C5ISR Market Size and Share

Market Overview

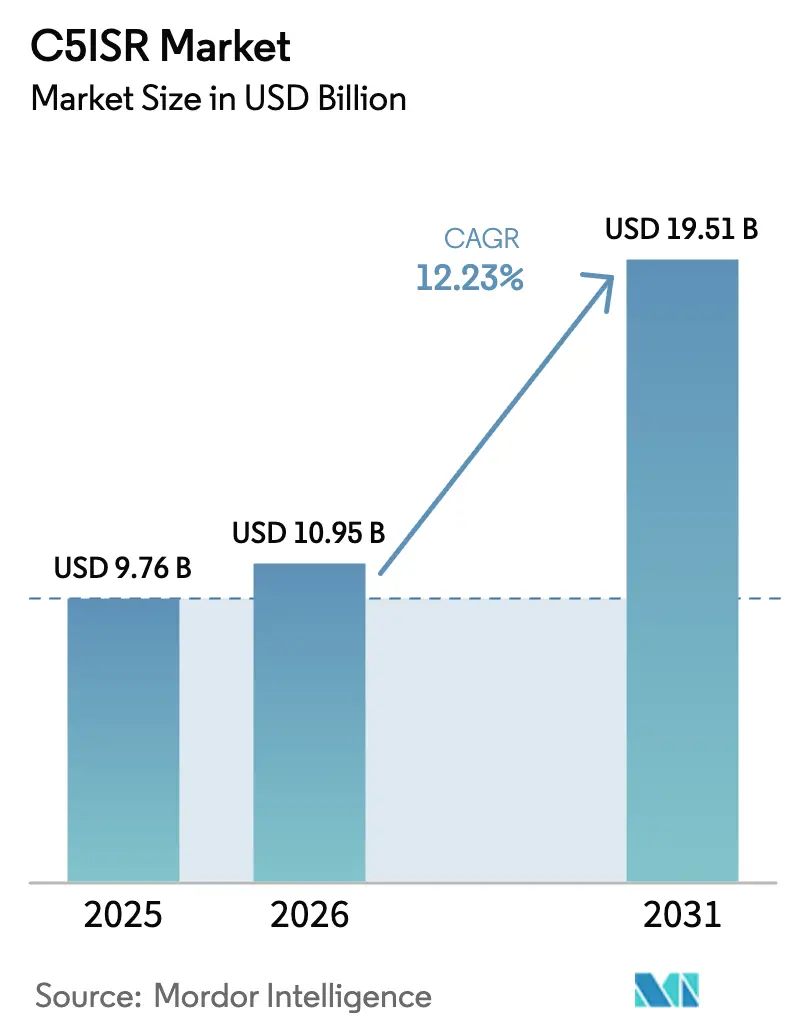

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.95 Billion |

| Market Size (2031) | USD 19.51 Billion |

| Growth Rate (2026 - 2031) | 12.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

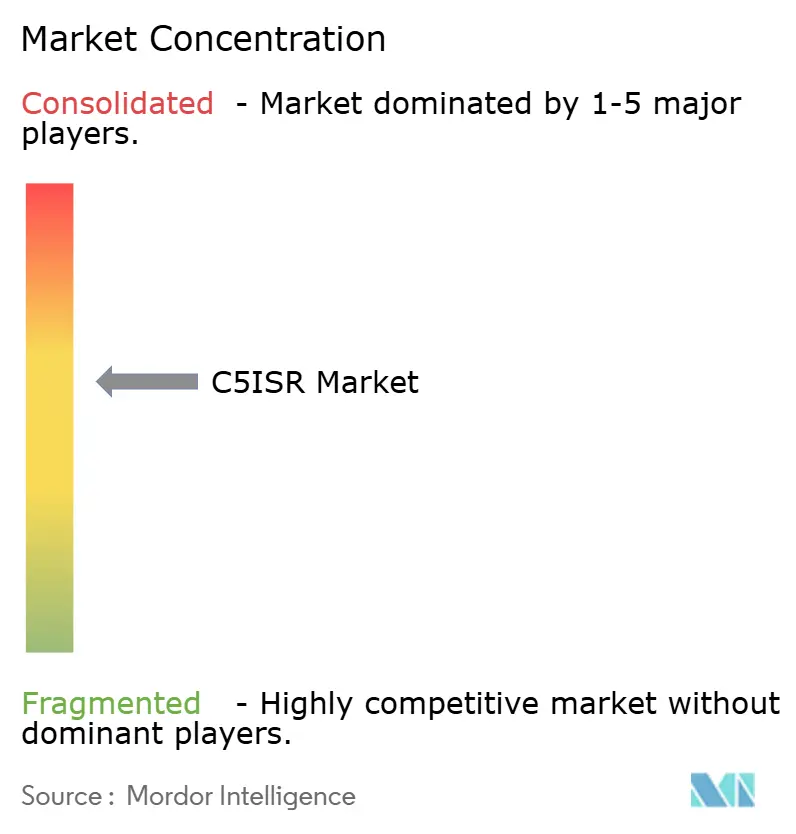

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

C5ISR Market Analysis by Mordor Intelligence

The C5ISR market size was valued at USD 9.76 billion in 2025 and estimated to grow from USD 10.95 billion in 2026 to reach USD 19.51 billion by 2031, at a CAGR of 12.23% during the forecast period (2026-2031). Sustained defense-modernization outlays, which reached USD 2.72 trillion in 2024, continue to underpin growth as armed forces seek real-time decision superiority. Investment momentum is reinforced by record regional budget hikes such as China’s 7.2% rise to USD 245 billion and Japan’s 21% surge to USD 55.3 billion in 2025. Convergence of electronic warfare and cyber operations, miniaturized multi-INT payloads, and field-deployable tactical networks are reshaping procurement priorities. Consolidation among prime contractors—exemplified by BAE Systems’ USD 5.5 billion purchase of Ball Aerospace and Boeing’s USD 8.3 billion Spirit AeroSystems bid—illustrates vertical-integration strategies that secure supply chains and novel technologies. Geopolitical flashpoints from Eastern Europe to the Indo-Pacific sustain demand for spectrum-dominance solutions even as export-control bottlenecks and talent shortages introduce execution risk.

Key Report Takeaways

- By platform, airborne systems led with 40.78% of C5ISR market share in 2025, while space-based assets are poised to expand at a 13.02% CAGR to 2031.

- By component, hardware commanded a 43.10% share of the C5ISR market size in 2025; software is projected to grow at an 11.74% CAGR through 2031.

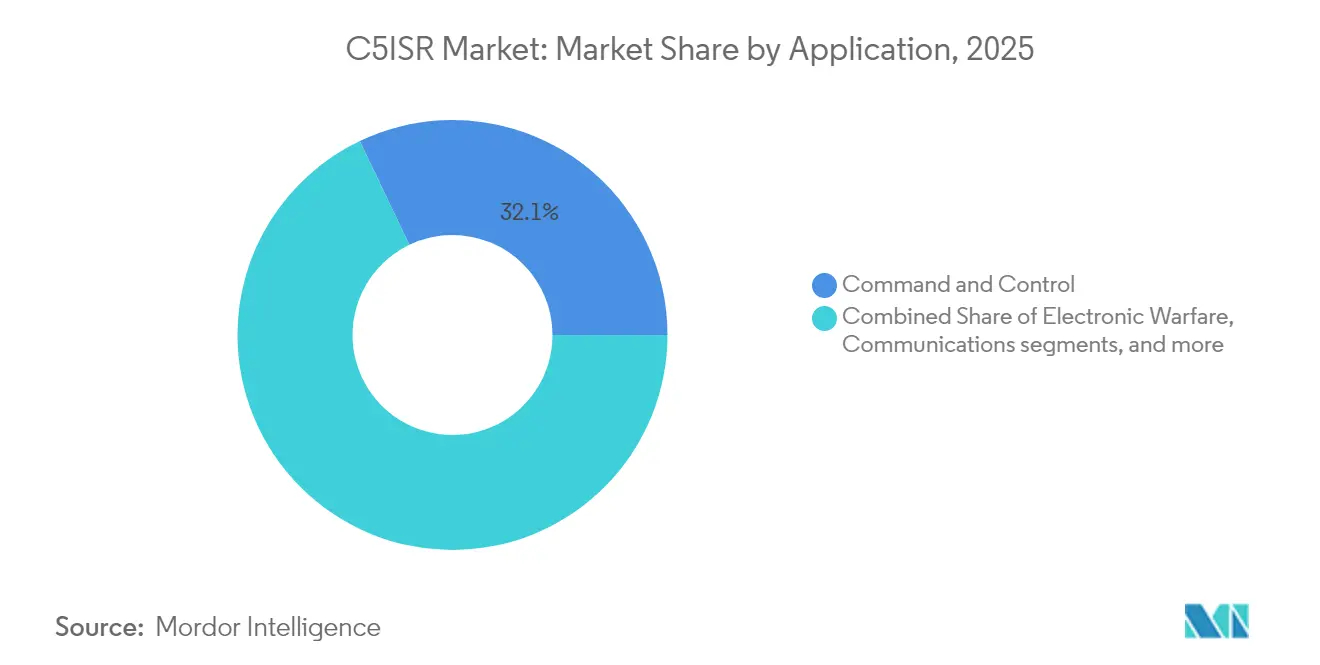

- By application, command and control (C2) captured 32.10% revenue in 2025, whereas cyber applications are set to advance at a 12.88% CAGR over the forecast period.

- By end-user, Army formations held a 39.20% share in 2025; Air Force programs exhibit the highest 12.55% CAGR as sixth-generation fighter roadmaps accelerate.

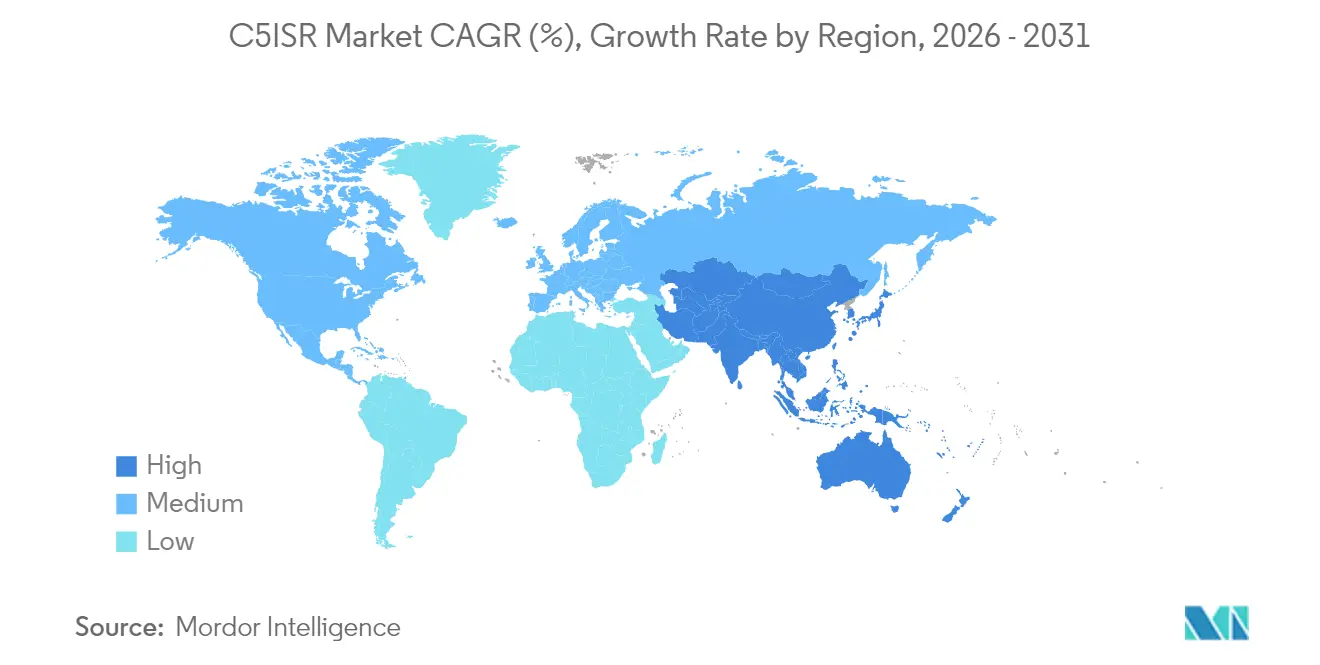

- By geography, North America accounted for 33.10% of the C5ISR market in 2025, while Asia-Pacific is the fastest-growing region at a 13.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global C5ISR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid field-deployable tactical networks | +0.8% | Global; early uptake in North America and Europe | Medium term (2-4 years) |

| Convergence of EW and cyber for spectrum dominance | +1.2% | US, China, Russia | Short term (≤2 years) |

| Miniaturised multi-INT sensor payloads for UxVs | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Defence cloud/edge AI for real-time ISR fusion | +1.1% | Global; US-led | Short term (≤2 years) |

| Budget spikes from geopolitical flashpoints | +0.7% | Conflict-adjacent regions | Short term (≤2 years) |

| Commercial LEO satcom integration | +0.6% | US, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Field-Deployable Tactical Networks Drive Operational Agility

Secure, rapidly erectable networks now arrive in theater within minutes, as demonstrated by the US Army’s USD 6.1 billion Integrated Tactical Network rollout.[1]Army Public Affairs, “Integrated Tactical Network rolls into fielding,” army.mil Rugged private 5G base stations from Thales and General Dynamics furnish low-latency links for autonomous weapons, while mesh protocols embedded in software-defined radios sustain connectivity when fixed infrastructure collapses. The capability allows dispersed formations to synchronize fires without exposing command nodes, a critical advantage visible during Project Convergence field tests.

Convergence of Electronic Warfare and Cyber Creates a New Battlespace Domain

Programs like the US Air Force Next Generation Jammer pair electromagnetic jamming with embedded malware payloads, enabling simultaneous disruption and exploitation of adversary networks.[2]Valerie Insinna, “Next Generation Jammer combines cyber and EW,” Defense News, defensenews.com Raytheon and L3Harris integrate EW antennas, cyber toolkits, and SIGINT receivers into single air-pod architectures, setting a procurement precedent for multi-mission payloads.

Miniaturized Multi-INT Sensor Payloads Transform Unmanned Operations

General Atomics’ High Roller package fuses SIGINT, SAR, and full-motion video into sub-200-pound pods that fit MALE drones. SWaP breakthroughs from AeroVironment now allow Group 1 systems to deliver ISR once reserved for theater-level platforms, democratizing data collection and enabling platoon-level commanders to access strategic-grade intelligence.

Defense Cloud and Edge AI Enable Real-Time Decision Superiority

Leonardo DRS’s 2025 AI Processor equips combat vehicles with onboard inference engines that classify threats in milliseconds while operating in temperature extremes.[3]Product Release, “Leonardo DRS unveils AI Processor,” leonardodrs.com The US Army’s SandboxAQ battery pilot highlights non-kinetic use-cases, proving that predictive analytics can extend logistic reach and enhance readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps in legacy platforms | -0.4% | Global; NATO interoperability issues | Long term (≥4 years) |

| Export-control and ITAR bottlenecks | -0.6% | US-allied nations | Medium term (2-4 years) |

| Skilled talent shortage in RF and SIGINT analytics | -0.5% | Developed economies | Long term (≥4 years) |

| Cyber-supply-chain vulnerabilities | -0.3% | Global critical infrastructure | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Constrain Coalition Operations

NATO’s Steadfast Dart 2025 exercise highlighted that aircraft and ground stations from different nations could not exchange full-motion video or targeting data in real time because each service used proprietary message formats and frequency plans. The after-action review pointed out that crews resorted to voice relays and thumb-drive transfers, adding minutes to sensor-to-shooter cycles and increasing fratricide risk. Program managers are now mandating zero-trust data fabrics that treat every user and device untrusted until authenticated. Still, these platforms require cryptographic modules that many legacy radios cannot host. Nations have agreed to adopt a common data model for ISR metadata by 2028. Yet, funding shortfalls and export-license hurdles mean older waveforms will stay in service well into the next decade. As a result, coalition commanders expect only incremental gains before 2030, leaving adversaries windows to exploit the remaining seams in allied sensor networks.[4]NATO Exercise Directorate, “Steadfast Dart 2025 after-action report,” nato.int

Export Control Bottlenecks Limit Technology Sharing

AUKUS negotiators still lack blanket ITAR exemptions for nuclear-propulsion control software, forcing Australia and the United Kingdom to run duplicate development lines that add cost and delay milestone tests. US regulations classify many AI inference engines and electronic-warfare algorithms as "defense services," so even allied engineers must obtain technical-assistance agreements before code reviews begin. These rules lengthen prototype cycles by 6–12 months and discourage smaller firms from bidding because legal compliance can exceed their R&D budgets. Parallel supply chains also erode standardization: when partners substitute domestic components to bypass licenses, interoperability certifications must be repeated, stretching schedules further. The bottlenecks undermine collective deterrence's objective by slowing the fielding of common, network-ready systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Assets Drive Next-Generation Capabilities

Space-based assets represent the fastest-growing platform at a 13.02% CAGR, enlarging their contribution to the C5ISR market as commercial LEO constellations mesh with government satellites. The US Space Force’s integration contracts with SpaceX and OneWeb validate the trend, spotlighting resilient beyond-line-of-sight communication during kinetic disruptions. Airborne systems, however, maintain the largest 40.78% slice of the C5ISR market size in 2025 as manned ISR aircraft and HALE drones remain indispensable for high-capacity data collection.

Boosted by AUKUS Virginia-class acquisitions, naval procurement demands submarine-borne mast sensors and secure VLF communications, broadening the maritime revenue pool. Land Systems modernization pushes mobile command posts in GPS-denied theaters, leveraging anti-jam PNT and secondary celestial navigation. Collectively, these dynamics illustrate how the C5ISR market must support seamless cross-domain orchestration under Joint All-Domain Command and Control (JADC2) constructs.

By Component: Software Growth Outpaces Hardware Investments

Software exhibits an 11.74% CAGR, eclipsing hardware growth as AI-enabled decision tools dominate modernization blueprints. OpenAI’s USD 200 million contract to craft war-fighting large-language models exemplifies commercial entrants penetrating defense workflows. Hardware still posting 43.10% of 2025 revenue reflects steady sensor and rugged compute refreshes required to host new code.

Service contracts shift toward outcome-based logistics, with vendors guaranteeing system availability rather than merely supplying parts. Emergent neuromorphic chips from KAIST foreshadow next-stage edge inference that slashes latency and power draw. These developments emphasize how the C5ISR market must marry agile software pipelines with sustainment ecosystems to preserve tactical overmatch.

By Application: Cyber Operations Surge as Domain Boundaries Blur

Cyber exhibits the highest 12.88% CAGR as doctrine embeds offensive cyber within combined-arms maneuver. Simultaneously, C2 retains a 32.10% share of the C5ISR market size due to enduring demand for battle-management systems spanning domains.

ISR fusion platforms now ingest signals, imagery, and human intelligence to generate predictive threat cues. Communications sub-segments concentrate on anti-jam, low-probability-of-intercept radios able to hop across 2–6 GHz in microseconds. EW applications trend toward AI-directed cognitive jammers capable of self-reprogramming in the fight. Saab’s Project Beyond AI agents validated autonomous maneuver for beyond-visual-range engagements, highlighting the convergence between EW, cyber, and kinetic fires.

By End-User: Air Force Modernization Accelerates

Air Force programs lead growth at 12.55% CAGR, fuelled by sixth-generation fighter fleets such as GCAP and NGAD, which mandate onboard sensor fusion and collaborative autonomy. Yet, Army formations hold the deepest 39.20% demand share in 2025, reflecting the sheer volume of land vehicles requiring networking upgrades.

Naval users ride a submarine and an unmanned surface vessel wave, where mast apertures and underwater comms stacks are vital. Joint and Special Operations commandos seek low-signature, multi-band radios and mini-SATCOM terminals for denied-area raids. Homeland Security Agencies widen C5ISR intake for border and critical-infrastructure protection, integrating counter-drone sensors with AI analytics.

Geography Analysis

North America sustained 33.10% of the global C5ISR market share in 2025 on the back of the USD 961.6 billion FY2025 US defense budget. Programs like Project Convergence, JADC2, and the Navy’s Project Overmatch drive procurement of cloud-native C2 and resilient network transport. Canada’s interest in GCAP demonstrates a diversification of the supplier base beyond traditional US prime reliance, whereas Mexico’s border-security partnership sparks demand for integrated sensor towers and aerial ISR. The American technology ecosystem also injects commercial AI prowess; OpenAI’s defense award captures this civilian-military convergence.

Europe registers escalating outlays driven by the Ukraine war. Germany’s 28% budget prioritizes Leopard 3 tanks equipped with open-architecture vetronics and Active Protection System (APS) sensors. The UK’s Strategic Defence Review 2025 champions hybrid carrier air wings blending F-35B and autonomous platforms, requiring unified air-tasking networks. Arrow 3’s USD 3.5 billion sale to Germany frames Israel’s strategic entry into European missile-defense value chains. France’s involvement in SCAF and the UK–Italy–Japan GCAP venture illustrates a continental pivot toward indigenous sixth-generation fighter ecosystems that rely on interoperable, exportable C5ISR middleware.

Asia-Pacific is the fastest limb of the C5ISR market, advancing 13.48% annually through 2031. China’s USD 245 billion budget and nuclear deterrent modernization drive satellite-enabled C4 and strategic early-warning radars. Japan lifted defense allocations by 21%, channeling funds into F-35 expansion, ballistic-missile defense, and space-situational-awareness ground stations. Australia’s AUKUS timeline underscores submarine-specific C5ISR packages, from integrated combat systems to secure VLF comms. South Korea’s Hanwha Ocean yard servicing US Navy vessels amplifies industrial collaboration. India’s Tiger Triumph 2025 joint exercise showcased network-enabled amphibious operations, underscoring sub-continental focus on cross-domain interoperability.

Competitive Landscape

The C5ISR market demonstrates moderate consolidation; the top five vendors commanded a major share of 2024 revenue, yielding a concentration score of 6. BAE Systems' acquisition of Ball Aerospace extends electro-optical payload reach, while Boeing's bid for Spirit AeroSystems insulates aerostructure supply continuity. Lockheed Martin partners with Google to accelerate AI model deployment atop classified clouds, bridging commercial DevSecOps with defense accreditation paths.

Technology differentiation centers on AI/ML autonomy, space-based mesh networking, and cognitive electronic warfare. Leonardo DRS rolled out an AI co-processor hardened for armored-vehicle shock and vibration, and Saab's Project Beyond matured autonomous air-combat agents. White-space abounds in cyber-supply-chain hardening; compliance gaps incentivize start-ups that deliver zero-trust hardware provenance.

New entrants leverage venture capital: CHAOS Industries' USD 275 million Series C signals Silicon Valley's appetite for defense products. SpaceX disrupts protected SATCOM pricing, offering low-latency broadband that traditional GEO satellite integrators struggle to match. Meanwhile, legacy primes double down on sovereign capability assurances to secure exports in politically sensitive deals such as Türkiye's USD 10 billion KAAN jet contract with Indonesia.

C5ISR Industry Leaders

Northrop Grumman Corporation

L3Harris Technologies, Inc.

BAE Systems plc

Thales Group

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The US Army launched its annual Network Modernization Experiment, or NetModX, marking a significant shift toward accelerating advanced technology development to equip soldiers. The service branch announced that the seventh NetModX will transform the Army's C5ISR Center into a dedicated testing environment.

- October 2024: Viasat received an Indefinite Delivery, Indefinite Quantity (IDIQ) contract from the General Services Administration to enhance C5ISR capabilities for US defense forces, worth up to USD 568 million.

- April 2024: Leidos received a follow-on prime contract to provide the US Army with technology services, including hardware sustainment, modernization, refresher training, and logistics support. Under the task order, Leidos specialists in C5ISR will evaluate Army hardware capabilities against performance parameters, develop hardware configurations, and implement upgrades.

- January 2024: HII received a USD 458 million contract through its Mission Technologies division to upgrade communications and information technology (IT) networks for the US government, enhancing battlefield decision-making capabilities.

Global C5ISR Market Report Scope

C5ISR refers to command, control, computers, communications, combat and intelligence, surveillance, and reconnaissance. C5ISR plays a vital role in combat as well as military operations by providing real-time information to the military forces for taking vital battlefield decisions.

Additionally, the report has been segmented by type, application, and by geography. By type, the market has been segmented into land, naval, and airborne. By application, the market has been segmented by electronic warfare, reconnaissance and surveillance, and command and control. The report also covers market sizes and forecasts of different geographical regions. Moreover, the report offers a market forecast and is represented by USD million. Furthermore, the report also includes various key statistics on the market status of leading market players and provides key trends and opportunities in the C5ISR market.

| Land Systems |

| Naval Systems |

| Airborne Systems |

| Space-based Assets |

| Hardware |

| Software |

| Services |

| Electronic Warfare (EW) |

| Intelligence, Reconnaissance, and Surveillance (ISR) |

| Command and Control (C2) |

| Communications |

| Cyber |

| Army |

| Navy |

| Air Force |

| Joint and Special Operations |

| Homeland Security Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Land Systems | ||

| Naval Systems | |||

| Airborne Systems | |||

| Space-based Assets | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Application | Electronic Warfare (EW) | ||

| Intelligence, Reconnaissance, and Surveillance (ISR) | |||

| Command and Control (C2) | |||

| Communications | |||

| Cyber | |||

| By End-User | Army | ||

| Navy | |||

| Air Force | |||

| Joint and Special Operations | |||

| Homeland Security Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the C5ISR market?

The C5ISR market was valued at USD 10.95 billion in 2026 and is forecasted to advance to USD 19.51 billion by 2031, translating to a 12.23% CAGR.

Which platform segment holds the largest share?

Airborne systems lead with 40.78% of 2025 revenue, driven by continued demand for manned and unmanned ISR aircraft.

Why is software growing faster than hardware in C5ISR?

Software growth at 11.74% CAGR reflects investments in AI-enabled decision tools and autonomous capabilities that overlay existing sensor networks.

Which region is the fastest-growing C5ISR market?

Asia-Pacific is expanding at a 13.48% CAGR through 2031 due to elevated tensions and modernization programs in China, Japan, Australia, and India.

How are electronic warfare and cyber operations converging?

Integrated payloads now blend jamming, cyber intrusion, and SIGINT within single systems, allowing forces to dominate the electromagnetic spectrum while penetrating enemy networks.

What are the main restraints facing the C5ISR industry?

Key challenges include export-control bottlenecks, legacy-platform interoperability gaps, skilled-talent shortages, and cyber-supply-chain vulnerabilities that together temper market growth.

Page last updated on: