Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

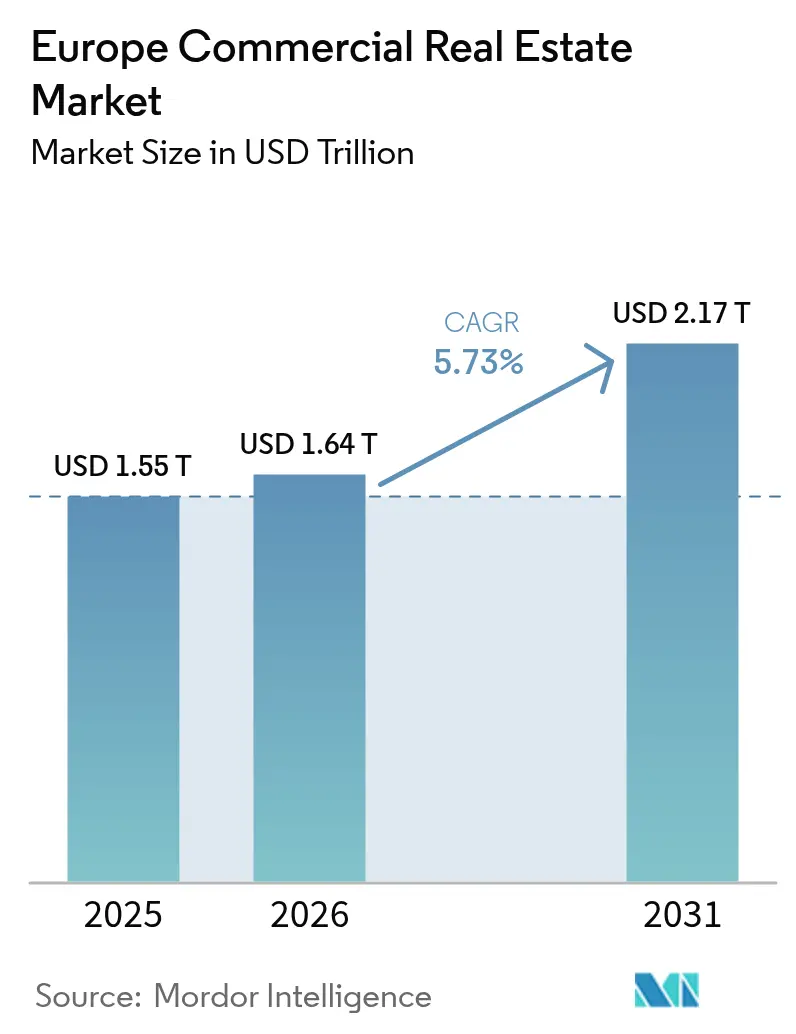

| Base Year Market Size (2025) | USD 1.55 Trillion |

| Market Size (2026) | USD 1.64 Trillion |

| Market Size (2031) | USD 2.17 Trillion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

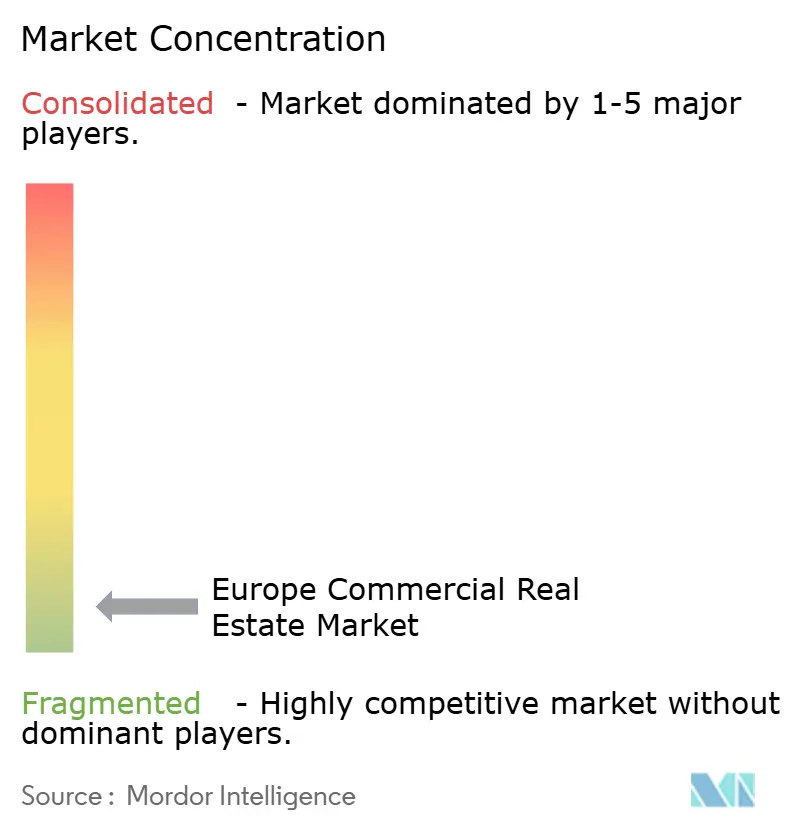

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Commercial Real Estate Market Analysis by Mordor Intelligence

The European commercial real estate market size is expected to grow from USD 1.55 trillion in 2025 to USD 1.64 trillion in 2026 and is forecast to reach USD 2.17 trillion by 2031 at 5.73% CAGR over 2026-2031. A 25% rebound in transaction volumes to EUR 213 billion in 2025 signals renewed confidence, spurred by the European Central Bank’s rate reductions and improving financing conditions [1].Christine Lagarde, “ECB Monetary Policy Decisions – 11 April 2025,” European Central Bank, ecb.europa.eu Capital is gravitating toward Grade-A logistics facilities and green-certified offices, while mixed-use “living-as-a-service” projects gain traction for their resilience and alignment with new urban lifestyles. Regional performance is increasingly polarized: the United Kingdom retains scale leadership, Central and Eastern Europe accelerate on near-shoring demand, and Southern Europe leverages special-economic-zone incentives to attract fresh capital. Corporate net-zero mandates, demographic realignments, and evolving occupier preferences collectively sustain the growth outlook of the European commercial real estate market through 2030.

Key Report Takeaways

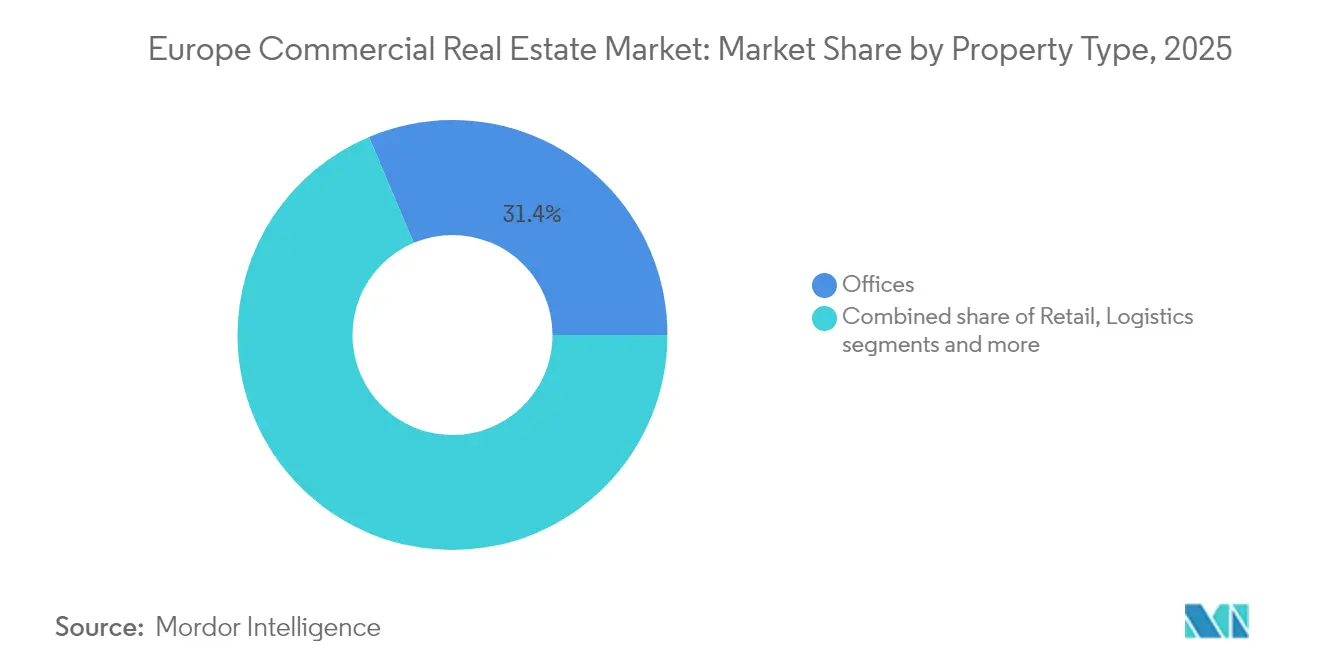

- By property type, offices held 31.35% of the European commercial real estate market share in 2025, while logistics assets are projected to expand at a 6.87% CAGR through 2031.

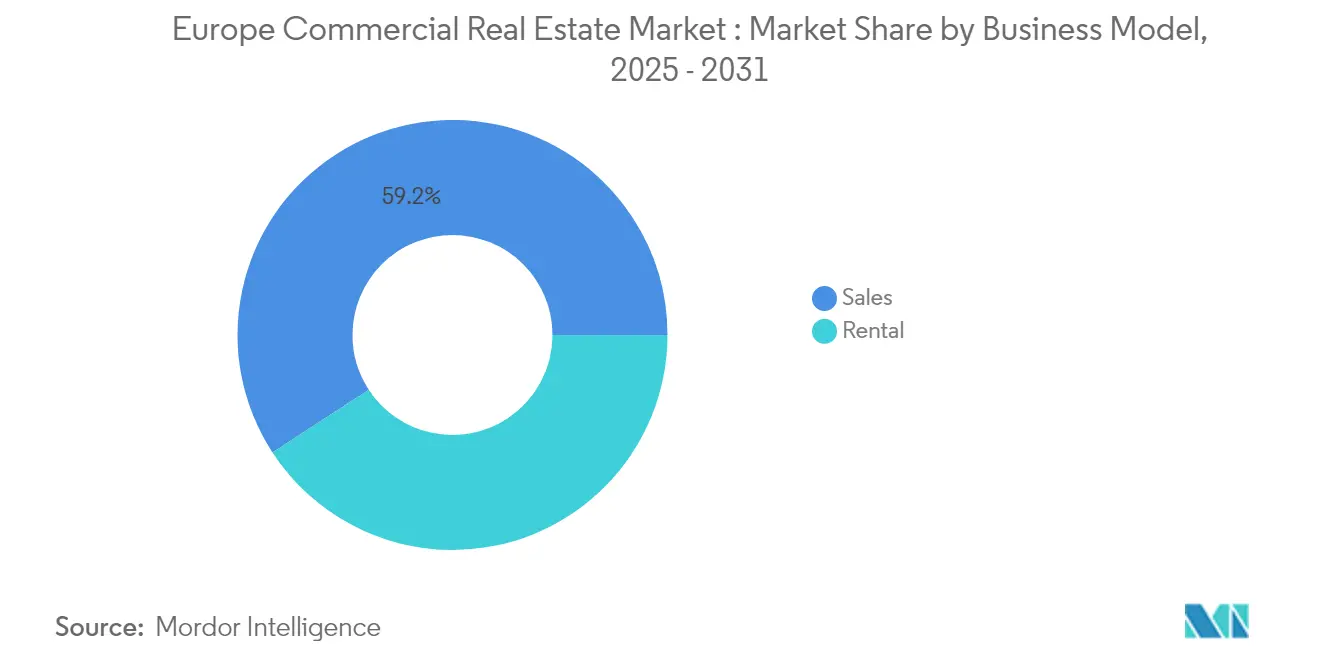

- By business model, the sales segment accounted for 59.20% of the European commercial real estate market size in 2025; the rental segment is advancing at a 6.01% CAGR between 2026-2031.

- By end-user, corporates and SMEs commanded 69.10% share of the European commercial real estate market size in 2025 and are growing at a 6.45% CAGR to 2031.

- By geography, the Germany led with 27.60% of European commercial real estate market share in 2025, while Poland is forecast to record the fastest 6.29% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Commercial Real Estate Market*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic-led urbanisation clusters | +1.1% | Germany, UK, spillover to Netherlands and France | Medium term (2-4 years) |

| Accelerated e-commerce demand for logistics assets | +1.9% | Pan-European, especially Poland, Netherlands, Germany | Short term (≤ 2 years) |

| Near-shoring and re-industrialisation in CEE | +1.6% | Poland, Czech Republic, Romania | Medium term (2-4 years) |

| Corporate net-zero mandates for Grade-A offices | +1.4% | UK, France, Germany, Netherlands | Medium term (2-4 years) |

| SEZ-linked tax incentives | +0.8% | Spain, Italy, Greece, Portugal | Long term (≥ 4 years) |

| Rise of living-as-a-service formats | +1.0% | Urban centres Europe-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic-led Urbanisation Clusters Reshaping Development Priorities

Secondary cities such as Manchester, Birmingham, Munich and Hamburg are absorbing population growth outpacing national averages, compressing office vacancy 2-3 percentage points below primary markets. Investment volumes in these German hubs grew 23% in 2024 as institutional capital seeks stable yields outside saturated capitals. Retail and mixed-use developments tailored to emerging live-work hubs dominate new pipelines, reflecting the European commercial real estate market’s shift toward decentralised growth nodes [2] Eurostat, “Population Change and Urbanisation Trends in the EU, 2024 Edition,” Eurostat, ec.europa.eu. Developers now prioritise flexible floor plates and community-oriented amenities that match the demographic profile of young, mobile workforces. The trend is expected to influence land-use planning, infrastructure spending and forward-funding structures over the medium term.

E-commerce Acceleration Transforms Logistics Landscape

Online retail penetration is projected to reach 25% of total European sales by 2030, intensifying demand for modern distribution centres along key corridors in Poland, the Netherlands and Germany. Urban logistics hubs within 30-minute drive times of major populations command 15-20% rent premiums and near 98% occupancy. Forward leasing often secures entire projects before completion, underscoring scarcity of scalable, automation-ready stock. Advanced picking and sorting systems are incorporated into 73% of new warehouses as operators chase fulfilment speed and lower cost-per-package. The European commercial real estate market is therefore seeing logistics yields compress faster than any other sector, setting new benchmarks for prime-grade performance.

Near-shoring Initiatives Fuel Industrial Real Estate Boom

Re-industrialisation programs channel an estimated EUR 4.7 trillion toward Central and Eastern Europe over the next three years, catalysing clusters around automotive, electronics and pharmaceuticals. In Poland alone, industrial take-up jumped 25% year-on-year in 2024 as manufacturers relocate capacity from Asia to mitigate geopolitical risk. Built-to-suit facilities with specialised power, floor loading and ESG credentials fetch premium rents, illustrating how supply-chain resilience is directly shaping the European commercial real estate market. Governments support the trend through tax incentives and streamlined permitting, creating positive spill-overs for local employment and transport infrastructure.

Corporate Sustainability Mandates Redefine Office Quality Standards

Between 80-85% of leasing in 2025 targets green-certified buildings, driving occupancy to 80-90% and rental premiums up to 25% for ESG-compliant stock. Western European occupiers consolidate into fewer but higher-spec spaces that feature renewable onsite power, advanced energy management and biophilic design. Non-compliant assets exhibit vacancy rates 7-10 points higher, accelerating obsolescence and discouraging debt financing. The European commercial real estate market therefore rewards owners who retrofit early, with green-bond frameworks and sustainability-linked loans emerging as preferred funding channels for redevelopment pipelines.

Restraints Impact Analysis of Europe Commercial Real Estate Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPC-class upgrade costs under EU Taxonomy | -1.2% | France, Germany, Netherlands | Medium term (2-4 years) |

| Financing volatility under tightening monetary policy | -0.8% | Pan-European, most acute in leveraged markets | Short term (≤ 2 years) |

| Geopolitical risk premium | -0.6% | Eastern Europe | Medium term (2-4 years) |

| Saturation of prime high-street retail | -0.5% | UK, France, Germany, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Costs Strain Investment Returns

EU energy-performance requirements oblige owners in Germany, France, Spain and Italy to spend EUR 165 billion on retrofits by 2024 or risk asset stranding over the next decade. Renovations can exceed 30% of asset value, discouraging upgrades in lower-grade stock and widening the valuation gap between prime and secondary holdings. Financing for heavy-capex assets is scarce, steering capital toward already compliant buildings and amplifying a two-tier market. As a consequence, the European commercial real estate market is seeing opportunistic funds target discounted secondary inventories for deep-green repositioning strategies that can unlock value post-compliance.

Financing Conditions Create Market Uncertainty

Although base rates have fallen, lending margins remain above pre-pandemic levels, compressing yields and forcing repricing, especially for value-add plays. About EUR 114 billion of European commercial real estate debt matures through 2027, exposing borrowers to refinancing spreads that could erode returns. Banks apply stricter covenants on office assets facing obsolescence, prompting equity top-ups or asset sales. Countercyclical buyers with access to corporate-bond or private-credit lines gain acquisition advantages, reinforcing the importance of capital agility in the European commercial real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Commercial Real Estate Market Segment Analysis

By Property Type:

Logistics Thrives Amid Supply Chain ReconfigurationOffices retained the largest share of 31.35% of 2025 revenue, but shifting work models and sustainability imperatives force owners to reposition portfolios. Prime CBD towers and adaptive-reuse campuses outperform, while legacy suburban stock falls into value-add or opportunistic territory. Retail is stabilising around experiential flagships that integrate digital-native concepts, registering 3.5% annual rental growth in top high-street districts. Meanwhile, data centres, life-science labs and hospitality are expanding faster than the broader European commercial real estate market, supported by AI workloads, demographic travel rebounds and specialised operator demand. Logistics assets are projected to clock the fastest 6.87% CAGR between 2026-2031, propelled by near-shoring, e-commerce and the need for resilient distribution networks. Occupancy for new-generation facilities stays close to 95% despite robust development pipelines, evidencing structural undersupply. Tenant demand emphasises automation readiness, ESG certification and proximity to multimodal nodes, attributes that allow landlords to pass through indexed rental escalations. In the European commercial real estate market size calculations, logistics’ incremental revenue contribution is set to outstrip offices through the forecast horizon.

By Business Model:

Rental Sector Evolves Beyond Traditional LeasingThe sales model, holding 59.20% of 2025 value, centres on prime income-producing assets sought by pension funds and sovereign investors chasing stable cash flows within the European commercial real estate market. Hybrid structures such as sale-leasebacks bridge both approaches, freeing corporate capital while preserving operational control. Rental-focused platforms are advancing at a 6.01% CAGR as occupiers favour flexibility and service-rich environments. Co-working, managed offices and turnkey logistics suites embed technology overlays that optimise space utilisation and cost predictability. Landlords increasingly differentiate through digital tenant-experience apps, predictive maintenance and ESG reporting dashboards. Growing demand for turnkey solutions compresses the performance gap between traditional leasing and service-oriented arrangements. Revenue models now blend base rent with ancillary service charges for connectivity, wellness and sustainability features, unlocking higher yield on cost. Capital-stack innovation—ranging from revenue-participating debt to green-performance-linked loans—provides owners with avenues to monetise these integrated offers and remain competitive within the evolving European commercial real estate market.

By End-user:

Corporates Drive Sustainable Building DemandCorporates and SMEs represented 69.10% of spending in 2025 and are forecast to expand at a 6.45% CAGR as real estate becomes a strategic lever for talent acquisition and brand signalling. Lease mandates increasingly reference carbon footprints, indoor-air-quality thresholds and smart-building certifications. Tier-one tenants are also signing longer green leases in productive knowledge hubs, reducing churn in prime portfolios across the European commercial real estate market. Technology firms and professional services anchor demand, though manufacturing and logistics occupiers now specify renewable-energy contracts and EV infrastructure as standard fit-out clauses. Residential demand from individuals grows steadily amid housing undersupply; institutional build-to-rent investors marshal scaled capital to deliver bulk housing portfolios. Public-sector entities support healthcare, education and civic infrastructure, often within public-private partnership frameworks that de-risk delivery. Across all end-user categories, digitisation accelerates predictive maintenance, energy optimisation and user-centric design, ensuring assets remain future-proof within the European commercial real estate market.

Geography Analysis

Germany Commercial Real Estate Market

Germany now captures 27.60% of European commercial real estate market share, reflecting its expansive core-asset inventory and deep domestic investor pool. Transaction volumes approached EUR 40 billion in 2024 as financing stabilised and international capital targeted Frankfurt, Munich and Berlin for their liquidity and robust occupier fundamentals. Logistics along the Rhine-Ruhr and Hanover-Berlin corridors saw record pre-lets, while Munich and Hamburg led office take-up in net-zero-ready developments. The German government’s energy-efficiency incentives accelerate retrofits, further enhancing value in compliant stock.

Poland Commercial Real Estate Market

Poland leads growth projections with a 6.29% CAGR to 2031, following EUR 5 billion of completed 2024 deals that doubled 2023 totals. Near-shoring manufacturers spurred build-to-suit demand across Wroclaw, Poznan and Lodz, while Warsaw CBD saw flight-to-quality leasing that tightened vacancy rates near historical lows. National infrastructure upgrades, including motorway expansions and new intermodal hubs, underpin sustained developer interest and validate Poland’s emergence as the most dynamic node in the European commercial real estate market.

Broader European Markets

France, the Netherlands, Spain and Italy round out the continental picture. Paris attracts luxury retail and prime office allocations amid constrained supply, contributing materially to pan-European core-plus strategies. The Netherlands logged 425,000 m² of logistics take-up in early 2025, with cold-chain facilities linked to Rotterdam’s port achieving record headline rents. Spain and Italy benefit from SEZ-driven incentives and tourism rebounds, energising retail park refurbishments and mixed-use coastal redevelopments that further diversify the European commercial real estate market.

Competitive Landscape

Competition is moderately fragmented, featuring global asset managers, region-specific investors and technology-enabled challengers. Consolidation rose 17% by deal value in 2024 as scale becomes essential for meeting EU taxonomy disclosure, accessing green finance and spreading retrofit costs. Institutional leaders concentrate on prime ESG-aligned portfolios, leaving value-add opportunities in secondary stock that can be repositioned to capture rising green demand within the European commercial real estate market.

Digital twins, Internet-of-Things sensors and data analytics underpin asset-performance management across large portfolios, allowing owners to benchmark energy intensity and optimise capital expenditure. Blackstone Property Partners Europe’s green-financing platform illustrates the shift toward structured capital tied to emissions targets, while smaller proptech entrants pioneer space-as-a-service models that bundle workplace analytics, community curation and flexible lease terms. Market incumbents respond by forming strategic partnerships with software vendors and sustainability consultants, reinforcing the service-oriented evolution of the European commercial real estate market. [3]Blackstone Property Partners Europe, “Green Financing Framework (2025 Update),” Blackstone, bppeh.blackstone.com

M&A strategies increasingly focus on specialist operators in logistics, residential, life-sciences and data centres, reflecting investor appetite for secular-growth verticals. Partners Group’s acquisition of Empira Group and Hayfin’s loan-portfolio purchase highlight moves to build thematic expertise and scale. Overall, competitive dynamics hinge on sustainability performance, access to alternative capital platforms and ability to blend real-estate fundamentals with technology, all of which shape long-term positioning in the European commercial real estate market.

Europe Commercial Real Estate Industry Leaders

Covivio

Blackstone Inc.

Hines

Strabag Group

Servotel

- *Disclaimer: Major Players sorted in no particular order

Europe Commercial Real Estate Market Companies Covered in this Report

- Unibail-Rodamco-Westfield

- Covivio

- SEGRO Plc

- Landsec

- Vonovia SE

- British Land Company

- Klepierre SA

- Gecina SA

- Prologis Europe

- Goodman European Partnership

- Logicor Europe

- Blackstone Inc. (European Real Estate)

- Brookfield Asset Management (European Real Estate)

- Hines Europe

- Tishman Speyer Europe

- Strabag Real Estate

- HB Reavis Group

- CA Immo

- AG Real Estate

- Futureal Group

- Merlin Properties Socimi

- Deka Immobilien

Recent Industry Developments in Europe Commercial Real Estate Market

- April 2025: Partners Group acquired Empira Group, adding a EUR 14 billion residential portfolio with strong sustainability priorities.

- February 2025: PGIM Real Estate secured three single-family-home portfolios across south and south-west England, bringing its UK Affordable Housing commitment above EUR 310 million

- January 2025: Spain proposed a 100% property-purchase tax for non-EU buyers, targeting speculative acquisitions totalling 27,000 units in 2023

- December 2024: Coldwell Banker Commercial entered Poland by integrating Nuvalu Poland into its network.

Europe Commercial Real Estate Market Report Scope and Research Methodology

Market Definition and Coverage

Our study counts every income-yielding office, retail, logistics, hospitality, and mixed-use asset that changed hands, entered service, or remained under lease across the 27-member EU, the UK, Norway, and Switzerland during 2019-2030. Land valuations and owner-occupied premises are left out to keep the frame purely commercial.

Scope exclusion: student housing, senior-living, and multifamily rental blocks are excluded because they obey different funding and regulatory logics.

Segments Covered in This Report

- By Property Type

- Offices

- Retail

- Logistics

- Others (industrial real estate, hospitality real estate, etc.)

- By Business Model

- Sales

- Rental

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Country

- United Kingdom

- Germany

- France

- Netherlands

- Spain

- Italy

- Sweden

- Poland

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed developers, fund managers, valuers, and municipal planning officials across the DACH region, the Nordics, Iberia, and CEE. Their inputs helped us tighten average selling price bands, cross-check vacancy spreads, and stress-test growth drivers such as green-building premiums and logistics take-up.

Desk Research

Mordor analysts first mapped stock and turnover using open datasets such as Eurostat building permits, ECB transaction volumes, national land registries, and listed-REIT disclosures, supplemented by trade bodies like EPRA and RICS. Macro indicators (GDP, vacancy, prime yield curves) were taken from the OECD, the European Commission, and UN-DESA urbanization files, while deal-level sanity checks drew on D&B Hoovers and Dow Jones Factiva feeds for company filings and news. For supply pipeline sizing, construction-start statistics from national statistics offices and IMTMA machinery shipments informed completion lags. The sources cited illustrate the breadth of coverage; many additional public records were tapped during validation.

Market-Sizing & Forecasting

A top-down build anchored in ECB transaction totals and Eurostat floor-space completions establishes the demand pool. Selective bottom-up roll-ups of major listed landlords and sampled asset sales are then used as guardrails. Key variables like prime yield compression, refinancing costs, e-commerce penetration, Grade-A office absorption, and renovation cap-ex for ESG retrofits drive our multivariate-regression forecast. Where bottom-up gaps persist, we interpolate using region-specific price-per-square-meter benchmarks before aligning all figures to constant 2024 US dollars.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer review, and variance checks against MSCI quarterly capital-value indices; any swing beyond ±5% triggers a re-run. The model refreshes annually, with ad-hoc updates when material policy or rate shocks emerge, ensuring buyers always receive the latest view.

How Mordor Intelligence's Europe Commercial Real Estate Market Size Compares to Other Published Estimates

Published estimates diverge because firms juggle different asset universes, price bases, and refresh cadences.

Key gap drivers include whether residential-like segments sneak into totals, if figures depict book value or transaction value, and how quickly rising renovation costs are layered into forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.55 T (2025) | Mordor Intelligence | - |

| USD 3.8 T (2024) | Global Index Provider A | Counts only professionally managed investment stock and folds Middle-East assets into Europe scope |

| ~USD 10 T (2024) | Industry Data Portal B | Uses GDP-share proxies, mixes residential with commercial, limited forward modeling |

| USD 1.42 T (2024) | Regional Consultancy C | Tracks only income-producing transfers, omits development pipeline and land banking |

Taken together, the comparison shows that Mordor's scope choice, dual-approach modeling, and yearly refresh strike a middle path between asset-stock tallies and narrow deal logs, giving decision-makers a dependable, transparent baseline.

Key Questions Answered in the Report

What is the current size of the European commercial real estate market?

The market is valued at USD 1,638.82 billion in 2026 and is forecast to reach USD 2,170.03 billion by 2031

Which property type is growing fastest in Europe?

Logistics facilities lead with a 6.87% CAGR through 2031, spurred by e-commerce and near-shoring demand.

Why are green-certified offices commanding rental premiums?

About 80-85% of leasing now targets ESG-aligned buildings, driving premiums up to 25% due to corporate net-zero mandates and higher occupancy.

Which European country offers the strongest growth outlook?

Poland is projected to post a 6.29% CAGR to 2031, leveraging its logistics hub status and sustained foreign investment.

How are financing conditions influencing investment strategies?

Elevated lending margins and EUR 114 billion in upcoming debt maturities encourage equity-rich investors to pursue value-add acquisitions at attractive prices.

What role does technology play in asset management?

Digital twins, IoT sensors and analytics optimise energy use and maintenance, enhancing returns and supporting regulatory compliance across European commercial real estate portfolios.

Page last updated on: