Pulmonary Arterial Hypertension Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

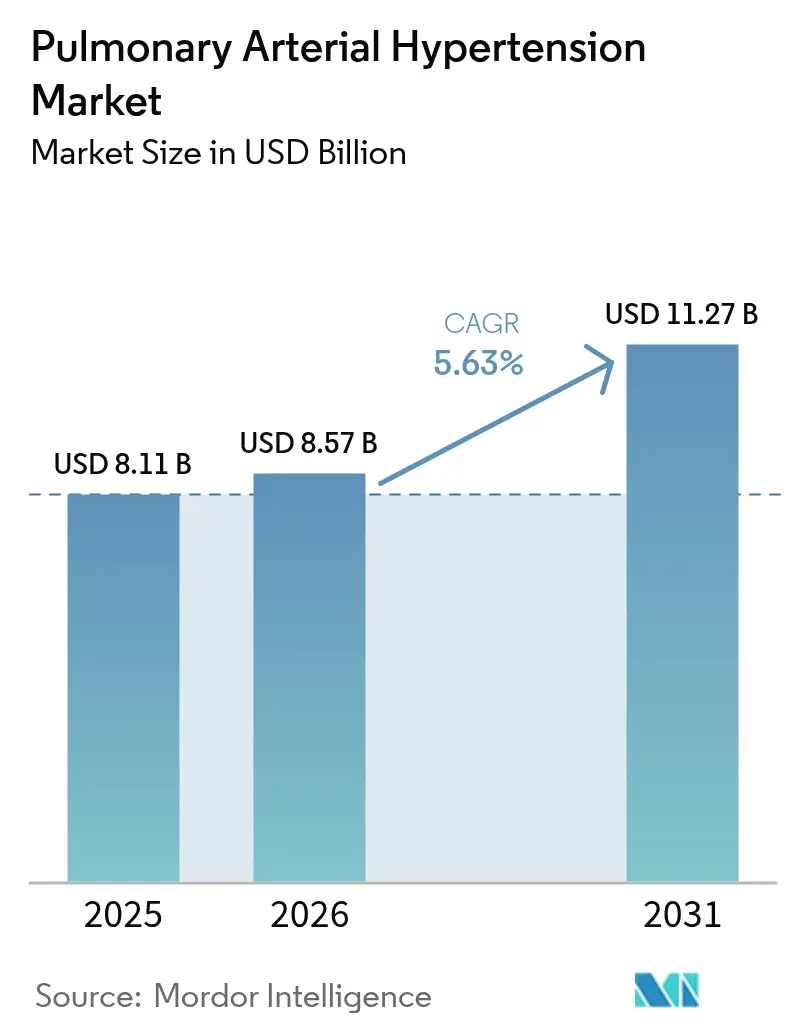

| Market Size (2026) | USD 8.57 Billion |

| Market Size (2031) | USD 11.27 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulmonary Arterial Hypertension Market Analysis by Mordor Intelligence

The pulmonary arterial hypertension market size was valued at USD 8.11 billion in 2025 and estimated to grow from USD 8.57 billion in 2026 to reach USD 11.27 billion by 2031, at a CAGR of 5.63% during the forecast period (2026-2031). Accelerated uptake of disease-modifying agents, notably activin-signaling inhibitors such as sotatercept, is widening treatment choices and tempering pricing pressure. North America leads demand on the back of generous reimbursement and early adoption of dual and triple oral regimens, while Asia Pacific is poised for rapid growth thanks to AI-enabled echocardiography that shortens time to diagnosis. Endothelin receptor antagonists (ERAs) still anchor most first-line prescriptions, but novel Smad-signaling modulators are beginning to reshape late-stage pipelines. Oral formulations dominate because convenience drives adherence, yet inhaled dry-powder prostacyclin products are gaining share as they combine targeted delivery with simplified dosing. Competitive intensity is rising as large pharmas secure pipeline assets through acquisitions and alliances to defend their positions in the pulmonary arterial hypertension market.

Key Report Takeaways

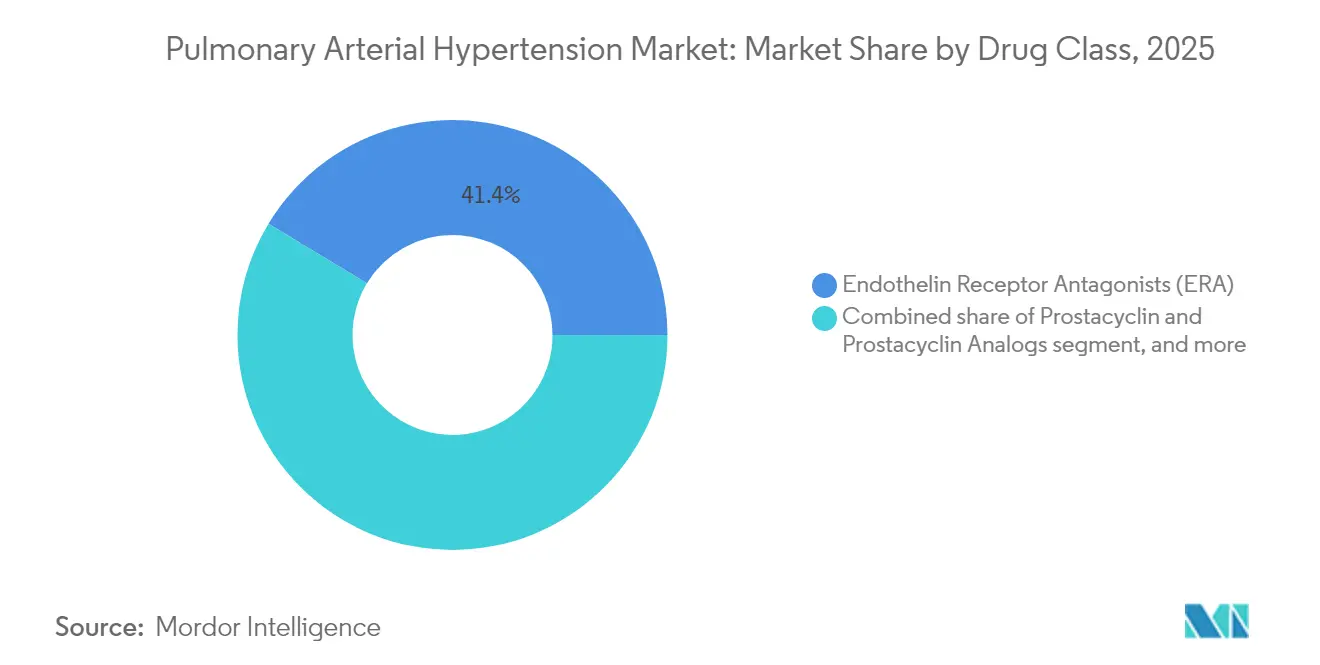

- By drug class, endothelin receptor antagonists held 41.35% of pulmonary arterial hypertension market share in 2025; Smad-signaling modulators headline the fastest growth at a 9.02% CAGR to 2031.

- By route of administration, oral therapies commanded 65.40% of the pulmonary arterial hypertension market size in 2025, while inhaled products are projected to expand at an 8.22% CAGR through 2031.

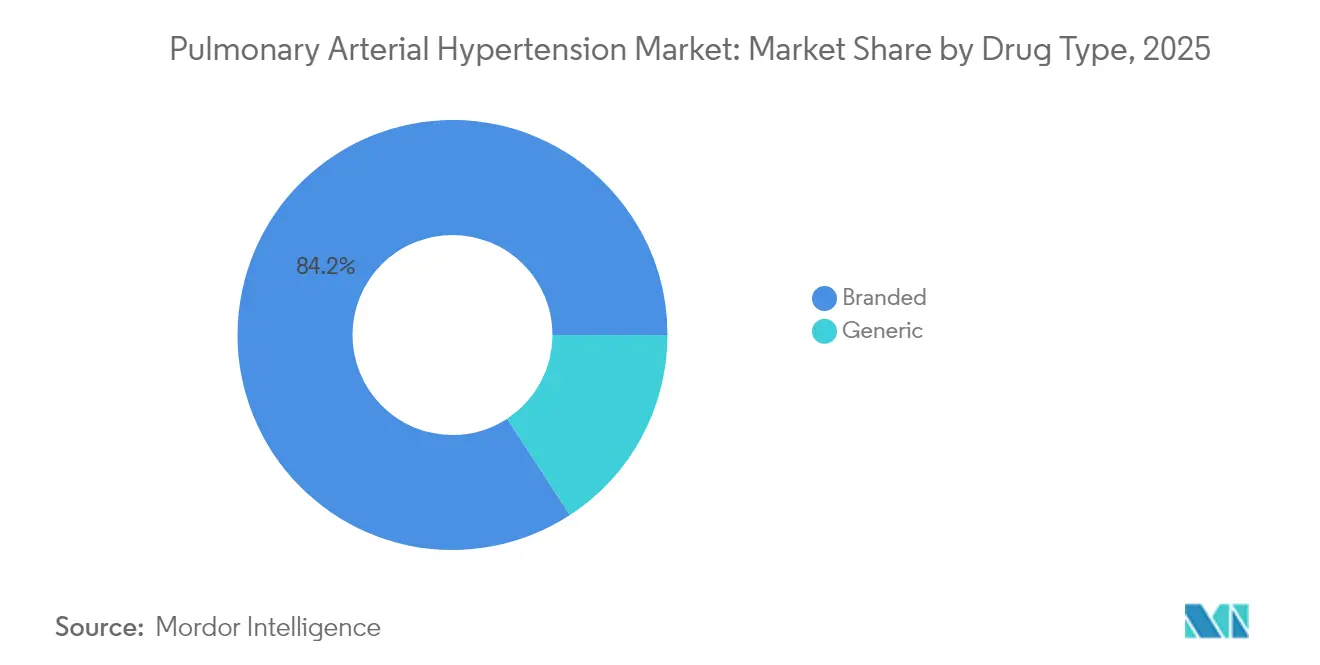

- By drug type, branded products controlled 84.20% share of the pulmonary arterial hypertension market size in 2025; generics are forecast to grow at a 11.28% CAGR between 2026 and 2031.

- By distribution channel, hospital pharmacies accounted for 57.20% revenue share in 2025, whereas online pharmacies are set to record an 10.37% CAGR to 2031.

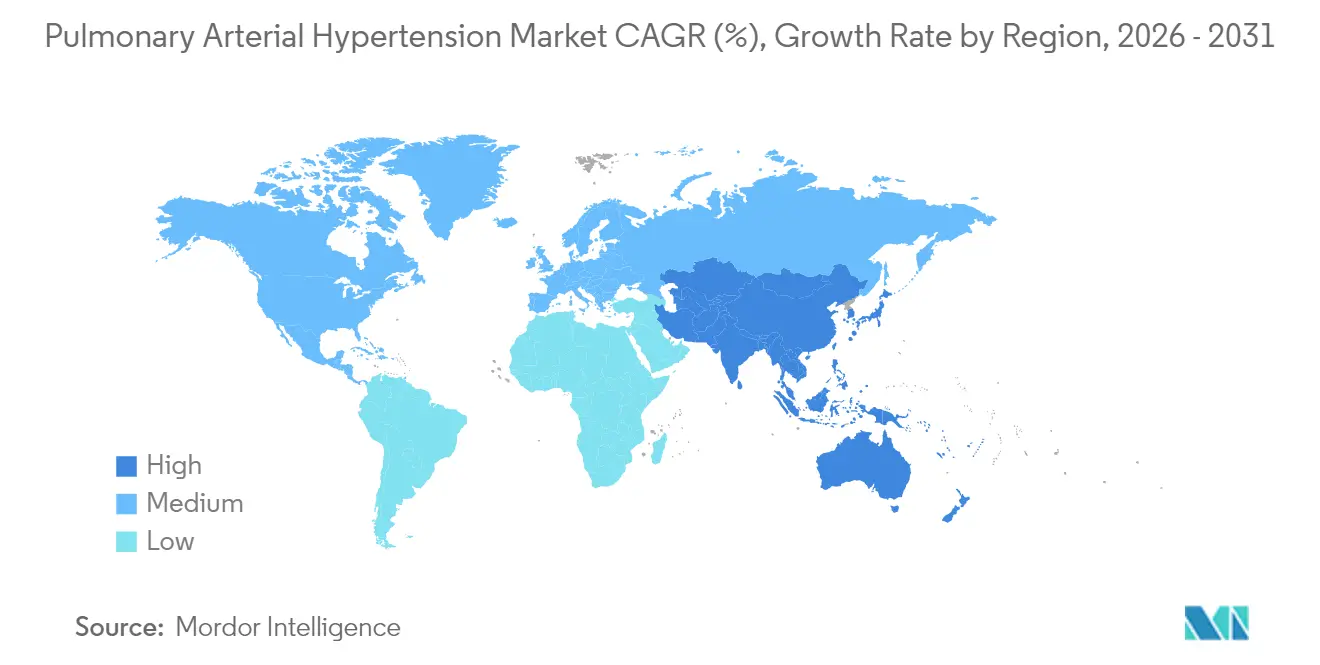

- By geography, North America held 44.30% of the pulmonary arterial hypertension market in 2025; Asia Pacific is advancing at a 6.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pulmonary Arterial Hypertension Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CHD-survivor cohort expansion | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Earlier-line combination therapy adoption | +1.5% | US, EU-5 | Medium term (2-4 years) |

| Commercialization of oral prostacyclin agents | +1.0% | Global | Medium term (2-4 years) |

| Breakthrough Smad-signaling modulators | +1.8% | Global | Long term (≥ 4 years) |

| Orphan-drug incentives & premium pricing sustain high revenue per patient in developed markets | +0.9% | US, Western Europe, Japan | Short term (≤ 2 years) |

| AI-enabled echocardiography screening programs boost early diagnosis in high-burden Asian countries | +1.3% | China, India, South-East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of PAH Linked to CHD-Survivor Cohort Expansion

Clinical advances in congenital heart disease (CHD) surgery and care have extended survival, creating a larger reservoir of patients who later develop PAH. Prevalence reaches 25.0% in children with trisomy 21 and rises to 45.0% when CHD co-exists, reshaping the patient pool and driving demand for tailored therapies[1]Jennifer K. Peterson et al., “Trisomy 21 and Congenital Heart Disease,” Journal of the American Heart Association, ahajournals.org. Eisenmenger syndrome patients in the REHAP registry show poorer outcomes, underscoring the need for specialized drug regimens that control vascular remodeling and manage high pulmonary resistance. As clinicians emphasize early hemodynamic assessment before corrective procedures, the pulmonary arterial hypertension market sees sustained growth from this evolving demographic. Long-term monitoring needs are also expanding ancillary service opportunities such as remote hemodynamic surveillance.

Rapid Label Expansions & Earlier-Line Combination Therapy Adoption in US & EU5

Guidelines from the 7th World Symposium recommend dual or triple oral therapy upfront for non-high-risk patients, accelerating demand for fixed-dose combinations. Johnson & Johnson’s single-tablet Opsynvi improved pulmonary vascular resistance versus monotherapies in the A DUE study, giving prescribers an easy path to initiate combination treatment. Early addition of selexipag cut disease-progression risk by 52.0% when layered onto ERA + PDE-5i backbones[2]Wei Huang et al., “Early Addition of Selexipag to Double Therapy,” JAMA Network Open, jamanetwork.com. These data validate multi-pathway suppression and stimulate payers to expand coverage, which amplifies volume-driven growth in the pulmonary arterial hypertension market.

Commercialization of Oral Prostacyclin & Non-Prostanoid IP-Receptor Agonists Enhancing Adherence

Oral agents such as selexipag and oral treprostinil delay clinical worsening and trim hospitalization rates, improving real-world persistence. Maintenance dosing studies found no adherence drop-off across individualized regimens, supporting precision dosing models that keep patients on therapy longer. Comparative analyses reveal similar safety but superior convenience versus parenteral prostanoids. These adherence gains translate into higher lifetime therapy value and reinforce the shift toward oral dominance within the pulmonary arterial hypertension market.

FDA Breakthrough Approvals of Novel Smad-Signaling Modulators Driving Pipeline Momentum

Sotatercept secured FDA approval in March 2024 after delivering a 34.4 m improvement in 6-minute walk distance in STELLAR and an 84.0% reduction in clinical worsening in ZENITH, prompting early trial stoppage. Its success validates vascular-remodeling reversal and spurs investment in similar mechanisms such as HDAC inhibitors CS1 and inhaled imatinib AV-101. As sponsors pivot toward disease modification, combination regimens pairing sotatercept with ERAs or prostacyclin pathway agents could expand addressable segments and uplift revenue intensity for the pulmonary arterial hypertension market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Parenteral prostacyclin adverse events & infections | −0.7% | Global, Elderly cohorts | Short term (≤ 2 years) |

| Reimbursement constraints in South America & Africa | −1.1% | LMICs in South America, Africa | Long term (≥ 4 years) |

| Persistent diagnostic delays >24 months in rural Asia-Pacific reducing treatable patient pool | −0.8% | Rural India, Indonesia, Vietnam | Medium term (2-4 years) |

| 2026-28 patent cliff for ERA & PDE-5 agents triggering generic price erosion | −0.9% | Global developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Serious Adverse Events & Infection Risk with Parenteral Prostacyclin Pumps Deter Uptake in Elderly

Continuous intravenous prostacyclin carries risks of hypotension, nausea, and catheter-related bloodstream infections that discourage early use, especially in older patients with multiple comorbidities[3]Martha Kingman et al., “Management of Prostacyclin Side Effects,” Pulmonary Circulation, journals.sagepub.com. A real-world survey found intermediate-risk patients often do not receive guideline-recommended parenteral therapy because clinicians weigh infection hazards against benefit. This safety profile drags on uptake and shifts demand toward oral and inhaled alternatives in the pulmonary arterial hypertension market.

Constrained Reimbursement Budgets Limiting Triple Therapy Access in South America & Africa

Triple regimens can exceed USD 300,000 annually, a daunting cost for health systems with modest drug budgets. The Access to Medicine Index shows sluggish progress in company programs to widen treatment access in low-income countries. Orphan-drug pricing debates highlight the tension between rewarding innovation and maintaining affordability. Limited reimbursement restricts penetration and slows overall revenue expansion for the pulmonary arterial hypertension market in emerging regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Endothelin Antagonists Hold Leadership amid Modulator Momentum

Endothelin receptor antagonists generated 41.35% of revenue in 2025 as macitentan and ambrisentan remain foundational across disease severities. This segment benefits from fixed-dose combinations such as Opsynvi that simplify multipathway blockade. The pulmonary arterial hypertension market size for ERAs is projected to grow modestly through 2031 as competition from disease-modifying agents intensifies.

Smad-signaling modulators headline the “Other” segment and are forecast to post a 9.02% CAGR through 2031, reflecting clinical enthusiasm for sotatercept’s robust mortality benefit. PDE-5 inhibitors stay relevant for their favorable safety profile, while prostacyclin analogs retain utility in advanced disease. The pulmonary arterial hypertension industry is likely to see increased experimentation with dual-action molecules such as sparsentan that integrate endothelin blockade with additional pathways to raise efficacy.

By Route of Administration: Oral Dominance Faces Inhalation Upswing

Oral drugs accounted for 65.40% of sales in 2025 and remain the preferred first-line modality thanks to convenience and the push for early combination therapy. Inhaled formulations, led by Tyvaso DPI, are projected to be the fastest-growing subsegment at an 8.22% CAGR because they deliver prostacyclin directly to the pulmonary bed without invasive hardware.

Subcutaneous and intravenous routes remain indispensable for decompensated patients, and innovations such as RemunityPRO pumps seek to reduce infection risk and boost quality of life. Nonetheless, the pulmonary arterial hypertension market will keep migrating to less invasive modalities as efficacy gaps narrow.

By Drug Type: Branded Portfolio Dominates Despite Looming Patent Cliffs

Branded drugs held 84.20% revenue share in 2025, sustained by the complexity of biologics and delivery devices. High-value products such as Winrevair are priced at USD 14,000 per vial, translating into an annual therapy cost near USD 238,000. The pulmonary arterial hypertension market share of generics will grow after 2026 as patents expire on Remodulin and nebulized Tyvaso, and the Generic Drug User Fee Agreement accelerates abbreviated approvals.

Manufacturers counter generic erosion by layering new indications and delivery formats onto existing brands. The pulmonary arterial hypertension industry also witnesses branded players investing in pipeline first-in-class assets to retain pricing power beyond current expirations.

By Distribution Channel: Hospital Pharmacies Lead as Digital Dispensing Gains Traction

Hospital pharmacies dispensed 57.20% of therapies in 2025 because many patients initiate parenteral or complex combination regimens under specialist oversight. However, telehealth expansion is lifting online pharmacy penetration, projected to grow 10.37% per year to 2031 as remote adherence tools improve persistence.

Retail outlets continue to service stable patients on oral regimens, but supply chain stakeholders are reassessing direct-to-consumer models that could streamline costs and transparency. These shifts will gradually dilute hospital share yet keep institutional channels central to advanced care within the pulmonary arterial hypertension market.

Geography Analysis

North America generated 44.30% of global revenue in 2025, supported by premium pricing and dense networks of accredited PAH centers. Sotatercept’s launch at USD 238,000 annually exemplifies the region’s willingness to fund high-cost orphan drugs, propelling Merck’s product to USD 419 million in first-year sales. Uptake of single-tablet combinations further consolidates the region’s share in the pulmonary arterial hypertension market.

Europe remains a vital revenue base thanks to coordinated registries and harmonized guidelines that speed incorporation of new evidence. National health systems negotiate steep discounts yet enable broad access to breakthrough drugs when survival benefits are compelling. Treatment-pattern surveys show higher combination-therapy use in Germany than in the United States, illustrating how reimbursement structures shape practice.

Asia Pacific is forecast to post a 6.79% CAGR through 2031 as AI-enhanced echocardiography tools such as US2.AI improve early detection accuracy, registering an AUC of 0.88 for pulmonary hypertension. Vision-language models like MePH further reduce mean pulmonary arterial pressure estimation error by nearly 50%. These diagnostic gains, along with rising healthcare spend, accelerate therapy adoption in the pulmonary arterial hypertension market.

Middle East & Africa and South America witness slower uptake due to reimbursement gaps. Access challenges limit triple-therapy penetration, yet pilot risk-sharing agreements and patient-assistance programs could unlock latent demand over the forecast horizon.

Competitive Landscape

Market concentration is moderate as multinational incumbents battle nimble biotechs exploring novel targets. Merck vaulted into a leading position by acquiring Acceleron for USD 11 billion, securing sotatercept, which could peak at USD 4 billion. Johnson & Johnson differentiates with once-daily Opsynvi, while United Therapeutics dominates prostacyclin delivery, generating USD 1.62 billion from Tyvaso products in 2024.

White-space opportunities include therapies for patients with cardiovascular comorbidities, where initial combination regimens require careful titration. Biotechs like Cereno Scientific are advancing HDAC inhibitor CS1, and Aerovate is developing inhaled imatinib AV-101, targeting a 70,000-patient market in the US and Europe. Artificial-intelligence applications for patient identification and dose-optimization promise a new layer of competitive differentiation in the pulmonary arterial hypertension market.

Pulmonary Arterial Hypertension Industry Leaders

United Therapeutics Corporation

Johnson & Johnson (Actelion Pharmaceuticals Ltd.)

Bayer AG

Gilead Sciences Inc.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Merck’s Phase III ZENITH trial showed Winrevair cut the composite risk of death, transplant, or hospitalization by 76%, prompting early halt

- April 2025: United Therapeutics posted Q1-2025 revenue of USD 794.4 million and confirmed RemunityPRO pump launch for late-2025

- March 2024: FDA approved Johnson & Johnson’s once-daily combo tablet Opsynvi following positive A DUE outcomes

- March 2024: FDA cleared Merck’s Winrevair, the first activin-signaling inhibitor for adult PAH

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pulmonary arterial hypertension market as the global revenue generated by prescription medicines that lower pulmonary vascular resistance in WHO Group 1 patients, including endothelin-receptor antagonists, prostacyclin analogs, soluble guanylate-cyclase stimulators, phosphodiesterase-5 inhibitors, calcium-channel blockers, and emerging activin-signaling inhibitors. Care settings span hospital, specialty, retail, and online pharmacies, and values are expressed in constant 2024 US dollars.

Scope Note: devices for right-heart support, surgical interventions, and drugs targeting non-Group 1 pulmonary hypertension lie outside this assessment.

Segmentation Overview

- By Drug Class

- Prostacyclin and Prostacyclin Analogs

- Calcium Channel Blockers

- Phosphodiesterase 5 (PDE-5)

- Endothelin Receptor Antagonists (ERA)

- Other Drug Class

- By Route of Administration

- Oral

- Intravenous

- Subcutaneous

- Inhalation

- By Drug Type

- Branded

- Generic

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team spoke with pulmonologists, specialty pharmacists, payers, and patient-advocacy leaders across North America, Europe, and Asia Pacific. These discussions clarified real-world combination-therapy penetration, post-launch discounting on first-in-class agents, and regional adherence patterns, helping us validate and fine-tune desk findings.

Desk Research

We extracted foundational statistics from tier-1 open sources such as the World Health Organization's Global Health Observatory, Orphanet's epidemiology files, American Lung Association morbidity reports, CMS Medicare Part D utilization data, and regulatory label archives from the US FDA and EMA. Trade association briefs (Pulmonary Hypertension Association), peer-reviewed journals like Circulation, and company 10-Ks provided treated-patient counts, pricing corridors, and launch timelines. D&B Hoovers, Dow Jones Factiva, and Questel enriched company revenue splits and patent expiry alerts. These illustrate but do not exhaust the broader universe of references our analysts consulted for data collection and cross-checks.

A second round of desk work captured import-export tallies for inhaled treprostinil (Volza), clinical-trial registries for sotatercept uptake, and national reimbursement tariffs that shape average sales prices. This layering anchored incidence, therapy mix, and pricing assumptions before we moved to interviews.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build modeled each country's patient pool. Outputs were corroborated through selective supplier roll-ups and sampled ASP × volume checks to balance totals. Key variables include diagnosed prevalence per million adults, first-line therapy share shifts after sotatercept approval, branded-to-generic price decay, hospital versus retail dispensing mix, and regional reimbursement ceilings. Multivariate regression projected each driver through 2030, guided by consensus ranges gathered during primary research. Where bottom-up estimates lacked transparency, gap factors were aligned back to prevalence data and historical sales to maintain internal consistency.

Data Validation & Update Cycle

Analysts reconciled modeled revenue with quarterly company disclosures, prescription audit signals, and mortality trends, then escalated variances for peer review before sign-off. Reports refresh each year, and we trigger mid-cycle updates for material events such as new FDA approvals or accelerated generic entry.

Why Mordor's Pulmonary Arterial Hypertension Baseline Is Trustworthy

Published estimates rarely match because firms differ in therapy scope, geographic breadth, and refresh cadence. Our disciplined variable selection, transparent assumptions, and yearly updates minimize those gaps.

Key gap drivers include competitor models that exclude generics, apply uniform ASP erosion across regions, or freeze epidemiology inputs for multiple years, whereas Mordor Intelligence rolls forward prevalence and therapy mix each cycle and re-prices drugs by payer segment.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.11 B (2025) | Mordor Intelligence | - |

| USD 8.02 B (2024) | Global Consultancy A | Excludes generics; one-year older baseline |

| USD 8.48 B (2025) | Industry Intelligence B | Uses list prices, not net realized prices |

| USD 8.0 B (2024) | Regional Consultancy C | Omits Asia Pacific and Latin America markets |

The comparison shows that when scope, price realization, and geography are harmonized, figures converge toward Mordor's baseline. Our step-wise validation therefore offers decision-makers a balanced, reproducible reference point they can trust.

Key Questions Answered in the Report

What is the current size of the pulmonary arterial hypertension market?

The market stands at USD 8.57 billion in 2026 and is projected to reach USD 11.27 billion by 2031.

Which drug class holds the largest pulmonary arterial hypertension market share?

Endothelin receptor antagonists lead with 41.35% share in 2025.

Why is sotatercept considered a game-changer?

Sotatercept is the first activin-signaling inhibitor and reduced clinical worsening or death by 84.0% in the ZENITH trial, signaling a shift toward disease-modifying therapy.

Which region is expected to grow fastest through 2031?

Asia Pacific is forecast to expand at a 6.79% CAGR thanks to improved diagnostics and healthcare access.

How are inhaled therapies shaping future treatment?

Dry-powder inhalers such as Tyvaso DPI deliver prostacyclin directly to the lungs, offering targeted efficacy with greater convenience than intravenous pumps.

Page last updated on: