Europe Private 5G Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

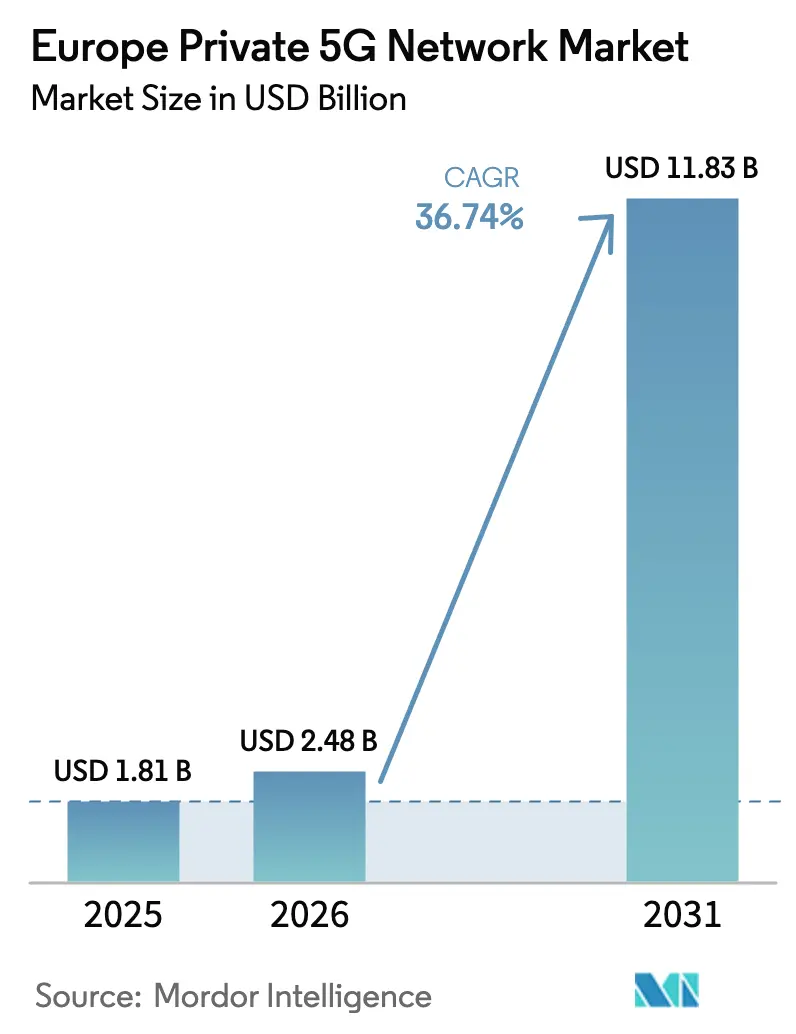

| Base Year Market Size (2025) | USD 1.81 Billion |

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 11.83 Billion |

| Growth Rate (2026 - 2031) | 36.74% CAGR |

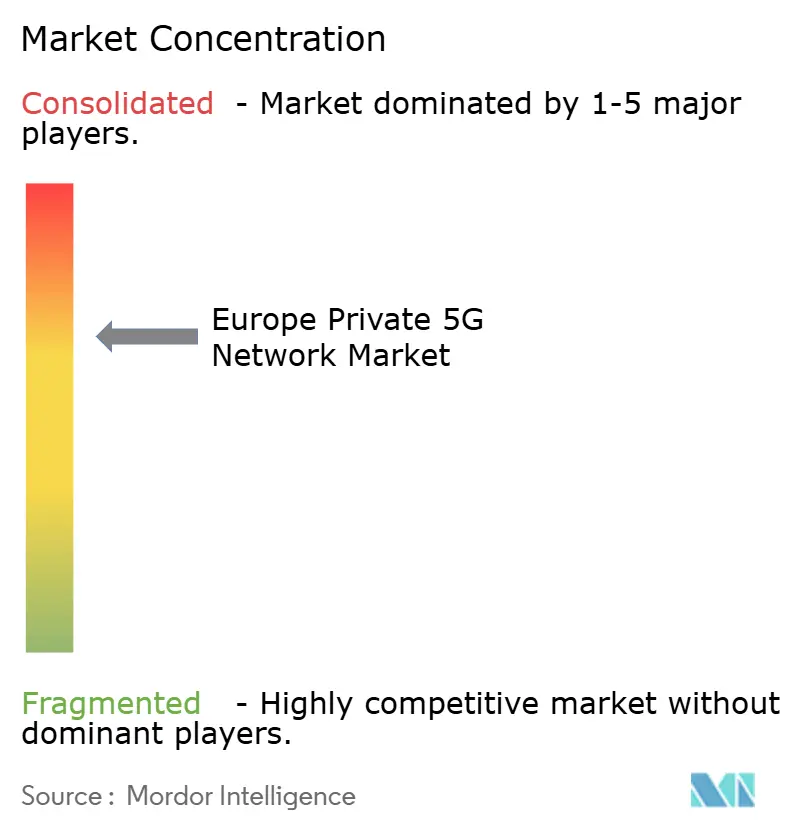

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Private 5G Network Market Analysis by Mordor Intelligence

Europe Private 5G Network Market size in 2026 is estimated at USD 2.48 billion, growing from 2025 value of USD 1.81 billion with 2031 projections showing USD 11.83 billion, growing at 36.74% CAGR over 2026-2031.

This substantial Private 5G network market size growth reflects enterprises’ urgency to secure ultra-reliable, low-latency wireless infrastructure that guarantees data sovereignty and operational autonomy from public cellular networks. Regulatory milestones, such as the European Union’s carbon-border adjustment mechanism, are also catalyzing real-time emissions monitoring requirements that only dedicated 5G can satisfy. Industrial digitalization programs, spectrum liberalization in the 3.8 – 4.2 GHz band, and the commercialization of mmWave solutions together anchor demand. Germany continues to lead in large-scale campus deployments, while the United Kingdom registers the fastest expansion owing to local spectrum licensing and marquee maritime rollouts. Service-centric business models and Network-as-a-Service (NaaS) offerings are lowering adoption barriers, enabling small and medium enterprises (SMEs) to participate in the Private 5G network market and reinforcing the market’s long-term momentum.

Key Report Takeaways

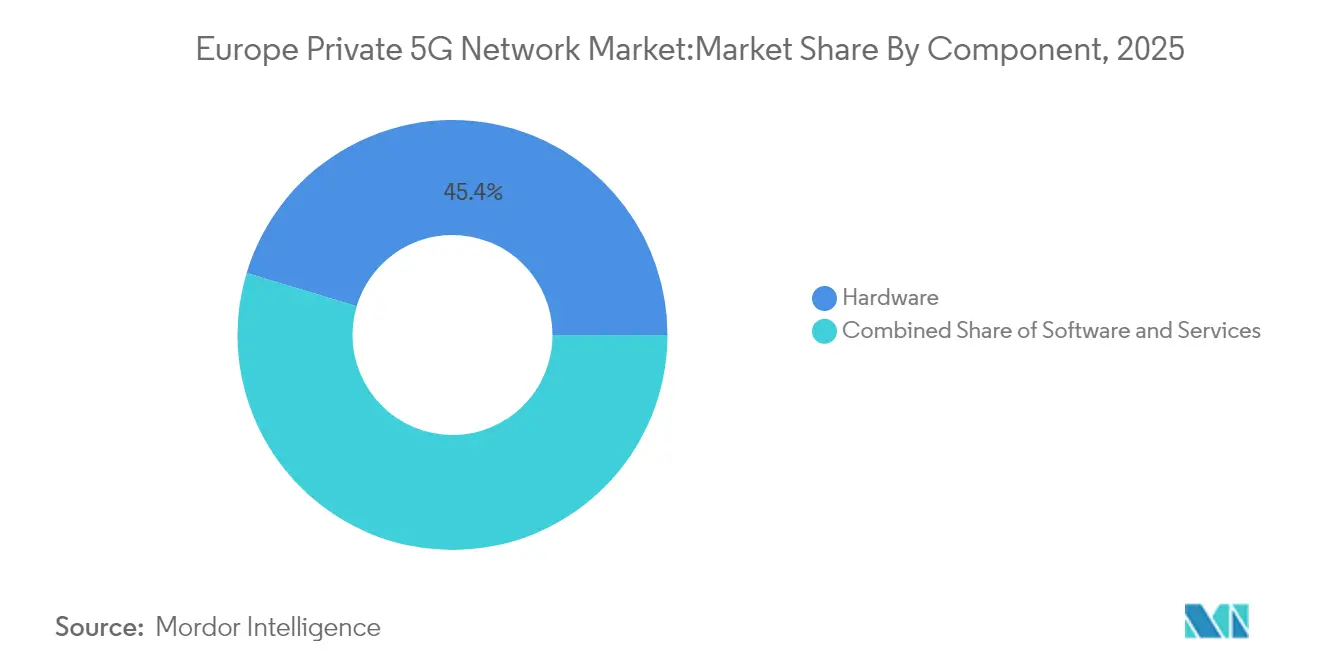

- By component, hardware accounted for 45.35% of the Private 5G network market share in 2025, whereas services are forecast to grow at a 44.92% CAGR through 2031.

- By frequency, the 26 GHz band is set to achieve a 59.40% CAGR, the fastest within the Private 5G network market.

- By spectrum model, unlicensed and shared bands are projected to expand at 37.60% CAGR, reshaping cost dynamics.

- By deployment model, Network-as-a-Service is advancing at 38.20% CAGR and is expected to erode stand-alone dominance.

- By enterprise size, SMEs are predicted to register a 39.90% CAGR, highlighting democratization trends.

- By end-user industry, healthcare is on track to grow at 38.10% CAGR, outpacing manufacturing’s current 37.45% contribution to the overall Private 5G network market size.

- By country, Germany held 31.62% Private 5G network market share in 2025, while the United Kingdom is poised for a 37.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Private 5G Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-reliable low-latency industrial connectivity | +8.50% | Germany, Nordics, Central Europe | Medium term (2-4 years) |

| Industry 4.0-led enterprise digital transformation | +7.20% | Germany, France, Netherlands | Long term (≥ 4 years) |

| Liberalization of local spectrum licensing (3.8-4.2 GHz) | +6.80% | EU-wide, notably Germany, UK | Short term (≤ 2 years) |

| EU carbon-border emissions monitoring | +3.40% | Export-oriented EU member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for ultra-reliable low-latency industrial connectivity

Industrial production lines now require deterministic performance that public networks cannot deliver. Mercedes-Benz’s Factory 56 leverages a private 5G system to orchestrate autonomous robots and quality-inspection sensors with sub-10 millisecond latency. Public Wi-Fi has proven inadequate for such mission-critical workloads. ArcelorMittal’s 5G-enabled steel plant in Dunkirk extends the concept by running augmented-reality maintenance and autonomous rail vehicles that rely on 99.99% availability. Growing industrial IoT density compounds bandwidth needs, while artificial-intelligence decision loops amplify the value of on-premises data processing and private spectrum control. As a result, dedicated wireless networks have become foundational rather than experimental, driving scale in the Private 5G network market.

Industry 4.0-led enterprise digital transformation

European manufacturers are embedding private 5G into wider digitization roadmaps that unite edge analytics, digital twins, and predictive maintenance. Siemens operates multiple German factories on site-licensed 3.7 – 3.8 GHz spectrum to power mobile robotics and autonomous logistics[2]Siemens AG, “5G Smart Factory Deployments,” siemens.com. Volkswagen’s Wolfsburg complex employs private 5G to interlink production lines for smart-factory orchestration. Pairing 5G with edge platforms keeps sensitive data local, aligning with EU sovereignty mandates and enabling virtual replicas of machinery that optimize uptime. These large-scale deployments raise peer expectations across automotive, food, and chemicals, reinforcing growth in the Private 5G network market.

Liberalization of local spectrum licensing (3.8-4.2 GHz)

The German regulator set a precedent by reserving 100 MHz for industrial users at nominal fees, sparking a wave of license applications. Twenty-one EU countries now operate comparable frameworks, allowing enterprises to secure dedicated channels without mobile operator mediation. Easy access to mid-band spectrum has eroded a key structural barrier, unlocking the business case for private campus networks and accelerating uptake within the Private 5G network market.

EU carbon-border rules expanding energy-monitoring use cases

Mandatory real-time emissions reporting drives dense sensor rollouts that demand uninterrupted connectivity. Enterprises adopt private 5G to stream environmentally and process data securely to on-site AI engines for immediate optimization. EDF’s nuclear facilities already leverage private LTE and roadmap 5G upgrades to comply with evolving regulations. As carbon audits grow stricter, emissions-intensive exporters are expected to accelerate private network deployments across Europe, adding momentum to the Private 5G network market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and OPEX for brownfield plants | -5.20% | Industrial regions across Europe, particularly Germany and Italy | Short term (≤ 2 years) |

| Fragmented spectrum policy across member states | -3.10% | EU-wide, with particular challenges in cross-border operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and OPEX for brownfield plants

Retrofitting legacy factories demands costly radio planning, rugged device integration, and sometimes production downtime. The OECD notes that SMEs struggle to justify these expenditures despite strong digital ambitions[3]OECD, “SME Digitalization Outlook,” oecd.org. NaaS offerings from Boldyn Networks now shift investment from capital to operating budgets, but recurring license and maintenance costs still deter cash-constrained operators, tempering a portion of the Private 5G network market’s potential.

Fragmented spectrum policy across member states

While the European Commission promotes harmonization, procedural variations remain. Enterprises with cross-border footprints must navigate separate applications, equipment certifications, and interference protocols, complicating network design and inflating costs. Absence of private network roaming rules further inhibits seamless logistics corridors. These inconsistencies dampen deployment velocity in the Private 5G network market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services accelerate monetization

Hardware captured 45.35% of revenue in 2025, covering radios, core servers, and edge compute modules that form the skeletal layer of any deployment. However, services are expanding at a 44.92% CAGR as enterprises opt for design, integration, and full life-cycle management rather than owning assets outright. Managed services platforms allow organizations to scale capacity on demand and offload security tasks to accredited specialists. For example, Ericsson’s carrier-grade 5G Core-as-a-Service empowers operators to provision enterprise slices in minutes. This shift indicates commercial maturity: decision makers prefer predictable OPEX over lumpy CAPEX, a trend that will reinforce the trajectory of the Private 5G network market.

At the same time, support contracts covering updates, optimization, and incident response ensure high availability, transforming vendor relationships into long-term partnerships. Systems integrators that combine vertical expertise with 5G skill sets stand to capture consulting spend, especially where factories must knit 5G into existing manufacturing execution systems. As a result, services are expected to hold an outsized portion of the future Private 5G network market size relative to hardware.

By Frequency: mmWave unlocks data-intensive use-cases

Sub-6 GHz accounted for 77.30% of deployments in 2025 because it offers balanced propagation inside metal-dense environments. Nevertheless, the 26 GHz band is forecast to post a 59.40% CAGR through 2031, becoming a magnet for factory segments that require multi-gigabit uplink. Deutsche Telekom’s industrial campus solution already sustains 4 Gbps downlink with 3-4 millisecond latency on mmWave. Though denser radio grids raise costs, the capacity dividend justifies investment for computer-vision quality checks and real-time AI inference. Hybrid architectures, where mmWave hot-zones complement broader mid-band coverage, are emerging as the reference design and will continue to enlarge the Private 5G network market.

Coverage limitations can be mitigated by smart antenna steering and reflective surfaces, while device ecosystems are maturing as chipsets from Qualcomm and MediaTek add industrial temperature support. Rapid improvements in beam-tracking algorithms further enhance reliability, fostering confidence among conservative process-automation buyers.

By Spectrum Model: Unlicensed gains commercial traction

Licensed spectrum still underpins 45.20% of deployments because interference control is critical for mission-critical machinery. However, 5G NR-U, which uses 5 GHz and 6 GHz bands, is set for a 37.60% CAGR as enterprises weigh cost against performance. NR-U permits rapid proof-of-concept builds with simple regulatory notification rather than full licensing. SMEs find the model attractive, particularly when paired with cloud-hosted cores that streamline management. Dual-slice architectures marry licensed mid-band for safety loops and unlicensed high-bandwidth lanes for analytics, maximizing spectral efficiency and broadening the Private 5G network market.

Equipment vendors have responded by integrating dynamic channel-selection engines that sense neighboring interference and reprioritize traffic in real time. Regulatory bodies in France and the Netherlands are pilot-testing coordinated database solutions to formalize interference management for industrial NR-U, which should further expand adoption.

By Deployment Model: Network-as-a-Service lowers entry barriers

Stand-alone systems secured 41.35% revenue in 2025 due to early adopters’ preference for total control. Yet NaaS will record a 38.20% CAGR as flexible subscription structures resonate with CFOs. Boldyn Networks’ four-tier Private 5G-as-a-Service model allows clients to start with an innovation tier and graduate to mission-critical coverage without changing hardware. Edge automation and AI-driven operations mitigate skills shortages, letting operators run sophisticated policies via graphical dashboards. Consequently, NaaS is predicted to claim a double-digit share of the Private 5G network market size by 2031.

Hybrid public-private models also advance, interconnecting campus cores with operator clouds to maintain mobility for field staff. Seamless handover between public and private slices reduces downtime and ensures enterprise traffic remains encrypted end-to-end, further enlarging the addressable base for the Private 5G network market.

By Enterprise Size: SMEs gain momentum

Large corporations held 62.20% of spending in 2025, having both budget and in-house engineering resources. However, SMEs are projected to expand at 39.90% CAGR as simplified deployment kits and targeted government grants close capability gaps. Plug-and-play starter kits featuring compact radios and cloud-hosted core networks can be commissioned within days, letting smaller factories upgrade legacy SCADA links without protracted projects. The European Recovery and Resilience Facility earmarks digitalization funds that specifically address SME connectivity, further broadening penetration in the Private 5G network market.

Vendor ecosystems now offer verticalized blueprints such as “pharma-in-a-box” or “food-processing-in-a-box,” incorporating pre-certified devices and orchestration templates. These shrink risk for first-time adopters and support the inclusive growth narrative of the Private 5G network industry.

By End-User Industry: Healthcare accelerates adoption

Manufacturing retained a 37.45% revenue share in 2025, but healthcare is projected to have a 38.10% CAGR. Europe’s first 5G Standalone hospital network in Oulu enables low-latency image transfer, remote consultations, and AR-assisted surgery. Pandemic-era telehealth growth highlighted the need for deterministic wireless inside clinical environments, where interference or latency gaps are unacceptable. Simultaneously, pharmaceutical plants demand secure connectivity for continuous environmental monitoring and real-time batch tracking, integrating private 5G into good-manufacturing-practice workflows. These cross-sector tailwinds position healthcare as a pivotal contributor to the expanding Private 5G network market.

Energy utilities and transportation operators also accelerate implementations. EDF’s nuclear plants employ private wireless for radiation monitoring and secure voice, while the Port of Kemi uses a campus network to orchestrate vessel traffic and shorten turnaround. Such multi-industry adoption confirms that the Private 5G network market has progressed beyond single-vertical dependence.

Geography Analysis

Germany commands 31.62% of today’s Private 5G network market size across Europe. Nominal spectrum fees, state-backed Industry 4.0 programs, and leadership from Siemens and Deutsche Telekom combine to keep campus network rollouts brisk. Deutsche Telekom plans to extend national 5G coverage from 78% to 95% by 2027, ensuring macro support for hybrid public-private models.

The United Kingdom is poised for a 37.10% CAGR through 2031, propelled by Ofcom’s local licensing portal and investments from BT, Vodafone, and a vibrant neutral-host ecosystem. Maritime logistics showcases early success: Southampton port’s private network now tracks container moves and autonomous tugs in real time, slashing berth delays. France and the Nordics form a high-innovation belt. France hosts flagship deployments at ArcelorMittal and EDF nuclear sites, while Sweden and Finland spearhead defense-grade Open RAN and port-automation projects. The Netherlands and Belgium leverage logistics positions to equip rail yards and warehouses, gradually lifting their share of the Private 5G network market. Southern Europe, led by Italy and Spain, is catching up as spectrum prices ease and municipal smart-city bids begin to specify private 5G clauses. Collectively, these regional dynamics diversify revenue streams and add resilience to overall Private 5G network market growth.

Competitive Landscape

The European Private 5G network market remains moderately concentrated. Nokia leads with 890 private-wireless customers worldwide and reports that enterprise now constitutes 13.5% of group revenue. Ericsson follows closely, leveraging its AI-infused 5G Core-as-a-Service to close managed service deals across ports and utilities. Cisco partners with NEC to widen the distribution of its 5G packet core, aiming for mid-market customers that prefer turnkey bundles.

Specialist providers are intensifying rivalry. Boldyn Networks expanded rapidly by purchasing Cellnex’s EDZCOM unit, inheriting over 50 operational networks and launching a tiered NaaS catalog. Regional systems integrators such as SPIE focus on public-safety use cases, while hyperscalers collaborate with telecom vendors to combine edge compute and network slices on a single invoice. Competition increasingly hinges on vertical expertise, integration speed, and flexible pricing rather than pure hardware performance, shaping the strategic contours of the Private 5G network industry.

Commercial alliances are growing in importance. Ericsson and Google Cloud bundle AI life-cycle management with on-demand core functions to shorten time-to-market for operators entering enterprise segments. Deutsche Telekom and Qualcomm are refining mmWave reference architectures to court automotive OEMs. Such partnerships accelerate innovation and will likely compress timeframes between technology generations, keeping pressure on incumbents to reinvest in R&D and ecosystem development.

Europe Private 5G Network Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co Ltd.

Nokia Corporation

Telefonaktiebolaget LM Ericsson

Deutsche Telekom AG (T-Systems)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson, SPIE, and Unitel deployed a private 5G network in Istres, France, supporting AI-enabled public-safety services.

- June 2025: Ericsson and Google Cloud launched carrier-grade 5G Core-as-a-Service, embedding AI for automated scaling.

- February 2025: Nokia sealed a new 5G agreement with Orange France to modernize private networks nationwide.

- November 2024: Boldyn Networks introduced tiered Private 5G-as-a-Service packages aimed at lowering upfront costs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Europe private 5G network market as all on-premise or campus-wide 5G RAN, core and edge solutions deployed by enterprises or public entities for exclusive use, independent or logically separated from public mobile networks.

Scope exclusion: Public 5G macrocells that merely dedicate slices to enterprise traffic are not covered.

Segmentation Overview

- By Component

- Hardware (Servers, RAN, MEC)

- Software (Core, Network Slicing, Orchestration)

- Services (Design and Integration, Managed, Support)

- By Frequency

- Sub-6 GHz (3.3-4.2)

- 700 MHz

- 26 GHz mmWave

- By Spectrum Model

- Licensed

- Shared/Local

- Unlicensed (NR-U)

- By Deployment Model

- Stand-Alone (SA)

- Hybrid (Public-Private)

- Network-as-a-Service

- By Enterprise Size

- SMEs

- Large Enterprises

- By End-user Industry

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Defense and Public Safety

- Healthcare

- Smart Cities and Campuses

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics (DK, SE, FI, NO)

- Benelux

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed network architects at system integrators, operational leads at manufacturing plants, and policy specialists inside telecom regulators across Germany, the United Kingdom, France, Italy, Spain, and the Nordics. These discussions validated spectrum usage patterns, realistic per-site capital outlays, and adoption hurdles, filling gaps that secondary sources leave open.

Desk Research

We began with open datasets that anchor European connectivity trends, such as Eurostat's ICT usage panels, the European Commission spectrum inventory, GSMA Intelligence adoption trackers, and ETSI work items, because they reveal addressable site counts, spectrum availability, and device readiness. Trade bodies including 5G-ACIA and the European Automobile Manufacturers Association supply granularity on industrial use cases, while national regulators (Ofcom, Bundesnetzagentur, ARCEP, ComReg) publish license grants that signal deployment velocity. Company filings and press releases enrich vendor shipment and pricing context, and paid platforms like D&B Hoovers and Dow Jones Factiva add revenue splits and project announcements that are rarely in the public domain. The sources listed illustrate our desk work and are not exhaustive.

Market-Sizing & Forecasting

We apply a top-down model that reconstructs spend from production and trade data on 5G radio units, small cells, and MEC servers, then align it with enterprise penetration rates in key verticals. Bottom-up cross-checks, sampled supplier shipments multiplied by average selling price brackets, calibrate totals. Variables tracked include spectrum fee trajectories, campus footprint averages, indoor/outdoor radio mix, device attach ratios, and Industry 4.0 grant flows; each feeds multivariate regression that projects value through 2030. When supplier roll-ups under- or over-shoot the top-down baseline, gaps are reconciled through follow-up calls and scenario analysis.

Data Validation & Update Cycle

Outputs pass three layers of review: automated variance flags, peer analyst audits, and finally senior sign-off. We refresh every twelve months, and an interim update is triggered if spectrum policy, equipment ASPs, or more than 10 MW of new factory floor space materially shift demand. Just before publication, an analyst re-runs key formulas so clients receive the latest view.

Credibility Anchor: Why Our Europe Private 5G Network Baseline Commands Reliability

Published estimates diverge because firms pick different inclusions, base years, and validation rigor.

Some bundle public-slice revenue, while others model hardware only.

Key gap drivers include:

Scope: several studies mix public network slicing revenues with true standalone deployments.

Forecast logic: certain publishers extrapolate linear device shipments without reconciling site-level CapEx ceilings or spectrum fees.

Refresh cadence: figures built on 2022 data miss the 2024 German and French license waves that Mordor incorporates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.81 B (2025) | Mordor Intelligence | - |

| USD 678 M (2022) | Regional Consultancy A | Excludes software and services; hardware-only model |

| USD 568 M (2023) | Trade Journal B | Uses limited country set; omits Nordics and Benelux |

| USD 1.14 B (2022) | Global Consultancy C | Combines private LTE with private 5G; no spectrum fee adjustments |

In sum, by aligning clearly defined scope with updated regulatory and shipment data and by validating every assumption with market participants, Mordor Intelligence delivers a dependable, transparent baseline that decision-makers can trace back to explicit variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the European private 5G network market by 2031?

It is expected to reach USD 11.83 billion, reflecting a 36.74% CAGR from 2026.

Which segment is expanding fastest in the European private 5G network market?

The services component segment is growing at 44.92% CAGR as enterprises favor managed and NaaS offerings.

Why is the 26 GHz band gaining traction in private 5G deployments?

It delivers over 4 Gbps throughput and sub-5 millisecond latency, enabling high-resolution video analytics and AI at the industrial edge.

How does spectrum liberalization influence private 5G adoption?

Affordable local licenses in the 3.8 – 4.2 GHz band remove a key cost barrier, encouraging factories and logistics hubs to build dedicated networks.

Which European country holds the largest share of the Private 5G network market?

Germany leads with a 31.62% share due to favorable policy, dense manufacturing, and strong telecom vendor presence.

What factors could restrain the Private 5G network market in the short term?

High retrofit costs for brownfield sites and fragmented spectrum policies across EU member states may slow deployment for some enterprises.

Page last updated on: