Central And Eastern Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

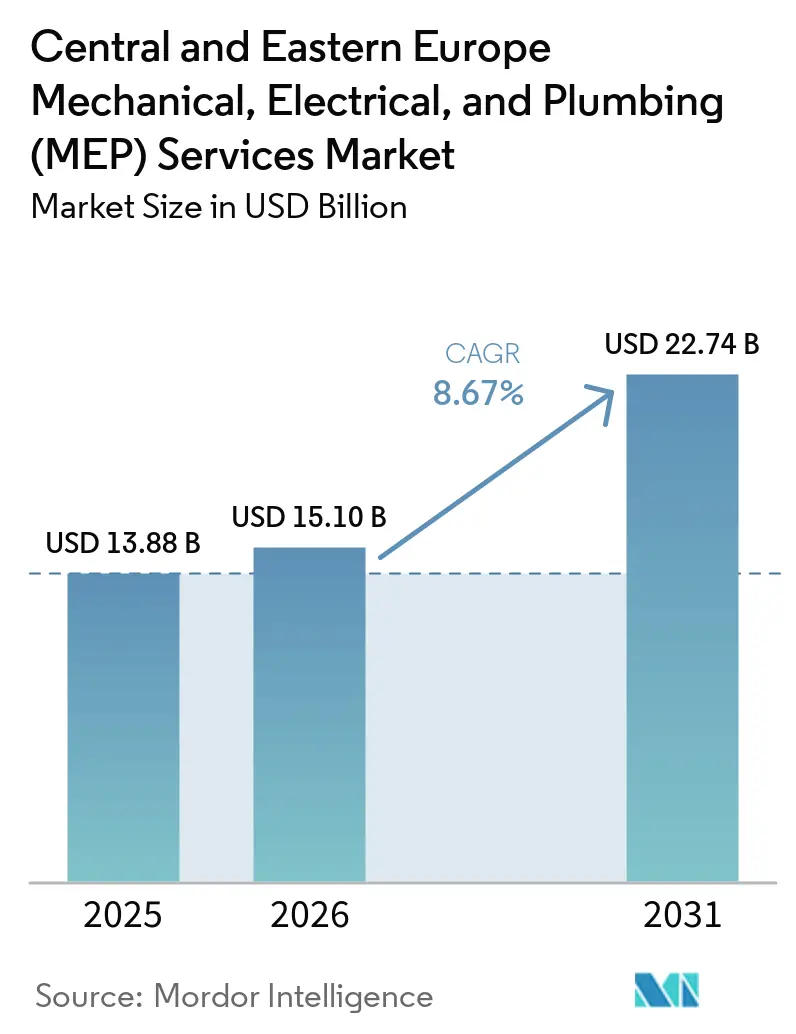

| Base Year Market Size (2025) | USD 13.88 Billion |

| Market Size (2026) | USD 15.10 Billion |

| Market Size (2031) | USD 22.74 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

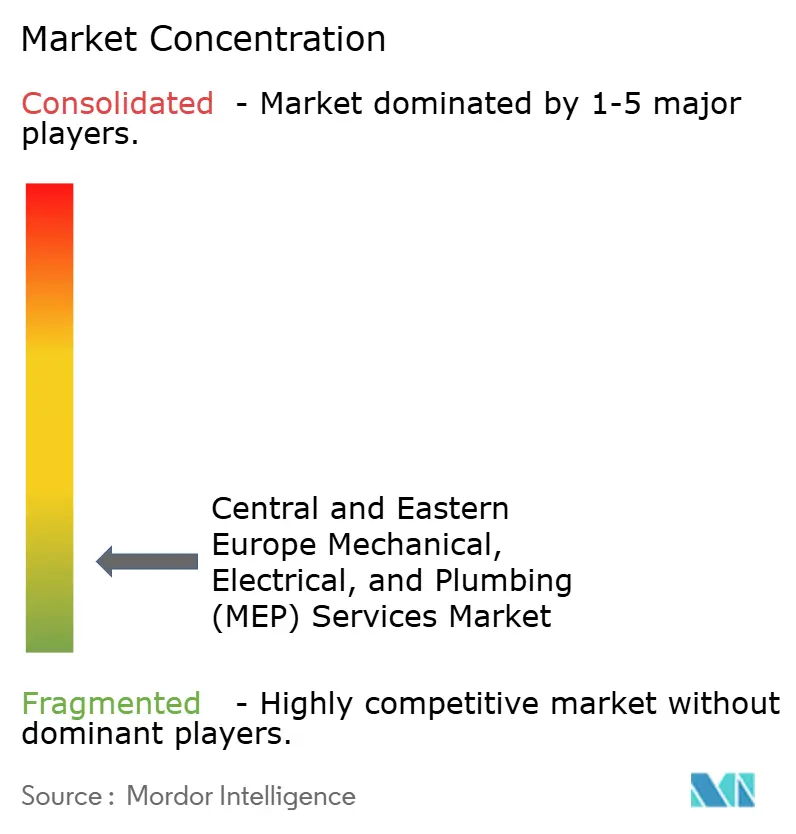

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central And Eastern Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The Central And Eastern Europe Mechanical, Electrical, And Plumbing Services Market size was valued at USD 13.88 billion in 2025 and is estimated to grow from USD 15.10 billion in 2026 to reach USD 22.74 billion by 2031, at a CAGR of 8.67% during the forecast period (2026-2031). This growth reflects 3 shifts moving at the same time: the decarbonization of weak building stock, a broader industrial build-out linked to nearshoring and EU capital, and a larger pipeline in data centers and grid modernization than the region has seen since accession-led expansion. Public capital is helping hold up demand, and the European Investment Bank Group’s record EUR 8 billion (USD 8.8 billion) in Poland in 2025 showed that infrastructure funding is moving into asset classes that generate high MEP subcontracting volumes. The revised Energy Performance of Buildings Directive is also turning compliance into a recurring source of work for HVAC, electrical, solar integration, and building controls across the Central and Eastern Europe MEP services market. At the same time, labor shortages and tighter private financing in parts of the region are pushing growth toward public programs, regulated upgrades, and mission-critical assets where spending is harder to defer. The competitive field is therefore becoming more uneven, with multi-technical groups trying to build density through broader delivery scope, while responsive local specialists keep an edge on smaller regional projects in the Central and Eastern Europe MEP services market

Key Report Takeaways

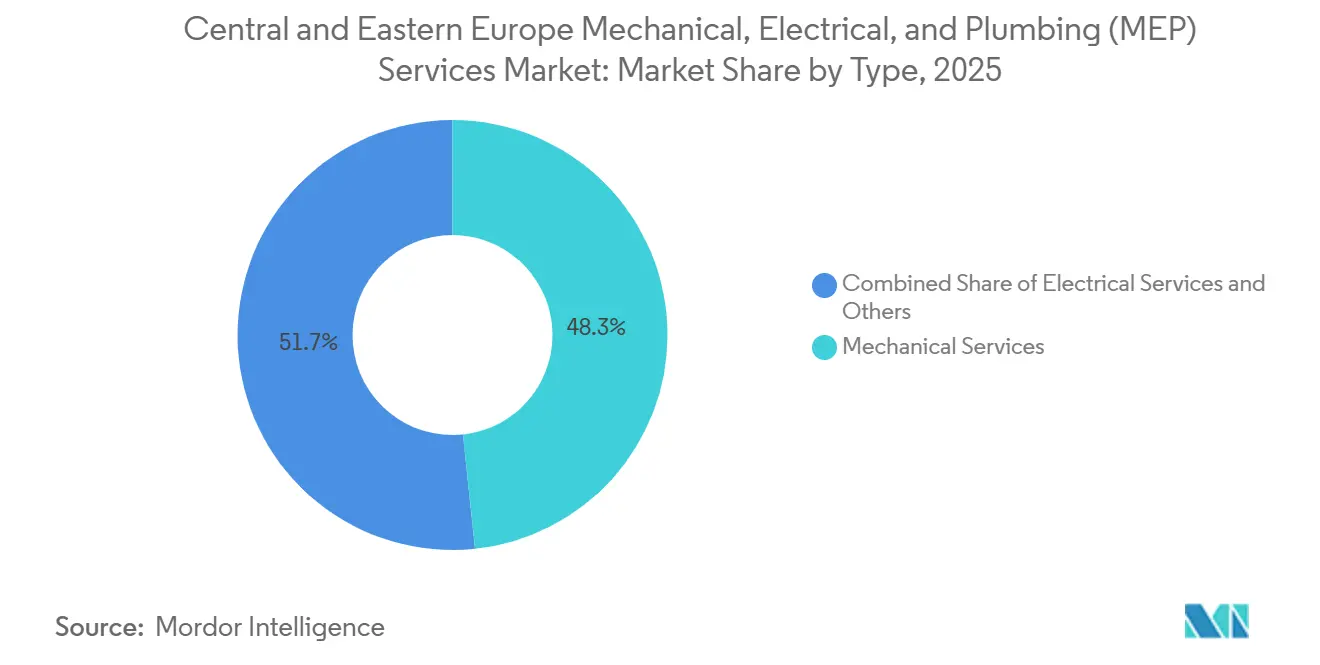

- By type, mechanical services led with 48.3% of revenue in 2025, while integrated MEP services is forecast to expand at 11.1% CAGR through 2031.

- By service type, design & engineering held 36.3% share in 2025, while other services is forecast to grow at 10.1% CAGR through 2031 in the Central and Eastern Europe MEP Services market size.

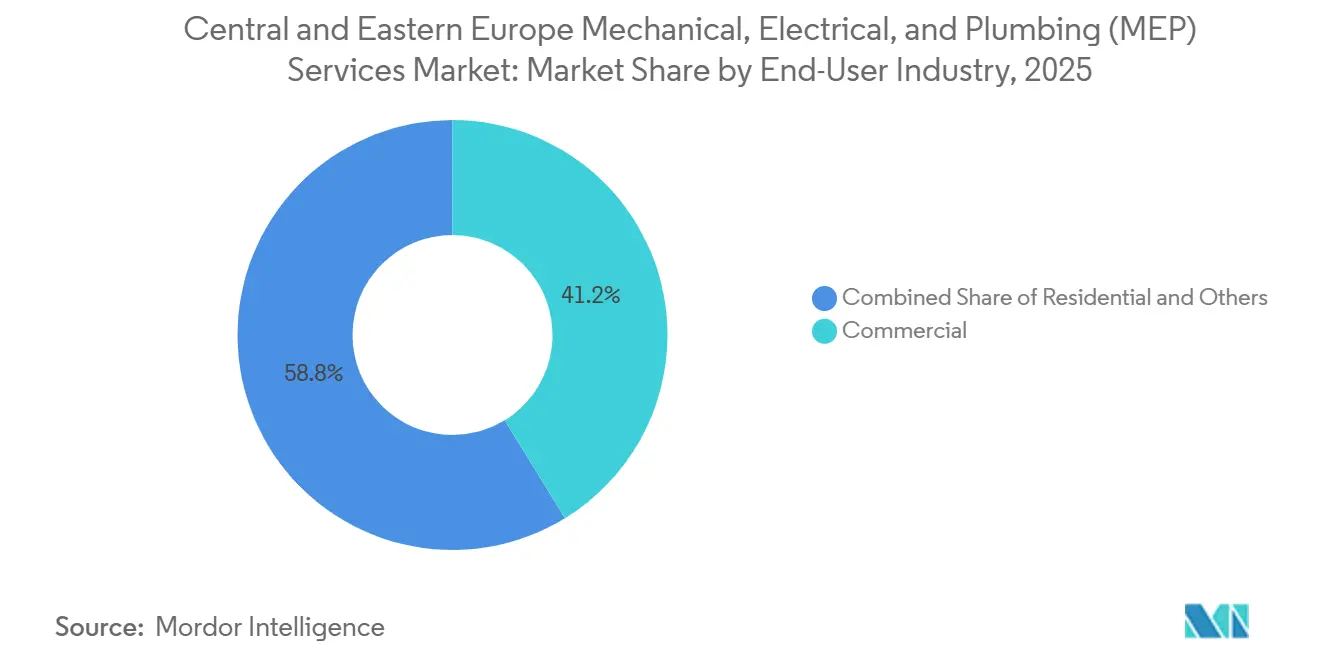

- By end-user industry, commercial accounted for 41.2% of the Central and Eastern Europe MEP services market share in 2025, while infrastructure is projected to grow at a 11.6% CAGR through 2031.

- By geography, Poland held 55.1% of the Central and Eastern Europe MEP services market share in 2025, while the Slovak Republic is forecast to expand at 10.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Central And Eastern Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep-Renovation Demand from EPBD and Fit-For-55 | +2.1% | EU-wide, strongest in Poland, Romania, Hungary | Long term (≥ 4 years) |

| EU-Funded Transport and Utility Modernization | +1.8% | Poland, Romania, Czech Republic, Slovakia, TEN-T corridor states | Medium term (2-4 years) |

| Data-Center and Digital Infrastructure Expansion | +1.5% | Poland, Croatia, Romania | Medium term (2-4 years) |

| Nearshoring-Led Industrial and Logistics Build-Out | +1.3% | Poland, Czech Republic, Slovakia, Hungary | Short term (≤ 2 years) to Medium term (2-4 years) |

| District-Heating Decarbonization and Heat-Pump Retrofits | +1.0% | Poland, Romania, Czech Republic, Hungary, Lithuania | Long term (≥ 4 years) |

| BIM and E-Procurement Mandates in Public Projects | +0.5% | Czech Republic, Romania, Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deep-Renovation Demand from EPBD and Fit-for-55 Creates Recurring MEP Pipeline

The revised Energy Performance of Buildings Directive requires a 16% reduction in average residential primary energy use by 2030 and a 20% to 22% reduction by 2035, with at least 55% of that cut coming from the lowest-performing buildings[1]European Commission, “Directive (EU) 2024/1275 on the Energy Performance of Buildings,” European Commission, commission.europa.eu. In Central and Eastern Europe, 75% of buildings were built before 2000 and the annual renovation rate had stayed near 1%, which means compliance needs a structural increase in retrofit throughput rather than a small improvement[2]Building Performance Institute Europe, “Factsheets on Europe’s Building Stock and Renovation Rate,” BPIE, bpie.eu. For the Central and Eastern Europe MEP services market, that translates into recurring work in HVAC replacement, electrical upgrades, building management systems, and heat-pump integration. The solar requirement under EPBD Article 10 extends the electrical scope, as new public buildings above 250 m² must install solar-energy systems in 2026. That creates additional demand for PV integration, inverters, grid-tie interfaces, and control-system connectivity, on top of the standard project packages. The European Commission’s March 2026 guidance on one-stop shops also supports a more organized referral path for renovation demand into the Central and Eastern Europe MEP services market.

EU-Funded Transport and Utility Modernization Drives Sustained MEP Investment

The Connecting Europe Facility allocated EUR 2.8 billion (USD 3.1 billion) in July 2025 across 94 transport projects, and 77% of that envelope went to rail electrification, ERTMS signaling, and port shore-power upgrades. In the Central and Eastern Europe MEP services market, funding matters because transport modernization involves substantial systems content in substations, low-voltage distribution, fire and life safety, tunnel ventilation, and control layers. These packages pull MEP work into long-duration public contracts instead of one-time building installations. The result is a steadier project flow for electrical and mechanical contractors that can work across transport and utility assets. It also increases the value of firms that can coordinate commissioning, safety compliance, and operations handover under a single scope. As more corridor projects move into delivery, the Central and Eastern Europe MEP services market should continue to draw demand from regulated spending that is less sensitive to private financing cycles.

Data-Center and Digital Infrastructure Expansion Transforms Electrical Services Demand

Data-center and digital infrastructure expansion is changing the demand mix across the region and pushing electrical engineering deeper into project leadership. The Central and Eastern Europe MEP services market is seeing a wider scope that combines high-voltage engineering, BESS integration, cooling plants, and resilient control systems into a single delivery package. New facilities also require closer coordination between mechanical cooling, UPS, BMS, and fire suppression than traditional multi-subcontractor models can easily provide. This pushes clients toward single-responsibility procurement and raises barriers for smaller single-discipline firms. A further layer is now appearing in district heating design, where Bucharest’s decarbonization planning modeled 1.2 MWth of recoverable waste heat from server halls into low-temperature 4th-generation heating networks. As digital infrastructure deepens, the Central and Eastern Europe MEP services market should continue shifting toward electrical intensity, commissioning discipline, and lifecycle service capability.

Nearshoring-Led Industrial and Logistics Build-Out Generates High-Value MEP Contracts

Nearshoring is pulling new manufacturing and logistics capacity into Poland first, and then into Czech Republic, Slovakia, and Hungary through supply-chain spillover. For the Central and Eastern Europe MEP services market, these projects carry more technical content than standard office or retail work. Advanced logistics facilities require HVAC, fire protection, LED warehouse lighting with smart controls, and EV charging infrastructure for fleet operations. Higher-spec manufacturing adds process cooling, clean-room HVAC, industrial electrical systems, and automation links that materially raise value per square meter. Client demand is therefore shifting toward contractors that can manage several technical systems together and still deliver faster commissioning. This keeps contract values high in the Central and Eastern Europe MEP services market, even when built-area growth is not uniform across countries.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor Shortages and Wage Inflation | -1.2% | Region-wide, strongest in Czech Republic, Hungary, Romania | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Interest Rates and Fiscal Tightening | -0.8% | Romania, Hungary, Poland | Medium term (2-4 years) |

| Permitting Delays and Cross-Border Compliance Complexity | -0.6% | Romania, Poland, region-wide cross-border projects | Medium term (2-4 years) |

| War-Risk, Insurance, and Grid-Connection Bottlenecks | -0.4% | Eastern border interfaces including Poland, Romania, Slovakia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages and Wage Inflation Constrain Project Throughput

Skilled-labor shortages are limiting how much work the Central and Eastern Europe MEP services market can execute at one time. The pressure is strongest in electricians, HVAC fitters, pipefitters, and certified commissioning staff. In Poland, the F-gas-certified HVAC technician pool of 60,000 remains below the level needed for the installation wave expected in late 2026 and early 2027. Wage inflation is also lifting bid prices for electrical and HVAC packages across the region. Smaller contractors feel this pressure first because they cannot offset labor costs through scale, wider purchasing power, or multi-country staffing. The result is slower project throughput, higher pricing, and a greater premium on firms that already control certified in-house teams in the Central and Eastern Europe MEP services market.

High Interest Rates and Fiscal Tightening Squeeze Private-Sector Investment

High interest rates and fiscal tightening are narrowing the private project pipeline in parts of the region, especially in Romania and Hungary. In the Central and Eastern Europe MEP services market, this appears first in discretionary office projects, private commercial projects, and some speculative industrial projects. Public programs backed by EU funding remain steadier, which is why growth is clustering around regulated and non-discretionary work. Financing standards are also becoming stricter for projects that cannot demonstrate strong energy performance credentials. That change favors MEP contractors that can document compliance, commissioning quality, and alignment with green-building requirements. Even with these pressures, the Central and Eastern Europe MEP services market retains momentum because public infrastructure, compliance retrofits, and mission-critical assets continue to move forward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Services Lead While Integrated Delivery Grows Fastest

Mechanical services accounted for 48.3% of the Central and Eastern Europe MEP services market share in 2025, making it the largest segment in the region. This lead reflects the heavy value of HVAC retrofits, cooling systems, ventilation, and plant-room upgrades across old building stock and new industrial projects. Electrical and plumbing services remained core to project execution, but Mechanical Services accounted for the largest contract value because thermal systems and cooling infrastructure are central to both renovation and new-build demand. The regional project mix also favored mechanical scope in factories, logistics facilities, hospitals, and data centers, where cooling performance and environmental control are essential. This kept mechanical work at the center of the Central and Eastern Europe MEP services market, even as procurement models started to broaden.

Integrated MEP services is projected to expand at a 11.1% CAGR through 2031, making it the fastest-growing segment in the Central and Eastern Europe MEP services market. The shift reflects rising demand for single-responsibility delivery in data centers, hospitals, and advanced manufacturing facilities where multiple technical systems must work together from the start. Clients are increasingly preferring bundled mechanical, electrical, plumbing, and controls coordination because traditional fragmented subcontracting creates greater interface risk on complex projects. This trend should continue to favor firms that can combine engineering, installation, testing, and commissioning under one delivery structure. Over time, integrated capability is likely to take share from single-discipline models at the top end of the Central and Eastern Europe MEP services market.

By Service Type: Design and Engineering Holds the Largest Share While Other Services Accelerate

Design & engineering accounted for 36.3% of the market in 2025, making it the largest service type across the Central and Eastern Europe MEP services market. This position reflects the growing complexity of system layouts, energy-efficiency upgrades, and compliance work linked to transport modernization, deep renovation, and industrial build-outs. More projects now require early-stage coordination among HVAC, electrical distribution, plumbing, controls, and fire systems, underscoring the value of front-end technical planning. Design & engineering also benefits from stricter energy-performance standards because owners need a clearer project definition before committing to capital deployment. Installation, testing, commissioning, and maintenance & repair remained important, but front-end engineering captured the largest share in 2025 because system coordination is becoming more demanding.

Other services is projected to grow at 10.1% CAGR through 2031, making it the fastest-growing service type in the Central and Eastern Europe MEP services market. This category includes maintenance, retrofit, and performance-monitoring work, and its growth points to a larger installed base of heat pumps, BESS, and intelligent HVAC systems across the region. Owners are increasingly looking beyond first-time installation and are spending more on uptime, optimization, monitoring, and periodic upgrades. That creates a more durable revenue base for contractors with service platforms and field support capability. As the installed equipment base expands, Other Services should keep gaining weight within the Central and Eastern Europe MEP services market.

By End-User Industry: Commercial Remains the Largest Base While Infrastructure Posts the Fastest Growth

Commercial accounted for 41.2% share in 2025, making it the largest end-user industry in the Central and Eastern Europe MEP services market. This reflects the region’s broad stock of office, retail, mixed-use, hospitality, and other non-residential assets that require HVAC, electrical, plumbing, controls, and retrofit work. The commercial base also faces recurring modernization demand as energy performance and building-system efficiency become more important to asset owners and occupiers. Residential remained relevant through renovation-led activity, but Commercial held the lead because building complexity and contract value are usually higher in non-residential projects. This made Commercial the main revenue anchor for the Central and Eastern Europe MEP services market in 2025.

Infrastructure is forecast to expand at 11.6% CAGR through 2031, making it the fastest-growing end-user industry in the Central and Eastern Europe MEP services market size. Rail electrification, utility modernization, grid-connection work, and public capital deployment are driving this growth across several CEE countries. These projects require heavy electrical and mechanical scope, including substations, low-voltage systems, ventilation, safety systems, and controls integration. Infrastructure demand is also more resilient than discretionary private investment because it is often tied to public funding and regulatory priorities. This is why infrastructure is expected to outpace Residential and Commercial through the forecast period in the Central and Eastern Europe MEP services market.

Geography Analysis

Poland accounted for 55.1% of regional revenue in 2025, making it the clear center of demand in the Central and Eastern Europe MEP services market. Its lead reflects faster EU fund absorption, stronger nearshoring inflows, and a deeper pipeline in transport, utilities, industrial construction, and digital infrastructure. The country also benefits from scale, since a larger installed base supports both project work and follow-on service revenue. Record EIB investment in Poland in 2025 reinforced this position by channeling capital into infrastructure categories with significant electrical and mechanical scope[3]European Investment Bank Group, “EIB Group Activity in Poland in 2025,” European Investment Bank, eib.org. For the Central and Eastern Europe MEP services market, Poland remains the first location where regional strategies, supplier relationships, and workforce deployment are tested at scale.

The next tier is shaped by Czech Republic, Slovakia, Hungary, and Romania, each with a different balance of industrial, infrastructure, and compliance-driven demand. Czech Republic and Slovakia benefit from supply-chain links to German manufacturing, which supports technically demanding factory and logistics work. Hungary remains relevant for industrial spillover, but tighter financing conditions can keep private pipelines more selective than in Poland. Romania offers meaningful public and utility opportunity, yet delivery conditions are less even because administrative and financing pressures can slow private execution. This tiered pattern means the Central and Eastern Europe MEP services market does not move as one block, and contractor strategies need country-by-country capacity planning.

Emerging pockets such as Croatia are gaining visibility through digital infrastructure, while eastern interface areas face added friction from war-related risk, insurance pressure, and grid-connection bottlenecks. Across the wider region, the strongest demand tends to appear where EU-backed infrastructure, renovation policy, and industrial relocation overlap in the same geography. That is why growth is clustering rather than spreading evenly, with the biggest opportunities centered on countries that can move capital into projects quickly and manage approvals with fewer delays. In that setting, the Central and Eastern Europe MEP services market rewards contractors that can allocate labor across borders, read local procurement rules, and stay close to public-program funding cycles.

Competitive Landscape

The competitive landscape remains fragmented, but it is becoming more uneven as larger multi-technical groups target the most complex and highest-value scopes. In the Central and Eastern Europe MEP services market, that divide is visible between pan-European platforms building density and domestic contractors that still compete hard on price and response time. Public infrastructure, data centers, hospitals, and advanced manufacturing are steadily raising the minimum capability needed to lead full-scope projects. As a result, competition is no longer defined only by labor cost, and it increasingly depends on integration, certification depth, commissioning control, and service reach.

SPIE’s work on Daikin Manufacturing Poland’s 110,000 m² facility in Ksawerów showed how leading contractors are using technically dense industrial projects to deepen their regional credentials. The package included a 3.6 MW heat-pump system, medium-pressure helium and refrigerant pipework, and full BMS automation, which points to the level of coordination clients now expect. WBS Power’s secured 3.2 GW grid connection for the Baltic Data Center Campus in Lublewo showed the scale of electrical capability being pulled into digital infrastructure programs. Cisco’s planned 200 million PLN investment in a Krakow data center, equal to USD 56.5 million, further shows that enterprise and managed-service demand is widening the addressable pool for contractors with resilient power and cooling capability. These moves reinforce why the top end of the Central and Eastern Europe MEP services market is shifting toward firms with stronger engineering leadership and balance-sheet capacity.

Even so, domestic specialists still hold a real advantage on sub-regional work where local permitting knowledge, field flexibility, and faster mobilization matter more than corporate scale. Labor shortages are amplifying that divide, because certified teams in HVAC, electrical installation, and commissioning are becoming strategic assets rather than standard inputs. Firms that can pair those teams with maintenance platforms are better placed to capture both project revenue and follow-on service contracts. The Central and Eastern Europe MEP services market should therefore keep seeing selective consolidation at the high end while remaining broad and contested across local project categories. This balance supports high competitive intensity today, but it also leaves room for capable regional players to defend share where speed, cost discipline, and customer proximity still drive awards.

Central And Eastern Europe Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

STRABAG SE

PORR Group

Skanska

Warbud

Budimex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The EPBD’s transposition deadline of May 29, 2026 triggers mandatory minimum energy-performance standards for non-residential buildings, concentrating MEP scope into HVAC, electrical, and building management system upgrades.

- March 2026: The European Commission’s guidance on one-stop shops, issued as part of the EPBD implementation package, provides the technical assistance architecture through which renovation referrals will be channeled to MEP contractors over the medium term.

- February 2026: The European Investment Bank Group’s record USD 8.8 billion investment in Poland in 2025, representing 2.5% of GDP, illustrates the scale of public capital now channeled into infrastructure categories that generate disproportionate MEP subcontracting volume.

Central And Eastern Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The Central and Eastern Europe MEP Services Market is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation & Commissioning, Maintenance & Repair, Other Services), and End-User Industry (Residential, Commercial, Infrastructure), and Geography (Poland, Czech Republic, Hungary, Romania, and more). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance & Repair |

| Other Services |

| Residential |

| Commercial |

| Infrastructure |

| Poland |

| Czech Republic |

| Hungary |

| Romania |

| Slovenia |

| Rest of CEE |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance & Repair | |

| Other Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Poland |

| Czech Republic | |

| Hungary | |

| Romania | |

| Slovenia | |

| Rest of CEE |

Key Questions Answered in the Report

What is the current size of Central and Eastern Europe MEP services?

The Central and Eastern Europe MEP services market size stood at USD 13.88 billion in 2025 and is projected to value at USD 15.01 billion in 2026, with USD 22.74 billion expected by 2031 at an 8.7% CAGR

Which service line leads regional revenue?

Mechanical services led with 48.3% of 2025 revenue because HVAC retrofits, cooling plants, ventilation, and hydronic upgrades remain the heaviest-value packages in building modernization

Which end-user group is expanding the fastest?

Infrastructure is the fastest-growing end-user segment, with 11.6% CAGR through 2031, supported by rail electrification, grid reinforcement, and utility modernization

How is the EPBD changing contractor demand?

EPBD compliance is increasing recurring work in HVAC, electrical upgrades, solar integration, and building controls, especially across older building stock that needs deep renovation

Page last updated on: