Vital Signs Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

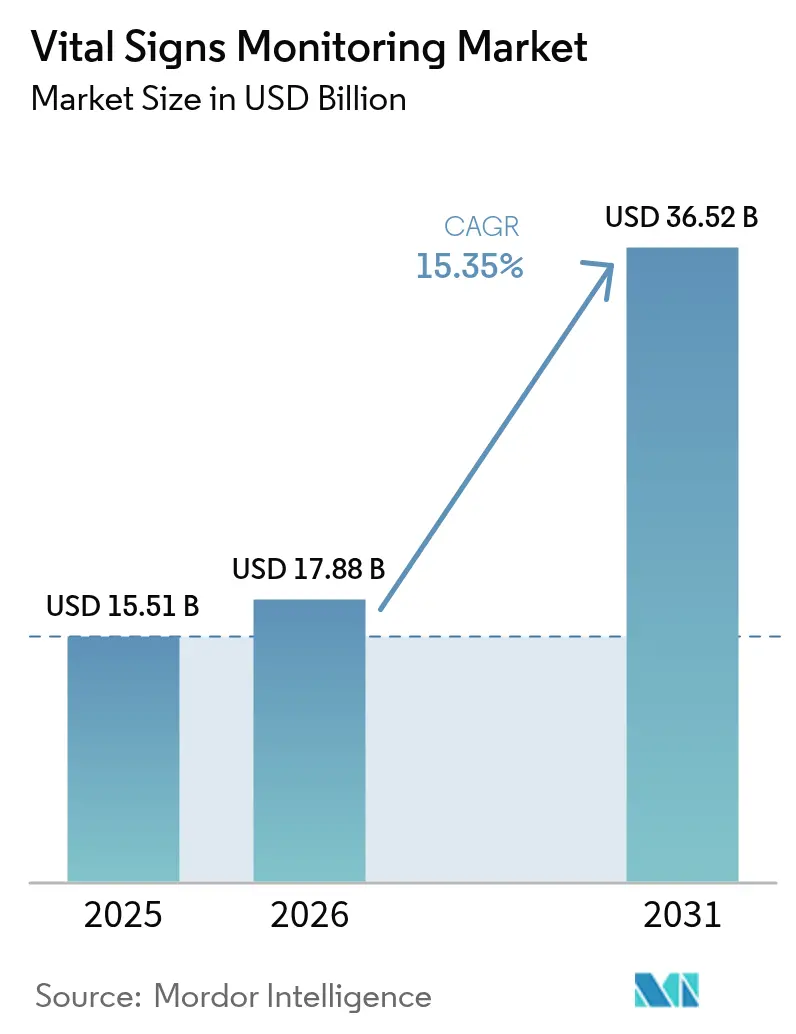

| Market Size (2026) | USD 17.88 Billion |

| Market Size (2031) | USD 36.52 Billion |

| Growth Rate (2026 - 2031) | 15.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vital Signs Monitoring Market Analysis by Mordor Intelligence

The Vital Signs Monitoring Market size is projected to expand from USD 15.51 billion in 2025 and USD 17.88 billion in 2026 to USD 36.52 billion by 2031, registering a CAGR of 15.35% between 2026 to 2031.

Steady reimbursement for remote patient monitoring, the rapid scaling of Hospital-at-Home programs, and AI-enabled early-warning scores are shifting purchasing decisions toward connected, multi-parameter devices. Hospitals are reallocating capital budgets from stand-alone bedside units to enterprise software bundles that feed directly into electronic health records, while employers and payers are accelerating direct-to-consumer supply chains to curb chronic-care expenses. Technology roadmaps now prioritize Bluetooth Low Energy 5.4 compatibility and multi-wavelength LED arrays that address pigmentation-related accuracy gaps. Competition is intensifying as consumer electronics brands parade FDA-cleared features once restricted to critical-care hardware, compelling legacy device makers to pivot toward subscription analytics and cybersecurity-hardened firmware.

Key Report Takeaways

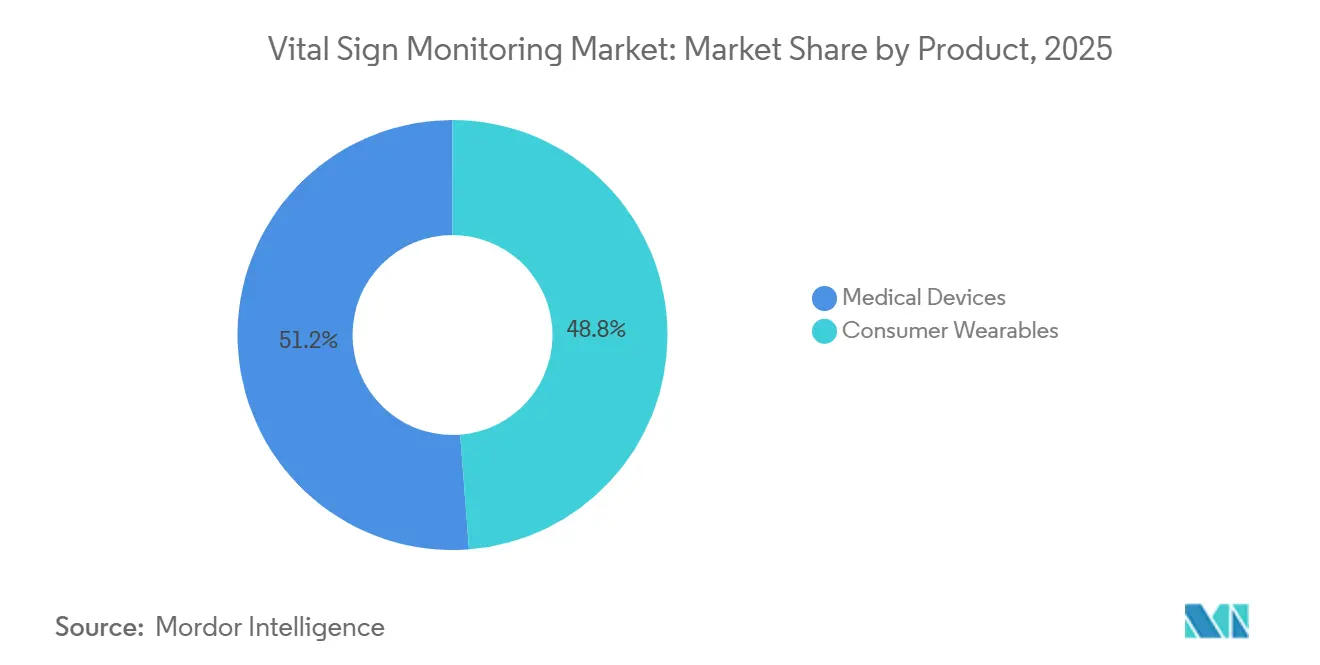

- By product category, medical devices commanded 51.23% of the vital signs monitoring market share in 2025; consumer wearables are forecast to advance at a 16.78% CAGR through 2031.

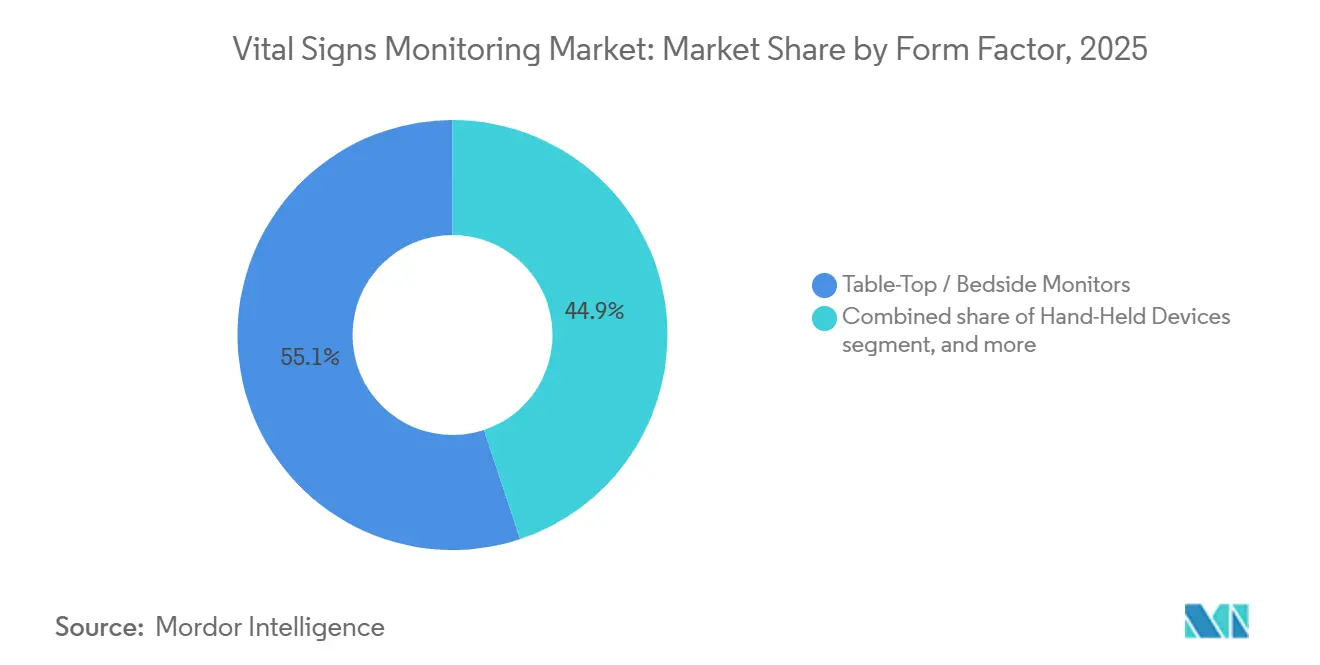

- By form factor, table-top and bedside monitors retained 55.1% share of the vital signs monitoring market size in 2025, while wearable devices are projected to expand at 17.56% CAGR to 2031.

- By end-user, hospitals and clinics held 61.89% revenue share in 2025, yet home-care settings are set to grow at an 18.54% CAGR over 2026-2031.

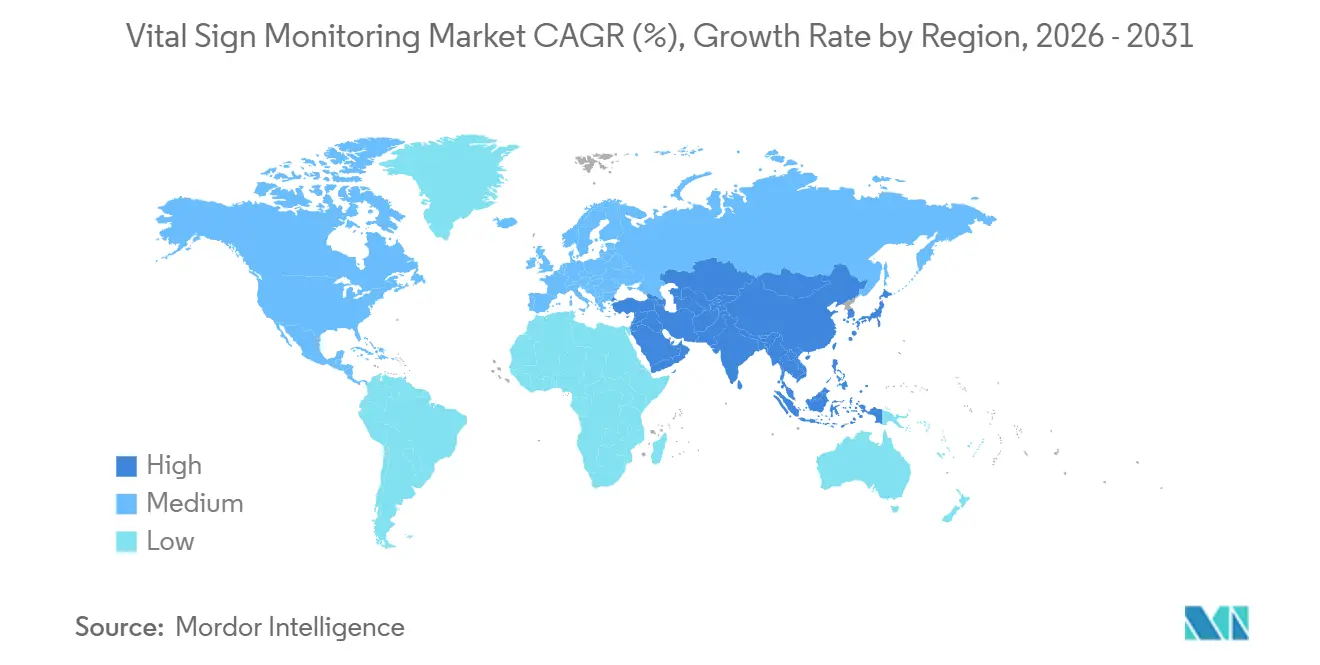

- By geography, North America led with 45.3% revenue share in 2025; Asia-Pacific is positioned to grow at 18.11% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vital Signs Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in chronic cardio-metabolic disorders | +3.2% | Global, with an acute burden in North America and Europe | Long term (≥ 4 years) |

| Expanding adoption of tele-health & RPM reimbursement | +4.1% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Continuous sensor & wireless technology advances | +2.8% | Global, led by Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Rising preference for home-based care & self-management | +3.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Hospital-at-Home programs creating ICU-grade domiciliary demand | +2.9% | United States, United Kingdom, Canada | Short term (≤ 2 years) |

| AI-driven early-deterioration algorithms bundled with devices | +2.6% | North America, Western Europe, select APAC metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Lifestyle Diseases

Cardiovascular mortality climbed 18.6% globally between 2020 and 2024, prompting health systems to shift resources to continuous cardiac surveillance tools. As 48% of U.S. adults now live with some form of heart disease, ambulatory monitoring solutions that capture arrhythmia and nocturnal hypertension are gaining priority funding. Diabetes prevalence reached 537 million adults in 2024, reinforcing demand for multi-parameter monitors that track glucose alongside blood pressure and heart rate. Payers face a USD 4.1 trillion annual chronic-disease burden and are rewarding remote monitoring platforms that demonstrate outcome improvements, accelerating procurement of integrated vital-sign solutions. Collectively, these epidemiologic forces underpin the long-run expansion of the vital signs monitoring market [1]World Health Organization, “Cardiovascular Diseases,” who.int.

Expanding Adoption of Tele-Health & RPM Reimbursement

CMS preserved core Remote Patient Monitoring (RPM) codes while private insurers mirrored coverage, guaranteeing a predictable fee schedule for data-driven care pathways. Although CPT 99457 faces a modest payment cut, large provider groups are offsetting the hit by scaling virtual nursing centers that can supervise hundreds of at-home patients simultaneously. In parallel, UnitedHealthcare and Anthem expanded RPM eligibility to nearly 20 million commercial members, stipulating ISO-validated accuracy for connected blood-pressure devices. Internationally, the United Kingdom’s NHS Digital earmarked GBP 450 million to supply 2.5 million citizens with connected monitors, cementing Europe’s reimbursement momentum. Sustained funding de-risks capital allocation for manufacturers, anchoring the volume growth that underpins the vital signs monitoring market.

Continuous Sensor & Wireless Technology Advances

The Bluetooth 5.4 specification slashes connection latency and device power draw, allowing patch-based sensors to operate for almost two weeks on coin-cell batteries. Improved motion-artifact compensation algorithms now deliver ±1.5% SpO₂ accuracy during patient ambulation, meeting the FDA’s stricter pigmentation benchmarks. Masimo’s W1 smartwatch highlights these improvements, doubling battery life relative to its predecessor while streaming three physiologic channels. R&D budgets are therefore skewing toward low-power silicon, advanced photonics, and edge-AI firmware, accelerating the technical refresh cycle across the vital signs monitoring market.

Hospital-at-Home Programs Creating ICU-Grade Domiciliary Demand

Hospital systems continue to shift acute-care episodes into domiciliary environments under CMS’s Acute Hospital Care at Home waiver. Deployed solutions must match ICU-accuracy in uncontrolled settings, prompting vendors to pair ruggedized sensors with cloud dashboards that triage alerts to remote nurses. Economic analyses show 30-day episode costs fall by nearly 40%, incentivizing wider rollout. Device makers that secure enterprise cybersecurity certifications and HL7-FHIR interoperability are winning long-term supply contracts, reinforcing corporate share in the vital signs monitoring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy / cyber-security compliance burden | -2.4% | Global, acute in North America and EU | Medium term (2-4 years) |

| High cap-ex & pricing pressure in commoditised SKUs | -1.8% | Global, most severe in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Accuracy bias on dark-skin tones & motion artefacts | -1.3% | Global, regulatory focus in North America | Medium term (2-4 years) |

| Battery-life limits for multi-parameter, always-on wearables | -0.9% | Global, R&D concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy / Cyber-Security Compliance Burden

An upsurge in ransomware attacks has pushed regulators to tighten cybersecurity requirements. The FDA now demands a software bill-of-materials, proof of secure coding, and evergreen patching processes as part of every 510(k) submission. European MDR frameworks impose parallel obligations that include annual penetration testing and incident reporting within 72 hours. Compliance can lift pre-market development costs by up to USD 1.8 million for a single device family, diluting the margins of smaller entrants. Larger incumbents are scaling dedicated security teams and spreading overhead across wider portfolios, but startups face delayed launches or strategic exits, mildly dampening the overall CAGR of the vital signs monitoring market [2]U.S. Department of Health and Human Services, “HIPAA Breach Notification Rule,” hhs.gov.

High Cap-Ex & Pricing Pressure in Commoditized SKUs

Group Purchasing Organizations are leveraging aggregated buying power to negotiate 18-25% price concessions on bedside monitors. At the same time, Asian manufacturers with 20-30% cost advantages are undercutting incumbent list prices, especially in emerging markets. Gross-margin compression forces Western OEMs to bundle analytics subscriptions or pivot toward high-acuity, multi-parameter devices where differentiation is harder to commoditize. Capital constraints in public health systems, particularly across India and Brazil, further limit uptake of premium AI-enabled hardware. These dynamics restrain near-term revenue growth but also accelerate portfolio transitions toward cloud-connected platforms within the vital signs monitoring market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumer Wearables Outpace Medical Devices

Medical devices captured a dominant 51.23% share of the vital signs monitoring market and consumer wearables are projected to rise at a 16.78% CAGR, eroding the long-held dominance of regulated medical devices. Apple Watch Series 10 introduced FDA-cleared sleep-apnea screening at a mass-market price point, proving that consumer brands can meet clinical thresholds without hospital distribution. Smartwatches captured a notable share of 2025 consumer revenue, while patch-based monitors are scaling in post-surgical pathways where their adhesive form eliminates patient setup steps. Within regulated medical devices, pulse oximeters still held significant share of 2025 receipts, but mandatory pigmentation-stratified validation is adding six to nine months to approval queues, tilting R&D dollars toward multi-parameter platforms. Together, these shifts broaden addressable users and underpin sustained expansion of the vital signs monitoring market.

Hardware makers are also converging glucose, ECG, and blood-pressure sensors into unified kits. This consolidation simplifies app ecosystems and multiplies reimbursable billing codes, shortening return-on-investment cycles for providers. The vital signs monitoring market size linked to consumer wearables, therefore, stands to leapfrog that of single-parameter medical devices well before 2031.

By End-User: Home-Care Settings Surge

Home-care environments are on course to record an 18.54% CAGR, the fastest across all user categories. Medicare’s RPM codes fueled USD 2.8 billion in 2025 claims, validating the economic case for continuous at-home surveillance over sporadic clinic visits. Device requirements include intuitive onboarding, voice prompts for older adults, and automatic data uplinks via cellular gateways to avoid Wi-Fi dependencies. Hospitals still accounted for 61.89% of 2025 spend, but their procurement teams increasingly buy enterprise cloud licenses rather than incremental bedside monitors, reshaping revenue composition inside the vital signs monitoring market.

Ambulatory care centers and employer clinics, are rapidly adopting wrist-based blood-pressure devices to manage hypertension between doctor visits. Their uptake illustrates how reimbursement certainty and user-friendly hardware funnel growth from acute facilities into lower-acuity settings, thereby expanding the overall vital signs monitoring market size.

By Form Factor: Wearables Displace Bedside Monitors

Wearable devices are projected to grow at 17.56% CAGR, outstripping bedside systems that are tethered to fixed locations. Wrist-worn platforms like Apple and Samsung smartwatches provide photoplethysmography and single-lead ECG in packages acceptable to mainstream consumers. Patches and rings fill clinical niches such as post-surgical ambulation and nocturnal arrhythmia tracking. The vital signs monitoring market share for wearables, therefore, widens annually, eating into the legacy 55.1% stake of table-top monitors.

Power-management breakthroughs, spearheaded by Bluetooth 5.4, add seven or more battery days to multi-parameter streams, eliminating the last practical barrier to round-the-clock tracking. As firmware updates extend over-the-air, hospital IT teams accept wearables into electronic record systems, thereby reinforcing institutional demand and fortifying revenue diversity across the vital signs monitoring market.

Geography Analysis

North America kept its 45.3% lead in 2025, benefiting from clear CPT codes, large employer wellness budgets, and 124 health systems that run Hospital-at-Home wards. Provincial efforts in Canada and emerging pilots in Mexico further lift regional unit volumes. Asia-Pacific is set for the fastest proportional climb, at 18.11% CAGR, powered by China’s RMB 1.2 trillion digital-health investment and India’s unified health-record rollout. Reimbursement expansions in Japan and South Korea support incremental device densification in super-aging societies, while Australia targets rural connectivity gaps with federal grants.

Europe represents a significant share of 2025 revenue and is unified by national frameworks that reimburse connected devices for chronic heart failure, COPD, and diabetes. Germany’s Digital Healthcare Act saw EUR 380 million in 2025 claims, validating statutory insurance appetite. France’s centralized remote-monitoring platform pulls data from 18 device brands, proving interoperability at scale. South America and the Middle East & Africa collectively registered notable share, but strategic tender awards in Brazil and the Gulf states demonstrate the future upside for vendors that localize language support and battery-safety certifications. These regional nuances collectively orchestrate multi-speed expansion of the vital signs monitoring market.

Competitive Landscape

The vital signs monitoring market remains moderately fragmented. Medtronic and Philips held significant share primarily through entrenched hospital estates and integrated software dashboards. Each is migrating toward recurring SaaS revenue to soften hardware margin erosion. Apple, Samsung, and Garmin weaponize consumer brand power, chipping away at low-acuity segments and forcing legacy OEMs into patent disputes, as seen in Masimo’s Section 337 campaign that temporarily blocked certain Apple imports.

Start-ups such as BioBeat and VivaLNK focus on patch-based devices that deliver 24/7 ambulatory accuracy without cuffs, carving premium sub-niches. M&A continues; Baxter’s earlier absorption of Hill-Rom fused infusion pumps with Welch Allyn monitors, indicating sustained appetite for vertically integrated portfolios. Asian entrants Mindray and Contec leverage double-digit cost advantages to win public-hospital tenders in South America and Africa, although FDA and CE hurdles still gate North American and EU penetration. Competitive dynamics therefore hinge on cybersecurity credentials, AI-enhanced analytics, and the agility to certify multi-parameter wearables under evolving home-use guidance, factors that collectively mold strategic posturing across the vital signs monitoring market

Vital Signs Monitoring Industry Leaders

Nihon Kohden Corporation

Koninklijke Philips N.V.

Apple Inc.

A&D Company

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cardinal Health launched Kendall DL Multi, a single-patient cable set that tracks cardiac activity, SpO₂, and temperature through one port, easing nurse workflows

- May 2025: Zynex filed a 510(k) for NiCO, a non-invasive CO-oximeter aimed at continuous monitoring.

- February 2025: BioIntelliSense partnered with Hicuity Health to blend continuous monitoring with 24/7 virtual nursing oversight

Global Vital Signs Monitoring Market Report Scope

The vital sign monitoring market comprises all devices and monitoring services used in hospitals, clinics, ambulatory surgical centers, and home care settings for measuring the vital signs of the human body, such as body temperature, heart rate or pulse rate, respiratory rate, and blood pressure.

The vital sign monitoring market is segmented by product and end user. By product, the market is segmented into consumer wearables (smartwatches, fitness & activity trackers, smart patches, and other wearables) and medical devices (blood pressure monitors, pulse oximeters, temperature monitoring devices, and respiratory-rate monitors). By end-user, the market is segmented into hospitals and clinics, ambulatory and health centers, homecare. By form factor, the market is segmented into hand-held devices, table-top, and wearables. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Consumer Wearables | Smartwatches |

| Fitness & Activity Trackers | |

| Smart Patches | |

| Other Wearables | |

| Medical Devices | Blood Pressure Monitors |

| Pulse Oximeters | |

| Temperature Monitoring Devices | |

| Respiratory-Rate Monitors |

| Hospitals & Clinics |

| Ambulatory & Health Centres |

| Home-Care Settings |

| Hand-Held Devices |

| Table-Top / Bedside Monitors |

| Wearables |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Consumer Wearables | Smartwatches |

| Fitness & Activity Trackers | ||

| Smart Patches | ||

| Other Wearables | ||

| Medical Devices | Blood Pressure Monitors | |

| Pulse Oximeters | ||

| Temperature Monitoring Devices | ||

| Respiratory-Rate Monitors | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory & Health Centres | ||

| Home-Care Settings | ||

| By Form Factor | Hand-Held Devices | |

| Table-Top / Bedside Monitors | ||

| Wearables | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How quickly are Hospital-at-Home programs adopting connected monitors?

By late 2025, 124 U.S. health systems had enrolled, treating 38,000 patients with ICU-grade wearables and driving fresh device orders.

Which product category is growing fastest?

Consumer wearables are projected to expand at a 16.78% CAGR, outpacing regulated medical devices through 2031.

What are the main cybersecurity requirements for new monitors?

The FDA now mandates a software bill-of-materials, vulnerability disclosure policies, and documented secure coding for all 510(k) filings.

Why is pigmentation bias a regulatory focus?

Pulse-oximeter accuracy can degrade by up to 5 percentage points on darker skin, prompting the FDA to require skin-type-stratified validation.

Which geography offers the highest incremental growth?

Asia-Pacific leads with an 18.11% CAGR, anchored by China’s RMB 1.2 trillion digital-health investment and India’s unified health-record rollout.

Page last updated on: