Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

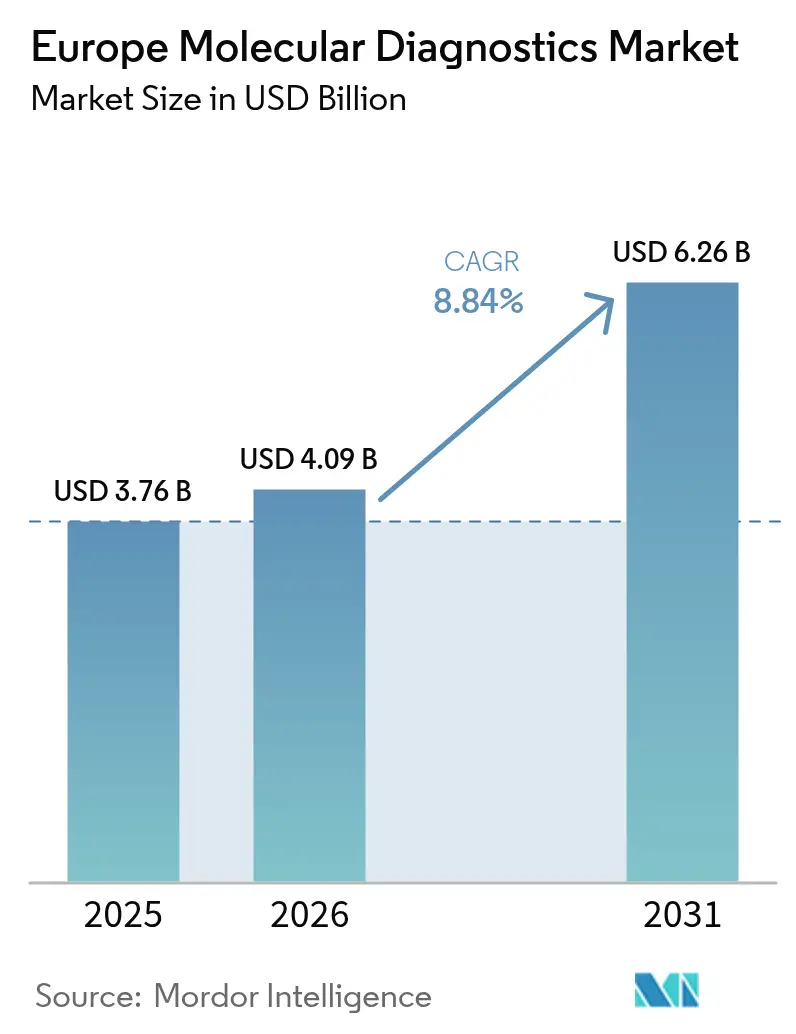

| Base Year Market Size (2025) | USD 3.76 Billion |

| Market Size (2026) | USD 4.09 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Molecular Diagnostics Market Analysis by Mordor Intelligence

Europe molecular diagnostics market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.76 billion with 2031 projections showing USD 6.26 billion, growing at 8.84% CAGR over 2026-2031. Adoption of precision-medicine protocols, full enforcement of the In Vitro Diagnostic Regulation (IVDR), and stable funding for antimicrobial-resistance surveillance shape this outlook[1]European Commission, “Regulation (EU) 2017/746 on in vitro diagnostic medical devices,” ec.europa.eu. Point-of-care (POC) platforms reduce diagnostic turnaround to under an hour, while next-generation sequencing (NGS) moves routine testing from single-gene PCR toward comprehensive genomic profiling. NGS run costs, now below USD 500 per whole exome, make high-throughput sequencing affordable for mid-tier laboratories. Artificial-intelligence (AI) engines that optimize primer and probe design shorten assay-development cycles, attracting venture funding in Germany, the Netherlands, and France. Together, these factors reinforce the Europe molecular diagnostics market as a cornerstone of hospital modernization programs across the region.

Key Report Takeaways

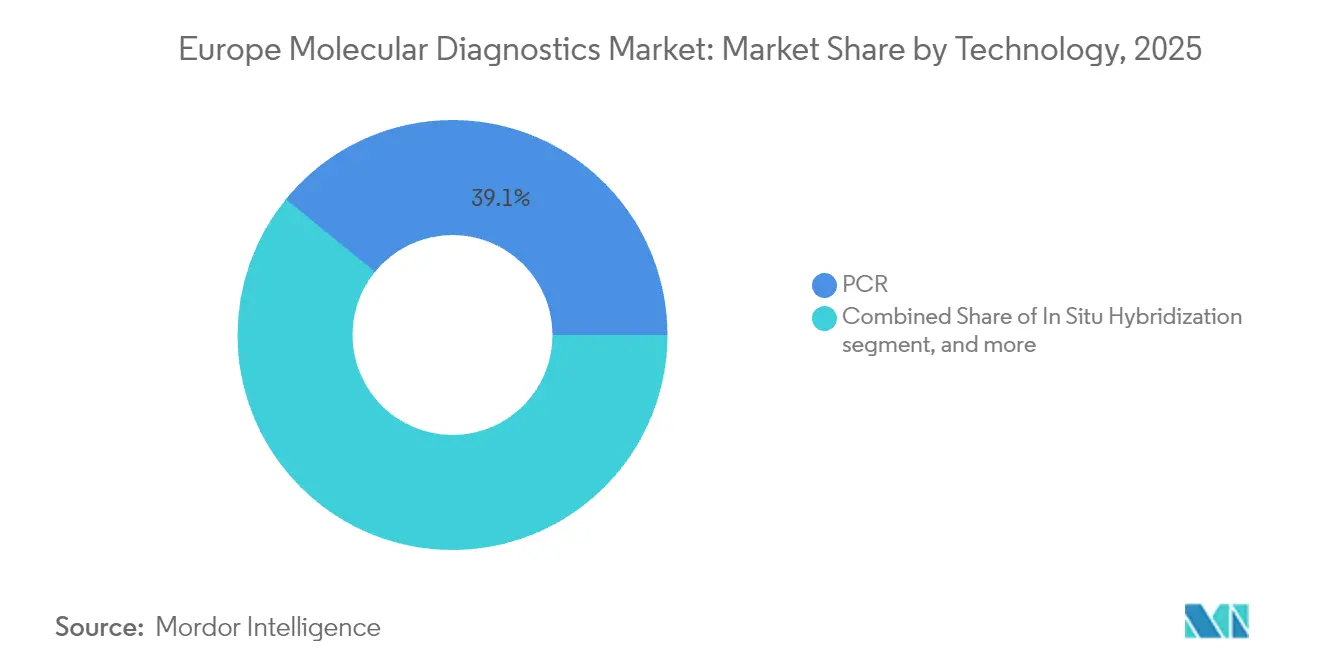

- By technology, PCR commanded 39.12% revenue share in 2025, while sequencing is projected to expand at a 9.45% CAGR through 2031.

- By application, infectious-disease diagnostics led with a 46.10% share in 2025; oncology and liquid biopsy tests are advancing at a 9.52% CAGR over 2026-2031.

- By product, reagents and kits generated 53.85% of 2025 sales, whereas software and services are growing fastest at a 8.98% CAGR.

- By end-user, hospitals and hospital laboratories accounted for 40.92% of 2025 revenue; point-of-care and near-patient settings are rising at a 10.08% CAGR.

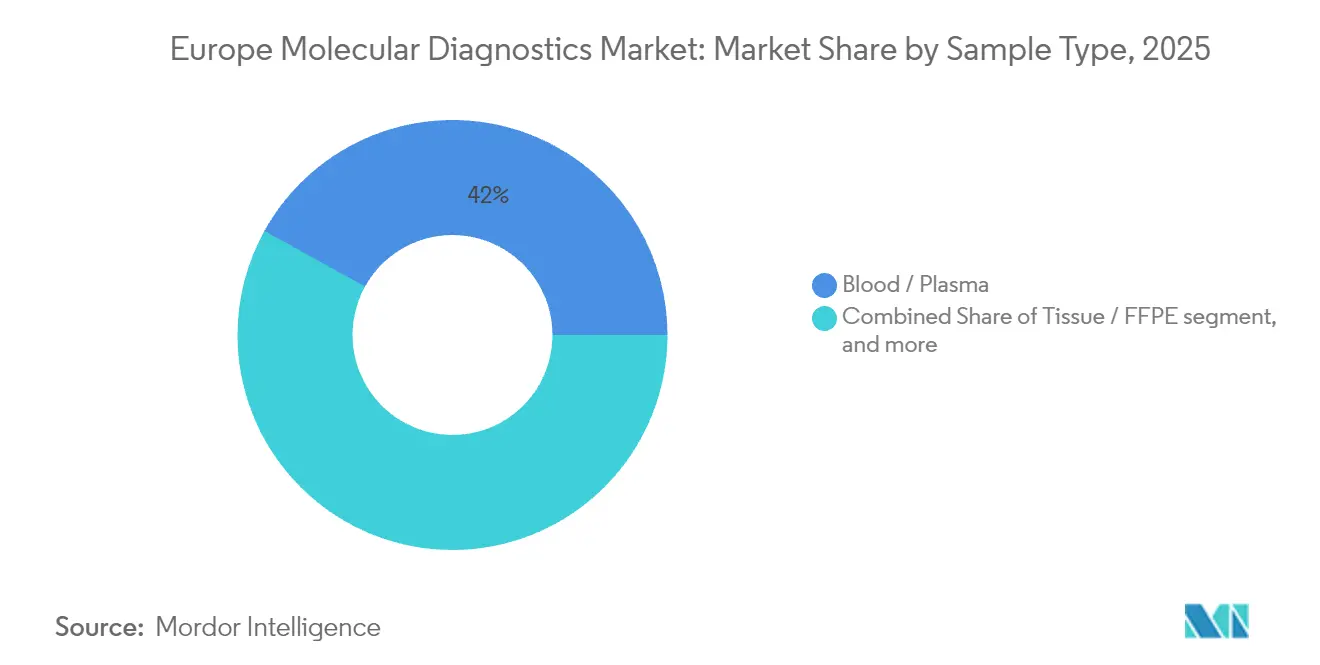

- By sample type, blood and plasma specimens represented 41.95% of 2025 testing volume, while urine and other body fluids are set to grow at an 8.38% CAGR.

- By test setting, centralized laboratories held 55.10% share in 2025 and are expected to progress at an 8.84% CAGR through 2031.

- By country, Germany captured 23.30% of regional revenue in 2025; Spain is anticipated to post the highest growth at a 9.18% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of point-of-care molecular assays | +2.1% | EU-wide; strongest in Germany, Netherlands, Nordic countries | Medium term (2 – 4 years) |

| Advances in NGS and pharmacogenomics platforms | +1.8% | Western Europe core; expanding to Central/Eastern Europe | Long term (≥ 4 years) |

| Surge in EU-wide antimicrobial-resistance surveillance mandates | +1.2% | All EU-27 member states | Short term (≤ 2 years) |

| IVDR-driven demand for CE-IVD companion diagnostics | +0.9% | EU-wide | Medium term (2 – 4 years) |

| Growth of AI-assisted primer and probe design startups | +0.7% | Innovation hubs: Germany, UK, France, Netherlands | Long term (≥ 4 years) |

| EU4Health and cohesion-funded lab-modernization programs | +0.6% | Central and Eastern Europe | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Point-of-Care Molecular Assays

Europe’s hospitals now place cartridge-based PCR and isothermal devices in emergency and outpatient units, cutting respiratory-pathogen turnaround from 24 hours to 45 minutes. German tertiary centers report that 60% of emergency departments use POC molecular panels for sepsis triage by 2024. Integrated analyzers upload results directly to electronic records, enabling antibiotic stewardship teams to adjust therapy within a single shift. Scandinavian primary-care clinics pilot near-patient multiplex panels for influenza, RSV, and SARS-CoV-2, reinforcing epidemiologic surveillance. Vendors respond with ruggedized instruments validated for bedside operation, barcoded reagent tracking, and secure cloud dashboards that meet GDPR requirements.

Advances in NGS & Pharmacogenomics Platforms

Sequencing consumable prices dropped 38% between 2023 and 2025, enabling mid-tier labs to offer 500-gene oncology panels under EUR 450 per sample (USD 489). Liquid-biopsy assays detect minimal residual disease months before imaging, prompting therapy adjustments without invasive tissue sampling. The European Medicines Agency now lists 28 companion diagnostics requiring NGS—double the 2022 count—which accelerates test-menu expansion. French payers reimburse CYP450 and DPYD panels, improving antidepressant and fluoropyrimidine safety. Eastern European reference labs outsource bioinformatics to cloud pipelines hosted in Frankfurt and Dublin, bypassing local skill shortages while meeting data-residency rules. Collectively, these factors propel the Europe molecular diagnostics market toward data-rich oncology workflows.

Surge in EU-wide Antimicrobial-Resistance Surveillance Mandates

The European Centre for Disease Prevention and Control (ECDC) requires genomic typing of carbapenem-resistant Enterobacterales and methicillin-resistant Staphylococcus aureus across all member states. EU4Health funding covers sequencer procurement, staff training, and external-quality schemes. National reference labs in Poland, Romania, and Hungary integrate robotic sample prep to meet weekly quotas, feeding data to the ECDC’s surveillance dashboard. Automated PCR systems now include 384-well plates and barcode readers to standardize protocols between decentralized sites. These mandates inject consistent demand across the Europe molecular diagnostics market, sustaining test volumes even during non-pandemic cycles.

IVDR-Driven Demand for CE-IVD Companion Diagnostics

Full IVDR enforcement in May 2022 establishes clear performance-classification rules that favor manufacturers with robust clinical-evidence portfolios. Pharmaceutical sponsors co-develop CE-IVD companion diagnostics alongside targeted therapies, securing synchronized approvals. Roche partnered with oncology drug developers to add EGFR and BRAF assays to its automated slide-staining line, reinforcing one-vendor procurement convenience. Laboratories value harmonized performance standards, easing multi-country test adoption. Over the forecast window, companion diagnostics are set to expand from oncology into cardiology and rare-disease domains, enlarging the Europe molecular diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Requirement for high-complexity testing infrastructure | -1.4% | Eastern Europe; rural regions across EU | Medium term (2 – 4 years) |

| Fragmented payer reimbursement across EU-27 | -0.8% | Variable by member state; most acute in Southern/Eastern Europe | Long term (≥ 4 years) |

| Shortage of certified molecular bioinformaticians | -0.6% | EU-wide; especially Central/Eastern Europe | Medium term (2 – 4 years) |

| IVDR compliance cost burden for small laboratories | -0.5% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Requirement for High-Complexity Testing Infrastructure

Advanced workflows need ISO 15189 accreditation, biosafety cabinets, and precision thermocyclers—assets scarce outside Western Europe[2]World Health Organization Europe, “Laboratory Infrastructure Gaps,” who.int. In 2024, demand for clinical bioinformaticians exceeded supply by 40%, delaying report sign-off in many Eastern European labs. Limited broadband hampers cloud pipelines in rural districts. EU cohesion funds finance upgrades, yet disbursement cycles stretch to five years. These infrastructure gaps temper near-term uptake, moderating the Europe molecular diagnostics market’s reach in less-resourced regions.

Fragmented Payer Reimbursement Across EU-27

Each member state runs separate health-technology-assessment (HTA) bodies, creating 27 reimbursement pathways. Spain and Italy bundle reagents, interpretation, and counseling into single tariffs, while Greece reimburses per-reaction PCR only. Companion diagnostics can wait 18–24 months for tariff assignment after CE-IVD approval, straining cash flow for smaller firms. Divergent evidence thresholds force duplicative utility studies, complicating price-volume negotiations and stalling diffusion of new tests across the Europe molecular diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PCR Dominance Faces Sequencing Disruption

PCR platforms generated USD 1.47 billion in 2025, equal to 39.12% of the Europe molecular diagnostics market size. Syndromic respiratory and sepsis panels remain anchored in qPCR due to mature workflows. Sequencing outpaces all technologies at a 9.45% CAGR, capturing oncology and infectious-disease tie-outs. Oxford Nanopore’s portable sequencers type meningitis pathogens in 45 minutes, encouraging hybrid strategies in which rapid PCR rules out common infections and on-demand NGS clarifies resistance profiles. Mass spectrometry and microarrays retain niches, but AI-enabled reagent design increasingly blurs platform borders, deepening vendor competition across the Europe molecular diagnostics market.

By Application: Infectious Disease Leadership Challenged by Oncology Growth

Infectious disease assays produced USD 1.73 billion in 2025, or 46.10% of the Europe molecular diagnostics market size. Multiplex panels detect 20+ pathogens per sample, reducing sequential testing. Whole-genome sequencing traces hospital outbreaks, feeding infection-control dashboards. Oncology assays grow at 9.52% CAGR, driven by liquid biopsy and targeted therapy selection. Pharmacogenomics panels cross into psychiatry and cardiology, though payer support lags in Southern Europe. Expanded newborn-screening programs push genetic-disease testing, while antimicrobial-resistance assays integrate qPCR with sequencing to oversee surveillance.

By Product: Reagents Lead; Software Integration Accelerates

Reagents and kits held 53.85% revenue share in 2025, leveraging recurring ordering cycles. Software and services climb 8.98% CAGR as labs adopt subscription-based informatics that translate raw data to clinical reports. GDPR compliance drives demand for European data centers and encryption. Instruments face price compression; however, analyzers that combine automation, multiplexing, and AI-enhanced quality control retain premiums. Service bundles now cover IVDR documentation, external-quality-assessment coordination, and workflow redesign—broadening revenue diversity within the Europe molecular diagnostics market.

By End-User: Hospital Labs Lead While POC Sites Accelerate

Hospital laboratories captured 40.92% market share in 2025, aligning molecular testing with oncology and transplant care. Consolidating pathology across regions delivers scale economies. Point-of-care sites grow 10.08% CAGR: community clinics run STI panels onsite, and mobile units in rural Spain sequence tuberculosis in field conditions. Independent reference labs offer esoteric panels and bioinformatics outsourcing, while academic centers validate next-generation assays ahead of IVDR filing. This layered ecosystem sustains the Europe molecular diagnostics market across centralized and distributed settings.

By Sample Type: Blood Plasma Leadership Faces Diversification

Blood and plasma samples contributed 41.95% revenue in 2025, vital for liquid biopsy and sepsis workflows. Tissue biopsies remain gold standard for solid tumors but face logistic delays. Urine, saliva, and other fluids grow 8.38% CAGR on self-collection programs for HPV and Chlamydia screening. Vendors develop stabilizing buffers that keep nucleic acids intact for seven days at ambient temperature, facilitating mail-in programs and widening the Europe molecular diagnostics market’s reach.

By Test Setting: Centralized Labs Maintain Scale; Hybrid Models Emerge

Centralized labs held 55.10% share and mirror the overall 8.84% CAGR, running automation tracks that cut hands-on time by 40%. Hub-and-spoke models let regional clinics perform urgent POC tests while batch-sending complex assays to national centers. Middleware transmits anonymized results to surveillance dashboards, securing epidemiologic coverage. Remote instrument qualification and e-proficiency testing lower compliance costs for spoke sites, embedding hybrid workflows firmly in the Europe molecular diagnostics market.

Geography Analysis

Germany generates 23.30% of regional revenue, anchored by dense tertiary networks, state reimbursement for NGS panels, and export-oriented biotech clusters in Munich and Heidelberg. Digital pathology adoption integrates molecular data with whole-slide imaging, streamlining tumor boards. The United Kingdom’s NHS Genomic Medicine Service standardizes 28 gene panels, while France’s Plan France Médecine Génomique funds 500,000 exomes over five years. Italy and Spain tap EU recovery funds for laboratory automation; Spain’s decentralized health system lets autonomous communities pilot NGS platforms, pushing a 9.18% CAGR through 2031. Eastern European recipients of cohesion funds upgrade sequencing lines, yet workforce shortages and reimbursement gaps moderate speed. Collectively, these dynamics solidify the Europe molecular diagnostics market as a mosaic where mature economies anchor volume and emerging regions drive incremental growth.

Regulatory Landscape

Europe molecular diagnostics is regulated under Regulation (EU) 2017/746 (IVDR). Its risk-based classification, strengthened clinical evidence expectations, and expanded Notified Body oversight shape market access for PCR, sequencing, and companion diagnostics. Regulation (EU) 2024/1860 also extended transitional provisions for legacy IVDs with class-specific timelines (extending into 2027 and 2028), while keeping key compliance milestones in force for manufacturers seeking continuity of supply.

The EU is moving lifecycle controls into EUDAMED, and from 28 May 2026 mandatory use of core EUDAMED modules (including actor registration, UDI/device registration, certificates, and vigilance) became effective for IVDR stakeholders. Companion diagnostics operate within an EU consultation framework involving the European Medicines Agency (EMA) and Notified Bodies, tightening alignment between therapeutic labeling and CE-IVDR diagnostic approvals and affecting launch sequencing for oncology panels across multi-country European pathways.

Value Chain Analysis

The Europe molecular diagnostics value chain spans inputs (high-purity enzymes, oligonucleotides, primers/probes, plastics/consumables), assay and instrument manufacturing, software and bioinformatics pipelines, and distribution into hospital labs, independent reference laboratories, and point-of-care settings. Reagents and kits remain the largest recurring procurement element, and the chain relies on cold-chain logistics and consistent lot-to-lot quality systems, while GDPR-aligned informatics and local data-center hosting have become key downstream workflow components for sequencing and syndromic testing.

IVDR compliance is a major operational layer across the chain, adding documentation and supplier-qualification lead times (often cited in the 12 to 24 month range for new supplier onboarding) and amplifying the impact of Notified Body capacity constraints (only 19 designated as of late 2025 in the evidence pack). Production constraints also concentrate around specialized capacities such as GMP-grade oligonucleotide synthesis and lyophilization, reported at 80 to 90% utilization, which pushes laboratories and procurement networks toward multi-year framework agreements with tier-one suppliers to reduce discontinuation and shortage risk during the IVDR transition.

Competitive Landscape

Roche, Abbott, Thermo Fisher Scientific, QIAGEN, and bioMérieux combine for roughly 58% revenue, delivering integrated hardware–reagent–software stacks that streamline procurement. Oxford Nanopore and Seegene leverage differentiated chemistries and portable devices to challenge incumbents. AI-native platforms offer cloud interpretation, charging per analysed gigabase and addressing bioinformatics shortages. Thermo Fisher’s USD 180 million plant expansion in Germany shores up reagent supply, and Roche’s USD 295 million acquisition of LumiraDx’s portfolio extends cartridge diagnostics into decentralized sites. QIAGEN’s Azure tie-up automates secondary analysis, easing GDPR compliance. Such moves highlight an arms race for full-stack capability across the Europe molecular diagnostics market.

Europe Molecular Diagnostics Industry Leaders

Abbott Laboratories

Danaher Corporation

Agilent Technologies

F Hoffmann-la Roche Ltd

Hologic Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace in Europe is localized manufacturing and supply resilience for high-volume molecular test menus (respiratory/infectious disease syndromic panels, AMR surveillance workflows, and oncology companion diagnostics), under the administrative and continuity pressures created by IVDR transition activity. Capacity additions and site expansions provide concrete evidence of this shift. In May 2026, bioMeriéux announced an investment of over EUR 250 million for a new BIOFIRE PCR manufacturing facility in La Balme-les-Grottes, France, and Roche confirmed continuation of a EUR 600 million diagnostic production investment in Penzberg, Germany. Early 2026 also saw QIAGEN open a new 8,000 square meter site in Esplugues de Llobregat, Spain, designed to support the full value chain for QIAstat-Dx syndromic testing systems.

Regulatory digitization also creates an opportunity in software and services that reduce compliance friction and support faster multi-country deployment. Mandatory EUDAMED usage for core modules (including UDI/device registration) from 28 May 2026, alongside the November 28, 2026 registration deadline for legacy devices, increases demand for vendor-provided regulatory services, UDI-ready labeling and traceability, and middleware that links instrument fleets to quality and vigilance processes. This supports continued product mix shift toward integrated platforms that bundle reagents, instruments, and informatics, as well as service offerings that help laboratories manage IVDR documentation, external quality schemes, and cross-site standardization.

Recent Industry Developments

- July 2026: Roche received a CE Mark for a new blood-based test to identify tuberculosis infections. The launch broadens access to molecular testing approaches beyond sputum-dependent pathways and supports decentralized screening and triage use cases across European care settings.

- September 2025: Agilent Technologies received European IVDR certification for its MMR IHC Panel pharmDx (Dako Omnis) as a companion diagnostic for colorectal cancer. The certification strengthens compliant CDx availability under IVDR and reinforces demand for integrated assay platforms tied to oncology treatment selection.

- July 2024: Roche completed the acquisition of LumiraDx’s point-of-care portfolio for USD 295 million. The transaction expanded Roche’s decentralized diagnostics footprint and increased competitive intensity in near-patient molecular workflows where cartridge-based testing drives faster clinical decision-making.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as revenues earned in Europe from molecular diagnostics products used to detect or monitor diseases by analyzing nucleic acids, and it is measured in USD at the prices realized by suppliers and channels.

Scope exclusions: Excludes purely research-use-only assays and instruments that are not intended for clinical diagnostics.

Segmentation Overview

- By Technology

- In Situ Hybridization

- Chips and Microarrays

- Mass Spectrometry (MS)

- Sequencing

- PCR

- Other Technologies

- By Application

- Infectious Disease Diagnostics

- Oncology & Liquid Biopsy

- Pharmacogenomics

- Genetic Disease Testing

- Microbiology & Antimicrobial-Resistance

- Other Applications

- By Product

- Instruments & Analysers

- Reagents & Kits

- Software & Services

- By End-user

- Hospitals & Hospital Labs

- Independent Reference Laboratories

- Point-of-Care / Near-Patient Settings

- Academic & Research Institutes

- By Sample Type

- Blood / Plasma

- Tissue / FFPE

- Saliva & Buccal Swab

- Urine & Other Body Fluids

- By Test Setting

- Centralised Laboratories

- Decentralised / POC Sites

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a clear view of Europe level testing demand and the regulated IVD environment that molecular diagnostics operates in. Public sources were used to anchor disease burden and screening context, including the European Centre for Disease Prevention and Control (for infectious disease surveillance), Eurostat (for health system indicators), OECD health statistics, and WHO Europe publications.

To turn that context into sizing inputs, we also reviewed sources such as national public health institute updates, EU regulatory communication related to IVD oversight, and peer reviewed clinical journals that describe test adoption patterns and technology use. Company annual reports, investor presentations, and reputable press were then used to cross-check product mix signals and pricing direction, and paid subscriptions for company financials and patent databases were used selectively to reduce gaps when mapping technology and vendor footprints. The sources listed above are illustrative, and other public and paid references were also consulted to collect, validate, and clarify the final dataset.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with hospital and reference laboratory stakeholders, diagnostic procurement and lab operations roles, and industry specialists who track assay utilization and instrument placement trends across major European countries. Coverage was spread across APAC, EMEA, and the Americas based expert pools where relevant, and it helped us validate the assumptions behind secondary inputs, fill pricing and utilization gaps, and confirm which tests are being run in routine settings versus research contexts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | |

| Mid tier: 44% | Functional/Unit leaders: 39% | |

| Smaller Players: 20% | Managers: 45% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up combined logic, where Europe level demand pools were reconstructed from testing activity and disease area signals, then cross-checked using selective supplier and channel approximations. In practice, the top-down side leaned on indicators such as infectious disease testing volumes, oncology and genetic testing adoption trends, instrument installed base direction, and a realistic split between centralized labs and hospital labs. The market value was then derived using typical assay and consumable price bands.

Those totals were corroborated using bottom-up checks like sampled supplier revenue splits by region, channel feedback on average selling price movement, and utilization assumptions for key platforms. When a country level input was missing, it was proxied using closely comparable markets in Europe, followed by normalization using population, lab capacity, and healthcare spending signals to avoid overstating smaller countries.

Forecasting used scenario analysis, with a base case tied to expert expectations on IVDR related compliance timing, platform replacement cycles, and the pace of menu expansion for high-throughput and syndromic testing. A lighter statistical smoothing was applied to avoid sharp year-to-year jumps unless supported by clear external signals and interview confirmation.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including consistency tests across countries, cross-verification against known diagnostic spending signals, and a review of implied pricing and utilization levels for plausibility. When a variance was flagged, the underlying drivers were re-tested, and follow-up calls were triggered to re-check assumptions on assay mix, tender pricing, or lab workflow shifts.

Before sign-off, the model and write-up go through an analyst review sequence so that inputs, calculations, and conclusions stay aligned. Reports are refreshed annually, and interim updates are made when material events affect pricing, regulation, or demand. Right before delivery, a final sweep is done to ensure the latest view is reflected for clients.

Mordor Intelligence's Europe Molecular Diagnostics Market Size Measured Against Other Published Estimates

Published market sizes for Europe molecular diagnostics can look far apart because the scope is not always aligned, and because pricing and volume assumptions are refreshed at different times. Differences also show up when one estimate leans heavily on manufacturer revenues, while another leans more on test activity and utilization signals.

Software and standalone diagnostic services are outside Mordor Intelligence's scope here, which is one reason the 2025 value does not match sources that bundle informatics and service revenues into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.76 B (2025) | |

| Industry Publisher A | USD 5.60 B (2025) | Often bundles software and diagnostic services alongside instruments and kits, and it may apply broader product definitions that raise the total even if underlying testing volumes are similar. |

| Data Platform B | USD 6.80 B (2024) | Uses a different base year and a shorter forecast window, and it can reflect a wider view of molecular diagnostics that includes self-testing and a broader reagents basket, which shifts the starting value upward. |

Taken together, the spread is mainly explained by what gets counted as part of molecular diagnostics and how pricing and base year timing are handled. By keeping the scope tied to core molecular diagnostic products and then checking totals against utilization and channel pricing signals, the final number stays easier to trace back to clear, repeatable inputs.

Key Questions Answered in the Report

What is the projected value of the Europe molecular diagnostics market in 2031?

The market is expected to reach USD 6.26 billion by 2031 given its 8.84% CAGR.

Which technology segment is expanding fastest?

Sequencing platforms are advancing at a 9.45% CAGR on falling run costs and wider oncology use.

Why is Spain the fastest-growing geography?

SpainÕs healthcare investments in laboratory automation and decentralized testing drive a 9.18% CAGR.

How are point-of-care platforms reshaping testing pathways?

Cartridge-based systems cut result times to under 1 hour, improving antimicrobial stewardship and triage decisions.

What are the main hurdles for wider adoption in Eastern Europe?

Limited high-complexity infrastructure and fragmented reimbursement slow deployment of advanced assays.

How is AI influencing assay development?

Machine-learning platforms shorten primer design cycles and enhance assay specificity, supporting rapid response to emerging pathogens.

Page last updated on: