Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

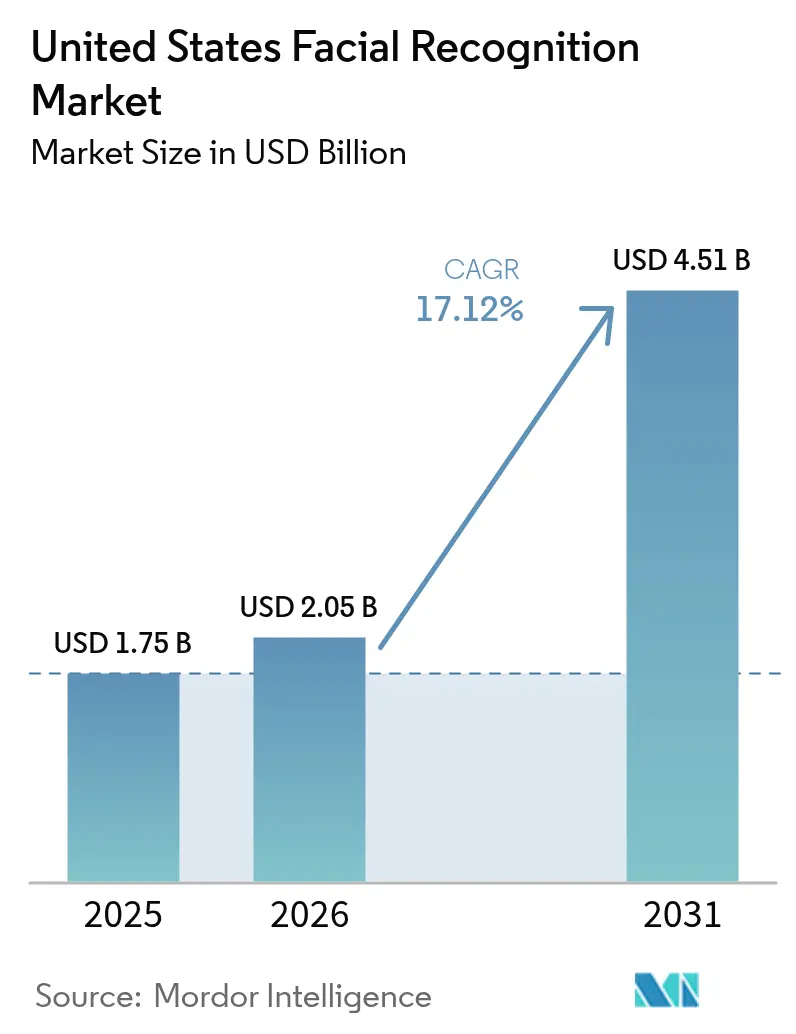

| Base Year Market Size (2025) | USD 1.75 Billion |

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Facial Recognition Market Analysis by Mordor Intelligence

The US facial recognition market size is expected to grow from USD 1.75 billion in 2025 to USD 2.05 billion in 2026 and is forecast to reach USD 4.51 billion by 2031 at 17.12% CAGR over 2026-2031. Rapid roll-outs across border control, retail security, digital identity programs, and healthcare authentication are accelerating adoption. Government modernization funds, airline and port digitization, and e-commerce fraud counter-measures continue to anchor demand, while the 3D technology stack pushes accuracy and spoof-resistance higher. Retailers confronting organized crime, hospitals tackling costly patient misidentification, and financial institutions battling deepfake fraud are deploying solutions at scale. At the same time, a fragmented state privacy regime and component cost inflation raise compliance and margin pressures that favor well-capitalized suppliers able to bundle hardware, software, and managed services.

Key Report Takeaways

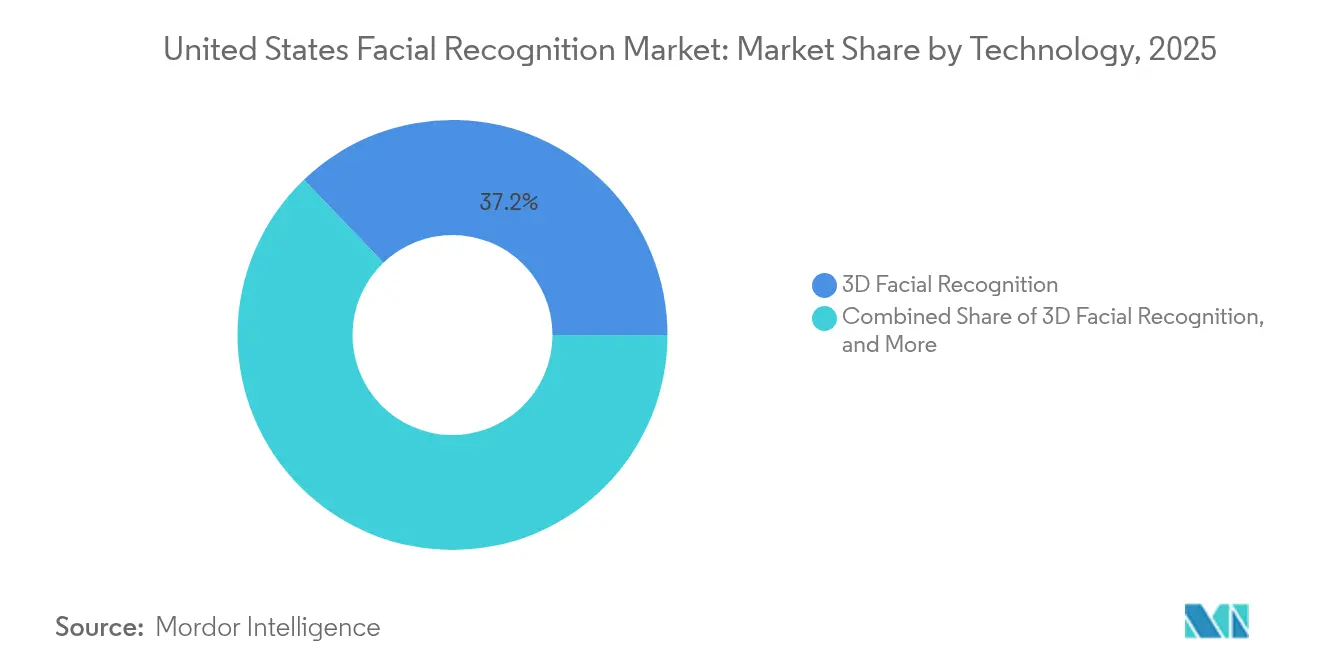

- By technology, 3D facial recognition captured 37.15% of the US facial recognition market share in 2025; facial analytics and emotion detection is forecast to expand at a 19.95% CAGR through 2031.

- By component, hardware held 41.60% of the US facial recognition market size in 2025; the services segment is projected to grow at an 18.15% CAGR between 2026-2031.

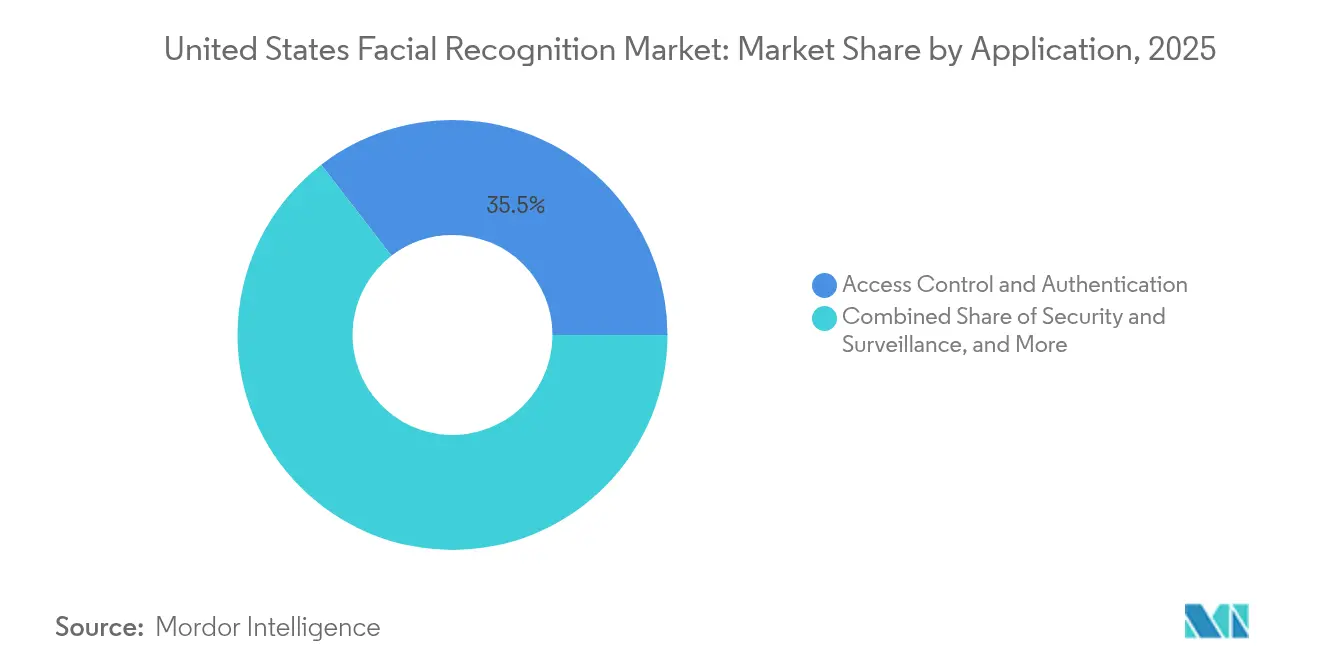

- By application, access control and authentication commanded 35.45% share of the US facial recognition market size in 2025, while security and surveillance is set to advance at a 16.65% CAGR to 2031.

- By end-user industry, government and law enforcement led with 27.90% revenue share in 2025; healthcare and life sciences is positioned to post a 18.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Facial Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Homeland Security modernization funds fueling AI-based border surveillance | +3.2% | National, concentrated at border states and ports | Medium term (2-4 years) |

| REAL-ID deadline driving state DMV facial capture upgrades | +2.5% | National, early adoption in tech-forward states | Short term (≤ 2 years) |

| Retail shrink & organized retail crime pushing loss-prevention deployments | +2.8% | Urban centers with high retail density | Medium term (2-4 years) |

| TSA 2026 road-map for touch-less airport checkpoints | +3.5% | Major transportation hubs | Medium term (2-4 years) |

| FinTech fraud surge & deepfake risk boosting e-KYC face verification | +3.8% | National, financial centers | Short term (≤ 2 years) |

| State-backed digital ID pilots requiring liveness detection | +2.1% | CA, NY, TX | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Homeland Security modernization funds fueling AI-based border surveillance

Fresh federal allocations are expanding autonomous surveillance towers and the Traveler Verification Service, which has already processed more than 300 million travelers and identified 1,800 impostors.[1]U.S. Customs and Border Protection, “FY21 Office of Information and Technology Year In Review,” cbp.govIntegration with airline and cruise line systems is reshaping traveler journeys, creating a contiguous identity layer from curb to boarding gate. Vendors able to deliver cloud-native, high-accuracy platforms are positioned to win long-term service contracts as coverage extends to 79 airports and 12 seaports.

REAL-ID deadline driving state DMV facial capture upgrades

The May 2025 enforcement date is accelerating DMV investments, with only 61-66% of credentials expected to be compliant at the deadline. [2]Federal Register, “Minimum Standards for Driver’s Licenses and Identification Cards Acceptable by Federal Agencies for Official Purposes,” federalregister.gov Mobile driver’s licenses tied to liveness-verified face biometrics, already piloted by 625,000 Californians, indicate a longer-range pivot toward digital wallets. System integrators linking enrollment, credential issuance, and mobile verification stand to capture a multi-year replacement cycle.

Retail shrink & organized retail crime pushing loss-prevention deployments

Shoplifting incidents rose 24% in 2024, with losses projected to surpass USD 150 billion by 2026. Retailers are deploying real-time offender watch-lists such as SAFR Guard, while New York’s security tax credit offsets capital outlays. Cloud analytics that combine face, gait, and behavioral cues are emerging as a competitive differentiator in high-footfall stores, though privacy optics require opt-in loyalty models.

TSA 2026 road-map for touch-less airport checkpoints

USD 9.3 million in CAT-2 funding is scaling facial-matching kiosks, yet current appropriations could push full deployment to 2049 if not accelerated.[3]Transportation Security Administration, “Fiscal Year 2025 President's Budget Request for the Transportation Security Administration,” tsa.gov Suppliers offering modular upgrades and privacy-preserving inference on devices help mitigate the budget bottleneck and align with TSA’s digital ID roadmap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchwork of state biometric privacy laws escalating litigation risk | −2.7% | IL, TX, WA, other strict states | Medium term (2-4 years) |

| Municipal moratoriums on police use reducing public-sector demand | −1.9% | Progressive urban centers | Short term (≤ 2 years) |

| Algorithmic bias scrutiny triggering federal procurement delays | −2.3% | Federal agencies | Medium term (2-4 years) |

| Edge-AI chip cost inflation from US–China trade controls | −1.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FinTech fraud surge & deepfake risk boosting e-KYC face verification

Deepfakes caused USD 158 billion in financial losses in 2023, with 40% of attacks aimed at banks. Liveness-assured facial verification, combined with voice or behavioral biometrics, is fast becoming the default e-KYC standard. Vendors embedding spoof-resistant AI in low-latency APIs are gaining wallet share as traditional video-ID workflows phase out.

State-backed digital ID pilots requiring liveness detection

California, New York, and Texas are piloting digital wallets that mandate liveness-verified facial enrollment. Legislative guidance is now aligning state pilots with federal interoperability, setting the stage for nationwide credential portability and annual refresh revenue for certifying providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 3D precision widens the performance gap

3D recognition accounted for 37.15% of the US facial recognition market share in 2025, underscoring its superiority in accuracy and spoof resistance. The segment’s depth mapping allows consistent matches across lighting variables and partial occlusions, making it the benchmark in border, airport, and high-security enterprise use cases. Texture-rich deep-learning algorithms are further raising accuracy; NIST tracked 1,149 algorithms from 378 developers in its latest evaluation.At the same time, facial analytics and emotion detection are the fastest-growing niche, projected at a 19.95% CAGR, as retailers and clinicians mine sentiment for merchandising and diagnostics. Thermal imaging maintains relevance for low-light installations such as critical infrastructure, while 2D remains in budget-constrained deployments.

Developers are iterating on transformer architectures that process multi-spectral inputs, shortening inference latency at edge nodes. This technical evolution reinforces a tiered pricing model that packages premium 3D or thermal hardware with subscription analytics services. Over the forecast horizon, vendors able to combine on-device privacy with cloud retraining will capture outsized cross-sell in analytics-driven verticals of the US facial recognition market.

By Component: hardware dominance meets service-centric growth

Hardware secured 41.60% of the US facial recognition market size in 2025, driven by camera modules and edge AI chipsets. Yet services, covering integration, cloud APIs, and managed monitoring, are advancing at an 18.15% CAGR as buyers shift to operating-expense models. US-China trade controls are inflating chip prices and prompting buyers to evaluate domestic silicon, creating openings for fabless startups specializing in low-power vision neural processors.

Service providers are differentiating through rapid deployment toolkits, zero-trust data governance, and outcome-based service-level guarantees. Their recurring revenue stabilizes margins, offsetting hardware cyclicality. This blended delivery strategy underscores a broader movement toward end-to-end stacks that lock in lifetime value across the US facial recognition market.

By Application: authentication scale leads, surveillance momentum builds

Access control and authentication represented 35.45% of the US facial recognition market size in 2025, reflecting embedded sensors in mobile devices and corporate entry systems. Security and surveillance is primed for the quickest advance at 16.65% CAGR, propelled by organized retail crime counter-measures and smart-city programs. Compliance mandates in finance and healthcare push e-KYC and patient ID workflows into mainstream adoption, with liveness detection now table stakes.

Vendors integrating multimodal biometrics and contextual analytics drive higher conversion in unattended scenarios. Emotion recognition pilots in telehealth and customer experience illustrate the breadth of emerging use cases. Together, these vectors reinforce the widening footprint of facial recognition across enterprise applications in the US facial recognition market.

By End-user Industry: public sector scale, healthcare breakout

Government and law enforcement commanded 27.90% of 2025 revenue, anchored by border, aviation, and DMV deployments. Healthcare is forecast as the fastest-rising customer group, expanding at a 18.95% CAGR as hospitals combat the 24% patient misidentification rate. Retail chains, airports, and financial institutions round out demand, each seeking frictionless yet auditable identity frameworks.

Hospital systems integrating facial biometrics with electronic health records report lower duplicate charts and streamlined patient check-in, driving strong return on investment. Meanwhile, transportation hubs endorse touchless passenger flows as competitive differentiators. Such sector-specific imperatives sustain broad-based momentum throughout the US facial recognition market.

Geography Analysis

California, New York, and Texas form the core triad of high-adoption states, each blending tech ecosystems with large consumer bases. California’s mobile driver’s license pilot, executed through Apple Wallet, signals institutional readiness for biometric wallets at scale and sets a regulatory benchmark other states are likely to follow. The Northeast corridor adds a potent mix of federal procurement and Wall Street e-KYC demand, although algorithmic bias reviews are lengthening agency procurement cycles.

Southern border states are intensifying deployments in land ports and airports, urged by Customs and Border Protection’s expansion of Simplified Arrival facial matching. Retail corridors in Florida and Texas equally invest in loss-prevention analytics, even as state privacy statutes introduce nuanced compliance clauses. The Midwest lags on account of more conservative privacy sentiment but shows upside as digital ID pilots mature.

Across all regions, municipal moratoriums introduce a checkerboard of permissible uses, compelling vendors to design geo-fenced feature toggles. Such configurability is fast becoming a pre-requisite for scalable roll-outs, reinforcing the premium on vendors with agile compliance engineering inside the US facial recognition market.

Competitive Landscape

The supplier field spans major cloud platforms, dedicated biometric specialists, and niche AI hardware startups. Consolidation accelerated when BigBear.ai acquired Pangiam, adding advanced vision analytics to a defense-focused portfolio. Amadeus’s purchase of Vision-Box and Entrust’s acquisition of Onfido further illustrate the trend toward integrated identity stacks that cover enrollment through real-time verification.

Product differentiation now revolves around liveness accuracy, privacy-preserving architectures, and modular deployment models that lower integration friction. Clear Secure operates at 58 airports and logged 235 million platform uses by December 2024, validating subscription throughput economics. In parallel, chip suppliers compete on TOPS-per-watt metrics that reduce edge-node thermal envelopes. Startups with diverse training datasets and transparent model cards target enterprise buyers wary of algorithmic bias litigation.

United States Facial Recognition Industry Leaders

Amazon Web Services (Rekognition)

Microsoft Corp. (Azure Face)

NEC Corporation

Thales Group (Idemia)

Clearview AI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SAFR launched SAFR Guard, providing real-time alerts against known retail offenders

- May 2025: The US-UAE agreement cleared exports of 500,000 advanced AI chips annually, easing component supply for facial recognition systems

- April 2025: Clearview AI settled biometric privacy litigation for USD 51.75 million, highlighting spiraling compliance costs

- March 2025: Lawmakers introduced the MATCH IT Act to cut healthcare misidentification through biometrics

United States Facial Recognition Market Report Scope

Facial recognition is the process of verifying the identity of an individual using feature recognition. It captures the features, analyzes them, and compares patterns based on the person's facial details. The report provides a detailed analysis of technologies such as 3D Facial Recognition, 2D Facial Recognition , and Facial Analytics in various end-user industries.

By Technology

| 2D Facial Recognition |

| 3D Facial Recognition |

| Thermal/Infra-red Facial Recognition |

| Facial Analytics and Emotion Detection |

By Component

| Hardware (Cameras, Edge AI Chipsets) |

| Software/Algorithms |

| Services (Integration, Managed, Cloud API) |

By Application

| Access Control and Authentication |

| Security and Surveillance |

| Identity Verification / e-KYC |

| Attendance and Workforce Management |

| Emotion Recognition and Customer Insights |

By End-user Industry

| Government and Law Enforcement |

| Transportation (Airports, Ports, Public Transit) |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Travel and Hospitality |

| Automotive and Smart Mobility |

| Education |

| Energy and Utilities |

| By Technology | 2D Facial Recognition |

| 3D Facial Recognition | |

| Thermal/Infra-red Facial Recognition | |

| Facial Analytics and Emotion Detection | |

| By Component | Hardware (Cameras, Edge AI Chipsets) |

| Software/Algorithms | |

| Services (Integration, Managed, Cloud API) | |

| By Application | Access Control and Authentication |

| Security and Surveillance | |

| Identity Verification / e-KYC | |

| Attendance and Workforce Management | |

| Emotion Recognition and Customer Insights | |

| By End-user Industry | Government and Law Enforcement |

| Transportation (Airports, Ports, Public Transit) | |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-commerce | |

| Travel and Hospitality | |

| Automotive and Smart Mobility | |

| Education | |

| Energy and Utilities |

Key Questions Answered in the Report

What is the projected growth of the US facial recognition market through 2031?

The US facial recognition market is forecast to grow from USD 2.05 billion in 2026 to USD 4.51 billion by 2031 at a 17.12% CAGR.

Which technology segment currently holds the largest share?

3D facial recognition leads with 37.15% of market share on account of its superior accuracy and anti-spoofing performance.

Why is healthcare the fastest-growing end-user industry?

Hospitals are adopting biometric patient ID systems to curb misidentification, driving a 18.95% CAGR for healthcare deployments.

How do state privacy laws affect vendors?

Strict statutes such as Illinois’s BIPA increase litigation exposure, trimming the market CAGR by an estimated 2.7 percentage points.

What is driving demand in security and surveillance applications?

Rising organized retail crime and airport modernization plans are propelling surveillance deployments at a 16.65% CAGR.

How will chip export policy shifts influence component costs?

Easing export restrictions like the US–UAE chip deal improves supply, while ongoing US–China trade controls may keep edge-AI chip prices elevated.

Page last updated on: