Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

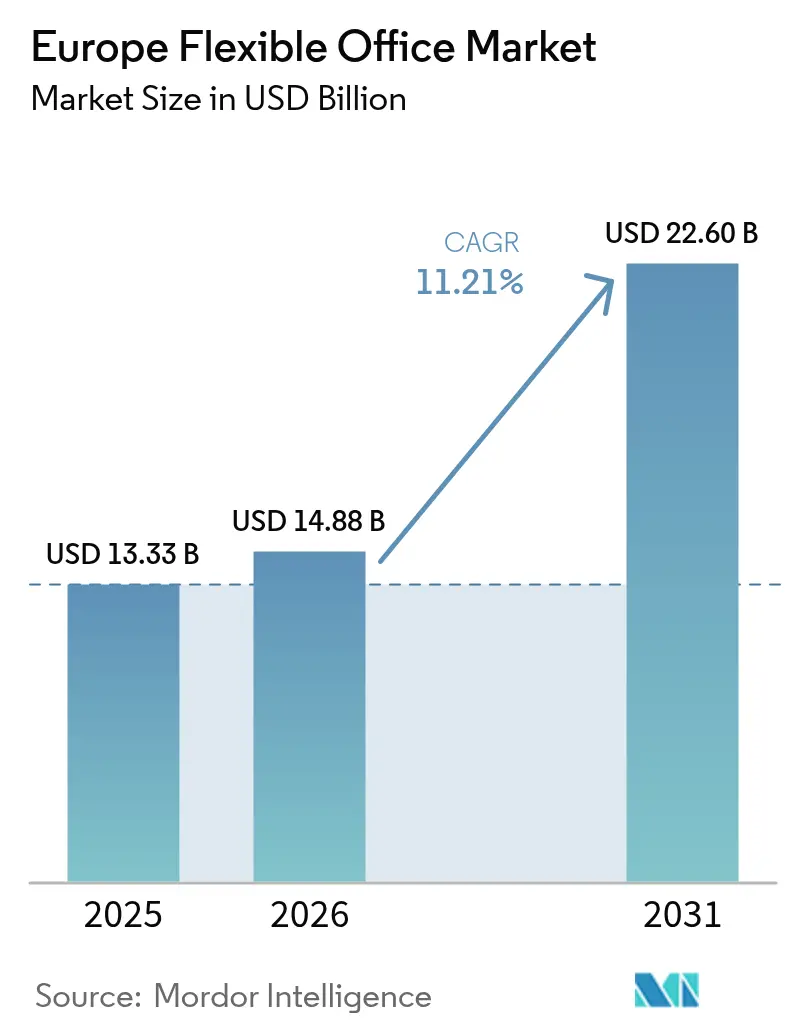

| Base Year Market Size (2025) | USD 13.33 Billion |

| Market Size (2026) | USD 14.88 Billion |

| Market Size (2031) | USD 22.60 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Flexible Office Market Analysis by Mordor Intelligence

The Europe flexible office market size is projected to be USD 13.33 billion in 2025, USD 14.88 billion in 2026, and reach USD 22.60 billion by 2031, growing at a CAGR of 11.21% from 2026 to 2031. Base-year revaluation, which now captures previously untracked serviced-office inventory as well as embedded flex desks inside corporate headquarters, produced the sharp 2025-2026 step-change, aligning European reporting with North American IFRS 16 lease-accounting standards[1]Eurostat Statistical Office, “Construction Cost Inflation Europe,” ec.europa.eu. Hybrid work policies that require three to four days in the office each week, together with rising demand for Grade-A, ESG-certified buildings, have created a resilient baseline for occupiers that view flex space as an essential portfolio component rather than surge capacity. AI-enabled occupancy analytics and private 5G connectivity are lifting revenue per workstation and lowering entry barriers for independent operators. Meanwhile, sustainability-linked loans are channeling capital into retrofit projects, expanding high-quality supply and keeping vacancy for premium assets structurally tight.

Key Report Takeaways

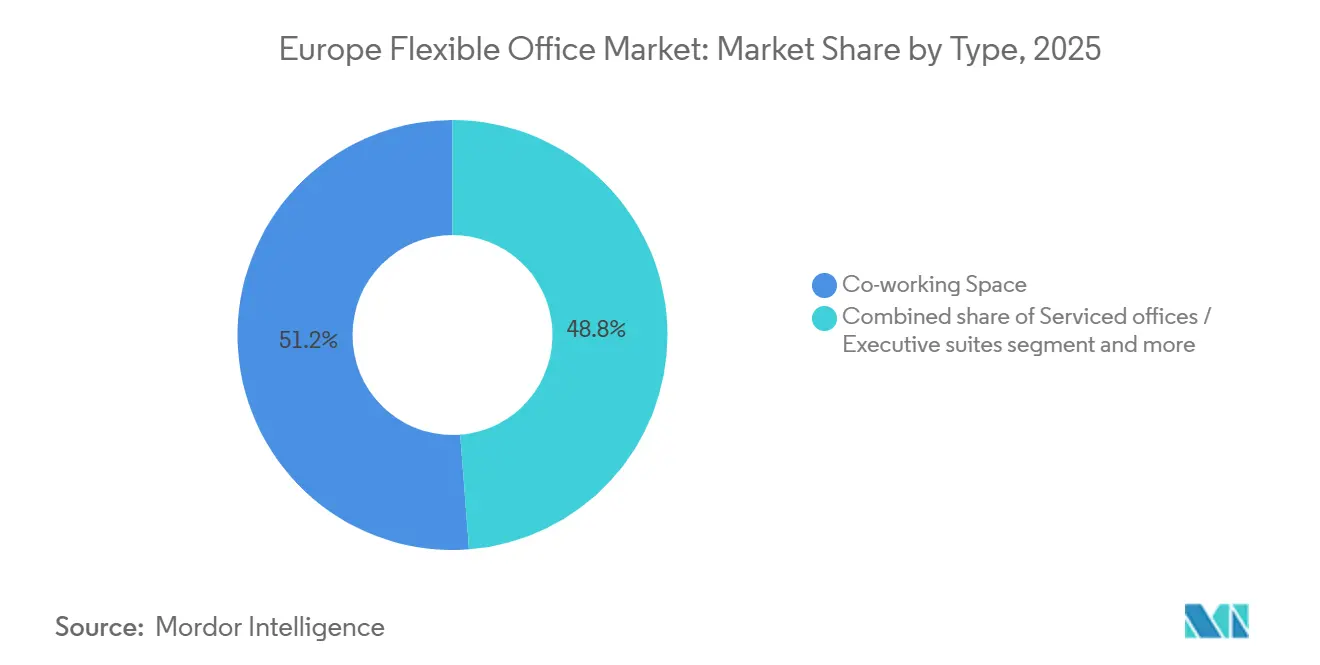

- By type, co-working spaces led with 51.22% revenue share in 2025, while serviced and executive suites are forecast to expand at a 12.1% CAGR through 2031.

- By sector, information technology and IT-enabled services captured 32.11% of the Europe flexible office market share in 2025; banking, financial services, and insurance is projected to grow fastest at an 11.98% CAGR to 2031.

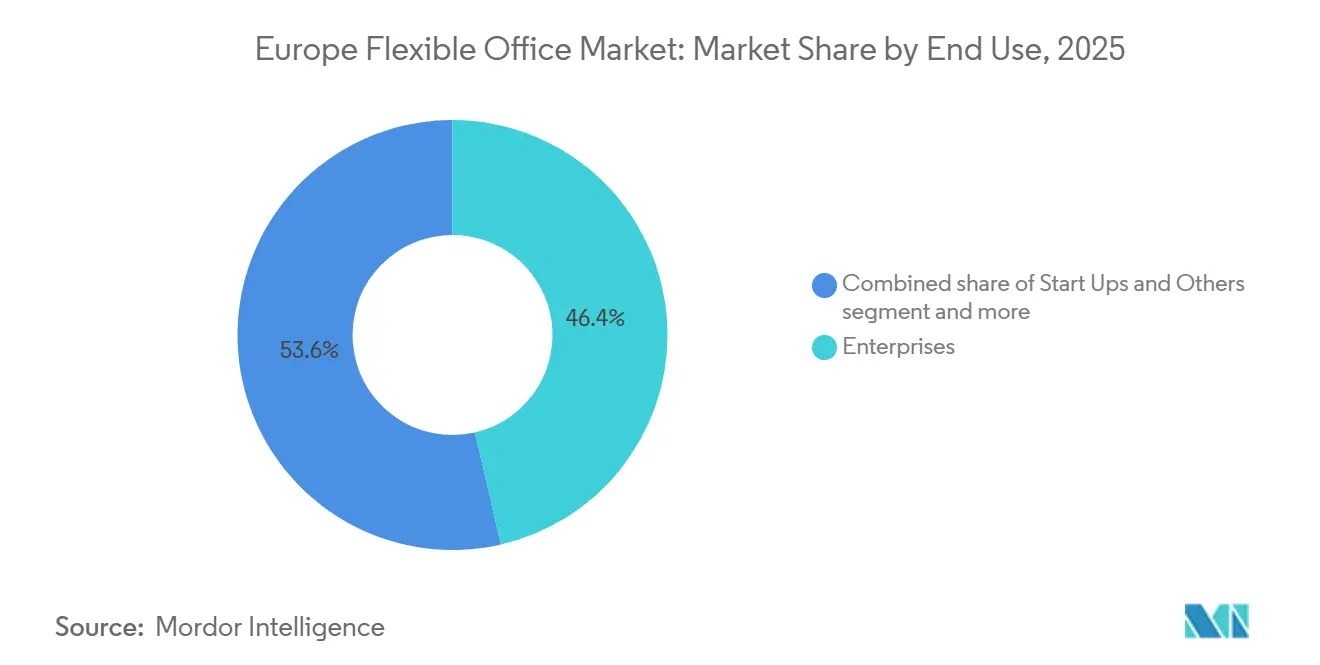

- By end use, enterprises accounted for 46.4% of demand in 2025, whereas freelancers are set to rise at a 12.55% CAGR between 2026 and 2031.

- By geography, the United Kingdom contributed 26.8% of 2025 revenue, yet Germany is poised to post the highest national growth at a 13.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flexible Office Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flight-to-quality toward Grade-A, ESG-compliant flex offices | +2.1% | UK, Germany, France, Nordic region | Long term (≥4 years) |

| Mandatory 3-to-4-day office policies sustain hybrid flex-space demand | +1.8% | UK, Germany, France, Benelux | Medium term (2-4 years) |

| Corporate decarbonization & EU Taxonomy accelerate retrofit flex hubs | +1.5% | EU-27, notably Germany, France, Netherlands | Long term (≥4 years) |

| Green-linked loans unlock refinancing of distressed assets into flex space | +1.2% | UK, France, Germany, Spain | Medium term (2-4 years) |

| AI-driven occupancy analytics lift revenue per workstation | +0.9% | UK, Germany, Nordic markets | Short term (≤2 years) |

| Private 5G neutral-host roll-out lowers IT barriers for satellite flex offices | +0.7% | Germany, UK, France, CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flight-to-Quality Toward Grade-A, ESG-Compliant Flex Offices

Occupiers are trading up to buildings that deliver verifiable environmental performance, widening the rent premium for certified space to 15–20% over secondary stock in 2025. EU Corporate Sustainability Reporting Directive rules compel disclosure of Scope 3 emissions from leased real estate, making uncertified space a reputational liability. Operators such as IWG and The Office Group publish granular carbon-intensity metrics and have portfolio-wide net-zero commitments. In turn, landlords favor revenue-share partnerships with flex brands that help de-risk stranded assets. This quality flight anchors price resilience for prime flex hubs even while incentives proliferate in lower-grade buildings.

Mandatory 3-to-4-Day Office Policies Sustain Hybrid Flex-Space Demand

Europe’s largest employers have converted temporary hybrid schedules into permanent policy. Vodafone requires eight office days per month, the European Central Bank has extended its hybrid framework through 2027, and Microsoft keeps a three-day rule for regional staff[2]Vodafone Group, “Hybrid Work Policy,” vodafone.com. Because daily attendance remains unpredictable, enterprises hedge by locking multi-year memberships that guarantee overflow capacity, ensuring stable occupancy for operators. Policy reversals such as Stellantis’s 2024 full-time return order underscore volatility, reinforcing flex space as insurance against mandate changes. Even with tech head-count reductions, desk-per-employee ratios are rising, supporting revenue growth. This structural shift explains why the Europe flexible office market continues expanding despite cyclical layoffs.

Corporate Decarbonization & EU Taxonomy Accelerate Retrofit Flex Hubs

The revised Energy Performance of Buildings Directive requires all non-residential stock to hit at least EPC class E by 2030 and class D by 2033, forcing deep energy retrofits across Europe. Flex operators sign long leases on discounted secondary offices, use green-debt proceeds to fund upgrades, and reopen as ESG-compliant hubs. HB Reavis secured USD 134 million of green financing in 2024, while Oxford Properties refinanced USD 198 million tied to carbon-intensity step-downs. Retrofits both extend asset life and unlock rental premiums, producing a two-speed market favoring owners with capital and technical know-how. Combined with tenant decarbonization pledges, regulation ensures long-run demand for compliant flex supply.

Green-Linked Loans Unlock Refinancing of Distressed Assets Into Flex Space

Sustainability-linked instruments reduce borrowing costs for retrofit projects. Barings, Ardian, and AXA IM collectively arranged more than USD 627 million of green financing for Manchester, Madrid, and Paris conversions during 2024. Loan margins fall once buildings hit certification milestones, aligning lenders and borrowers. Cheaper debt lets operators underwrite aggressive repositionings, importing high-quality supply into submarkets with double-digit vacancy. Because proceeds refinance stressed owners, the mechanism also mitigates systemic risk in bank loan books. As conventional refinancing remains expensive, the green-debt channel will keep accelerating flex conversions across the Europe flexible office industry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fit-out & M&E costs erode operator margins | –1.4% | UK, Germany, France, Nordic markets | Short term (≤2 years) |

| Vacant secondary offices undercut flex rents with incentives | –1.1% | Spain, Italy, peripheral EU markets | Medium term (2-4 years) |

| NIS2 / GDPR privacy scrutiny delays large-enterprise uptake of small brands | –0.8% | EU-27, notably Germany, France, Netherlands | Medium term (2-4 years) |

| Cross-border VAT gaps inflate TCO for multi-country occupiers | –0.6% | EU-wide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Fit-Out & M&E Costs Erode Operator Margins

Construction-cost inflation ran 8–12% annually in 2024–2025, lifting premium fit-out spend to USD 870–1,305 per m². Advanced HVAC controls, LED lighting, and smart-building sensors demanded by EU Taxonomy compliance add another 15–20% to budgets. Because new sites often take 18–24 months to reach break-even, capital-constrained operators risk prolonged cash burn. Smaller brands lacking bulk-purchase agreements or in-house engineering are most exposed, pushing them toward lower-value freelancer niches and away from enterprise contracts.

Vacant Secondary Offices Undercut Flex Rents With Incentives

Office vacancy in Europe’s secondary stock exceeds 12% in many cities, prompting landlords to offer 12–18-month rent-free periods and generous tenant-improvement allowances. For needs above 50 desks, conventional leases can run 20–30% cheaper than co-working memberships once incentives are capitalized. Flex operators must either accept lower utilization or double down on prime, ESG-certified buildings where landlord competition is muted. The pricing squeeze limits geographic diversification and caps addressable demand in cost-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serviced Suites Gain on Privacy Demands

Co-working spaces captured 51.22% of Europe flexible office market revenue in 2025, underscoring their appeal to freelancers and creative agencies that prize collaboration. Serviced offices and executive suites, however, are forecast to grow at a 12.1% CAGR to 2031, outpacing overall Europe flexible office market size expansion as banks and consulting firms prioritize data security. The serviced segment’s rise mirrors NIS2 compliance pressure; enclosed layouts with dedicated HVAC, lockable access, and private server racks command 30–40% pricing premiums[3]. Operators respond with hybrid products that combine private suites and shared lounges, balancing confidentiality with community.

Continued flight-to-quality strengthens serviced-suite demand. IWG, for example, pre-leased 250,000 m² of new ESG-certified space across Germany, France, and Spain under a 2025 alliance with Allianz Real Estate. Meanwhile, modular fit-out systems cut build times to eight weeks, reducing capital cycles and de-risking expansion. Co-working’s share remains large but is edging lower as enterprise occupiers reshape the Europe flexible office market share mix in favor of privacy-first formats.

By Sector: BFSI Overtakes IT Growth Trajectory

Information technology and IT-enabled services accounted for 32.11% of demand in 2025, reflecting tech’s early adoption of remote work and clustering in London, Berlin, and Stockholm. Yet layoffs at Meta and Amazon, which shed European office footprints in 2024–2025, temper growth. Banking, financial services, and insurance is projected to expand at an 11.98% CAGR through 2031, the fastest pace among sectors, as Basel III rules make off-balance-sheet occupancy attractive. Secure project rooms and data-residency guarantees align serviced-suite features with BFSI compliance needs, lifting the segment’s Europe flexible office market size contribution.

Consulting and professional-services firms maintain steady mid-single-digit growth, using flex hubs for client teams in secondary cities. Life sciences startups locate near biotech clusters such as Cambridge and Basel, demanding wet-lab-adjacent offices that few operators can supply, thereby opening niche opportunities. Overall, sector diversification insulates the Europe flexible office industry against single-segment downturns and supports sustained absorption across cycles.

By End Use: Freelancers Accelerate Fastest

Enterprises represented 46.4% of end-use demand in 2025, benefiting from volume discounts and priority booking for peak days. However, freelancers should climb at a 12.55% CAGR between 2026 and 2031, buoyed by France’s 2024 auto-entrepreneur tax reforms and Germany’s portable-pension scheme. These policies reduce financial risk for independents, encouraging them to swap home offices for professional desks. Operators cater with lower-commitment passes, community events, and price-sensitive packages.

Startups and non-profits form the residual group, growing roughly in line with the overall Europe flexible office market. Scale-ups value capital-light occupancy that spares equity for product development, while non-profits appreciate the ability to scale desks rapidly for project funding cycles. This bifurcation forces operators to segment offerings: Regus addresses enterprise needs, whereas Spaces targets freelancers, illustrating brand stratification within portfolios

Geography Analysis

Germany is forecast to register a 13.01% CAGR through 2031, the fastest rate among major European markets. Federal Mittelstand incentives and zoning reforms in Berlin and Munich have cut permitting times for conversions to nine months, accelerating the supply of Grade-A flex hubs. Strong apprenticeship programs feed skilled labor into R&D centers, spawning demand for short-tenure project rooms that match flex economics. Accounting rules classify memberships as service contracts, giving CFOs balance-sheet flexibility and reinforcing adoption among manufacturing exporters that increasingly operate hub-and-spoke models.

The United Kingdom retained a 26.8% share in 2025, anchored by London’s concentration of financial and legal services. Brexit-driven supply-chain friction raised fit-out costs by roughly 10–15%, nudging occupiers toward regional cities like Manchester and Edinburgh, where cost-per-desk is up to 50% lower. IFRS 16 still treats sub-12-month memberships as operating expenses, preserving off-balance-sheet appeal for corporate users. As green-loan capital floods retrofit projects, high-spec London assets sustain premium pricing, whereas secondary stock faces persistent vacancy pressures.

France, Spain, Italy, and the rest of Europe round out the regional landscape. Paris and Lyon dominate French supply; tax simplification for freelancers is expected to lift demand for smaller-format memberships. Spain’s recovery centers on Madrid and Barcelona, aided by near-shore outsourcing that values bilingual talent pools. Italy remains fragmented but is benefiting from fiber-infrastructure upgrades and startup incentives in Milan and Turin. Nordic markets command premium rents for ESG-certified space, while Central and Eastern Europe offers cost arbitrage but wrestles with infrastructure gaps. EU-wide retrofit mandates synchronize supply upgrades, elevating energy performance and sustainability as decisive tenant criteria.

Competitive Landscape

Enterprise clients gravitate toward brands that deliver ISO 27001 credentials and unified service-level agreements across borders, raising switching costs and concentrating demand at the top. IWG’s 2025 partnership with Allianz Real Estate will add 250,000 m² of space, all targeting BREEAM Excellent certification, further solidifying its enterprise moat.

Strategic maneuvers emphasize balance-sheet flexibility. WeWork shed USD 4 billion of debt in its 2025 restructuring, exited 170 under-performing sites, and secured USD 450 million for technology upgrades, allowing it to refocus on high-margin European hubs. The Office Group raised USD 253 million from Blackstone in late 2024 to fund ESG-aligned retrofits and integrate proprietary occupancy analytics, signaling investor appetite for tech-enabled operators.

Technology and partnerships are emerging differentiators. Operators deploy AI analytics to price desks dynamically and partner with telecom carriers for private 5G, as seen in Huckletree’s Paddington flagship using BT connectivity. Modular construction trims fit-out times, letting challengers capture opportunities in secondary cities before incumbents mobilize. Aggregator platforms like Deskpass threaten to commoditize desk supply, pushing brands to deepen service bundles—wellness programs, curated events, and data-driven facilities management—to preserve pricing power.

Europe Flexible Office Industry Leaders

Regus Group Companies

WeWork

The Office Group

Mindspace

Wojo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Great Portland Estates confirmed that the 28,700 sq ft first phase of its Fully Managed conversion at City Tower, London EC2, is now 100% let or under offer, securing USD 5.3 million in annual rent and launching the 19,900 sq ft second phase for March 2026.

- January 2026: IWG agreed deals for more than 60,000 sq ft of new UK space, including openings at Elizabeth House in Bolton and 39 Fitzroy Square in London, to meet rising provincial demand for hybrid work solutions.

- October 2025: Orega signed a management agreement with Brookfield Properties to deliver a 23,252 sq ft BREEAM Excellent flexible workspace at CityPoint, London EC2, scheduled to open in spring 2026.

- October 2025: Swedish operator Ioffice acquired United Spaces from Castellum, creating the country’s largest flexible-workspace group with 67,500 sq m across 20 locations.

Europe Flexible Office Market Report Scope

A flexible office is a workspace that provides employees with various places and ways to work. Unlike traditional offices with fixed and assigned desk positions, workers in a flexible office space can choose the office area that best suits the type of work they need to do.

The European flexible office market is segmented by type (private offices, coworking spaces, and virtual offices), end user (IT and telecommunications, media and entertainment, and retail and consumer goods), and geography (Germany, the United Kingdom, France, and the Rest of Europe). The report offers market size and forecasts in values (USD) for all the above segments.

By Type

| Co-Working Space |

| Serviced Offices / Executive Suites |

| Others (Hybrid, Virtual Office) |

By Sector

| Information Technology (IT & ITES) |

| BFSI (Banking, Financial Services & Insurance) |

| Business Consulting & Professional Services |

| Other Services (Retail, Life-Sciences, Energy, Legal) |

By End Use

| Freelancers |

| Enterprises |

| Start-Ups & Others |

By Country

| Germany |

| France |

| UK |

| Spain |

| Italy |

| Rest of Europe |

| By Type | Co-Working Space |

| Serviced Offices / Executive Suites | |

| Others (Hybrid, Virtual Office) | |

| By Sector | Information Technology (IT & ITES) |

| BFSI (Banking, Financial Services & Insurance) | |

| Business Consulting & Professional Services | |

| Other Services (Retail, Life-Sciences, Energy, Legal) | |

| By End Use | Freelancers |

| Enterprises | |

| Start-Ups & Others | |

| By Country | Germany |

| France | |

| UK | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How large will Europe’s flexible office space sector become by 2031?

The market is projected to reach USD 22.60 billion by 2031, expanding from USD 14.88 billion in 2026 at an 11.21% CAGR.

Which product type is growing fastest within flexible offices?

Serviced offices and executive suites are forecast to rise at a 12.1% CAGR through 2031 as banks and consultants demand privacy-centric layouts.

Why is Germany the fastest-growing national market?

Federal Mittelstand incentives, streamlined zoning for conversions, and robust hybrid-work norms support a 13.01% CAGR for German flexible offices.

How are sustainability rules influencing the sector?

EU Taxonomy and the Energy Performance of Buildings Directive push landlords to retrofit aging stock, channeling green-loan capital into ESG-certified flex hubs that earn rental premiums.

What technologies are improving operator economics?

AI-driven occupancy analytics cut vacancy drag by up to 15 percentage points, while private 5G slices deliver enterprise-grade connectivity without costly fiber builds.

Who holds the largest share of the European flexible office arena?

IWG remains the market leader, and together with WeWork, The Office Group, Mindspace, and Wojo, the top five operators account for roughly 35–40% of regional revenue.

Page last updated on: