Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

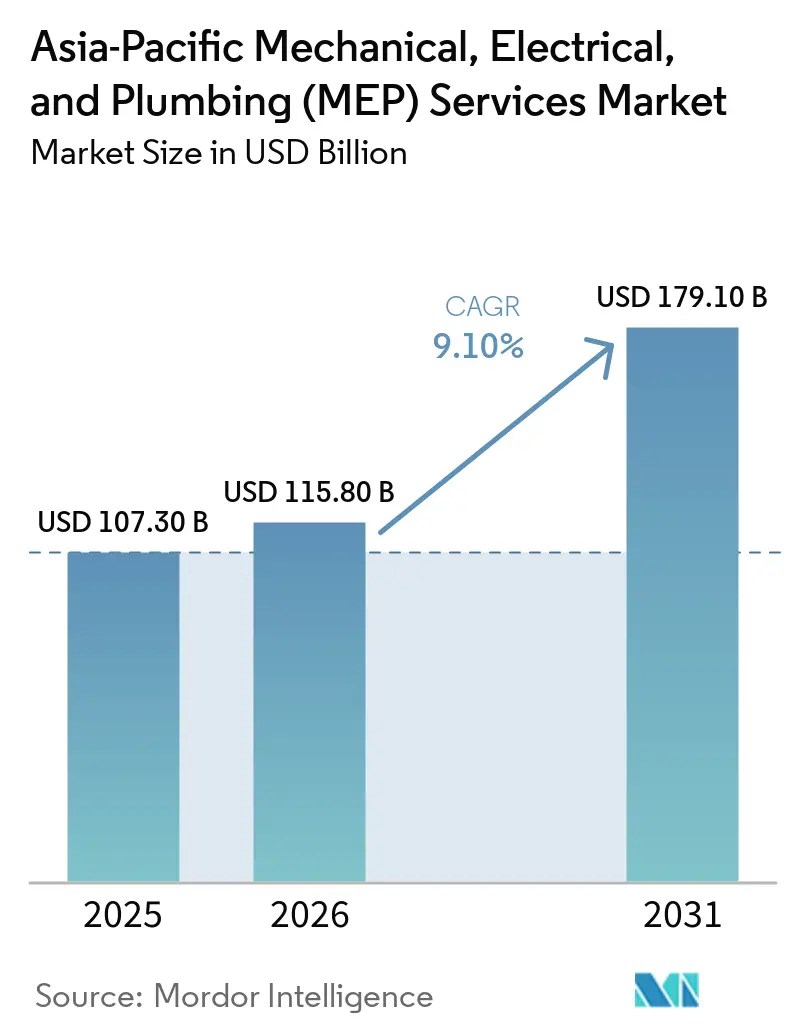

| Base Year Market Size (2025) | USD 107.30 Billion |

| Market Size (2026) | USD 115.80 Billion |

| Market Size (2031) | USD 179.10 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The Asia-Pacific Mechanical, Electrical, And Plumbing Services Market size is projected to be USD 107.30 billion in 2025, USD 115.80 billion in 2026, and reach USD 179.10 billion by 2031, growing at a CAGR of 9.10% from 2026 to 2031. The rise in 2026 reflects overlapping infrastructure cycles across the region’s largest economies, which is keeping project flow active across transport, industrial, commercial, and retrofit work. China remains the largest country market, but its demand mix is changing as residential construction slows and higher-specification industrial and data-centered work gains weight. India, Australia, South Korea, Indonesia, Japan, and Vietnam are each expanding for different reasons, which means firms cannot scale regionally with a single-country operating model. Developers are also shifting toward single-package delivery on complex facilities, which supports faster adoption of integrated scopes across the Asia-Pacific MEP services market. Competition remains layered between global engineering groups and regional specialists, and rising cost pressure is pushing more companies toward joint ventures, capability acquisitions, and tighter project selection.

Key Report Takeaways

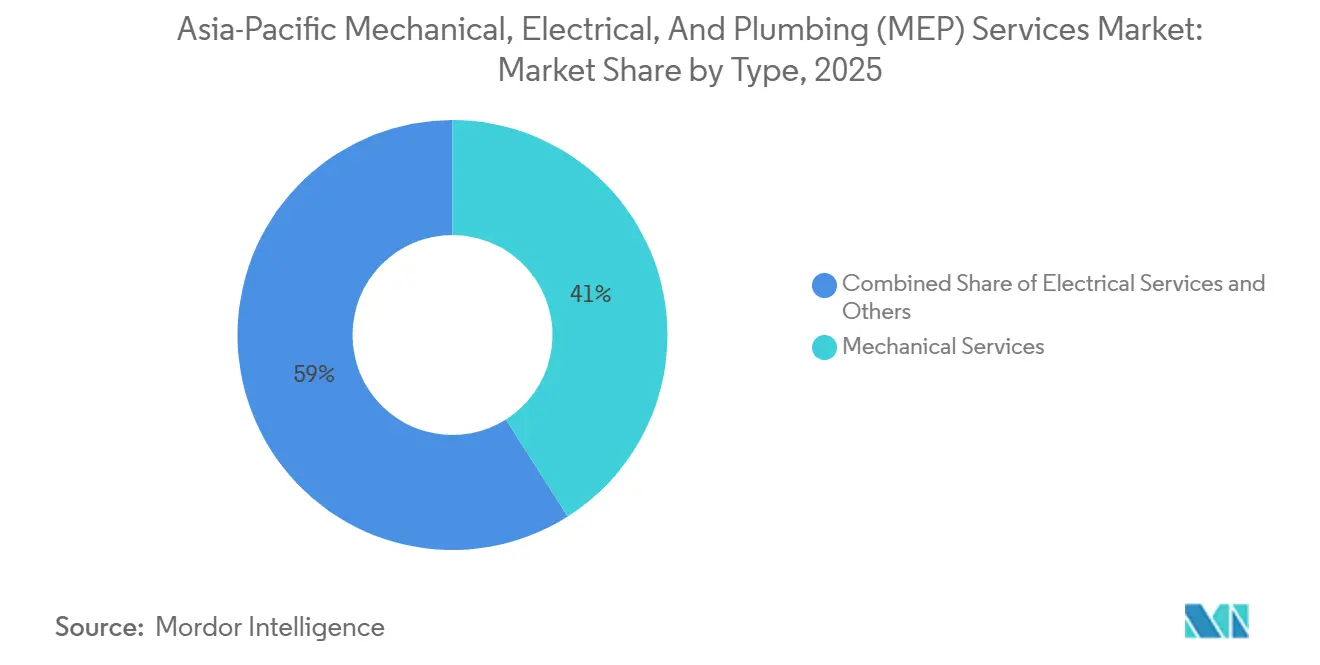

- By type, mechanical services led with 41% revenue share in 2025, while integrated MEP services is forecast to expand at 11.65% CAGR through 2031.

- By service type, maintenance, repair, and retrofit held 37.8% share of the Asia-Pacific MEP services market size in 2025, while managed or performance-based Services recorded the highest projected CAGR at 10.56% through 2031.

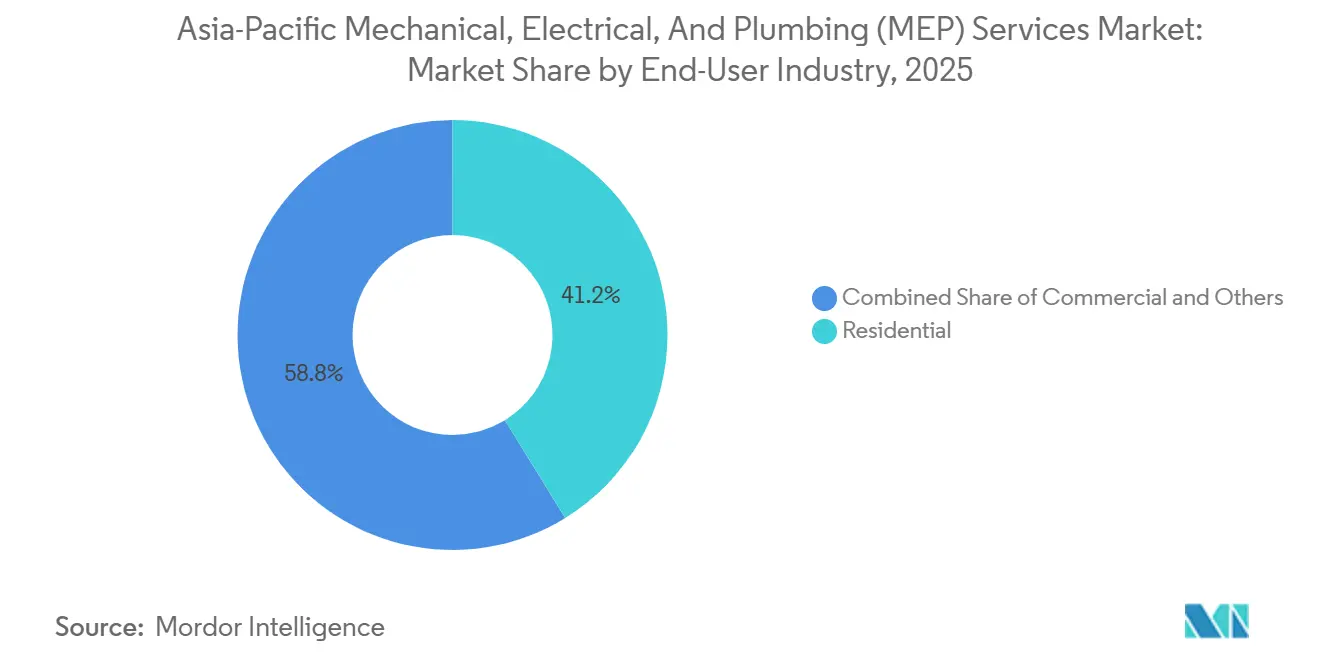

- By end-user industry, residential held 41.22% of Asia-Pacific MEP services market share in 2025, while commercial is projected to grow at 12.19% CAGR through 2031.

- By geography, China accounted for 32.45% revenue share in 2025, while Vietnam is forecast to expand at 11.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transit-Led Urban Megaproject Spending | +2.2% | APAC-wide, concentrated in Australia, Vietnam, Thailand, and India | Medium term (2-4 years) |

| Data-Center and Semiconductor Facility Build-Out | +1.8% | Malaysia, Indonesia, India, Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Green-Building and Refrigerant Compliance Tightening | +1.4% | Australia, Singapore, China, Taiwan, with spillover to ASEAN | Short term (≤ 2 years) |

| Industrial Relocation into ASEAN and India | +1.1% | Vietnam, Indonesia, India, Thailand, and Malaysia | Medium term (2-4 years) |

| Public-Project BIM Mandates and Prefab MEP Adoption | +0.7% | Singapore, Malaysia, Hong Kong, Australia, and South Korea | Medium term (2-4 years) |

| District Cooling and Heat-Pump Retrofit Acceleration | +0.6% | Singapore, India, Thailand, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transit-Led Urban Megaproject Spending

Government infrastructure pipelines continue to support the Asia-Pacific MEP services market, even as private construction cycles lose momentum. Vietnam approved the Lao Cai to Hanoi to Hai Phong standard-gauge railway in 2025, and the project includes 174 bridges and 55 tunnels that will require tunnel ventilation, fire-life-safety, traction power, and related systems during delivery[1]Vietnam.vn, “Lao Cai Hanoi Hai Phong Railway Project, Investment of 200,000 Billion VND and Roadmap to 2030,” Vietnam.vn, vietnam.vn . Large transit packages also favor contractors that can coordinate multiple systems within one scope instead of splitting the work trade by trade. That supports firms with railway-grade certifications, linewide systems experience, and proven commissioning depth, especially in parts of ASEAN where that talent pool remains limited. The result is that public transport spending continues to create high-value opportunities in the Asia-Pacific MEP services market across Australia, Vietnam, Thailand, and India.

Data-Center and Semiconductor Facility Build-Out

Mission-critical facilities remain one of the clearest growth pockets in the Asia-Pacific MEP services market. AI-ready data centers require denser power, cooling, backup, and control architectures than legacy server rooms, so contractors must redesign entire service layouts rather than repeating standard office MEP templates. Johnson Controls committed up to USD 60 million over 5 years in 2026 to expand its Singapore Innovation Center, with the site focused on advanced cooling and thermal management to meet regional data center demand. Semiconductor projects add a parallel stream because cleanroom HVAC, ultra-pure water plumbing, and high-availability electrical systems require tighter performance standards than ordinary commercial buildings. ASEAN investment reporting also highlighted major manufacturing projects, including TSMC’s USD 4.3 billion Singapore fab, Infineon’s USD 5.4 billion Malaysian silicon carbide expansion, and United Microelectronics’ USD 5 billion Singapore facility. This is pushing the Asia-Pacific MEP services market toward more specialized engineering, tighter commissioning, and stronger integrated delivery capability.

Green-Building and Refrigerant Compliance Tightening

Compliance rules are steadily turning building upgrades into a direct growth engine for the Asia-Pacific MEP services market. China’s 2025 to 2030 implementation plan under the Montreal Protocol and Kigali Amendment bans household refrigerators and freezers using HFCs from 2026 and will require room air-conditioner refrigerants with GWP below 750 from 2029. Singapore’s amended Building Control Act also pushes owners toward energy retrofits, with mandatory improvement plans targeting at least a 10% reduction in energy use intensity, and chiller replacement standing out as a major compliance route. These requirements expand the project scope because lower-GWP cooling systems and energy upgrades often trigger electrical, controls, and balance-of-plant work simultaneously. That raises retrofit value per site and supports higher-specification contract work across the Asia-Pacific MEP services market.

Industrial Relocation into ASEAN and India

Industrial relocation is broadening the demand base for Asia-Pacific MEP services beyond urban building construction. Manufacturing FDI into ASEAN reached USD 226 billion in 2024, with electronics and electrical equipment greenfield projects accounting for USD 31 billion, underscoring the scale of the current factory investment cycle. Every new plant requires power distribution, compressed air, process cooling, water systems, and fire protection, often requiring compliance with multinational operating standards. That is encouraging developers and occupiers to award more integrated packages, especially when facilities need tight scheduling and a rapid production ramp-up after handover. Vietnam stands out in the Asia-Pacific MEP services market because manufacturing FDI reached USD 20 billion in 2024, which is sustaining a dense pipeline of factory MEP work across its industrial zones

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Trade Shortages and Wage Inflation | -1.5% | Australia, New Zealand, Singapore, with spillover to India and ASEAN | Short term (≤ 2 years) |

| Copper, Switchgear, and HVAC Component Volatility | -1.3% | Global supply chain, acute in APAC project markets | Short term (≤ 2 years) |

| Cross-Border Code Fragmentation and Local-Content Rules | -0.6% | ASEAN including Indonesia, Vietnam, and Thailand, plus India | Long term (≥ 4 years) |

| Utility-Connection Bottlenecks for Mission-Critical Projects | -0.5% | Core APAC markets including Singapore, Japan, Australia, and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Trade Shortages and Wage Inflation

Labor availability remains one of the clearest delivery limits in the Asia-Pacific MEP services market. Electrical installers, HVAC technicians, plumbing crews, and fire-protection specialists are difficult to secure in the region’s busiest hubs, especially when transport, energy, industrial, and building programs move forward at the same time. Tight labor conditions raise wage bills, increase overtime exposure, and push contractors to rely more heavily on imported labor or specialist subcontract crews. The larger problem is contract timing because many jobs are priced well before site execution begins. That mismatch can turn fixed-price work into margin loss and it slows capacity expansion across the Asia-Pacific MEP services market even when demand conditions are strong.

Copper, Switchgear, and HVAC Component Volatility

Material price swings continue to undermine bid certainty in the Asia-Pacific MEP services market. Copper, switchgear, transformers, and HVAC components all carry procurement risk that remains more disruptive than in earlier project cycles. Long delivery windows on electrical equipment can delay installation sequencing across multiple trades, which is especially difficult on data centers, industrial plants, and large infrastructure sites. Contractors are responding by shortening bid validity periods and inserting escalation mechanisms for major material categories wherever clients allow them. That shifts a greater share of commodity risk back to project owners and makes tender comparison less straightforward. The result is a more defensive contracting environment in the Asia-Pacific MEP services market, particularly for fixed-price packages with long delivery schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Services Anchored by Cooling Demand, Integrated Contracts Gain Share

Mechanical Services held 41% of Asia-Pacific MEP services market share in 2025, which kept cooling and ventilation work at the center of regional project spend. Demand remains strongest in dense urban markets where HVAC, chilled-water loops, and district cooling systems account for a large share of installed building value. Mechanical scope also stays central to compliance because energy retrofits usually begin with chillers, pumps, air-side systems, and controls rather than with cosmetic upgrades. Electrical Services and Plumbing Services followed as the next-largest categories, both supported by data centers, industrial facilities, and high-rise projects that require reliable power and water systems.

Integrated MEP Services is projected to grow at 11.65% CAGR within the Asia-Pacific MEP services market size mix through 2031 as developers shift toward single-package awards on complex facilities. This reflects concern over coordination risk, rework, and schedule slippage when multiple trade contractors operate under separate scopes. In the Asia-Pacific MEP services industry, firms with BIM capability, clash detection, and full-cycle execution are gaining ground on companies that supply only one trade. That advantage is strongest on transit systems, data centers, and semiconductor facilities, where service density is great and late-stage changes are expensive. The Asia-Pacific MEP services market is therefore moving toward fewer interfaces and larger integrated mandates, even though mechanical, electrical, and plumbing specialization still matter within the final package.

By Service Type: Retrofit Base Outweighs New Build, Performance Contracts Redefine Value

Maintenance, Repair, and Retrofit accounted for 37.8% share of the Asia-Pacific MEP services market size in 2025, reflecting the region’s large installed asset base and the rising importance of brownfield upgrades. Owners are no longer limiting retrofit work to isolated equipment replacement because energy costs and compliance deadlines are pushing them toward whole-system improvements. Chiller replacement, building management system upgrades, and lighting plus controls integration now appear together more often in the same program. Singapore’s Tampines district cooling retrofit shows the scale of this shift, with 7 existing buildings connected through a closed-loop system that saves more than 2,300,000 kWh per year[2]SP Group Asia, “Tampines Town Cooling,” SP Group Asia, spgroup-asia.com.

Managed or Performance-based Services is forecast to expand at 10.56% CAGR through 2031, making it the fastest-growing service model in the Asia-Pacific MEP services market. This approach links contractor value to uptime, energy use, or lifecycle outcomes rather than only to labor hours and material inputs. In the Asia-Pacific MEP services industry, that model is gaining traction in facilities where downtime costs are high, especially hospitals and mission-critical commercial assets. Building owners increasingly prefer service partners that can install, monitor, optimize, and stand behind measurable results after handover. That is why the Asia-Pacific MEP services market is assigning more value to long-duration service relationships than to one-time transactional maintenance work alone.

By End-User Industry: Residential Breadth Meets Commercial Intensity

Residential held 41.22% share in 2025, giving it the largest end-user position in the Asia-Pacific MEP services market. That breadth came from affordable housing activity in large population centers and from continued high-rise development in dense urban locations. Residential work still favors repeatable volume across plumbing, electrical, ventilation, and building services support systems, even though average contract values are lower than on mission-critical facilities. Infrastructure remained another important demand base, with stations, airports, public buildings, and utility-linked assets carrying high technical complexity despite lower project counts.

Commercial is set to grow at 12.19% CAGR through 2031, which makes it the fastest-growing end-user group in the Asia-Pacific MEP services market. Data centers, semiconductor fabs, and green-certified offices are driving this shift because they need tighter thermal control, cleaner power, and deeper commissioning than standard buildings. Singapore’s Green Mark framework for data centers shows how power efficiency, cooling efficiency, water use, and responsible refrigerant management are becoming a formal compliance package for commercial projects. In the Asia-Pacific MEP services industry, this is extending contractor involvement beyond installation because clients increasingly want post-occupancy verification and sustained operating performance. The result is a commercial pipeline that is smaller in project count than housing, but richer in engineering content and service intensity.

Geography Analysis

China held 32.45% of Asia-Pacific MEP services market share in 2025, which kept it in the lead despite a weaker residential backdrop. Demand is shifting from housing-linked work toward retrofit, industrial, and higher-specification commercial assets, which changes the contractor mix best placed to grow there. China’s 2025 to 2030 implementation plan under the Kigali Amendment is also accelerating replacement demand in cooling systems that no longer meet refrigerant rules. Siemens stated in its FY2025 reporting that China’s real estate crisis and construction-sector correction weighed on its Smart Infrastructure business, which supports the view that residential and ordinary commercial demand has softened. India remains one of the most important expansion markets in the Asia-Pacific MEP services market, and Siemens also identified India as a standout market within its Asia-Australia cluster, which aligns with the country’s strong infrastructure and building activity.

Vietnam is projected to grow at a 11.01% CAGR through 2031, giving it the fastest national growth rate in the Asia-Pacific MEP services market. Manufacturing FDI reached USD 20 billion in Vietnam in 2024, and this inflow is translating into strong MEP demand across major industrial provinces.Indonesia is following a similar path because manufacturing investment and data-centered activity are expanding at the same time, which strengthens demand for power, cooling, and fire-safety systems. Australia and South Korea are more mature markets, but both remain important because compliance standards, large public projects, and the rising use of modular assemblies support higher-value work. These conditions mean regional firms cannot rely on a single-country template if they want scale in the Asia-Pacific MEP services market.

Japan remains a major developed market within the Asia-Pacific MEP services market because strict energy-efficiency rules and large mission-critical facilities keep technical thresholds high. The country continues to attract MEP-intensive investment in data centers and advanced facilities, which supports long-cycle demand for electrical resilience, cooling, and controls integration. Across the wider region, differences in licensing, procurement rules, labor availability, and project mix keep expansion strategies highly local. That is why firms that pair regional client coverage with domestic execution capability are better placed to capture growth across the Asia-Pacific MEP services market.

Competitive Landscape

The Asia-Pacific MEP services market is moderately fragmented at the top and highly fragmented across the mid-tier. Global firms such as AECOM, WSP Global, Jacobs, and Fluor compete on digital design capability, cross-border delivery, and their ability to staff large multi-discipline packages. Regional specialists including Larsen & Toubro Construction, Voltas Limited, Shinryo Corporation, and Kinden Corporation compete differently, using domestic licensing, local procurement, and state-linked client relationships to defend position. Thousands of firms below USD 500 million in MEP revenue keep pricing competitive in standard project categories, even as specialized work commands better margins.

Strategic moves in the Asia-Pacific MEP services market are increasingly centered on capability depth rather than simple scale. Johnson Controls expanded its Singapore Innovation Centre in 2026 with an investment of up to USD 60 million, showing how suppliers are adding regional cooling and thermal-management capability close to demand growth.

SP Group was appointed in 2026 to design, build, and operate a distributed district cooling system for Singapore’s HarbourFront Precinct, which shows how service delivery and energy infrastructure are converging in brownfield precinct projects[3]District Energy, “SP Group to Build Distributed District Cooling System in HarbourFront Precinct,” District Energy, districtenergy.org. Voltas reported that its Electro-Mechanical Projects and Services segment generated INR 4,157 crore (USD 499 million) in FY2025 and returned to profit after tighter project selection and better working capital management. These moves show that firms are combining technology, execution discipline, and lifecycle service capability rather than competing on installation volume alone.

The Asia-Pacific MEP services market is also moving toward more joint ventures, selective acquisitions, and performance-based contracts as companies respond to cost volatility and tighter coordination demands. Larger firms hold an advantage when clients want integrated packages with BIM support, commissioning depth, and service commitments after handover. Smaller contractors can still win in domestic niches, but they face more pressure when copper, switchgear, and specialist labor costs move sharply and clients transfer those risks down the chain. Consolidation is therefore most likely to continue in complex project categories where technical credentials and balance-sheet strength matter more than the lowest initial bid.

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

AECOM

WSP Global

Jacobs

Fluor Corporation

Johnson Controls

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Johnson Controls announced an investment of up to USD 60 million over five years to expand its Singapore Innovation Center, adding 90-100 engineering roles focused on thermal management and advanced cooling solutions for the region's data-center sector, with Singapore's data centers projected to rise from 7% to 12% of national energy consumption by 2030.

- January 2026: SP Group was appointed by Mapletree Investments and MPACT to design, build, and operate a distributed district cooling system for Singapore's HarbourFront Precinct, connecting 5 buildings including VivoCity, in one of Singapore's largest brownfield MEP cooling deployments.

- March 2025: SP Group launched the Tampines Town distributed district cooling network in Singapore, the world's first large-scale brownfield distributed cooling system retrofitted across 7 existing commercial buildings, projecting carbon savings of 1,000 tonnes per year and SGD 50.8 million in lifecycle economic benefits for building owners.

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The Asia-Pacific MEP Services Report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair, Others), End-User Industry (Residential, Commercial, Infrastructure), and Geography (China, India, Japan, South Korea, Australia, Indonesia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance & Repair |

| Managed / Performance-based Services |

| Residential |

| Commercial |

| Infrastructure |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Rest of Asia-Pacific |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance & Repair | |

| Managed / Performance-based Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current outlook for Asia-Pacific MEP services through 2031?

The Asia-Pacific MEP services market stands at USD 115.8 billion in 2026 and is expected to reach USD 179.1 billion by 2031 at a 9.1% CAGR over 2026-2031.

Which service category contributes the most revenue in this space?

Maintenance, Repair, and Retrofit leads service type demand with a 37.8% share in 2025, supported by the region’s large installed building base and rising retrofit requirements.

Which end-user group is growing the fastest across Asia-Pacific MEP services?

Commercial is the fastest-growing end-user segment with a 12.19% CAGR through 2031, driven by data centers, semiconductor facilities, and green-certified office upgrades.

Why are integrated contracts gaining traction in large projects?

Integrated MEP Services is projected to grow at 11.65% CAGR through 2031 because developers want fewer coordination gaps and tighter control on complex transit, industrial, and mission-critical projects.

Page last updated on: