Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

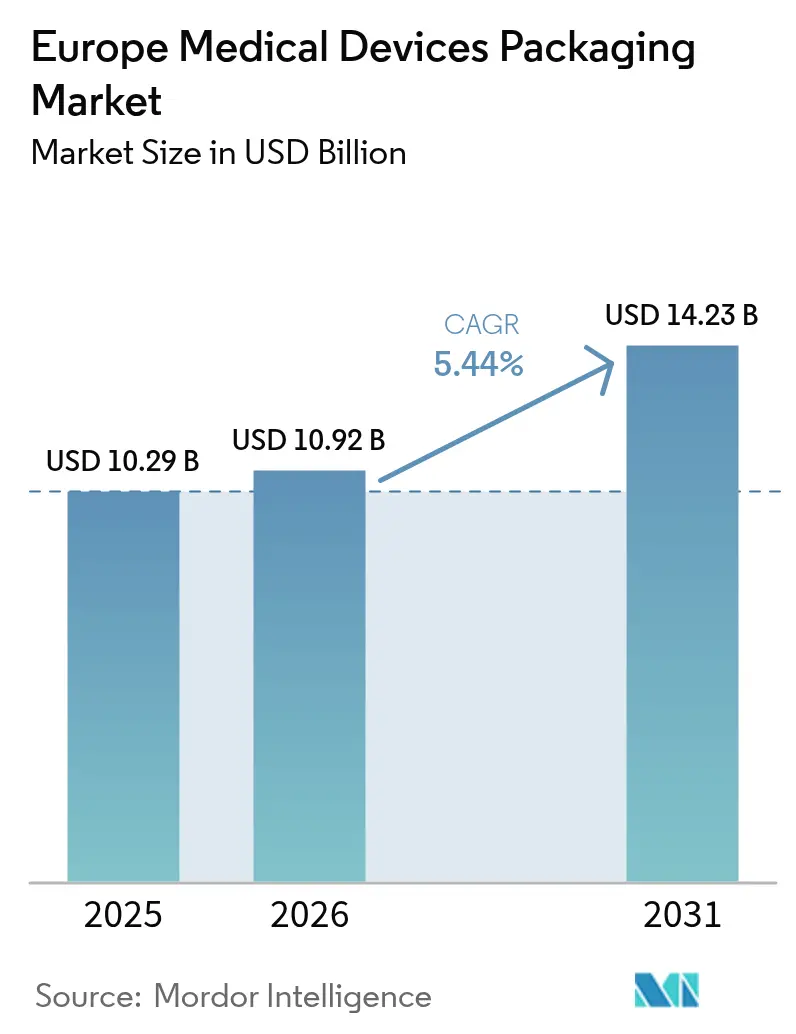

| Base Year Market Size (2025) | USD 10.29 Billion |

| Market Size (2026) | USD 10.92 Billion |

| Market Size (2031) | USD 14.23 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

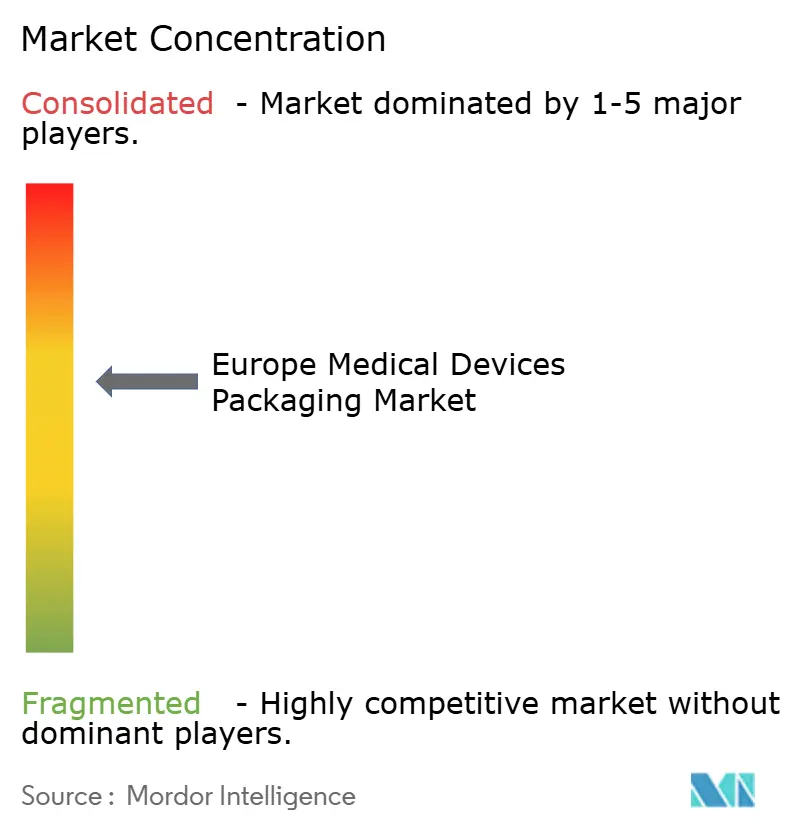

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medical Devices Packaging Market Analysis by Mordor Intelligence

The Europe medical devices packaging market size is projected to be USD 10.29 billion in 2025, USD 10.92 billion in 2026, and reach USD 14.23 billion by 2031, growing at a CAGR of 5.44% from 2026 to 2031. Demand is being lifted by the European Union Medical Device Regulation 2017/745, which obliges unique-device identification, and by rapid device miniaturization that favors thinner, traceable packs. Hospital buyers continue to specify validated sterile barriers, yet the shift toward home-health delivery is encouraging tamper-evident, easy-open formats. Sustainability mandates add further momentum, penalizing non-recyclable composites and rewarding bio-based polymers. Resin-price swings and carbon-reduction audits, however, are pressuring converters to optimize material use while safeguarding margins.

Key Report Takeaways

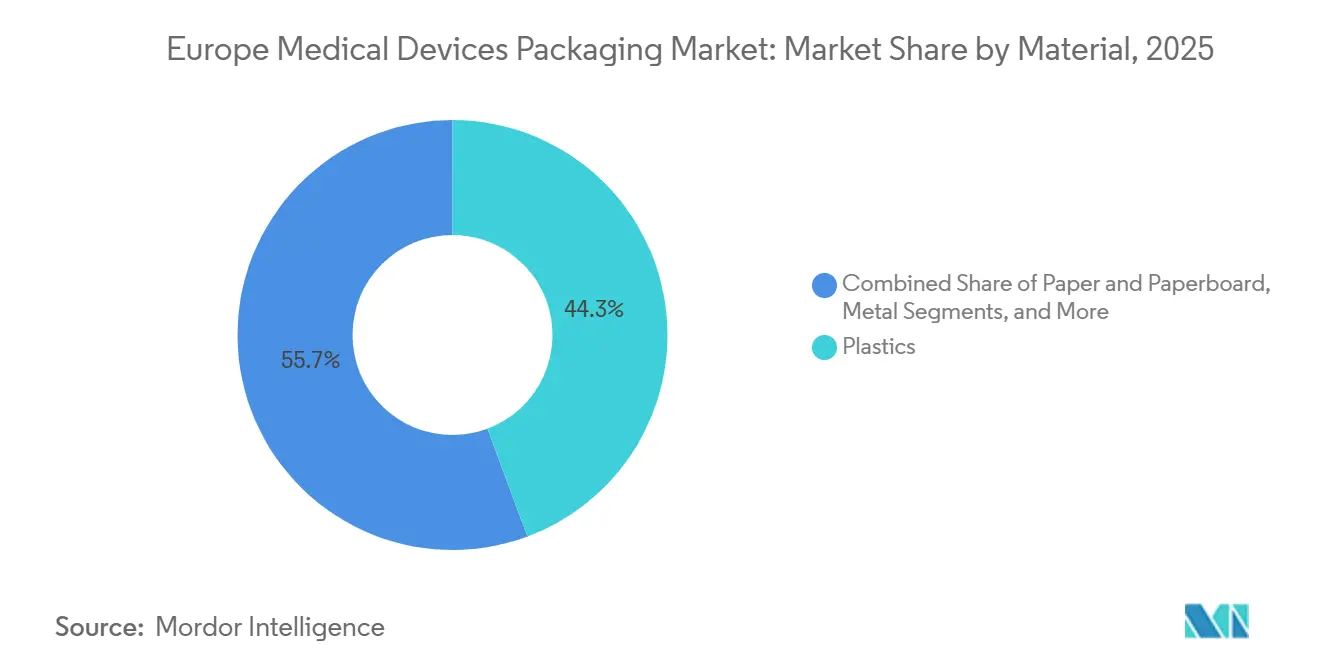

- By material, plastics led with 63.68% of Europe Medical Devices Packaging market share in 2025; bio-based polymers are forecast to expand at an 8.28% CAGR through 2031.

- By packaging format, pouches and bags captured 35.10% of Europe Medical Devices Packaging market size in 2025, while trays and clamshells are set to climb at a 7.29% CAGR to 2031.

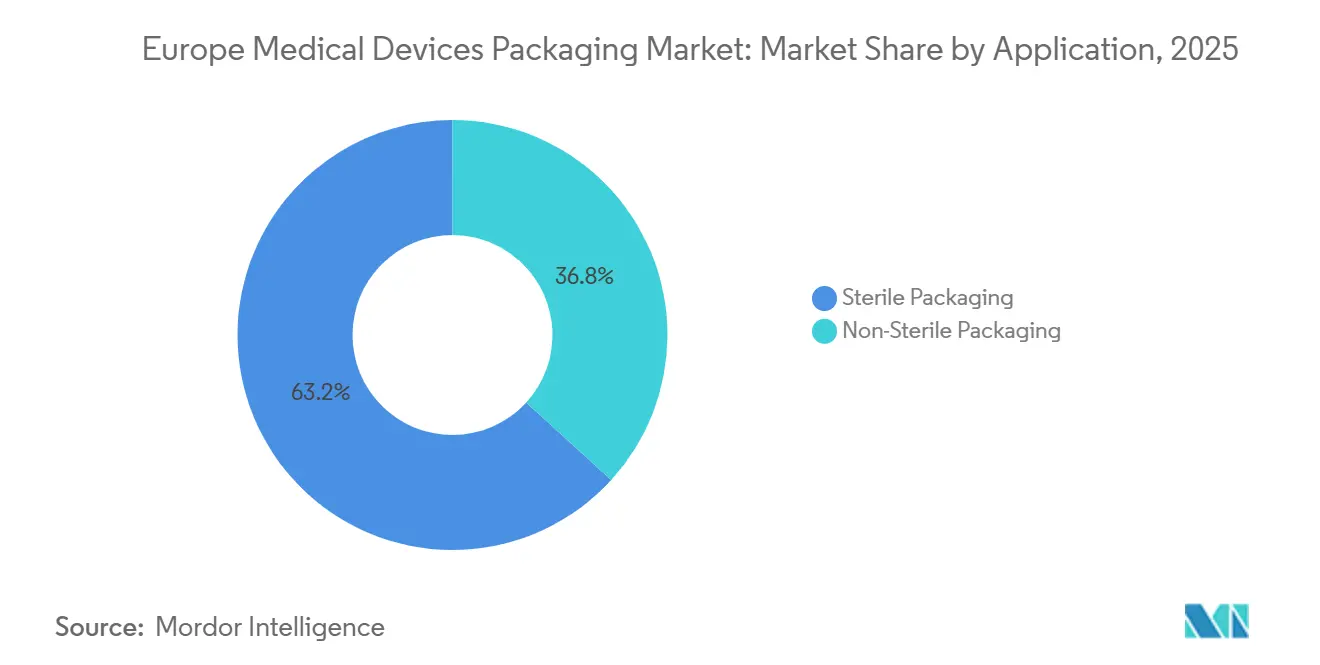

- By application, sterile packaging accounted for 82.05% of the Europe Medical Devices Packaging market size in 2025 and is advancing at a 6.12% CAGR through 2031.

- By end user, hospitals and clinics held 46.42% revenue share in 2025; home-health settings exhibit the highest projected CAGR at 7.73% through 2031.

- By country, Germany led with 22.30% market share in 2025, whereas Spain posted the fastest growth at an 8.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Longer Shelf-Life Packaging Solutions | +1.2% | Germany, France, United Kingdom, Netherlands | Medium term (2-4 years) |

| Accelerating Device Miniaturization Driving Innovative Pack Formats | +0.9% | Germany, United Kingdom, Netherlands, Spain, Italy | Short term (≤ 2 years) |

| EU MDR-Driven Traceability and UDI Labelling Requirements | +0.8% | EU-wide, strongest in Germany, France, Netherlands | Long term (≥ 4 years) |

| Growth of Home-Based and Remote Patient Monitoring Devices | +0.7% | United Kingdom, Germany, France, Spain | Medium term (2-4 years) |

| Sustainability Mandates Boosting Recyclable and Bio-Based Packs | +0.6% | France, Netherlands, Germany, Nordic region | Long term (≥ 4 years) |

| AI-Enabled Inline Inspection Improving Quality and Reducing Recalls | +0.5% | Germany, Netherlands, United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Longer Shelf-Life Packaging Solutions

Extended shelf-life targets are reshaping material choices as brand owners seek to cut inventory write-offs and support multi-region distribution. High-barrier laminates blending aluminum foil with ethylene vinyl alcohol now dominate sterile-pouch specifications, enabling three- to five-year stability for implantables and surgical instruments.[1]International Organization for Standardization, “ISO 11607-1:2019 Packaging for Terminally Sterilized Medical Devices,” iso.org ISO 11607-1:2019 obliges accelerated-aging proof, pushing converters to add peel testers and climate chambers. Contract manufacturers in Germany and the Netherlands report double-digit growth in ultra-high-barrier film requests since 2024, favoring suppliers with ISO 13485-aligned clean rooms. Larger converters therefore gain share, while smaller firms face entry hurdles tied to validation costs.

Accelerating Device Miniaturization Driving Innovative Pack Formats

Sensors and wearables weighing under 10 g require cavity depths below 5 mm, forcing precision thermoforming and micro-pouch production. Amcor logged a 22% jump in 2025 micro-pouch orders for diabetes patches. Film gauges have fallen to 50 µm, reducing resin use but heightening pin-hole risk, which is mitigated by in-line vision inspection. West Pharmaceutical Services integrated cameras that verify seals at 200 units per minute. High-volume, low-complexity jobs now migrate to automated hubs, while specialty packs remain with niche converters.

EU MDR-Driven Traceability and UDI Labelling Requirements

Full enforcement of EU MDR in 2024 mandates unique-device identification on Class I reusable and all higher-risk devices. Labels must survive sterilization and distribution, prompting uptake of laser-etched codes and high-contrast ribbons.[2]European Commission, “Medical Devices Sector-New Regulations,” europa.eu Gerresheimer stated that UDI redesigns made up 12% of its Q3 2025 project pipeline. The regulation links pack-level data to adverse-event reporting, elevating serialization infrastructure as a strategic asset.

Growth of Home-Based and Remote Patient Monitoring Devices

Europe’s aging population and payer pressure to cut readmissions are accelerating adoption of home-health kits. A 2025 peer-reviewed study noted that 38% of patients over 65 favor at-home monitoring. Berry Global introduced senior-friendly blisters catering to this shift. Packs must now balance tamper evidence, courier durability, and multilingual instructions, adding design complexity for converters previously focused on hospital bulk formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Layer EU Regulations and Compliance Costs | -0.6% | EU-wide, highest in Germany, France, Netherlands | Long term (≥ 4 years) |

| Volatility in Polymer Raw-Material Prices | -0.5% | Global, with pass-through across Europe | Short term (≤ 2 years) |

| Limited Recycling Infrastructure for Multi-Material Sterile Packs | -0.4% | Southern and Eastern Europe, moderate in West | Medium term (2-4 years) |

| Supply-Chain Carbon Reduction Targets Shrinking Blister Use | -0.3% | United Kingdom, France, Netherlands, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Layer EU Regulations and Compliance Costs

EU MDR, IVDR, the Packaging and Packaging Waste Regulation, and REACH restrictions create an overlapping web that strains mid-sized converters. Notified-body queues can delay technical-file reviews for 12-18 months, forcing dual inventories and hiking working capital. A 2025 MedTech Europe survey showed 29% of SMEs cite regulatory costs as the prime barrier, with consulting fees reaching EUR 150,000-300,000 (USD 169,500-339,000) per SKU.[3]MedTech Europe, “SME Regulatory Compliance Survey 2025,” medtecheurope.org The burden accelerates consolidation as larger firms amortize costs over wider portfolios.

Volatility in Polymer Raw-Material Prices

Polyethylene and polypropylene prices swung 18-25% between Q1 2024 and Q4 2025, driven by crude-oil volatility and feedstock outages. DuPont noted that European medical-grade polymer volumes rose 4.2% yet revenue lagged at 2.8%, underscoring margin squeeze. Bio-based alternatives fetch 20-30% premiums and are capacity-constrained, leaving converters a choice between absorbing costs, passing them on, or accelerating higher-priced sustainable materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bio-Based Polymers Gain Traction Amid Circular-Economy Push

Plastics held 44.32% of the Europe medical devices packaging market share in 2025, led by polyethylene and polypropylene in pouches and trays. Bio-based polymers are forecast to record a 6.23% CAGR, the fastest among materials, because Extended Producer Responsibility fees penalize non-recyclable composites. Polylactic acid has matured for non-sterile diagnostic kits, aligning with hospital waste-reduction targets.

Metal, chiefly aluminum foil, remains crucial for high-barrier laminates, though lightweighting from 20 µm to near 12 µm trims material costs. Paperboard continues to serve secondary roles but moisture sensitivity limits primary-pack use. Constantia Flexibles’ recyclable polyethylene-aluminum laminate, certified ISO 11607-2 in 2025, illustrates how converters respond to circular mandates. The Europe medical devices packaging market size for metal-foil laminates is likely to plateau as recyclability pressures mount.

By Packaging Type: Trays and Clamshells Rise on Surgical-Kit Standardization

Pouches and bags commanded 37.12% of 2025 volume and remain the workhorse for catheters and syringes. Trays and clamshells, however, are projected to expand at a 6.19% CAGR as hospitals adopt pre-sterilized surgical kits that cut set-up time and reduce instrument loss. Nelipak’s 2025 Dutch capacity boost targets this demand.

Boxes and cartons act as tertiary shippers and labeling surfaces, but e-commerce pushes designers to slimmer outer packs. Clamshell hybrids that pair thermoformed bases with sealed lids are winning share in pharmacy-shelf diagnostics. The Europe medical devices packaging market size attached to rigid trays benefits from damage-reduction savings that justify higher unit costs.

By Application: Sterile Packaging Sustains Leadership Through ISO 11607 Rigor

Sterile packaging captured 63.22% of 2025 revenue and is anticipated to post a 5.83% CAGR, sustained by implant launches and strict hospital infection-control protocols. ISO 11607 validation demands peel-strength and microbial tests that raise technical hurdles for new entrants. West Pharmaceutical Services disclosed that 68% of its European medical-packaging sales stem from sterile formats.

Non-sterile packaging grows more slowly but profits from the home-health boom, where usability trumps barrier performance. The Europe medical devices packaging market share for non-sterile packs is thus linked to consumer-grade diagnostics, a segment regulated under general product-safety directives rather than GMP inspections.

By End User: Home-Health Settings Surge as Care Decentralizes

Hospitals and clinics generated 40.70% of 2025 demand, underpinned by surgical volumes and centralized tenders. Home-health settings are on track for the highest 7.43% CAGR, propelled by chronic-disease management outside inpatient walls. Deloitte estimated 19% growth in home-health device shipments during 2025.

Diagnostic centers and laboratories provide steady mid-single-digit growth and often specify non-sterile sample-collection kits. Contract manufacturing organizations leverage turnkey assembly and sterile-pack services to attract start-ups seeking asset-light models. The Europe medical devices packaging market size allocated to home-health kits will therefore widen the gap with slower-growing hospital bulk formats.

Geography Analysis

Germany led the Europe medical devices packaging market in 2025 with a 21.00% revenue share, supported by ISO 13485 facilities and proximity to Siemens Healthineers and B. Braun. Spain is forecast for the fastest 7.93% CAGR through 2031, aided by a EUR 200 million (USD 226 million) incentive program that lures foreign converters. The United Kingdom, accounting for roughly one-sixth of demand, confronts post-Brexit dual-labeling costs that complicate SKU management.

France mandates recyclability under the AGEC law, accelerating R&D into mono-material pouches. Italy benefits from a pharmaceutical-packaging cluster in Emilia-Romagna, while the Netherlands, anchored by Rotterdam and Schiphol, operates as a logistics gateway. Central and Eastern markets such as Poland and Hungary offer labor arbitrage yet lag in recycling infrastructure, tempering adoption of circular-ready formats.

Converters often duplicate lines to satisfy divergent CE and UKCA marks, lifting fixed costs but preserving market access. Spain’s nearshoring pull aligns with supply-chain risk mitigation, and Germany’s dense notified-body presence speeds MDR compliance cycles. The Europe medical devices packaging market continues to diversify geographically, balancing mature high-spec hubs with fast-growing, cost-competitive locales.

Competitive Landscape

The top five suppliers Amcor, Berry Global, Gerresheimer, West Pharmaceutical Services, and DuPont held an estimated 35-40% combined 2025 share, indicating moderate concentration. Amcor filed a peelable recycled-content lidding patent that maintains gamma-sterile integrity.[4]European Patent Office, “Peelable Recycled-Content Lidding Film Patent,” epo.org Berry Global secured a five-year deal for child-resistant clamshells, underscoring the home-health trend. Gerresheimer expanded through a Barcelona thermoformer acquisition, reinforcing its Iberian footprint.

AI-enabled inspection is emerging, and Wipak integrates machine-learning defect detection that scans at 300 units per minute. Smaller specialists such as SteriPack and Oliver Healthcare Packaging win share by offering rapid prototyping and Tyvek expertise attractive to wearable-sensor brands.

Converters increasingly co-locate sterilization services, delivering turnkey solutions that lower customer cycle times. The Europe medical devices packaging market rewards firms that demonstrate validated clean-room capacity, serialization systems, and recyclability-focused innovation.

Europe Medical Devices Packaging Industry Leaders

Amcor plc

DuPont de Nemours Inc.

West Pharmaceutical Services Inc.

Tekni-Plex Inc.

Gerresheimer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Amcor announced a EUR 45 million (USD 50.85 million) expansion of its Sligo, Ireland, facility, adding ISO Class 7 space and three ultra-thin pouch lines.

- January 2026: Gerresheimer acquired a specialty thermoformer in Barcelona, Spain, gaining orthopedic-tray tooling.

- December 2025: West Pharmaceutical Services launched bio-based polyethylene pouches with 30% recycled content.

- November 2025: Berry Global signed a five-year supply deal for child-resistant clamshells for glucose-monitoring kits.

Europe Medical Devices Packaging Market Report Scope

The Europe Medical Devices Packaging Market is witnessing significant growth due to the increasing demand for advanced packaging solutions that ensure the safety, sterility, and integrity of medical devices. Factors such as the rising prevalence of chronic diseases, advancements in medical technology, and stringent regulatory requirements are driving the adoption of innovative packaging materials and designs in the region.

The Europe Medical Devices Packaging Market Report is Segmented by Material (Plastics, Paper and Paperboard, Metal, Bio-based Polymers), Packaging Type (Pouches and Bags, Trays and Clamshells, Boxes and Cartons, Other Packaging Type), Application (Sterile Packaging, Non-Sterile Packaging), End-User (Hospitals and Clinics, Home-Health Settings, Diagnostic Centres and Laboratories, CMOs and CDMOs), and Geography (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics |

| Paper and Paperboard |

| Metal |

| Bio-based Polymers |

By Packaging Type

| Pouches and Bags |

| Trays and Clamshells |

| Boxes and Cartons |

| Other Packaging Type |

By Application

| Sterile Packaging |

| Non-Sterile Packaging |

By End-User

| Hospitals and Clinics |

| Home-Health Settings |

| Diagnostic Centres and Laboratories |

| Contract Manufacturing Organisations (CMOs and CDMOs) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Material | Plastics |

| Paper and Paperboard | |

| Metal | |

| Bio-based Polymers | |

| By Packaging Type | Pouches and Bags |

| Trays and Clamshells | |

| Boxes and Cartons | |

| Other Packaging Type | |

| By Application | Sterile Packaging |

| Non-Sterile Packaging | |

| By End-User | Hospitals and Clinics |

| Home-Health Settings | |

| Diagnostic Centres and Laboratories | |

| Contract Manufacturing Organisations (CMOs and CDMOs) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe medical devices packaging market?

It was valued at USD 10.92 billion in 2026 and is projected to reach USD 14.23 billion by 2031.

Which material segment is growing fastest?

Bio-based polymers are forecast to expand at a 6.23% CAGR through 2031.

Why are trays and clamshells gaining popularity?

Surgical-kit standardization improves operating-room efficiency, driving a 6.19% CAGR for trays and clamshells.

How does EU MDR influence packaging design?

The regulation mandates traceable UDI codes that must remain legible after sterilization, pushing converters toward laser-etching and durable labels.

Which geography is expected to post the highest growth?

Spain is forecast for a 7.93% CAGR from 2026 to 2031 because of incentives for local device production.

What is the main challenge posed by raw-material pricing?

Resin price swings of up to 25% compress margins for converters locked into fixed-price hospital tenders.

Page last updated on: