Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Flexible Packaging Market Analysis by Mordor Intelligence

The Morocco Flexible Packaging Market size is projected to expand from USD 1.98 billion in 2025 and USD 2.07 billion in 2026 to USD 2.51 billion by 2031, registering a CAGR of 3.92% between 2026 to 2031.

Robust consumer spending in modern retail, the rapid rise of e-commerce fulfillment hubs, and policy-led investments in agri-food and fertilizer production are reshaping the purchasing behavior that drives the Morocco flexible packaging market. Proximity to European export corridors and a widening portfolio of value-added films, pouches, and industrial sacks give converters better pricing power even as raw-material volatility persists. Multinational players deepen their Moroccan footprints through targeted acquisitions and greenfield facilities, while local specialists pivot toward niche applications such as compostable laminates and variable-data labels. At the same time, new subsidy frameworks under the Investment Charter shorten payback periods on high-spec equipment, signaling that the Morocco flexible packaging market will move steadily toward more capital-intensive, digitally enabled production.

Key Report Takeaways

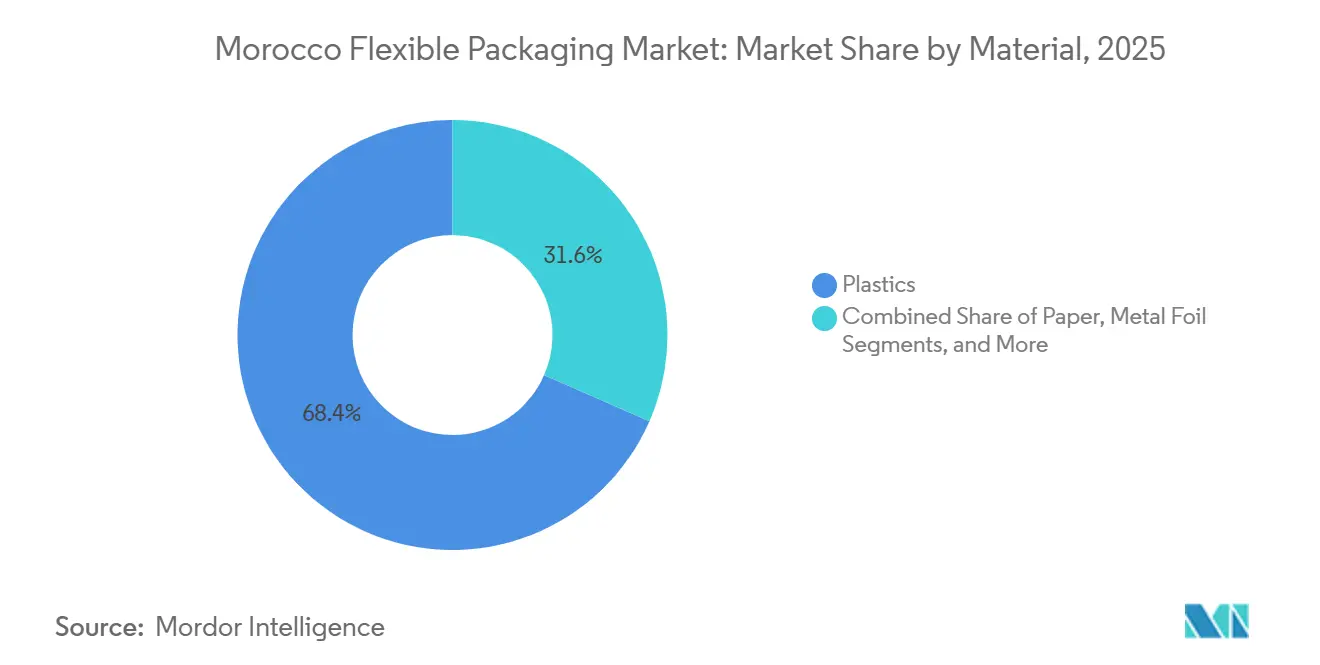

- By material, plastics led with 68.43% of Morocco's flexible packaging market share in 2025, whereas biodegradable and compostable materials are forecast to expand at a 4.73% CAGR through 2031.

- By product type, bags and pouches commanded 48.54% share of the Moroccan flexible packaging market in 2025, while sachets and stick packs have the strongest outlook, with a 4.87% CAGR between 2026 and 2031.

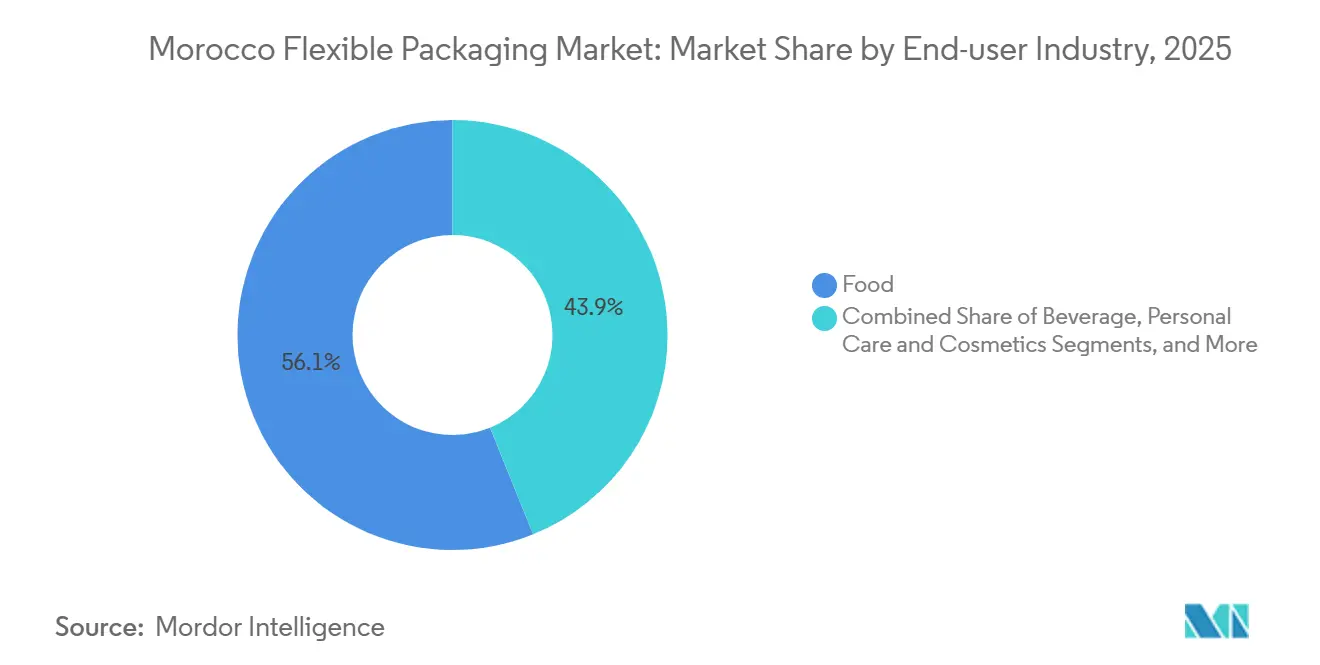

- By end-user industry, food accounted for 56.12% of 2025 revenue, yet agriculture and horticulture are projected to grow at a 5.22% CAGR through 2031.

- By printing technology, flexography held 60.21% of the Morocco flexible packaging market in 2025, but digital printing is expected to post a 4.67% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Convenient Lightweight Packs in Modern Retail and E-Commerce | +0.9% | Casablanca, Rabat, Tangier, Marrakech | Short term (≤ 2 years) |

| Demand for Sustainable and Recyclable Solutions | +0.7% | Coastal municipalities under SWITCH2CE | Medium term (2-4 years) |

| Government-Backed Agri-Food Processing Expansion | +0.8% | Souss-Massa, Gharb-Chrarda-Beni Hssen, Tadla-Azilal | Medium term (2-4 years) |

| Growth of Chilled Dairy Pouch Formats From New Aseptic Lines | +0.5% | Casablanca and Meknes clusters | Short term (≤ 2 years) |

| OCP Fertilizer Downstream Bagging Surge | +0.6% | Jorf Lasfar and Safi complexes | Long term (≥ 4 years) |

| Digital Public-Procurement Pushes Favoring Traceable Packs | +0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Convenient Lightweight Packs In Modern Retail And E-Commerce

Morocco’s modern retail penetration reached 21% of total trade in 2023, and online grocery sales touched USD 704.8 million in 2025, trends that obligate brands to specify puncture-resistant flow-wraps and tamper-evident pouches that survive automated sortation. Tourism’s rebound to 17.4 million arrivals in 2024 amplified single-serve demand in hotels and quick-service restaurants, accelerating procurement cycles for converters able to produce 10,000-unit digital runs within three days. Infrastructure builds for the 2025 African Cup of Nations and the 2030 FIFA World Cup are generating temporary spikes in snack and beverage consumption, making rapid artwork changes a baseline requirement. Lightweight structures under 50 g/m² reduce freight costs to remote worksites, such as the EUR 425 million Chtouka desalination project, where road quality increases handling risks.[1]Ministry of Environment, “Programme SWITCH to Circular Economy Value Chains,” environnement.gov.ma Collectively, these factors raise average value-added per kilogram of film and push the Morocco flexible packaging market toward high-performance co-extrusions.

Demand For Sustainable And Recyclable Solutions

The Zero Mika law bans conventional shopping bags, while Law 28-00 forbids recycled content in direct food contact, forcing converters to develop mono-material polyethylene or polypropylene laminates that remain recyclable after delamination-free wash cycles. SWITCH2CE targets a 70% recycling rate by 2030 and introduces extended producer responsibility fees that already add 2-4% to packaging costs. Paper exports of 21,000 tonnes in 2024 at USD 745 t−¹ reveal cost competitiveness that encourages fiber substitution for low-moisture foods. Centrale Danone now sources 52% of plant electricity from renewables, creating supplier scorecards that reward converters running solar arrays and closed-loop water systems. Formalizing waste pickers into cooperatives could lift bale purity above 95%, unlocking new mechanical recycling economics.

Government-Backed Agri-Food Processing Expansion

In December 2024, the World Bank approved USD 250 million to modernize cold-chain logistics, traceability, and export-grade packing lines.Generation Green mobilizes 1 million hectares of collective land and aims to create 350,000 jobs by 2030, emphasizing horticulture that requires modified-atmosphere films capable of extending shelf life to 21 days.[2]Ministry of Agriculture, “Generation Green Strategy,” agriculture.gov.ma Tomato exports approaching 700,000 tonnes require EU-compliant QR-coded pouches, lifting demand for digital printing among converters. Pilot schemes in Souss-Massa already collect used greenhouse covers for recycling into construction liners, lowering virgin-resin dependency by up to 20%. Regional investment centers can now approve mid-sized processing plants without central clearance, accelerating the adoption of flexible-pack among second-tier food processors.

Growth Of Chilled Dairy Pouch Formats From New Aseptic Lines

Centrale Danone’s Meknes site is expanding aseptic pouch output to satisfy rising per-capita dairy intake, now 85 liters in 2024. Ambient-stable 100-250 milliliter pouches lower logistics costs by MAD 0.15 per unit on 300-kilometer routes, while offering a 40% weight reduction over PET bottles. Regional processors such as Colaimo are adding ultra-high-temperature lines to target tariff-free West African exports under AfCFTA, further boosting high-barrier laminate demand. Achieving oxygen-transmission rates below 0.5 cc m−² day−¹ requires imported aluminum foils, adding USD 0.20–0.30 kg−¹ to costs, but longer shelf life offsets the premium in rural retail. Suppliers that meet ISO Class 7 cleanroom standards and BRC certification enjoy multi-year contracts, supporting capacity utilization above 85%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-Waste Regulation and Compliance Costs | -0.4% | Urban municipalities and tourist zones | Medium term (2-4 years) |

| Shortage of Food-Grade PCR Resin | -0.3% | Nationwide | Long term (≥ 4 years) |

| Volatile Polymer Import Duties | -0.2% | Nationwide | Short term (≤ 2 years) |

| Weak Reverse-Logistics Outside Casablanca | -0.2% | Marrakech-Safi,Fes-Meknes, Oriental | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Waste Regulation And Compliance Costs

Law 77-15 bans single-use bags and imposes fines up to MAD 500,000, forcing converters to maintain chain-of-custody audits for exempt industrial sacks. A 1% ecotax adds roughly MAD 100 t−¹ to polyethylene and polypropylene prices, squeezing SMEs that lack volume discounts.[3]World Bank, “Morocco Overview,” worldbank.org Forthcoming EU-aligned food-contact orders demand migration testing that costs up to MAD 15,000 per formulation, resetting qualification cycles whenever additives change. Draft producer-responsibility schemes could push 2-4% of packaging value into take-back fees, and formalizing informal collectors may raise feedstock costs by another 20-30%.[4]OECD, “OECD Economic Surveys: Morocco 2024,” oecd.org These layers of compliance erode margin headroom and defer capex for value-added printing.

Shortage of Food-Grade PCR Resin

Morocco imports most resin, and only limited domestic mechanical recycling can produce food-contact-qualified PCR under ONSSA rules. Global demand spikes and shipping volatility, therefore, expose local converters to price swings and spot shortages. Some compensate by lightweighting film gauges or blending up to 30% recyclate in non-contact layers, yet achieving EU export compliance for direct food contact remains challenging. High capital needs for chemical recycling or advanced sortation delay meaningful capacity additions until at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastics Remain Dominant While Bio-Based Laminates Advance

Plastics represented 68.43% of Morocco flexible packaging market share in 2025, with polyethylene grades supplying everyday bags, shrink films, and stand-up pouches. Biaxially oriented polypropylene delivers gloss above 85% and ink adhesion that drives premium snack wrappers, while cast polypropylene secures retort and aseptic laminates used in dairy. Polyamide and EVOH barrier layers support meat and seafood packs with shelf lives beyond 180 days, although their cost, MAD 30–50 kg−¹, limits adoption to high-value foods. The Morocco flexible packaging market for biodegradable and compostable materials is small today, yet that pool is expanding fastest at a 4.73% CAGR as PLA and PHA trials move from pilot to limited commercial runs. Mondi’s Tangier plant adds 100 million paper sacks annually, illustrating how fiber competes in dry goods where moisture exposure is minimal. Metal foil remains essential for oxygen-sensitive coffee and pharmaceutical sachets, notwithstanding its USD 0.80–1.20 m−² premium. Over the next five years, localized polymer production in OCP’s integrated petrochemical venture could reduce logistics costs and keep plastics competitive, though brand-owner sustainability pledges guarantee continued share gains for certified compostables.

The rapid growth of bio-based substrates will depend on scaling industrial composting, which remains limited to fewer than 10 certified facilities nationwide. Converters that integrate de-inking, water-based adhesives, and laser-perforation lines can command margins 200–300 basis points above commodity film averages. Regulatory clarity on carbon disclosure and recyclability labels will further accelerate the shift toward drop-in monomaterial PE or PP films that are compatible with recycling lines at reasonable cost. As the Morocco flexible packaging market matures, plastics will remain the volume engine while compostables and specialty papers capture discrete premium niches.

By Product Type: Sachets And Stick Packs Steal Share From Rigid Formats

Bags and pouches accounted for 48.54% of 2025 revenue, reflecting their versatility across food, fertilizer, and personal-care goods. Three-side-seal dairy pouches cost just MAD 0.30–0.50 per unit compared with MAD 0.80–1.20 for PET bottles, reinforcing their lead in price-sensitive rural retail. Woven polypropylene valve sacks dominate OCP fertilizer distribution with fill-weight tolerances below 0.5%. On the growth front, sachets and stick packs are forecast to post a 4.87% CAGR, capitalizing on pharmaceutical oral powders, instant coffee, and single-serve confectionery that benefit from portion control and extended shelf life. Hikma’s upcoming injectables plant will require aluminum-foil sachets with moisture-vapor transmission below 0.1 g m−² day−¹, challenging converters to meet ISO 15378 standards.

Films and wraps remain indispensable for palletizing produce exports and protecting hotel supplies in Morocco’s thriving tourism sector. Stretch-film demand directly correlates with the country’s 17.4 million tourist arrivals and the resulting bump in back-of-house logistics. Shrink sleeves and 360-degree labels are used for beverages, and ECCBC’s line expansion increases throughput and raises graphics standards. As the Morocco flexible packaging market evolves, unit-dose convenience and merchandising flexibility ensure that sachet and stick-pack formats will continue taking incremental share from legacy pillow packs and rigid containers.

By End-user Industry: Personal Care Accelerates Beyond Food Leadership

Food applications captured 56.12% of 2025 revenue, driven by Morocco’s USD 16.2 billion agri-food sector and 2,100 processors. Edita’s on-shore snack facility, producing 400,000 pouches daily, proves the economic logic of localizing high-volume confectionery packs. Vacuum-skin and MAP solutions extend protein shelf life to support modern retail meat cases, while premium biscuit brands adopt anti-fog OPP to secure window clarity. Pet food, though niche, employs degassing valves to preserve aroma, underscoring packaging sophistication gains.

Agriculture and horticulture will grow fastest at a 5.22% CAGR, driven by 40,000 hectares of greenhouse cultivation and EU-bound tomato exports, which already consume roughly 14,000 tonnes of stretch wrap. Souss-Massa growers need UV-stabilized PE films rated for up to 36 months of outdoor exposure, prompting steady demand for prime virgin resin. Beverage expansion follows ECCBC’s USD 77.6 million line upgrade, combining shrink-bundle films and tamper-proof sleeves for carbonated soft drinks and juices. Healthcare and pharmaceuticals will absorb high-barrier laminates once Hikma and Cooper Pharma bring new capacity online. Across sectors, sustainability scorecards and traceability codes intensify pressure on package design, bolstering the Morocco flexible packaging market outlook.

By Printing Technology: Digital Presses Gain Ground On Variable-Data Needs

Flexography accounted for 60.21% of the 2025 value, thanks to high-speed runs exceeding 300 m min−¹ and ink costs below USD 1.20 kg−¹. Water-based and UV-curable systems replace solvent inks to meet air-emission rules, though new dryers raise capex requirements. Rotogravure remains unmatched for 500,000-meter commodity runs, yet the high costs of cylinder engraving and 10-day lead times discourage frequent artwork changes. Digital printing, forecast to grow at a 4.67% CAGR, thrives on Morocco’s e-procurement rules that mandate QR codes and batch-level serialization for state purchases on. Inkjet presses eliminate plates, enabling profitable runs of 500 meters and language versioning for Arabic, French, and Berber in a single shift.

While offset and screen technologies have carved out specific niches, particularly in laminated tubes and heavy-duty sacks, the emphasis remains on abrasion resistance, even at a higher cost. Looking ahead, there's a notable trend: a 10-15% shift from traditional flexographic printing to digital methods. This transition is especially pronounced for labels on export produce, where farm-of-origin data is paramount.

Geography Analysis

Casablanca-Settat, Morocco's industrial heart, accounts for over half of the nation's industrial turnover and two-thirds of its investments. This concentration has birthed a bustling ecosystem, home to resin suppliers, press maintenance teams, and ISO 9001 and BRC-certified quality control labs. Such a dense industrial cluster has led to reduced inbound freight costs, solidifying the region's status as the cornerstone of Morocco's flexible packaging market. Meanwhile, the Tanger-Tétouan-Al Hoceima region is capitalizing on the expansive nine-million-TEU capacity of the Tanger Med Port. This strategic advantage allows for swift deliveries to European clients within a tight 72-hour window. Notably, both ALPLA's preform plant and Mondi's paper-bag facility are heavily reliant on this port for their just-in-time export needs.

Morocco's geographical proximity, just 14 kilometers from Spain, bolsters its role as a pivotal player in free-trade logistics, catering to the European Union, the United States, and Turkey. The upcoming Nador West Med port, set to commence operations in 2026 with a robust capacity of 3.4 million TEUs, promises to revolutionize logistics. By slashing Mediterranean dwell times to under two days, the port enhances the cold-chain integrity crucial for produce and pharmaceutical exports. However, challenges persist. Outside the bustling Casablanca, fewer than 20 sorting centers are operational, resulting in a subpar PCR collection rate of under 25% in the more rural provinces. Furthermore, converters situated in the Marrakech-Safi and Oriental provinces face hurdles, having to import food-grade pellets at a premium of USD 210–315 per ton, which curtails their ability to utilize recycled content.

While Morocco's southern provinces, rich in phosphate mining and fisheries, present a promising demand for industrial films, infrastructural challenges like road and power limitations dampen immediate investment enthusiasm. Despite these hurdles, the allure of Morocco's flexible packaging market remains strong. Regional disparities necessitate that converters judiciously weigh factors like proximity to ports, availability of subsidies, and logistics of feedstock when deciding on new capacity allocations. As the landscape evolves, the balance of these considerations will shape the future of Morocco's flexible packaging industry.

Competitive Landscape

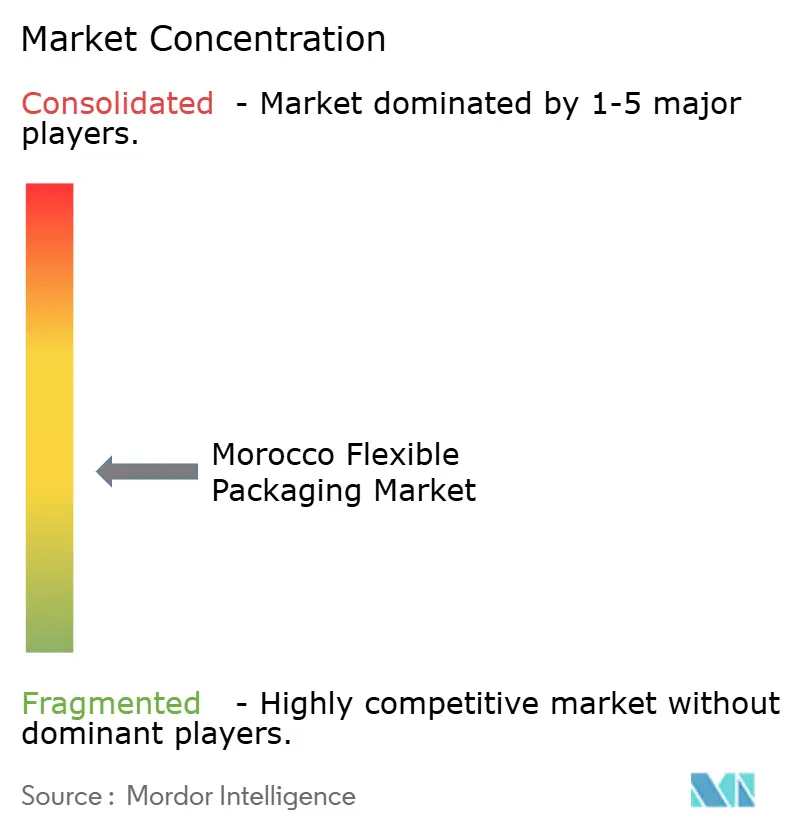

Morocco's flexible packaging market is characterized by a moderate level of fragmentation. Multinational converters, including Amcor, Mondi, and ALPLA, collectively hold an estimated 35% to 40% market share. These industry giants leverage their scale advantages in resin procurement, maintain multi-site production networks, and possess advanced technical capabilities in barrier coatings and aseptic lamination. In contrast, regional specialists like Altea Packaging and local entities such as Manusac, Unibag Maghreb, and Atlantic Packaging (now under ALPLA's wing) focus on proximity, customization, and expedited lead times, catering primarily to mid-volume orders. A notable move in the market was Mondi's establishment of a greenfield paper-bag plant in Tangier, with an investment of EUR 16 million (USD 18 million) in December 2022. This facility, boasting an annual output of 100 million bags, not only elevates West African capacity to over 500 million units but also underscores a strategic shift towards fiber-based substrates. This pivot aligns with Morocco's circular-economy initiatives and the sustainability goals of European clientele. Such a shift intensifies the pressure on polyethylene-centric converters, urging them to either invest in monomaterial structures or face potential margin declines.

ALPLA's strategic maneuvers further highlight the market's dynamics. In November 2023, ALPLA acquired Atlantic Packaging, a move that not only tripled the preform output from 100 million to a staggering 300 million units annually but also secured a prime 12,000-square-meter site in Tangier. With an additional 20,000 square meters earmarked for expansion, this acquisition underscores the significance of vertical integration within the beverage and dairy supply chains. Long-term contracts with industry giants like Centrale Danone and ECCBC (the Coca-Cola bottler) not only provide volume predictability but also validate ALPLA's hefty investments in blow-molding and aseptic-filling technologies.

As the market evolves, certain areas present lucrative opportunities. One such area is the supply of food-grade post-consumer recycled resin. However, challenges loom large. Law 28-00 in Morocco prohibits recycled content from direct food contact, creating a pressing demand for advanced chemical recycling technologies. Techniques like pyrolysis and depolymerization can produce virgin-equivalent polymers, a capability Morocco currently lacks. Establishing a 20,000-tonne-per-year plant, a venture estimated to cost between USD 30 million to USD 50 million, is essential to bridge this gap. Meanwhile, Morocco's digitalized procurement platform, launched in August 2023, mandates digital traceability for public procurement. This push favors converters who invest in advanced digital presses, capable of printing variable QR codes and multi-language labels without the need for plate changes. Companies like Hotpack and Constantia Flexibles are already testing these capabilities in pharmaceutical and export-produce sectors, highlighting the industry's shift towards digitalization.

Morocco Flexible Packaging Industry Leaders

Amcor plc

Mondi plc

ALPLA Werke Alwin Lehner GmbH & Co KG

Hotpack Packaging Industries LLC

Altea Packaging SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ECCBC invested MAD 715 million (USD 77.6 million) to add two lines at its Nouaceur beverage plant, raising shrink-film and multi-pack demand.

- May 2025: Cooper Pharma entered a strategic cooperation with Jemincare to boost generic-drug output, creating incremental requirements for high-barrier sachet laminates.

- December 2025: The World Bank approved USD 250 million for cold-chain and traceability upgrades across Morocco’s agri-food sector, prioritizing modified-atmosphere and aseptic pouches.

- December 2024: The World Bank approved USD 250 million for cold-chain and traceability upgrades across Morocco’s agri-food sector, prioritizing modified-atmosphere and aseptic pouches.

- December 2024: APM Terminals completed a 2 million TEU expansion at MedPort Tangier, boosting total capacity to 5.2 million TEUs and enhancing regional packaging logistics.

Morocco Flexible Packaging Market Report Scope

The Morocco Flexible Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foil, Biodegradable Materials), Product Type (Bags and Pouches, Films and Wraps, Sachets and Stick Packs), End-user Industry (Food, Beverage, Healthcare, Personal Care, Agriculture), and Printing Technology (Flexography, Rotogravure, Digital Printing). Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Biodegradable and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

By End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Biodegradable and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Other Product Types | ||

| By End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-Use Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the projected value of the Morocco flexible packaging market by 2031?

The market is forecast to reach USD 2.51 billion by 2031, expanding at a 3.9% CAGR from 2026.

Which product type is growing fastest across Moroccan converters?

Sachets and stick packs are expected to post the highest growth, with a 4.87% CAGR through 2031, driven by single-serve demand in pharmaceuticals and confectionery.

Why are biodegradable materials gaining share in Morocco’s flexible pack segment?

SWITCH2CE recycling targets and the Zero Mika bag ban push brand owners toward compostable stand-up pouches and bio-based laminates that meet evolving regulatory standards.

How will OCP Group’s investment program affect flexible packaging demand?

OCP’s expansion to 20 million t y−¹ of fertilizer output will require an additional 40,000–50,000 tonnes of woven polypropylene valve bags each year.

What regions outside Casablanca are attracting new converter investment?

Incentive bonuses are directing greenfield projects to Fes-Meknes, Marrakech-Safi, and Souss-Massa, where land is cheaper, but utilities and reverse logistics need upgrading.

Which printing technology is set to gain share by 2031?

Digital printing is forecast to grow at a 4.67% CAGR, driven by variable-data requirements in public procurement and e-commerce packaging.

Page last updated on: