardware secured 54.20% of revenue in 2025 as firms outfitted lines with sensors, drives, and GPU-accelerated servers. NVIDIA’s new industrial AI cloud in Germany, housing 10,000 GPUs, exemplifies regional infrastructure that lets manufacturers train vision models locally. Edge-computing devices are rising 14.1% per year, shrinking latency for sub-millisecond control loops and satisfying data-sovereignty requirements. Machine-vision cameras tied to on-prem inference platforms inspect 100% of parts without bandwidth choke points, escalating uptake inside the Europe smart manufacturing market size.

Software layers now differentiate competitive advantage. SCADA suites integrate digital-twin replicas, and AI analytics engines rank root-cause variables. ERP-to-PLM integration creates a single product genealogy, vital for heavily regulated sectors. Service revenue climbs as integrators provide 24/7 managed detection-and-response to fulfil Cyber Resilience Act mandates. These offerings shift the value pool toward recurring subscriptions, reshaping gross-margin profiles throughout the Europe smart manufacturing market.

By End-User Industry: Automotive Leadership Faces Electronics Challenge

Automotive represented 22.55% of 2025 demand, yet its electrification pivot requires flexible body-in-white and battery-module lines. BMW’s automated driving in-plant system shows how OEMs harness lidar infrastructure to cut intralogistics idle time. Electronics & semiconductors outpaces all peers at a 14.5% CAGR, buoyed by the European Chips Act and ams OSRAM’s EUR 588 million (USD 626 million) fab expansion. Aerospace & defense follows with AI-enabled NDT tools financed by GE Aerospace’s EUR 78 million (USD 83 million) upgrade program. Cross-sector rollouts broaden the customer slate feeding the Europe smart manufacturing market size.

Process industries also accelerate. Chemicals operators deploy digital twins to trial catalyst shifts virtually, trimming costly pilot runs. Food & beverage groups invest in vision inspection for allergen compliance, while pharma plants utilise continuous-manufacturing skids with model-predictive control for throughput agility. The resulting diversification shelters the Europe smart manufacturing market from single-sector cyclicality.

Geography Analysis

Germany accounted for 23.75% of Europe smart manufacturing market size in 2025, underpinned by a dense Mittelstand and EUR 150 million (USD 160 million) Manufacturing-X data-space initiative. Yet labour costs sit 13% above peer averages, spurring automation as a cost-neutraliser. Poland leads growth at 12.32% CAGR, attracting green-tech investments such as Aira’s EUR 300 million (USD 320 million) heat-pump factory that will ship 500,000 units annually. Government grants and proximity to Western OEMs make Poland a logical overflow location for capacity extensions, adding volume to the Europe smart manufacturing market.

The United Kingdom leverages a robust private-5G ecosystem to pilot edge analytics across aerospace and energy clusters. France emphasises open-source AI frameworks, while Italy channels aerospace stimulus funds into composite-part machining centres. Smaller markets—Netherlands, Sweden, Austria, and Switzerland—capitalize on advanced broadband grids and university-industry collaboration to pilot high-variety, low-volume production, collectively enriching geographic diversity in the Europe smart manufacturing market.

Regulatory Landscape

The Europe smart manufacturing market operates under an increasingly prescriptive EU framework that links connectivity and AI use to product cybersecurity, documentation, and traceability. Regulation (EU) 2024/2847 (Cyber Resilience Act) raises the bar for security-by-design across connected industrial products. Conformity assessment body notification provisions apply from June 11, 2026, and mandatory vulnerability and incident reporting obligations commence on September 11, 2026, which affects how OEMs and automation suppliers design, update, and support smart equipment deployed on the factory floor.

Regulation (EU) 2024/1689 (EU AI Act) also shapes governance for AI-enabled industrial systems, especially where specific functions fall into high-risk categories. European standardization priorities for 2026 (European Commission notice) emphasize interoperability and secure deployment to enable cross-border industrial data exchange. Programs referenced in the report, including the EU Digital Decade and Gaia-X, reinforce data-sovereignty expectations and support demand for edge analytics, sovereign cloud options, and standardized data-space architectures in manufacturing.

Value Chain Analysis

The value chain spans industrial automation and robotics OEMs, sensor and edge-hardware suppliers, connectivity providers (including private 5G and industrial Ethernet), IIoT platforms, MES/PLM and analytics software vendors, and a large layer of system integrators and managed service providers that connect brownfield assets to new data and control stacks. Public initiatives and research programs form an additional upstream enabler, with European Commission and CORDIS-backed projects such as DMaaST (cognitive digital twins and decentralized knowledge graphs) and COMPLIANCE4DPP (digital product passport compliance workflows) contributing to reference architectures that vendors productize into deployable smart-manufacturing solutions.

Delivery on the ground remains sensitive to integration and supply chain frictions. Deteriorating supplier delivery times, highlighted by the Eurozone Manufacturing PMI (weakest since June 2022, cited in June 2026 reporting), and higher logistics complexity steer manufacturers toward resilience-focused deployments, including on-prem/edge processing and buffer-stock planning supported by better production visibility. On the demand side, policy signals such as the European Commission proposal for an Industrial Accelerator Act (COM(2026) 100, March 2026) link permitting simplification and capacity acceleration with digitalized procedures, strengthening the business case for standardized, auditable production data flows that reduce commissioning and compliance overhead.

Competitive Landscape

The Europe smart manufacturing market shows moderate fragmentation but intensifying consolidation. Siemens’ USD 10.6 billion Altair acquisition layers CAE and AI simulation atop its Xcelerator portfolio, pursuing full-stack design-to-deployment control. Hitachi’s EUR 71.5 million (USD 76 million) purchase of MA micro automation adds medical-device assembly expertise, extending value-chain reach. ABB’s planned robotics spin-off signals strategic portfolio focus, aiming to unlock shareholder value and speed vertical-specific innovation.

Partnerships with AI leaders redefine roadmaps: Rockwell and NVIDIA co-develop autonomous mobile robots, while KION teams with NVIDIA and Accenture to algorithmically optimise warehouse flows. Edge-AI start-ups such as ROBOVIS secure institutional backing to serve SME niches that incumbents overlook. Suppliers now differentiate through cyber-secure architectures compliant with the Cyber Resilience Act, turning certification readiness into a sales qualifier across the Europe smart manufacturing market.

Europe Smart Manufacturing Industry Leaders

ABB Ltd

Honeywell UK Ltd.

Siemens AG

Rockwell Automation Inc.

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Factory modernization programs that explicitly combine industrial AI, digital twins, and autonomous logistics are creating near-term whitespace for platform vendors and integrators that can deliver secure, interoperable deployments. Siemens plans to invest over EUR 200 million to modernize its Amberg, Germany facility into an intelligent factory, and Infineon is opening its Smart Power Fab in Dresden as a EUR 5 billion digital-twin and AI-enabled manufacturing site, showing how modernization budgets are being tied to advanced software, edge infrastructure, and industrial cybersecurity controls rather than standalone automation upgrades.

Robotics and electrification-driven equipment demand is also widening the opportunity set across hardware, software, and services. ABB is building a USD 280 million robotics hub in Vaesteras, Sweden (scheduled to open in late 2026), and Siemens announced a EUR 300 million expansion of its Frankfurt switchgear factory plus a supplier facility in Offenbach. As the Cyber Resilience Act timelines move into execution and reporting obligations, managed services, secure update mechanisms, and OT-security partnerships are increasingly embedded into procurement for connected assets, creating room for suppliers that bundle certification-ready architectures with lifecycle support for multi-site European manufacturers.

Recent Industry Developments

- July 2026: Siemens announced a collaboration with NCC Group to strengthen cybersecurity for UK critical infrastructure, extending OT security practices to environments where industrial systems and enterprise IT converge. The announcement increases emphasis on security-by-design and operational monitoring in smart manufacturing deployments, aligning vendor offerings with tightening EU and UK cyber requirements.

- March 2026: Siemens committed over EUR 200 million to modernize its Amberg, Germany facility into an intelligent factory using industrial AI, digital twins, and autonomous logistics as part of its Smart Infrastructure operations. The investment reinforces the shift from isolated automation projects to integrated, data-driven production architectures that standardize how software and edge hardware are purchased and deployed.

- June 2025: NVIDIA inaugurated an industrial AI cloud in Germany with 10,000 GPUs to support manufacturers including BMW, Mercedes-Benz, and Schaeffler. The expanded access to localized AI compute for vision and simulation workloads supports data-sovereignty requirements while accelerating adoption of edge-to-cloud analytics in European plants.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe smart manufacturing market covers hardware, software, and related services used inside manufacturing sites to connect factory equipment with digital systems, so production can be monitored, automated, and improved using data.

Scope exclusions: We exclude general office IT and enterprise projects that are not directly tied to plant-floor assets and production workflows.

Segmentation Overview

- By Technology

- Automation Control Systems (PLC, SCADA, DCS)

- Industrial Robotics

- Industrial IoT Platforms

- Human-Machine Interface (HMI)

- Manufacturing Execution System (MES)

- Product Lifecycle Management (PLM)

- Digital Twin and Simulation

- Additive Manufacturing / 3-D Printing

- By Component

- Hardware

- Sensors

- Controllers / IPC

- Edge-Computing Devices

- Machine-Vision Systems

- Robotics

- Software

- SCADA and HMI Software

- Analytics and AI Software

- ERP and PLM Software

- Services

- Integration and Consulting

- Maintenance and Support

- Managed Services

- Hardware

- By End-user Industry

- Automotive

- Aerospace and Defense

- Chemicals and Petrochemicals

- Food and Beverage

- Pharmaceuticals and Biotechnology

- Metals and Mining

- Electronics and Semiconductors

- Oil and Gas

- Utilities and Energy

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Sweden

- Poland

- Belgium

- Austria

- Switzerland

- Norway

- Finland

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the factual base for the model and keep the scope focused on manufacturing operations, not broader digital spending. We reviewed public sources such as Eurostat industry and ICT statistics, European Commission policy and funding releases, OECD manufacturing and productivity indicators, and public standards and guidance from ISO and IEC.

To keep assumptions realistic, we also used annual reports, earnings decks, and product documentation from solution providers, plus reputable press coverage and association websites focused on automation and industrial digitalization. For cross-checks on company scale and activity, we referenced paid subscriptions for company financials and intelligence, and we used a patent database to identify where innovation and investment are rising. These examples are not exhaustive, and additional public and paid sources were used for data collection, validation, and scope clarification.

Primary Interviews and Surveys

Primary work focused on validating adoption patterns and spending mixes across major European manufacturing hubs, and then confirming what is counted as smart manufacturing versus adjacent automation or IT budgets. We spoke with a mix of solution providers, system integrators, plant engineering teams, and operations leaders, so we could adjust desk assumptions on penetration, replacement cycles, and the services intensity of plant deployments where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 53% | Functional/Unit leaders: 34% | |

| Smaller Players: 18% | Managers: 54% |

Market-Sizing & Forecasting

Sizing started with a top-down build where manufacturing activity in Europe was translated into an addressable digital-and-automation spend pool, then filtered by smart manufacturing adoption and use inside plants. The total was then corroborated with selective bottom-up checks, such as sampled vendor revenues, channel feedback on project sizes, and ASP-by-unit estimates for common automation layers, which helped correct totals that were being overstated or understated.

Inputs that influenced the model included industrial production and manufacturing value-added trends, automation intensity by industry, the mix of greenfield versus retrofit projects, software and services attach rates on plant deployments, and refresh cycles for control and robotics equipment. When a bottom-up signal was missing for smaller countries or niche deployments, we used proxy indicators like manufacturing output weight and technology adoption levels, then re-tested the direction through expert calls.

For forecasting, we used scenario analysis supported by a light multivariate regression, where the dependent market value was linked to manufacturing output, capital expenditure direction, and digitalization funding signals. Assumptions on adoption pace and pricing progression were stress-tested using interview feedback before the final curve was set.

Data Validation & Update Cycle

Validation was done through several checks to keep the final numbers consistent with market signals. Model outputs were compared against independent indicators such as industrial automation ordering commentary, patent activity direction, and observed rollout timelines for factory connectivity projects, and any outliers were reviewed and reworked before sign-off.

A second analyst review was used to check math, year alignment, and currency handling, followed by targeted re-contacts when large variances appeared between desk inputs and field feedback. The report is refreshed annually, and interim updates are made when major events materially change demand, pricing, or investment timing. Before delivery, a final pass is completed so clients get the most current view available.

Mordor Intelligence's Europe Smart Manufacturing Market Market Sizing Compared With Other Published Estimates

Published market sizes for Europe smart manufacturing often do not match, even when the topic name looks identical, because the counted scope and the spending triggers are not the same. Differences typically show up around what is treated as factory-floor smart manufacturing versus broader Industry 4.0 or enterprise digitization.

The main spread usually comes from whether estimates include only plant-deployed OT-IT systems and related services, or also add adjacent items like general IT modernization, generic cloud spend, and wider industrial software not tied to production assets. Timing choices also matter, since some publishers report different base years, apply different EUR-USD conversion timing, or use aggressive adoption curves without re-checking replacement cycles and services attach rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 62.31 B (2025) | |

| Industry Research Publisher A | USD 63.09 B (2025) | Often uses a wider Europe definition and a broader component bucket that can pull in adjacent digital transformation spend, which can lift totals when enterprise software and general IT upgrades are counted alongside factory deployments. |

| Industry Blog B | USD 26.60 B (2025) | Typically applies a narrower scope focused on selected automation hardware and near-term plant projects, and may undercount software platforms and integration services that expand the total addressable spend. |

Taken together, the table shows that scope choices around plant-only deployments versus wider digitization, plus how software and services are treated, explain most of the variance across sources. By counting smart manufacturing only when OT and IT are connected inside production facilities and then cross-checking adoption and refresh assumptions through field feedback, the estimate is kept tied to a repeatable demand pool, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current valuation of the Europe smart manufacturing market?

The market stands at USD 69.87 billion in 2026 and is projected to reach USD 123.78 billion by 2031.

Which technology segment leads the market?

Industrial robotics holds the largest 27.35% share, driven by automotive and labor-substitution projects.

Why is Poland growing faster than other European countries?

Poland combines lower labor costs with government incentives, attracting investments such as Aira’s EUR 300 million heat-pump plant, resulting in a 12.32% CAGR through 2031.

How does the Cyber Resilience Act influence manufacturers?

The act mandates rigorous cybersecurity compliance for connected products and can levy fines up to EUR 15 million (USD 17.39 million) or 2.5% of global turnover, compelling firms to embed security-by-design.

Which component segment is expanding the quickest?

Edge-computing hardware is advancing at a 14.1% CAGR as manufacturers move real-time analytics closer to the production line.

What strategic moves are incumbents making to stay competitive?

Major players are acquiring AI-centric firms, such as Siemens’ USD 10.6 billion Altair deal, and forging alliances with GPU leaders to integrate advanced analytics and robotics.

Page last updated on: