Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

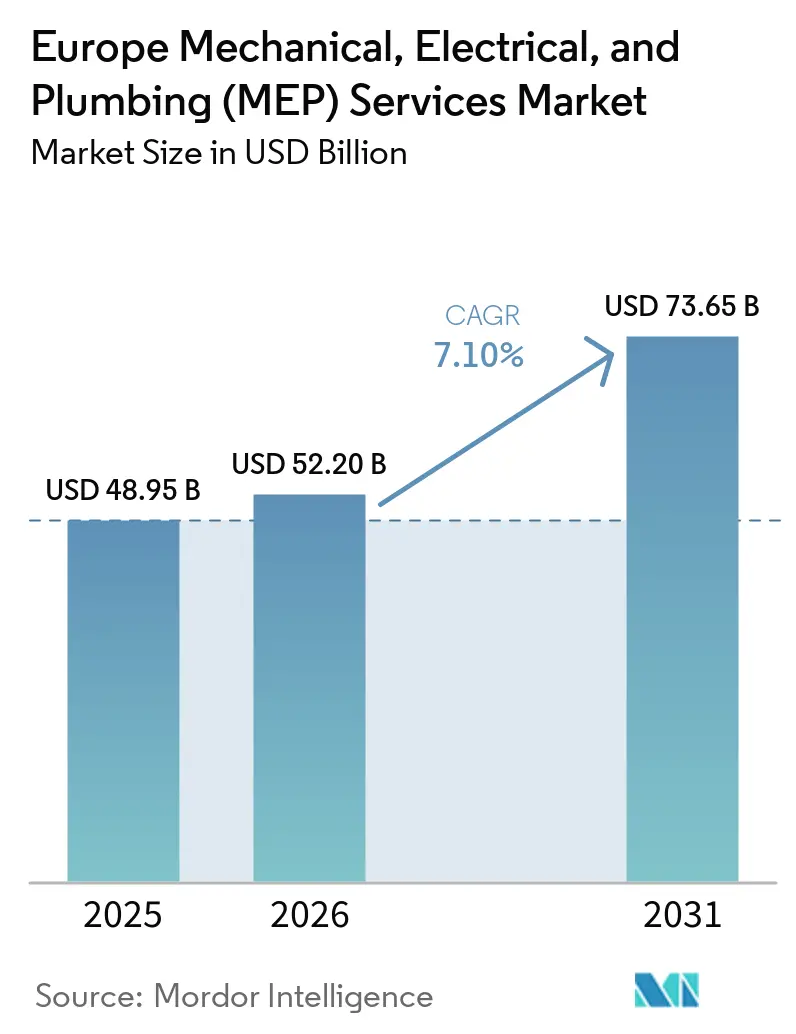

| Base Year Market Size (2025) | USD 48.95 Billion |

| Market Size (2026) | USD 52.20 Billion |

| Market Size (2031) | USD 73.65 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

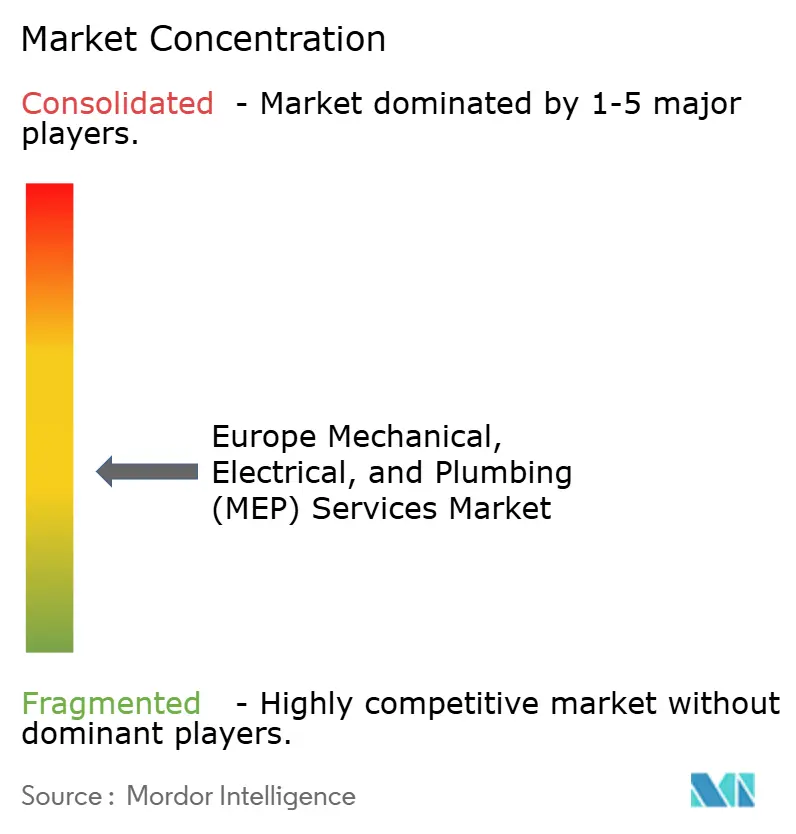

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The Europe Mechanical, Electrical, And Plumbing Services Market size was valued at USD 48.95 billion in 2025 and is estimated to grow from USD 52.20 billion in 2026 to reach USD 73.65 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031). The Europe Mechanical, Electrical, and Plumbing (MEP) Services market is being shaped by the recast EPBD, which requires EU member states to cut residential primary energy use, renovate the least efficient non-residential buildings, and expand building automation requirements across a wide installed base, with national transposition due by May 29, 2026. Demand is also supported by the region’s aging building base, where 75% of buildings underperform on energy efficiency and 85% to 95% of current buildings are expected to remain in use in 2050. Investment needs remain high, with building sector funding requirements estimated at EUR 242 billion (USD 261.4 billion) each year through 2030, and public money covering only 15% of that total, leaving a large role for private capital and specialist service providers. The Europe Mechanical, Electrical, and Plumbing (MEP) Services market is also gaining support from subsidy-backed renovation programs and new life-cycle carbon rules for buildings, which strengthen the position of firms that can combine engineering, controls, and carbon modeling in one delivery model.

Key Report Takeaways

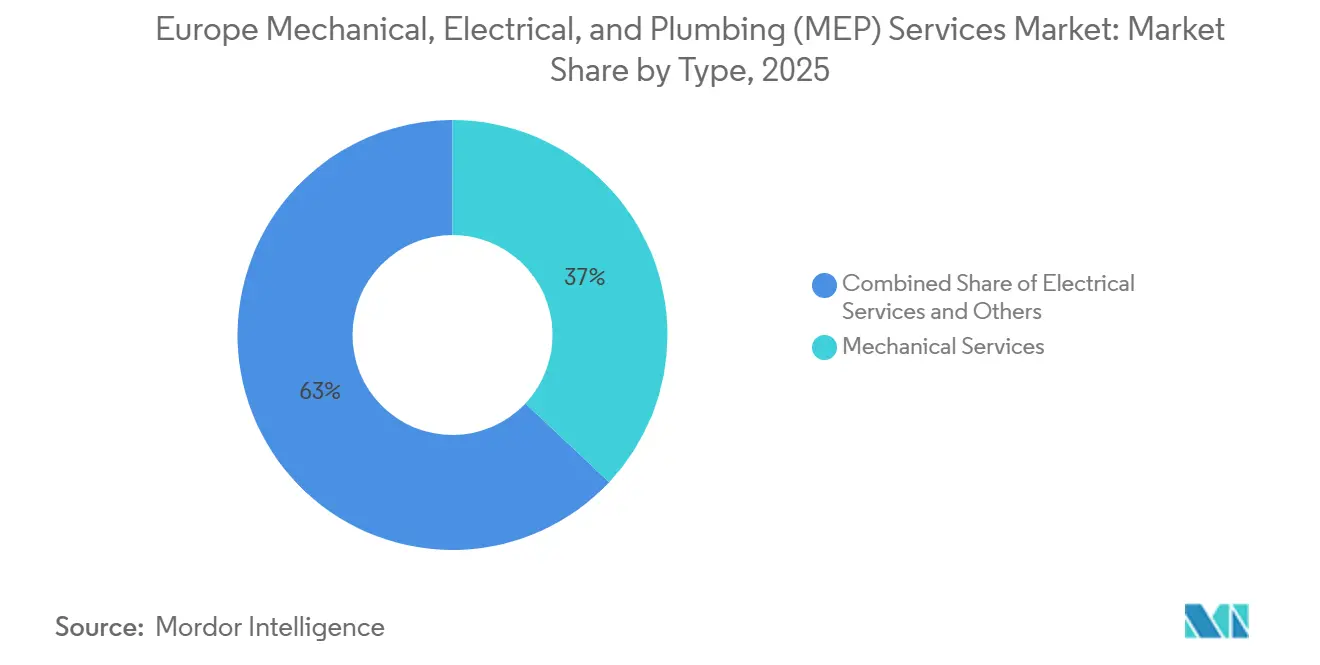

- By type, mechanical services led with 37% share in 2025, while integrated MEP services is forecast to expand at a 9.09% CAGR through 2031.

- By service type, maintenance, repair, and retrofit held 34% share in 2025, while managed / performance-based services are projected to grow at an 8.24% CAGR through 2031.

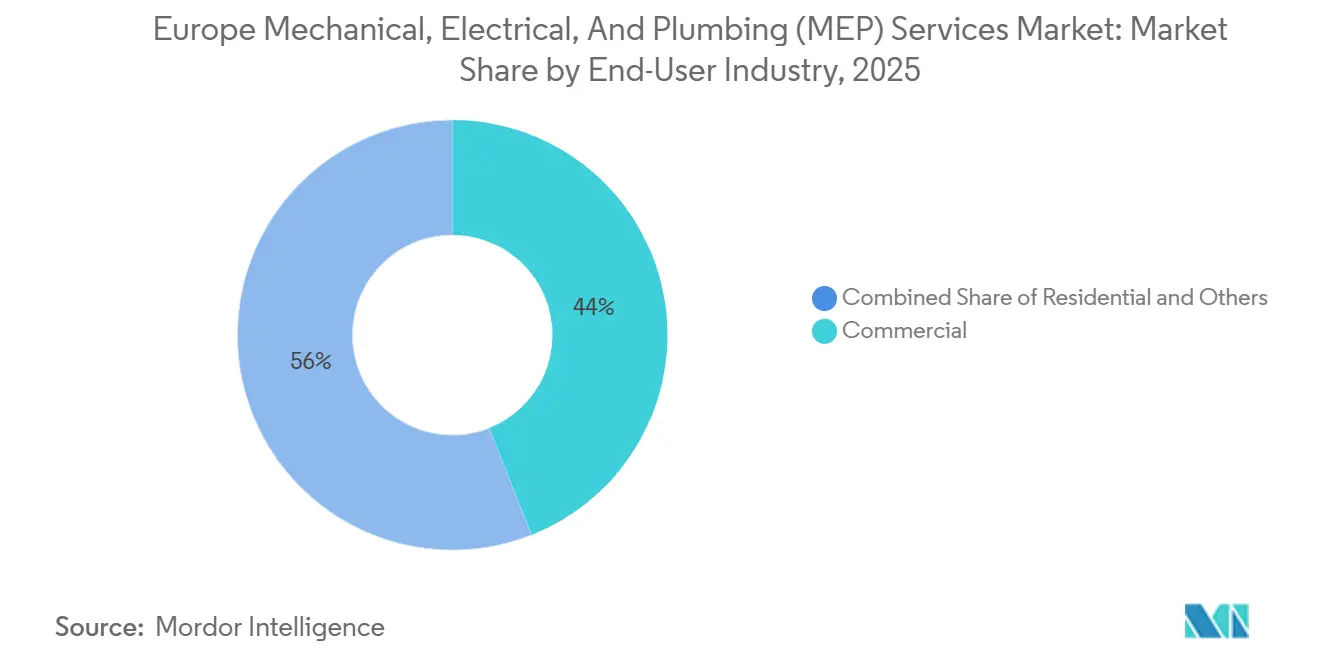

- By end-user industry, the commercial sector accounted for 44% of the market in 2025, while infrastructure is expected to grow at a 9.51% CAGR through 2031.

- By geography, Germany held 19% of the Europe MEP services market share in 2025, while Sweden is projected to record the highest CAGR at 8.59% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPBD Recast and Minimum Energy Performance Standards | +2.0% | EU-wide | Medium term (2-4 years) |

| Electrification Replacing Fossil Boiler-Led Retrofits | +1.5% | EU-wide, strongest in Germany, France, UK | Medium term (2-4 years) |

| Building Automation and Digital EPC Rollout | +1.2% | EU-wide, leadership in Germany, Netherlands, UK | Short term (≤ 2 years) |

| District And One-Stop-Shop Renovation Programs | +0.8% | EU-wide, Spain, France, Nordics | Medium term (2-4 years) |

| Smart Readiness Upgrades in Large Tertiary Buildings | +0.7% | North-West Europe, Germany, Netherlands, UK | Medium term (2-4 years) |

| Whole-Life Carbon Reporting Driving System Redesign | +0.6% | Denmark, Sweden, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EPBD Recast and Minimum Energy Performance Standards

The recast EPBD remains the strongest policy driver for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market in the current cycle[1]European Parliament and Council of the European Union, “Directive (EU) 2024/1275 of the European Parliament and of the Council of 24 April 2024 on the Energy Performance of Buildings (Recast),” Official Journal of the European Union, eur-lex.europa.eu. It requires renovating the worst-performing 16% of non-residential buildings by 2030 and 26% by 2033, while residential buildings must reduce average primary energy use by 16% by 2030 and by 20% to 22% by 2035. Member states were required to submit draft National Building Renovation Plans by December 31, 2025, and final plans are due by December 31, 2026, providing contractors and engineering firms with clearer visibility into future workloads. The rule set is more targeted than earlier policy cycles because it directs countries toward the worst-performing part of the stock first, creating a concentrated pool of buildings requiring deep MEP intervention. EU energy efficiency funding also expanded sharply for 2021 to 2027, with EUR 144.7 billion (USD 156.3 billion) allocated and EUR 79.4 billion (USD 85.8 billion) of Recovery and Resilience Facility funding directed to buildings, which improves project bankability across the region. This makes the Europe Mechanical, Electrical, and Plumbing (MEP) Services market less dependent on short new-build cycles and more dependent on compliance-led upgrades across existing assets.

Electrification Replacing Fossil Boiler-Led Retrofits

Electrification is reshaping the Europe Mechanical, Electrical, and Plumbing (MEP) Services market because financial support for stand-alone fossil fuel boilers ended from January 1, 2025 under Article 17(15) of the recast EPBD. Heat pump sales in the EU recovered to 2.34 million units in 2025 from 2.11 million units in 2024, and preliminary data from 13 EU member states pointed to 11% market growth in 2025. This shift changes the nature of retrofit scopes because contractors now need electrical upgrades, hydraulic balancing, controls integration, and commissioning rather than simple boiler replacements. Germany’s planned GModG framework adds another layer by tightening modernization rules and expanding obligations for low-emission buildings, which keeps retrofit activity active even as technology choices evolve. The EU Heat Pump Accelerator Platform and the future ETS2 regime for buildings add further policy support to this direction of travel. For the Europe Mechanical, Electrical, and Plumbing (MEP) Services market, this means demand is shifting toward more complex, higher-value retrofit packages.

Building Automation and Digital EPC Rollout

Building automation is creating a distinct stream of electrical and controls work inside the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. Non-residential buildings with heating, cooling, or ventilation systems above 290 kW were required to install building automation and control systems by the end of 2024, and the threshold falls to 70 kW by the end of 2029. This expands the addressable base from large buildings to a much wider stock of mid-sized commercial properties, which supports a broader installation and upgrade pipeline. The Netherlands moved early and required GACS from January 1, 2026 for non-residential buildings above 290 kW, which makes compliance work immediate rather than distant in that market. A peer-reviewed study in Energies found that moving from Class D to Class B automation under EN ISO 52120 can deliver 15% to 30% HVAC energy savings in heating-dominated buildings. That performance case makes the Europe Mechanical, Electrical, and Plumbing (MEP) Services market more attractive for integrated contractors that can combine HVAC replacement with automation and controls.

District and One-Stop-Shop Renovation Programs

District and one-stop-shop renovation programs are supporting the Europe Mechanical, Electrical, and Plumbing (MEP) Services market by turning fragmented building upgrades into larger and more manageable project pipelines. This matters because the EU still faces a large funding gap in building renovation, with annual investment needs estimated at EUR 242 billion (USD 261.4 billion) through 2030 and public funding covering only 15% of total requirements, underscoring the value of coordinated delivery models that can improve project execution and capital deployment. The Social Climate Fund, which starts deploying EUR 86.7 billion (USD 93.6 billion) from 2026, further strengthens this driver by directing funding toward energy-efficient renovation and clean heating for vulnerable households, creating a more stable retrofit pipeline for service providers. France already shows how public support can sustain demand, with annual support for building energy renovation of EUR 9.3 billion (USD 10 billion) across state, tax, and CEE mechanisms, while ANAH’s 2025 budget reached EUR 4.4 billion (USD 4.8 billion). Spain also adds momentum through its public buildings rehabilitation program, which targets the renovation of at least 1.23 million m², with 30% reductions in primary energy use by June 2026. These programs are especially relevant in France, Spain, and the Nordics because they help bundle technical work across HVAC, controls, electrical upgrades, and plumbing systems, which supports medium-term order visibility for integrated MEP contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Retrofit Technicians | -0.9% | EU-wide, acute in Germany, UK | Short term (≤ 2 years) |

| High Capex Across Fragmented Legacy Building Stock | -0.8% | EU-wide, most severe in Southern and Eastern Europe | Long term (≥ 4 years) |

| Split Incentives Between Landlords and Tenants | -0.6% | Germany, Sweden, broader EU | Long term (≥ 4 years) |

| Data and Interoperability Compliance Burden for BACS | -0.5% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Retrofit Technicians

Labor availability remains the clearest delivery constraint for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. The European Commission estimates that at least 750,000 additional heat pump installers are needed, and at least 50% of current installers will need reskilling for heat pump work. The same policy framework also recognizes skills barriers and one-stop-shop gaps as material obstacles to renovation delivery, indicating that the constraint is both institutional and operational. Shortages matter more now because retrofit scopes increasingly combine electrical, mechanical, wet-services, automation, and controls work in a single project. Qualification schemes also narrow the eligible contractor base, thereby improving technical quality but reducing the number of firms that can bid for complex compliance-led projects. This keeps demand intact but slows conversion of policy demand into booked revenue across the Europe Mechanical, Electrical, and Plumbing (MEP) Services market.

High Capex Across Fragmented Legacy Building Stock

High capital expenditure across Europe’s fragmented legacy building stock remains a long-term restraint on the Europe Mechanical, Electrical, and Plumbing (MEP) Services market because many retrofit projects require deep system upgrades rather than limited replacements. The cost burden is amplified by the age and quality of the region’s building base, where 75% of buildings underperform on energy efficiency, and 85% to 95% of today’s buildings are expected to remain in use in 2050, which means a large share of future demand sits in complex existing assets rather than standardized new buildings. The financing gap is also significant, with EU building-sector investment needs estimated at EUR 242 billion (USD 261.4 billion) per year through 2030, while public funding covers only 15% of total requirements. This limits project conversion because owners often need to combine heating, cooling, controls, electrical, and plumbing upgrades within a single renovation cycle to meet compliance targets under the recast EPBD. The burden is most severe in Southern and Eastern Europe, where fragmented ownership structures and weaker funding capacity make large-scale renovation harder to organize within a single investment plan. As a result, the European Mechanical, Electrical, and Plumbing (MEP) Services market continues to face a slower delivery pace in parts of the region, even when regulatory demand remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Services Lead While Integrated Platforms Accelerate

Mechanical Services held 37% of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market share in 2025, which made it the largest type segment in the region. This lead reflects HVAC replacement cycles, heat pump adoption, and district heating retrofit work that are all moving higher under the current policy mix. Electrical Services and Plumbing Services remain important adjacent volumes because most energy upgrades now involve power upgrades, controls wiring, hydraulic balancing, and wet-services work in the same package. Plumbing Services also benefits from the move toward heat pump and low-temperature system redesign, where water-side optimization becomes part of the core engineering scope. This keeps the Europe Mechanical, Electrical, and Plumbing (MEP) Services market firmly tied to whole-system retrofits rather than isolated equipment replacements.

Integrated MEP Services is projected to grow at a 9.09% CAGR through 2031, and the Europe Mechanical, Electrical, and Plumbing (MEP) Services market size for this segment is expanding faster because buyers want single-point responsibility for design, installation, automation, and commissioning. Within the Europe Mechanical, Electrical, and Plumbing (MEP) Services industry, this shift is most visible in data centers, life sciences, and technically demanding public projects where interface risk is costly. Germany’s modernization framework is also increasing the need for bundled scopes that combine automation, balancing, and performance compliance in the same contract. VINCI Energies’ 2025 acquisitions of Zimmer & Hälbig and R+S in Germany show how major players are building deeper integrated delivery capacity rather than relying on single-trade expansion.

By Service Type: Retrofit Work Leads While Performance Contracts Gain Ground

Maintenance, Repair, and Retrofit commanded 34% share in 2025, which made it the largest service-type segment in the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. That pattern fits a region where policy, subsidy, and compliance measures are focused on existing buildings rather than a broad-based new-build cycle. Design and engineering, together with installation, testing, and commissioning, still forms the core project-delivery pipeline, but those activities are more exposed to weaker construction starts in some large national markets. The Europe Mechanical, Electrical, and Plumbing (MEP) Services market therefore draws more stability from renovation programs and planned upgrades than from short-cycle building completions.

Managed / Performance-based Services is projected to grow at an 8.24% CAGR through 2031, and the Europe Mechanical, Electrical, and Plumbing (MEP) Services market size for this segment is rising because clients are shifting from equipment purchase to guaranteed operational outcomes. Within the Europe Mechanical, Electrical, and Plumbing (MEP) Services industry, this model is attractive because it aligns contractor incentives with energy performance, uptime, and digital monitoring. VINCI Energies expanded its NETO low-carbon performance contracts in France, and DSM-Firmenich signed for four manufacturing sites in April 2025, which shows that industrial clients are willing to buy measurable efficiency outcomes[2]VINCI Energies, “Yearbook 2025,” VINCI Energies, vinci-energies.com. SPIE’s multi-year facility management work in Frankfurt and Belgium also shows that technical monitoring, lighting upgrades, HVAC oversight, and optimization services are becoming part of longer operating contracts rather than short service calls. This makes recurring service revenue more important to the Europe Mechanical, Electrical, and Plumbing (MEP) Services market over the forecast period.

By End-User Industry: Commercial Spending Leads While Infrastructure Expands Faster

Commercial accounted for 29% share in 2025, which kept it as the structural anchor of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. Offices, retail assets, hospitals, hotels, and public buildings face the heaviest pressure from automation rules, smart-readiness requirements, and minimum performance expectations, so much of the region’s compliance work sits in this stock. That keeps commercial demand broad even when private investment sentiment weakens. It also creates room for bundled contracts that combine controls, HVAC, electrical upgrades, and ongoing monitoring in one service package. In practical terms, the Europe Mechanical, Electrical, and Plumbing (MEP) Services market continues to lean on commercial buildings because they sit at the center of both regulatory enforcement and measurable energy savings.

Infrastructure is projected to expand at a 9.51% CAGR through 2031, and the Europe Mechanical, Electrical, and Plumbing (MEP) Services market size for this segment is being lifted by data centers, grid assets, hydrogen projects, and other transition-linked facilities. Equans Data Centers delivered more than 80 MW of IT power in 2024 and 2025 across Europe, which underlines the scale of MEP activity now tied to digital infrastructure. Mercury Engineering’s Schönebeck facility in Germany also shows how supply chains are being organized around data center, semiconductor, and life-sciences delivery in mainland Europe. Residential demand remains weaker on new-build activity, but subsidy-backed renovation programs in France and wider EU support keep retrofit work active in that end-user group.

Geography Analysis

Germany held 19% of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market share in 2025, which kept it as the largest single-country market in the region. Its medium-term demand case rests heavily on the GModG pathway, which adds stronger modernization requirements, broader automation obligations, and a clearer path toward net-zero-emission buildings. That policy direction matters because Germany remains the largest addressable base for retrofit activity, even while parts of the construction cycle remain soft. The United Kingdom follows a separate regulatory path outside the EU framework, but it continues to generate meaningful engineering and infrastructure services work, as shown by AtkinsRéalis securing a GBP 780 million (USD 990.6 million) professional services framework in April 2024 and Jacobs, with AtkinsRéalis joining England’s National Highways SPaTS3 framework in July 2025. France remains one of the strongest renovation-backed markets because public financial support for building energy renovation stands near EUR 9.3 billion (USD 10 billion) each year, with ANAH’s 2025 budget reaching EUR 4.4 billion (USD 4.8 billion) and RE2020 applying in full to new tertiary buildings from the first quarter of 2025.

Sweden is the fastest-growing country market through 2031 in the Europe Mechanical, Electrical, and Plumbing (MEP) Services market, and demand there is increasingly shaped by energy systems rather than only traditional building construction. Swedish public sources show that more than 90% of multi-dwelling buildings already use district heating, which shifts project demand toward controls, network integration, automation, and compliance upgrades in older housing stock. Sweden also stands out because its renovation challenge is centered on older multi-dwelling stock from the 1960s and 1970s rather than on mass heating fuel conversion alone. Denmark and Norway, together with Sweden, form a Nordic cluster where district energy, heat recovery, and smart building integration remain the main demand themes, and Denmark already applies binding whole-building carbon limits from 2025.

Spain, Italy, and the Netherlands form the next layer of opportunity in the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. Spain’s public buildings rehabilitation program targets renovation of at least 1.23 million m² of public buildings with 30% primary energy reductions by June 2026, which sustains upgrade work in institutional assets. The Netherlands is moving quickly on controls compliance because non-residential buildings above 290 kW have been subject to GACS requirements from January 1, 2026. Italy’s incentive reset has cooled the earlier Superbonus push, but the large base of older residential stock still supports multi-year MEP workload through renovation and systems replacement. The rest of Europe is also becoming more active as EPBD transposition deadlines turn policy obligations into funded projects across a wider set of national markets.

Competitive Landscape

The Europe Mechanical, Electrical, and Plumbing (MEP) Services market is moderately concentrated at the top, where SPIE, VINCI Energies, Equans, ENGIE Solutions, and Eiffage Énergie Systèmes compete across design, installation, maintenance, and performance-based work. The market still remains fragmented below that level because several hundred regional specialists and trade-focused contractors serve local niches, technical sub-trades, and specific customer groups. This structure means scale matters in major tenders, but local execution depth still matters in day-to-day project delivery. It also helps explain why integrated platforms are gaining share while independent specialists continue to fill capacity gaps. For the Europe Mechanical, Electrical, and Plumbing (MEP) Services market, competition is being shaped as much by delivery model and technical breadth as by price.

Acquisition activity is one of the clearest signs of strategic positioning in the market. VINCI Energies completed 33 acquisitions in 2025, including Zimmer & Hälbig for HVAC in sensitive buildings and R+S for electrical and automation work in Germany, which shows how major groups are filling capability gaps through bolt-ons rather than waiting for organic growth. Turner Construction completed the acquisition of Dornan Group in January 2025, bringing a combined backlog above USD 33 billion and adding North American-scale capital to the European specialist tier. Mercury Engineering’s opening of its Schönebeck offsite manufacturing facility in April 2026 shows a parallel strategy that focuses on industrialized delivery capacity for data centers, semiconductors, and life sciences.

A second competitive theme is the growing importance of digital controls and reporting capability in long-cycle contracts. SPIE’s use of Smart FM 360° and the Beeldi interface at Siemens’ Huizingen site shows how firms are combining technical facility management with data-driven optimization and energy reporting[3]SPIE, “Siemens Entrusts the Maintenance of Its Site in Huizingen, Belgium to SPIE for the Next Four Years,” SPIE, spie.com. The opportunity is still wider in fragmented residential renovation, where European Commission material shows that many owners remain unaware of one-stop shops in their area, which leaves room for coordinators and managed-service models that simplify the customer journey. Entry barriers are also rising because EPBD Article 23, automation standards, and smart-readiness requirements demand better integration across HVAC, electrical, controls, and compliance reporting. That environment favors contractors that can prove technical depth, digital capability, and multi-trade coordination over a long service life.

Europe Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

SPIE

VINCI Energies

Equans

ENGIE Solutions

Eiffage Énergie Systèmes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EWE awarded Bilfinger a major contract for steelwork, piping, and component assembly for its 320 MW hydrogen production plant in Emden, Germany, one of the largest scopes under Europe's IPCEI-funded "Clean Hydrogen Coastline" project, with plant commissioning targeting late 2027.

- April 2026: Mercury Engineering officially opened its EUR 25 million (USD 27 million) Offsite Manufacturing (OSM) facility in Schönebeck, Germany, covering 13,000 m² of production space and serving as the company's mainland Europe engineering and fabrication hub for data center, semiconductor, and life sciences MEP delivery.

- February 2026: Bilfinger secured contracts as part of a consortium for BP's 100 MW green hydrogen electrolyser in Lingen, Germany, covering prefabrication, assembly, and HVAC installation, with commissioning planned for 2027.

- January 2026: Equans and BESIX received the Taking-Over Certificate for Phase 1A and 1B of the KevlinX 40 MVA Tier III data center in Neder-Over-Heembeek, Belgium, with Equans delivering the full MEP scope including HVAC, cooling, power, fire, and security systems.

Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The Europe MEP Services Market Report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation & Commissioning, Maintenance & Retrofit, Managed Services), End-User (Residential, Commercial, Infrastructure), and Geography (Germany, UK, France, Spain, Italy, Netherlands, Sweden, Denmark, Norway, Rest of Europe). Forecasts are Provided in Terms of Value (USD Billion).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance, Repair, and Retrofit |

| Managed / Performance-based Services |

| Residential |

| Commercial |

| Infrastructure |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Sweden |

| Denmark |

| Norway |

| Rest of Europe |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance, Repair, and Retrofit | |

| Managed / Performance-based Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market?

The Europe Mechanical, Electrical, and Plumbing (MEP) Services market is estimated at USD 52.2 billion in 2026 and is projected to reach USD 73.65 billion by 2031 at a 7.1% CAGR.

What is driving demand for MEP services across Europe?

The strongest demand drivers are the recast EPBD, mandatory renovation of inefficient buildings, building automation rollouts, heat pump adoption, and subsidy-backed renovation funding across existing building stock.

Which service category leads spending in Europe?

Maintenance, Repair, and Retrofit led with a 34% share in 2025, which reflects Europe’s renovation-first policy direction and the age of the installed building base.

Which type segment is growing fastest in this space?

Integrated MEP Services is the fastest-growing type segment, with a projected 9.09% CAGR through 2031, as clients increasingly want one contractor to handle multi-trade scopes.

Which end-user group offers the strongest growth outlook?

Infrastructure shows the highest growth at a 9.51% CAGR through 2031, supported by data centers, grid expansion, hydrogen projects, and other energy-transition assets.

Page last updated on: